Week 9 Accounting Information Systems Romney and Steinbart Linda Batch March 2012.

date post

19-Dec-2015Category

view

225download

1

Accounting Information Accounting Information Systems: An OverviewSystems: An Overview

Professor MartinProfessor MartinProfessor XiongProfessor Xiong

CSUSCSUS

This lecture is based primarily on Romney & This lecture is based primarily on Romney & Steinbart(2003). It also draws on Martin (2002).Steinbart(2003). It also draws on Martin (2002).

Updated on: Monday, January 27, 2003Updated on: Monday, January 27, 2003

AgendaAgenda The Accounting Information The Accounting Information

System (AIS)System (AIS) Why study AIS?Why study AIS? The Role of AIS In the Value ChainThe Role of AIS In the Value Chain

What is information System?What is information System? A system is a set of two or more A system is a set of two or more

interrelated components that interact interrelated components that interact to achieve a goal.to achieve a goal.

Systems are almost always Systems are almost always composed of smaller subsystems, composed of smaller subsystems, each performing a specific function each performing a specific function supportive of the larger system.supportive of the larger system.

Components of AISComponents of AIS PeoplePeople ProceduresProcedures DataData SoftwareSoftware Information technologyInformation technology

AIS FunctionsAIS Functions• Collect and store data about activities and transactionsCollect and store data about activities and transactions

• Transaction Processing Systems Transaction Processing Systems (TPS)(TPS)• Process data into information useful for making Process data into information useful for making

decisionsdecisions• Provide adequate controls to safeguard organization’s Provide adequate controls to safeguard organization’s

assetsassets

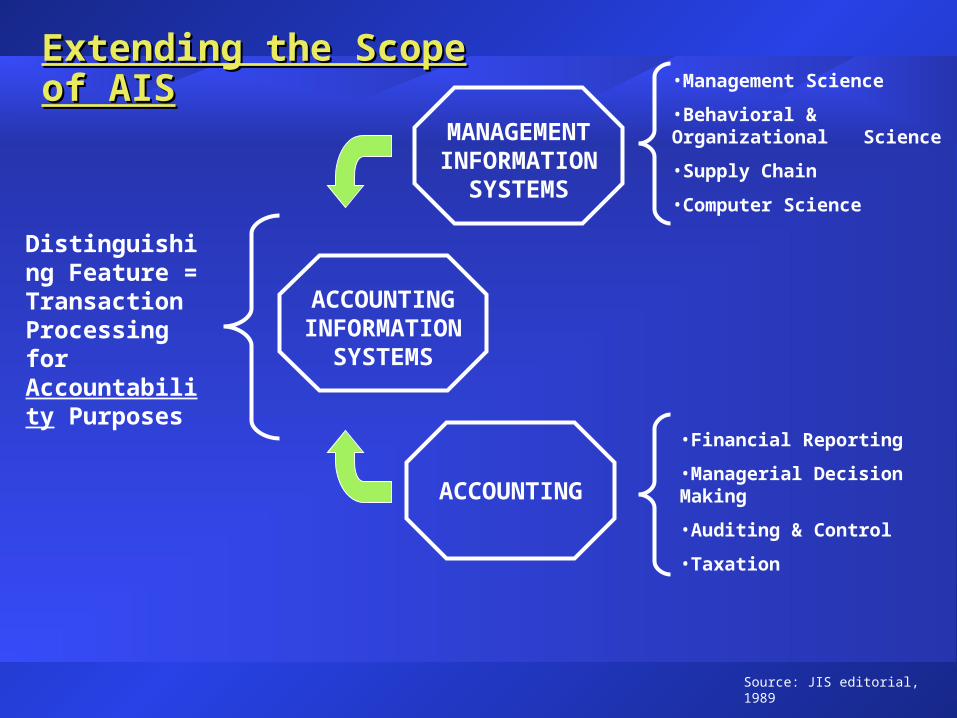

Extending the Scope of AISExtending the Scope of AIS

ACCOUNTING INFORMATION

SYSTEMS

MANAGEMENT INFORMATION

SYSTEMS

ACCOUNTING

Distinguishing Feature = Transaction Processing for Accountability Purposes

•Financial Reporting

•Managerial Decision Making

•Auditing & Control

•Taxation

•Management Science

•Behavioral & Organizational Science

•Supply Chain

•Computer Science

Source: JIS editorial, 1989

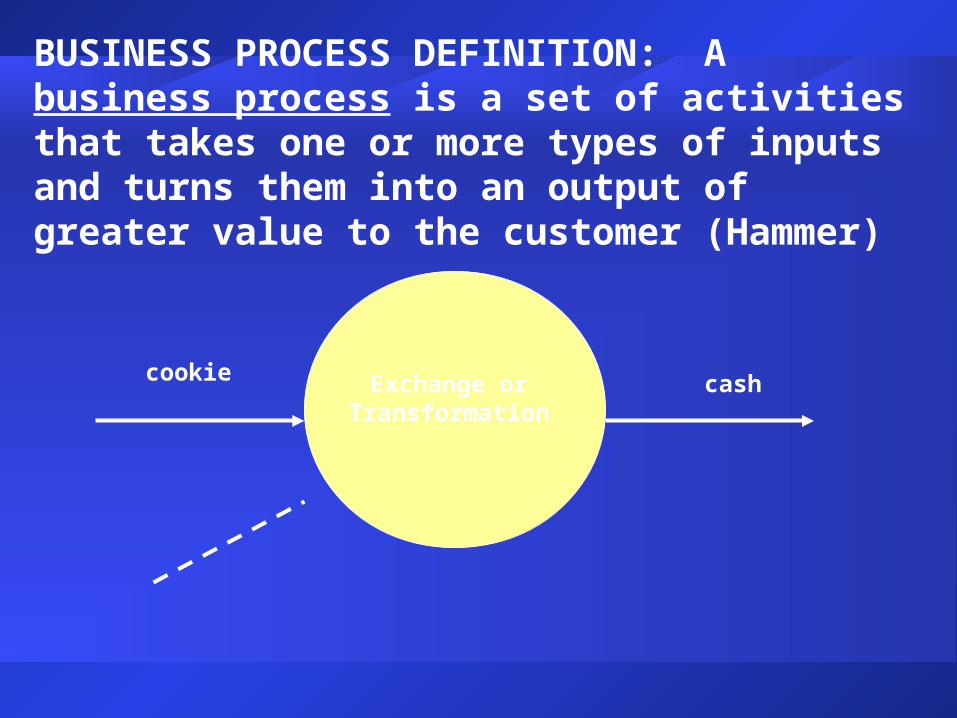

cookie cashExchange or Transformation

BUSINESS PROCESS DEFINITION: A business process is a set of activities that takes one or more types of inputs and turns them into an output of greater value to the customer (Hammer)

delivered raw materials

delivered manufactured goods

$$$$

$$

$$manufactured goods

payment

sale

Cash payment

Cash payment

logistical operation

shipment

labor

payment

labor acquire

labor

labor

facilities, services & technology

payment

service acquire

manufacture job

material issue

manufacture operation

$$

$$

service contract

service operation product services

labor

raw materialspurchase

payment

$$

Example Value Chain (source, make,

deliver) ______ ______ _______ Source: ebXML BP Catalog

delivered raw materials

delivered manufactured goods

$$$$

$$

$$manufactured goods

cash recsale

Cash receipt

Cash paymnt

logistical operation

shipment

labor

payment

labor acquire

labor

labor

facilities, services & technology

payment

service acquire

manufacture job

material issue

manufacture operation

$$

$$

service contract

service operation product services

labor

raw materialspurchase

payment

$$

Example Value Chain (per Porter

and SCOR) Source: ebXML BP Catalog

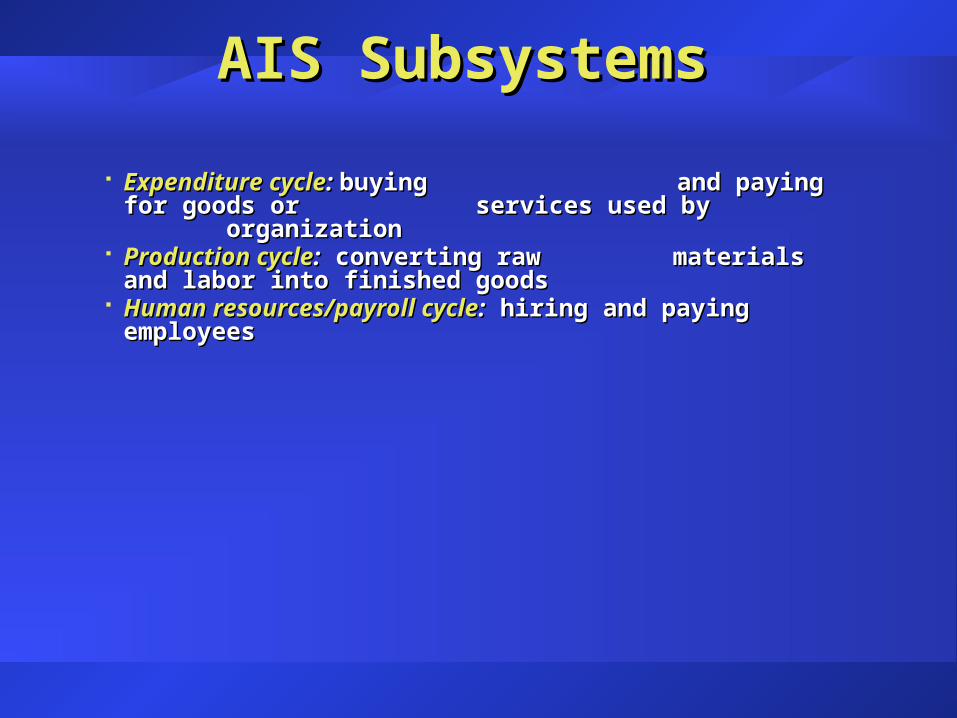

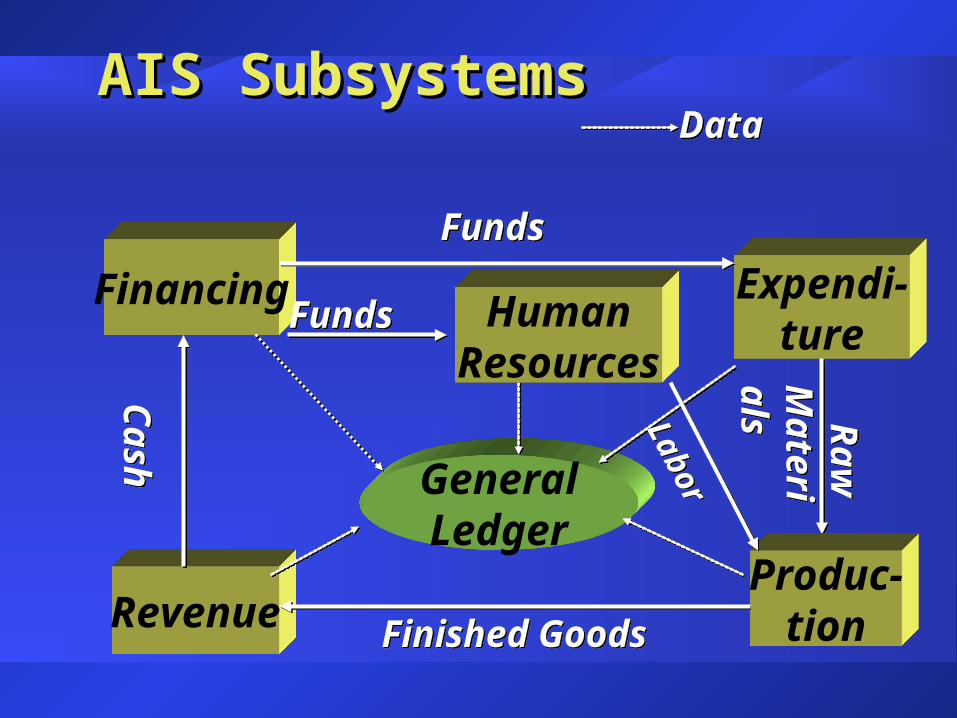

AIS SubsystemsAIS Subsystems

Expenditure cycleExpenditure cycle: : buying and paying for goods or buying and paying for goods or services used by organization services used by organization

Production cycleProduction cycle:: converting raw materials and labor converting raw materials and labor into finished goodsinto finished goods

Human resources/payroll cycleHuman resources/payroll cycle:: hiring and paying employees hiring and paying employees

AIS SubsystemsAIS Subsystems Revenue cycleRevenue cycle: : selling goods or services and selling goods or services and

collecting payment collecting payment Financing cycleFinancing cycle:: obtaining necessary funds to obtaining necessary funds to

run organizationrun organization repay creditorsrepay creditors distribute profits to investorsdistribute profits to investors

AIS SubsystemsAIS Subsystems

Financing

Revenue

Expendi-ture

GeneralLedger

FundsFunds

HumanResources

FundsFunds

Produc-tion

Raw

Materials

Raw

Materials

LaborLabor

Finished GoodsFinished Goods

Cash

Cash

DataData

AgendaAgenda The Accounting Information System The Accounting Information System

(AIS)(AIS) Why Study AIS?Why Study AIS? The Role of AIS in the Value ChainThe Role of AIS in the Value Chain

Why Study AISWhy Study AIS In Statement of Financial Accounting In Statement of Financial Accounting

Concepts No. 2, The FASB...Concepts No. 2, The FASB...– defined accounting as an information defined accounting as an information

system.system.– stated that the primary objective of stated that the primary objective of

accounting is to provide information accounting is to provide information useful to decision makers.useful to decision makers.

Why Study AIS?Why Study AIS?

To understand how the accounting system To understand how the accounting system works.works. How to collect data about an How to collect data about an

organization’s activities and transactionsorganization’s activities and transactions How to transform that data into How to transform that data into

information that management can use to information that management can use to run the organizationrun the organization

How to ensure the availability, reliability, How to ensure the availability, reliability, and accuracy of that informationand accuracy of that information

Why Study AIS?Why Study AIS? Auditors need to understand the Auditors need to understand the

systems that are used to produce a systems that are used to produce a company’s financial statements.company’s financial statements.

Tax professionals need to Tax professionals need to understand enough about the client’s understand enough about the client’s AIS to be confident that the AIS to be confident that the information used for tax planning information used for tax planning and compliance work is complete and compliance work is complete and accurate.and accurate.

Why Study AIS?Why Study AIS? One of the fastest growing types of One of the fastest growing types of

consulting services entails the design, consulting services entails the design, selection, and implementation of new selection, and implementation of new Accounting Information Systems.Accounting Information Systems.

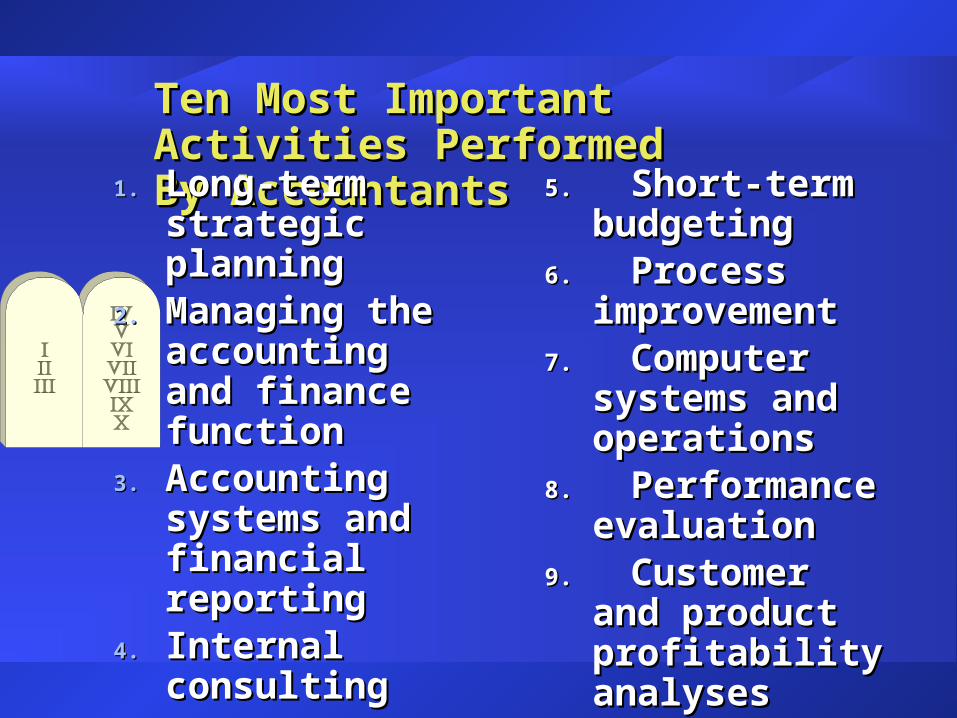

A survey conducted by the Institute of A survey conducted by the Institute of Management Accountants (IMA) Management Accountants (IMA) indicates that work relating to indicates that work relating to accounting systems was the single accounting systems was the single most important activity performed by most important activity performed by corporate accountants.corporate accountants.

Ten Most Important Activities Ten Most Important Activities Performed By AccountantsPerformed By Accountants

1.1. Long-term strategic Long-term strategic planningplanning

2.2. Managing the Managing the accounting and accounting and finance functionfinance function

3.3. Accounting systems Accounting systems and financial and financial reportingreporting

4.4. Internal consultingInternal consulting

5. 5. Short-term Short-term budgetingbudgeting

6. 6. Process Process improvementimprovement

7. 7. Computer systems Computer systems and operationsand operations

8. 8. Performance Performance evaluationevaluation

9. 9. Customer and Customer and product profitability product profitability analysesanalyses

Factors InfluencingFactors InfluencingDesign of the AISDesign of the AIS

OrganizationalCulture

Strategy

InformationTechnology

AIS

Technology and the Accounting Technology and the Accounting CurriculumCurriculumResponses from 151 universities and 62 Responses from 151 universities and 62

firms ( survey by Hastings et al. (2002)firms ( survey by Hastings et al. (2002)5 areas out of 14 are seen by % of 5 areas out of 14 are seen by % of

respondents as needing coverage to 3 respondents as needing coverage to 3 weeks or moreweeks or more

Excel (80%)Excel (80%) Access (74%)Access (74%) E-Business Concepts (61%)E-Business Concepts (61%) System Security (52%)System Security (52%) Business Process Analysis (66%)Business Process Analysis (66%)

CITP DesignationCITP Designation Certified Information Certified Information

Technology Professional Technology Professional (CITP)(CITP)

Identifies CPAs who possess a broad Identifies CPAs who possess a broad range of technological knowledge and the range of technological knowledge and the manner in which information technology manner in which information technology (IT) can be used to achieve business (IT) can be used to achieve business objectives objectives

Reflects the AICPA’s recognition of the Reflects the AICPA’s recognition of the importance and interrelationship of IT importance and interrelationship of IT with accountingwith accounting

CISACISA

Certified Information Systems Certified Information Systems Auditor-Newest DesignationAuditor-Newest Designation

AgendaAgenda The Accounting Information System The Accounting Information System

(AIS)(AIS) Why Study AIS?Why Study AIS? The Role of AIS in the Value ChainThe Role of AIS in the Value Chain

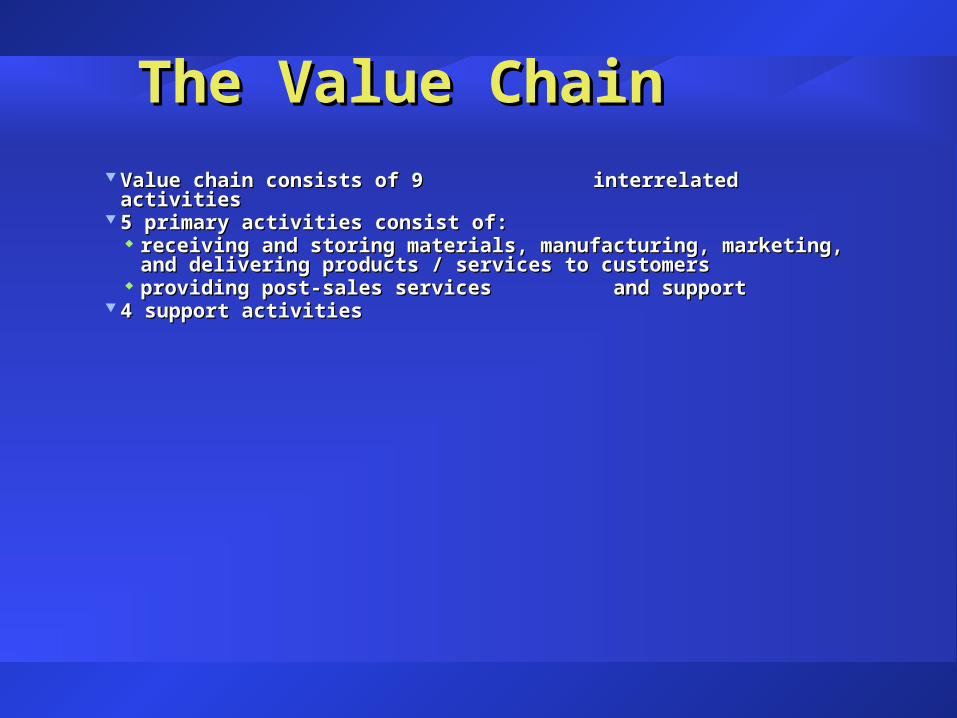

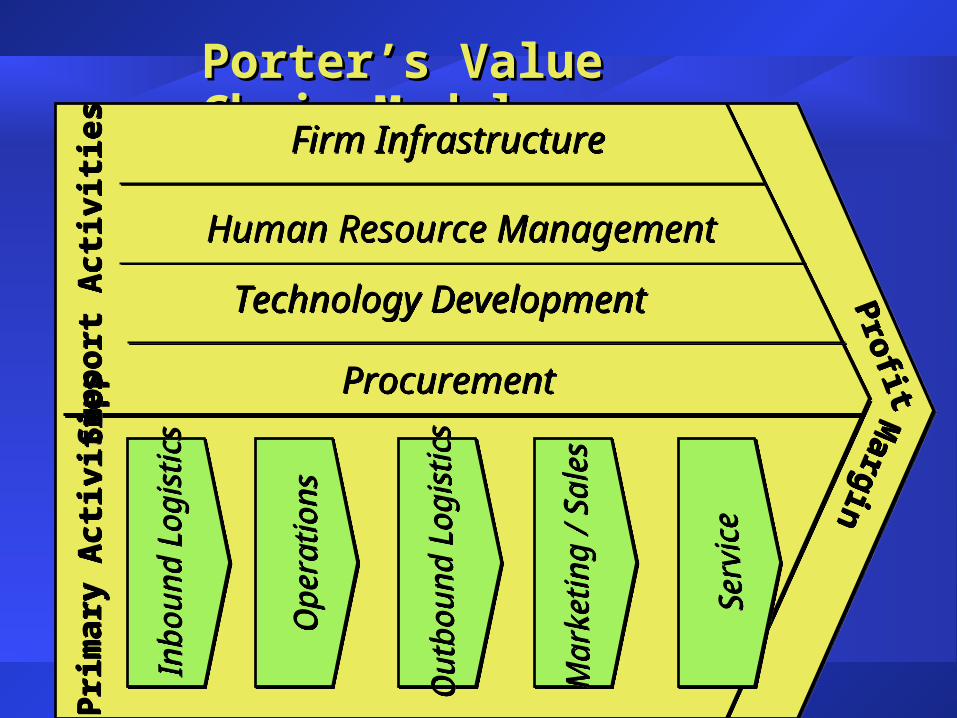

The Value ChainThe Value Chain

Value chain consists of 9 interrelated activities Value chain consists of 9 interrelated activities 5 primary activities consist of: 5 primary activities consist of:

receiving and storing materials, manufacturing, marketing, and receiving and storing materials, manufacturing, marketing, and delivering products / services to customers delivering products / services to customers

providing post-sales services and supportproviding post-sales services and support 4 support activities4 support activities

Porter’s Value Chain ModelPorter’s Value Chain Model

Firm InfrastructureFirm Infrastructure

Human Resource ManagementHuman Resource Management

Technology DevelopmentTechnology Development

ProcurementProcurementSupp

ort A

ctiv

ities

Supp

ort A

ctiv

ities

Prim

ary

Act

ivit i

esPr

imar

y A

ctiv

it ies

ProfitProfit

Margin

Margin

Inbo

und

Logi

stic

sIn

boun

d Lo

gist

ics

Ope

ratio

nsO

pera

tions

Out

boun

d Lo

gist

ics

Out

boun

d Lo

gist

ics

Mar

ketin

g / S

ales

Mar

ketin

g / S

ales

Serv

ice

Serv

ice

The Value SystemThe Value System

Value chain concept can be extended by Value chain concept can be extended by recognizing that organizations must interact recognizing that organizations must interact with suppliers, distributors, and customerswith suppliers, distributors, and customers

An organization’s value chain and value chains of its An organization’s value chain and value chains of its suppliers, distributors, and customers collectively form a suppliers, distributors, and customers collectively form a value systemvalue system

Supply Supply ChainChain

RetailerRetailer

WholesalerWholesaler

DistributorDistributor

ManufacturerManufacturer

Ord

ers

Ord

ers

CustomerCustomer

Del

iver

ies

Del

iver

ies

E-Commerce BypassE-Commerce Bypass

Demand

Demand

How AIS Adds ValueHow AIS Adds Value An AIS adds value by:An AIS adds value by:

– providing accurate and timely information to providing accurate and timely information to perform various value chain activitiesperform various value chain activities

– improving efficiency and effectiveness of value chain improving efficiency and effectiveness of value chain

activitiesactivities

InformationInformation

DataData : facts collected, stored, and : facts collected, stored, and processed by information systemprocessed by information system

IInformationnformation:: data organized and processed so it is data organized and processed so it is meaningfulmeaningful for business decision makingfor business decision making

Information and Information and Decision MakingDecision Making

Characteristics of Useful Information

Understandable

Verifiable

TimelyRelevant

Reliable

Complete

Useable

Value of InformationValue of Information Value of informationValue of information

benefit produced by benefit produced by informationinformation

minus cost of producing it.minus cost of producing it.

Topics DiscussedTopics Discussed

The Accounting Information The Accounting Information System (AIS)System (AIS)

Why Study AIS?Why Study AIS? The value of AISThe value of AIS