ADX Energy Limited (ADX) 20100617.pdf · ADX Energy Limited (ADX) Company Snapshot RN Wilson HTM...

12

ADX Energy Limited (ADX) Company Snapshot RN Wilson HTM Equities Research – ADX Energy Limited 1 Issued by Wilson HTM Ltd ABN 68 010 529 665 - Australian Financial Services Licence No 238375 and should be read in conjunction with the disclosures/disclaimer in this report 17 June 2010 $0.18 NR John Young +61 3 9640 3846 Overview ADX is a Perth-based ASX listed company engaged in hydrocarbons and minerals exploration. Recent activities have been focused on conventional oil and gas exploration in Tunisia and Italy (offshore and onshore), Romania and Australia. Three “ready to drill” prospects (Lambouka, Dougga and Sidi Daher) have been identified in the Tunisia and Italy licenses with exploration wells Lambouka-1 (deepwater) to spud in Jun 2010 and Sidi Daher (onshore) in late CY2010. The company is in the process of divesting its Australian assets (PEL 182 & gold/ base metal assets) to complete the progression from the minerals to energy sector. [email protected] Charmaine Cornford +61 3 9640 3897 [email protected] Price Performance $0.00 $0.05 $0.10 $0.15 $0.20 $0.25 Jun 08 Dec 08 Jun 09 Dec 09 Jun 10 Security/Capital Details ASX Code ADX Market Cap (undil) $56.91 M Issued Shares (undil) 316.17 M Avg Mth T’over 42.52 M 12 Mth High – Low $0.212 –0.081 Key Data/Ratios –31 Mar 2010 Cash $ 1.4 M Debt $ 0 M Key Points This report is a “Company Snapshot” based on meetings with Ian Tchacos (Chairman) and Wolfgang Zimmer (MD) on 24 May 2010. It is provided for general information. We have not valued the company and do not provide an investment recommendation. Investment thesis: Company secures funding for drilling via farmouts to mitigate financial risk while retaining significant equity interests for leverage to success. Maintain operatorship during exploration and appraisal phase of all projects to ensure appropriate control. Significant potential in mapped prospects which are surrounded by hydrocarbon discoveries. Potentially benefit from planned demerger/ divestment of gold and base metal assets with planned IPO in 2HCY2010. Business strategy: Acquire highly prospective acreage in proven basins with good access to infrastructure, with politically stable governments and attractive fiscal terms. Focus on areas where company has past experience and established relationships. Secure funding via farm-outs while retaining high equity interests. Value proposition: Deepwater exploration well Lambouka-1 (offshore Sicily channel) to spud imminently in Jun 2010 targeting P50 resources of 270 mmboe in 3 targets (Birsa oil, Ain Grab oil and Abiod gas condensate) and is expected to take 30 days and ~US$20m to drill and log. Structure is well defined with good seals and chance of success is considered high. Well is fully carried. Dougga field (15 km away) was a gas condensate discovery by Shell in the 1980s. With advanced technologies and current prices, project NPV is ~US$1billion. Appraisal well is planned for CY2011. Multi- target exploration well Sidi Daher (onshore, Chorbane license) is expected to spud in 2HCY2010 which has P50 resources of 175 bcf recoverable gas and 54 mmbbls oil. Pros: At least 3 projects in proven petroleum area that are “ready to drill”. Potential of unrisked P50 1 billion bbls resource. Strong encouragement from Tunisian government to develop domestic gas source. Good fiscal terms in Tunisia (PSC) and in offshore Italy (royalty). Existing infrastructure in proximity of prospects allows discovery to be tied into existing facilities with minimal costs and delay. Gas prices ~ 2 - 3 times of those in Australia. Cons: Small scale; tight cash; small to mid-cap Australian energy companies operating overseas have not been “market favourites” which could limit share price appreciation. Risks: Exploration outcomes; funding for development; commodity prices. Next steps: Drilling program to commence in Tunisia and Italy; demerger of mining assets in Australian; Resources/ reserves upgrades. Price catalysts: Significant discovery; certification of reserves.

Transcript of ADX Energy Limited (ADX) 20100617.pdf · ADX Energy Limited (ADX) Company Snapshot RN Wilson HTM...

ADX Energy Limited (ADX) Company Snapshot

RN

Wilson HTM Equities Research – ADX Energy Limited 1 Issued by Wilson HTM Ltd ABN 68 010 529 665 - Australian Financial Services Licence No 238375 and should be read in conjunction with the disclosures/disclaimer in this report

17 June 2010

$0.18

NR

John Young +61 3 9640 3846

Overview ADX is a Perth-based ASX listed company engaged in hydrocarbons and minerals exploration. Recent activities have been focused on conventional oil and gas exploration in Tunisia and Italy (offshore and onshore), Romania and Australia. Three “ready to drill” prospects (Lambouka, Dougga and Sidi Daher) have been identified in the Tunisia and Italy licenses with exploration wells Lambouka-1 (deepwater) to spud in Jun 2010 and Sidi Daher (onshore) in late CY2010. The company is in the process of divesting its Australian assets (PEL 182 & gold/ base metal assets) to complete the progression from the minerals to energy sector.

Charmaine Cornford +61 3 9640 3897 [email protected]

Price Performance

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

Jun 08 Dec 08 Jun 09 Dec 09 Jun 10

Security/Capital Details ASX Code ADX Market Cap (undil) $56.91 M Issued Shares (undil) 316.17 M Avg Mth T’over 42.52 M 12 Mth High – Low $0.212 –0.081

Key Data/Ratios –31 Mar 2010

Cash $ 1.4 M Debt $ 0 M

Key Points This report is a “Company Snapshot” based on meetings with Ian Tchacos

(Chairman) and Wolfgang Zimmer (MD) on 24 May 2010. It is provided for general information. We have not valued the company and do not provide an investment recommendation.

Investment thesis: Company secures funding for drilling via farmouts to mitigate financial risk while retaining significant equity interests for leverage to success. Maintain operatorship during exploration and appraisal phase of all projects to ensure appropriate control. Significant potential in mapped prospects which are surrounded by hydrocarbon discoveries. Potentially benefit from planned demerger/ divestment of gold and base metal assets with planned IPO in 2HCY2010.

Business strategy: Acquire highly prospective acreage in proven basins with good access to infrastructure, with politically stable governments and attractive fiscal terms. Focus on areas where company has past experience and established relationships. Secure funding via farm-outs while retaining high equity interests.

Value proposition: Deepwater exploration well Lambouka-1 (offshore Sicily channel) to spud imminently in Jun 2010 targeting P50 resources of 270 mmboe in 3 targets (Birsa oil, Ain Grab oil and Abiod gas condensate) and is expected to take 30 days and ~US$20m to drill and log. Structure is well defined with good seals and chance of success is considered high. Well is fully carried. Dougga field (15 km away) was a gas condensate discovery by Shell in the 1980s. With advanced technologies and current prices, project NPV is ~US$1billion. Appraisal well is planned for CY2011. Multi-target exploration well Sidi Daher (onshore, Chorbane license) is expected to spud in 2HCY2010 which has P50 resources of 175 bcf recoverable gas and 54 mmbbls oil.

Pros: At least 3 projects in proven petroleum area that are “ready to drill”. Potential of unrisked P50 1 billion bbls resource. Strong encouragement from Tunisian government to develop domestic gas source. Good fiscal terms in Tunisia (PSC) and in offshore Italy (royalty). Existing infrastructure in proximity of prospects allows discovery to be tied into existing facilities with minimal costs and delay. Gas prices ~ 2 - 3 times of those in Australia.

Cons: Small scale; tight cash; small to mid-cap Australian energy companies operating overseas have not been “market favourites” which could limit share price appreciation.

Risks: Exploration outcomes; funding for development; commodity prices.

Next steps: Drilling program to commence in Tunisia and Italy; demerger of mining assets in Australian; Resources/ reserves upgrades.

Price catalysts: Significant discovery; certification of reserves.

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 2

ADX Energy Limited ADX

Overview ADX is a Perth-based ASX listed company engaged in hydrocarbons and minerals exploration. Recent activities have been focused on conventional oil and gas exploration in Tunisia and Italy (offshore and onshore) and Romania. The company is in the process of divesting its interests in PEL 182 (Cooper Basin, SA) and spinning off its gold and base metal assets and to complete the progression from the minerals sector to the energy sector. Its overseas office is located in Vienna, Austria.

Board and Management

Ian Tchacos (Chairman), Wolfgang Zimmer (MD), Andrew Childs (NED), Paul Fink (Technical Director), Peter Ironside (Coy Sec).

Ian Tchacos replaced Gary Roper, who resigned on 2 Mar 2010, as non executive Chairman.

Capital Structure

Listed on ASX since 29 Jan 1987. Shares on issue: 316.17m (337.4m post rights issue). Options on issue: 58.05m (24.10m quoted, 33.95m unquoted).

Market cap: A$56.91m (based on share price of A$0.18, 16 Jun 2010).

As at 1 Sep 2009, top 20 shareholders accounted for 32.58% interests (issued shares then was 229.31m). Institutional holders accounted for ~3%. Shares held by ~2,600 shareholders.

Funding/ Financials

Cash ~ A$1.39M and no debt (as at 31 March 2010).

A committed equity facility agreement to secure a A$20k facility was executed on 1 Oct 2009 with Trafalgar Capital Specialised Investment Fund, Luxembourg in which ADX may at any time over the next 30 months issue shares to Trafalgar.

In Aug and Sep 2009, raised A$5.5m at issue price of A$0.10 - 0.105/share.

Non-renounceable rights issue in May 2010 to raise A$7.23m (1 for 6 ratio offering 48.2m shares at A$0.15/share) with 1 free new option for every 2 new shares exercisable at A$0.25 (expiry 31 Mar 2011). Offer closed on 28 May with 21.3m shortfall shares. Issue is fully underwritten.

A$2.5m bond to be released by the Tunisian government on spudding of exploration well Lambouka-1 (expected to be on 18 Jun 2010).

Expected cash outflows for 2QCY2010 estimated A$1.96m.

Estimated cash at end of 2QCY2010 = A$10.26m [1.39 +7.23 +2.5 +1.1 (sale of PEL182) – 1.96].

Other Corporate

Headquarter: West Perth, WA. Technical Office: Vienna, Austria.

Reporting year end: June Functional currency: A$ Presentation currency: A$

Reserves & Resources

Independently certified by Tracs: • Kerkouane and Pantelleria licenses (Lambouka & Dougga): P50 resources of 75 mmboe gas and

condensate & 42 mmbbl liquids (P10 resources of 117 mmboe gas and condensate and 65 mmbbl liquids);

• Dougga field: P50 resources of 177 bcf gas, 28.4 mmbbl condensate and 9.4 mmbbl LPG;

Not certified: • Chorbane license: P50 resources of 175 bcf gas at the Eocene level and 54 mmbbl oil for the

Abiod Formation. Key assets Assets categorised in terms of near term growth opportunities:

• Large size: Tunisia & Italy offshore (Lambouka Prospect); • Mid to large size: Tunisia offshore (Dougga gas and condensate field); • Mid size: Tunisia onshore (Chorbane exploration) and Romania 10th Round opportunities; and • Low leverage position: Australia (PEL 182 Cooper Basin, Vanessa gas/condensate discovery;

and Western Australia gold mining tenements).

On 15 Jun 2010, ADX advised it has executed a sale and purchase agreement with Victoria Petroleum (ASX: VPE) for the sale of its interest in PEL 182 for A$1.1m cash consideration. The agreement is subject to approval by the SA government.

Demerger and spin-off of gold and base metal assets is at an advanced stage of completion with an IPO offering planned for the 2HCY2010. ADX will retain a substantial interest in the new entity.

Other ADX has changed its name from AuDAX Resources Limited to ADX Energy Limited effective 10 Jun 2010. There was no change to its ASX code.

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 3

Tunisia (Kerkouane & Chorbane)

Italy: GR15PU (Pantelleria)

Location of prospects

Source: ASX Release 18 May 2010

Source: Company 30 Jun 2009 Annual Report, ASX Release 24 Sep 2009

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 4

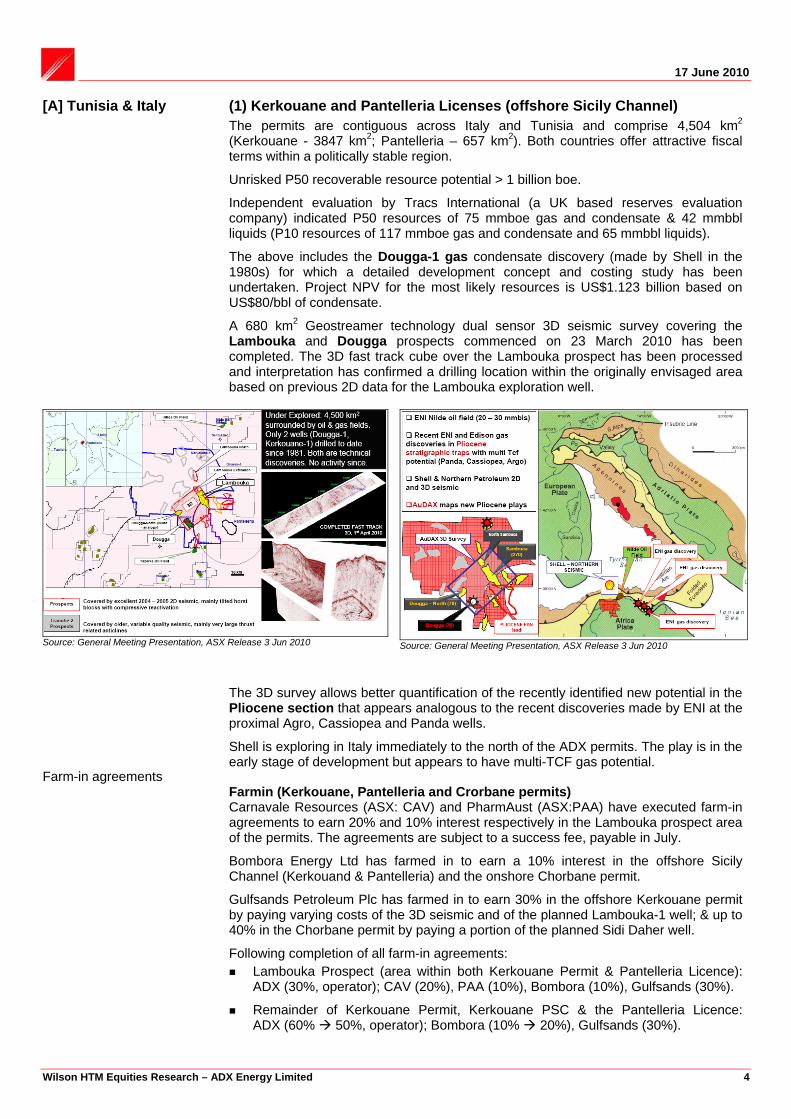

[A] Tunisia & Italy

(1) Kerkouane and Pantelleria Licenses (offshore Sicily Channel) The permits are contiguous across Italy and Tunisia and comprise 4,504 km2 (Kerkouane - 3847 km2; Pantelleria – 657 km2). Both countries offer attractive fiscal terms within a politically stable region.

Unrisked P50 recoverable resource potential > 1 billion boe.

Independent evaluation by Tracs International (a UK based reserves evaluation company) indicated P50 resources of 75 mmboe gas and condensate & 42 mmbbl liquids (P10 resources of 117 mmboe gas and condensate and 65 mmbbl liquids).

The above includes the Dougga-1 gas condensate discovery (made by Shell in the 1980s) for which a detailed development concept and costing study has been undertaken. Project NPV for the most likely resources is US$1.123 billion based on US$80/bbl of condensate.

A 680 km2 Geostreamer technology dual sensor 3D seismic survey covering the Lambouka and Dougga prospects commenced on 23 March 2010 has been completed. The 3D fast track cube over the Lambouka prospect has been processed and interpretation has confirmed a drilling location within the originally envisaged area based on previous 2D data for the Lambouka exploration well.

Source: General Meeting Presentation, ASX Release 3 Jun 2010

Source: General Meeting Presentation, ASX Release 3 Jun 2010

Farm-in agreements

The 3D survey allows better quantification of the recently identified new potential in the Pliocene section that appears analogous to the recent discoveries made by ENI at the proximal Agro, Cassiopea and Panda wells.

Shell is exploring in Italy immediately to the north of the ADX permits. The play is in the early stage of development but appears to have multi-TCF gas potential.

Farmin (Kerkouane, Pantelleria and Crorbane permits) Carnavale Resources (ASX: CAV) and PharmAust (ASX:PAA) have executed farm-in agreements to earn 20% and 10% interest respectively in the Lambouka prospect area of the permits. The agreements are subject to a success fee, payable in July.

Bombora Energy Ltd has farmed in to earn a 10% interest in the offshore Sicily Channel (Kerkouand & Pantelleria) and the onshore Chorbane permit.

Gulfsands Petroleum Plc has farmed in to earn 30% in the offshore Kerkouane permit by paying varying costs of the 3D seismic and of the planned Lambouka-1 well; & up to 40% in the Chorbane permit by paying a portion of the planned Sidi Daher well.

Following completion of all farm-in agreements: Lambouka Prospect (area within both Kerkouane Permit & Pantelleria Licence):

ADX (30%, operator); CAV (20%), PAA (10%), Bombora (10%), Gulfsands (30%).

Remainder of Kerkouane Permit, Kerkouane PSC & the Pantelleria Licence:ADX (60% 50%, operator); Bombora (10% 20%), Gulfsands (30%).

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 5

Lambouke Prospect

Lambouka drilling in CY2010: 3 targets

Lambouka Prospect

ADX (30%, operator) CAV (20%), PAA (10%), Bombora (10%), Gulfsands (30%).

Lambouka Prospect is an area ~150km2 within both Kerkouane Permit & Pantelleria Licence. It is a multi-target prospect with over 60 km2 of structural closure that results in P50 resources of 270 mmboe for two Tertiary targets (Miocene aged Birsa Formation and Ain Grab) and the deeper Upper Cretaceous Abiod Formation.

Source: General Meeting Presentation, ASX Release 3 Jun 2010

While the primary target is a Tertiary age oil reservoir with very high flow rates seen in nearby wells (+20,000 bbl/d), it also has the same Cretaceous target as found in Dougga (15 km away) with the potential of another gas condensate discovery. Together with Dougga, P50 gas resource is ~1 tcf & 70 mmbbl of condensate.

Environmental studies and a detailed well design program have been completed. As well, ADX has completed the selection of a well location on the Tunisian side in order to limit exposure to only 1 commitment well.

The deepwater Lambouka-1 exploration well (Kerkouane permit, offshore Tunisia) preparation is at an advanced stage and has a scheduled spud date of 18 Jun 2010. The well will be fully funded, will be ~60m offshore in ~600m of water and target depth ~3300m. The Atwood Southern Cross semi-submersible rig was contracted in Jan 2010 to drill the well to the value of US$20m. Long lead items have been secured.

Estimated drilling time: First reservoir target (Birsa oil) after 10 days;

Second reservoir target (Ain Grab oil) after 12 days;

Third reservoir target (Abiod gas condensate) after 20 days; and

Logging of well after ~30 days.

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 6

Source: General Meeting Presentation, ASX Release 3 Jun 2010

Dougga Appraisal Project

Dougga Appraisal Project

Shell’s discovery well, Tunirex Dougga-1, was drilled in 1981 (TD 3,992 m. WD 328 m). While gas/condensate was discovered in the Abiod & Allam Formations, the discovery was considered non-commercial and the well was plugged and abandoned.

The Dougga Appraisal Project now finds the discovery commercially viable: 2004 seismic data confirms large structural closure of ~43 km2;

Significant upside (Dougga-1 drilled ~300 m down dip from crest of structure);

No gas/water encountered at Dougga-1;

Test data and pressures indicate a gas column of about 600 m;

High angle/ horizontal wells significantly increase productivity and commerciality;

Dougga hydrocarbons can be developed with proven technology;

Conceptual study (FPSO). Dry raw gas to onshore separation and CO2 removal plant ~40km (BG-Miskar 130km offshore). 4 well development with total off-take rate ~100 mmscf/d. 12kbbl condensate/day plus LPG and power export;

Dougga field independently certified by Tracs to contain:

- P50 resource (177 bcf gas, 28.4mmbbl condensate, 9.4 mmbbl LPG); - P10 resource (308 bcf gas, 49.1mmbbl condensate, 16.3 mmbbl LPG);

Appraisal well Dougga-2 to spud in CY2011 (planned depth ~4,000m).

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 7

Combined Lambouka & Dougga: Large offshore gas condensate hub

Source: General Meeting Presentation, ASX Release 3 Jun 2010

Source: General Meeting Presentation, ASX Release 3 Jun 2010

(2) Chorbane License (onshore PSC and Convention, Tunisia)

ADX (100% 60%, operator) Gulfsands (0 40%).

The Tunisian Chorbane block is on trend with the Jurassic through Tertiary proven petroleum systems and lies immediately west of a number of producing fields and discoveries. Existing infrastructure is in proximity.

8 wells have previously been drilled on the property and have established the presence of reservoirs and hydrocarbons, however, modern seismic suggests that the wells were not optimally located or not drilled to a depth adequate to test all prospective targets.

ADX was awarded permit on 18 Sep 2009 and in October, DNO International ASA (Norwegian) executed a letter of intent to farm into the permit and fully funding the first US$ 5m well cost to earn 50%. Discussions with DNO were terminated in 1QCY2010. ADX is continuing discussions with other interested parties.

The Tunisian Authorities have approved a 1 year extension to the Chorbane permit exploration period. The permit expiry data is 12 Jul 2011.

The extended term allows adequate time to prepare for the drilling of the multi-target Sidi Daher exploration well which has P50 resources of 175 bcf recoverable gas at the Eocene level in addition to the deeper Upper Cretaceous targets; the Abiod Formation, the Douleb and Bireno Members of the Aleg Formation and the Zebbag Formation.

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 8

The P50 Abiod Formation recoverable resources are estimated to be 54 mmbbl of oil. All reservoirs are proven and producing in the area.

A technical evaluation has identified a Direct Hydrocarbon Indicator (DHI) over the Sidi Daher prospect and the prospect has been upgraded to “ready to drill” status. Plan to spud exploration well in 2HCY2010.

Source: General Meeting Presentation, ASX Release 3 Jun 2010

Chorbane is a multi-target prospect with 20-80 km2 of structural closure: Eocene Nummulitic Reservoirs: DHI

Abiod Limestone 140 m thick at REF-1. Potential for southwards strat trap on crest of horst, 50 mmbbl produced from field to the North;

Bireno is 88m at REF-1;

Zebbag likely to be an important reservoir with 95m of development in REF-1;

Serdj Formation; and

Lower Nara Formation is gas-bearing along strike.

[B] Romania

Romania Area of Mutual Interest (AMI) ADX operator. 60% interest.

Caspian Oil & Gas (ASX: CIG) and Sibinga Petroleum have elected to farm in at a working interest of 20% each in 1QCY2010.

Following a 2 year evaluation and high grading program, ~ 90 leads & prospects have been identified. Activity has been focused on evaluation of and the preparation for the Romanian 10th Bid Round where 30 concessions covering ~30,000 km2 area are available for bid. Bids were due on 19 May 2010.

ADX submitted bids on 4 blocks in the Pannonian Basin (Voivozi, Tria, Biled & Parta) of western Romania.

Romanian gazettal submission has now been completed and ADX is accredited as the E&P operator from the National Agency for Minerals and Resources (NAMR) on 25 May 2010.

The NAMR will evaluate the submissions and shall announce the successful bidders on 1 Jul 2010.

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 9

Source: Company 31 March 2010 Quarterly Activities Report

Farm-in and acquisition evaluations are ongoing and are part of the strategy to successfully bid for and acquire perspective exploration and development acreage within the European community.

[C] Australia

(1) PEL 182 (Cooper Basin, South Australia) ADX operator. 49.9% interest.

PEL 182 is a largely under-explored block in the Cooper Basin on trend with oil and gas discoveries. ADX took over operatorship in May 2008 and has negotiated a revised work commitment and achieved a permit suspension with PIRSA. This has allowed ADX to focus exploration efforts and determine the value of the Vanessa gas condensate discovery and the nearby satellite structures which have been identified through a reinterpretation of the area.

Permit years 2 and 3 have been combined to allow time for the acquisition of prospect oriented 2D seismic data and reprocessing of existing data.

A technical evaluation of the Vanessa gas condensate discovery was completed and showed a significant resource potential. Gas marketing remains a challenge.

Due to strong rainfalls and subsequent heavy flooding in 1QCY2010, ADX has applied for a temporary suspension of the permit to postpone the commitment 2D seismic acquisition.

During 2QCY2010, ADX has received two offers for the operated share.

On 15 Jun 2010, ADX advised it has executed a sale and purchase agreement with Victoria Petroleum (ASX: VPE) for the sale of its interest in PEL 182 for AS$1.1m cash consideration and future plugging and liability for the Emily-1 and Vanessa-1 wells estimated at A$200k. The agreement is subject to approval by the SA government and to pre-emption and consent by all PEL 182 JV parties.

(2) Mining Tenements (Western Australia) ADX holds varying interests in View Resources, Gondwana Resources, St Barbara Ltd,

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 10

Strategic Energy and Enterprise Gold Mines; and maintains various hard rock exploration projects including Millrose and Mt. Webb and non-managed JVs at Bronzewing South, Kara, Dulcie, Prophry and West Yandal.

ADX is planning to spin off its portfolio of gold and base metal assets into a new listed company. ADX will retain a substantial interest in the new entity.

[D] Next Steps

Next Steps

1. Drill deepwater exploration well Lambouka-1 (offshore Sicily Channel), expect to spud on 18 Jun 2010, tendering completed & contracts in place, site survey completed, rig tow imminent;

2. Drill exploration well in Sidi Daher Prospect (onshore Chorbane) in CY2010;

3. Divest holding in PEL 182 (Cooper Basin, Australia) in CY2010;

4. Drill Dougga appraisal well (offshore Sicily Channel) in CY2011.

5. Drill exploration or appraisal well in PEL 182 in late CY2011 (if not already divested); and

6. Drill exploration well in Romania AMI in late CY2011 (~ less than US$3m/well).

Funding for CY2010 program has been firmed up with:

Sicily channel farmouts completed;

Chorbane farmouts near finalisation;

Rights issue (A$7.2m) completed with the despatch of securities into shareholders’ security holdings on 8 Jun 2010.

Programs for 2009- 2011:

Source: General Meeting Presentation, ASX Release 3 Jun 2010

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 11

ADX Energy Limited (ADX)Year end Jun. All figures in A$M unless markedProfit & loss 05A 06A 07A 08A 09A Balance sheet 05A 06A 07A 08A 09AOperating revenue 0 0 0 0 0 Cash & deposits 3 1 0 2 1Total Revenue 0 0 1 1 0 Trade debtors 2 1 0 1 0EBITDA Pre Assoc. -5.1 -2.7 -4.6 -3.5 -3.1 Inventories 0 0 0 0 0Associates 0.0 0.0 0.0 0.0 0.0 Other curr assets 0 0 0 0 0EBITDA -5.1 -2.7 -4.6 -3.5 -3.1 Total current assets 4 3 1 2 1Depreciation/Amort -0.1 -0.1 -0.1 -0.4 -0.1 Fixed Assets 0 0 0 0 0EBIT -5.1 -2.7 -4.6 -3.9 -3.2 Goodwill 0 0 0 0 0Net Interest 0.1 0.1 0.0 0.1 0.1 Intangibles ex goodwill 0 0 0 2 0Pre-tax profit -5.0 -2.7 -4.6 -3.8 -3.1 Other non-curr assets 3 3 2 3 7Tax expense 0.0 0.0 0.0 0.0 0.0 Total assets 8 6 3 8 9Minorities/Prefs 0.0 0.0 0.0 0.0 0.0NPAT -5.0 -2.7 -4.6 -3.8 -3.1 Trade creditors 0 0 0 0 0Non recurring items 0.0 0.0 0.0 0.0 0.0 Curr borrowings 0 0 0 0 0Reported profit -5.0 -2.7 -4.6 -3.8 -3.1 Other curr liabilities 0 0 0 0 0

Total current liab. 0 0 0 0 0EPS & DPS 05A 06A 07A 08A 09A Borrowings 0 0 0 0 0Reported profit -5.0 -2.7 -4.6 -3.8 -3.1 Other non-curr liabilities 0 0 0 0 0Add back non-recurring 0.0 0.0 0.0 0.0 0.0 Total liabilities 0 0 0 0 0Add back Goodwill 0.0 0.0 0.0 0.0 0.0 Minorities/Convertibles 0 0 0 0 0Add back Prefs 0.0 0.0 0.0 0.0 0.0 Shareholders equity 8 6 3 7 8Adjusted profit -5.0 -2.7 -4.6 -3.8 -3.1EFPOWA (m shares) 73 89 121 152 194 Net debt (cash) -3 -1 0 -2 -1Adjusted EPS (cents) -6.8 -3.0 -3.8 -2.5 -1.6Rep. Dil. EPS (cents) -6.8 -3.0 -3.8 -2.5 -1.6 Growth Rates 05A 06A 07A 08A 09AReported EPS (cents) -6.8 -3.0 -3.8 -2.5 -1.6 Asset growth (%) -20.1 -55.8 171.5 15.4

Revenue growth (%) n/a n/a n/a n/aDividend/share (cents) n/a n/a n/a n/a 0 EBITDA growth (%) -46.8 69.2 -23.9 -12.0Franking (%) n/a n/a n/a n/a n/a EBIT growth (%) -46.3 67.6 -15.8 -18.4Payout ratio (%) n/a n/a n/a n/a 0 NPAT growth (%) -46.8 72.0 -16.5 -18.2

Adj. EPS growth (%) -56.4 26.7 -34.0 -35.7Cashflow summary 05A 06A 07A 08A 09A Rep. EPS growth (%) -56.4 26.8 -33.6 -36.3EBITDA -5.1 -2.7 -4.6 -3.5 -3.1Interest and tax 0.1 0.1 0.0 0.1 0.1 Profitability Analysis 05A 06A 07A 08A 09AOther operating items 4.2 2.6 4.0 2.3 1.3 EBITDA Margin (%) 0.0 -15,457.5 -1,226.5 0.0 0.0Operating cashflow -0.7 0.1 -0.5 -1.1 -1.7 EBIT Margin (%) 0.0 -15,779.8 -1,240.4 0.0 0.0Capex -2.1 -2.4 -2.4 -2.9 -3.3 NPAT Margin (%) 0.0 -15,218.9 -1,227.2 0.0 0.0Free cashflow -2.8 -2.3 -2.9 -4.0 -5.0 Tax rate (%) 0 0 0 0 0Dividends 0.0 0.0 0.0 0.0 0.0 Return on Equity (%) -65 -43 -174 -53 -37Acq/Disp 0.2 -0.1 0.7 1.2 -0.8 Return on Assets (%) -62.9 -41.9 -163.2 -50.2 -35.6Other investing items -1.3 0.0 0.3 -1.1 1.0Cashflow pre finance -3.9 -2.4 -1.9 -3.9 -4.8 Net Interest Cover (x) 0.0 0.0 0.0 51.9 61.0Equity 3.2 1.1 1.1 5.4 4.2 Debt/Equity (%) -33 -19 -12 -23 -11Debt inc/(red'n) 0.7 1.3 0.9 -1.6 0.6 Debt/(Debt+Equity) (%) -49 -24 -14 -30 -13

Capex to deprec'n (%) 3657 4217 4710 5636 11528

Inventory Turnover (x) #N/A #N/A #N/A #N/A #N/AAsset Turnover (x) 0.0 0.0 0.1 0.0 0.0Current Ratio (x) 33.5 24.3 6.2 6.2 3.2

Source: IRESS

17 June 2010

Wilson HTM Equities Research – ADX Energy Limited 12

Recommendation Structure BUY: Total return +10% or more over a 12 month period HOLD: Total return expected to be between +10% to -10% over a 12-month period SELL: Total return expected to be -10% or more over a 12 month period TOTAL RETURN OR TSR = capital growth in share price + expected dividend yield in that period Other definitions CS Coverage Suspended. Wilson HTM Ltd has suspended coverage of this company. NR Not Rated. The recommendation has been suspended temporarily. Such suspension is in line with Wilson HTM Investment Group Ltd policies in circumstances where Wilson HTM Corporate Finance Ltd is acting in an advisory capacity in a merger or strategic transaction involving the company and in certain other situations. Disclaimer Whilst Wilson HTM Ltd believes the information contained in this communication is based on reliable information, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. To the extent permitted by law Wilson HTM Ltd disclaims all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage) however caused, which may be suffered or arise directly or indirectly in respect of such information. Any projections contained in this communication are estimates only. Such projections are subject to market influences and contingent upon matters outside the control of Wilson HTM Ltd and therefore may not be realised in the future.

The advice contained in this document is general advice. It has been prepared without taking account of any person’s objectives, financial situation or needs and because of that, any person should, before acting on the advice, consider the appropriateness of the advice, having regard to the client’s objectives, financial situation and needs. Those acting upon such information without first consulting one of Wilson HTM Ltd investment advisors do so entirely at their own risk. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever. If the advice relates to the acquisition, or possible acquisition, of a particular financial product – the client should obtain a Product Disclosure Statement relating to the product and consider the Statement before making any decision about whether to acquire the product. This communication is not to be disclosed in whole or part or used by any other party without Wilson HTM Ltd's prior written consent

Disclosure of Interest. ADX Energy Limited The Directors of Wilson HTM Ltd advise that at the date of this report they and their associates have relevant interests in ADX Energy Limited. They also advise that Wilson HTM Ltd and Wilson HTM Corporate Finance Ltd A.B.N. 65 057 547 323 and their associates have received and may receive commissions or fees from ADX Energy Limited in relation to advice or dealings in securities. Some or all of Wilson HTM Ltd authorised representatives may be remunerated wholly or partly by way of commission. In producing research reports, members of Wilson HTM Ltd Research may attend site visits and other meetings hosted by the issuers the subject of its research reports. In some instances the costs of such site visits or meetings may be met in part or in whole by the issuers concerned if Wilson HTM Ltd considers it is appropriate and reasonable in the specific circumstances relating to the site visit or meeting. BRISBANE SYDNEY MELBOURNE GOLD COAST Ph: 07 3212 1333 Ph: 02 8247 6600 Ph: 03 9640 3888 Ph: 07 5509 5500 Fax: 07 3212 1399 Fax: 02 8247 6601 Fax: 03 9640 3800 Fax: 07 5509 5599 DALBY HERVEY BAY TOWNSVILLE GEELONG Ph: 07 4660 8000 Ph: 07 4197 1600 Ph: 07 4725 5787 Ph: 03 5225 1500 Fax: 07 4660 4169 Fax: 07 4197 1699 Fax: 07 4725 5104 Fax: 03 5225 1599

Our web site: www.wilsonhtm.com.au