Adhi Satriya, PT Andritz Hydro, 2014 ASEAN-OECD Investment Policy Conference

22

www.andritz.com Combined REBID, Cluster Development & GVC Strategy Total Solution for Renewables in SEA Integrating ASEAN Firms into Global Value Chains Session during the 2 nd ASEAN-OECD Investment Policy Conference, Jakarta, Indonesia, 10-11 December 2014 By Ir. Adhi Satriya M.Sc.

-

Upload

oecd-directorate-for-financial-and-enterprise-affairs -

Category

Documents

-

view

177 -

download

2

description

This presentation by Adhi Satriya was made at the session "Integrating ASEAN firms into global value chains through investment" during the 2nd ASEAN-OECD Investment Policy Conference held on 10-11 December 2014. Find out more at: http://www.oecd.org/daf/inv/investment-policy/2014-asean-oecd-investment-policy-conference.htm

Transcript of Adhi Satriya, PT Andritz Hydro, 2014 ASEAN-OECD Investment Policy Conference

www.andritz.com

Combined REBID, Cluster Development & GVC Strategy

Total Solution for Renewables in SEA

Integrating ASEAN Firms into Global Value Chains Session during the 2nd ASEAN-OECD

Investment Policy Conference, Jakarta, Indonesia, 10-11 December 2014

By Ir. Adhi Satriya M.Sc.

2 www.andritz.com

Overview

KEY CHALLENGES

CLUSTER DEVELOPMENT

GLOBAL VALUE CHAINS

REBID STRATEGY

3

Renewables awareness and cost-benefits analysis minded approach

Non-harmonized legal landscape

Renewables long development lead time

Over population and difficulty of resettlement

Remote location and poor access infrastructure

Lack of local technical expertise

www.andritz.com

SEA Key Challenges

4

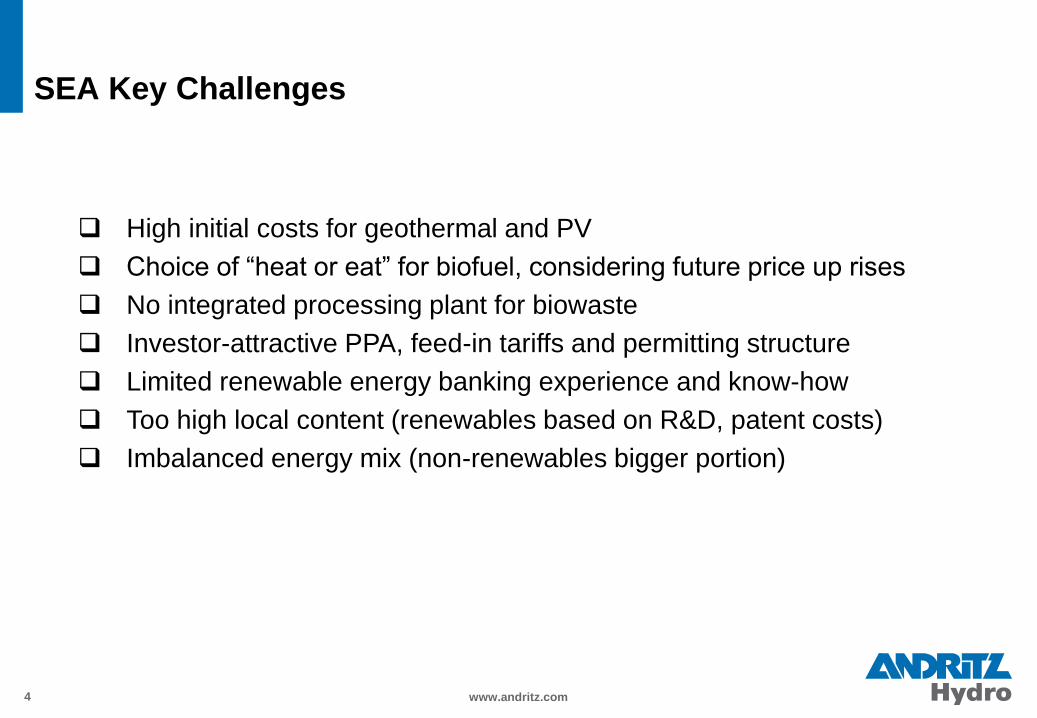

High initial costs for geothermal and PV

Choice of “heat or eat” for biofuel, considering future price up rises

No integrated processing plant for biowaste

Investor-attractive PPA, feed-in tariffs and permitting structure

Limited renewable energy banking experience and know-how

Too high local content (renewables based on R&D, patent costs)

Imbalanced energy mix (non-renewables bigger portion)

www.andritz.com

SEA Key Challenges

www.andritz.com5 www.andritz.com

Hydro Energy & Marine Energy

The Future Backbone of SEA & Pacific Renewables Sector

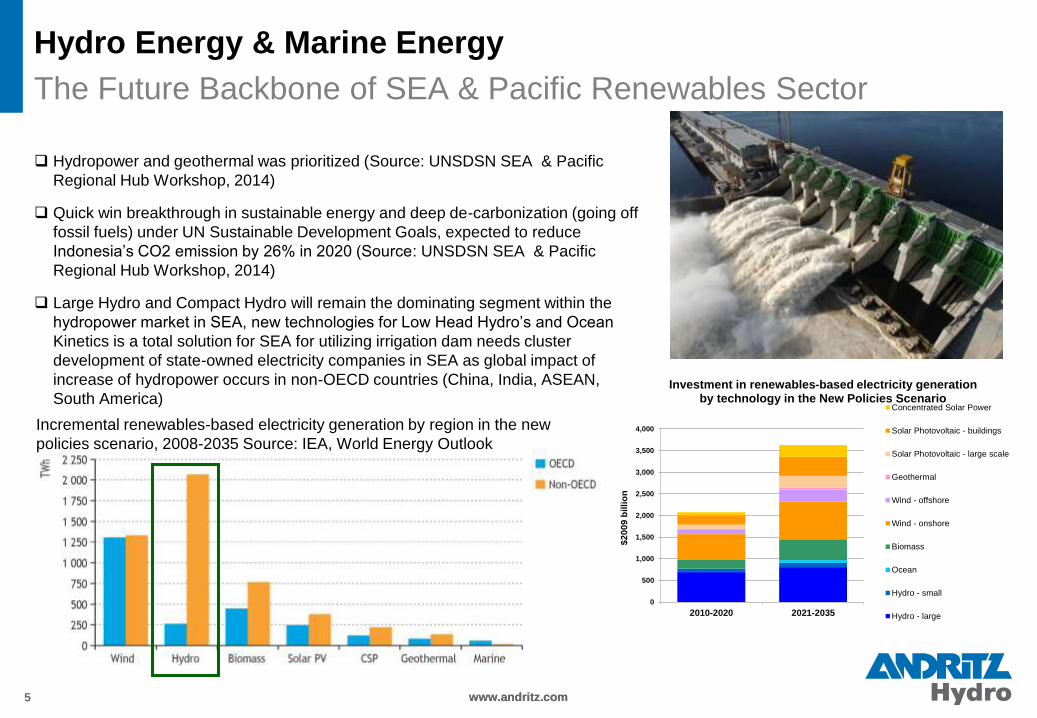

Hydropower and geothermal was prioritized (Source: UNSDSN SEA & Pacific

Regional Hub Workshop, 2014)

Quick win breakthrough in sustainable energy and deep de-carbonization (going off

fossil fuels) under UN Sustainable Development Goals, expected to reduce

Indonesia’s CO2 emission by 26% in 2020 (Source: UNSDSN SEA & Pacific

Regional Hub Workshop, 2014)

Large Hydro and Compact Hydro will remain the dominating segment within the

hydropower market in SEA, new technologies for Low Head Hydro’s and Ocean

Kinetics is a total solution for SEA for utilizing irrigation dam needs cluster

development of state-owned electricity companies in SEA as global impact of

increase of hydropower occurs in non-OECD countries (China, India, ASEAN,

South America)

Incremental renewables-based electricity generation by region in the new

policies scenario, 2008-2035 Source: IEA, World Energy Outlook

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2010-2020 2021-2035

$2

00

9 b

illi

on

Investment in renewables-based electricity generation by technology in the New Policies Scenario

Concentrated Solar Power

Solar Photovoltaic - buildings

Solar Photovoltaic - large scale

Geothermal

Wind - offshore

Wind - onshore

Biomass

Ocean

Hydro - small

Hydro - large

6 www.andritz.com

Overview

KEY CHALLENGES

CLUSTER DEVELOPMENT

GLOBAL VALUE CHAINS

REBID STRATEGY

7

Cluster: grouping among small and medium enterprises (SME)

belonging to the same value chain (electricity) and same area (SEA)

linked by relations of cooperation (network, consortiums)

supported by partnership with regional public research institutions

to implement collective projects aiming at developing SEA common

competitiveness

Cluster needs:

elaborating strategy: diagnosis/identification of common challenges,

vision, action plan

management of collective quick win projects, structuring collective

projects with external alliances

Mobilization of research and innovation among SMEs

www.andritz.com

SEA Cluster Development

8

Objectives:

technology upgradation

quality and productivity improvement

database development

networking and formation of consortium

marketability improvement

www.andritz.com

SEA Cluster Collective Projects

for Development of Minor E/M Equipment

9

Strategy 1:

collective diagnosis: SWOT analysis for the different interest

composing the clusters

identification of common problems and challenges

collective vision: to be a global player under cluster strategy and

under consensual projection in the future

selection of goals and collective means to reach

regularly revised and actualized process according to cluster’s

growth in scope and vision

short term, medium term and long term action plan

www.andritz.com

SEA Cluster Development

10

Strategy 2:

integrated perspective

different themes as per need of the cluster

adoption and promotion of energy efficiency and clean

technologies strengthening policy and institutional structure

supporting capacity building

establish several key clusters and its experiences to be

disseminated to other clusters

e-Management of information

www.andritz.com

SEA Collective Projects

for Development of Minor E/M Equipment

11

Assessment of joint implementing collective projects and pilot projects:

common impact, monitoring, economic intelligence, search for value

chain strategy and search for new competitive advantages

Collective short term pilot projects, with the following impact:

New markets

New know how

Scale economies

Productive cooperation

Medium and long term structuring projects, with the following impact:

From global export-orientation to ASEAN Economic Community’s

trade-in value-added

Increased responsible business conduct in global value chains

(GVC)

Research innovation

Breakthrough for provision of infrastructure

www.andritz.com

SEA Cluster Development

12

Activities:

diagnostic study

awareness seminars

developing resource person

enterprises upgradation programs

technological workshop

individual counselling

minor equipment manufacturing and outsourcing of small and fast-

moving expendable parts

www.andritz.com

SEA Collective Projects

for Development of Minor E/M Equipment

13 www.andritz.com

Overview

KEY CHALLENGES

CLUSTER DEVELOPMENT

GLOBAL VALUE CHAINS

REBID STRATEGY

14

GVC is a full range of coordination of activities across geographies that

are required to bring a product from its conception, through design,

sourced raw materials and intermediate inputs, marketing, distribution

and support to end consumers

GVC is basically a production sharing in which different stages of

production process are located across different countries in which

companies:

structure

optimize

their operations internationally through outsourcing and offshoring of

activities is designed

GVC considering the value added by each country in the production of

goods and services wherever the necessary skills and materials are

available at competitive cost and quality

www.andritz.com

SEA GVC (Global Value Chains) Development

15

Andritz has done GVC in Indonesia since years ago by dividing the

offshore supply and services of major components (from Austria and

India) and onshore services (Indonesia, for automation and installation

services)

As a result of leveraging geographic separation of product design and

manufacturing, Andritz hires 24,126 workers worldwide as of June

2014, while its foreign subcontractors, local manufactures employs

more

www.andritz.com

SEA GVC (Global Value Chains) Development

16

Opportunity offered by Andritz’s GVC:

Enables SEA companies to perform some tasks in low added value

services

Accessing global distribution network and markets

Taking advantages of technology innovations

Enjoying global markets due to innovations of developed countries

such as OECD

Benefiting brand images of Andritz

Reducing information costs of reverse engineering and catching up

Plugging into GVC is accelerated way to become industrialized

countries

www.andritz.com

SEA GVC (Global Value Chain) Development

17 www.andritz.com

Overview

KEY CHALLENGES

CLUSTER DEVELOPMENT

GLOBAL VALUE CHAINS

REBID STRATEGY

2 Approaches for Harnessing Renewables

(way forward)

www.andritz.com

Hydro Power Potential

Development Strategy

(RUKN) ͣ

Demand Driven

DevelopmentDemand Creation

Development

Electricity Power

Development Plan by

PLN (RUPTL) b

Hydro Power Developed

4,284 MW

Renewable Energy Based

Industrial Development

(REBID)

Hydro Power Potential

70,692 MW

Future Direction of Hydro Power

Development in Indonesia(a) RUKN : National Electric Power Development Plan

(b) RUPTL : Electricity Planning by National Electricity

Company (PLN)

Sample: Indonesia situation

Combined REBID Cluster GVC Approach

www.andritz.com

Characteristics:

Bottom-up paradigm (interested investors come with integrated package with

end-user industries)

Isolated system

Based on supply (electricity creates its own demand for surrounding industry)

Based on private needs

Government role and presence as regulator (now still inexistence)

Consider environmental and spatial zoning (now still inexistence)

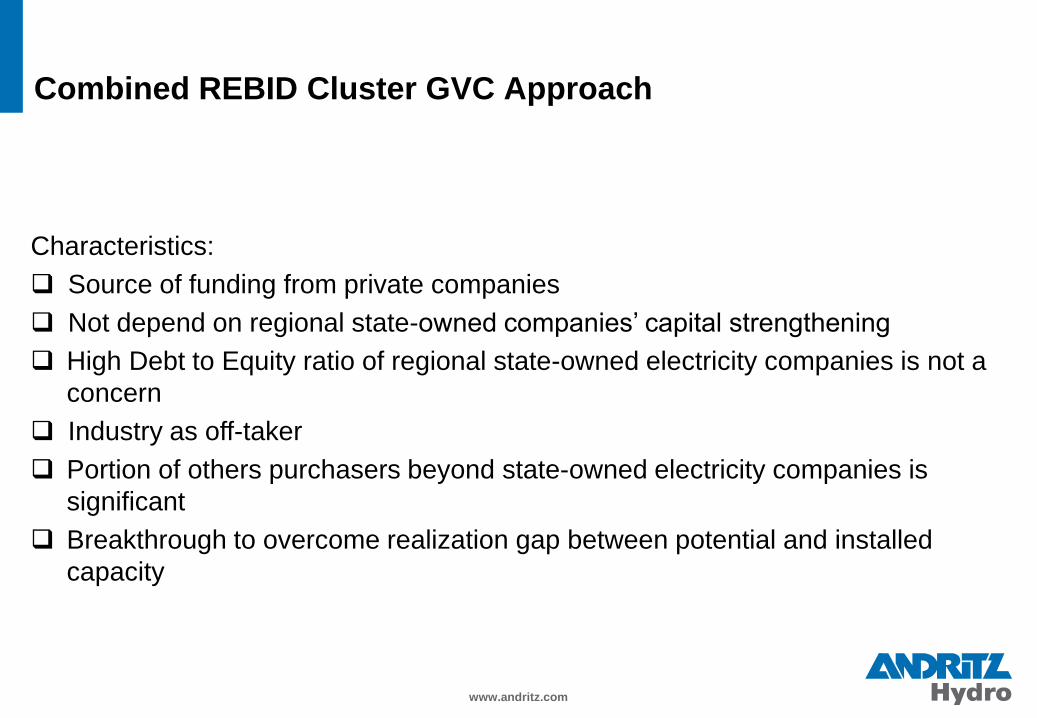

Combined REBID Cluster GVC Approach

www.andritz.com

Characteristics:

Source of funding from private companies

Not depend on regional state-owned companies’ capital strengthening

High Debt to Equity ratio of regional state-owned electricity companies is not a

concern

Industry as off-taker

Portion of others purchasers beyond state-owned electricity companies is

significant

Breakthrough to overcome realization gap between potential and installed

capacity

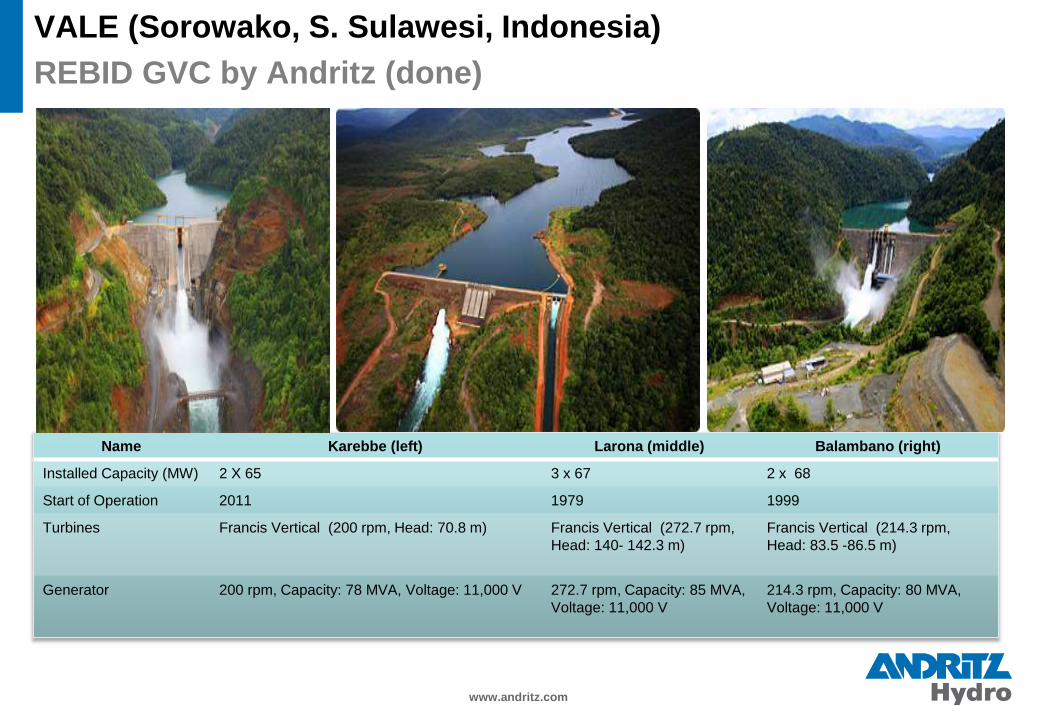

VALE (Sorowako, S. Sulawesi, Indonesia)

REBID GVC by Andritz (done)

www.andritz.com

Name Karebbe (left) Larona (middle) Balambano (right)

Installed Capacity (MW) 2 X 65 3 x 67 2 x 68

Start of Operation 2011 1979 1999

Turbines Francis Vertical (200 rpm, Head: 70.8 m) Francis Vertical (272.7 rpm,

Head: 140- 142.3 m)

Francis Vertical (214.3 rpm,

Head: 83.5 -86.5 m)

Generator 200 rpm, Capacity: 78 MVA, Voltage: 11,000 V 272.7 rpm, Capacity: 85 MVA,

Voltage: 11,000 V

214.3 rpm, Capacity: 80 MVA,

Voltage: 11,000 V

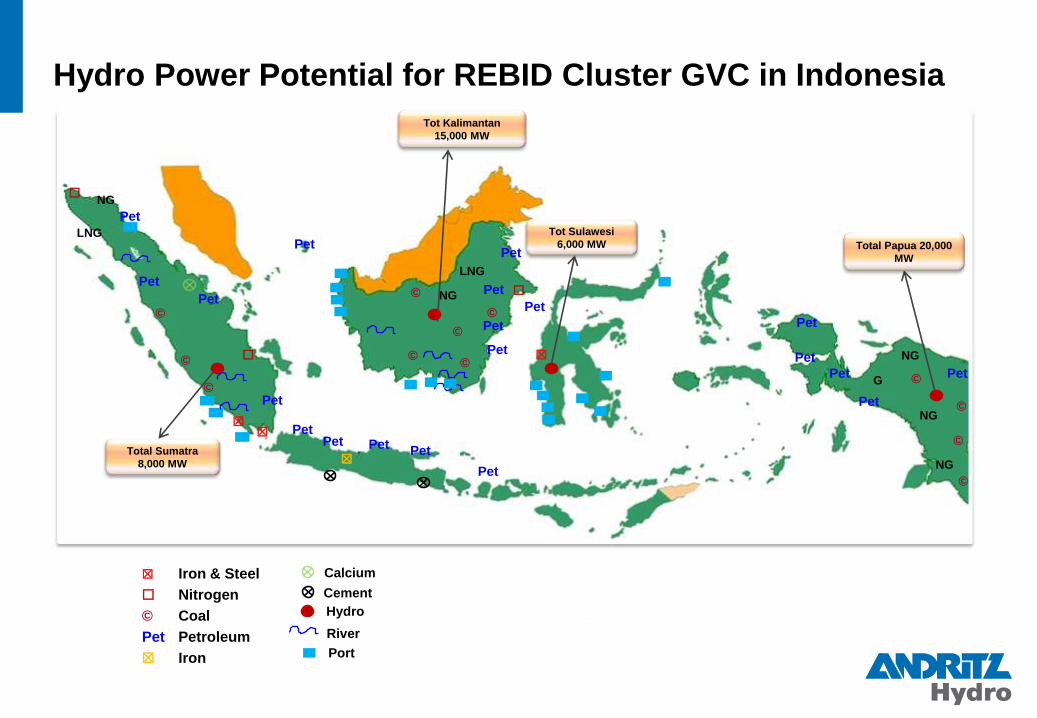

Planned Hydro

☐

☒ Iron & Steel

☐ Nitrogen

© Coal

Pet Petroleum

☒ Iron

☒

☒☒

☐

☐

©

©

©

Calcium

Cement

Pet

Pet

Pet

Pet

PetPet Pet

Pet

Pet

Pet

Pet

Pet

Pet

Pet

☒

©

©

©©

©

LNG

LNGPet

Pet

Pet

NG

NG

NG

NG

NG

Pet

Pet Pet©

©

©

©

G

Total Sumatra

8,000 MW

Tot Kalimantan

15,000 MW

Tot Sulawesi

6,000 MW

Hydro

Port

River

Total Papua 20,000

MW

Hydro Power Potential for REBID Cluster GVC in Indonesia