ACCOUNTING SYSTEMS refining the journalizing process.

63

ACCOUNTING SYSTEMS refining the journalizing process

-

date post

22-Dec-2015 -

Category

Documents

-

view

232 -

download

1

Transcript of ACCOUNTING SYSTEMS refining the journalizing process.

ACCOUNTING SYSTEMS

refining the journalizing process

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 2

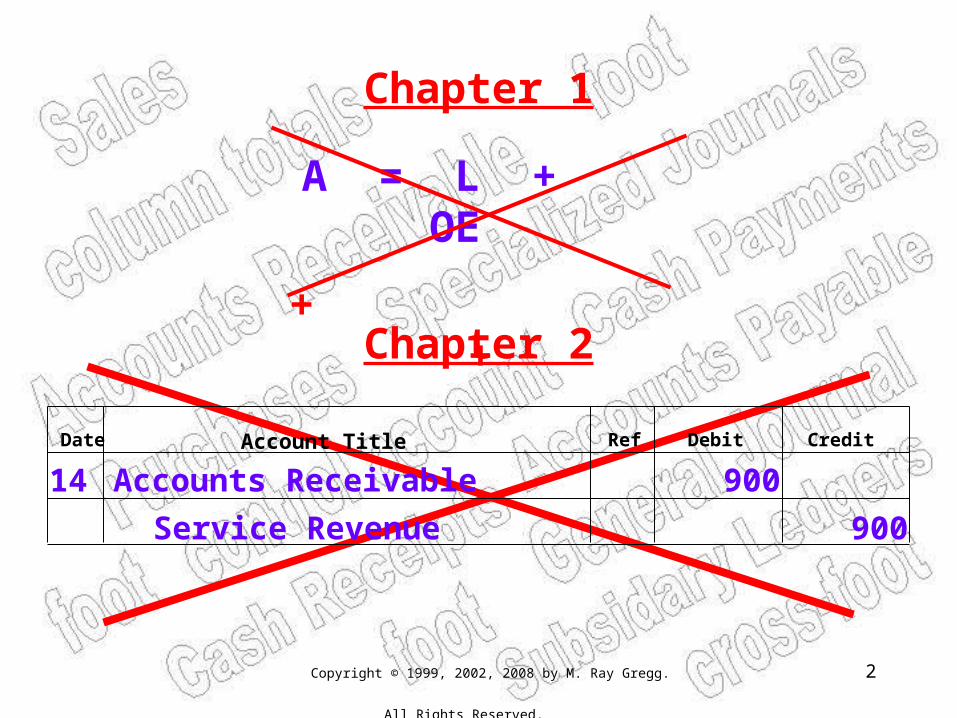

Chapter 1

Chapter 2

A = L + OE

+ +

900

Accounts Receivable Date Account Title Ref Debit Credit

900

Service Revenue

14

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 3

Time Saving Devices

Specialized JournalsSubsidiary Ledgers

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 4

Problems of HavingOnly One Journal

1. Only one person can work at a time

2. Book becomes VERY largeSolution

Specialized Journals

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 5

Specialized Journals

• Save a little time journalizing• Save a LOT of time posting

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 6

Problems of HavingOnly One Ledger

1. Only one person can work at a time

2. Book becomes VERY largeSolution

Subsidiary Ledgers

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 7

General Ledger

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 8

General Ledger

Drs.

Crs.

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 9

General Ledger

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 10

General Ledger

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 11

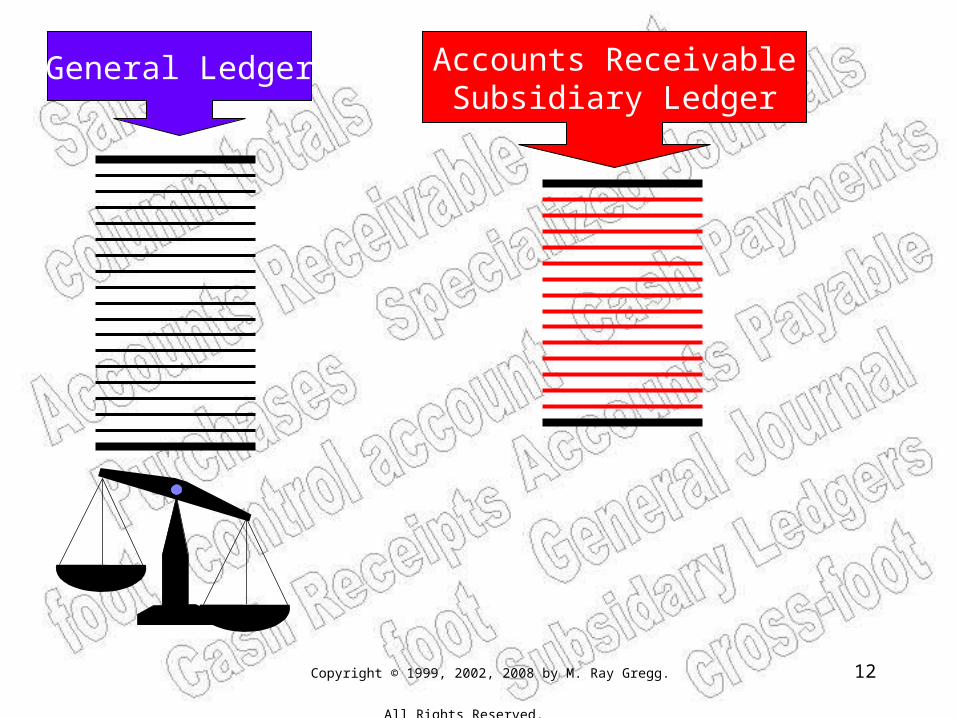

General Ledger Accounts ReceivableSubsidiary Ledger

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 12

General Ledger Accounts ReceivableSubsidiary Ledger

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 13

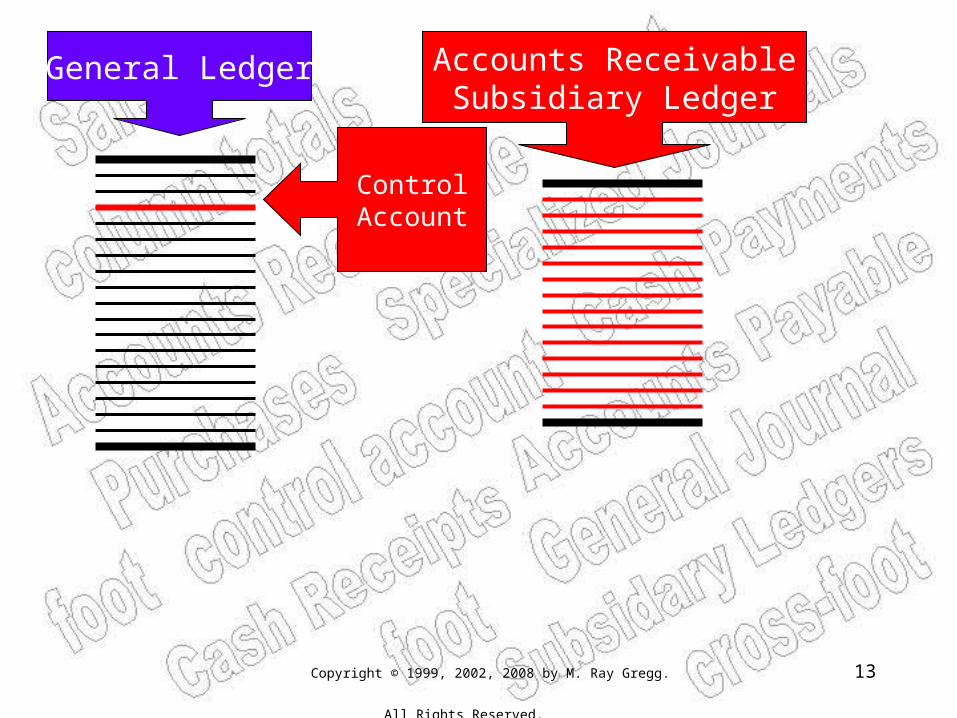

General Ledger Accounts ReceivableSubsidiary Ledger

ControlAccount

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 14

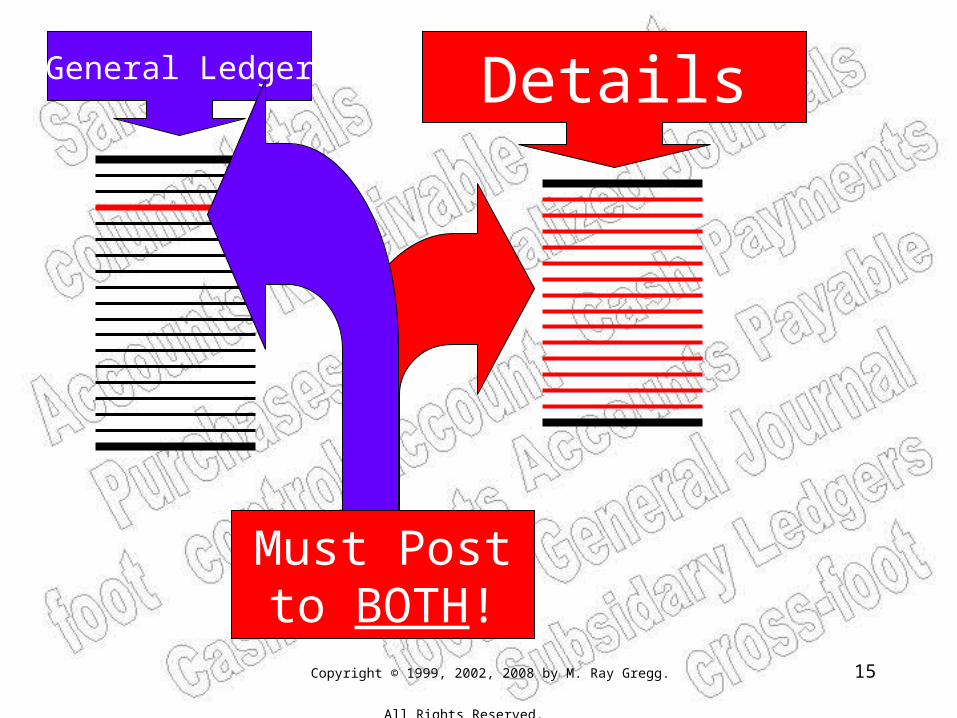

General Ledger DetailsSummary

Info.

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 15

General Ledger Details

Must Postto BOTH!

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 16

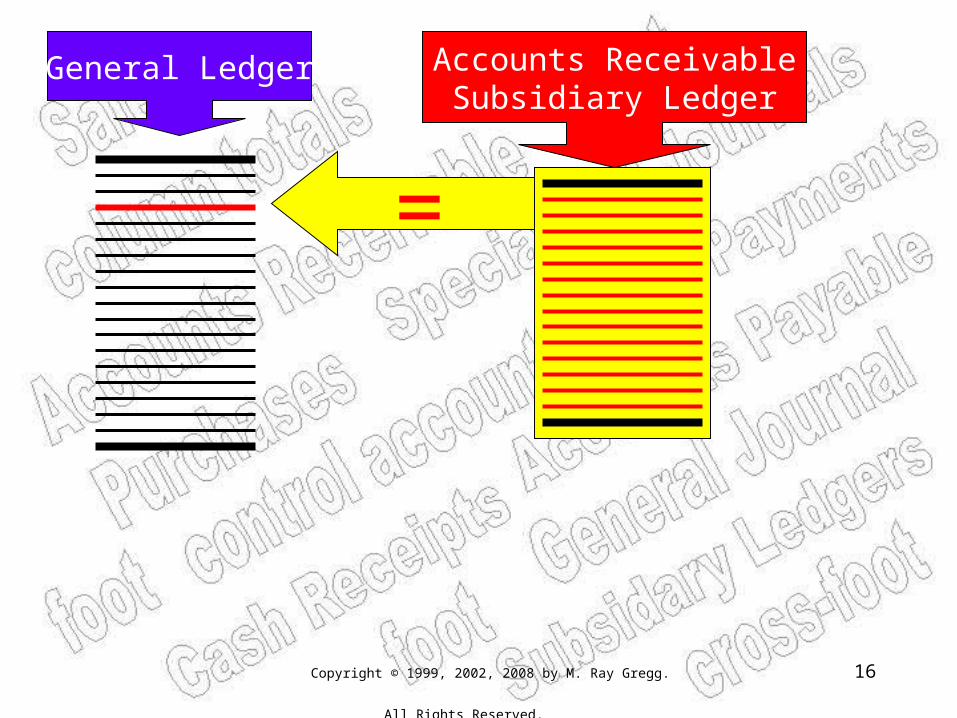

General Ledger Accounts ReceivableSubsidiary Ledger

=

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 17

Subsidiary Ledgers

Accounts Receivable Accounts Payable

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 18

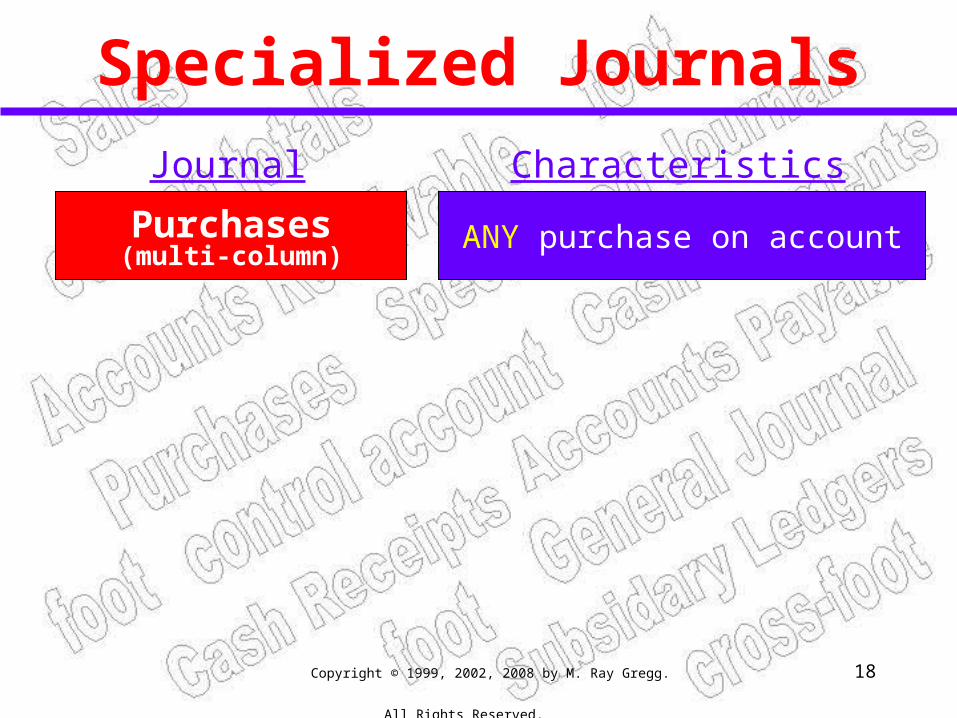

Specialized Journals

Purchases(multi-column)

ANY purchase on account

Journal Characteristics

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 19

Specialized Journals

Purchases(single column)

Sales

Cash Receipts

Cash Payments

General Journal

Purchase of MERCHANDISE on account

Sale of MERCHANDISE on account

ANY collection of cash

ANY cash disbursement

Anything that will not fit someplace else!

Journal Characteristics

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 20

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 21

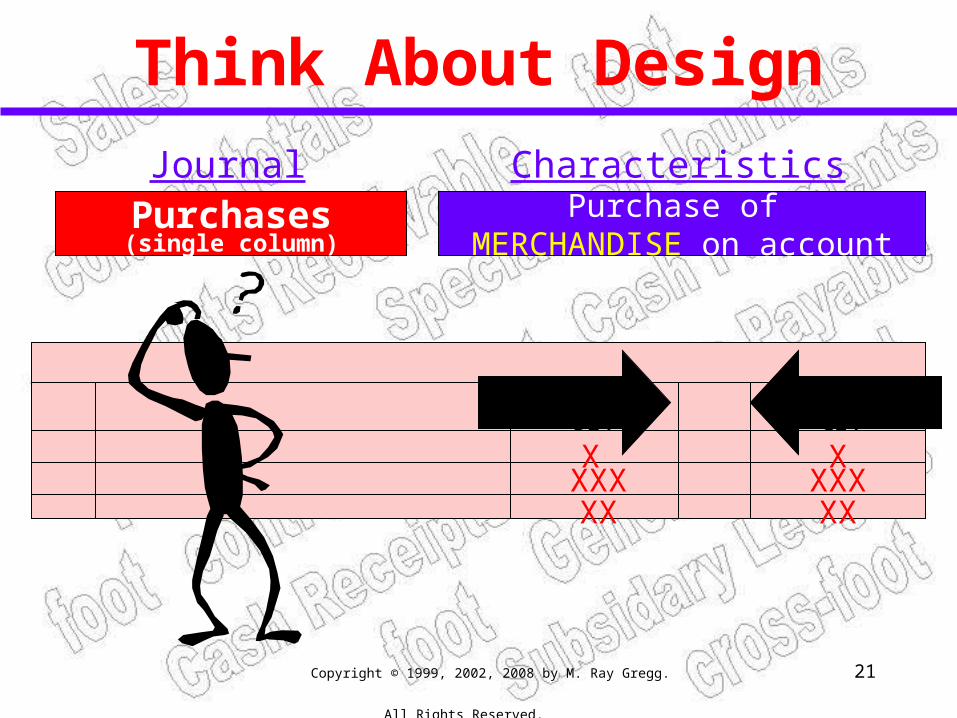

Think About Design

Purchases(single column)

Purchase of MERCHANDISE on account

Journal Characteristics

Mdse Inv.Dr.

Accts. Pay.Cr.

X X

XX XXXXX XXX

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 22

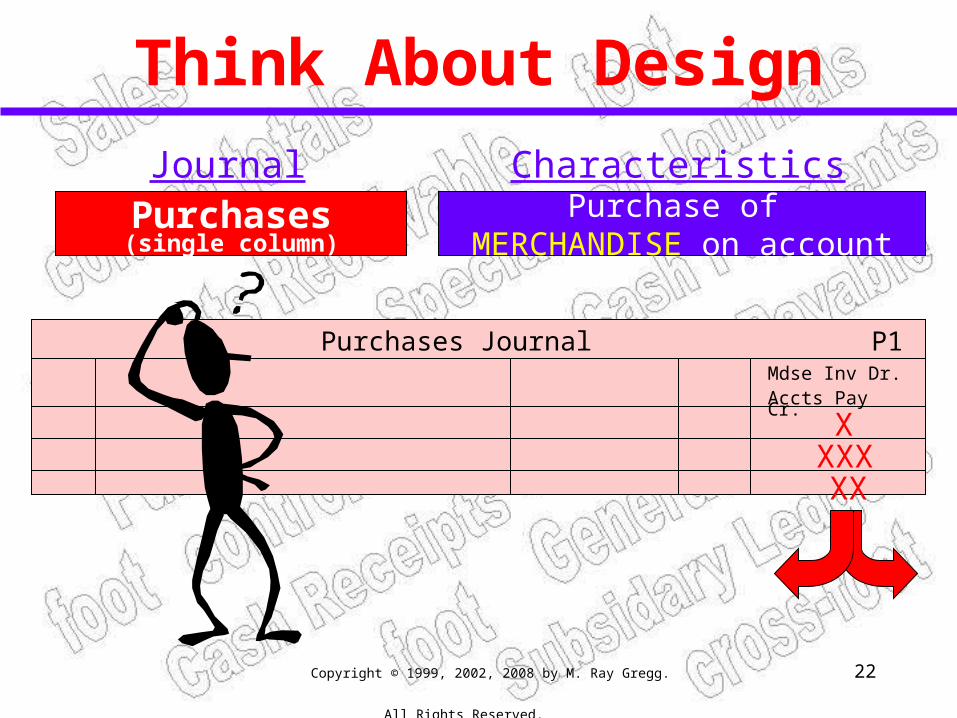

Think About Design

Purchases(single column)

Purchase of MERCHANDISE on account

Journal Characteristics

Purchases Journal P1Mdse Inv Dr.Accts Pay Cr.

XXXXXX

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 23

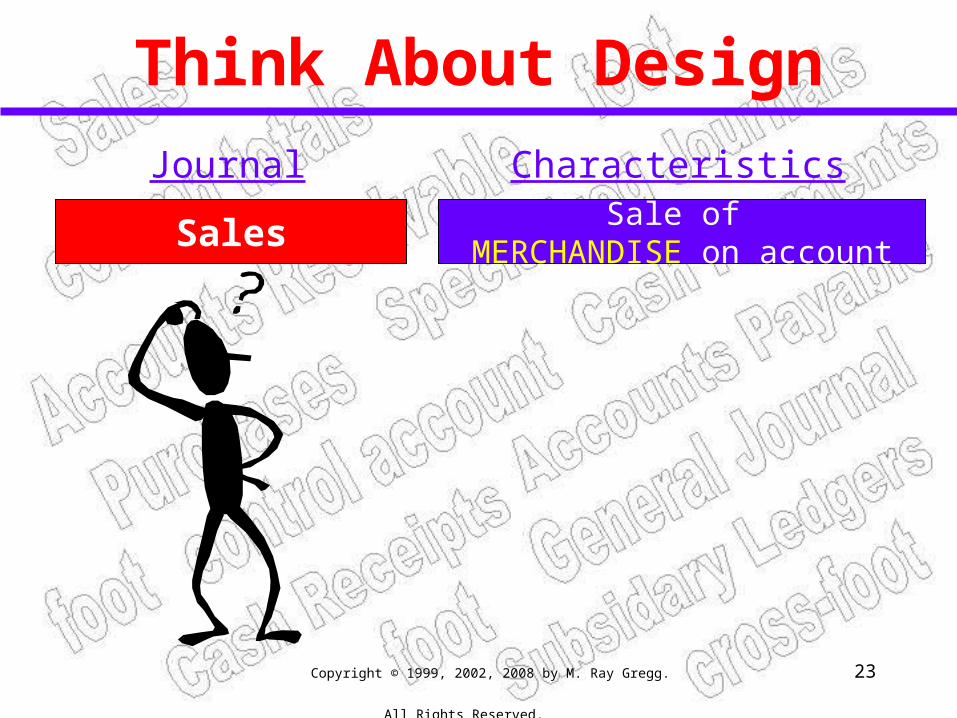

Think About Design

Sales Sale of MERCHANDISE on account

Journal Characteristics

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 24

Think About Design

Cash Receipts ANY collection of cash

Journal Characteristics

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 25

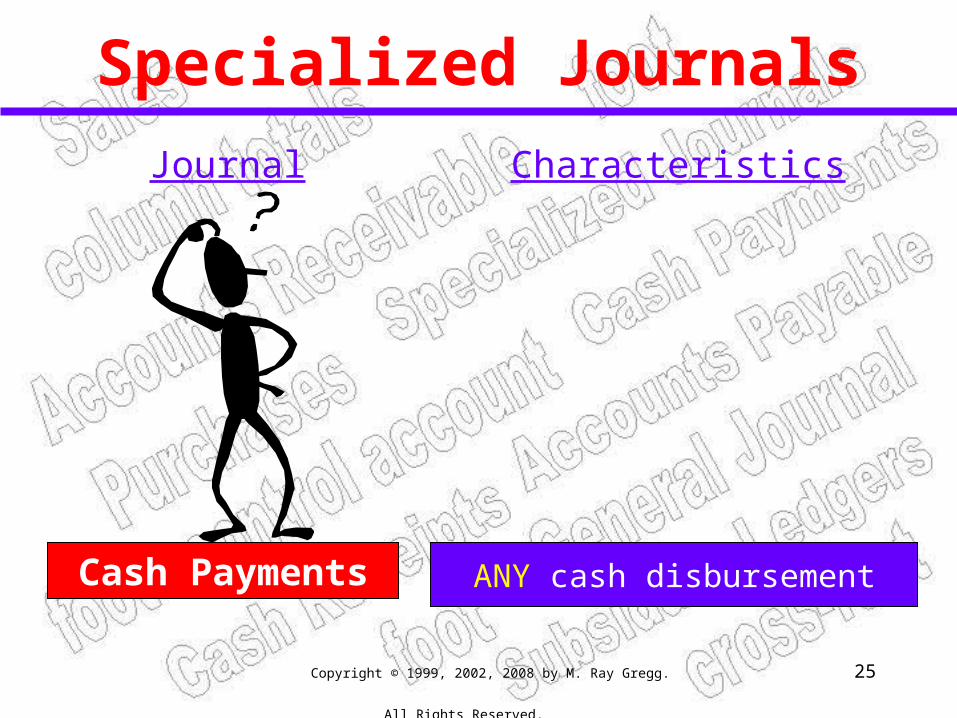

Specialized Journals

Cash Payments ANY cash disbursement

Journal Characteristics

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 26

Caution!

Please continue to THINK in “two column” or “General Journal” format.

We will ALWAYS record our entries in “General Journal” format.

Caution

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 27

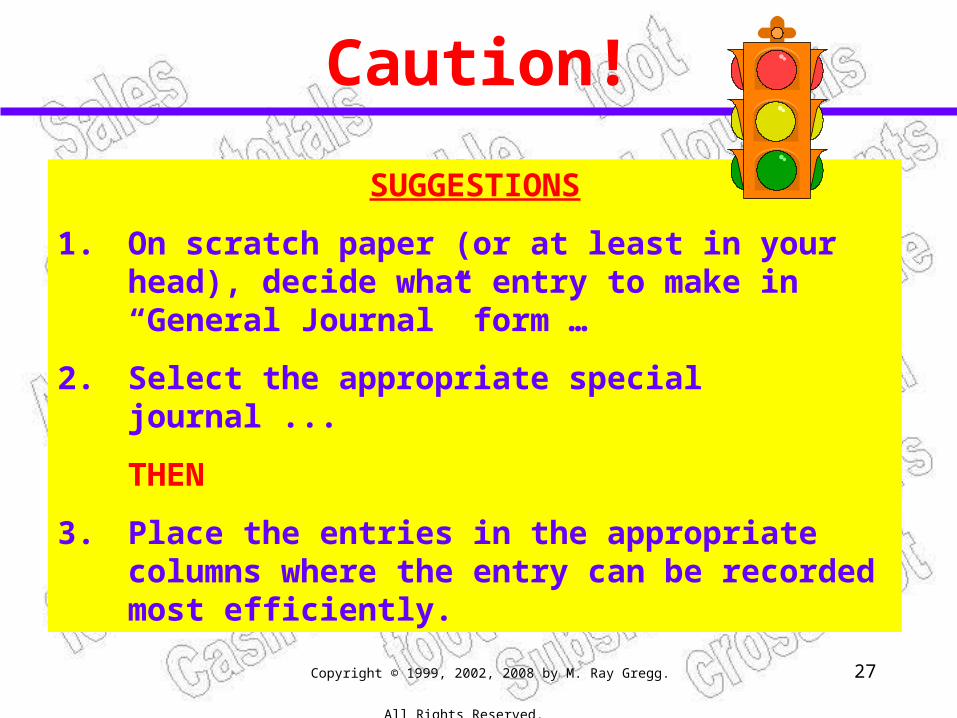

Caution!

SUGGESTIONS

1. On scratch paper (or at least in your head), decide what entry to make in “General Journal” form …

2. Select the appropriate special journal ...

THEN

3. Place the entries in the appropriate columns where the entry can be recorded most efficiently.

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 28

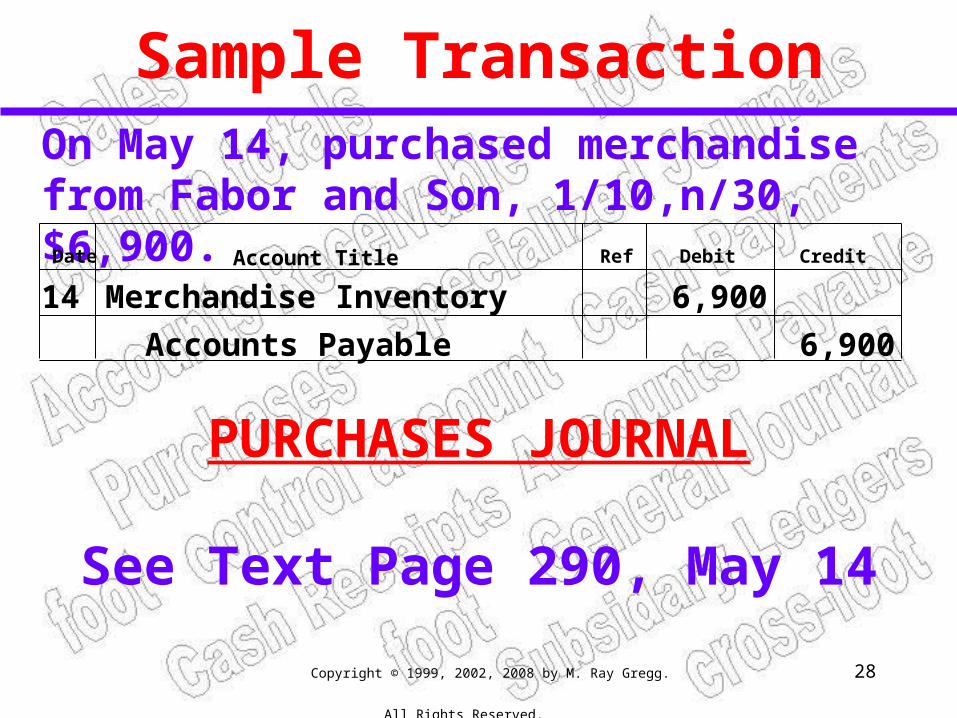

On May 14, purchased merchandise from Fabor and Son, 1/10,n/30, $6,900.

Sample Transaction

Date Account Title Ref Debit Credit

Merchandise Inventory 6,900

6,900Accounts Payable

14

PURCHASES JOURNAL

See Text Page 290, May 14

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 29

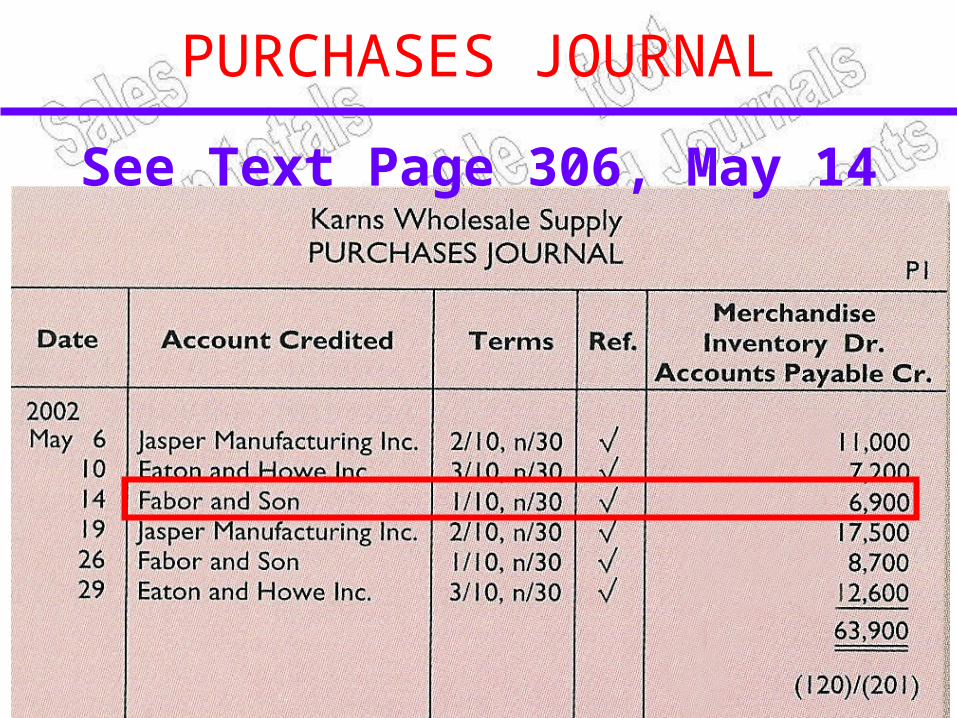

Purchases Journal P1

Date Account Credited Terms Ref

Fabor & Son14

Mdse Inv Dr.Accts Pay Cr.

1/10,n/30 6,900

PURCHASES JOURNAL

See Text Page 306, May 14

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 30

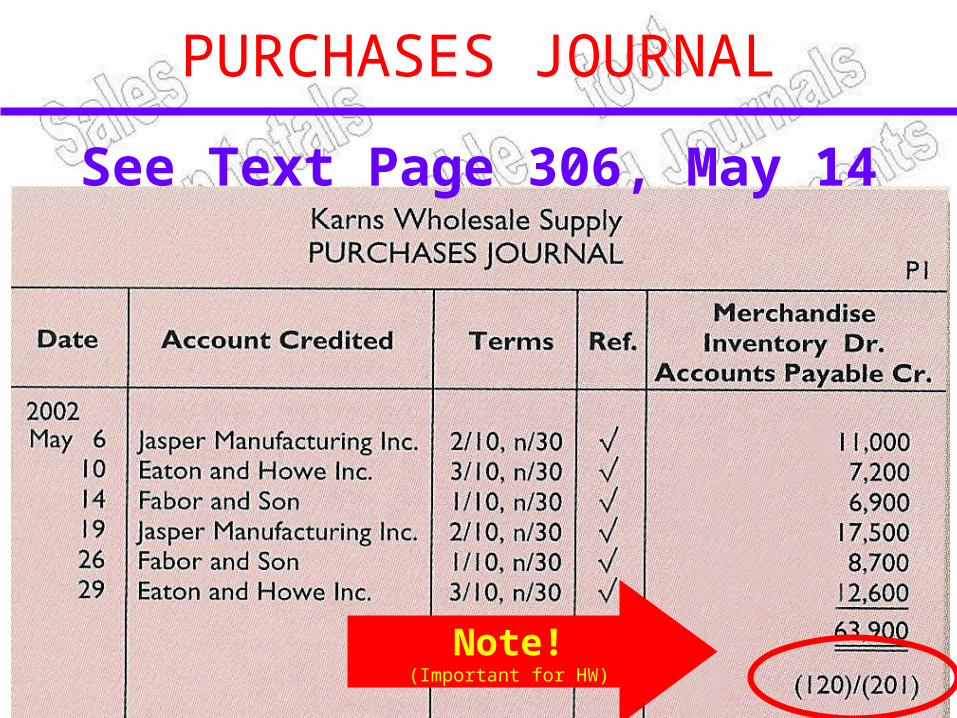

Purchases Journal P1

Date Account Credited Terms Ref

Fabor & Son14

Mdse Inv Dr.Accts Pay Cr.

1/10,n/30 6,900

PURCHASES JOURNAL

See Text Page 306, May 14

Note!(Important for HW)

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 31

Purchases Journal P1

Date Account Credited Terms Ref

Fabor & Son14

Mdse Inv Dr.Accts Pay Cr.

1/10,n/30 6,900

On May 14, purchased merchandise from Fabor and Son, 1/10,n/30, $6,900.

Comparison

Date Account Title Ref Debit Credit

Merchandise Inventory 6,900

6,900Accounts Payable

14

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 32

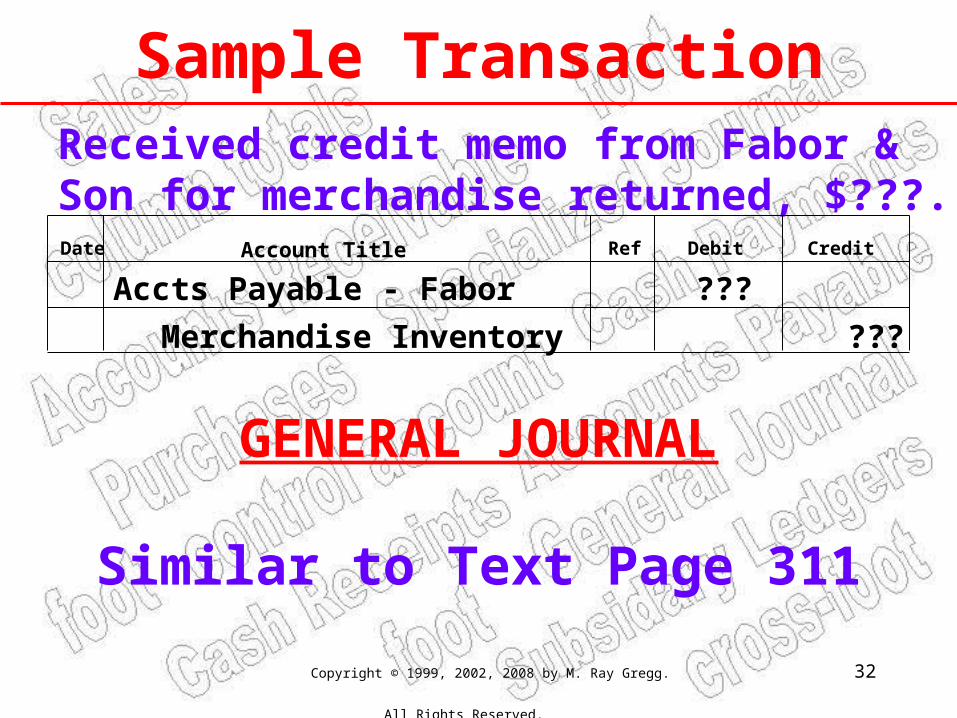

Sample TransactionReceived credit memo from Fabor & Son for merchandise returned, $???.

Date Account Title Ref Debit Credit

Merchandise Inventory

???Accts Payable - Fabor

???

GENERAL JOURNAL

Similar to Text Page 311

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 33

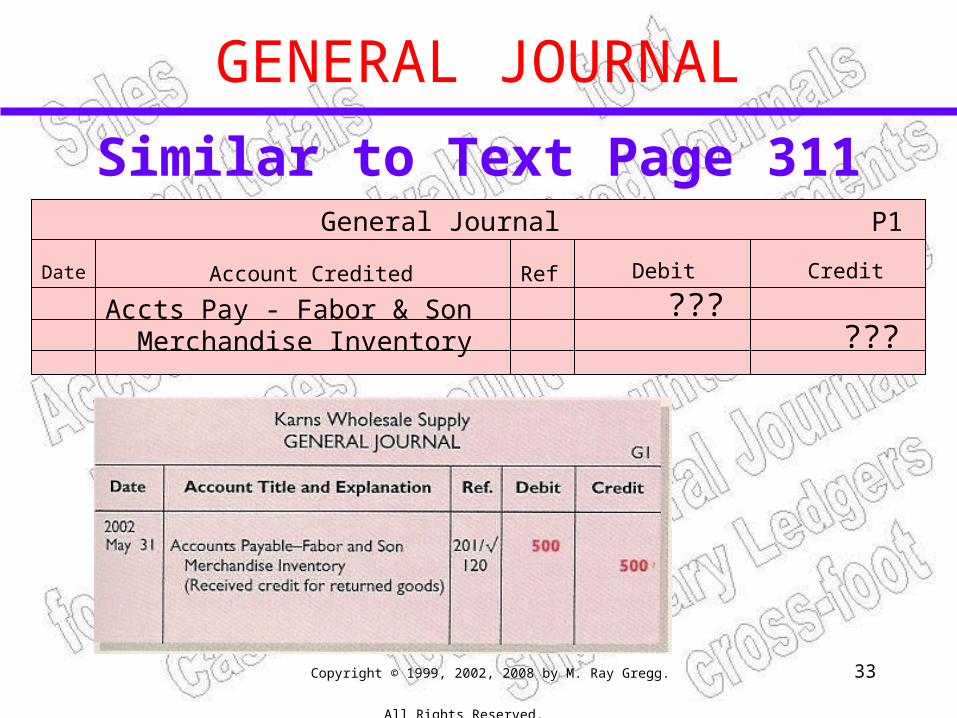

GENERAL JOURNAL

Similar to Text Page 311General Journal P1

Date Account Credited Ref

Accts Pay - Fabor & Son

Debit

???Merchandise Inventory

Credit

???

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 34

ComparisonReceived credit memo from Fabor & Son for merchandise returned, $???. Date Account Title Ref Debit Credit

Merchandise Inventory

???Accounts Payable

???

General Journal P1

Date Account Credited Ref

Accts Pay - Fabor & Son

Debit

???Merchandise Inventory

Credit

???

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 35

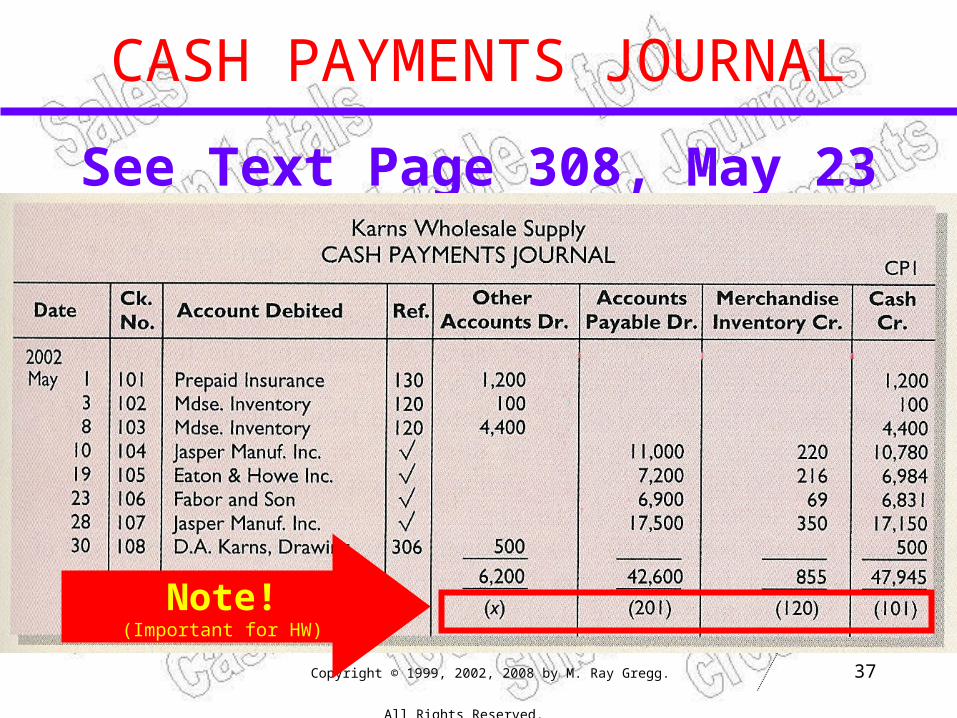

On May 23, paid Fabor and Son the amount due on the May 14 invoice.(Note: in the text example, the credit memo related to a different transaction.)

Sample Transaction

CASH PAYMENTS JOURNALSee Text Page 308, May 23

69

Date Account Title Ref Debit Credit

Merchandise Inventory

6,900Accts Pay - Fabor & Son

Cash 6,831

23

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 36

CASH PAYMENTS JOURNAL

See Text Page 308, May 23Cash Payments Journal CP1

Date Account Debited Ref

Fabor & Son

CashCr.

6,83123 106

Ck.No.

Other

Accounts

Dr.

AccountsPayable

Dr.

MdseInventory

Cr.

696,900

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 37

CASH PAYMENTS JOURNAL

See Text Page 308, May 23Cash Payments Journal CP1

Date Account Debited Ref

Fabor & Son

CashCr.

6,83123 106

Ck.No.

Other

Accounts

Dr.

AccountsPayable

Dr.

MdseInventory

Cr.

696,900

Note!(Important for HW)

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 38

Cash Payments Journal CP1

Date Account Debited Ref

Fabor & Son

CashCr.

6,83123 106

Ck.No.

Other

Accounts

Dr.

AccountsPayable

Dr.

MdseInventory

Cr.

696,900

On May 23, paid Fabor and Son the amount due on the May 14 invoice.(Note: in the text example, the credit memo related to a different transaction.)

Comparison

Date Account Title Ref Debit Credit

Merchandise Inventory

6,900

69

Accts Pay - Fabor & Son

Cash 6,831

23

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 39

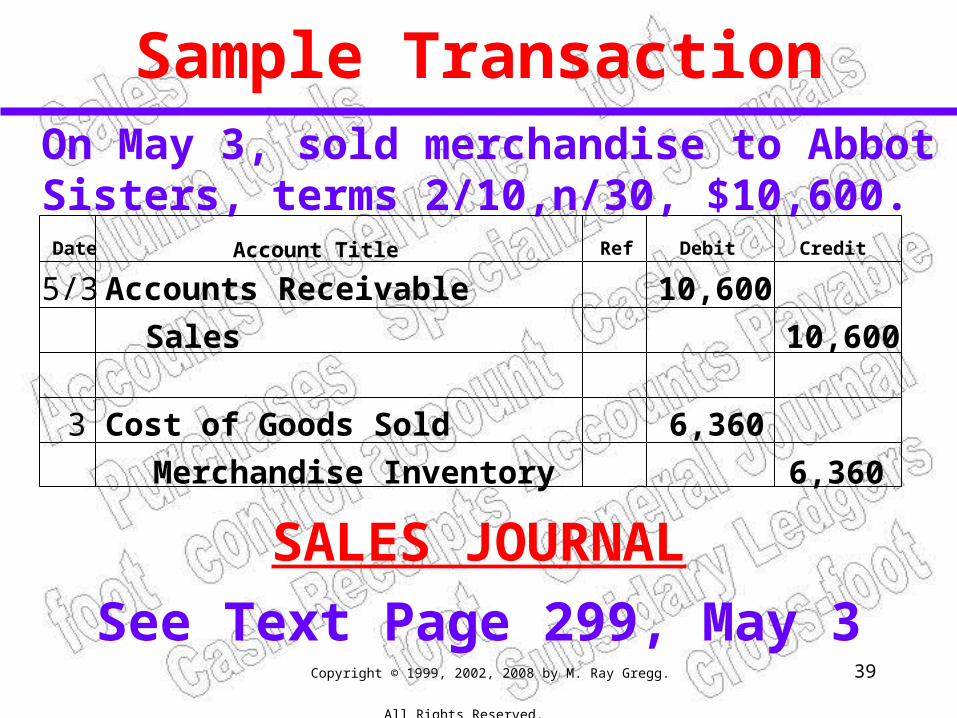

On May 3, sold merchandise to Abbot Sisters, terms 2/10,n/30, $10,600.

Sample Transaction

SALES JOURNAL

See Text Page 299, May 3

Date Account Title Ref Debit Credit

Accounts Receivable 10,600

10,600Sales

5/3

Cost of Goods Sold

Merchandise Inventory

6,360

6,360

3

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 40

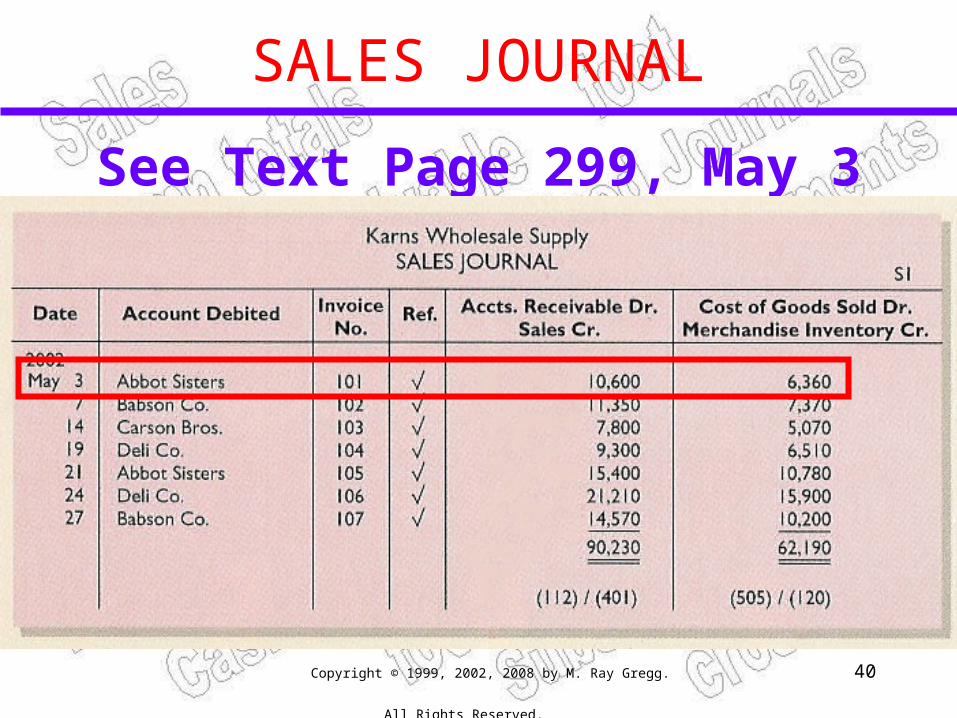

SALES JOURNAL

See Text Page 299, May 3Sales Journal S1

Date Account Debited Ref

Abbot Sisters

COGS Dr.Mdse Inv Cr.

6,3605/3

InvoiceNo.

Accts Rec Dr.Sales Cr.

10,600

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 41

SALES JOURNAL

See Text Page 299, May 3Sales Journal S1

Date Account Debited Ref

Abbot Sisters

COGS Dr.Mdse Inv Cr.

6,3605/3

InvoiceNo.

Accts Rec Dr.Sales Cr.

10,600

Note!(important for HW)

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 42

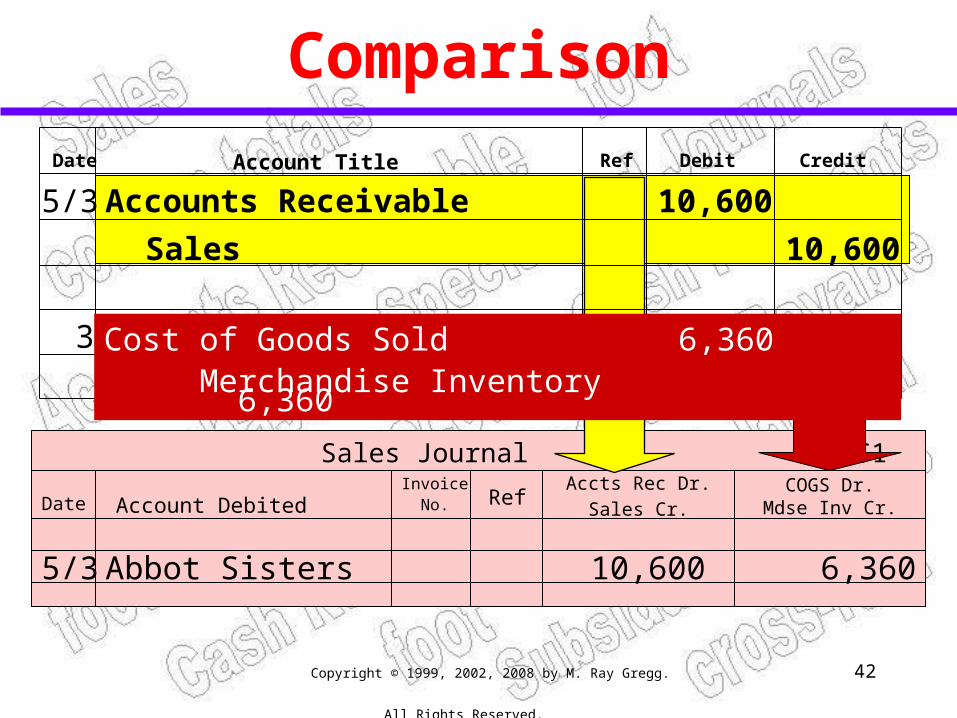

Comparison

Sales Journal S1

Date Account Debited Ref

Abbot Sisters

COGS Dr.Mdse Inv Cr.

6,3605/3

InvoiceNo.

Accts Rec Dr.Sales Cr.

10,600

Accounts Receivable 10,600

10,600Sales

Date Account Title Ref Debit Credit

Cost of Goods Sold

Merchandise Inventory

6,360

6,360

5/3

3 Cost of Goods Sold 6,360 Merchandise Inventory 6,360

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 43

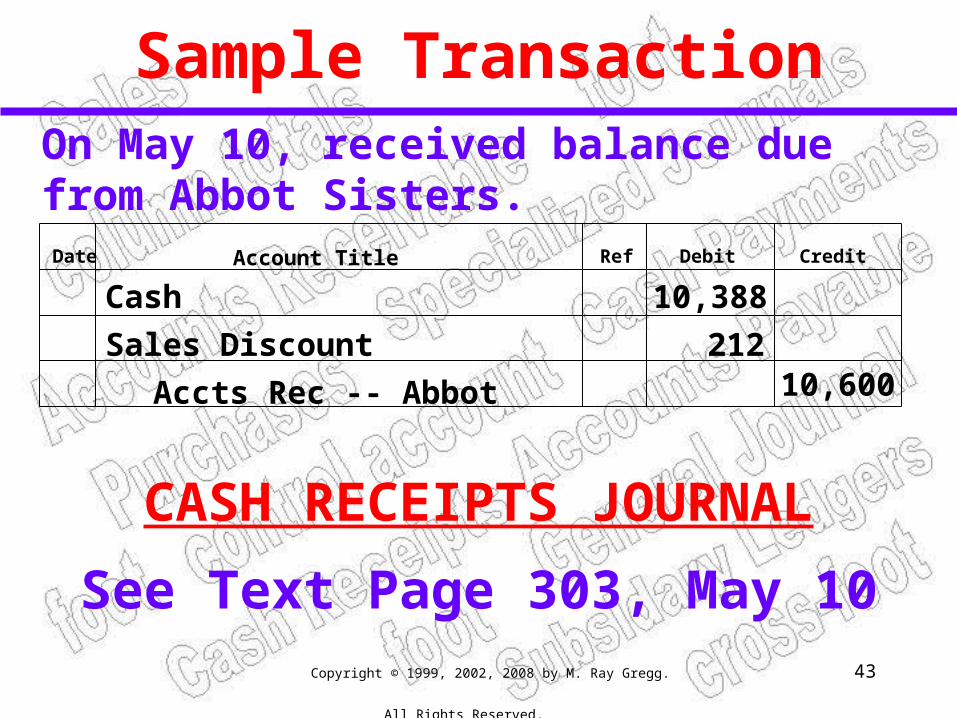

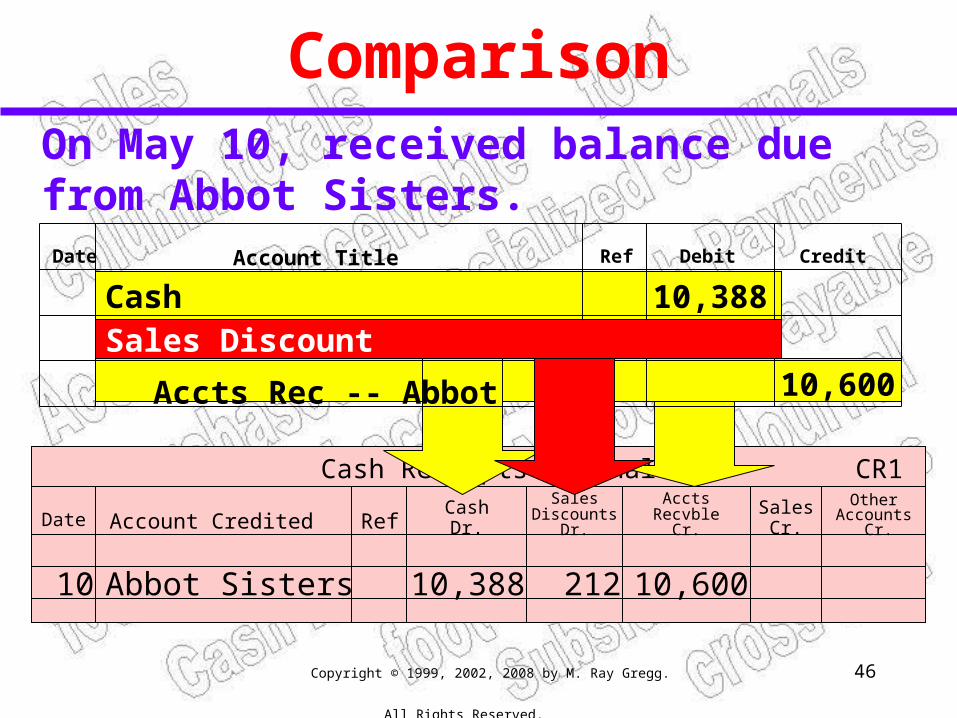

On May 10, received balance due from Abbot Sisters.

Sample Transaction

CASH RECEIPTS JOURNAL

See Text Page 303, May 10

Date Account Title Ref Debit Credit

Sales Discount

10,388

212

Cash

Accts Rec -- Abbot 10,600

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 44

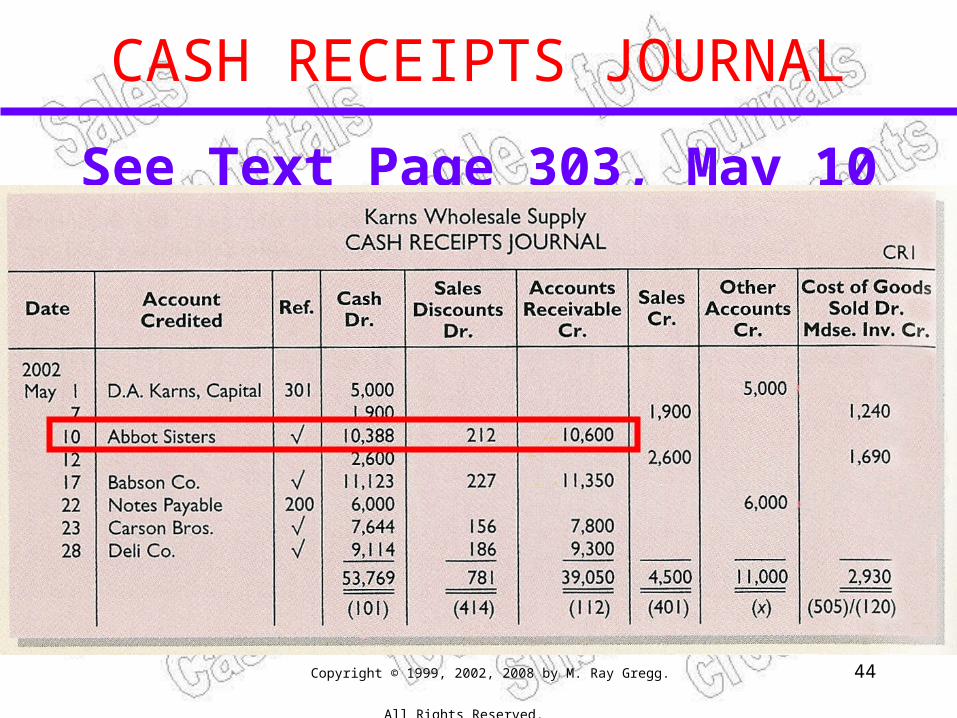

CASH RECEIPTS JOURNAL

See Text Page 303, May 10Cash Receipts Journal CR1

Date Account Credited Ref

Abbot Sisters

OtherAccounts

Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

10,600

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 45

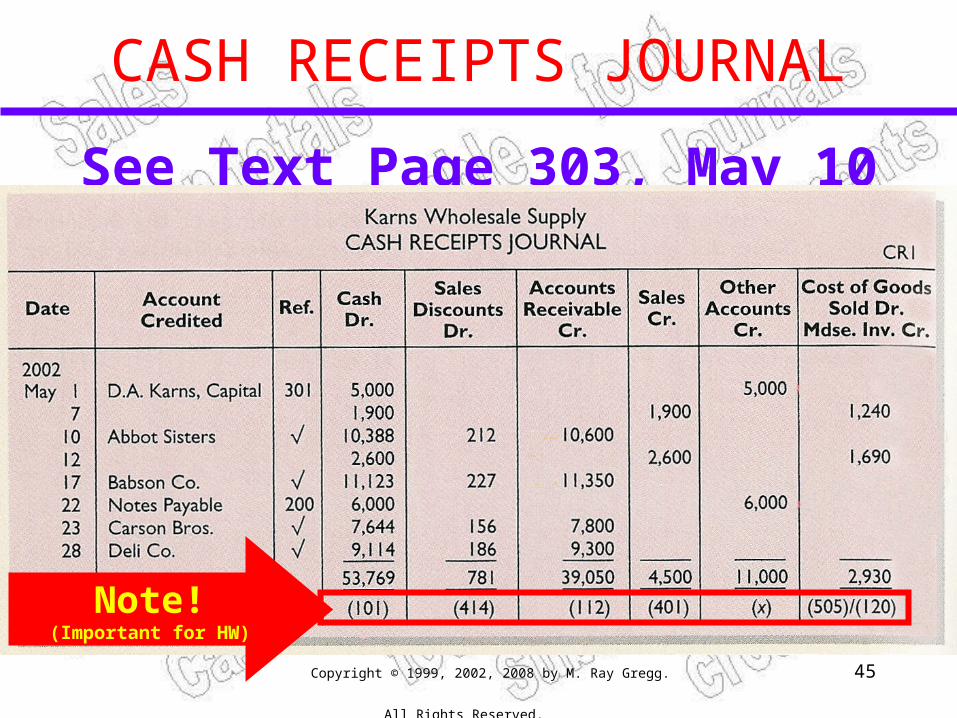

CASH RECEIPTS JOURNAL

See Text Page 303, May 10Cash Receipts Journal CR1

Date Account Credited Ref

Abbot Sisters

OtherAccounts

Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

10,600

Note!(Important for HW)

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 46

Cash Receipts Journal CR1

Date Account Credited Ref

Abbot Sisters

OtherAccounts

Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

10,600

On May 10, received balance due from Abbot Sisters.

Comparison

Date Account Title Ref Debit Credit

Sales Discount

10,388

212

Cash

Accts Rec -- Abbot 10,600Sales Discount 212

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 47

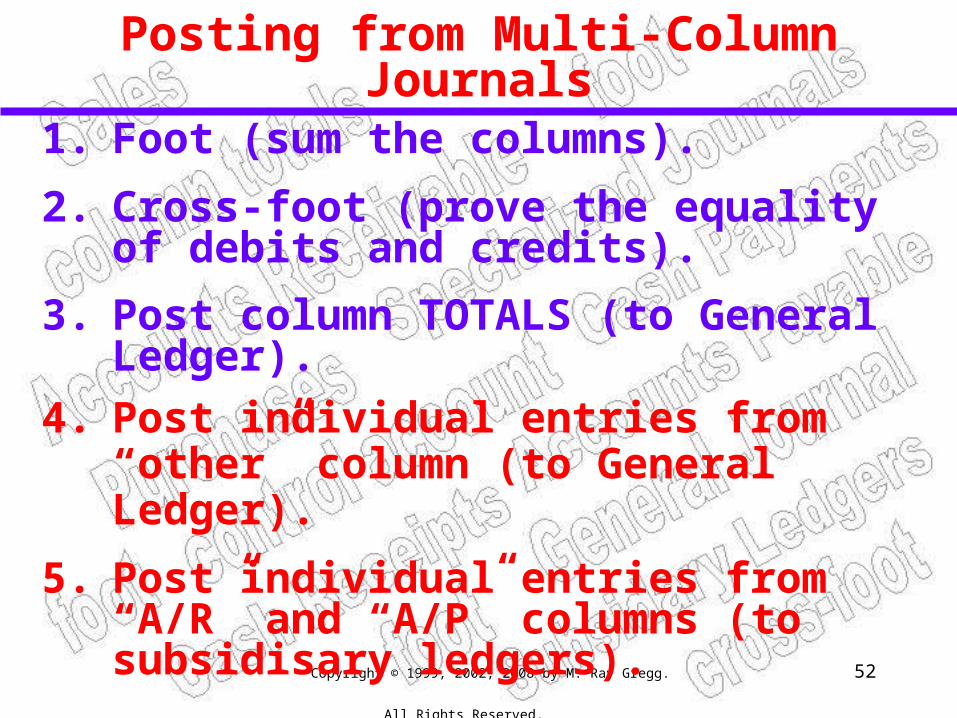

1. Foot (sum the columns).

Posting from Multi-Column Journals

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 48

1. Foot (sum the columns).

2. Cross-foot (prove the equality of debits and credits).

Posting from Multi-Column Journals

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 49

1. Foot (sum the columns).

2. Cross-foot (prove the equality of debits and credits.

Posting from Multi-Column Journals

3. Post column TOTALS (to General Ledger).

Rule: Post columntotals ONLY!

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 50

1. Foot (sum the columns).

2. Cross-foot (prove the equality of debits and credits.

Posting from Multi-Column Journals

3. Post column TOTALS (to General Ledger).

Anyexceptions?

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 51

1. Foot (sum the columns).

2. Cross-foot (prove the equality of debits and credits.

Posting from Multi-Column Journals

3. Post column TOTALS (to General Ledger).

Yes.Two.

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 52

1. Foot (sum the columns).

2. Cross-foot (prove the equality of debits and credits).

3. Post column TOTALS (to General Ledger).

Posting from Multi-Column Journals

4. Post individual entries from “other” column (to General Ledger).

5. Post individual entries from “A/R” and “A/P” columns (to subsidisary ledgers).

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 53

Posting from Multi-Column Journals

Cash Receipts Journal CR1

Date Account Credited Ref

Abbot Sisters

OtherAccounts

Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

10,600

5/1 Karns,Capital 5,000 5,000

7 Cash Sales 1,900 1,900

12 Cash Sales 2,600 2,600

Babson Co. 22717 11,123 11,350 22 Notes Payable 6,000 6,000

43937,011 21,950 4,500 11,000

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 54

.

Posting from Multi-Column Journals

Cash Receipts Journal CR1

Date Account Credited Ref

Abbot Sisters

OtherAccounts

Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

10,600

5/1 Karns,Capital 5,000 5,000

7 Cash Sales 1,900 1,900

12 Cash Sales 2,600 2,600

Babson Co. 22717 11,123 11,350 22 Notes Payable 6,000 6,000

43937,011 21,950 4,500 11,000

Drs.

Crs.

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 55

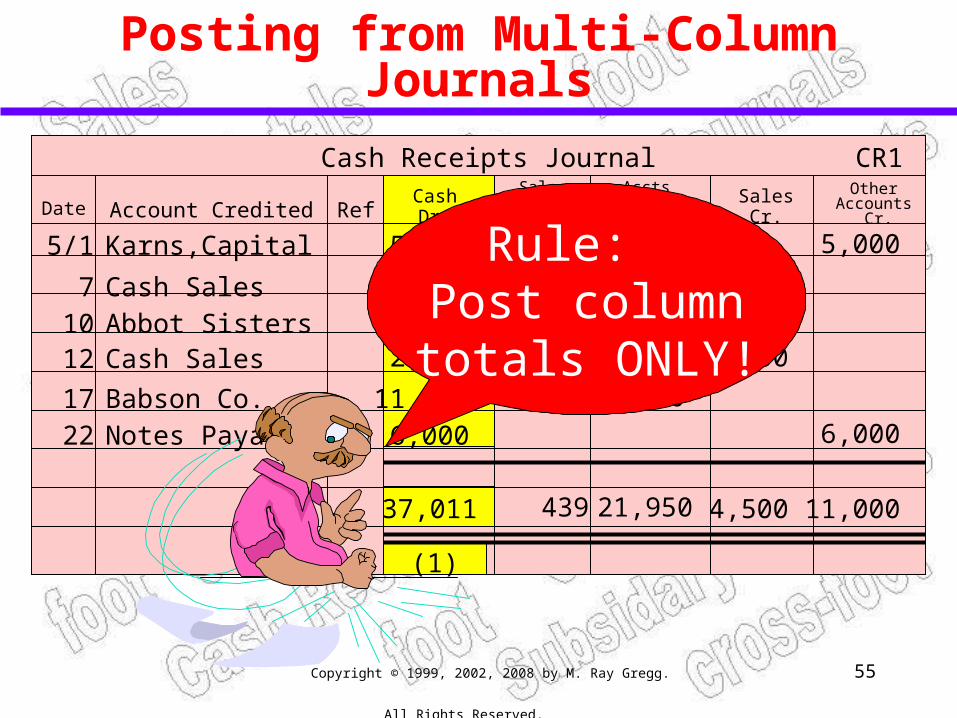

Posting from Multi-Column Journals

Cash Receipts Journal CR1

Date Account Credited Ref

Abbot Sisters

OtherAccounts

Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

10,600

5/1 Karns,Capital 5,000 5,000

7 Cash Sales 1,900 1,900

12 Cash Sales 2,600 2,600

Babson Co. 22717 11,123 11,350 22 Notes Payable 6,000 6,000

43937,011 21,950 4,500 11,000

(1)

Rule: Post columntotals ONLY!

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 56

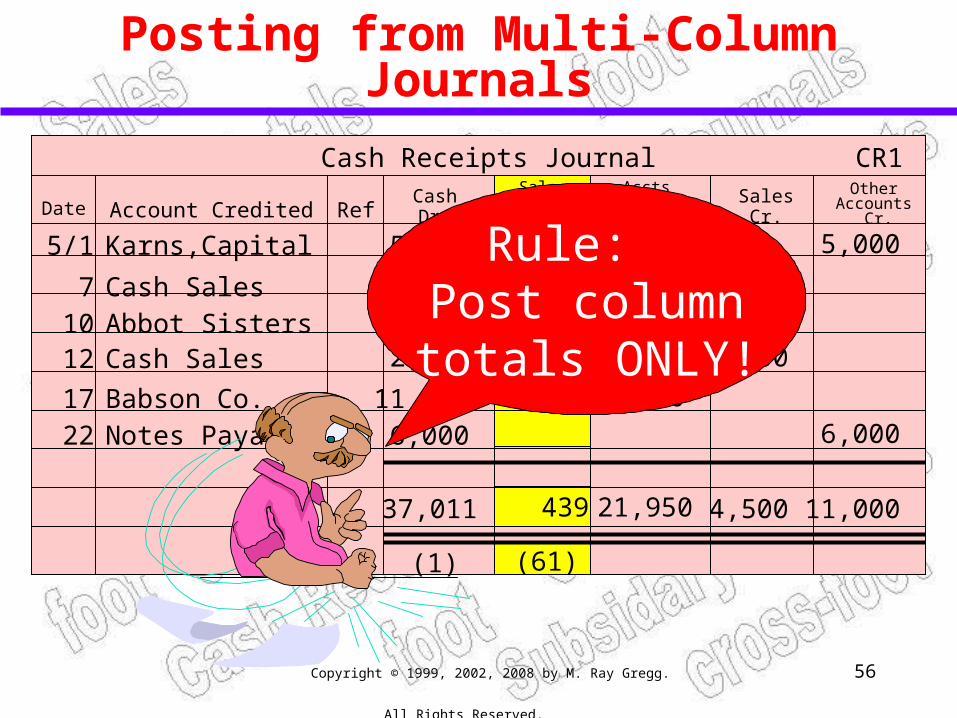

Posting from Multi-Column Journals

Cash Receipts Journal CR1

Date Account Credited Ref

Abbot Sisters

OtherAccounts

Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

10,600

5/1 Karns,Capital 5,000 5,000

7 Cash Sales 1,900 1,900

12 Cash Sales 2,600 2,600

Babson Co. 22717 11,123 11,350 22 Notes Payable 6,000 6,000

43937,011 21,950 4,500 11,000

(61)(1)

Rule: Post columntotals ONLY!

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 57

Abbot Sisters 10,600

Posting from Multi-Column Journals

Cash Receipts Journal CR1

Date Account Credited RefOther

Accounts Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

5/1 Karns,Capital 5,000 5,000

7 Cash Sales 1,900 1,900

12 Cash Sales 2,600 2,600

Babson Co. 22717 11,123 11,350 22 Notes Payable 6,000 6,000

43937,011 21,950 4,500 11,000

(61)(1)

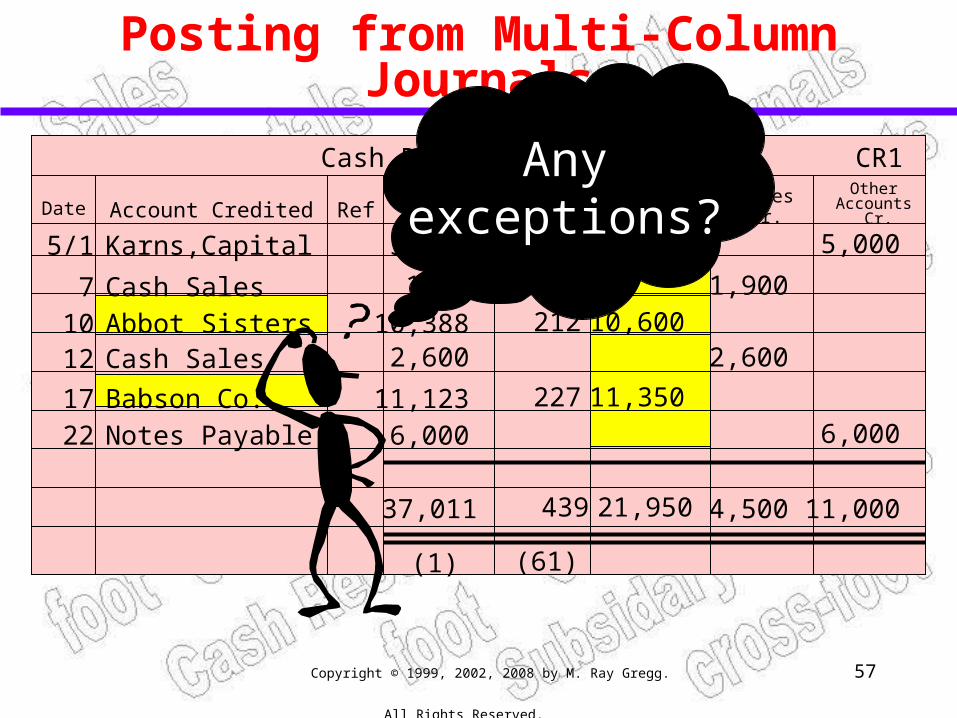

Anyexceptions?

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 58

Abbot Sisters 10,600

Posting from Multi-Column Journals

Cash Receipts Journal CR1

Date Account Credited RefOther

Accounts Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

5/1 Karns,Capital 5,000 5,000

7 Cash Sales 1,900 1,900

12 Cash Sales 2,600 2,600

Babson Co. 22717 11,123 11,350 22 Notes Payable 6,000 6,000

43937,011 21,950 4,500 11,000

(61)(1)

To A/RSubsidiary

Ledger

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 59

General Ledger Details

Must Postto BOTH!

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 60

Abbot Sisters 10,600

Posting from Multi-Column Journals

Cash Receipts Journal CR1

Date Account Credited RefOther

Accounts Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

5/1 Karns,Capital 5,000 5,000

7 Cash Sales 1,900 1,900

12 Cash Sales 2,600 2,600

Babson Co. 22717 11,123 11,350 22 Notes Payable 6,000 6,000

43937,011 21,950 4,500 11,000

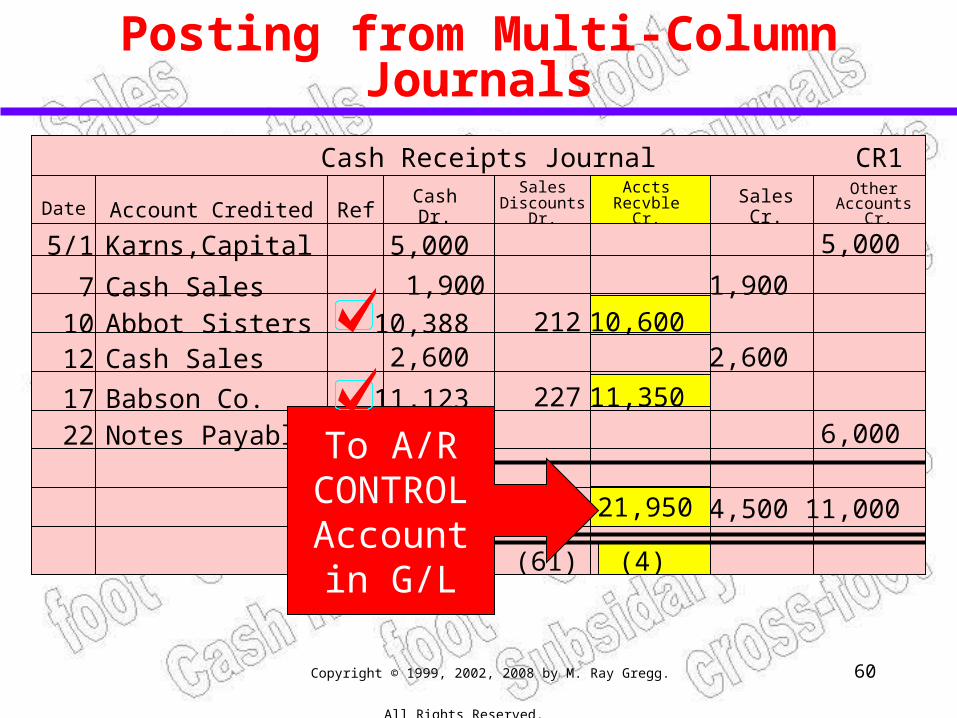

(61)(1) (4)

To A/RCONTROLAccountin G/L

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 61

Posting from Multi-Column Journals

Cash Receipts Journal CR1

Date Account Credited Ref

Abbot Sisters

OtherAccounts

Cr.

21210

CashDr.

10,388

SalesDiscounts

Dr.SalesCr.

AcctsRecvble

Cr.

10,600

5/1 Karns,Capital 5,000 5,000

7 Cash Sales 1,900 1,900

12 Cash Sales 2,600 2,600

Babson Co. 22717 11,123 11,350 22 Notes Payable 6,000 6,000

43937,011 21,950 4,500 11,000

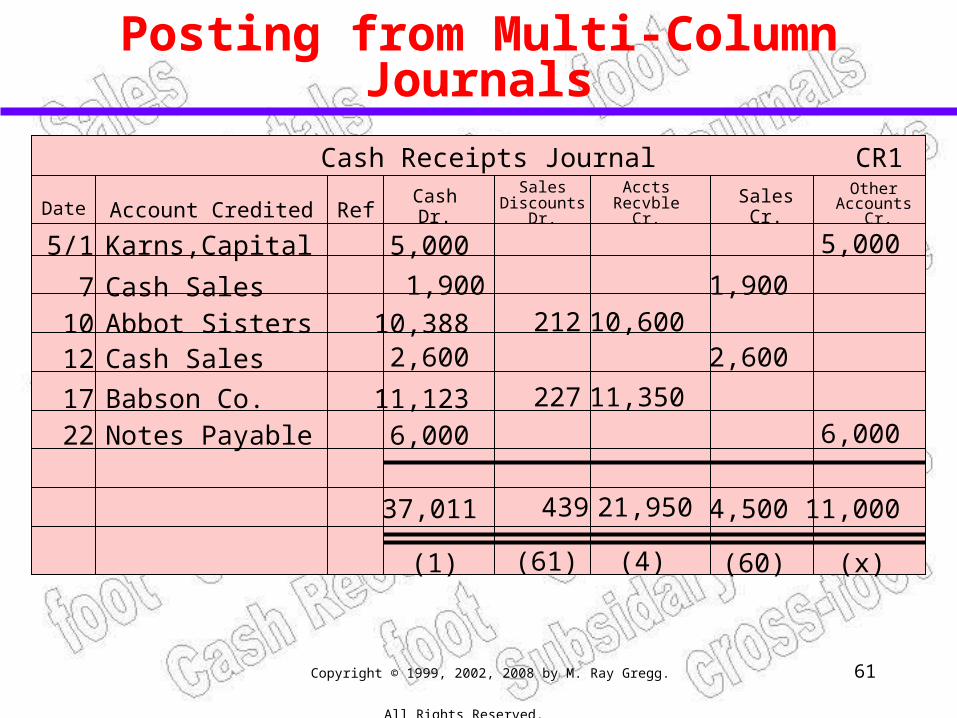

(61)(1) (4) (60) (x)

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 62

Rule: Post columntotals ONLY!

Copyright © 1999, 2002, 2008 by M. Ray Gregg.

All Rights Reserved. 63

…and have agood week

in accounting!