Acquisition of Lafarge´s assets in Honduras500 2,600 2,700 2,800 2,900 3,000 ... Cement plant...

21

1 1 Acquisition of Lafarge´s assets in Honduras September 2013 Barco Selenna , muell de Haití Exportaciones desde el puerto Cartagena, Colombia Mural of premixed architectonical ready-mix, Bogotá, Colombia

Transcript of Acquisition of Lafarge´s assets in Honduras500 2,600 2,700 2,800 2,900 3,000 ... Cement plant...

11

Acquisition of Lafarge´s assets in HondurasSeptember 2013

Barco Selenna , muell de HaitíExportaciones desde el puerto Cartagena, ColombiaMural of premixed architectonical ready-mix, Bogotá, Colombia

22

DISCLAIMERThis document contains forward-looking statements relating to Cementos Argos S.A. and its subsidiaries (Argos) based upon management projections.

These projections reflect Argos’ opinion on future events that may be subject to a number of risks, uncertainties and assumptions. Various factors may cause actual results to differ from those expressed herein.

Argos assumes no obligation to update or correct the information contained in this presentation.

Mixers in the Margaret Hunt Hill Bridge, Dallas, Texas, USA

33

Agenda

1. Transaction details

Macroeconomics, cement market, acquired assets details.

2. Honduras

4. Rationale

4

7

12Integration of the new assets to Argos network, the Argos Model and its potential

4

TRANSACTION DETAILS

Mixer trucks on the 4 South Bridge, Medellín, Colombia

55

Relevant transaction for Cementos Argos:

Overview

Cement installed capacity

Argos reaffirms leadership in the Central America & the Caribbean regional

17m tTotal cement installed capacity

+ 8% + 15%ConsolidatedEBITDA

Total concrete installed capacity

14m m3

Cement installed capacity

4m tRegional cement installed capacity

+ 51% + 68%EBITDA of the regional

EBITDA of the regional

USD 163m

6

HondurasEBITDA EUR 50.5 m

Honduras

53%

Asset Valuation

Acquired ownership

Cash out

EUR m434.6

EUR m434.6

EV/EBITDA8.6x

EUR m231.5

With a cash out of 53% of the total asset value, we will consolidate 100% of the assets

100% funded with owned resources , coming from the preferred shares issuance

Positive impact to the balance structure

Transaction structure overview

7

HONDURAS

Tegucigalpa

8

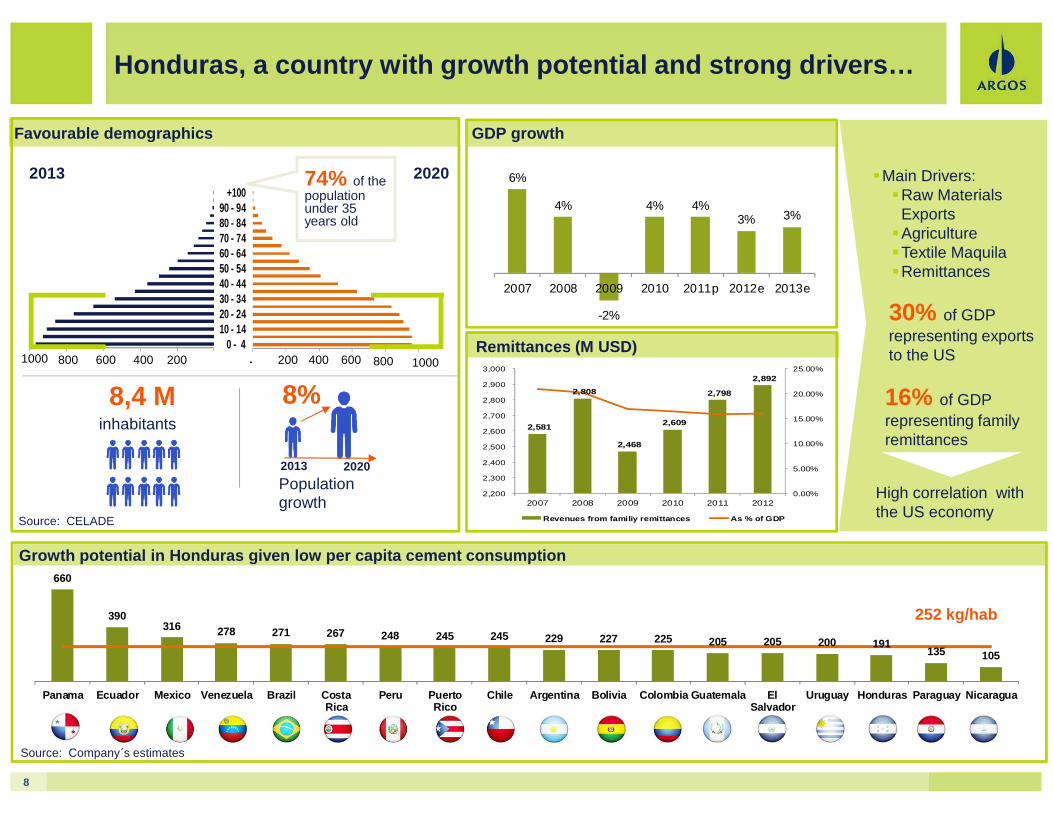

6%

4%

-2%

4% 4%3% 3%

2007 2008 2009 2010 2011p 2012e 2013e

Honduras, a country with growth potential and stron g drivers…

GDP growthFavourable demographics

Growth potential in Honduras given low per capita c ement consumption

Source: Company´s estimates

Remittances (M USD) - 200 400 600 800 1,000

0 - 410 - 1420 - 2430 - 3440 - 4450 - 5460 - 6470 - 7480 - 8490 - 94

+100

(1,000) (800) (600) (400) (200) -

2013 2020

2004006008001000 200 400 600 800 1000

252 kg/hab

74% of the population under 35 years old

8,4 Minhabitants

2013 2020

8%

Population growth

30% of GDP representing exports to the US

16% of GDP representing family remittances

High correlation with the US economy

�Main Drivers:�Raw Materials

Exports �Agriculture�Textile Maquila�Remittances

Source: CELADE

2,581

2,808

2,468

2,609

2,798

2,892

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2,200

2,300

2,400

2,500

2,600

2,700

2,800

2,900

3,000

2007 2008 2009 2010 2011 2012

Revenues from familiy remittances As % of GDP

660

390316 278 271 267 248 245 245 229 227 225 205 205 200 191

135 105

Panama Ecuador Mexico Venezuela Brazil CostaRica

Peru PuertoRico

Chile Argentina Bolivia Colombia Guatemala ElSalvador

Uruguay Honduras Paraguay Nicaragua

9

Source: BCH, Lafarge

Current distribution channels

Retailers 55%Wholesalers 45%

Distribution

53% 47%

Argos Cenosa

1.2 1.31.4 1.4

1.61.7 1.8

1.61.5

1.7 1.7

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Source: Lafarge

Cement Consumption (M Tons)

94%

6%

Ensacado Granel

Cement consumption(M TMPA)

… with a cement market with high growth potential

Total market (2012):1,718,352 MTPA

Market share

Source: BCH, Lafarge

1 According to the National Statistics Institute of Honduras

Potential for market deepening

� In Honduras, the cement price is indexed in USD

� Cement industry growth will be driven by:

� High Infrastructure needs:

� Housing Deficit: 30k housing units and ~ 800k1 in need of improvements.

� Urban Non residential construction demand (offices)

Cement per capita consumption: 191 kg

87%

4%2%3% 4%

Distribution Contractor Pre-cast companies Ready-mix companies Others

Sector Investment USD M

Roads 680

Airports 114

Ports 674

Energy 154

Services 30

Total 1652

10

Competitive advantages

Efficient assets with a privileged location…

Privileged location

Argos Cenosa

Cement Plant

Grinding facility

Port

Private Funds*

Argos

Minority shareholders

45.9%

*IPM de Honduras (Instituto de Previsión Militar): Autonomous agencyfor pension, retirement and credit funding of the military forces.

Lafarge Cementos

Integrated Plant Piedras Azules

Cementosdel Sur (Cesur)

Grinding facility San Lorenzo

CESUR (0.3 M MTPA)

Cementos del Norte (1.5 M MTPA)

Piedras Azules(1.0 M MTPA)

San Lorenzo Port

Piedras Azules

Tegucigalpa

La Ceiba

0.9%

Overview of the acquired assets

Piedras Azules Plant

Ownership structure

105 km

158 km

184 kmSan Pedro Sula

53.28%

� High Operational efficiency:� Clinker/cement factor: 62%� 15% in alternative fuels� Load factor ~ 93%

• Privileged location closed to urban centers� Employee force: 189 direct employees� Local partner: Advantages of having knowledge of the

local economy

�Piedras Azules: Dry process integrated plant

�Cement capacity: 1 M MTPA�Limestone reserves: 100 years� Important puzzolanic reserves

�Cesur: Grinding facility�Location: San Lorenzo�Grinding capacity: 0.3 M TPA�Port facilities

11

Piedras Azules plant

… with growing margins

789

882 874

500

550

600

650

700

750

800

850

900

950

2010 2011 2012

Cement Volume Sold

47.6%

49.7% 49.6%

46%

47%

48%

49%

50%

2010 2011 2012

EBITDA Margin

12

RATIONALE

Camiones mezcladores en Puente de la 4 Sur, Medellí n, ColombiaVessel in Haiti’s port

1313

Advantages of our strategical geographic zone

Source: Cementos Argos

Logistics synergies given our geographic area, port infrastructure and maritime know-how

Countries with consumption per capita growth potential

Economies with different market cycles

Balance between developed & emerging economies

14

Ecuador

Colombia

Suriname

Guyana

Cuba

Jamaica

Bahamas

Honduras

Nicaragua

Panama

El Salvador

French Guyana

Venezuela

0.2 M TM

Haiti

1.6 M TM

3.5 M TM

0.6 M TM

5.5 M TM 0.08 M TM

0.07 M TM0.08 M TM

Lesser Antilles

1 M TM

0.3 M TM

0.08 M TM

Dom.Rep.

Costa Rica

Puerto Rico

The integration of the newly acquired assets in Arg os’ network

Honduras is located within our strategic geographic area

1

14

Cementplant

Grindingstation

TerminalArgosAcquired assets

Argos Model

14

15

Ecuador

Colombia

Suriname

Guyana

Cuba

Jamaica

Bahamas

Honduras

Nicaragua

Panama

El Salvador

13

Haiti

1.6 M TM

3.5 M TM

0.6 M TM

5.5 M TM 0.08 M TM

0.07 M TM0.08 M TM

Lesser Antilles

1 M TM

0.3 M TM

0.08 M TM

Dom.Rep.

0.2 M TM

Venezuela

FrenchGuyana

15

Costa Rica

Puerto Rico

Honduras is located within our strategic geographic area

1

Potential for synergy generation: operating, administrative and distribution

2

The integration of the newly acquired assets in Arg os’ network

Cementplant

Grindingstation

TerminalArgosAcquired assets

Argos Model

16

Ecuador

Colombia

Venezuela

Suriname

Guyana

Cuba

Jamaica

Bahamas

Honduras

Nicaragua

Panamá

El Salvador

13

Haiti

1.6 M TM

3.5 M TM

0.6 M TM

5.5 M TM 0.08 M TM

0.07 M TM0.08 M TM

Lesser Antilles

1 M TM

0.3 M TM

0.08 M TM

Dom. Rep.

0.2 M TM

FrenchGuyana

16

Costa Rica

Puerto Rico

Honduras is located withinour estrategic geographicarea

1

Potential for synergygeneration: operating, administrative and distribution

Potencial to adapt the Argos Model and to offer valueadded products

2

3

The integration of the newly acquired assets in Arg os’ network

Cementplant

Grindingstation

TerminalArgosAcquired assets

Argos Model

17

Ecuador

Colombia

Suriname

Guyana

Cuba

Jamaica

Bahamas

Honduras

Nicaragua

Panama

El Salvador

Venezuela

0.2 M TM

Dom.Rep.

Haiti

1.6 M TM

3.5 M TM

0.6 M TM

5.5 M TM 0.08 M TM

0.07 M TM0.08 M TM

Lesser Antilles

1 M TM

0.3 M TM

0.08 M TM

Costa Rica

Puerto Rico

1317

Honduras is located withinour strategic geographicarea

1

Potential for synergygeneration: operating, administrative and distribution

Potencial to adapt the Argos Model and to offer valueadded products

2

3

Cementplant

Grindingstation

TerminalArgosAcquired assets

Argos Model

The integration of the newly acquired assets in Arg os’ network

FrenchGuyana

1818

Satisfaction, loyalty and brand recognition steadily maintained above international standards.

Argos Model, understanding each client, adding valu e through a segmented proposal with replicable results

Argos is one of the 10 top of mind brands in Colombia

Top of Mind

Value propositions for retail customers Value propositions for industrial customers

Argos Model

One high-value brand

Differential service

Technological platform

Commercial assistance

Technical assistance

� Promote our customers’ business growth

� Develop initiatives to create demand

� Proximity and ease of access to our products

� Recognition and use of our brand

� Tailor-made concrete solutions based on a unique understanding of each project

� Access to technology and equipment (on-site plants, placement equipment)

� Specialized technical assistance : Durability, concrete technologies

� Lead time optimization

We are participating in different high impact infrastructure projects in the three regional divisions.

Canal de Panamá

With proven results

19

Our Argos Model will allow us to:

� Adapt our value proposition to the specific economic dynamics of Honduras

� Capture value through market segmentation (retail and industrial customers)

� Offer a product under one emotionally binding brand

� Establish a distribution model adding value to our end customers, as accomplished in Panama and Colombia

With the opportunity to offer a value proposition i n Honduras…

Colombia

79%

21%

2006Ensacado

Granel

67%

33%

2012 Ensacado

Granel

Argos Model

54%46% 2012 Ensacado

Granel

66%

34%2006

Ensacado

Granel

Panama

Honduras today

2012 2012

94%

6%

Bagged

Bulk45%

55%

Wholesaler

Retailer

Bagged

Bulk

Bagged

Bulk

Bagged

Bulk

Bagged

Bulk

20

Conclusions

Argos Panama plant

Argos. Green Light.

� We accomplish the goals that were set and communicated to the public within the context of the shares emission, using the resources of said emission to generate value for all our shareholders.

� We are consistent with our growth strategy:

� Geographical area with potential of interconnection

� Strong economic and demographic indicators

� The acquired assets will be incorporated into Argos’ current network, creating operational synergies.

� The assets have high operational efficiency and are exceptional EBITDA generators, which makes this acquisition a profitable transaction even without including the potential for synergies.

� We are taking advantage of the historical momentum of the industry and our capacity of integration.

� We maintain our financial solidity and flexibility, using the resources raised through the emission of preferred shares to finance the expansion.

2121

Acquisition of Lafarge´s assets in HondurasSeptember 2013

Barco Selenna , muell de HaitíExportaciones desde el puerto Cartagena, ColombiaMural of premixed architectonical ready-mix, Bogotá, Colombia