Policies on Health Care for Undocumented Migrants in EU27 ...

Upload

nguyenliemCategory

view

212download

0

Addressing the future of the aluminium industry in Europe

"Industrial change to build sustainable EIIs facing the resource efficiency

objective of the Europe 2020 strategy"

6 July 2011

2

Outline

• The aluminium industry in Europe

• Key competitiveness challenges

• The energy and resource conservation challenge

• Conclusions

3

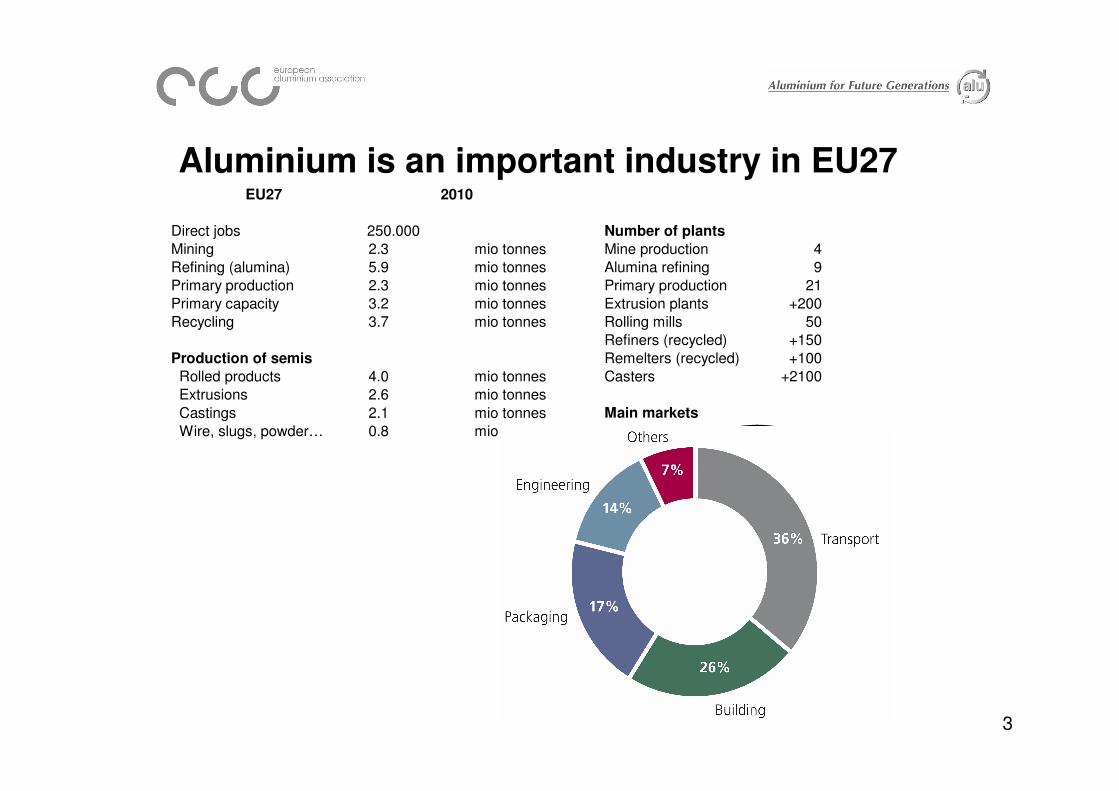

Aluminium is an important industry in EU27EU27 2010

Direct jobs 250.000 Number of plants

Mining 2.3 mio tonnes Mine production 4

Refining (alumina) 5.9 mio tonnes Alumina refining 9

Primary production 2.3 mio tonnes Primary production 21

Primary capacity 3.2 mio tonnes Extrusion plants +200

Recycling 3.7 mio tonnes Rolling mills 50

Refiners (recycled) +150

Production of semis Remelters (recycled) +100

Rolled products 4.0 mio tonnes Casters +2100

Extrusions 2.6 mio tonnes

Castings 2.1 mio tonnes Main markets

Wire, slugs, powder… 0.8 mio tonnesOthers

7%

Engineering

14%

Packaging

17%

Building

26%

Transport

36%

4

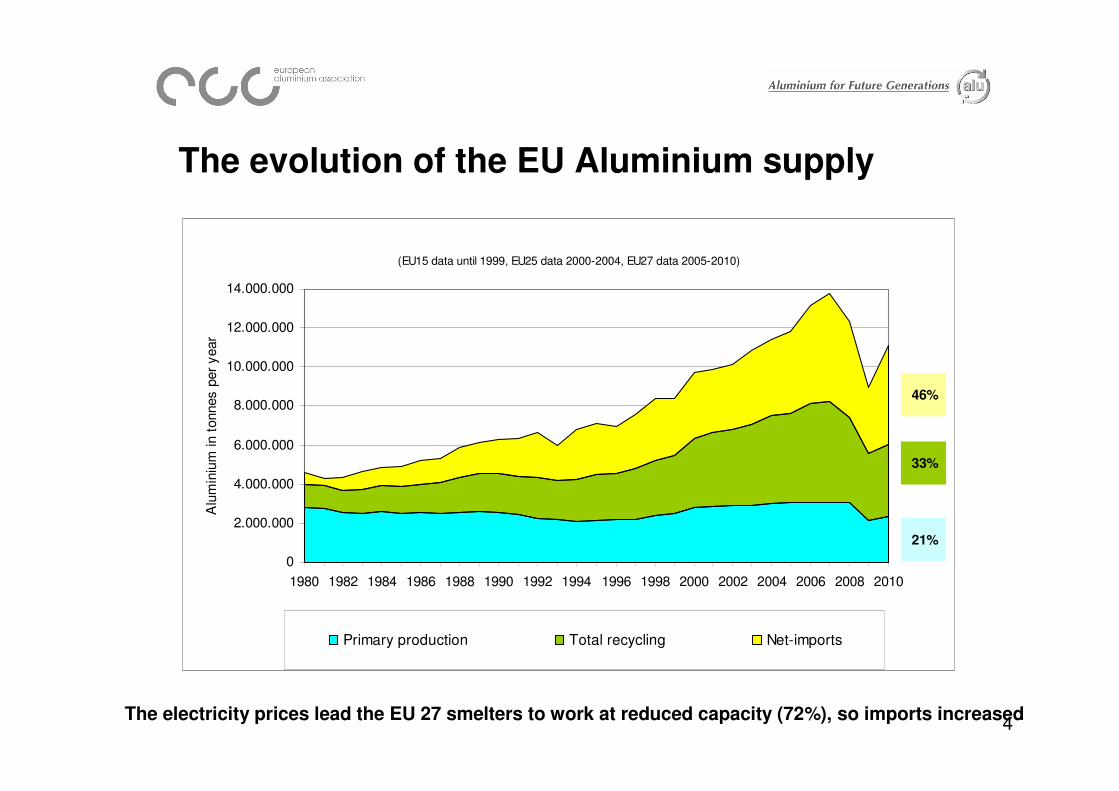

The evolution of the EU Aluminium supply

The electricity prices lead the EU 27 smelters to work at reduced capacity (72%), so imports increased

(EU15 data until 1999, EU25 data 2000-2004, EU27 data 2005-2010)

0

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

14.000.000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Alu

min

ium

in t

onnes p

er

year

Primary production Total recycling Net-imports

33%

21%

46%

5

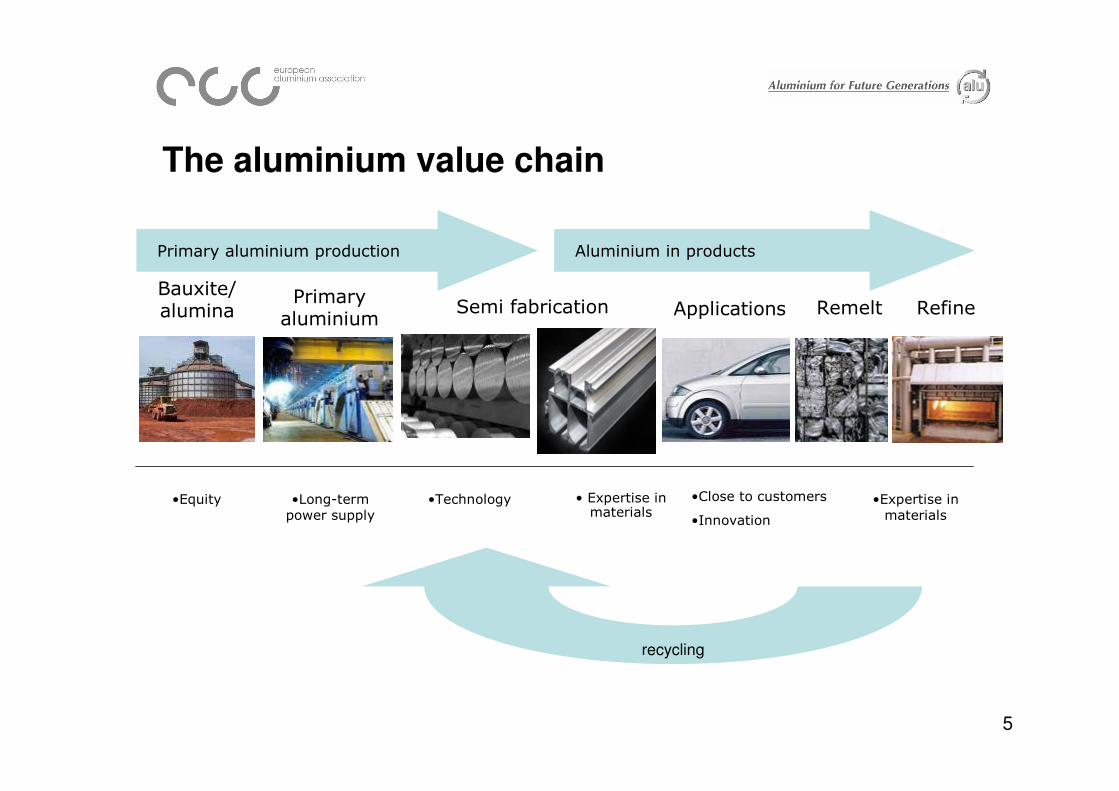

The aluminium value chain

Bauxite/alumina

Primary aluminium

Semi fabrication Remelt

Aluminium in productsPrimary aluminium production

•Equity •Long-term power supply

•Technology • Expertise in materials

•Close to customers

•Innovation

•Expertise in materials

RefineApplications

recycling

6

A strategic material all along its value chain

• Close interlinks all along the value chain.

• Loss of primary aluminium know-how/production would damage the whole supply chain, including design, innovation and end-use.

• SME’s active from innovation to recycling need the proximity of primary metal production for the right alloy and tailor-made shapes.

• Reliance on imported metal against SMEs interest.

• EU needs to retain existing primary aluminium production and to recreate conditions to build new ones.

7

Aluminium saves energy, reduces emissions & is safe

Key challenge:

Current regulation on cars and on vans both discourage the most straightforward emission reduction measure, which is light weighting.

Transport represents 25% of European emissions and the energy required to move a vehicle is proportional to its mass

1 kg of aluminium in a road vehicle = -20kg of CO2In average, a European car contains 140kg of aluminium

Aluminium has been used in 9 million crash management systems (CMS) produced in Europe in 2008.

8

Towards sustainable buildings

40% of global energy is used in buildings and construction. Demolition represent 25% of EU wasteflow

Key challenge:

European criteria for sustainable buildings should include end-of-life recycling (EoL) in the environmental assessment in order to promote recyclable materials.

Intelligent buildings incorporating aluminium

systems can decrease energy consumption by up to 50%

During demolition, 96% of aluminium is collected

and recycled

9

Collection, Sorting & Recycling of Packaging makes sense!

Level playing field betweenthe various materials andpackaging solutions in aproperly functioninginternal market isessential.

Some local authoritiesfavour specific options(e.g. reuse over recycling)without a properenvironmental assesmentor taxation measures thatmay lead to market distortion.

Key challenge:

Promote cost-efficient non-discriminating systems not favouring one type of

material and/or packaging over another. This can be either incentive-based (deposits, scrap value) or via separate collection systems.

The amount of aluminium packaging effectivelyrecycled greatly depends on the efficiency of the collection schemes with huge discrepancies within the EU.

10

Aluminium: 100% recyclable for ever

• In Europe aluminium enjoys high recycling rates, ranging from 63 % in beverage cans to more than 95% in building, construction, automotive and transportation.

• Aluminium has unique recycling qualities: the quality of aluminium is not impaired by recycling - it can be repeatedly recycled.

• Aluminium recycling saves energy: recycled aluminium saves up to 95% of the energy needed to produce the primary product.

• Aluminium recycling is economical: it uses less energy and recycling is self-supporting because of the high value of used aluminium.

Key competitiveness challenges

12

Endangered Primary Smelters (EU+EFTA)

Blue: mainly due to the existence of Long Term Contracts

Already closed

Severe threat

No immediate

threat

Under threat

Not members

13

Key competitiveness challenges

• Aluminium market is a worldwide commodity and the European industry has to compete in this global market.

• All aluminium related prices are linked to the London Metal Exchange (LME).

• Regionally imposed costs, such as those arising from the EU unilateral environmental targets cannot be passed on consumers.

• Aluminium production requires long-term energy contracts/supply which are the norm worldwide.

• Without competitive and predictable energy prices there will be no new investments in aluminium smelting in the EU.

14

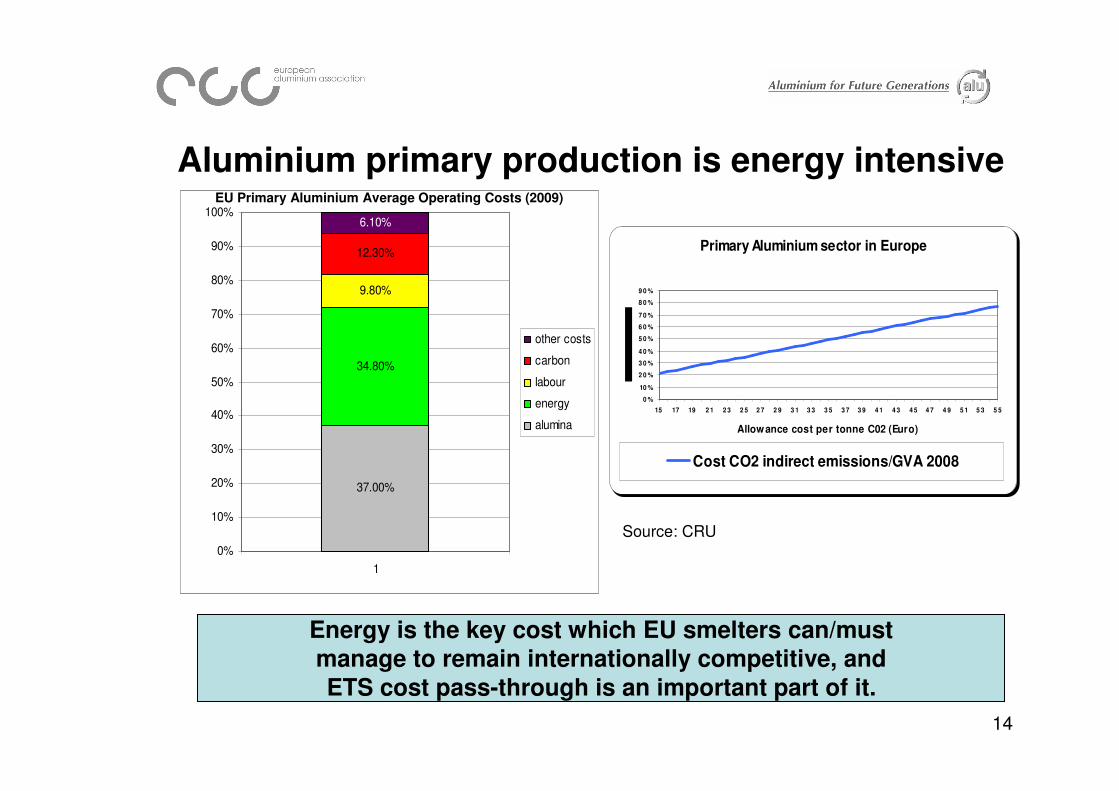

Aluminium primary production is energy intensive

Source: CRU

37.00%

34.80%

9.80%

12.30%

6.10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1

other costs

carbon

labour

energy

alumina

Energy is the key cost which EU smelters can/mustmanage to remain internationally competitive, and

ETS cost pass-through is an important part of it.

Primary Aluminium sector in Europe

0 %

10 %

2 0 %

3 0 %

4 0 %

5 0 %

6 0 %

7 0 %

8 0 %

9 0 %

15 17 19 2 1 2 3 2 5 2 7 2 9 3 1 3 3 3 5 3 7 3 9 4 1 4 3 4 5 4 7 4 9 5 1 5 3 5 5

Allowance cost per tonne C02 (Euro)

Cost CO2 indirect emissions/GVA 2008

EU Primary Aluminium Average Operating Costs (2009)

The energy and resource conservation challenge

16

Major achievements of the EU industry

• The level of use of electrical energy for primary production is close to

the achievable limit of the current technology

• However 48% of the electrical energy needed to produce primary

aluminium comes from renewable sources

• Emissions of CO2eq per tonne of primary aluminium were reduced almost 50% since 1997, with PFCs emissions reduced by 90% since

1990 (Source: EAA SDI report 2010)

• Emissions of CO2eq per tonne of recycled aluminium were reduced

over 50% since 1997 through combustion improvements

• Benefits in the use phase:

- Over 6% of avoided CO2 emissions in cars

- Prevention of the spoilage of food, whose CO2 content is very high

- Indirect benefits of the energy efficiency in buildings

17

EU used to be a net scrap importer…and now?

-1.000.000

-800.000

-600.000

-400.000

-200.000

0

200.000

400.000

balance 108.000 54.000 50.000 -31.000 -34.000 32.000 52.000 154.000 276.000 139.507 39.967 -104.10 -117.56 -148.24 -434.63 -287.21 -690.15 -695.33 -865.02 -724.18

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2001 2002 2003 2004 2005 2006 2007 2008 2009est.

2010

EU scrap balance in EU (net imports/exports)

18

Aluminium scrap is energy containing material

• Recycling aluminium is one of the less energy consuming recycling processes.

• Aluminium scrap can be considered as an energy saver.

• Europe’s mature and increasingly green economy is the largest aluminium scrap generator in the World.

• Europe, by tradition aluminium scrap importer, has become in a decade a substantial net scrap exporter.

• Emerging economies, short of energy production (i.e.: China), are very interested by European scrap.

• Countries like Russia have raised 50% aluminium scrap export duties, and Ukraine a total export ban.

Conclusions

20

Conclusions

• Support our industry’s assets towards resource efficiency:

- Stop lightweighting discrimination in transport/environmental policy

- Promote the appropriate recycling approach

- Promote non-discriminating recycling systems

• Grant immediate access to real (i.e.: full) CO2 cost pass

through compensation

• Facilitate negotiation of long term contracts for our sector

• We need a level playing field for the scrap and recycling in

order to keep a chance to lower our energy needs by using

the aluminium scrap generated in Europe by ourselves.

�Failure to provide the right operating conditions will lead to the closure of this vital industry in Europe

Thank you for your attention