ACE 2007

14

ACE 2007 Potentially excessive prices and switching costs: banking cases from Hungary (OTP Bank) Bruno Jullien

-

Upload

hilda-zamora -

Category

Documents

-

view

27 -

download

1

description

Potentially excessive prices and switching costs: banking cases from Hungary (OTP Bank). ACE 2007. Bruno Jullien. A case in « Hungarian » Short but based on economic reasoning (effect based approach) I will focus on termination fees (on personal loans) and ignore « handling fees ». - PowerPoint PPT Presentation

Transcript of ACE 2007

ACE 2007

Potentially excessive prices and switching costs: banking cases from Hungary (OTP Bank)

Bruno Jullien

2

A case in « Hungarian »

Short but based on economic reasoning (effect based approach)

I will focus on termination fees (on personal loans) and ignore « handling fees »

3

Summary

OTP former monopoly facing growing competition

The credit market has been growing fast and seems to stabilize

OTP personal loans : 40-60% contracts (30-40% value)

OTP raises termination fees unilaterally in 2005 (personal loans, housing loans)

Allowed by regulation, legal requirement fulfilled

4

On Banks

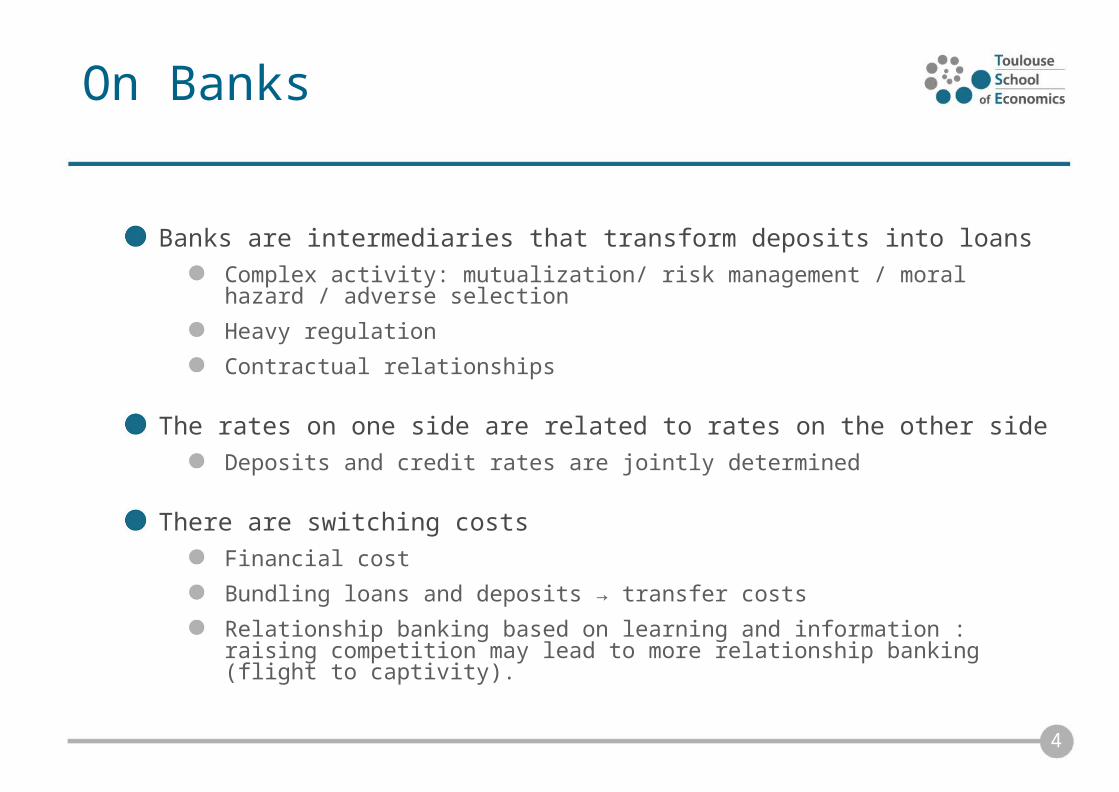

Banks are intermediaries that transform deposits into loansComplex activity: mutualization/ risk management / moral hazard / adverse selection

Heavy regulation

Contractual relationships

The rates on one side are related to rates on the other sideDeposits and credit rates are jointly determined

There are switching costsFinancial cost

Bundling loans and deposits → transfer costs

Relationship banking based on learning and information : raising competition may lead to more relationship banking (flight to captivity).

5

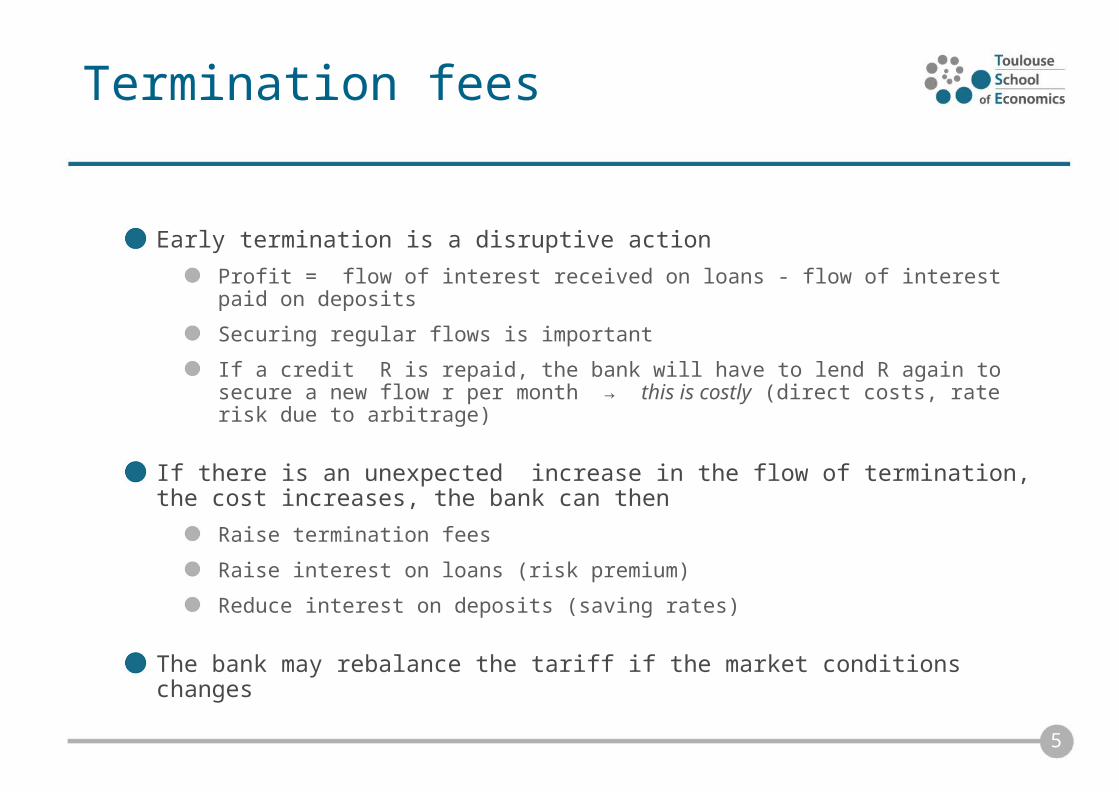

Termination fees

Early termination is a disruptive action

Profit = flow of interest received on loans - flow of interest paid on deposits

Securing regular flows is important

If a credit R is repaid, the bank will have to lend R again to secure a new flow r per month → this is costly (direct costs, rate risk due to arbitrage)

If there is an unexpected increase in the flow of termination, the cost increases, the bank can then

Raise termination fees

Raise interest on loans (risk premium)

Reduce interest on deposits (saving rates)

The bank may rebalance the tariff if the market conditions changes

6

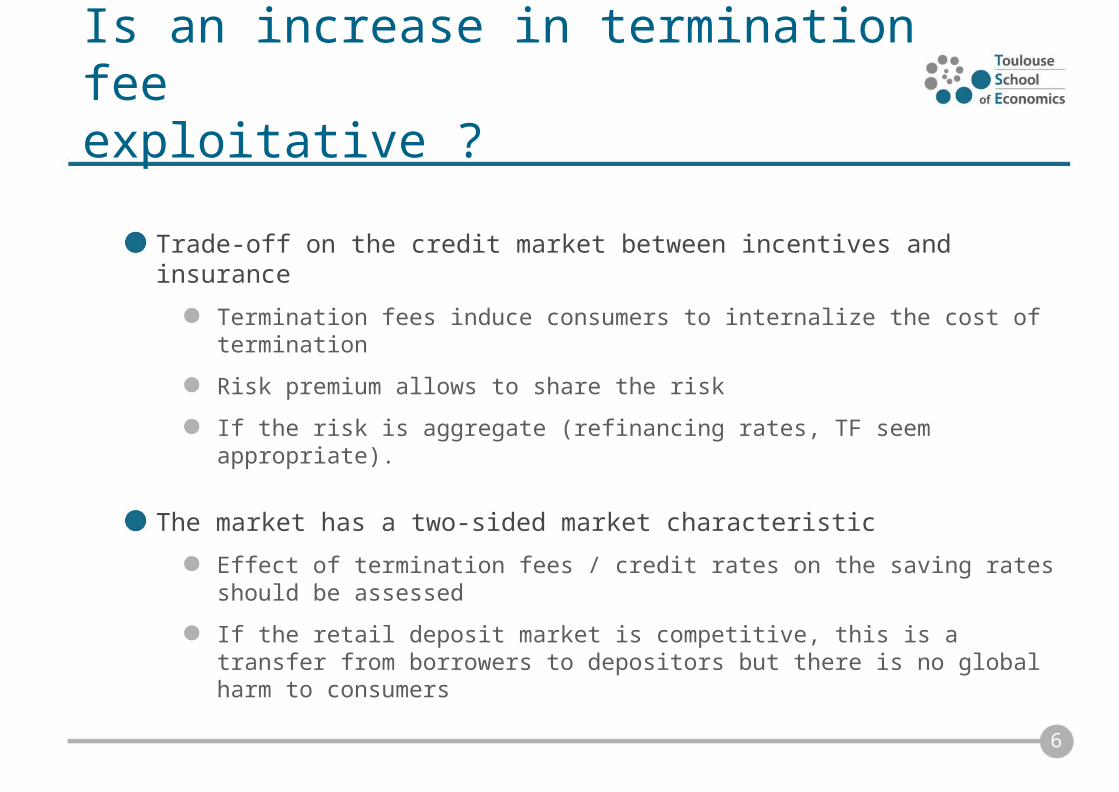

Is an increase in termination feeexploitative ?

Trade-off on the credit market between incentives and insurance

Termination fees induce consumers to internalize the cost of termination

Risk premium allows to share the risk

If the risk is aggregate (refinancing rates, TF seem appropriate).

The market has a two-sided market characteristic

Effect of termination fees / credit rates on the saving rates should be assessed

If the retail deposit market is competitive, this is a transfer from borrowers to depositors but there is no global harm to consumers

7

Market assessment An “effect based” approach

No real assessment of a “relevant market”Substantial switching costs, high market share for OTP

But evidence of competition on the credit market

Unilateral changes of contractLack of information due to inadequate regulation, lack of market transparency, switching costs

The text establishes that there is No significant market power on the credit market

But “SMP toward their locked-in consumers….”

No discussion of the saving side

But no assessment of the elasticity of termination to the fee

8

Economic theories of abuse with switching cost

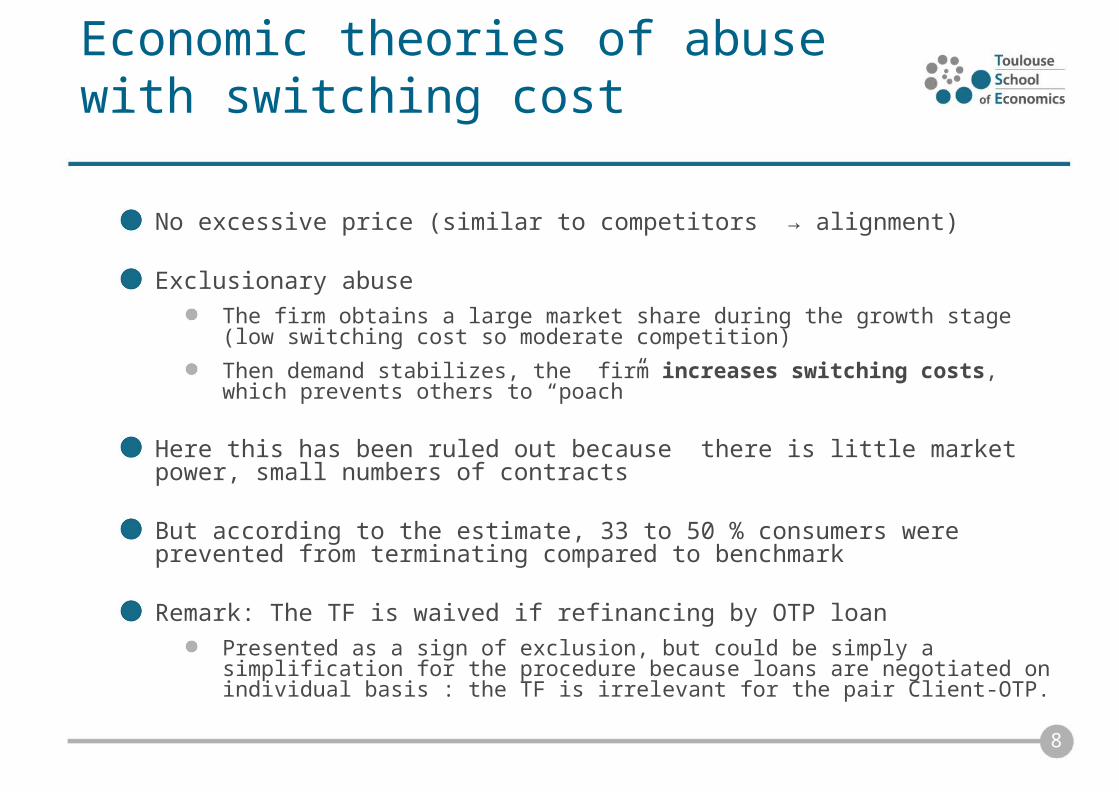

No excessive price (similar to competitors → alignment)

Exclusionary abuseThe firm obtains a large market share during the growth stage (low switching cost so moderate competition)

Then demand stabilizes, the firm increases switching costs, which prevents others to “poach”

Here this has been ruled out because there is little market power, small numbers of contracts

But according to the estimate, 33 to 50 % consumers were prevented from terminating compared to benchmark

Remark: The TF is waived if refinancing by OTP loanPresented as a sign of exclusion, but could be simply a simplification for the procedure because loans are negotiated on individual basis : the TF is irrelevant for the pair Client-OTP.

9

Economic theories of abuse with switching cost

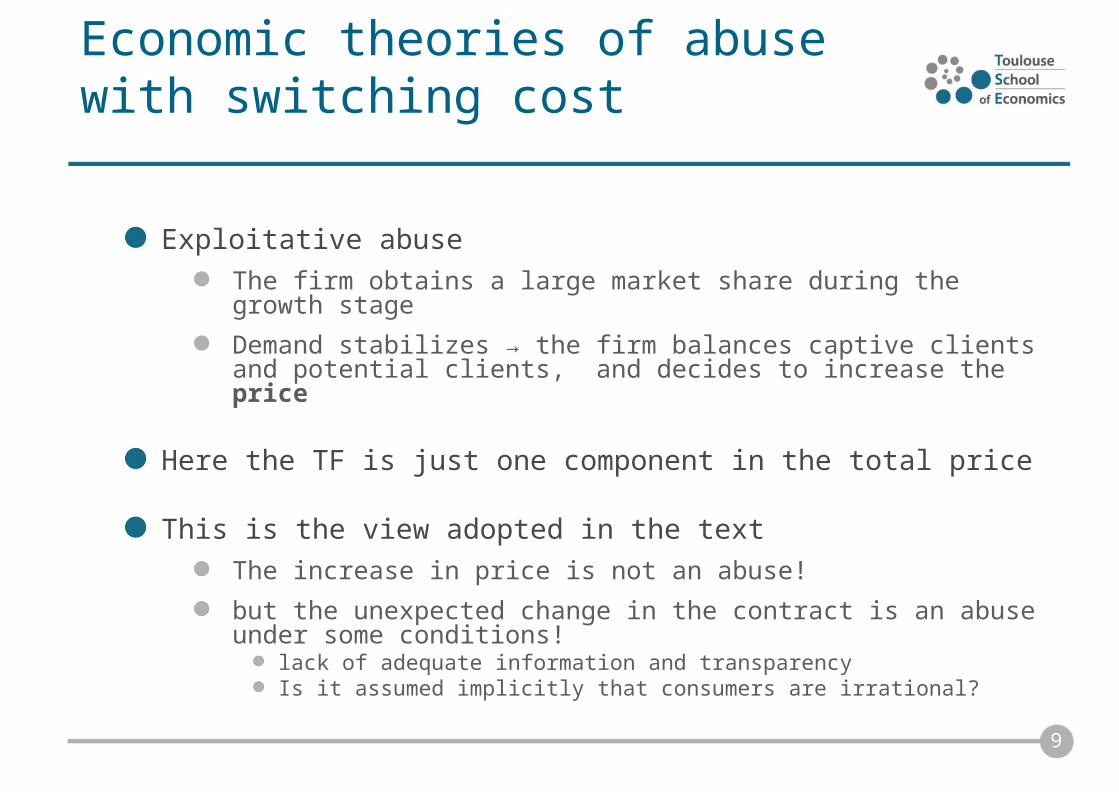

Exploitative abuse The firm obtains a large market share during the growth stage

Demand stabilizes → the firm balances captive clients and potential clients, and decides to increase the price

Here the TF is just one component in the total price

This is the view adopted in the textThe increase in price is not an abuse!

but the unexpected change in the contract is an abuse under some conditions!

lack of adequate information and transparencyIs it assumed implicitly that consumers are irrational?

10

The decision is based on finding little effect of TF on the demand for loans measurement problem creates an illusion as the ex-post individual cost is observable but not ex-ante cost

Both the benefits of OTP on captive clients and the cost imposed on new clients are proportional to the probability of termination

Needs to be quantified ? How was it done ?

In the text, the TF is viewed as another price, not as part of a banking contract

No discussion of rebalancing of the rates / counterfactuals

The main motive for raising TF could be to reduce the amount for termination

Pro-competitive effect if termination is not efficient

Strong elasticity of termination ?

There is a tension between treating the TF as a price and the nature of TF (hence insistence on information)

Does the same reasoning applies for other fees → handling fees ?

11

Abuse ?Regulation or anti-trust

Here the issue is not the price level but the change in contractual terms

The abuse is: not informing consumers and not giving them enough opportunity to react

But there is a regulation for information and the firm followed it

Different from no regulation when there is a regulator

Obligation to act beyond regulation ?

There is the common law for contracts

12

Exploitative abusesRegulation or anti-trust

Can AA intervene if there is a regulator?

Yes for exclusionary practices that cannot be addressed by ex-ante structural remedies

But exploitative abuses ?

Most economists argue that

Exploitative abuses should be the exception Difficulty in defining “normal prices”Effects of prices on entry , Motor of innovation and growth Ex-post monitoring for remedies

Remedies should be structural

When there is a regulator, “excessive prices” should be left to regulators

Little on non-price abuses

Little on how to discipline regulators with different agendas

13

Remedies

The remedy has two dimensions1. Correct for the “inadequate” regulation by imposing a structural remedy

2. Compensate the consumers

If the facts are established, the structural remedy seems to generate an improvement for the sector, but

But the decision creates jurisdiction conflictsRegulator uncertainty / regulatory squeeze

It would be preferable to convince the regulator to change the rules

There is no fine, but the authority decides on the consumers’ compensation

All the decisions are concentrated in the hand of the same entity

This has a flavor of ex-post price regulation

14

Conclusion

The existence of a market failure is not sufficient to establish an abuse:

How to draw the line with effect based approach?

Outcome would most likely differ with a relevant market definition and dominance test (compatibility with art. 82?)

Lack of an analysis of financial contracts (including rates, fees, insurance, …), incentives of OTP, business justification (in the hand-out).

Abuse reduced to “lack of information”, no excessive price

What to do when the regulator is not doing the job?