Accounting systems

35

ACCOUNTING SYSTEMS

-

Upload

drbinodini-dash -

Category

Economy & Finance

-

view

104 -

download

2

Transcript of Accounting systems

ACCOUNTING SYSTEMS

BASES OF ACCOUNTING

Cash Basis

Accrual Basis

CASH BASISActual cash receipts and actual cash

payments are recorded.

Credit transactions are not recorded at all until the cash is actually received or paid.

Ignores outstanding, prepaid expenses, accrued income, income received in

advance.

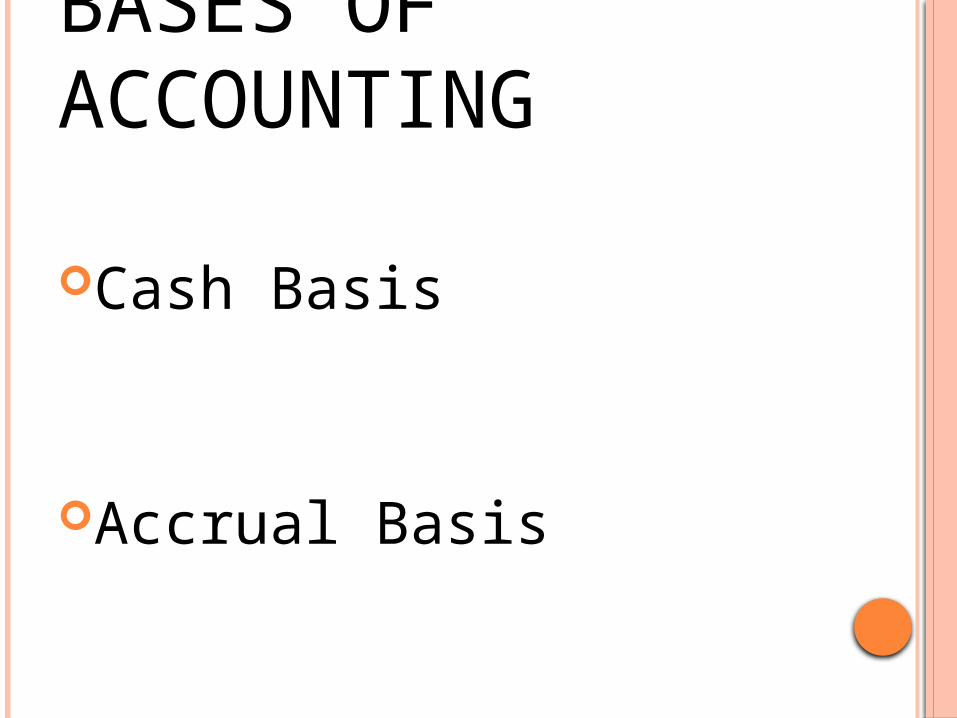

ACCRUAL BASISIncome if earned or

due(accrued) and cash paid or payment outstanding(due)

forms part of the period in which services have been given or received even if actual cash has not been

received or paid.

ACCRUAL BASIS VS CASH BASISAccrual Basis of

AccountingCash Basis of Accounting

1. Under this method there may be outstanding expenses, prepaid expenses, accrued income, income received in advance in the Balance Sheet

1. There is no outstanding or prepaid expenses, accrued income, income received in advance in the Balance Sheet

2. Income statement will show relatively higher income because of prepaid expenses and accrued income

2. Income statement will show lower income in case there are prepaid expenses and accrued income

3. Income statement will show relatively lower income because of outstanding expenses and income received in advance

3. Income statement will show higher income if there are items of outstanding expenses and income received in advance

Accrual Basis Cash Basis

4. The basis is recognized under the Companies Act 1956

4. The basis is not recognized under the Companies Act 1956

5. Depreciation is recorded 5. Depreciation cannot be recorded

6. Enterprises with cash and credit transactions prefer this basis

6. Enterprises with mostly cash transactions prefer this basis of accounting

7. Business enterprises with profit motive ascertain their profit or loss under this basis

Professional people like doctors, lawyers etc. and small non-trading concerns ascertain their profit or loss under cash basis

Accrual Basis Cash Basis

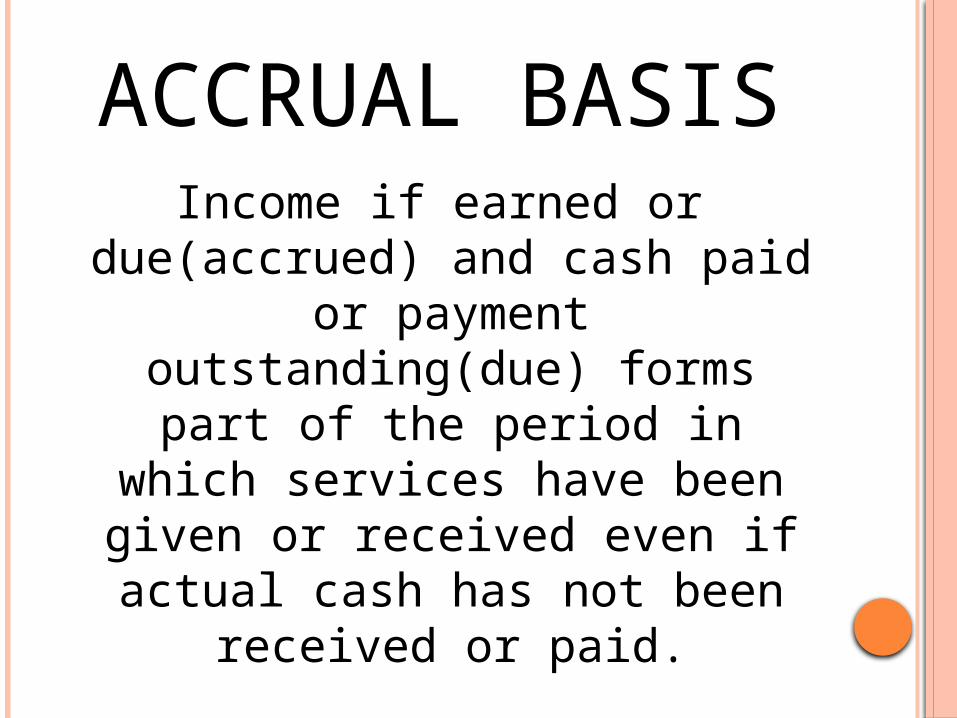

8. Reliable Basis as it makes a complete record of all cash and credit transactions and ascertains correct profit & loss

8. Not reliable

9. Is technical because it involves adjustments of accounts for preparing the final accounts

9. Simple basis

10. Basis gives a true and fair view of P&L for a particular period and exhibits true financial position of business on a particular day

10. Does not give true and fair view.

ACCOUNTING STANDARDSTo maintain uniformity in accounting

principles throughout the world, International Accounting Standards Committee (IASC) came into being on 29th June, 1973.

The Institute of Chartered Accountants of India(ICAI) being the premier accounting body in India has tried to improve its accounting and auditing standards continuously.

CONTINUED…ICAI set up Accounting Standard Board

(ASB) in 1977 whose main function is to formulate accounting standards so that the standards are established by the Council of the ICAI.

In the formulation and finalization of AS, the ASB seeks the views and guidance of members of ICAI, ICWAI, ICSI, Government, Industrial concerns are taken.

TASK OF ASB

RMPTDR=RecognitionM=MeasurementP=PresentationT=TreatmentD=Disclosure

CONTINUED… Areas (Eg: Fixed

Assets, Depreciation)

Definition

Class of enterprise

Date

Content

Exposure Draft

STANDARD

EXAMPLESAS 2: Inventory

AS 3: Cashflow

AS 6: Depreciation

AS 10: Fixed assets

CLASSIFICATION OF ACCOUNTS

An account is an individual

representation of assets, liabilities,

incomes or expenses

ACCOUNTS ARE OF TWO TYPES

Personal Account

Impersonal Account

PERSONAL ACCOUNTS ARE OF 3 TYPES

1. Natural Personal Account(Ram A/C, Hari A/C, Sangeeta A/C etc.)

2. Artificial Personal Account (Companies Eg: Vinod & Bros Co., etc, Bank)

3. Representative Personal Accounts (Outstanding Expenses, Prepaid expenses, Income received in advance, Accrued Income)

CONTINUED…

Any nominal account suffixed or prefixed

becomes a representative personal

account. Eg- Outstanding rent, Prepaid salary etc.

IMPERSONAL ACCOUNTS ARE OF 2 TYPES

Real Account (Assets)

Nominal Account(Expenses)

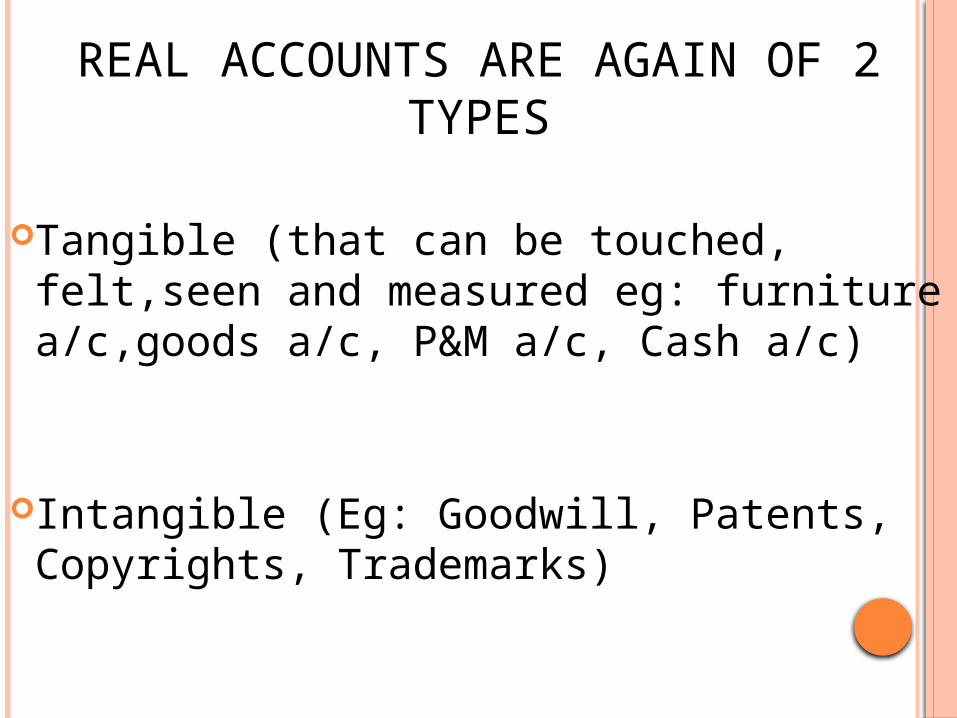

REAL ACCOUNTS ARE AGAIN OF 2 TYPES

Tangible (that can be touched, felt,seen and measured eg: furniture a/c,goods a/c, P&M a/c, Cash a/c)

Intangible (Eg: Goodwill, Patents, Copyrights, Trademarks)

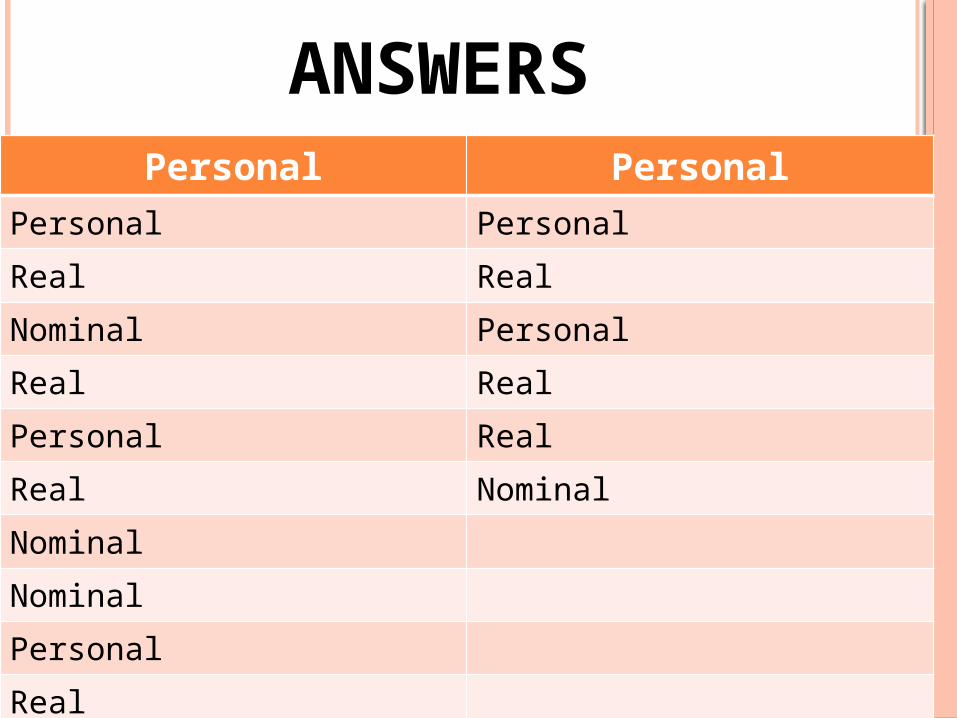

IDENTIFY THE TYPE OF ACCOUNTS BELOW

DrawingsBankCash DiscountPatent Arihant Industries LtdGoodwillSalariesBad DebtsCapital

MachinerySalary OutstandingUnexpired Insurance/Prepaid InsuranceStock AccountBank OverdraftPurchasesBills ReceivableReserve for Discount on creditors

ANSWERSPersonal Personal

Personal Personal

Real Real

Nominal Personal

Real Real

Personal Real

Real Nominal

Nominal

Nominal

Personal

Real

THERE ARE TWO SYSTEMS OF ACCOUNTING

Single Entry System: Only personal accounts are maintained. It does not record complete business transactions during a specified period. Hence final accounts cannot be prepared. It is less costly system and is adopted by small business concerns where business transactions are few.

Double Entry System: Owes its origin to Fra Luca Pacioli. All business transactions have two sides i.e receipt and payment. Eg: Purchase of goods. This method of recording every transaction in two accounts is known as Double Entry system. One account is debited and the other is credited with the same amount

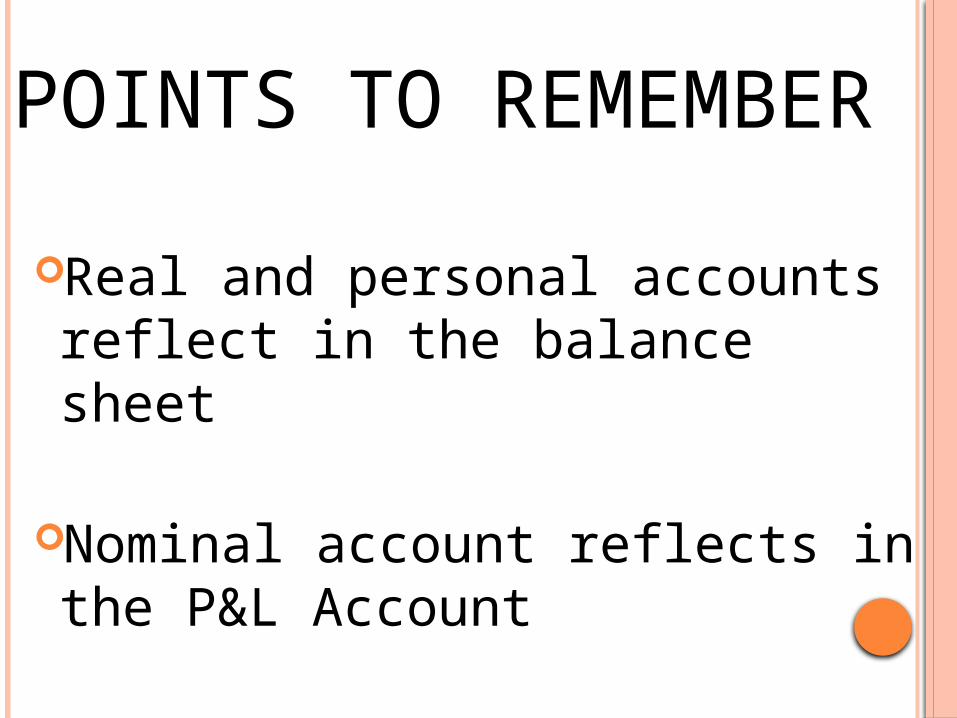

POINTS TO REMEMBER

Real and personal accounts reflect in the balance sheet

Nominal account reflects in the P&L Account

WHAT IS AN ASSET?Resources owned by a company which

have future economic value that can be measured and can be expressed in monetary terms.

Examples: cash, investments, accounts receivable, inventory, supplies, land, buildings, equipment, and vehicles.

Anything which has an income generating ability and is a property owned by the organization.

WHAT IS A LIABILITY?Where the company is liable to pay outsiders

Obligations of a company or organization.

Eg: Amounts owed to lenders and suppliers, income received in advance, loan,creditors, outstanding expenses

Liabilities often have the word "payable" in the account title.

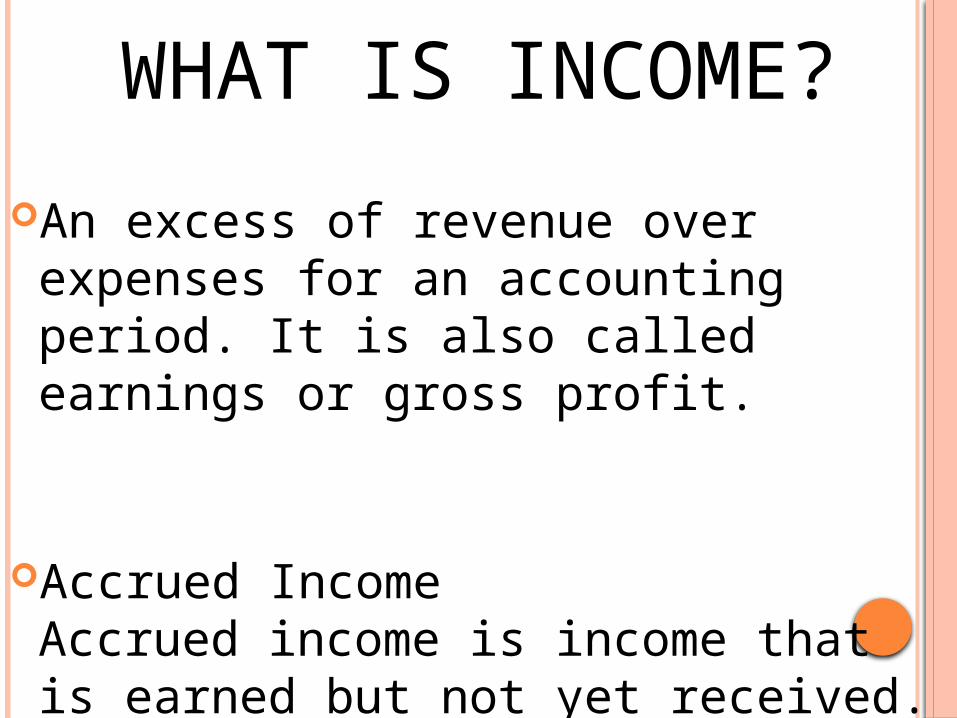

WHAT IS INCOME?

An excess of revenue over expenses for an accounting period. It is also called earnings or gross profit.

Accrued Income Accrued income is income that is earned but not yet received.

ACCRUED EXPENSES/OUTSTANDING

EXPENSES

Accrued expenses are those expenses which

have been incurred but not paid.

WHAT IS EXPENSE?

Expense is any amount paid by the organisation the benefit of which has already been exhausted.

Costs that have been consumed in the process of producing revenue are expired costs or expenses.

Example: Insurance, Wages, Advertising, Interest .

Expense is different from

Loss

WHAT IS REVENUE?1. Revenue results from the sale of

goods and rendering of services.

2. Revenue is the increase in capital attributable to business activities.

3. Net income can be calculated by subtracting expenses from revenue

REVENUE VS GAIN VS INCOME.

Revenue is the amount earned from a company’s main activities such as selling merchandise or providing services.

A gain results from secondary activities, such as selling the old delivery truck. A gain is the amount received that is in excess of the asset’s carrying amount (book value). For example, if the company receives Rs 3,000 for the truck, and its carry amount was Rs 600, the company will report a gain of Rs 2,400.

CONTINUED…Income is sometimes used instead of the word revenue.

Generally, accountants use the word income to mean “net of revenues and expenses.” For example, a retailer’s income from operations is sales minus the cost of goods sold minus other expenses.

WHAT IS EXPENDITURE?

Expenditure is the amount incurred by the organization the

benefit of which is yet to be exhausted.

Eg: P&M, L&B, Furniture etc.

WHAT IS CAPITAL?1. Cash or goods used to generate income

either by investing in a business or a different income property.

2. The net worth of a business or the amount by which its assets exceed its liabilities.

3. The money, property, and other valuables which collectively represent the wealth of an individual or business.

WHAT IS MEANT BY DEFERRED REVENUE EXPENDITURE?

The expenditure done in the initial stage but the benefit of which will also be available in subsequent years is called deferred revenue expenditure.

Eg: Advertisement

Thanks