ADVANCED TAXATION PROFESSIONAL LEVEL EXAMINATION APRIL …

20

ADVANCED TAXATION PROFESSIONAL LEVEL EXAMINATION APRIL 2021 NOTES: Section A - You are required to answer Questions 1, 2 and 3. Section B - You are required to answer any two out of Questions 4, 5 and 6. Should you provide answers to all of Questions 4 to 6, only the answers to Questions 4 and 5 will be marked. TAXATION TABLES ARE PROVIDED TIME ALLOWED: 3.5 hours, plus 10 minutes to read the paper. This is a closed book examination. INSTRUCTIONS: During the reading time, candidates are encouraged to use this time to read each Question carefully. Please note, however, candidates will not be prevented from using this time to start typing notes and solutions. Marks for each question are shown. The pass mark required is 50% in total over the whole paper. You are reminded to pay particular attention to your communication skills, and care must be taken regarding the format and literacy of your solutions. The marking system will take into account the content of your answers and the extent to which answers are supported with relevant legislation, case law or examples, where appropriate. N.B. Please note that the right click function has been disabled during your examination. Should you wish to copy and paste, please use the following shortcuts: Copy (Ctrl + C) and Paste (Ctrl + V).

Transcript of ADVANCED TAXATION PROFESSIONAL LEVEL EXAMINATION APRIL …

ADVANCED TAXATION

PROFESSIONAL LEVEL EXAMINATION

APRIL 2021

NOTES: Section A - You are required to answer Questions 1, 2 and 3. Section B - You are required to answer any two out of Questions 4, 5 and 6. Should you provide answers to all of Questions 4 to 6, only the answers to Questions 4 and 5 will be marked.

TAXATION TABLES ARE PROVIDED

TIME ALLOWED:

3.5 hours, plus 10 minutes to read the paper. This is a closed book examination.

INSTRUCTIONS:

During the reading time, candidates are encouraged to use this time to read each Question carefully. Please note, however, candidates will not be prevented from using this time to start typing notes and solutions. Marks for each question are shown. The pass mark required is 50% in total over the whole paper.

You are reminded to pay particular attention to your communication skills, and care must be taken regarding the format and literacy of your solutions. The marking system will take into account the content of your answers and the extent to which answers are supported with relevant legislation, case law or examples, where appropriate. N.B. Please note that the right click function has been disabled during your examination. Should you wish to copy and paste, please use the following shortcuts: Copy (Ctrl + C) and Paste (Ctrl + V).

SECTION A Answer Questions 1, 2 and 3 in this Section.

(ALL are compulsory) Question 1 Maria (aged 45) and Jason (aged 51) are both Irish resident and domiciled and jointly assessed for Income Tax purposes. The couple have four children, Abby (aged 15), Kiera (aged 13), Jack (aged 10) and Emily (aged 5). Maria is employed part-time as a HR manager in a multinational company. Details of her income and other benefits from this employment for 2020 are as follows: • Gross salary for the year €65,000 from which PAYE of €24,000 was deducted. • A new company car purchased on 1 January 2020 that cost the company €70,000. The new car is

a category B vehicle. Maria’s business travel for the year was 35,000 kilometres. • On 2 January 2020, Maria was provided with a new mobile phone, that cost €1,200, and a laptop,

that cost €2,200. Both are used solely for business purposes. • Maria was paid a bonus of €25,000 on 15 November 2020. €20,000 of this bonus was paid for the

successful completion of two large business projects during 2020. €5,000 was paid to Maria for achieving a First-Class Honours from her master’s degree in human resources in October 2020.

• Maria received a Christmas voucher worth €300 on 20 December 2020. • Maria contributed €5,200 of her gross salary to an approved occupational pension scheme during

2020 and decided to use all of her bonus to make an additional voluntary contribution on 25 December 2020.

Other Income: • Irish deposit interest €650 (net) • Children’s allowance €3,120

Jason’s taxable profits from his veterinary practice for the year ended 31 December 2020 were €350,000. Capital allowances for the business for 2020 are €25,000. Professional Services Withholding Tax in the amount of €35,000 was incurred on income received by Jason for services provided to the State during the year ended 31 December 2020. In addition, Jason had the following sources of income during 2020: • Rental income from a residential apartment of €18,000 per annum. The tenancy was registered

with the Residential Tenancies Board (RTB). Jason paid insurance of €800, painting and maintenance costs of €1,500 and local property tax of €175 on the house for 2020. Mortgage interest paid for 2020 was €1,400. Jason carried forward a rental loss from 2019 of €3,000.

• Dividend income from an Irish company of €540 was received on 15 February 2020 (final dividend for the financial year ended 31 December 2019).

Details of other expenditure for 2020 are as follows: • Medical expenses €4,200, including €400 for a routine annual eye test and glasses for Kiera, €800

for orthodontic treatment for Abby. The couple were reimbursed €700 by their medical insurance company, including €100 towards the cost of Kiera’s eye test and glasses. No reimbursement was received for the orthodontic treatment.

• Jason maximised his retirement annuity contributions for tax relief purposes for 2020.

The couple’s Income Tax liability for the tax year 2019 was €50,000. REQUIREMENT: (a) Advise Maria and Jason on the maximum pension contribution they may make in order to

minimize their tax liability for the tax year 2020. Calculate the amount of tax they are likely to save as a result and state the latest date of payment for making the additional contribution.

(6 marks)

(b) Calculate Maria and Jason’s income tax liability for the tax year 2020, excluding the liability for PRSI and Universal Social Charge (USC).

(11 marks) (c) Advise Maria and Jason of their pay and file obligations for the tax year 2020 clearly outlining both

the relevant dates and the amounts to be paid. (3 marks)

[Total: 20 Marks]

Question 2 Windham Ltd is an Irish resident company. Extracts from the company’s accounts for the year ended 30 June 2020 show the following:

Notes € € Gross profit from trading 1,935,200 Other income (i) 90,000 2,025,200 Less expenses Salaries and wages (ii) 669,000 Depreciation 143,550 Patent Royalty (iii) 200,000 Repairs and maintenance (iv) 75,300 Rates and utilities (v) 150,000 Legal and professional fees (vi) 35,000 Motor expenses (vii) 240,000 Insurance (viii) 36,000 Miscellaneous allowable expenses 14,600 (1,563,450) Less finance costs (ix) (47,800) Net profit before tax 413,950

Notes: (i) Other income includes the following:

€ Rental income 70,000 Dividends from James Ltd, an Irish resident company 5,000 Dividends from Bucket plc, a US company 15,000 90,000

Rental income is received from a residential apartment complex that the company leases long-term through a letting agent. Dividends are received from a US trading company in which Windham Ltd holds 15% of the share capital. Dividends are paid out of the trading profits of the US company.

(ii) Salaries and wages include pension contributions of €82,000. The expense includes an accrual at the end of the year for pension contributions of €13,500. There was no opening accrual or prepayment in respect of the pension scheme.

(iii) Windham Ltd has a patent royalty agreement with an affiliate company. The amount unpaid by Windham Ltd to the connected company during the year ended 30 June 2020 was €120,000.

(iv) Repairs and maintenance include the following: € Premises maintenance 8,000 Equipment and machinery maintenance 14,000 Repairs in relation to rented apartment complex 17,500 Replacement of entrance to rented apartment complex with upgraded security gates 30,000 Loss on disposal of computer equipment 5,800 75,300

(v) Rates and utilities include the following:

€ Light, heat and telephone for trade premises 80,000 Replacement of mobile devices for sales employees 15,000 Installation of new security alarm system in rented apartment complex 30,000 Rates for trade premises 25,000 150,000

(vi) Legal and professional fees include the following:

€ Audit and accountancy fees 18,000 Trade subscription to employer representative group 10,000 Letting agent fees for rental premises 7,000 35,000

(vii) Motor and travel expenses include the following:

€ Mileage and subsistence for employee business travel 182,000 Annual servicing and repairs for company vehicles 40,000 Lease charge for delivery van (cost €42,000, category D) 7,400 Lease charges for company car (cost €46,000, category B) 8,600 238,000

(viii) Insurance costs include the following:

€ For rented property 4,000 For trade premises 21,000 25,000

(ix) Finance costs include the following:

• €10,000 interest was paid during the year ended 30 June 2020 in respect of a loan taken out to fund working capital requirements of the business.

• €17,800 relates to finance lease interest. Total finance lease repayments for the year ended 30 June 2020 amounted to €71,200.

• The remaining interest relates to long-term borrowings used for the purpose of the trade.

(x) Information relating to fixed assets: Assets held at 1 July 2019 Cost Tax Written Down Value Computer Equipment €48,000 €30,000 Industrial Buildings €750,000 €300,000

During the year ended 30 June 2020 computer equipment that originally cost €10,000 during the year ended 30 June 2015 was scrapped. REQUIREMENT: (a) Compute the corporation tax liability of Windham Ltd in respect of the year ended 30 June 2020.

(16 marks)

(b) Advise the company of its corporation tax compliance obligations for the year ended 30 June 2020. The company’s corporation tax liability for the year ended 30 June 2019 was €350,000.

(4 marks)

[Total: 20 Marks]

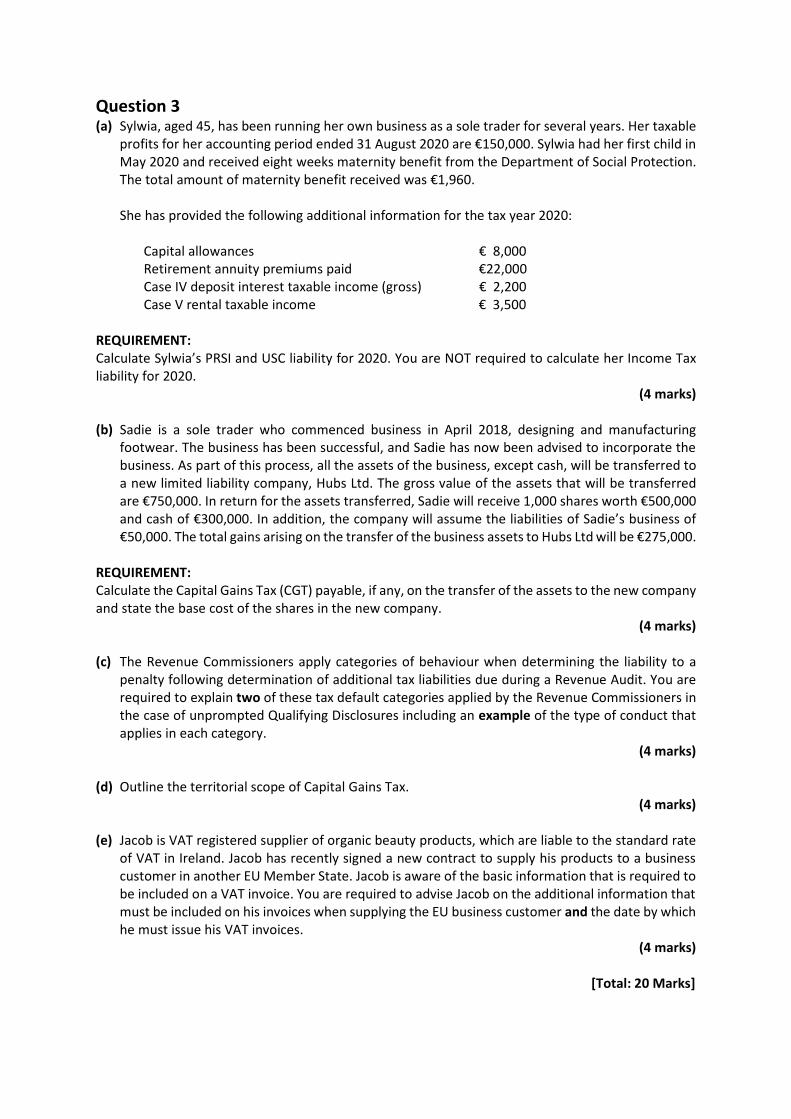

Question 3 (a) Sylwia, aged 45, has been running her own business as a sole trader for several years. Her taxable

profits for her accounting period ended 31 August 2020 are €150,000. Sylwia had her first child in May 2020 and received eight weeks maternity benefit from the Department of Social Protection. The total amount of maternity benefit received was €1,960. She has provided the following additional information for the tax year 2020:

Capital allowances € 8,000 Retirement annuity premiums paid €22,000 Case IV deposit interest taxable income (gross) € 2,200 Case V rental taxable income € 3,500

REQUIREMENT: Calculate Sylwia’s PRSI and USC liability for 2020. You are NOT required to calculate her Income Tax liability for 2020.

(4 marks)

(b) Sadie is a sole trader who commenced business in April 2018, designing and manufacturing footwear. The business has been successful, and Sadie has now been advised to incorporate the business. As part of this process, all the assets of the business, except cash, will be transferred to a new limited liability company, Hubs Ltd. The gross value of the assets that will be transferred are €750,000. In return for the assets transferred, Sadie will receive 1,000 shares worth €500,000 and cash of €300,000. In addition, the company will assume the liabilities of Sadie’s business of €50,000. The total gains arising on the transfer of the business assets to Hubs Ltd will be €275,000.

REQUIREMENT: Calculate the Capital Gains Tax (CGT) payable, if any, on the transfer of the assets to the new company and state the base cost of the shares in the new company.

(4 marks) (c) The Revenue Commissioners apply categories of behaviour when determining the liability to a

penalty following determination of additional tax liabilities due during a Revenue Audit. You are required to explain two of these tax default categories applied by the Revenue Commissioners in the case of unprompted Qualifying Disclosures including an example of the type of conduct that applies in each category.

(4 marks)

(d) Outline the territorial scope of Capital Gains Tax. (4 marks)

(e) Jacob is VAT registered supplier of organic beauty products, which are liable to the standard rate

of VAT in Ireland. Jacob has recently signed a new contract to supply his products to a business customer in another EU Member State. Jacob is aware of the basic information that is required to be included on a VAT invoice. You are required to advise Jacob on the additional information that must be included on his invoices when supplying the EU business customer and the date by which he must issue his VAT invoices.

(4 marks) [Total: 20 Marks]

SECTION B Answer ANY TWO of the three questions from this Section.

Question 4 (a) Aoife (age 59) and Adam (Age 65) are jointly assessed for tax purposes. The couple made the

following disposals of assets during 2020:

(i) In February 2020, Adam sold an antique watch for €4,000. He had inherited the watch from his father in January 1995 at which time it was valued at €300. Adam’s father had purchased the watch at an auction in June 1990 for €30.

(ii) Adam sold his car for €5,000 in May 2020. The car was purchased in July 2015 for €35,500.

(iii) In July 2020, Adam sold an investment property for €350,000. He had purchased the property in January 2003 for €200,000 and spent another €100,000 on an extension to the property in January 2007.

(iv) In September 2020, Aoife sold 4,000 shares in HTM Plc for €28,000. She had invested in the

shares of HTM Plc as follows: 1 February 1993 Purchased 2,000 shares for €4,000 10 May 1997 Received bonus shares, HTM Plc made a 1 for 1 bonus issue. The

market value of the shares on 10 May 1997 was €2.50 per share 6 November 2003 Purchased 6,000 shares for €36,000 20 October 2010 Sold 2,000 shares for €20,000

(v) On 1 December 2020, Adam sold his shares in his optician business to an unconnected person

for €950,000. €500,000 related to the shop premises, €25,000 related to equipment used for the purpose of the trade, €225,000 related to inventory and €200,000 for goodwill. Adam purchased the shares on 1 January 2007 for €500,000, when the business started. Adam has been a full-time working director in the company since acquiring the shares.

REQUIREMENT: Calculate Aoife and Adam’s Capital Gains Tax (CGT) liabilities in respect of the disposals (i) to (v). You are required to clearly explain the conditions of exemptions or reliefs available.

(15 marks)

(b) Elizabeth inherited investment shares from her sister on 14 June 2020. The shares were valued at €50,000 at the date of inheritance. Elizabeth had previously received a gift of €10,000 from her grandmother on 1 January 2005 and inherited €15,000 from her father on 7 December 2010. Stamp duty of €500 was payable by Elizabeth on the transfer of ownership of the shares to her name.

REQUIREMENT: Calculate Elizabeth’s Capital Acquisitions Tax (CAT) liability on the inheritance received on 14 June 2020.

(5 marks)

[Total: 20 Marks]

Question 5 (a) Brighter Future (BF) Ltd is an Irish resident company. The following information has been provided

for the last three accounting periods: 12-month accounting

year ended 31 December 2018

9-month accounting period ended 30 September 2019

6-month accounting period ended 31

March 2020 € € Case I 180,000 (360,000) 60,000 Case V 24,000 24,000 (10,000) Capital gain (not adjusted for corporation tax purposes)

2,500

REQUIREMENT: Prepare the Corporation Tax computation for each of the three accounting periods and detail the loss memorandum showing the use of the losses made by Brighter Future. You can assume the company maximises the use of its losses at the earliest opportunity.

(7 marks)

(b) Sunrise Ltd, an Irish resident trading company, is considering selling its 50% shareholding in Glow Ltd to a US multinational company. The shareholding was purchased in February 2018.

REQUIREMENT: State the exemption from Capital Gains Tax that Sunrise Ltd can claim on the disposal of its shareholding in Glow Ltd and outline the four main conditions that must be satisfied to claim this exemption.

(4 marks)

(c) Outline the two tests that apply in determining if a company is a close company for Irish tax purposes.

(4 marks) (d) Jasmine was made redundant on 15 June 2020. She had joined the company on 1 September 2005.

Her redundancy payment comprised the following:

€ Statutory redundancy 7,500 Ex-gratia payment 90,000 Holiday pay 3,000 Pay in lieu of notice (not provided for in Jasmine’s contract) 6,000 Company car (value on 15 June 2020) 15,000

Jasmine’s gross salary, including benefits-in-kind, for the three years up to 15 June 2020 was €110,000 per annum. The actuarial value of her tax-free lump sum entitlement from her occupational pension scheme is €40,000. REQUIREMENT: Calculate Jasmine’s taxable termination payment on the basis that she claims the maximum relief available to her.

(5 marks) [Total: 20 Marks]

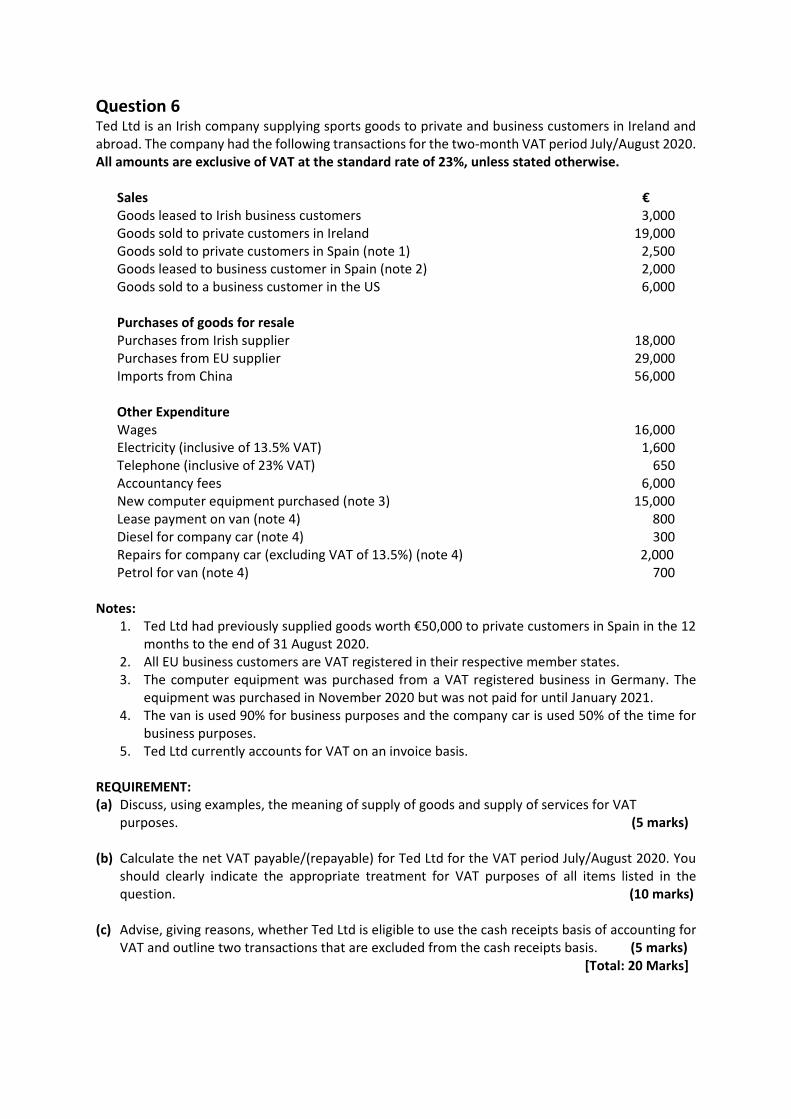

Question 6 Ted Ltd is an Irish company supplying sports goods to private and business customers in Ireland and abroad. The company had the following transactions for the two-month VAT period July/August 2020. All amounts are exclusive of VAT at the standard rate of 23%, unless stated otherwise.

Sales € Goods leased to Irish business customers 3,000 Goods sold to private customers in Ireland 19,000 Goods sold to private customers in Spain (note 1) 2,500 Goods leased to business customer in Spain (note 2) 2,000 Goods sold to a business customer in the US 6,000 Purchases of goods for resale Purchases from Irish supplier 18,000 Purchases from EU supplier 29,000 Imports from China 56,000 Other Expenditure Wages 16,000 Electricity (inclusive of 13.5% VAT) 1,600 Telephone (inclusive of 23% VAT) 650 Accountancy fees 6,000 New computer equipment purchased (note 3) 15,000 Lease payment on van (note 4) 800 Diesel for company car (note 4) 300 Repairs for company car (excluding VAT of 13.5%) (note 4) 2,000 Petrol for van (note 4) 700

Notes: 1. Ted Ltd had previously supplied goods worth €50,000 to private customers in Spain in the 12

months to the end of 31 August 2020. 2. All EU business customers are VAT registered in their respective member states. 3. The computer equipment was purchased from a VAT registered business in Germany. The

equipment was purchased in November 2020 but was not paid for until January 2021. 4. The van is used 90% for business purposes and the company car is used 50% of the time for

business purposes. 5. Ted Ltd currently accounts for VAT on an invoice basis.

REQUIREMENT: (a) Discuss, using examples, the meaning of supply of goods and supply of services for VAT

purposes. (5 marks)

(b) Calculate the net VAT payable/(repayable) for Ted Ltd for the VAT period July/August 2020. You should clearly indicate the appropriate treatment for VAT purposes of all items listed in the question. (10 marks)

(c) Advise, giving reasons, whether Ted Ltd is eligible to use the cash receipts basis of accounting for VAT and outline two transactions that are excluded from the cash receipts basis. (5 marks) [Total: 20 Marks]

THE INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS IN IRELAND

ADVANCED TAXATION PROFESSIONAL LEVEL APRIL 2021

Page 11

SUGGESTED SOLUTIONS

!"#$%&"'%!()*+,)%-,)$#+./$+,)%0(1+(23"#+"%4%#(1+(2%#(1"$(5%$,%678(5/1(%9%+)7,:( 3"#;*

!"#"$% &'()))*+,-.-/012"3%-/"$-456)()))-7-89:; 8<(&)) 8=))-----------

>"7"?#@-?03AB <)())) )=')-----------C7"1-"D"$E-?03AB ) )=')-----------

F0?G#@-2H03@IJ"2K02 ) )=')-----------LH$GBK1"B-M0A/H@$-430K-/"BH(-N-5')); ) )=')-----------

O6(&))

PQ@-R'-ST-1"7=-$@#G@U(-5O<(&))-7-<': <R(R))------------ )=')-----------L03K$G?AKG03B-1"E@-45'(<))-V-5<'())); W)(<))------------ )=')-----------F"7=-$@#G@U-U0$-2@3BG03-/03K$G?AKG03B <R(R)) 8=))-----------

<"*,)%4%#(1+(2%#(1"$(5%$,%-"*(%=%+)7,:(PQ@-'8-ST-1"7=-$@#G@U(-588'()))-7-W): WR('))----------------------------------------------------- 8=))-----------

>?@@%%%%%%%%%%%

!"#$%&.'%=)7,:(%A"B%-,:C/$"$+,) 3"#+" <"*,) 3"#;*D D

!/H@EA#@-C-4U$01-2"$K-"; O6(&))L"B@-+-45W')()))-.-5<'())); W<'())) )=')-----------L"B@-+X-4&')I)=&6; O6) )=')-----------L"B@-X-4D8; 88(W)) 8=')-----------!/H@EA#@-Y-45'R)-I-)=6'; 6<) )=')-----------LHG#E$@3ZB-"##0D"3/@-.-@7@12K ) )=')-----------

O9('6) WW6()<)P##0D"3/@[-\@3BG03-/03K$G?AKG03B-42"$K-"; 4<R(R)); 4WR(')); 8=))-----------

6R(86) W)<('<)>0K"#-G3/01@ W6&(&O)

>"7-/"#/A#"KG0356)(&))-]-<): 8R(8<) )=')-----------L"B@-+X-]-WW: W<) )=')-----------*"#"3/@-]-R): 8<<()R9 )=')-----------

8W&(R99>"7-L$@EGKB\@$B03"#-/$@EGKB 4W(W)); )=')-----------\P^C-/[email protected]"$G" 48(&'); )=')-----------C"$3@E-G3/01@-/[email protected]_"B03-.30K@-8(&')-$@K$0B2=(-8('))-"#B0-"//@2 48(&'); )=')-----------F@EG/"#-@72@3B@B-4D<; 4&R); 8=')-----------`+a> 4W<); )=')-----------`b> 489); )=')-----------\!b> 4W'())); )=')-----------\P^C-2"GE 4<R())); )=')----------->"7-2"%"?#@ &O(6R9

EE?@@%%%%%%%%

SOLUTION 1

Page 12

FG0H=IJ6K#(";5,L)%,2%3"#;*%2,#%F,#;+)M*%&$,$"1*%+)7,#C,#"$(5%+)%=)7,:(%A"B%-,:C/$"$+,)'b0$cG3Q-8[-L"B@-X-+3/01@ D D 3"#;*L"B@-X-a@3K"#-+3/01@a@3K"#-G3/01@ 89()))C72@3B@B+3BA$"3/@ 9))\"G3KG3Q 8('))J\> ) )=')-----------+3K@[email protected])):-"##0D@E 8(R))

4W(6));8R(W))

J0BB-/"$$G@E-U0$D"$E 4W())); )=')----------->"7"?#@-G3/01@ 88(W)) )=')-----------

!"#$%%%%%%%%%%

b0$cG3Q-<[-F@EG/"#-C72@3B@B D D 3"#;*

>0K"#-@72@3B@B R(<))C7/#AE@a0AKG3@-02KG/"#-@72@3B@B 4R)); )=')-----------a@G1?A$B@E-/0BKB-4U0$-@#GQG?#@-@72@3B@B;-46))-.-8)); 4&)); )=')-----------P##0D"?#@-@72@3B@B W(<))

>"7-$@#G@U-"K-<): &R) )=')-----------!"#$%%%%%%%%%%

!"#$%&7'%!"N%")5%O+1(%G.1+M"$+,)*%2,#%P@P@ 3"#;*8;-\$@#G1G3"$%-+3/01@->"7-2"%1@3K

`"K@ W8I8)I<)<)- 48)I8<I<)<)-U0$-ad!-UG#@$B; )=')-----------P10A3Ke-O):-0U-/A$$@3K-%@"$-0$-8)):-0U-2$G0$-%@"$

O):-0U-<)<) &<(66W )=')-----------8)):-0U-<)8O ')())) )=')-----------

\"%-"K-#@"BK-KH@-#0D@$-0U-KH@B@-KD0-"10A3KB ')())) )=')-----------

<;-*"#"3/@-0U-#G"?G#GK%-K0-?@-2"GE W8I8)I<)<8- 40$-ad!-@7K@3BG03-Q$"3K@E; )=')-----------

W;-YG#@-+3/01@->"7-a@KA$3 W8I8)I<)<8- 40$-ad!-@7K@3BG03-Q$"3K@E; )=')-----------

Q?@@%%%%%%%%%%%

Page 13

!"#"$%$&"'()'*+(),"'(+'-(..'/')(+',&)(+%#",(& !"#$% 0 '0'&'"%%()'"*+#(*'",(#'-.+/0 1234526778#9$'(+/:",$( ;+< 372777

627652677=$%%(-.,+/+%#'-#+"/(:"%#%>-0$%(-/.(%-?-'+$% ;++< @@32777A$)'$:+-#+"/ 1B42557C-#$/#('"D-?#D ;++< 6772777E$)-+'%(-/.(,-+/#$/-/:$ ;+F< G52477E-#$%(-/.(H#+?+#+$% ;F< 1572777=$0-?(-/.()'"*$%%+"/-?(*$$% ;F++< 452777I"#"'(-/.(#'-F$?($J)$/%$% ;F+++< 6B72777K/%H'-/:$( 4@2777I+%:$??-/$"H% ;+J< 1B2@77

;125@42B57<=$%%(*+/-/:$(:"%#% ;J< ;BG2L77<C'"*+#(M$*"'$(#-J B142357

1#2'3(+4(+#",(&'5#6'3(%47"#",(&3#.$'8'8&9(%$')(+'":$';$#+'$&<$<'=>'?7@7."'ABAB 0 '0' C#+D.C'"*+#(M$*"'$(#-J B142357 7N5

A$.H:#+"/%8#9$'(+/:",$ 372777 7N5O+/-/:$(?$-%$(P(#"#-?()-D,$/#% G12677 7N5Q-)+#-?(-??"R-/:$%(;R1< B724G5

;67125G5<S..M-:T%A$)'$:+-#+"/ 1B42557 7N5C-#$/#('"D-?#D 6772777 7N5>-0$%(-/.(%-?-'+$%(P()$/%+"/(-::'H-? 142577 7N5E$)-+'%(-/.(,-+/#$/-/:$Q-%$(U('$/#-?()'")$'#D(,-+/#$/-/:$ 1G2577 7N5Q-%$(U(MH+?.+/0(+,)'"F$,$/#% 472777 7N5="%%("/(.+%)"%-?("*(:",)H#$'($VH+),$/# 52L77 7N5

E-#$%(-/.(W#+?+#+$%!$R(,"M+?$(.$F+:$% 152777 7N5Q-%$(U(MH+?.+/0(+,)'"F$,$/#% 472777 7N5

=$0-?(-/.()'"*$%%+"/-?(*$$%(P(?$##+/0(-0$/#(*$$% G2777 7N5I"#"'(-/.(#'-F$?($J)$/%$%A$?+F$'D(F-/(?$-%$(P(-??"R-M?$ 7 7N5=$-%$(:9-'0$%(IU(;L2@77(J(B@TP6BTXB@T< B2114 1

K/%H'-/:$(P(Q-%$(U('$/#-?()'")$'#D(+/%H'-/:$ B2777 7N5O+/-/:$(:"%#%O+/-/:$(?$-%$(+/#$'$%# 1G2L77 7N5S??("#9$'(+/#$'$%#(-??"R-M?$(P(*"'(#'-.$()H')"%$% 7 7N5

BLL26@4Q-%$(K(+/:",$ G772@4L

EFGH8IJ!>"'T+/0(1(P(:-)+#-?(-??"R-/:$% 3(."Q",)H#$'(YVH+),$/# BL2777A+%)"%-? ;172777<S..+#+"/%(;'-#$(-/.(H#+?+#+$%(/"#$%< 152777

542777>$-'(Z(#$-'(6767 16N5[ @2@65 7N5

K/.H%#'+-?(\H+?.+/0 G572777K/.H%#'+-?(MH+?.+/0%(-//H-?(-??"R-/:$ BN7[ 472777 7N5

!"#$](\-?-/:+/0(-??"R-/:$X:9-'0$(P('$(A$?+F$'D(U-/Q"%#(6715 172777>$-'(Z(#$-'(6715(P(6713 ;@2657<^>AU(_(1(̀ H?D(6713 42G57C'":$$.% 7\-?-/:+/0(S??"R-/:$ 42G57 7N5^"#-?(:-)+#-?(-??"R-/:$%(*"'(6767 B724G5

SOLUTION 2

Page 14

>"'T+/0(6(P(Q-%$(U(E$/#-?(K/:",$K/:",$S//H-?('$/# G72777

YJ)$/%$%E$)-+'% 1G2577K/%H'-/:$ B2777=$##+/0(-0$/#(*$$% G2777Q-)+#-?(-??"R-/:$%(*"'(MH+?.+/0(+,)'"F$,$/#%;472777(a(472777<(J(16N5[ G2577 1

;4@2777< 1Q-%$(U( 4B2777

3FG*FG?58FI'5?K'3FC*L5?58FIQ-%$(K( G772@4L^'-.$(:9-'0$]()-#$/#('"D-?#D()-+.(;6772777(P(1672777< ;L72777< 7N5

@672@4LQ-%$(U((;R6< 4B2777 7N5OKK(P(K'+%9(.+F+.$/.(+/:",$(P($J$,)# 7 7N5Q-%$(KKK(P(*"'$+0/(.+F+.$/.(+/:",$ 152777

@@32@4L

Q-%$(K( @672@4L 16N5[ GG25L7 7N5Q-%$(KKK(;%61\(.+F+.$/.%(P("H#("*(#'-.+/0()'"*+#%< 152777 16N5[ 12LG5 7N5Q-%$(U( 4B2777 65N7[ L2577 7N5

LG2355K/:",$(̂ -J("/()-#$/#('"D-?#D()-D,$/# 1@2777 7N5^"#-?(Q"')"'-#+"/(̂ -J(=+-M+?+#D 1742355

>M

92'*#;'#&<'N,O$'G7O$.I"'$(#9-/(b6772777(*"'()'+"'(D$-'2(#9$'$*"'$(c?-'0$c(:",)-/D(*"'(6767 7N5

^R"(C'$?+,+/-'D(̂ -J()-D,$/#%(-'$('$VH+'$.2(#9$(*+'%#(@(,"/#9%(M$*"'$(#9$(D$-'($/.(-/.(#9$(%$:"/.("/$(,"/#9(M$*"'$(D$-'($/.1<(C'$?+,+/-'D(̂ -J(C-D,$/#(1

!"#$ 64(A$:(6713 7N5%&'()# B5[("*(:H''$/#(D$-'2("' PMQRSB 7N5

57[("*()'+"'(D$-' 1G52777

6<(C'$?+,+/-'D(̂ -J(C-D,$/#(6!"#$ 64(I-D(6767 7N5

%&'()# M'+/0(#"#-?(#"(37[("*(:D PMQRSB 7N5

4<(\-?-/:+/0()-D,$/#(-/.('$#H'/ 7N5!"#$ 64(I-'(6761 7N5

%&'()# \-?-/:$ >BQ=TU 7N5P

(b)

Page 15

!"#$%&'()"$*$+,%-$"./$0%1 2"345+,%-$ !"#$$%&'(#)* +,-.---

/012304%044#50'(*$ 67.---8 -9,:#%;*;<(32#'%=#"%1*'$2#'%1"*)2<)$ - -9,>03*"'23?%@*'*=23 - -9,/0$*%&A%2'(#)* B.B--/0$*%A%2'(#)* C.,--

+DE.E--

FGH& DI ,.J-7 -9,

0%1 !"#$$%&'(#)*%1*"%FGH& +DE.E--KL(4<;*%/0$*%&A%2'(#)* 6B.B--8 -9,

+D,.,--

6+B.-+B%%%%%%%%%%%%%%%%%%%%%%%%%%%%% M%-9,I N-9-N7.DEB%%%%%%%%%%%%%%%%%%%%%%%%%%%%%%%% M%BI +NJ9DD

DJ.,N-%%%%%%%%%%%%%%%%%%%%%%%%%%%%% M%D9,I B.BC-9B- -9,BJ.J,N%%%%%%%%%%%%%%%%%%%%%%%%%%%%% M%7I B.CJN9D7 -9,D,.,--%%%%%%%%%%%%%%%%%%%%%%%%%%%%% M%++I ,.--,9-- -9,

J.7N+

7

!8#$%"/)9$*$1":);"'$<").5$=">$;3".5?93$@?$8A5).955$39')9? 2"345O#304%P02'$ BE,.---Q*=*""*;%P02' 6BE,.---%L%,--.---RE,-.---8 6+7C.CCC8 +9,O0L0@4*%P02' J+.NNES''<04%*L*)132#' 6+.BE-8 -9,

J-.CJE/!O%M%CCI BCDEFG -9,

H"59$I@5;$@?$5J"395A04<*%#=%$T0"*$ ,--.--- -9,Q*=*""*;%P02' 6+7C.CCC8 -9,U0$*%(#$3 FGKDKKL -9,

7

SOLUTION 3

Page 16

!I#$,9M9.A9$NA/);5 2"345!"#"!"$%&'(

)*+"$%&'",-&"./012.,3.14"5%204-&3"5-&&05263)*+",-&"0#%$760"-,"809%:.-;&".1"0%59"5%204-&3

<"$%&'",-&"0#76%1%2.-1"-,"0%59"5%204-&3+8%Q*42@*"03*%@*T0V2#<"%

B8%/0"*4*$$%@*T0V2#<"%523T%$2P'2=2(0'3%(#'$*W<*'(*$=024<"*%3#%30X*%"*0$#'0@4*%(0"*

C8%/0"*4*$$%@*T0V2#<"%523T#<3%$2P'2=2(0'3%(#'$*W<*'(*$%;*=0<43$%#=%0%)2'#"%'03<"*%3T03%0"*%;2$(#V*"*;%;<"2'P%0%G*V*'<*%0<;23

7

!/#$1<=$*$=933);@3)"'$%I@:9 2"345&';2V2;<04%(2"(<)$30'(*$ Y20@2423?%3#%/!O&"2$T%"*$2;*'3.%#";2'0"24?%"*$2;*'3%0';%;#)2(24*; Z#"4;52;*%P02'$ +Q#)2(24*;%0';%#";2'0"24?%"*$2;*'3%#"%"*$2;*'3 Z#"4;52;*%P02'$ +:#'[;#)2(24*;%0';%"*$2;*'3R#"%#";%"*$2;*'3 &"2$T%$#<"(*%P02'%0';%"*)2330'(*$ +\3T*"$ H1*(2=2*;%0$$*3$ +

7

!9#$ON=$-.M@)I95 2"345S;;232#'04%;*3024$%"*W<2"*;%#'%("#$$%@#";*"%2'V#2(*$0$$<)2'P%@<$2'*$$%(<$3#)*"%2$%"*P2$3*"*;%=#"%ASO%2'%#3T*"%K]%)R$+9%(<$3#)*"$%ASO%"*P2$3"032#'%'<)@*" GC9%-I%&"2$T%ASO%01142*$ GD9%$303*)*'3%"*%(<$3#)*"%$*4=[0((#<'32'P%=#"%ASO%2'%#3T*"%K]%)R$ G

S%ASO%2'V#2(*%)<$3%@*%2$$<*;%523T2'%+,%;0?$%#=%3T*%*';%#=%3T*%)#'3T%2'%5T2(T G3T*%P##;$%R%$*"V2(*$%0"*%$<1142*;

7

;*42@*"03*%@*T0V2#<"%2'V#4V*$%0%@"*0(T%#=%0%30L%#@42P032#'%5T*"*%3T*"*%2$%2'3*'3%#'%3T*%10"3%#=%3T*%30L10?*"%0';%$#%;#*$%'#3%W<042=?%0$%(0"*4*$$%@*T0V2#<"9KL0)14*$%#=%;*42@*"03*%@*T0V2#<"%2'(4<;*%=024<"*%3#%)02'302'%@##X$%0';%"*(#";$.%#)2$$2#'%#=%

%%OT2$%(03*P#"?%0"2$*$%5T*"*%3T*%30L%<';*"102;%2$%4*$$%3T0'%+,I%#=%3T*%30L%420@2423?%<432)03*4?%;<*9

=#"%*L0)14*.%(#)1<3032#'04%*""#"$%0';%2'0;*W<03*%0;^<$3)*'3$%=#"%1*"$#'04%*L1*';23<"*%2'%3T*%1"#=23%0';%4#$$%0((#<'39

_H2P'2=2(0'3%(#'$*W<*'(*$`%01142*$%5T*"*%3T*%30L%<';*"102;%2$%P"*03*"%3T0'%+,I%#=%3T*%(#""*(3%30L%10?0@4*%=#"%3T*%"*4*V0'3%1*"2#;KL0)14*$%#=%(0"*4*$$%@*T0V2#<"%2'(4<;*%=024<"*%3#%30X*%0;V2(*.%'*P4*(32'P%3#%(03*P#"2$*%*L1*';23<"*%2'3#%044#50@4*%0';%;2$044#50@4*%(03*P#"2*$%=#"%30L%1<"1#$*$.%2'$<==2(2*'3%$30';0";%#=%"*(#";%X**12'P%2'%3T*%@<$2'*$$9

SOLUTION 4

Page 17

!"#$%&"' (")*$"+%,"*-.%/"0!"# $%&"'()*+,&-. 1 1 2"#3.

/01-))23* 45666713&*89*:;*!<4=<># ?66 6@>A%2)B,&"1%*C,-&10 D@?6< 6@>A%2)B)2*-13& !?<?#7,E"&,F*G,"% ?5H6I

7JK*L*??M D5D<671NE,0)*7JK*F",O"F"&P*&1*:,0G"%,F*0)F")CQ!45666*R*S5>46#*T*>6M 456 D:,0G"%,F*0)F")C*N10)*C,U1(0,OF)*!,%%(,F*)B)NE&"1%*%=,*&1*$2,N*C10*S6S65*3))*2"3E13,F*U#

!""# 7,0*R*V,3&"%G*-.,&&)F5*)B)NE& D

!"""# A%U)3&N)%&*/01E)0&P 1 1/01-))23* ?>65666713&*!S66?# !S665666#W%.,%-)N)%&*!S66I# !D665666#7,E"&,F*G,"% >65666 6@>

!"U# A%U)3&N)%&*X.,0)*Y"3E13,F7889:85 7884:8;

/(0-.,3)*!ZS# S5666[1%(3*!Z6# S5666 6@>/(0-.,3)*!Z<# H5666[,F,%-) 45666 H5666X1F2 !S5666# 6 6@>[,F,%-) S5666 H5666

/01-))23*R*D<<S=<?*3.,0)3 D45666 6@>713&*!<S=<?#*R*.,FC*1C*10"G"%,F*E(0-.,3)5*%1*-13&*0)*O1%(3*3.,0)3 S5666 DA%2)B,&"1%*C,-&10 D@?>H 6@>A%2)B)2*-13& !S5IDS#7,E"&,F*G,"% DD5S\\

/01-))23*R*D<<I=<\*3.,0)3 D45666713&*!<H=<I#* D\5666 6@>A%2)B,&"1%*C,-&10*R*"%2)B,&"1%*-,%%1&*"%-0),3)*F133 %=, DA%2)B)2*-13& !D\5666#$-&(,F*F133*1%*2"3E13,F !45666# 6@>

])&*G,"%*1%*2"3E13,F*1C*1C*̂ K:*EF-*3.,0)3 I5S\\

!U# _)&"0)N)%&*_)F")C/01-))23 <>65666713&*!S66I# !>665666#7,E"&,F*G,"% 4>65666

_)&"0)N)%&*0)F")C*-1%2"&"1%3Q$&*F),3&*>>*P),03*1C*,G) 6@>X.,0)3*1V%)2*C10*,&*F),3&*D6*P),03 6@>+10`"%G*2"0)-&10*C10*,&*F),3&*D6*P),03 6@>a(FF*&"N)*2"0)-&10*C10*,&*F),3&*>*P),03 6@>a(FF*)B)NE&"1%*"3*E01-))23*b*ZI>65666*!b*HH*P),03# 6@>

7.,0G),OF)*O(3"%)33*,33)&3*31F2*OP*$2,NX.1E*E0)N"3)3 >665666W'("EN)%& S>5666A%U)%&10P*%1&*7[$ 6J112V"FF S665666

IS>5666 D

c)33*&.,%*ZI>65666*&.)0)C10)*C(FF*)B)NE&"1%*C10*2"3E13,F*1C*O(3"%)335 6@>

Page 18

<=>>"#?%@A%(")*$"+%,"*-.% B@*AC BD">1 1

* !"#*+,&-. 6!""#*7,0 6!"""#*A%U)3&N)%&*E01E)0&P >65666!"U#*A%U)3&N)%&*3.,0)3 I5S\\!U#*[(3"%)33*3.,0)3 6

I5S\\ >65666$%%(,F*)B)NE&"1% !D5SI6# 6@>$%%(,F*)B)NE&"1%*R*%1%)*"%*P),0*1C*0)&"0)N)%&*0)F")C 6 DK,B,OF)*G,"% H56D\ >65666

7,E"&,F*J,"%3*K,B*L*??M D5<\H DH5>66 6@>:,0G"%,F*0)F")C*!"# I?6 6@>K1&,F*F",O"F"&P D5<\H DI5S?6

7E

!"#$%&F' (")*$"+%BGH=*.*$*@-.%/"0 2"#3.1 1

:,0`)&*U,F()*1C*"%.)0"&,%-) >65666 6@>c)33*-13&3d*3&,NE*2(&P !>66# D

4<5>66J01(E*&.0)3.1F2*[ ?S5>66 D/0)U"1(3*G01(E*[*G"C&3="%.)0"&,%-)3J0,%2N1&.)0 !D65666# 6@>a,&.)0*R*G01(E*$*R*%1&*"%-F(2)2*"%*,GG0)G,&"1% 6@>e%(3)2*G01(E*[*&.0)3.1F2 !SS5>66# 6@>XN,FF*G"C&*)B)NE&"1%*%=,*"%*-,3)*1C*"%.)0"&,%-) 6 6@>K,B,OF)*;,F() SI5666

7$K*!??M# \5<D6 6@>E

Page 19

!"# $%&'%&"()%*+,"-+.%//+012)13 4"&5/$,+$%6'7("()%* 819:;< =1':;> 4"&:?@!"#$%&%'()*+,-./)##0 1234333 3 5343336)##%7$/+$* .18943330 3 .5343330 1

:94333 3 3

!"#$%; <:4333 1=4888 3 1>),"/%&?@)A$ 5B4333 1=4888 3!C"(D$"E/$%D"+?# 3 3 54533 1>),"/%F()*+,# 5B4333 1=4888 54533!>%F"G"E/$H!"#$%&%"?I%!J%K%1<L9M 945<9 3 2<9 3L9!"#$%;%K%<9M 54333 :4888 3 1L9!J%K%1<L9M 3 3 3N8B5O%P"/Q$%E"#+#%($/+$* .:49330 .:48880 3 1L9>),"/%!>%RQ$ =41<9 3 2<9

=7*&)/1+.)6)(1A+:+.%//+416% 3L9!"#$%&%/)##%83%N$',$AE$(%<31B 85343336)##%($/+$*%SD()##%E"#+#S%T%<312%T%@)(($#')?I+?D%"-@%'$(+)I .1234333%U%B-1<0 .18943330

<<943336)##%($/+$*%P"/Q$%E"#+#%T%<31B 1:4333%U%<9M%-%1<L9M .8:455=0

1B348886)##%($/+$*%P"/Q$%E"#+#%T%<312%T%@)(($#')?I+?D%"-@%'$(+)I .54333%U%B-1<%-%1<L9M0 .8543330

19:4888!"((G%*)(V"(I%"D"+?#,%!"#$%&%'()*+,%T%<3<3 .5343330O"/"?@$ B:4888

!"#$%;%6)##%81%W"(@C%<3<3 134333!"((G%E"@X%!"#$%;%/)##%@)(($#')?I+?D%"-@%'$(+)I .134333Y5-B0 .5455=0!"#$%;%/)##%@"((+$I%*)(V"(I%,)%81%W"(@C%<3<1 84888 B

!C# $,D$E,+F"&()9)'"()%*+G-16'()%* 4"&5/F"(,+@+'",+)?%ZU$A',+)?

1

1

1

1H

!9# $,+$2%/1+$%6'"*I+,1/(/ 4"&5/!)A'"?G%@)?,()//$I%EG%*+P$%)(%*$V%'"(,+@+'",)(#4%)(%,C$+(%"##)@+",$# <[7!)A'"?G%@)?,()//$I%EG%'"(,+@+'",)(#%VC)%"($%"/#)%I+($@,)(#%.($D"(I/$##%)*%,C$%?QAE$(0 <

H

!A# +J*9%61+,"-+(1&6)*"()%*+'"I61*(+ K 4"&5/N,",Q,)(G%'"GA$?, $U$A', 3L9ZUTD(",+"%'"GA$?, B34333\)/+I"G%'"G #@C%Z 3L9F"G%+?%/+$Q%)*%?),+@$ 54333 3L9!)A'"?G%@"( 194333 3L9

1114333ZU$A',+)?#]$"(#%)*%#$(P+@$H%B-<339%T%5-<3<3%̂ %1:%@)A'/$,$%G$"(#O"#+@ 134153%_%.=59%U%1:0 <342=3 3L9&?@($"#$I <342=3%_%134333%T%:34333 ?-" 3L9N!NO 1134333%U%1:-19%T%:34333 5<455= 1L9

>$(A+?",+)?%'"GA$?, 1114333ZU$A',+)? .5<455=0>"U"E/$%,$(A+?",+)?%'"GA$?, :24888 3L9

L

10%&?P$#,)(%E$?$*+@+"//G%$?,+,/$I%,)%"%A+?+AQA%C)/I+?D%9M%)*%,C$%)(I+?"(G%%#C"($%@"'+,"/4%9M%)*%,C$%'()*+,#%"P"+/"E/$%*)(%I+#,(+EQ,+)?%"?I%9M%)*%,C$%"##$,#%"P"+/"E/$%*)(%I+#,(+EQ,+)?%%)?%"%V+?I+?D%Q'%<0%&?P$#,)(%@)A'"?G%AQ#,%C"P$%,C$%A+?+AQA%C)/I+?D%+?%,C$%+?P$#,$$%*)(%"%@)?,+?Q)Q#%'$(+)I%)*%1<%%A)?,C#%+?%,C$%<%G$"(#%'(+)(%,)%I+#')#"/80%&?P$#,$$%AQ#,%E$%"%,("I+?D%@)A'"?G%)(%,C$%EQ#+?$##%)*%,V)%@)A'"?+$#%,"X$?%,)D$,C$(%AQ#,%@)?#+#,%)*%VC)//G%)(%A"+?/G%)*%@"((G+?D%)?%,("I$#:0%̀ ,%,C$%,+A$%)*%I+#')#"/4%,C$%+?P$#,$$%@)A'"?G%AQ#,%E$%($#+I$?,%+?%"%A$AE$(%#,",$%)*%,C$%Za%)(%"%@)Q?,(G%%V+,C%VC+@C%&($/"?I%C"#%"%,"U%,($",G

SOLUTION 5

SOLUTION 6

Page 20

!"#$%&'(")*$+,-./ 0"-1/!"#$%&&$'(%)*&'+$,'-./,'0

!"##$%&'(&)''*+&,-.$"*/+ 0123-+(/2&'(&'4-/2+5,#&'(&)''*+&6%&3)2//7/-1+3$/+&'(&7'8/36$/&)''*+&152'")5&3-&"-*,+.$'+/*&3)/-153-*,-)&'8/2&'(&)''*+&1531&32/&+"69/.1&1'&:;&3)2//7/-1.'7#"$+'2%&#"2.53+/&'2&$/)3$&+/,<"2/&'(&)''*+123-+(/2&'(&)''*+&(2'7&13=36$/&1'&/=/7#1&3.1,8,1%+/$(>+"##$,/+

!"##$%&'(&!/28,./&,-.$"*/+? @+"##$%&'(&(''*&3-*&*2,-A&('2&.'-+"7#1,'-&4,15'"1&("215/2/#3231,'-&2/B",2/*'#/231,'-&'(&3&.3-1//-&6%&3&6"+,-/+++"##$%&'(&+/28,./&6%&3-&"-*,+.$'+/*&3)/-1$/3+,-)&3-*&5,2,-)&'(&)''*+/$/.12'-,.3$$%&+"##$%&+/28,./+&>&*,),+1,+/*&)''*+&3-*&."+1'7,+/*&+'(1432/

2

!3#$45+$6"(67("8)9*$:$,&'("*"8)9*/$-,;7)-,<$89$3,$)*6(7<,< 0"-1/C"1#"1&DEF = =G2,+5&6"+,-/++&."+1'7/2+ 0HIII&&&&&&&& =&@0J KLI&&&&&&&&&&&& IMNG2,+5,831/&."+1'7/2+ OLHIII&&&&& =&@0J PH0QI&&&&&&&& IMN!#3-,+5,831/&."+1'7/2+&R6/$'4&*,+13-./&+/$$,-)&152/+5'$*S @HNII&&&&&&&& =&@0J NQN&&&&&&&&&&&& IMN!#3-,+5&6"+,-/++&."+1'7/2&RT@T&>&-'&G2,+5&DEFS @HIII&&&&&&&& =&IJ >&&&&&&&&&&&&&& IMNU!&6"+,-/++&."+1'7/2&RV=#'21H&</2'&231/*S KHIII&&&&&&&& =&IJ >&&&&&&&&&&&&&& IMNVU&#"2.53+/+ @LHIII&&&&& =&@0J KHKQI&&&&&&&& IMNGWE&(2'7&X/273-%&>&+/$(>3..'"-1&('2&G2,+5&DEF ONHIII&&&&& =&@0J 0HPNI&&&&&&&& IMN

ONHQNN&&&&&G-#"1&.2/*,1+G2,+5&#"2.53+/+&RYOZHIII&=&@0JS PHOPI&&&&&&&& IMNVU&#"2.53+/+&RY@LHIII&=&@0JS KHKQI&&&&&&&& IMNG7#'21+&(2'7&W5,-3&>&DEF,*&31&;CV&RYNKHIII&=&@0JS O@HZZI&&&&& IMN[3)/+&>&-'&DEF >&&&&&&&&&&&&&& IMNV$/.12,.,1%&RYOHKII&\&OO0MN&=&O0MNS OLI&&&&&&&&&&&& OF/$/#5'-/&RYKNI&\&O@0&=&@0S O@@&&&&&&&&&&&& IMNE..'"-13-.%&(//+&RYKHIII&=&@0JS OH0ZI&&&&&&&& IMNG-123&.'77"-,1%&3.B",+,1,'-+&(2'7&X/273-%&RYONHIII&=&@0JS 0HPNI&&&&&&&& IMN]/3+/%7/-1&'-&83-&>&#/2+'-3$&"+/&,22/$/83-1&RYZII&=&@0JS OZP&&&&&&&&&&&& IMN^,/+/$&RY0II&=&@0JS KL&&&&&&&&&&&&&&& IMNW32&2/#3,2+&>&#/2+'-3$&"+/&,22/$/83-1&&RY@HIII&=&O0MNJS @QI&&&&&&&&&&&& IMN;/12'$&('2&83-&R-'&,-#"1&.2/*,1&3$$'4/*S >&&&&&&&&&&&&&& @LH0NNSR&&&&& IMNDEF%36$/ O0HKII>&&&&&

>?

!6#$@"/A$B,6,)'8/$C"/)/ 0"-1/_3%&6/&"+/*&6%&123*/2+&,(?OS&31&$/3+1&LIJ&'(&15/&+"##$,/+&32/&1'&"-2/),+1/2/*&#/2+'-+ IMN'2&@S&15/&1"2-'8/2&,+&-'1&$,A/$%&1'&/=.//*&Y@7&,-&3&.'-1,-"'"+&O@&7'-15&#/2,'* IMN

E##$%&1'&F/*&]1*? @F"2-'8/2&('2&14'&7'-15&#/2,'*&̀ '8/76/2\^/./76/2&@I@I& Y0@HNIIV+1,731/*&1"2-'8/2&('2&.'-1,-"'"+&O@&7'-15&#/2,'* Y0LIHIIIG(&̀ '8/76/2\^/./76/2&2/#2/+/-1+&3-&38/23)/&+3$/+&#/2,'*H&1"2-'8/2&4,$$&6/&$/++&153-&Y@7F5/&6"+,-/++&.3-&15/2/('2/&3##$%&('2&3##2'83$&1'&"+/&15/&.3+5&2/./,#1+&63+,+&'(&3..'"-1,-)&('2&DEF

F4'&123-+3.1,'-+&1531&4,$$&6/&/=.$"*/*&(2'7&.3+5&2/./,#1+&63+,+?OS&123-+3.1,'-+&4,15&.'--/.1/*Ł,/+ O@S'#/21%&123-+3.1,'-+ O

2