Adjusting financial policy -...

23

Adjusting financial policy 16 September 2009 – Investor day – London & New York Aditya Mittal – Chief Financial Officer and member of GMB

Transcript of Adjusting financial policy -...

Adjusting financial policy

16 September 2009 – Investor day – London & New York

Aditya Mittal – Chief Financial Officer and member of GMB

1

Disclaimer

Forward-Looking Statements This document may contain forward-looking information and statements about

ArcelorMittal and its subsidiaries. These statements include financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and expectations with respect to future operations, products and services, and statements regarding future performance. Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,”“target” or similar expressions. Although ArcelorMittal’s management believes that the expectations reflected in such forward-looking statements are reasonable, investors and holders of ArcelorMittal’s securities are cautioned that forward-looking information and statements are subject to numerous risks and uncertainties, many of which are difficult to predict and generally beyond the control of ArcelorMittal, that could cause actual results and developments to differ materially and adversely from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include those discussed or identified in the filings with the Luxembourg Stock Market Authority for the Financial Markets (Commission de Surveillance du Secteur Financier) and the United States Securities and Exchange Commission (the “SEC”) made or to be made by ArcelorMittal, including ArcelorMittal’s Annual Report on Form 20-F for the year ended December 31, 2008 filed with the SEC. ArcelorMittal undertakes no obligation to publicly update its forward-looking statements, whether as a result of new information, future events, or otherwise.

2

Agenda

• Reaction to the financial crisis• Adjusting financial policy• What would profitability be post crisis?• Financing the post crisis growth

3

Reaction to the financial crisis

4

ArcelorMittal financial ratios pre-crisis

ArcelorMittal financial position pre-crisis

Net debt / EBITDA* Gearing

* Based on latest twelve months (LTM) EBITDA

0.0

0.5

1.0

1.5

2.0

2.5

3Q2006

4Q2006

1Q2007

2Q2007

3Q2007

4Q2007

1Q2008

2Q2008

3Q2008

Upper limit targets

Lower limit targets

30%

35%

40%

45%

50%

55%

3Q2006

4Q2006

1Q2007

2Q2007

3Q2007

4Q2007

1Q2008

2Q2008

3Q2008

5

Target of USD 10 billion of net debt reduction near ly achieved in 9 months

In addition to focus on cost reduction focus was put on debt reduction

Net debt and gearing Main initiatives

• Positive cash-flow from operations achieved throughout the crisis due to significant cash inflow from reduction in working capital (USD 5.5 billion over 9 months)

• 2009 CAPEX cut to USD 3 billion from the USD 9 billion initially planned

• Dividend cut to USD 0.75 per share from USD 1.50 (annual savings of USD 1.1 billion)

• USD 2.5 billion of cash gained from unwinding of raw material hedging transaction

• USD 1.4 billion of proceeds from asset disposals over 9 months

• Capital increase of USD 3.2 billion

20

25

30

35

3Q 2008 4Q 2008 1Q 2009 2Q 2009

30%

35%

40%

45%

50%

55%

Net Debt in billion of USD(LHS) Gearing (RHS)

USD 10 billion target reduction

6

In 9 months of financial crisis, liquidity has been improved by more than USD 10 billion

An improved liquidity

Liquidity (USD billion) Cash & Cash equivalent in % of liquidity

0

5

10

15

20

25

3Q 2008 4Q 2008 1Q 2009 2Q 2009

Cash & Equivalent Unused credit line

1213.4

11.6

22.7

20%

30%

40%

50%

60%

3Q 2008 4Q 2008 1Q 2009 2Q 2009

7

Approximately USD 11.4 billion of equity, convertibl e and bond financings successfully issued

Successful refinancing

Bank debt75%

Bonds15%

Commercial paper10%

Bank debt49%

Convertibles bonds

6%

Bonds38%

Commercial paper

7%

Gross debt structure

At 30/09/08 At 30/06/09

Main initiatives

• USD 6.0 billion of bank refinancing secured through Forward Start facilities in February and March 2009

• USD 1.6 billion (EUR 1.25 billion) of convertible bonds issued on April 1, 2009

• USD 3.2 billion of capital increase through an accelerated book building on May 6, 2009

• USD 0.8 billion of additional convertible bond issued on May 6, 2009

• USD 2.25 billion of bonds issued on May 20, 2009

• USD 3.5 billion (EUR 2.5 billion) of bonds issued on June 3, 2009New covenants for main bank facilities

� Amendment to the Net Debt / EBITDA covenant to 4.5x for December 2009, 4.0x for June 2010 and reverting to 3.5x for December 2010

8

Average debt maturity profile extended to 3.8 years

A longer maturity profile

Liquidity and debt profile at 30/09/08 Liquidity and debt profile at 30/06/09

*

* Pro forma liquidity includes cancellation of USD 3.2 billion of credit facilities and prepayment of USD 3.4 billion of bank debt

0

10

20

30

40

50

Q4 2008 2009 2010 2011 2012 2013 Thereafter

Cumulative gross debt repayment

Liquidity

0

10

20

30

40

50

H2 2009 2010 2011 2012 2013 2014 Thereafter

Cumulative gross debt repayment

Liquidity

9

Adjusting financial policy

10

ArcelorMittal profitability has shown resilience to economic slowdown and inventory downturn but not to major economic crisis

What we learned from the crisis

0

2

4

6

8

10

1Q 2

0062Q

2006

3Q 2

0064Q

2006

1Q 2

0072Q

2007

3Q 2

0074Q

2007

1Q 2

0082Q

2008

3Q 2

0084Q

2008

1Q 2

0092Q

2009

40

60

80

100

120

140

160

180

200

EBITDA in billion of USD (LHS) Steel turnover in base 100 (RHS)

0

5

10

15

20

25

30

2004 2005 2006 2007 2008

ArcelorMittal EBITDA* and steel price

*Pro-forma in 2004, 2005 and 2006 in billion of USD

HRC FOB US Midwest USD/t

ArcelorMittal EBITDA* and turnover

11

Target of a Net Debt / Average EBITDA to be betwee n 0.5x and 1.8x

Setting a leverage target based on an average profitability

Net Debt / average EBITDA** depending cost of financing and interest coverage

Net debt / EBITDA*

* Based on latest twelve months (LTM) EBITDA** Based on average EBITDA since 2004 and including 2009 (based on Bloomberg consensus)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

6% 7% 8% 9% 10% 11% 12% 13%

Cost of financing

Net

deb

t /

Ave

rage

EB

ITD

A

Upper limit target

Lower limit target

Interest coverage

of 10x

Interest coverage of

15x

0.0

0.5

1.0

1.5

2.0

2.5

3Q 2

0064Q

2006

1Q 2

0072Q

2007

3Q 2

0074Q

2007

1Q 2

0082Q

2008

3Q 2

0084Q

2008

1Q 2

0092Q

2009

"Old" Upper limit targets

"Old" Lower limit targets

12

Gearing target of 25% to 40% in order to reduce equ ity volatility during crisis

Source Credit Suisse

Historical price to book value of the steel sector

Improve investment selectivity due to capital const rain

� Historical price to book of 0.75x during trough

Setting a new gearing target based on stock market trough

Gearing target for market capitalisation in trough to remain close to 2 times net debt

0%

10%

20%

30%

40%

50%

60%

70%

80%

1.0 1.5 2.0 2.5 3.0 3.5

Market capitalisation over net debt

Gea

ring

Gearing range

13

Committed to solid investment grade

Adjusted financial policy and new targets

Net debt over average EBITDA* Gearing

� Net Debt / average EBITDA between 0.5x and 1.8x � Gearing to be between 25% and 40%

* Based on average EBITDA since 2004 and including 2009 (based on Bloomberg consensus)

0.0

0.5

1.0

1.5

2.0

3Q2006

4Q2006

1Q2007

2Q2007

3Q2007

4Q2007

1Q2008

2Q2008

3Q2008

4Q2008

1Q2009

2Q2009

Target range

20%

25%

30%

35%

40%

45%

50%

55%

3Q2006

4Q2006

1Q2007

2Q2007

3Q2007

4Q2007

1Q2008

2Q2008

3Q2008

4Q2008

1Q2009

2Q2009

Target range

14

What would profitability be post crisis?

15

Despite the exceptional crisis steel industry funda mentals (growth, consolidation…) remain

Should we expect profitability to recover to previous levels?

Source WSA and ArcelorMittal estimates

ArcelorMittal shipments and EBITDA margin Global steel demand expectation (Mt)

600

800

1000

1200

1400

1600

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

E20

10E

2011

E20

12E

2013

E

The financial crisis

40

60

80

100

120

140

1Q 2

0062Q

2006

3Q 2

0064Q

2006

1Q 2

0072Q

2007

3Q 2

0074Q

2007

1Q 2

0082Q

2008

3Q 2

0084Q

2008

1Q 2

0092Q

2009

5%

10%

15%

20%

25%

30%

Shipments in base 100 (LHS) EBITDA Margin in % (RHS)

16

Historical average and peak/trough of EBITDA per to nne of around 150 USD/t

Historical profitability level

ArcelorMittal annual EBITDA per tonne ArcelorMittal peak and trough EBITDA per tonne

Annual Quarterly

*Analyst consensusSource Bloomberg

0

100

200

300

400

3Q 2008 1Q 2009

0

100

200

300

400

2008 2009E*0

10

20

30

2004 2005 2006 2007 2008 2009E*

0

100

200

300

400

EBITDA in USD billion (LHS) EBITDA in USD/t (RHS)

17

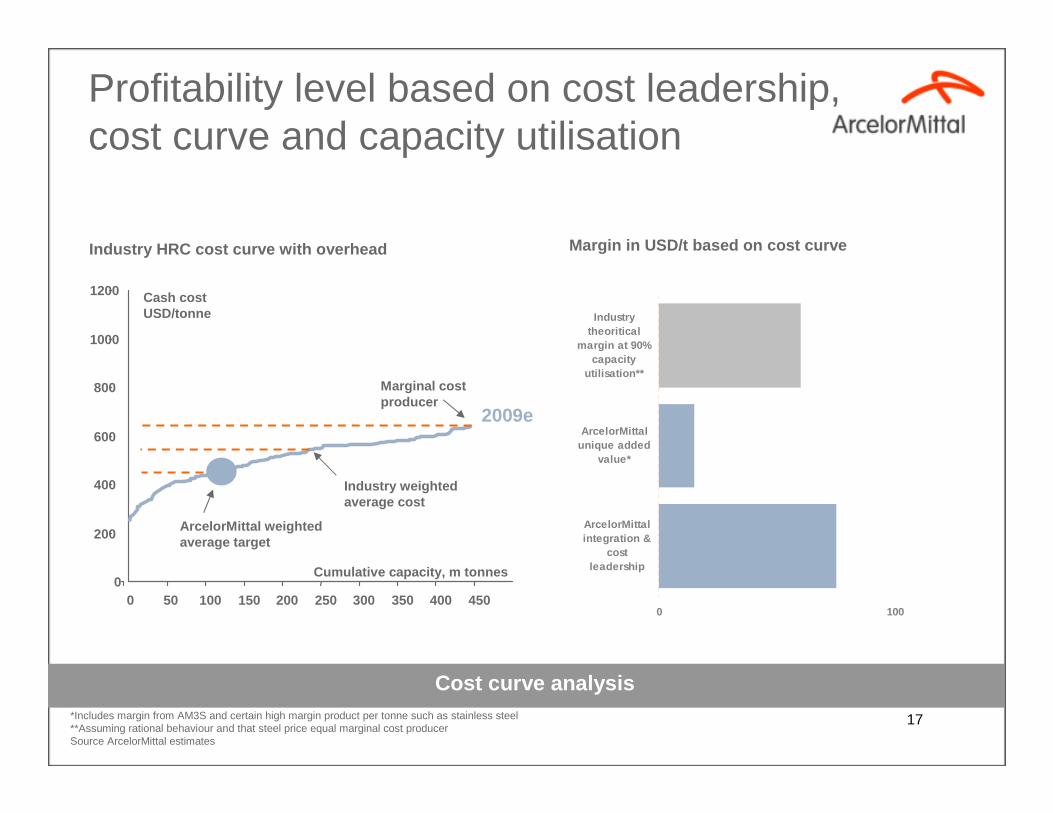

Profitability level based on cost leadership, cost curve and capacity utilisation

*Includes margin from AM3S and certain high margin product per tonne such as stainless steel**Assuming rational behaviour and that steel price equal marginal cost producerSource ArcelorMittal estimates

Margin in USD/t based on cost curveIndustry HRC cost curve with overhead

Cumulative capacity, m tonnes

Cash cost USD/tonne

0

200

400

600

800

1000

1200

0 50 100 150 200 250 300 350 400 450

2009e

ArcelorMittal weighted average target

Industry weighted average cost

Cost curve analysis

Marginal cost producer

0 100

ArcelorMittalintegration &

costleadership

ArcelorMittalunique added

value*

Industrytheoritical

margin at 90%capacity

utilisation**

18

Financing the post crisis growth

19

Over the last 3 years, ArcelorMittal has generated more than USD 38 billion of cash-flow from operation

Financing growth through cash-flow from operations

Cash-flow from operations (in billion USD)

0

1

2

3

4

5

6

7

1Q2006

2Q2006

3Q2006

4Q2006

1Q2007

2Q2007

3Q2007

4Q2007

1Q2008

2Q2008

3Q2008

4Q2008

1Q2009

2Q2009

USD 0.1bn

Net Debt increase since merger**

USD 22.2bn

M&A* since merger

USD 15.1bn

* Cash purchase price, assumed net debt and shares issued bought back** Since 30/06/06 to 31/12/08

CAPEX since merger

20

Growth CAPEX focus on key emerging markets such as South Americaand India, and Mining expansion

Growth CAPEX to be reinitiated cautiously

CAPEX plan pre-crisis (USD billion) New CAPEX plan (USD billion)

0

2

4

6

8

10

2005 2006 2007 2008 2009E

Grow th CAPEX planned pre-crisis

Grow th CAPEX realised

Maintenance CAPEX

0

2

4

6

8

10

2006 2007 2008 2009E 2010E

Grow th CAPEX planned

Grow th CAPEX realised

Maintenance CAPEX

Aceralia / Arbed / Usinor

Equity100%

21

ArcelorMittal to continue to create value through M& A leveraging leadership and integration know-how to deliver synergies

Targeted M&A opportunities to be re-examined

Financing of major historic Merger & Acquisition

Mittal Steel / ISG

Cash50% Equity

50%

Mittal Steel / Arcelor

Cash31%

Equity69%

ArcelorMittal / Arcelor Brasil

Cash31%

Equity69%

22

Q&A