Accounts Payable Corporate Office, Noida Audit period ......Sub: Internal Audit Report of Accounts...

29

. Confidential & Restricted Access 1 Internal Audit Report – Accounts Payable Corporate Office, Noida Report No: OIL/IA/AU-14.8./CO/2014-15/14 Period covered: April 1, 2014 to Dec 31, 2014 Audit period : February 02, 2015 to February 10, 2015 Report date: 12 th May, 2015

Transcript of Accounts Payable Corporate Office, Noida Audit period ......Sub: Internal Audit Report of Accounts...

.Confidential & Restricted Access1

Internal Audit Report – Accounts PayableCorporate Office, Noida

Report No: OIL/IA/AU-14.8./CO/2014-15/14

Period covered: April 1, 2014 to Dec 31, 2014Audit period : February 02, 2015 to February 10, 2015

Report date: 12th May, 2015

.Confidential & Restricted Access2

OIL INDIA LIMITEDInternal Audit Department

(For Internal Use Only)

Ref : OIL/IA/AU-14.8./CO/2014-15/14 Date : 12.05.2015

GGM(F&A)

Sub: Internal Audit Report of Accounts payable for Corporate Office for the period April 1, 2014 to December,2014

1. Please find attached herewith the Internal Audit report of Accounts -Payable for Corporate Office, Noida for theperiod April 1, 2014 to December, 2014. The report has been issued after incorporating the management commentswherever received and further audit comments for necessary action at your end.

2. The audit has been conducted on test check basis and based on the records / documents produced and theexplanations given to the audit. Consequently, the matters raised in this report are primarily those which have beenobserved during the course of our audit and are not necessarily a comprehensive statement of all the weaknesses orirregularities that may exist or all the compliances or improvements that could be made.

3. We take this opportunity of thanking you and your representatives for the assistance, co-operation and courtesyshown to us during our audit.

J. BhattacharyaSenior Manager (Internal Audit)

CC : Head (Finance) /GGM(RM &Audit ),NoidaCC: CM(IA)

.Confidential & Restricted Access3

Table of ContentsPage No.

Audit Scope and Audit Team 4Summary of audit observations 5Executive Summary 6Detailed Observations 11

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access4

Scope: Accounts Payable

Audit team

Name Designation Role

Sh.Jyotirmoy Bhattacharya Sr.Manager (IA) Team Lead

Sh. Arvind K. Sinha Dy. Manager (IA) Auditor

Sh. A. K .Pathak Sr. Internal Audit Officer Auditor

Audit Areas1 Vendor Master2 Matching PO3 Posting to payable4 Vendor Balance5 Debit/Credit Notes6 Legal case by Vendor7 Accounting Policy8 Bank Guarantee

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access5

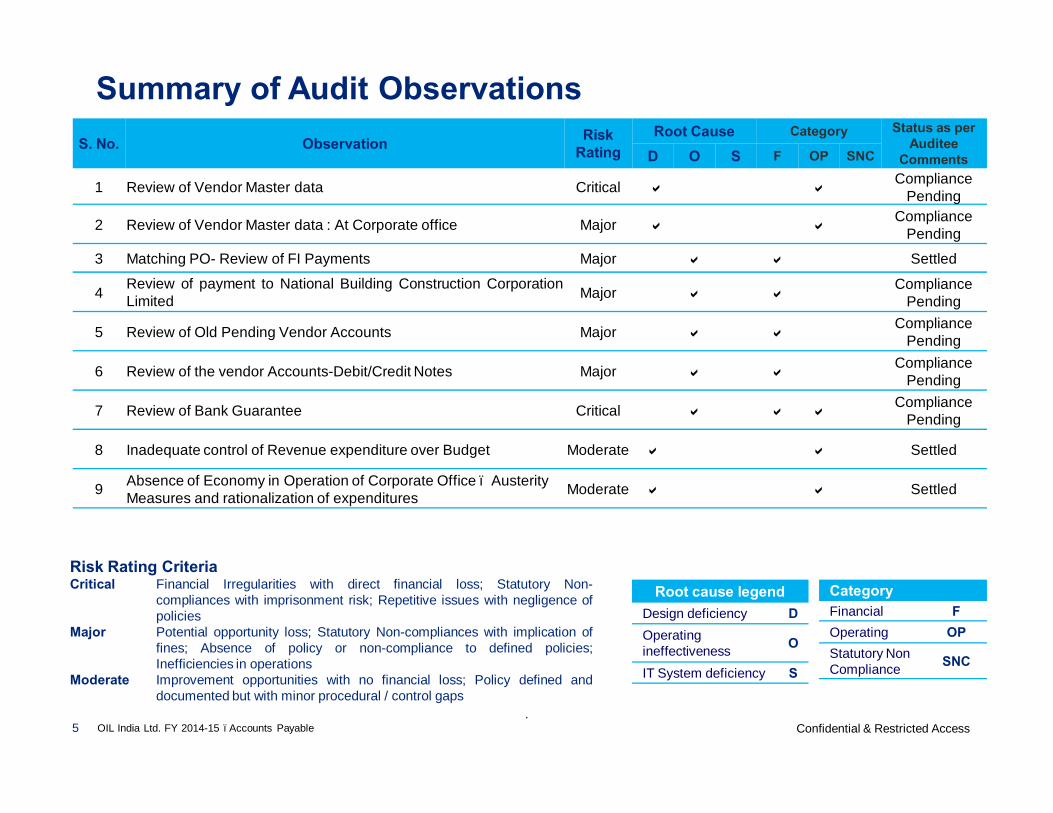

S. No. Observation Risk Rating

Root Cause Category Status as per Auditee

CommentsD O S F OP SNC

1 Review of Vendor Master data Critical a aCompliance

Pending

2 Review of Vendor Master data : At Corporate office Major a aCompliance

Pending3 Matching PO- Review of FI Payments Major a a Settled

4 Review of payment to National Building Construction CorporationLimited Major a a

Compliance Pending

5 Review of Old Pending Vendor Accounts Major a aCompliance

Pending

6 Review of the vendor Accounts-Debit/Credit Notes Major a aCompliance

Pending

7 Review of Bank Guarantee Critical a a aCompliance

Pending

8 Inadequate control of Revenue expenditure over Budget Moderate a a Settled

9 Absence of Economy in Operation of Corporate Office – Austerity Measures and rationalization of expenditures Moderate a a Settled

Summary of Audit Observations

Risk Rating CriteriaCritical Financial Irregularities with direct financial loss; Statutory Non-

compliances with imprisonment risk; Repetitive issues with negligence ofpolicies

Major Potential opportunity loss; Statutory Non-compliances with implication offines; Absence of policy or non-compliance to defined policies;Inefficiencies in operations

Moderate Improvement opportunities with no financial loss; Policy defined anddocumented but with minor procedural / control gaps

Root cause legendDesign deficiency DOperating ineffectiveness O

IT System deficiency S

CategoryFinancial FOperating OPStatutory Non Compliance SNC

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access6

Executive Summary

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access7

Key ObservationsS. No. Observations Impact Auditee Comments

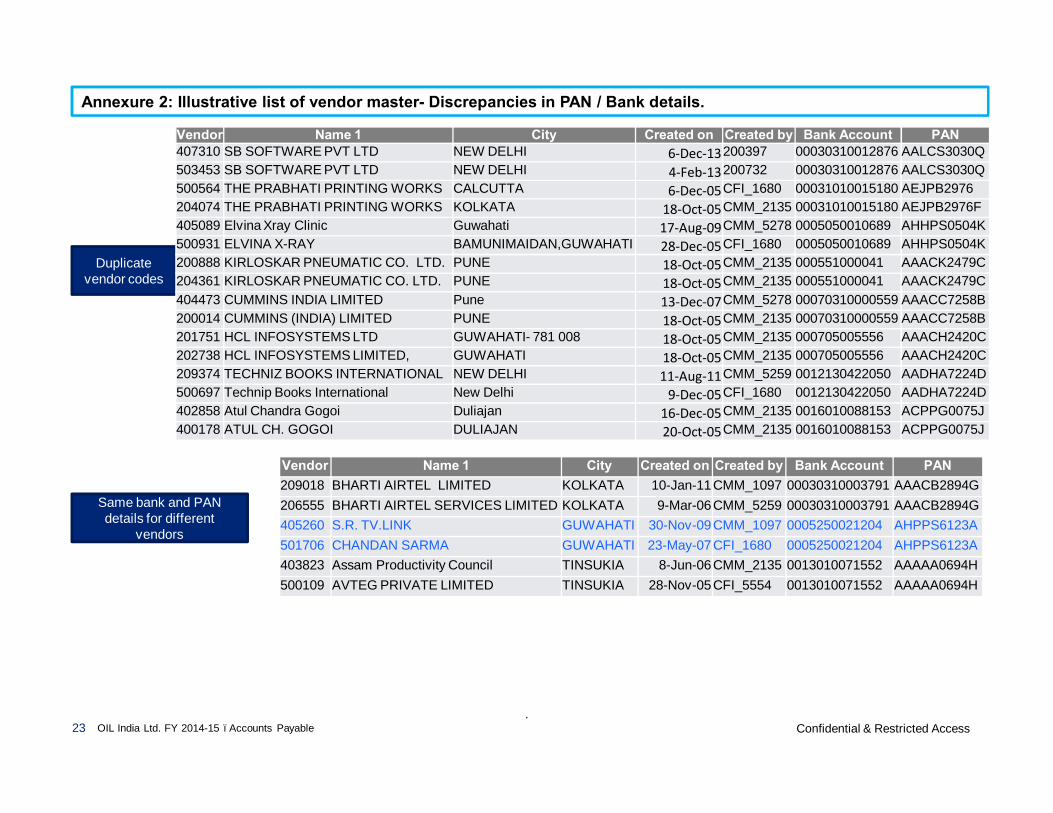

1 On analysis of 21296 vendor records* as on December23, 2014, it was noted that complete data were notupdated in vendor master. Further the details uploadedwere not correctly uploaded.§ PAN No. not updated in 12848 cases§ Wrong PAN no. were updated (illustrative list given in

annexure 1)§ Possible duplicate vendor codes (illustrative list given

in annexure 2)§ Same PAN and Bank details for different vendors

(illustrative list given in annexure 2)

Erroneous details in vendormaster may result in wrongor delayed payments

Audit has reviewed the creation &updation of the vendor master data asthe company as whole & report hasalready been submitted to ERP(MM).Maker checker control does not existnow and this is a matter of policy whichwould be looked into at appropriatelevel. As far as annexure referredherein are concerned, most of the entrypertains to year 2005 & 2006 enteredby the core team members fromDuliajan. These vendors may not be inuse now and the same may be verifiedby the Audit. We have done the samplechecking and found that vendorpertains to other spheres.It is also noted that this is a generalaudit observation which has beennoted. However, dealing persons will beadvised suitably to be extra vigilantwhile entering the master data.

Further Audit Remarks:The department reply is general innature .The issue is serious in natureand audit committee has also advised“In order to eliminate duplicateVendor code, evolve a centralizedsystem, for generating vendor code.’’

Please advise action taken report onthe above and confirm along withblocking of duplicate vendors as perrecords.

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access8

Key ObservationsS. No. Observations Impact Auditee Comments2. Review of Vendor Master data : At

Corporate office:On review of changes made in Vendormaster and following observation arefound :

1. The reason for changing thevendor master data is not recordedin the system as there is no spaceearmarked to capture the same.

2. The supporting documents formaking the changes in the vendormaster data are being kept in file asthere is no system for tagging thesupporting documents in SAP .

3. In few cases, PAN of the concernedvendor were not updated .

4. Maker checker concept is not therein updation of vendor master data.

5. No space for capturing Income taxexemption amount in the relevantcolumn in SAP

• Chances of wrong updation of vendor master data and lack of validation in SAP

• Facts have been stated by the Audit. Wheneverany mistake is detected in vendor master, thesame needs to be corrected. However, reasonsfor the same can not be recorded in the systemin the absence of the space therein. We aresure that all such issues as mentioned at serialno 1 to 6 above, have been taken care off whilesubmitting the report to ERP(MM) & the samewould be addressed while taking action on thereport

Further Audit Remarks :

Action taken report be furnished to audit. As thediscrepancies may result into financial / statutorycompliances risk.

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access9

Key ObservationsS. No. Observations Impact Auditee Comments4. Review of payment to National

Building ConstructionCorporation Limited (NBCC)

Delay in making the payments toNational Building ConstructionCorporation Limited (NBCC) in twoof the occasions leading to levy ofinterest by NBCC to the extent ofRs 24,18,914.

Financial outgo /Loss inform of interest due todelayed payment

No interest has been paid so far & Admin. is being advised topursue the matter with NBCC for waiver of interest.

Further Audit Remarks :

The company has got the demand of apprx. 25 lakh againstinterest on delayed payment. Reasons for this delayedpayment and probable loss of Rs. 25 lakh be furnished toaudit. If the waiver of interest has not been received till date,necessary provision in the books of accounts for the year2014-15 be made against the demand.Details of reasons and action taken for making provision befurnished to audit.

6 Review of the vendor Accounts-Debit/Credit Notes

Long outstanding balance is lying against the vendor (OIL executive deputed in various agencies) to the tune of Rs. 1.5 crore

• Blockage of fund aswell as loss of intereston the blocked fund

These organizations, sometimes, do not pay the full amountagainst the debit note raised by us and we take up the mattersubsequently with them. In the cases mentioned above, weshall find out the break up of the amount deducted from thedebit notes and matter will be ,once again, taken up with theconcerned organizations for an early settlement.

Further Audit Remarks :

Time bound action plan for recovery of Rs.1.5 crore and Rs.0.77 crore due for payment for long be initiated as there is lossof interest on the overdue balance amounts. Status report ofthe recovery/adjustment made of the above amount befurnished to audit by 31.05.2015

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access10

Key ObservationsS. No. Observations Impact Auditee Comments7 Review of Bank Guarantee

A total 46 Nos of BGs have beenmaintained in the system. It hasbeen observed that in few of thecases:

1) Amount has wrong beenupdated.

2) Validity date was wronglyupdated

3) BG status to be correctlyupdated

4) BG No have wrongly beenupdated

5) Currency key were wronglyentered leading to wrong MISgeneration

6) Bank confirmation letter to beobtained/ not available.

Wrong MIS as well aschances of expiration ofthe BG.

Noted. Action will be taken to rectify the updation afterverification. Also concerned persons have been advised totake more care while punching the data related to BGs.

Further Audit Remarks :

The observation is serious in nature. A compliance report ofthe reply as mentioned may please be provided to audit at anearly date.

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access11

Detailed Observations

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access12

All Master Data creation for MM Module is centralized and all Non-Stock Materials Codes are presently exclusively

created by the ERP core Team and Stock Materials by Materials Department. Similarly Vendor Master are also

created by ERP Core team only.

Internal Audit has reviewed the creation and updation of the vendor master data as the company as whole and the

report has already been submitted to ERP (MM). Following are the summary of the observation recorded in the

ERP MM Report.

On analysis of 21296 vendor records* as on December 23, 2014, it was noted that complete data were not updated

in vendor master. Further the details uploaded were not correctly uploaded.

§ PAN No. not updated in 12848 cases

§ Wrong PAN no. were updated (illustrative list given in annexure 1)

§ Possible duplicate vendor codes (illustrative list given in annexure 2)

§ Same PAN and Bank details for different vendors (illustrative list given in annexure 2)

* Only domestic vendors were selected for review on a sample basis. Special vendors like JV partners were also excluded.

Further Audit Remarks:The department reply is general in nature .The issue is serious in nature and audit committee has also advised “Inorder to eliminate duplicate Vendor code, evolve a centralized system, for generating vendor code.’’

Please advise action taken report on the above and confirm along with blocking of duplicate vendors as per records.Person responsible: Finance Target date: Immediate

1. Review of Vendor Master data

CategoryFinancialOperational aStatutory Non Compliance

Root Cause

Absence of maker checkercontrol and decentralization ofresponsibility to update vendormaster.

Implication

Erroneous details in vendormaster may result in wrong ordelayed payments.

Recommendation

Vendor master may be reviewedand necessary action should betaken to address theirregularities as mentioned.

Risk ratingCritical aMajorModerate

Auditee Remarks :Audit has reviewed the creation & updation of the vendor master data as the company as whole & report has alreadybeen submitted to ERP(MM). Maker checker control does not exist now and this is a matter of policy which wouldbe looked into at appropriate level. As far as annexure referred herein are concerned, most of the entry pertains toyear 2005 & 2006 entered by the core team members from Duliajan. These vendors may not be in use now and thesame may be verified by the Audit. We have done the sample checking and found that vendor pertains to otherspheres.It is also noted that this is a general audit observation which has been noted. However, dealing persons will beadvised suitably to be extra vigilant while entering the master data.

.Confidential & Restricted Access13

The updation and changes in the vendor Master data have recently been allowed to be done by the concerned

person in each sphere.

Internal audit has reviewed the changes made during the coverage of the audit period ie Jan’14 to Dec’14 at

corporate office and observed the following .

1. While updating the details such as bank accounts and PAN, the name of the vendor also corrected as the

same were initially created wrong .

2. The reason for changing the vendor master data is not recorded in the system as there is no space earmarked

to capture the same.

3. The supporting documents for making the changes in the vendor master data are being kept in file as there is

no system for tagging the supporting documents in SAP .

4. In few of the cases, the PAN of the concerned vendor were not updated while updating the other details.

5. Maker checker concept is not there in updation of vendor master data.

6. In certain cases the Income Tax exemption certificate is provided by the vendor, however there is no space for

capturing Income tax exemption amount in the relevant column.

A List of Vendor Master changes and PAN no. not updated is given in Annexure 3.

Further Audit Remarks : Action taken report be furnished to audit. As the discrepancies may result into financial/ statutory compliances risk.

Person responsible: Finance

Target date: Immediate

2. Review of Vendor Master data : At Corporate office

CategoryFinancialOperational aStatutory Non Compliance

Root Cause

Absence of maker checkercontrol and decentralization ofresponsibility to update vendormaster.

Implication

Chances of wrong updation ofvendor master data and lack ofvalidation in SAP

Recommendation1. It is to be ensured that

vendor master data isupdated correctly.

2. The matter is to be taken atERM (MM) for systemrelated issue.

Risk ratingCriticalMajor aModerate

Auditee Remarks : Facts have been stated by the Audit. Whenever any mistake is detected in vendor master, the same needs to becorrected. However, reasons for the same can not be recorded in the system in the absence of the space therein.We are sure that all such issues as mentioned at serial no 1 to 6 above, have been taken care off while submittingthe report to ERP(MM) & the same would be addressed while taking action on the report.

Name and PAN updation

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access14

Audit reviewed the FI payment made during Jan’14 to Dec’14 and observed that an amount of Rs. 84.26 crore wasmade directly though FI Module ie without routing the payment through MM Module. The audit also done acomparative study of the FI payment made during the current period with that of the corresponding period of theprevious year which shows that there has been an increase of 58 %.

It was also observed that main component of the FI Payment were payment related to NBCC, Rent, Contractothers, expenses towards Donations, Legal Expenses, Electricity, Telephone & Professional fees.

It was further noted that the contractual payment to National Building Construction Corporation Limited (NBCC)was for approximately Rs 105 crores for the 4 units of commercial space taken through NBCC. The aforesaidpayment was required to made in the different date schedules. The payment was made directly through FI Modulewithout preparing the service entry sheet(SES). It has being highlighted time and again in the past that to have aproper control on the payment of huge amounts or of regular nature or contractual in nature, these type ofpayments have to be routed through MM Module and proper SES should be prepared for the same.

Further Payment such as rent are of regular nature , other GL such as 732000 (contract hiringLMV),735000(Contract others) ,731032 (Contract service-other material) & 733001 (Contract Civil maintenance)pertains to various types of contracts, hence, it would be prudent to make the payment under these GL through MMmodule by making proper Service Entry sheet.A list of GL wise FI payment is given in Annexure 4.

Further Audit Remarks : In view of the compliances as stated above para is settled.

Person responsible: Finance

Target date: Settled.

3. Matching PO- Review of FI Payments

CategoryFinancial aOperationalStatutory Non Compliance

Root Cause

FI payment are not restricted

Implication

1.Monirtoring of payment isdifficult when the payment aredirectly made through FIModules.2. Chances of duplicatepayments

Recommendation

1. All payment of regularnature/ contractual in natureis required to be routedthrough MM Module.

2. High values payment is to berouted through MM Modules

Risk ratingCriticalMajor aModerate

Auditee Remarks :For NBCC except for bid submission, payments were released online. Also NBCC was one time vendor from whomwe have purchased commercial space. Audit has raised this point in the previous qtr. also & we have alreadyintimated to Audit that action is on to restrict the FI payments. In fact, we have advised concerned departments,with a copy to audit, to bring all Hotel/Hospital bills through SES route. All major payments are being processedthrough SES with rare exceptions.

GL wise FI payment details

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access15

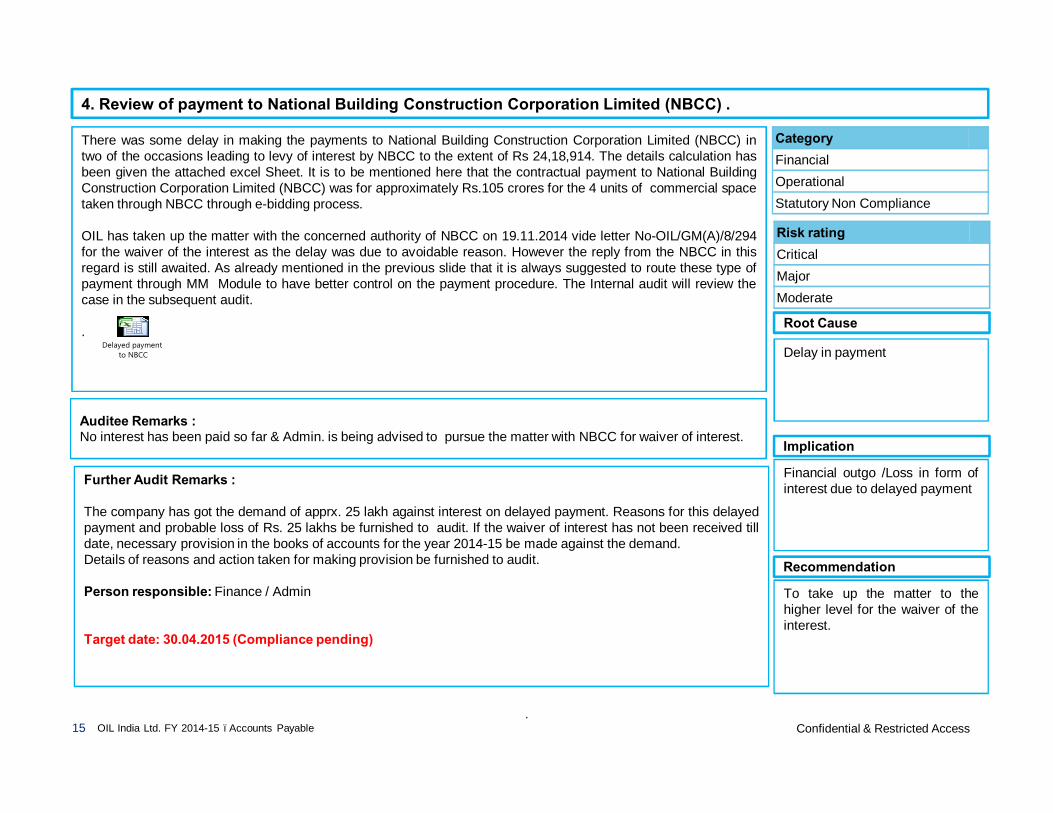

There was some delay in making the payments to National Building Construction Corporation Limited (NBCC) intwo of the occasions leading to levy of interest by NBCC to the extent of Rs 24,18,914. The details calculation hasbeen given the attached excel Sheet. It is to be mentioned here that the contractual payment to National BuildingConstruction Corporation Limited (NBCC) was for approximately Rs.105 crores for the 4 units of commercial spacetaken through NBCC through e-bidding process.

OIL has taken up the matter with the concerned authority of NBCC on 19.11.2014 vide letter No-OIL/GM(A)/8/294for the waiver of the interest as the delay was due to avoidable reason. However the reply from the NBCC in thisregard is still awaited. As already mentioned in the previous slide that it is always suggested to route these type ofpayment through MM Module to have better control on the payment procedure. The Internal audit will review thecase in the subsequent audit.

.

Further Audit Remarks :

The company has got the demand of apprx. 25 lakh against interest on delayed payment. Reasons for this delayedpayment and probable loss of Rs. 25 lakhs be furnished to audit. If the waiver of interest has not been received tilldate, necessary provision in the books of accounts for the year 2014-15 be made against the demand.Details of reasons and action taken for making provision be furnished to audit.

Person responsible: Finance / Admin

Target date: 30.04.2015 (Compliance pending)

4. Review of payment to National Building Construction Corporation Limited (NBCC) .

CategoryFinancial aOperationalStatutory Non Compliance

Root Cause

Delay in payment

Implication

Financial outgo /Loss in form ofinterest due to delayed payment

Recommendation

To take up the matter to thehigher level for the waiver of theinterest.

Risk ratingCriticalMajor aModerate

Auditee Remarks :No interest has been paid so far & Admin. is being advised to pursue the matter with NBCC for waiver of interest.

Delayed payment to NBCC

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access16

(a) Income Tax : - An amount of Rs 12,08,658 for the claim against excess tax deposited are lying open in thesystem from Jan’2006 onward. Almost 8 years have passed since the excess payment was made, however thedetails of the correspondence with the Income Tax Department regarding recovery of the said amount could not beavailable as the case is very old. The details of the GL are as follows :

Further Audit Remarks : A copy of write off approval note be furnished to audit . Please take necessaryprovision against these write off in the F.Y 2014-15 , if write off note is under process of approval.

Person responsible: Finance

Target date: 30.04.2015 (Year End closing for F.Y 2014-15)

5. Review of Old Pending Vendor Accounts

CategoryFinancial aOperationalStatutory Non Compliance

Root Cause

Excess payment

Implication

Blockage of Fund.

Recommendation

Effort shall be made to set theexcess tax paid.

Risk ratingCriticalMajor aModerate

Auditee Remarks :These are very old cases pertaining to 2006 & chances are remote that we shall get any refund from income taxauthorities. We shall initiate action to write off these amounts.

Assignment Doc-No TypePosting Date Amounts. Text

095/064 2605001854 SA 01.01.2006 9,06,233Claim against excess deposit to Income Tax Dept.

20060331 2605002502 SA 31.03.2006 3,02,425excess tax deposited against sec.192 to be claimed

Total 12,08,658

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access17

(b) Old Outstanding against vendor Accounts (OIL executive deputed in various agencies)Internal Audit has reviewed the outstanding balance recoverable against various vendor. It has been observed thatthe outstanding balance lying against the vendor (OIL executive deputed in various agencies) has not been settledsince long.Following are the example of few of the cases:

Further Audit Remarks : Time bound action plan for recovery of Rs.1.5 crore and Rs. 0.77 crore due for paymentfor long be initiated as there is loss of interest on the overdue balance amounts. Status report of therecovery/adjustment made of the above amount be furnished to audit by 31.05.2015.Person responsible: Finance Target date: 31.05.2015

6. Review of the vendor Accounts-Debit/Credit Notes

CategoryFinancial aOperationalStatutory Non Compliance

Root Cause

Delay in settlement ofDebit/Credit Notes

Implication

Blockage of fund as well as lossof interest on the blocked fund.

Recommendation

Effort shall be made to realisedthe amount at the earliest.

Risk ratingCriticalMajor aModerate

Auditee Remarks:These organizations, sometimes, do not pay the full amount against the debit note raised by us and we take up thematter subsequently with them. In the cases mentioned above, we shall find out the break up of the amountdeducted from the debit notes and matter will be ,once again, taken up with the concerned organizations for anearly settlement.

Sl.No

Name Vendor No

Deputation on

Amounts (Rs) Remarks (Main reason for o/s)

1 Pawan Kumar 501090 MoP&G 43,81,335 Debit Note for the Period Apr’13 toMarch’14

2 Chabin Chetia 503003 PCRA 12,11,614 Debit Note for the Period Apr’14 toDec’14 and lease rent

3 Kanti Lal Tak 503526 PCRA 22,85,462 Debit Note for the Period Apr’14 toDec’14 and lease rent

4 Prashanta K Purukaysatha

503628 DGH 19,33,223 Debit Note for the Period Apr’14 toDec’14 and lease rent

5 Abashish Pal 503805 MoP&G 52,50,190 Debit Note for the Period Nov’12 toMarch’14.

Total 1,50,62,004

Sl.No

Doc No Vendor No Amounts (Rs) Remarks (Main reason for o/s)

2612003535 502818 777,615 (33.33% SHARE OF EXPENDITURE FOR FEASIBILITY REPORT)-Pending since 01.07.2012

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access18

All the live Bank Guarantees are being maintained in the SAP. Internal Audit reviewed the Bank Guarantees (BGs)generated with the T.Code ZFIBG. A total 46 Nos of BGs have been maintained in the system. It has beenobserved that in few of the cases:

1) Amount has wrong been updated.2) Validity date was wrongly updated3) BG status to be correctly updated4) BG No have wrongly been updated5) Currency key were wrongly entered leading to wrong MIS generation6) Bank confirmation letter to be obtained/ not available.

Illustrative list of such cases have been given in Annexure-5

Further Audit Remarks :

The observation is serious in nature. A compliance report of the reply as mentioned may please be provided toaudit at an early date.

Person responsible: Finance

Target date: 31.05.2015

7. Review of Bank Guarantee

CategoryFinancial aOperational aStatutory Non Compliance

Root Cause

Incorrect updation of BG detailsin SAP.

Implication

Wrong MIS as well as chancesof expiration of the BG.

Recommendation

Bank Guarantee should becorrectly updated and reviewedon the periodic basis.

Risk ratingCritical aMajorModerate

Auditee Remarks :

Noted. Action will be taken to rectify the updation after verification. Also concerned persons have been advised totake more care while punching the data related to BGs.

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access19

There is an inadequate control of revenue expenditure in all the cost centres of Corporate Office for the period fromApril to December, 2014 (9 months) which can be explained as under :-

§ Against an overall budget of Rs.67.92 Crores under the Controllable Cost Elements, the actual expenditure isRs.101.98 Crores i.e. an increase by 50.16%;

§ Major components for increase in expenditures are given in the following table :-Rs./Crores

Audit Observation : Hence there is a lack of strict monitoring of expenditure over budget and inadequate controlof expenditure.

Further Audit Remarks :

In view of the compliances as stated above, the action taken report by the department may be sent to Audit for periodical review.

Person responsible: Finance

Target date: Ongoing, next review 30.06.2015

8. Inadequate control of Revenue expenditure over Budget

CategoryFinancial aOperationalStatutory Non Compliance

Root Cause

Lack of control over revenuebudget

Implication

Excess expenditure over budget

Recommendation

A control mechanism should beintroduced in SAP to monitor theactual expenditure to restrictagainst the budgeted figure

Risk ratingCriticalMajor aModerate

Auditee remarksCompany has introduced BPC module for revenue budget which would be implemented from 2015-16. Budget hasbeen prepared accordingly after taking input from various departments. New departmental cost centers have alsobeen opened. With the introduction of this BPC module, we shall be in a position to monitor actual expenses overthe budgeted expenses.

Major Cost elements Actual Budget Difference % increase

Contract Cost 65.34 37.71 27.63 73.27

Insurance, Rates & Taxes 4.12 3.70 0.42 11.20

Sundry Cost 19.97 11.69 8.28 70.84

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access20

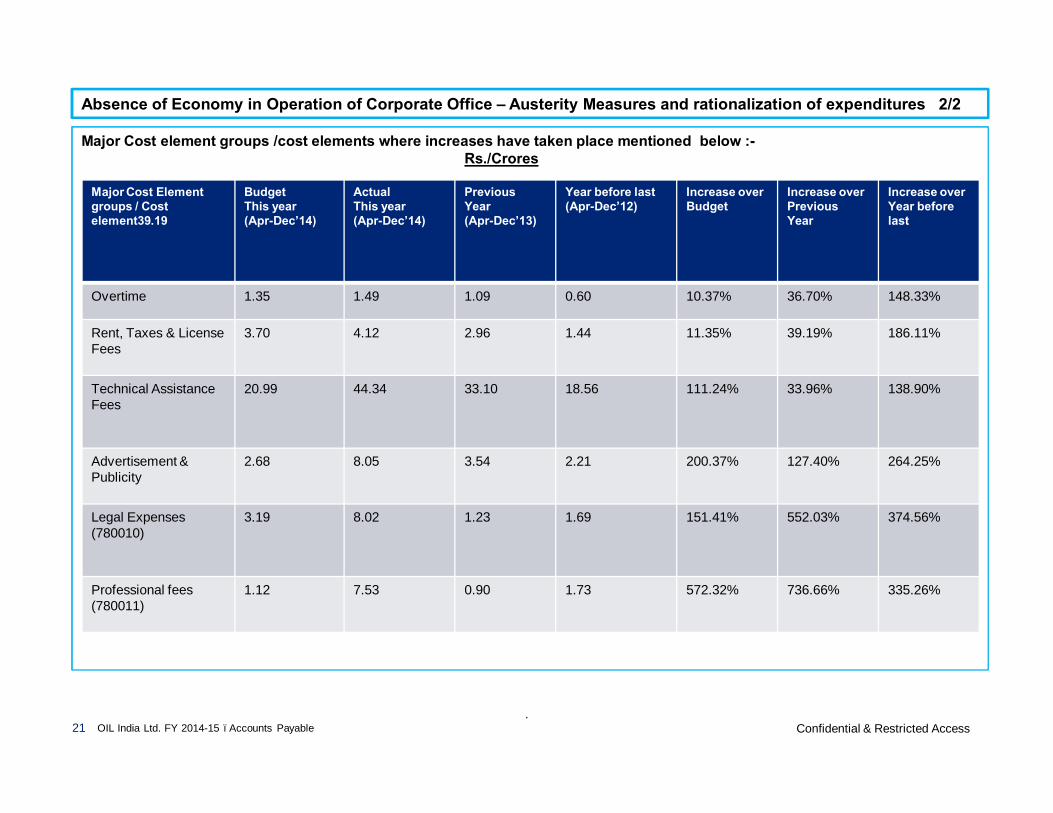

It may be noted that the Ministry of Petroleum & Natural Gas(MoPNG) has given various instructions on theausterity/ Economy measure vide letter Nos. G-38011/80/2013-Fin-I dated 11th November, 2014 which has beencommunicated to all the spheres of the Company including Corporate Office. MoPNG has again given furtherinstructions on economy measures and rationalization of expenditure. Director(Finance) vide letter no.OIL/44/1/3687 dated 7th January, 2015 has also given necessary instructions to ensure strict compliance of theGovt. instruction.Internal Audit(IA) has reviewed variance analysis of GLs related to Austerity Measure in all the cost centres for theperiod from April to December’2014 of Corporate Office, Noida with the budgeted amount as well as the Actualof the corresponding previous year same period.Observations:It is hereby observed that against a total budgeted costs of Rs.62.03 Crores, the actual expenditure hasgone up to Rs.94.77 Crores i.e. an increase of 52.76% ;Further it is also observed that the Corporate Office has also surpassed the expenditure during the 9 months periodfrom April to December of this year over corresponding same period of previous year and year before last in all theGLs mapped under Austerity measures. Thus there is absence of economy in operation of Corporate Office.The major elements of cost increase is given in next slide/page.

Further Audit Remarks :In view of the compliances as stated above, the action taken report by the department may be sent to Audit for periodical review.Person responsible: Finance Target date: Ongoing, next review 30.06.2015

9. Absence of Economy in Operation of Corporate Office – Austerity Measures and rationalization of expenditures(1/2)

CategoryFinancial aOperationalStatutory Non Compliance

Root Cause

Lack of control over revenuebudget

Implication

Excess expenditure over budget

Recommendation

A control mechanism should beintroduced in SAP to monitor theactual expenditure to restrictagainst the budgeted figure

Risk ratingCriticalMajorModerate a

Auditee Remarks It is a matter of fact that expenses have increased considerably during April to Dec., 2014 while compared to thebudgeted figures. Some actions have already been taken for control of OT & advertisement charges. Expensesrelated to technical assistance fee, legal expenses & professional fee etc. are such expenses which are incurredon need basis. Such kind of expenses, sometimes, are not even known at the time of budget preparations. Eventhen, matter will be taken up with the concerned departments so that a realistic budget can be prepared so as toavoid the huge gap between actual expenses & the budgeted figures. Further, it may be noted that BPC module isbeing implemented from 2015-16 for introducing budgetary control. We have also created separate cost centre toidentify the concerned departments who are exceeding the budget.

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access21

Major Cost element groups /cost elements where increases have taken place mentioned below :-Rs./Crores

Absence of Economy in Operation of Corporate Office – Austerity Measures and rationalization of expenditures 2/2

Major Cost Elementgroups / Cost element39.19

BudgetThis year(Apr-Dec’14)

ActualThis year(Apr-Dec’14)

Previous Year(Apr-Dec’13)

Year before last(Apr-Dec’12)

Increase over Budget

Increase over Previous Year

Increase over Year before last

Overtime 1.35 1.49 1.09 0.60 10.37% 36.70% 148.33%

Rent, Taxes & License Fees

3.70 4.12 2.96 1.44 11.35% 39.19% 186.11%

Technical AssistanceFees

20.99 44.34 33.10 18.56 111.24% 33.96% 138.90%

Advertisement & Publicity

2.68 8.05 3.54 2.21 200.37% 127.40% 264.25%

Legal Expenses(780010)

3.19 8.02 1.23 1.69 151.41% 552.03% 374.56%

Professional fees (780011)

1.12 7.53 0.90 1.73 572.32% 736.66% 335.26%

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access22

Annexure 1: Illustrative list of vendor master- Discrepancies in PAN details

Vendor Name 1 Created on Created by Permanent account number209977 PHARMA CENTRE 7-Aug-12CMM_1097 PANNOTABVL406536 MEMBER SECRETARY, BIHAR STATE POLLU 23-Jul-12CMM_5259 PANNOTABVL406488 SUPERITENDENT OF POLICE 2-Jul-12CMM_1097 PANNOTABVL208795 WIRE & CABLE CORPORATION 16-Jun-10CMM_1097 PANNOTABVL404766 Supdt. of Police, Sibsagar 5-Mar-09CMM_5278 PANNOTABVL208220 ELECTRONICS TEST AND DEVELOPMENT CE 12-Feb-09CMM_1097 TEMPA1882X501126 FA & CAO, E.C. RAILWAY, HAJIPUR 3-Mar-06CFI_1680 PANNOTABVL400741 EASTERN COMPANY 20-Oct-05CMM_2135 G-1002/2(5)/3(1)401150 KANTI BURAGOHAIN 20-Oct-05CMM_2135 PANC1526D200262 BHARAT FORGE & PRESS INDUSTRIES LTD 18-Oct-05CMM_2135 31-094-CN-6105 DC-SR-I201990 BHARAT MINERALS 18-Oct-05CMM_2135 18-025-PZ-6811203171 THE PIPELINERS COOP SOCIETY LTD. 18-Oct-05CMM_2135 PANNOTABVL204822 GLAND MECH INDUSTRIES 18-Oct-05CMM_2135 886154/24/41746/AIAPP0463E203136 YOKOGAWA INDIA LTD 10/18/2005CMM_2135 AAACY0840PST001500564 THE PRABHATI PRINTING WORKS 12/6/2005CFI_1680 AEJPB2976

Wrong PAN details >>>

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access23

Annexure 2: Illustrative list of vendor master- Discrepancies in PAN / Bank details.

Duplicatevendor codes

Vendor Name 1 City Created on Created by Bank Account PAN407310 SB SOFTWARE PVT LTD NEW DELHI 6-Dec-13200397 00030310012876 AALCS3030Q503453 SB SOFTWARE PVT LTD NEW DELHI 4-Feb-13200732 00030310012876 AALCS3030Q500564 THE PRABHATI PRINTING WORKS CALCUTTA 6-Dec-05CFI_1680 00031010015180 AEJPB2976204074 THE PRABHATI PRINTING WORKS KOLKATA 18-Oct-05CMM_2135 00031010015180 AEJPB2976F405089 Elvina Xray Clinic Guwahati 17-Aug-09CMM_5278 0005050010689 AHHPS0504K500931 ELVINA X-RAY BAMUNIMAIDAN,GUWAHATI 28-Dec-05CFI_1680 0005050010689 AHHPS0504K200888 KIRLOSKAR PNEUMATIC CO. LTD. PUNE 18-Oct-05CMM_2135 000551000041 AAACK2479C204361 KIRLOSKAR PNEUMATIC CO. LTD. PUNE 18-Oct-05CMM_2135 000551000041 AAACK2479C404473 CUMMINS INDIA LIMITED Pune 13-Dec-07CMM_5278 00070310000559 AAACC7258B200014 CUMMINS (INDIA) LIMITED PUNE 18-Oct-05CMM_2135 00070310000559 AAACC7258B201751 HCL INFOSYSTEMS LTD GUWAHATI- 781 008 18-Oct-05CMM_2135 000705005556 AAACH2420C202738 HCL INFOSYSTEMS LIMITED, GUWAHATI 18-Oct-05CMM_2135 000705005556 AAACH2420C209374 TECHNIZ BOOKS INTERNATIONAL NEW DELHI 11-Aug-11CMM_5259 0012130422050 AADHA7224D500697 Technip Books International New Delhi 9-Dec-05CFI_1680 0012130422050 AADHA7224D402858 Atul Chandra Gogoi Duliajan 16-Dec-05CMM_2135 0016010088153 ACPPG0075J400178 ATUL CH. GOGOI DULIAJAN 20-Oct-05CMM_2135 0016010088153 ACPPG0075J

Same bank and PAN details for different

vendors

Vendor Name 1 City Created on Created by Bank Account PAN209018 BHARTI AIRTEL LIMITED KOLKATA 10-Jan-11CMM_1097 00030310003791 AAACB2894G206555 BHARTI AIRTEL SERVICES LIMITED KOLKATA 9-Mar-06CMM_5259 00030310003791 AAACB2894G405260 S.R. TV.LINK GUWAHATI 30-Nov-09CMM_1097 0005250021204 AHPPS6123A501706 CHANDAN SARMA GUWAHATI 23-May-07CFI_1680 0005250021204 AHPPS6123A403823 Assam Productivity Council TINSUKIA 8-Jun-06CMM_2135 0013010071552 AAAAA0694H500109 AVTEG PRIVATE LIMITED TINSUKIA 28-Nov-05CFI_5554 0013010071552 AAAAA0694H

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access24

List of Vendor Master changes

Sl.No Date Vendor Changed By New value Old value

1 14-Nov-14 211474 99490 PROSHOP A UNIT OF DELHIGLOF HOUSE I PRO SHOP

2 1-Nov-14 406337 99490 CAP'N CHOPS CATERERS CAP'N CHOPS CATERERS

3 25-Oct-14 504104 99490 JATIN NIRWANI JATIN NIRWAN

4 29-Sep-14 504077 99490 FOODIES HEALTH AND SNACKS CO. FOODIES HEALTH AND SNACKES CO.

5 16-Aug-14 500223 99490 THE INST OF COMPANY SECRETARIES OF THE INSTITUTE OF COMPANY

6 6-Aug-14 504018 99490 SAURBH KIRPAL SAURBH KRIPAL

7 29-Jul-14 504006 99490 OM PRAKASH MITTAL HUF OM PRAKASH MITTAL

8 24-Jul-14 211301 5878 V JHAWAR AND CO V JHAWAR & CO

9 24-Jul-14 503997 5878 KARTAR SINGH CHAUHAN VITA BELLA COSULTANTS PVT LTD

10 13-Jul-14 502433 5878 FORTIS HOSPITALS LTD INTERNATIONAL HOSPITAL LTD

11 22-Jun-14 500341 5878 B.M.CHATRATH AND CO B.M.CHATRATH & CO

12 23-May-14 206797 5878 Eureka Forbes Ltd. Eureka Forbes Ltd.

13 23-May-14 503926 5878 RAJ SUKHIJA RAJ KUMARI SUKHIJA

14 12-May-14 407433 5878 M.V.KINI AND CO. M.V.KINI & CO.

15 10-May-14 503925 5878 YATHARTHWELLNESS HOSPITAL N YATHARTH WELLNESS HOSPITAL AND

16 10-May-14 7000578 5878 LYNETTE MASCARENHAS ERIC CLAUDIUS MASCARENHAS

17 24-Apr-14 503190 5878 BOMBAY STOCK EXCHANGE OF INDIA LTD BOMBAY STOCK EXCHANGE OF INDIA

18 22-Apr-14 503907 5878 COMMONWEALTH GAMES VILL APRT OWNERS COMMONWEALTH GAMES VILL APRT OWNERN

19 22-Apr-14 503907 5878 COMMONWEALTH GAMES VILL APRT OWNERN COMMONWEALTH GAMES VILLAGE

20 14-Mar-14 503878 5878 INDO GULFF DIAGNO N RESEAR CENTRE P INDO GULFF DIAGNOSTICS & RESEARCH C

21 13-Mar-14 503881 5878 DIMOND GENERATOR REPARING WORKS DIMOND GENERATOR

22 26-Feb-14 503880 5878 JOP HOTELS LTD-PARKPLAZA NOIDA RECE J.O.P HOTELS LTD-PARK PLAZA NOIDA

23 23-Feb-14 503870 5878 MUKESH UPPAL MUKESH UPAL

24 8-Feb-14 500204 5878 PETROLEUM CONSERVATION RESEARCH ASS PETROLEUM CONSERVATION RESEARCG ASS

25 31-Jan-14 503831 5878 FORTIS HEALTH MANAGEMENT(NORTH) LTD FORTIS HEALTH MANAGEMENT

26 30-Jan-14 7001567 5878 Shri A C V RAMANUJAM Shri ACV RAMANUJAM

27 16-Jan-14 503816 5878 SEA PRINCESS HOTELS N PROPERTIES PV SEA PRINCESS HOTELS & PROPERTIES

28 10-Jan-14 208011 5878 CENTRAL COTTAGE INDUSTRIES CORP OF CENTRAL COTTAGE INDUSTRIES

Annexure-3

.Confidential & Restricted Access25

List of Vendors where PAN and Bank Accounts details not updated

Sl.No Date Vendor S/code PAN BANK ACCOUNTS1 14-Nov-14 211474 99490 NIL UPDATED2 24-Jul-14 211301 5878 NIL UPDATED3 23-May-14 206797 5878 NIL UPDATED4 4-Oct-13 503735 5878 NIL UPDATED5 18-Sep-13 503723 5878 NIL NIL6 24-Apr-14 503190 5878 NIL NIL

.Confidential & Restricted Access26

Comparative statement of FI Payment2013 2014

GL Descritpion FI Payment (Rs) FI Payment (Rs)

714503Consumption-Capital Items 3765,04,358 6718,85,739

735000Contract Others 283,12,288 287,54,021

714501Consumption-Food Stuff - Manual Posting 177,19,730 185,38,936

780010Sund Exp-Legal Expenses. 116,48,922 180,50,910

780011Sund Exp-Professional Fees 82,38,721 168,25,903

731050Contract-Services-Management Consultancy Services (767,97,387) 161,23,905

721500Electricity Expenses 141,78,027 159,18,175

780076Sund Exp-Donations 527,27,000 101,15,000

751000Rent 431,97,606 73,31,047

780031Sund Exp - Telephone Expenses 55,94,535 64,61,379

780070Sund Exp-Guest House Expenses 57,74,703 55,19,343

732000Contract-Hiring-Light Motor Vehicle 41,43,032 51,18,017

780050Sund Exp - Other Freight 25,93,389 43,88,843

780075Sund Exp-Courtesy Expenses 30,17,071 29,80,646

780030Sund Exp-Postage & Courier Services 6,79,588 21,42,615

780191Sund Exp - Miscellaneous Expenses 24,06,665 20,57,613

721000Mat Consmptn-Fuel And Lube Oil 29,05,861 18,52,984

780003Sund Exp- Certification Fees 3,99,899 16,38,272

780080Sund Exp- Social Welfare Expenses 2,68,892 13,62,400

780077Sund Exp - Gifts 36,66,267 13,34,951

Annexure 4

.Confidential & Restricted Access27

2013 2014GL Descritpion FI Payment (Rs) FI Payment (Rs)

780040 Sund Exp - Books & Periodicals 7,32,665 10,52,296 751001 Rates, Taxes & License Fees 2,21,859 9,31,347 731032 Contract-Services-Other Maintenance 4,40,535 6,50,511 780062 Sund Exp - Water Charges - 4,86,630 714302 Consmptn-Stationery-Manual Entry 2,75,912 2,80,865 780016 Sund Exp-Advertisement & Publicity 100,00,000 2,40,000 731090 Contract-Services-Printing 1,15,331 2,12,500 735001 Contract Casual Labour - 1,65,920 735002 Contract Horticulture - 1,09,600 750001 Insurance Expenses-Motor Vehicle Policy 1,70,843 1,09,101 780020 Sund Exp - Bank Charges - 46,329 780008 Sund Exp-Auditors' Out of Pocket Expenses - 41,739 780190 Sund Exp - Petty Cash Expenses 10,619 20,000 780041 Sund Exp - Data Docket & Data Viewing Expenses 124,56,805 12,802 732001 Contract-Hiring-Bus 47,239 5,483 732008 Contract-Hiring-Others - 4,000 712200 Consmtpn-Computer Hardware & Software 11,000 (2,450)712300 Consumption-Electrical Items - (3,900)714300 Consumption -Stationery - (18,221)780182 Sund Exp-Rec Elec,Water,Gas,H Rent etc-Executive - (23,600)714200 Consmptn- Office Equipment And Accessories - (95,198)750004 Insurance Expenses-Others 7,58,430 -732006 Cont-Hiring-Eqpts 68,753 -780006 Internal Audit Fees 28,487 -780181 Sund Exp-Recoveries 8,831 -733001 Contract-Civil-Maintenance - -731070 Contract-Services-Security (5,91,602) -

Total 5319,34,874 8426,26,453

.Confidential & Restricted Access28

Annexure-5:List of the bank Guarantee

Sl.No BG Ref No.

Bank Guarantee Number Bank Key Vendor

Amount (Rs) Valid from Valid To Remarks

1 1000002522240GT02142610003 HDFMUM17 407483 363.1218.09.2014 15.07.2016Due to wrong selection of currency code (INR5 in place of INR) the report shown the amounts as 363.120 instead of 3,63,120. Currency code to be change accordingly.

2 1000001891IN-DL40157278677560L CORDEL24 407332 5,400.0027.07.2013 28.02.2016 Correct BG No to be updated (correct No-4/2013)

3 1000000771027611ILPER 310276 402632 110,000.0014.11.2011 31.03.2015 BG No and Bank Key to be correctly updated

4 1000000775Sep-13 SYBDEL19 402635 110,000.0005.02.2013 31.03.2015 Correct BG No to be updated (Correct BG No is BG9/2013)

5 10000023862717IGPER000214 BOBDEL13 206511 108,500.0017.10.2014 30.06.2015 BG Status to be changes as confirmed by the bank

6 1000002355BG/90-14 CANDEL24 205740 58,000.0002.06.2014 01.06.2016 BG Validity date was 02.12.2016

7 1000002191DL640902337396 IOBDEL12 407577 38,000.0005.06.2014 16.11.2016 Confirmation number mention by the bank does not match

8 1000002364003GT02142330009 HDFDEL15 405915 18,600.0022.10.2014 21.10.2017 Bank validity starting date was 21.08.2014 and expiry date was 21.04.2018

9 1000002574May-14 CANDEL48 402632 181,000.0001.10.2014 30.11.2016 Bank Guarantee Validity as per record was 31.03.2017, (Correct BG No) 5/2014

10 100000257349/2014 SYBDEL28 402635 181,000.0001.10.2014 30.09.2016 Bank Guarantee Validity as per record was 31.03.2017.

OIL India Ltd. FY 2014-15 –Accounts Payable

.Confidential & Restricted Access29

Annexure-5: List of the bank Guarantee where confirmation from the bank to be taken/kept in file

OIL India Ltd. FY 2014-15 –Accounts Payable

Sl.No BG Ref No. Bank Guarantee Numbr Bank Key Vendor BG Status Amount (Rs) Valid from Valid To Remarks

1 10000018860320-BG0009-12 PSBDEL11 404758Confirmed by Bank 1,396,00016.11.2012 30.04.2015confirmation letter by the bank to be seen

2 100000187312/2011/ICOMM SYBHYD11 209788Created 507,00021.04.2011 03.04.2017Confirmation from the bank to be obtained

3 1000001884120378IBGP00140-1 IDBSUR11 406601Confirmation Request 202,905,00021.11.2012 07.05.2015Confirmation from the bank yet to be obtained

4 1000001885120378IBGP00140-2 IDBSUR11 406601Created 28,595,00021.11.2012 07.05.2015Confirmation from the bank yet to be obtained