Accounting Fraud: Booms, Busts, and Incentives to … · Accounting Fraud: Booms, Busts, and...

66

1 Accounting Fraud: Booms, Busts, and Incentives to Perform Robert H. Davidson University of Chicago Booth School of Business [email protected] http://home.uchicago.edu/~rdavids2/ January 26, 2011 * I am grateful for many helpful comments from my dissertation committee: Abbie Smith (chair), Ray Ball, Ryan Ball, and Christian Leuz. I would also like to thank Phil Berger, Aiyesha Dey, Merle Erickson, Joseph Gerakos, Andrei Kovrijnykh, Michael Minnis, Valeri Nikolaev, Zoe-Vonna Palmrose, Haresh Sapra, Oren Yoeli, Shimeng Yu, and Sarah Zechman as well as participants in seminars at the University of Chicago Booth School of Business.

Transcript of Accounting Fraud: Booms, Busts, and Incentives to … · Accounting Fraud: Booms, Busts, and...

1

Accounting Fraud: Booms, Busts, and

Incentives to Perform

Robert H. Davidson

University of Chicago Booth School of Business

http://home.uchicago.edu/~rdavids2/

January 26, 2011

* I am grateful for many helpful comments from my dissertation committee: Abbie Smith (chair), Ray Ball, Ryan Ball,

and Christian Leuz. I would also like to thank Phil Berger, Aiyesha Dey, Merle Erickson, Joseph Gerakos, Andrei

Kovrijnykh, Michael Minnis, Valeri Nikolaev, Zoe-Vonna Palmrose, Haresh Sapra, Oren Yoeli, Shimeng Yu, and

Sarah Zechman as well as participants in seminars at the University of Chicago Booth School of Business.

2

Abstract

In this paper, I examine whether macroeconomic conditions influence the propensity to commit

accounting fraud. I find that the incidence of observed accounting fraud is increasing in GDP

and is at its highest in the periods leading up to an economic peak. In addition, the incidence of

observed accounting fraud is decreasing in the average correlation between firm and market

returns and the average magnitude of analyst forecast errors; the relation is increasing in

average price-earnings ratios. When examining the relation between macroeconomic conditions

and firm-level fraud determinants I find that the association between CEO compensation

incentives and the propensity to observe accounting fraud is generally negative, but is positive

and significant during periods of high price sensitivity to earnings news. Analyzing accounting

fraud by type reveals that revenue fraud is increasing in the price sensitivity to revenue news;

this relation does not exist for expense or balance sheet fraud. Additionally, balance sheet fraud

is increasing in the default risk premium. These results are consistent with the hypothesis that

market-wide incentives for managers to manipulate earnings influence the decision to commit

accounting fraud above and beyond firm-level determinants.

3

1. Introduction

Over the last 100 years, recessions have been routinely accompanied by revelations of

scandalous reporting failures at many firms. Fraudulent reporting was exposed after the Great

Crash in 1929, after the Savings & Loans scandal in the 1980s, and after the dot-com bubble of

the late 1990s/early 2000s1. Sweeping changes in regulation have often followed these scandals;

the Sarbanes-Oxley Act, for example, was drafted to reduce the likelihood of fraudulent

reporting after the dot-com crash. Additionally, Baker and Wurgler [2007] note the dramatic

decrease in stock prices that occurs during these periods. The overall cost of a wave of

accounting scandals to the economy - in terms of reduced firm value, reduced investor

confidence, bankrupt firms, increased unemployment, and additional regulation - is huge.

Managers have many financial incentives to meet their performance expectations. These

incentives include avoiding, among other things, termination, a decline in the value of their

stocks and options, a downgrade of the company’s debt, debt covenant violations, and

corporate bankruptcy. The dollar effect on stocks and options from failing to meet expectations

has varied over time. Likewise, the other financial incentives that can lead managers to commit

accounting fraud vary in strength over time. Moreover, differential effects across these

incentives are likely to exist as well.

Theoretical research predicts that the level of accounting fraud in the economy is

likewise not constant over time, and neither are financial incentives that the capital and labor

1 Galbraith [1961] discusses the scandals that followed the Great Crash. Ball [2009] discusses the wave of scandals

that came to light after the dot-com bubble burst.

4

markets exert on managers. Research on firm-level determinants of accounting fraud often

yields contradictory results and does not consider, first, how incentives can vary over time and,

second, that differential effects across incentives are likely. Do changes in the macro economy

influence managers’ reporting decisions above and beyond firm-level determinants? Are

certain hypothesized firm-level determinants of accounting fraud only important under certain

environmental conditions? Does the type of accounting fraud managers commit depend on the

source of their incentives?

To answer these questions I gather data on a comprehensive sample of instances of

accounting fraud that occurred in the United States between 1980 and 2005. Over 800 cases of

accounting fraud are revealed over the sample period, including such high profile cases as

Adelphia, Enron, Sunbeam, and WorldCom.

Having identified the period the violation began, I use survival analysis to test whether

observed accounting fraud is related to macroeconomic performance and whether we observe

more managers reporting fraudulently after a long ‚boom‛ period. I then construct several

macroeconomic proxies measuring the relative strength of incentives various markets create

and test whether these proxies explain the increase in fraudulent reporting observed during

certain periods. I interact hypothesized firm-level accounting fraud determinants with a market

measure of price sensitivity to short-term news to see whether the firm-level determinants affect

managers more strongly in certain environments. Finally, I split accounting fraud into three

groups – revenue fraud, expense fraud, and balance sheet fraud – to test for differential effects

across incentives to commit accounting fraud.

5

I find that more managers start committing accounting fraud during periods of strong

macroeconomic performance, as measured by detrended gross domestic product, and in the

two years leading up to an economic peak. Conversely, I find that fewer managers start

committing accounting fraud in the two years following an economic trough.

In survival analysis including fraud firms as well as a random sample of non-fraud

firms, I find more observed cases of accounting fraud start in periods of strong aggregate

performance. This finding is robust to the inclusion of potential firm-level determinants of

accounting fraud. Moreover, I find that more managers start committing accounting fraud in

periods wherein firm returns are less correlated with the market return, in periods wherein

predicting earnings is easier, and in periods wherein price-earnings ratios are high.

In logistic analysis testing the relation between accounting fraud and firm-level fraud

determinants interacted with price sensitivity to news, I find that the delta of the CEO’s stock

holdings is positive and significantly related to accounting fraud only in periods of high price

sensitivity to short-term news. I also find that while the relation between raising capital and

accounting fraud is generally positive, it is statistically significant only in periods of high price

sensitivity to news.

When analyzing accounting fraud by type, I find more observed cases of revenue fraud

in periods of high price sensitivity to revenue news; expense fraud is similarly related to

earnings news, rather than revenue news. I also find that balance sheet fraud is positively

related to the default risk premium; no significant relation exists between revenue or expense

6

fraud and the default risk premium. Overall, these findings are consistent both with the

environment playing a role in managers’ financial reporting decisions and with managers

responding to external market driven incentives by committing accounting fraud in periods

when those incentives are strongest.

This paper contributes to the literature in several ways. First, by demonstrating that a

given manager’s decision to commit accounting fraud is related to macroeconomic conditions, it

provides support for the argument that market driven incentives affect managers to such an

extent that they commit accounting fraud. Second, as logistic results suggest, given strong

enough financial incentives from a CEO’s incentive compensation or the firm’s need for external

financing, managers will resort to accounting fraud; in addition, these results explain the

channels through which market price sensitivity to news operates. Third, this paper documents

a differential effect across incentives to commit accounting fraud. For example, managers are

more likely to commit revenue fraud when the demand for top-line growth is high and are

more likely to commit balance sheet fraud when the risk of default is high. Finally, it provides a

novel explanation for the contradictory results reported in the literature and the lack of

consensus regarding the relation between accounting fraud and firm-level determinants thereof.

The remainder of this paper is organized as follows: section 2 reviews the relevant

literature; section 3 develops testable hypotheses; section 4 describes the data; section 5

describes my empirical tests and presents my results; section 6 discusses my tests for

robustness; section 7 presents future work to be included in a final draft of this paper and

section 8 concludes.

7

2. Literature

Most research on the relation between accounting fraud and the environment in which it

occurs is theoretical. Though each of these model’s assumptions and mechanisms are different,

they all find that more managers start to commit accounting fraud in periods of strong

aggregate performance.

Povel, Singh, and Winton [2007] present a model of collective accounting fraud wherein

a given manager is motivated to obtain funding for a project; investors choose either to rely on a

public signal from the manager or to invest in costly but unbiased private monitoring before

deciding whether to invest. Depending on investor’s beliefs about the state of the world, a

manager with a bad project can increase his chances of obtaining funding by overstating the

project’s value. In summary, they find that the relation between accounting fraud, actual

performance, and expected performance is non-monotonic. Specifically, fraud peaks in good

but not great states of the world. The primary determinant of their findings is the level of

monitoring effort investors exert, which they assume is influenced by the macro economy.

Hertzberg [2005] develops a model wherein variation in the manager’s short-term and

long-term incentives in turn creates variation in the incentives to commit accounting fraud.

Managers are more likely to commit accounting fraud when their short-term incentives are

strong. Hertzberg, however, does not model which forces alter the composition of the

manager’s incentives. Short-term incentives could be increased by various changes within the

firm, by capital and labor market incentives, or by other forces in the environment.

8

Rajgopal, Shivakumar, and Simpson [2007] develop and test a catering theory of

earnings management. In their model, the manager is concerned with obtaining the highest

possible price for his firm’s shares. They find that earnings management increases in periods of

high investor optimism, which they define as periods wherein positive earnings surprises

receive a larger price reaction. They do not, however, test whether earnings management

increases in periods wherein negative earnings surprises are severely punished.

Though Rajgopal et al [2007] do not model or directly test the link between earnings

optimism and actual performance, they allude to as much and cite some macroeconomic

theories (Taussig [1911], Keynes [1936], Lavington [1992], and Collard [1996]) that suggest that

periods of earnings optimism tend to coincide with periods of high real growth. In their model,

in periods wherein optimism coincides with high real growth, it is less costly for the manager to

overstate earnings because, during such periods, it is easier to replace borrowed funds later,

thus reducing the costs of earnings management. This model is in slight contrast to the one

presented by Povel et al [2007], who argue that when actual performance and expected

performance are both high, managers has less incentive to commit fraud because the true

performance of their firms’ is also high. This difference, however, may derive from the papers’

different focuses. Whereas Povel et al [2007] model the decision to commit accounting fraud,

which is a high risk decision that can lead to large fines and jail time, Rajgopal et al [2007]

appear to model cases of within GAAP earnings management which is a low-risk decision,

relatively speaking.

9

Two recent empirical papers study the relation between accounting fraud and the

environment in which it occurs. Kedia, Koh, and Rajgopal [2010] find that misreporting can

have a contagion effect. Specifically, they find that managers are more likely to begin

misreporting when another firm in their industry is revealed to have misreported. They find

this effect only in the absence of SEC litigation of the initial misconduct. While it is not clear

whether this effect is due to managers perceiving either a lax regulatory environment (i.e., a

reduced cost to misconduct) or a change in social norms (i.e., that misconduct is condoned), it

does appear to be driven by environmental, as opposed to firm-level, forces.

Fernandes and Guedes [2009] document the circumstances under which accounting

fraud is more likely to occur and examine the relation between accounting fraud and expected

and actual performance. They find a positive relation between the occurrence of accounting

fraud and expected growth and a negative relation between accounting fraud and actual

performance. I, on the other hand, after controlling for the difference between actual and

expected output find a positive relation between accounting fraud and output. Several

measurement issues related to Fernandes and Guedes’ [2009] calculation of accounting fraud

could account for our different results. For example, they average Foreign Corrupt Practices

Act violations over a three year period, which makes it impossible to identify which conditions

were present when the manager decided to start committing accounting fraud. Such averaging

can create a mechanical bias that leads to both overstating and understating the true number of

fraud firms present in a given year. A second measurement issue arises from the years to which

they attribute violations. Over their time period, fraudulent reporting lasts, on average, just

10

under three years. Over the same time period, government litigation releases tend to come

about three years after the fraud is detected. This means that a release in 2006 is likely to

address accounting fraud that began around 2001 and was committed through 2003. Fernandes

and Guedes [2009] average this release over the period 2004-2006.

Dechow, Ge, Larson, and Sloan [2010] use many hypothesized firm-level symptoms and

determinants of accounting fraud to develop a predictive model of fraud. They develop an

audit tool, the F-Score, which has the predictive power to identify fraud firms ex post. Though

their research question is different from mine, our papers have several similarities. First, to

build their sample of accounting fraud, Dechow et al [2010] hand collect, as I do, a large sample

(i.e., 2190) of Accounting and Auditing Enforcement Releases; theirs is also one of the few

papers to analyze several hundred fraud firms. The major difference between our reported

sample sizes is that while Dechow et al [2010] include in their analysis all fraud years for a

given firm, I include only the first year of fraudulent reporting. Second, both Dechow et al

[2010] and I test market-related motives for accounting fraud. Specifically, we both report a

positive association between accounting fraud and both the propensity to raise capital and

lagged abnormal returns. The motivation and findings that Dechow et al [2010] document for

these variables led me to include them in my analyses.

3. Hypothesis Development

Becker [1968] presents a rational theory of crime that reduces the decision to commit a

crime to a weighing of the benefits against the associated costs. A given manager’s decision to

11

report truthfully or to commit accounting fraud can be analyzed in this context. The costs to the

manager, if his crime is detected, include substantial fines, jail time, and loss of reputation. Add

to this the fact that accounting fraud is a rare event and it seems clear that for the manager the

costs of accounting fraud are substantial. Therefore, the perceived costs of reporting truthfully

– or, conversely, the perceived benefits of reporting fraudulently - must also be substantial

before a manager would choose to commit accounting fraud.

Analytical research supports the claim that the level of accounting fraud in the economy

is not constant over time. That accounting scandals come in waves is also supported by

anecdotal evidence. The forces that greatly influence the perceived costs of truthfully reporting

poor performance do not appear to be constant over time. These forces can arise from within

the firm, but can also arise from the environment the firm operates in.

Survey evidence from Graham, Harvey, and Rajgopal [2005] indicates that executives

manipulate earnings to maintain or increase their firm’s share price. Baker, Ruback, and

Wurgler [2007] suggest that managers manipulate earnings to cater to market demands.

Following this evidence, I assume that a given manager will be motivated to keep the price of

his firm’s shares high and, when faced with reporting numbers below ex ante expectation, will

base his decision of whether to report truthfully or fraudulently on the presence of

environmental factors that affect the net benefits of accounting fraud. A given manager’s

market driven incentives are not constant over time, so we should observe an increase in

fraudulent reporting in periods wherein those incentives are strongest.

12

3.1 Time Variance

Recent literature assumes that the correlation between accounting fraud and

macroeconomic performance is positive, though not necessarily monotonic2. Proposed

hypotheses for this correlation include the belief that monitors, such as external auditors, debt

holders, and shareholders reduce their effort during good times; the belief that investors in

general are more likely to believe what firms report during good times; and the belief that

managers have more to gain from insider trading during good times. Each of these specific

hypotheses, however, is difficult to test empirically because of difficulties in measuring monitor

effort, how willing investors are to believe financial statements, or a manager’s intent to engage

in insider trading from fraud3. These hypotheses seem to implicitly assume that managers are

always willing to commit accounting fraud and are simply waiting for the right opportunity to

do so.

Though all of the above forces could influence a manager’s decision to report

fraudulently, they do not consider the potential relation between the firm’s performance and

accounting fraud. A more comprehensive argument is that what matters to managers is their

performance measured both against their firm’s expected performance and performance

relative to peers and that performing poorly across either dimension can increase a manager’s

incentive to commit accounting fraud. Myers, Myers, and Skinner [2006] document the

2 Povel et al [2007], Hertzberg [2005], and Strobl [2008] all develop analytical models that support this result.

3 Agrawal and Cooper [2007] do find some evidence to suggest that managers engage in trades during the fraud

period, but it is difficult to know whether they committed accounting fraud expressly for the purpose of engaging

in insider trades.

13

importance to managers of consistently beating expected performance. They find that firms

with long strings of positive earnings surprises have higher share prices than firms with similar

long run performance but with breaks in positive surprises. Martin and McConnell [1991] find

that takeover targets perform better than the market but worse than their peer groups. Antle

and Smith [1986] and Gibbons and Murphy [1992] both find that relative performance is

sometimes expressly written into compensation contracts. Share price, CEO compensation, and

job retention are all influenced by the firm’s performance, both relative to its own expected

performance and relative to that of its peers.

Ball *2009+ argues that ‚high growth becomes built into performance expectations

during an extended boom‛ and that ‚managers therefore come under peer and financial

pressures to deliver strong earnings growth and share market performance‛4. When,

inevitably, some firms experience declining performance relative to their own expectations and

to those of their peers, the managers of these firms find themselves unable to meet their

heightened expectations. Such managers likely feel a great deal of pressure from the capital and

labor markets, and some may resort to accounting fraud to meet these expectations.

Building on research related to investor sentiment, Baker and Wurgler [2007] argue that

during the boom phase of the late 1990s extraordinary investor sentiment pushed the prices of

many stocks to unfathomable heights that simply could not be justified by the facts at hand.

They further note that risks and ‚limits to arbitrage‛ made it too difficult for contrarian

4 Galbraith [1961] makes a similar case for the events leading up to the 1929 market crash.

14

arbitrageurs to bring prices back down to appropriate levels. This extremely high optimism

was built into the market’s expectation of firm performance. Baker and Wurgler [2006] find that

investor sentiment has a greater effect on firms with higher growth prospects; on average, firms

have higher growth prospects when the aggregate economy is experiencing a high growth

boom. The prior literature therefore supports my first hypothesis:

H1A: The relation between macroeconomic performance and accounting fraud is positive.

Given that the costs associated with reporting truthfully increase dramatically for

managers when their firm is performing poorly relative to benchmarks, I expect to find that

periods characterized by high benchmarks and a reasonable number of firms starting to

perform below expectation have higher levels of observed cases of accounting fraud. These

characteristics describe the years leading up to an economic peak. Such periods are generally

characterized by years of sustained growth that does not continue far into the future. Many

firms experience high growth in the years leading up to the peak, and their current forecasts are

formulated, in part, on this prior growth. Ex post we know that a number of firms experience a

decrease in performance right before the economy peaks and starts to decline.

H1B: The relation between observed accounting fraud and the years before an economic peak is

positive.

A related area of research looks at the progression a firm and manager make to get to

the point where a given manager commits accounting fraud. Schrand and Zechman [2008]

argue that there is a slippery slope to accounting fraud wherein managers start off looking to

15

plug small gaps in performance and may have no intention of committing accounting fraud. If

their performance does not improve in subsequent periods, a manager may continue to plug the

small gaps; over time, however, the amount of manipulated earnings can grow egregious and

the manager will then face either reporting truthfully and reversing their past entries, or

continuing down the path towards accounting fraud. Empirical and anecdotal evidence

support the slippery slope theory, and its existence does not change the predictions I make in

this paper. I argue that market driven incentives and the firm’s environment will influence

managers in the same way regardless of whether a given manager has shown a willingness to

slightly manipulate earnings in the past or would have to reverse his past entries if he chose to

report truthfully. In other words, while a manager who has previously manipulated earnings

may be more willing to commit accounting fraud, environmental factors likely influence all

managers in the same way.

3.2 Market Based Incentives

Knowing when managers are more likely to commit accounting fraud is a helpful

starting point for developing hypotheses about which forces influence managers to either

truthfully report poor performance or to commit accounting fraud. If more managers report

fraudulently in good times, then we can shift our focus to forces that are particularly strong in

these periods. The analysis above supports the formulation of a market driven incentives

hypothesis. Market wide incentives affect all firms in the economy at the same time and to a

highly correlated degree. Looking at changes in these incentives over time seems like an

16

optimal way to test the theory that market driven incentives influence a manager’s reporting

decisions.

Many areas of research document that markets place significant pressure on managers

to perform5. Benmelech et al. [2010] show that while incentive-based compensation induces

managers to exert costly effort, it also induces them to conceal bad news about future growth

options and to choose sub-optimal investment policies. They argue that in periods with strong

market incentives, or periods wherein price is highly sensitive to short term news, incentive

compensation should be reduced. Ball [2009] also discusses the financial pressures that build

up during an extended boom. Though accounting fraud is not the focus of their paper,

Benmelech et al [2010] nevertheless mention that fraudulent reporting is one possible response a

manager can have to poor performance in periods wherein price sensitivity to news is high.

Such a manager has incentives to keep his firm’s share price high because this affects both his

compensation and job retention. Disappointing investors by performing poorly reduces the

price of the firm’s shares, reduces the value of a manager’s incentive based compensation, and

increases the likelihood of that manager being replaced.

H2: The relation between observed accounting fraud and market driven incentives is positive.

Empirically separating capital market from labor market incentives is difficult. Poor

performance reduces share price, increases the cost of capital, increases pressure from investors,

and increases the likelihood of replacement. If managers are ultimately concerned with their

5 For examples of the effects of market incentives, see Gray, Meek, and Roberts [1995], and Cao and Laksmana

[2010].

17

net worth, then we can assume that appeasing both the capital and labor markets will be

important to them. This hypothesis, however, does not specify whether the manager is

responding to incentives driven primarily by the capital or labor market, owing to the

difficulties with separating the two. Hypothesis 3 attempts to isolate the effects on accounting

fraud of the value of the manager’s incentive plans and net worth.

3.3 Relation between market-based incentives and firm-level accounting fraud determinants

Research on firm-level determinants of accounting fraud often produces inconsistent

and in some cases contradictory results. Common issues in this area of research are small

sample sizes6 and samples collected over short periods7. These issues could mean that the

differences in results have nothing to do with econometric or measurement issues, but are

driven by fluctuations in the strength of market wide incentives that influence both the decision

to commit accounting fraud and managers’ operating, financing, and accounting choices.

Essentially, prior research may have overlooked an important factor when modeling firm-level

accounting fraud determinants.

For example, research on the link between incentive compensation and accounting fraud

has yielded mixed results. While most academics believe that incentive compensation does

induce the manager to exert costly effort, the extent to which it also gives the manager

incentives to commit accounting fraud remains debatable. Johnson et al. [2009] find a positive

6 Beneish [1997] analyzes 49 fraud firms drawn from AAERs. Erickson et al [2004] analyze the amount of tax 27

fraud firms pay on fraudulent inflated earnings.

7 Kedia and Phillipon [2007] study violations between 1996 and 2001.

18

relation between CEO unrestricted stock holdings and accounting fraud while Armstrong et al.

[2009] find a negative relation between incentive compensation and accounting fraud.

Benmelech et al. [2010] argue that the effect of incentive compensation is not fixed and is, rather,

influenced by market behavior. In periods wherein the sensitivity of price to short-term news is

high, managers have increased incentives to conceal bad news. It is possible that a given

manager’s reporting decision will be influenced by his incentive compensation only in periods

wherein markets respond dramatically to short-term news.

H3: The relation between observed accounting fraud and CEO incentive compensation and net

worth is positive and more pronounced in periods wherein stock price is highly sensitive to short-

term news.

While Dechow et al. [1996] find that managers are often motivated in their decisions to

commit accounting fraud by concerns about the cost of external financing, Beneish [1999] finds

no support for this claim. Further, while Beneish [1999] finds that fraud firm managers are

more likely to sell their stock and exercise stock appreciation rights during the fraud period,

Dechow et al. [1996] find no support for this claim. The effect of firm performance on the cost of

external financing is not constant. It is possible that managers are more willing to commit

accounting fraud to raise capital on favorable terms in periods wherein the fraudulently inflated

earnings will have the greatest effect on the value of securities.

H4: The relation between observed accounting fraud and the decision to raise capital is positive

and more pronounced in periods wherein price is highly sensitive to short-term news.

19

4. Data: AAERs

I use SEC Accounting and Auditing Enforcement Releases (AAERs) as a proxy for

accounting fraud. These releases summarize investigations the SEC brings against the agents of

firms for violations of SEC and Federal rules. AAERs clearly state whether the violation was for

accounting fraud or some other infraction (e.g., securities law violations). To collect my sample,

I read through AAERs 1 – 3148 which were released between May 17, 1982 and June 29, 2010.

After limiting my sample to violations for accounting fraud wherein the fraud had a

determinable start date and then removing redundant cases, I was left with 824 firms.

Determining which types of violations to include involves a degree of subjectivity.

Ultimately, I include in my final sample only those firms for which it can be determined that

their financial statements (or notes) were materially misstated. One exception to this rule is

violations due to options backdating, which I exclude from the sample. Only a small number of

AAERs involve options backdating, and their inclusion marginally improves the results of some

of the tests. I nevertheless exclude these cases because the motivation to backdate options

seems clear.

The choice to include violations for revenue (or asset) understatement is also subjective.

As with cases of options backdating, only a small number of AAERs (i.e., 4 cases) involve

violations for revenue or asset understatement.8 This could be due to fewer managers having

strong incentives to understate revenues or to the SEC having weaker incentives to prosecute

8 Xerox and Microsoft are two well known cases of revenue/asset understatement litigated by the SEC.

20

these types of violations. Because my predictions relate to the incentives to overstate, rather

than understate, earnings or net assets, I exclude these cases.

Only firms under the jurisdiction of the SEC are prosecuted and included in the AAER

sample. Firms that do not issue debt or equity in the United States are not included. Given that

this paper tests the relation between market wide incentives and accounting fraud, collecting a

sample of fraud firms from the universe of firms under SEC jurisdiction should represent a fair

proxy, relative to the alternatives. Small private firms are not included because the owners of

these firms generally do not have concerns related to labor market incentives (i.e., they often

have a controlling interest) or to capital market incentives from shareholders (i.e., shareholders

are generally nonexistent). Debt holders tend to be concerned about downside risk and the cash

flows required to service debt, not about whether the firm exceeds high growth expectations.

The value of these firms to their owners does not fluctuate wildly based on quarterly

performance; often there are no traded shares whose value can be reduced greatly by a period

of poor performance.

Although a number of international firms do raise public capital in the United States and

fall under the jurisdiction of the SEC, the AAER sample contains only a handful of such firms.

It is not clear why the sample contains such a small number of international firms, but one

likely reason is the additional cost the SEC would incur to prosecute agents of firms who often

do not reside in the United States and whose firms have little to no physical presence in the

United States. I exclude these cases from my sample of 824 fraud firms available for time series

analysis.

21

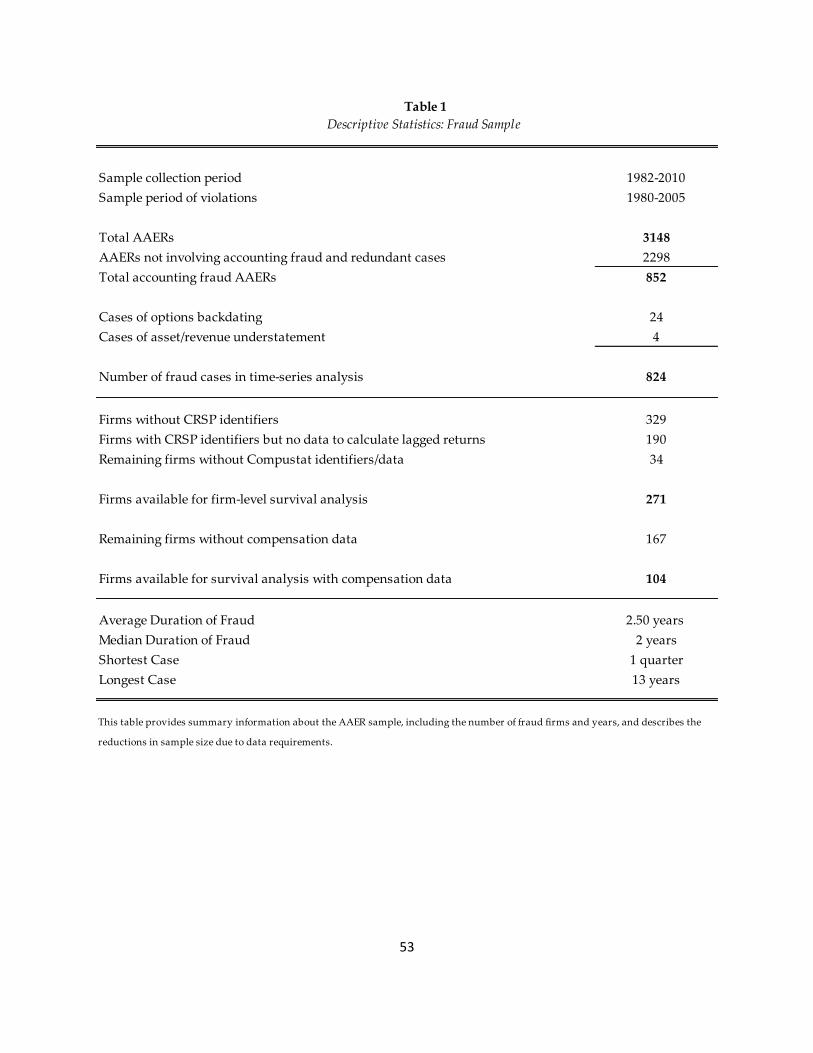

Data restrictions limit the number of fraud firm observations available for firm-level

analysis. Table 1 presents the number of firms lost at each stage. The two primary reasons for

the decline in sample size are the lack of any identifying code for the firm (363 firms) and the

absence of CRSP and Compustat data before and during the period wherein the fraud began

(190 firms). The primary survival analysis includes 271 firms. While this is large drop from my

original sample of 824 firms, it is large compared to many of the papers previously discussed

above9. Of these 271 firms, only 104 have compensation data available; I therefore conduct two

sets of analysis, one with and one without control variables for CEO compensation.

AAERs offer several advantages over other proxies for accounting fraud. First and

foremost, it is clear whether managers of the firms in the AAER sample actually committed

accounting fraud, making the probability of type 1 errors negligible. This is not true for

earnings restatements, which also occur because of clerical error, change in accounting policy,

or numerous other factors in addition to accounting fraud. This is also not true for observations

from the Stanford Law Database on Shareholder Lawsuits. Though many shareholder lawsuits

arise from intentional material misstatements many more arise for other reasons. Moreover,

many shareholder lawsuits allege intentional misstatements when there is no clear evidence to

support that claim.

9 Dechow et al [2010] is one important exception to the general trend of small sample sizes in prior research. Their

main analysis includes between 354 and 494 fraud firm years. My analysis, which includes several of the variables

they use in their most restrictive tests, is based on a sample of 271 individual fraud firms.

22

In the earnings management literature, some measure of abnormal accruals is often used

as a proxy for earnings management. Whether these measures have much ability to discern

earnings management in the aggregate, however, is debatable. Ball [2009] points out that

‚much academic research on earnings management establishes such a weak burden of proof

that earnings management appears almost universal.‛ Ball [2009] goes on to state that one

advantage of focusing on negligent or fraudulent financial reporting is that ‚a proven case of

negligent or fraudulent financial reporting is an institutional ‘fact’, as distinct from an error-

prone academic estimate.‛ Further, Correia *2010+ shows that accruals models are correlated at

less than 5 percent with ex post measures of accounting fraud.

Another advantage of using AAERs is that they provide a great deal of information

about the nature and timing of the violation. They generally provide clearer information about

the start and end dates of the violation than do releases of violations of the Foreign Corrupt

Practices Act’s (FCPA) books and records laws. Testing the environmental conditions present at

the time a manager starts to commit accounting fraud requires access to as detailed and

accurate information as possible about the start date of the violation.

AAERs do, however, have several limitations. One drawback of using any ex post

measure of accounting fraud (i.e., AAERs, restatements, FCPA releases) is that they only

document cases that are detected – a potentially important issue that is difficult to completely

control for, though attempts are made. If the SEC’s detection methods or litigation decisions

contain any bias, then this issue becomes particularly relevant to AAERs. That said, as Dechow

et al [2010] point out, the SEC identifies firms for review through anonymous tips, news reports,

23

voluntary firm restatements, and their own review practices. Several independent sources

provide information regarding potential malfeasance, which should reduce the possibility of

bias in the SEC’s detection methods.

The SEC also faces budgetary constraints and only prosecutes those cases where there is

strong evidence against the firm. On average, these cases should be the ones in which

accounting fraud most likely occurred. That said, time-variance in budget constraints could

influence the composition of the sample. To control for this possibility, I include the SEC’s

annual budget appropriation in my models. However, analyzing my sample of AAERs

provides anecdotal evidence that budget constraints are not a serious problem. Indeed, my

sample includes 24 cases in which the manipulation amounted to less than $1 million dollars,

which suggests that the SEC has the resources to prosecute cases of relatively small

manipulations as long as there is strong evidence of malfeasance. Further, there is no statute of

limitations for litigating fraud firms.

Another concern related to using AAERs is that lags in detection and/or AAER release

could cause the number of new fraud cases to be under-represented in the last few years of the

sample period. To mitigate this possibility, I include in the sample only violations that started

before 2006. In the AAER sample, accounting fraud lasts on average 10 quarters and the

corresponding release is published on average three years after the violation was detected.

24

Therefore, performing tests through 2005 should greatly reduce the likelihood that the most

recent years contain an unrepresentative number of fraud cases10.

5. Tests and Results

I examine Hypotheses 1A and 1B using time-series and survival analysis. While the

small number of years in my sample, concerns about degrees of freedom, and concerns about

correlated omitted variables limits the ability of the time-series regressions to establish

causality, these regressions still provide descriptive evidence on when we observe more

managers choosing to commit accounting fraud and on the magnitude of the effect that changes

in the macro economy has on the propensity to observe new cases of accounting fraud. To test

Hypotheses 1A and 1B, I estimate time-series regressions of the following general form:

_ifraud macro performance surprise .

Fraud is measured as the number of managers who start committing fraud during a

given year scaled by the number of Compustat firms in that year. Macro performance is

measured using GDP (inflation adjusted and expressed in chained 2005 dollars) with the time

trend removed using the Hodrick-Prescot [1997] filter1112. To test Hypothesis 1B I include

indicator variables that measure the run up before an economic peak and the recovery after an

10

Results are not sensitive to the choice of cutoff year. I also used 2003 and 2004 as end years and found that the

significance of my results remained unchanged.

11 I also used the Baxter-King [1999] filter and found no change in my results.

12 Focusing on the consumption and investment components of GDP does not change the results. Neither does

using corporate profits.

25

economic trough as defined by the National Bureau of Economic Research (NBER). Peak takes

a value of 1 if the current year falls within the two years before an NBER defined peak and 0

otherwise and Trough takes a value of 1 if the current year falls within the two years following

an NBER defined trough. I also include an indicator variable, PTT, to measure the period

between the peak and trough, which means the years peak and trough are measured against

those that are more than two years removed from peaks or troughs. Including these indicators

allows me to track accounting fraud through the business cycle and to observe how accounting

fraud builds and falls. GDP Surprise is defined as the difference between actual GDP and

expected GDP as forecasted by the Survey of Professional Forecasters, provided by the

Philadelphia FED. Like GDP, GDP Surprise is detrended because the forecasts show evidence

of a trend. I include GDP Surprise because the decision to commit accounting fraud could be

related more to the performance-expectation gap than to performance per se. Because the vast

majority (over 75%) of observed cases of accounting fraud start in the fourth calendar quarter, I

measure and test macro variables contemporaneously with observed cases of accounting fraud

in both the time-series and survival analysis.

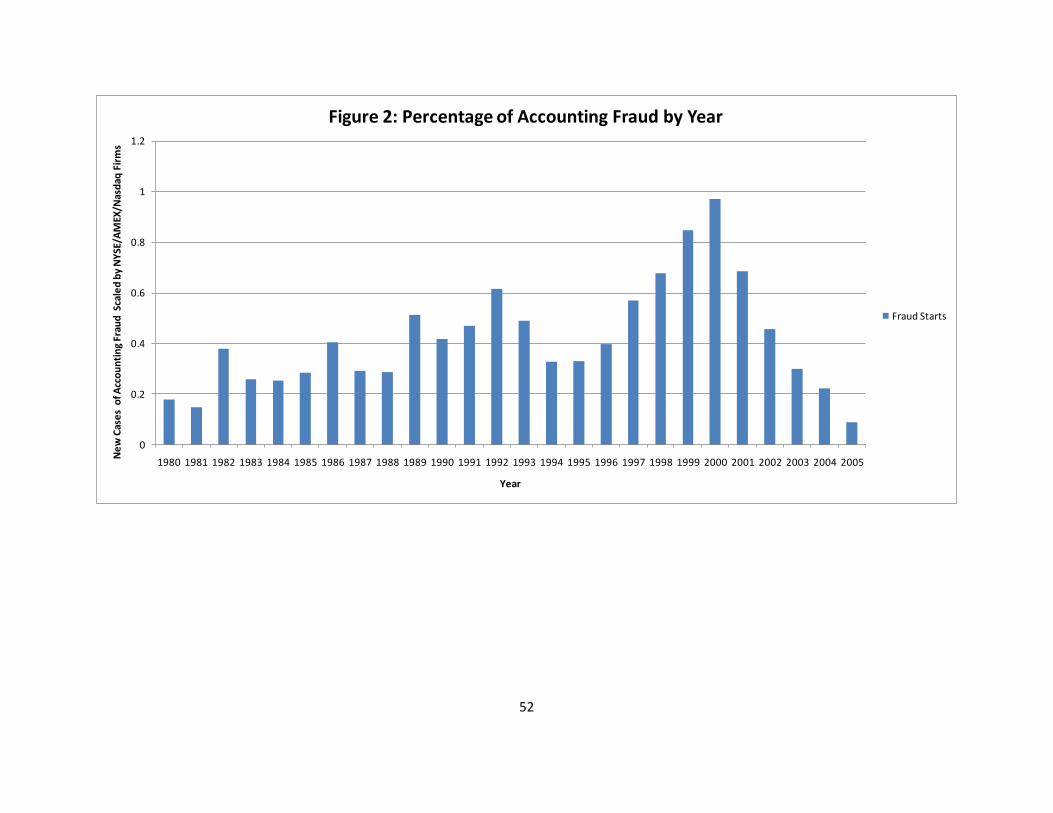

To control for the possibility that the level of accounting fraud is positively related to the

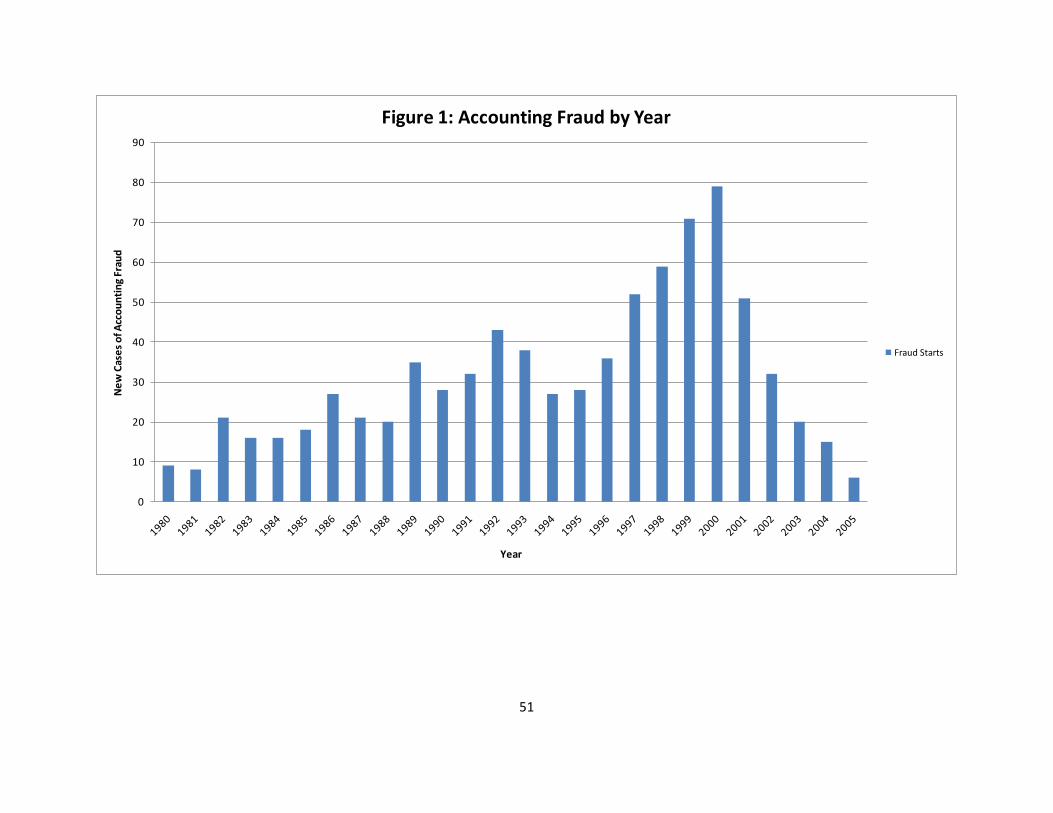

number of firms in the economy, I measure Fraud as a percentage. Figures 1 and 2 show the

effect of deflating accounting fraud by the number of Compustat firms. Figure 1 plots new

cases of detected accounting fraud by year. I find evidence of a time trend in accounting fraud.

However, as shown in Figure 2, when I replace the number of cases of accounting fraud with

the percentage of accounting fraud firms I no longer find such a trend over the sample period.

26

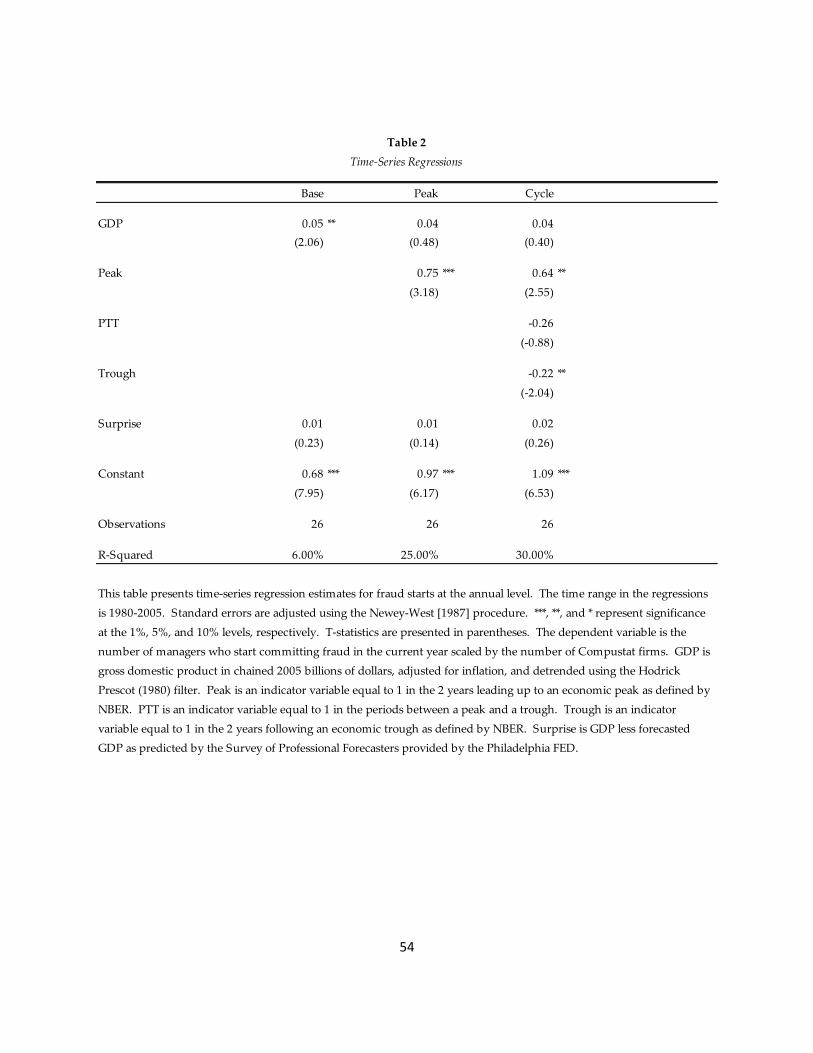

As presented in Table 2, the results from annual time-series regressions are consistent

with Hypotheses 1A and 1B. New cases of observed accounting fraud are positively related to

detrended GDP and economic peaks, and are negatively related to economic troughs. All time-

series standard errors are adjusted using the Newey-West correction. Because the dependent

variable is scaled by total Compustat firms, interpreting the magnitude of the coefficients yields

an increase in the percentage of fraud firms. The 0.05 coefficient on GDP in the base model of

Table 2 indicates that a one standard deviation increase in GDP ($141 billion) increases the

percentage of fraud firms by 0.07 percent. In 1996, for example, this increase translates into 6

additional cases of accounting fraud - a result that is both economically significant and feasible.

These findings are consistent with the theoretical literature, which predicts that managers are

more likely to commit accounting fraud in strong economic periods.

Survival analysis allows me to extend tests to the firm level and allows for both

macroeconomic and firm-level controls. To test Hypothesis 1A and 1B, I estimate a Cox

proportional hazards model of the following general form:

_ _ _i j kfraud macro perf macro controls firm controls . Fraud is now an

indicator variable equal to 1 in the period during which failure occurs (i.e., when the manager

starts committing accounting fraud) and 0 otherwise. Macroeconomic controls include GDP

surprise, stock market volatility, the default risk premium, the number of IPOs in the previous

three years, and the SEC budget appropriation. Stock market volatility captures some aspect of

the information environment; accounting fraud could be related more to variance in

performance and expectation than to actual output per se. The default risk premium controls

27

for default risk and the rate at which future cash flows are discounted in the price-earnings ratio

analysis. Many AAERs report that the detection of fraud came after the firm became insolvent

and no longer had enough cash to service its debt obligations or continue operating. The

number of IPOs over a 3 year period controls for changes in the composition of firms in the

economy. Generally, the number of IPOs increases during periods of prosperity; if a large

number of fraud firms are IPO firms, then it is possible that the observed increase in accounting

fraud during strong economic periods is related to concurrent increases in the number of IPOs.

Though the number of IPOs is unlikely to influence individual fraud firms, it could still explain

a significant coefficient on GDP. The SEC’s budget appropriation controls for the SEC’s ability

to detect and litigate accounting fraud. As suggested in Dyck et al [2007] the SEC is often not

the first agent to detect accounting fraud, which means the SEC budget may not control for a

large portion of the detection environment. However, since my sample of fraud firms is

collected from SEC AAERs, the SEC budget should effectively control for the effect of litigation

constraints on the sample. I have no clear prediction for the relation between fraud and the SEC

budget. On the one hand, if the SEC having additional resources makes accounting fraud more

costly, then we should observe fewer cases of accounting fraud in periods wherein the SEC has

an increased budget. On the other, if these increases in the SEC budget are in response to

increase in fraudulent reporting, then we could observe a positive relation.

I include the following firm-level determinants of accounting fraud as controls: a raising

capital indicator variable, lagged abnormal returns, and deltas of CEO incentive compensation

and net worth. Capital takes a value of 1 if the firm issued debt or sold common shares in the

28

current period and 0 otherwise. Dechow [1996] argue that among the reasons managers commit

accounting fraud is that the inflated share price reduces the cost of raising capital. Dechow et al

[2010] test several different proxies of dependency on external financing and find that,

compared with other proxies, an indicator for whether the firm raised capital in the fraud year

has superior predictive power. Lagged abnormal return is defined as the value-weighted

market adjusted firm return for the previous year. Dechow et al [2010] argue that managers

whose firms have optimistic expectations built into their stock price may be more prone than

other managers to misstate their earnings for the purpose of hiding decreasing performance. A

significant coefficient on this variable supports the hypothesis that high expectations and

market driven incentives are among the reasons managers commit accounting fraud. Incentive

compensation is measured using the delta of current CEO option grants based on Black Scholes

values and the delta of all CEO stock options based on Execucomp values. Wealth is measured

using the delta of all shares held by the CEO based on Execucomp values. While the relation

between accounting fraud and incentive compensation is not clear, it is nevertheless an

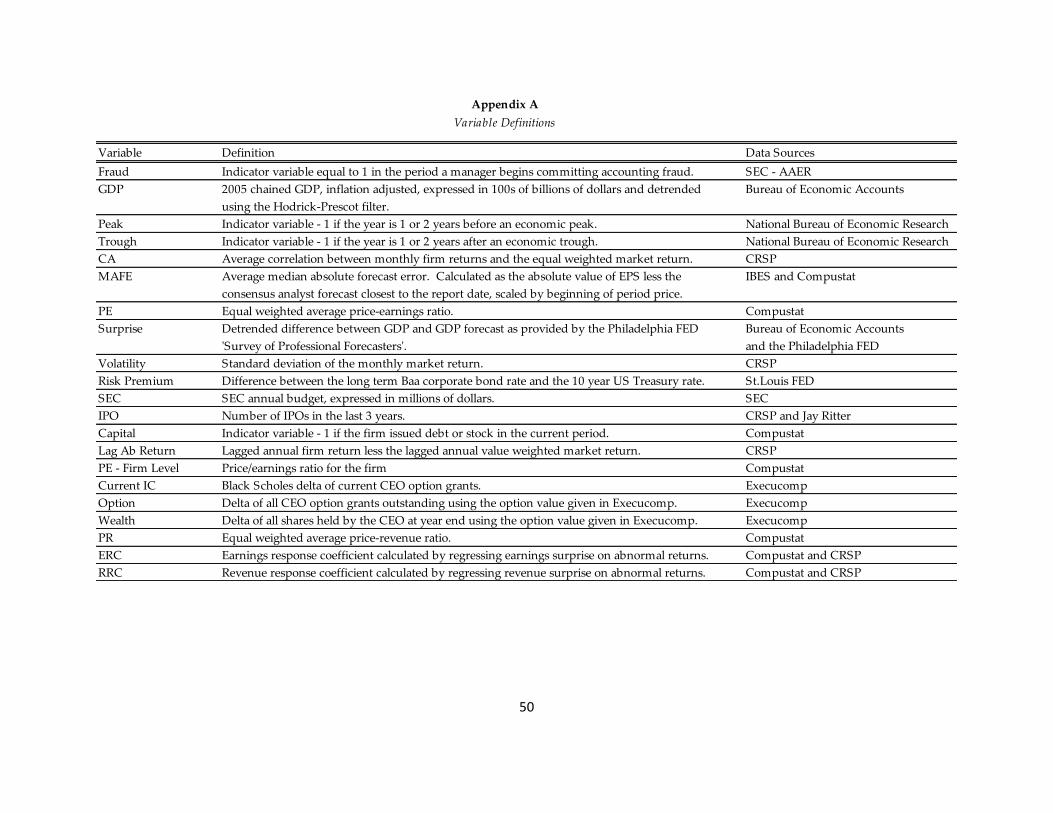

important consideration. All variables are defined in Appendix A.

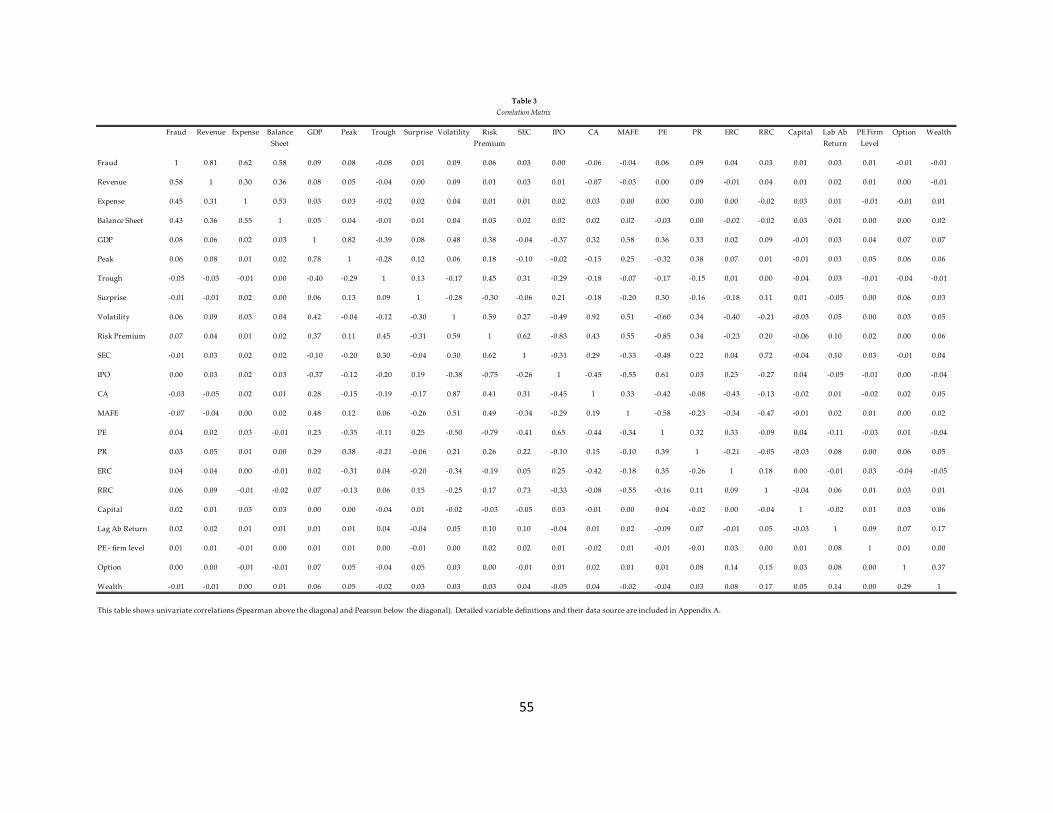

Table 3 presents Spearman and Pearson correlations for variables I use in survival

analysis. Univariate correlations between accounting fraud, macroeconomic performance, and

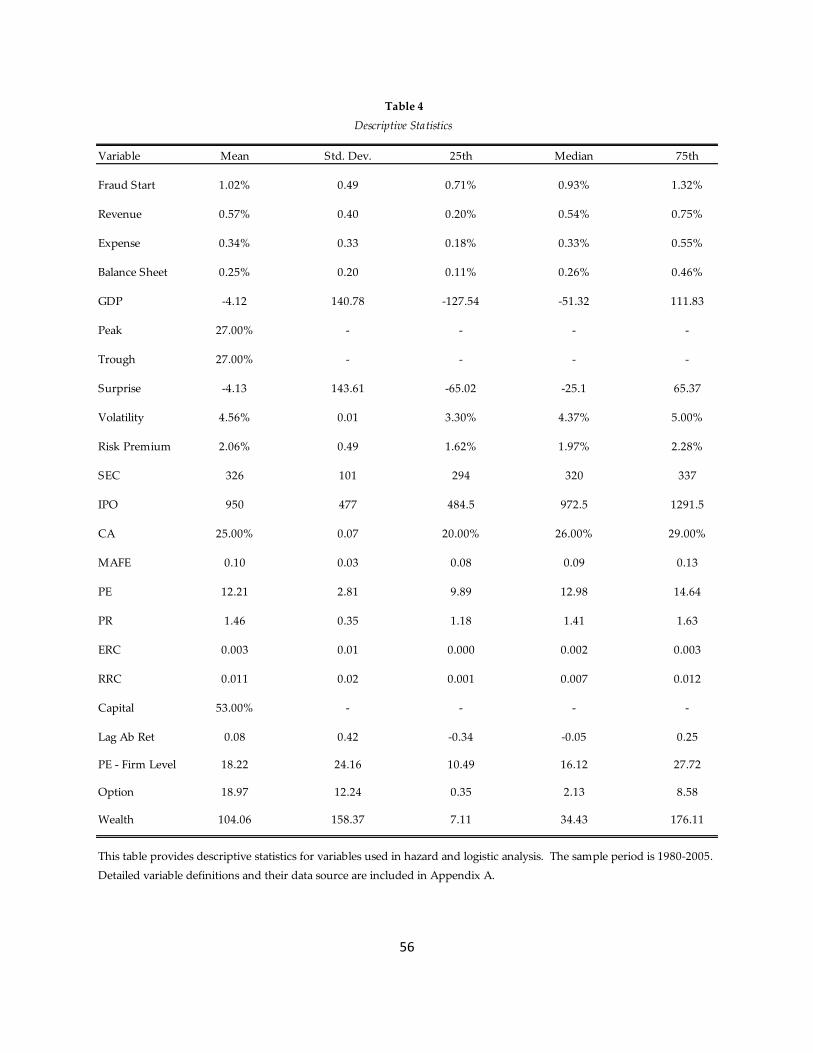

the market incentive proxies are consistent with Hypotheses 1 and 2. Table 4 presents

descriptive statistics for the variables used in survival analysis. Each year, approximately 1

percent of managers of firms listed on Compustat start committing fraud. GDP can show a

negative mean because the values are detrended. The value for the peak and trough indicators

29

is the percentage of years that meet the inclusion criteria. The firm-level variables (i.e., lagged

abnormal returns, current IC, option, and wealth) are winsorized at the 1 percent level to reduce

the influence of outliers.

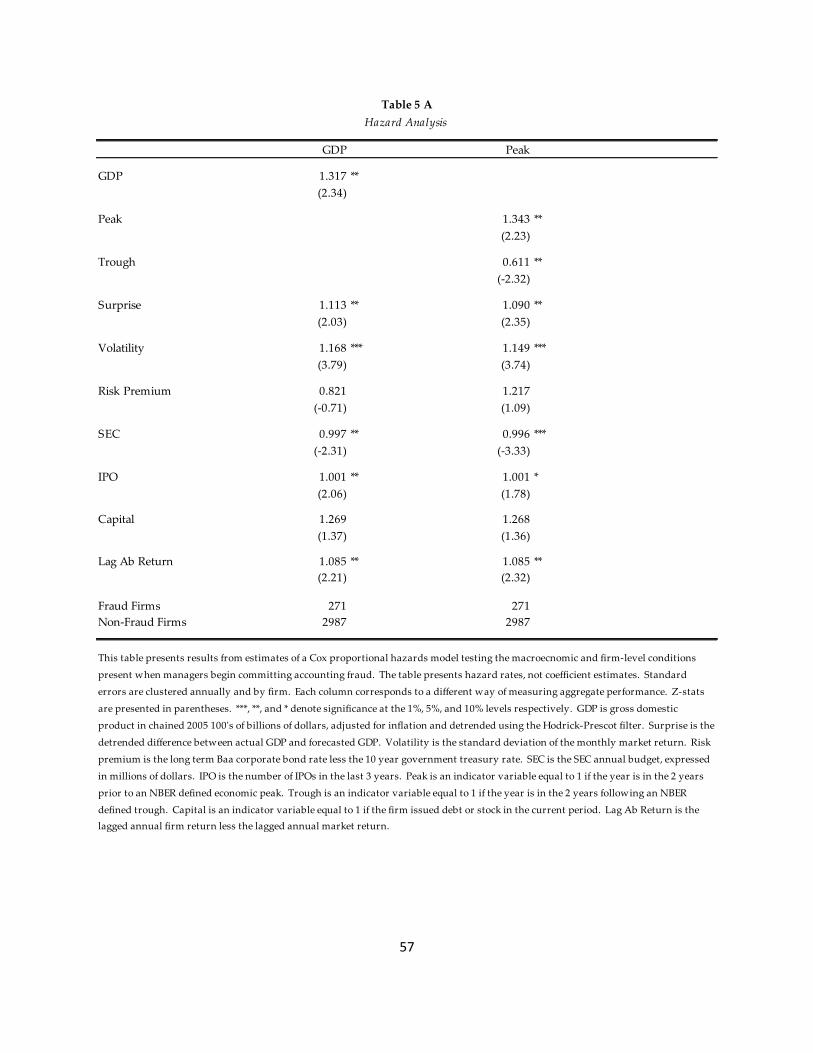

Tables 5A and 5B report results supporting Hypotheses 1A and 1B. GDP and economic

peaks are significant and positively related to the hazard rate while economic troughs are

negatively related to the hazard rate. I find that more managers start to commit accounting

fraud in periods of strong aggregate performance and in the two years leading up to an

economic peak.

In addition, I find that the SEC variable is negative and significant. This finding

suggests that managers are less likely to commit accounting fraud in periods wherein the SEC

has more resources at its disposal. Incentive compensation is negatively related to accounting

fraud and is significant when measured using the delta of CEO stock options. The economic

effect appears small though; a base hazard rate of 1.000 indicates that the variable has no effect

on whether fraud occurs and the hazard rate for incentive compensation always falls between

0.998 and 0.999. To decrease the likelihood of accounting fraud by even 1 percent, the delta of

options would have to increase by several standard deviations.

The hazard rate for the risk premium is negative in the GDP models and positive in the

peak/trough models, though it is not significant in any estimation. As Table 3 shows, the risk

premium is highly correlated with GDP and economic troughs. Finding that the risk premium

is not highly correlated with non-trough periods could explain why the hazard rate switches

30

from negative to positive. The hazard rate for IPO is positive and significant in Table 5A but is

negative (though insignificant) in Table 5B. This switch, however, is not driven by a correlation

with IPO and compensation measures; what causes the switch is not clear, but in an economic

sense, the hazard rate of 0.999 in Table 5B is not significant. The relation between raising capital

and accounting fraud is positive, as predicted by the extant literature, but not significant. This

finding, however, could be due to the downward bias of coefficients that attends modeling rare

events in non-linear models, as documented by King and Zeng [2001]. Time variance in the

relation is explored in Table 9. The relation between lagged abnormal returns and accounting

fraud is positive, consistent with Dechow et al [2010], though it is significant only in Table 5A.

One explanation for this finding is that the relation is not strong enough to be detected with the

smaller number of fraud observations included in the tests presented in Table 5B.

To mitigate the potential of downward bias of the coefficients that typically attends

models of rare events, I perform my analysis using a subset of non-fraud firms. King and Zeng

[2001] provide a detailed discussion of the difficulty of modeling rare events. To summarize,

the difficulty arises for two reasons: (1) because the statistical properties of binary regression

models are not invariant to the (unconditional) mean of the dependent variable and (2) because

the method of computing probabilities of events in logit analysis is suboptimal in finite samples

of rare events data. Indeed, King and Zeng [2001] show that the biases can be as large as some

of the estimated effects reported in the literature. Given that fraud firms represent

approximately 1 percent or less of the population in most periods, accounting fraud qualifies as

a rare event. As using a random subsample of observations drawn from the total population is

31

one technique for dealing with this issue, I select 15% of Compustat firms during the sample

period.13 To be included in the analysis, firms must have two years of data.14

Because incentive compensation data is only available for a subset of firms and only

from 1992 onward, I report my results in two separate tables. The hazard models presented in

Table 5B include 104 fraud firms and 1046 non-fraud firms. In both tables, standard errors are

clustered by firm and by year.

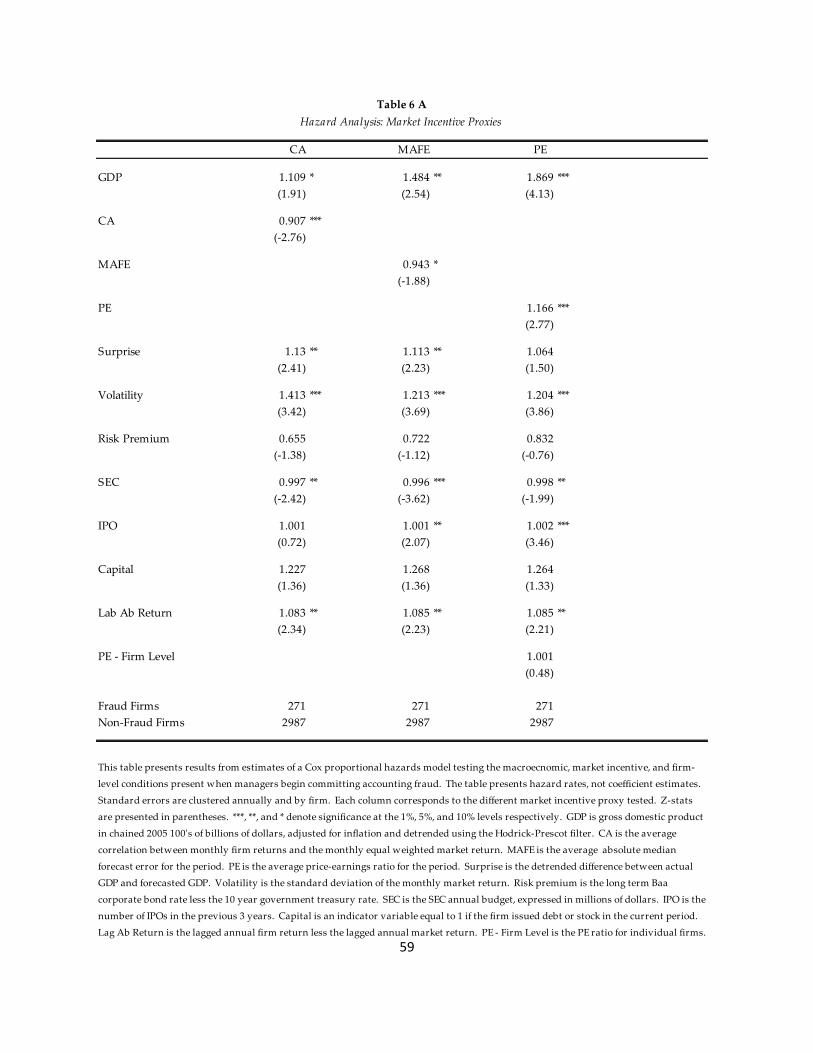

I test Hypothesis 2 using survival analysis. Here, I extend the Cox proportional hazards

model I estimated to test Hypothesis 1 to include three proxies for market wide incentives. The

market-incentive proxies measure the average correlation between firm returns and the market

return, the average median absolute forecast error for the period, and the average price-

earnings ratio for the period. Because these proxies are reasonably highly correlated with one

another, I test each proxy separately.

How much weight the market places on idiosyncratic news influences the benefit of

committing accounting fraud. Ang and Chen [2002] show that the correlation between firm

returns and the market return is systematically correlated with the business cycle. The

correlation is relatively high during recessions and relatively low during booms. During

13

I conducted hazard analysis using random samples of 5%, 10%, and 15% of the Compustat population and found

that the magnitude and statistical significance of my results remained unchanged. Further, 25 random samples

were generated to insure that the results were not determined by the specific firms in the random sample.

14 Two years of data is required to calculate lagged abnormal returns for the fraud year. My results are not

sensitive to this distinction. I repeated my analysis requiring three years of data and imposing no restriction on the

data with similar results in terms of magnitude and statistical significance. Requiring more than two years of data

severely reduces the size of my sample.

32

recessions, price is primarily determined by news about markets and industries with firm-level

news being of relatively low importance. During booms, on the other hand, the market places

greater weight on idiosyncratic news when setting price. In periods wherein firm news is more

important than market news, managers have more to gain from fraudulently inflating earnings.

In periods wherein strong inferences about individual ability are made from reported earnings,

managers may face a greater risk of losing their job if they report performance below their

firm’s expectations.

Earnings news is not highly informative without context. Whether it is explicitly written

into compensation contracts or used as a general evaluation metric, firm performance is

measured against that of other firms in the economy. A firm that misses its forecast is evaluated

differently in periods wherein many firms miss their forecasts than in periods wherein few

firms miss their forecasts. Uncertainty about performance can also affect incentives to commit

accounting fraud. In periods characterized by high uncertainty and low forecast accuracy, both

the ex ante forecast and whether or not that forecast is met are likely to have a dampened effect

on price. There are many explanations for high uncertainty about performance and low forecast

accuracy and many of these also explain poor performance. The less certain the market is when

forming expectations, the less likely it is to be surprised when a manager falls short. As such,

managers have fewer incentives to commit accounting fraud when predicting performance is

difficult.

The sensitivity of price to news can, over time, greatly change the incentives to commit

accounting fraud. In periods wherein earnings has a large effect on price, managers will

33

experience stronger incentives to avoid reporting poor performance. As mentioned in Dechow

et al [2010], class action lawsuits are often filed against firms when their stock prices suffer large

decreases. Managers have strong incentives to avoid these lawsuits and the large decreases in

their firm’s stock price that precede them. Additionally, the effect of fraudulently inflating

earnings on a manager’s wealth will be higher in periods wherein these inflated earnings have

the largest effect on price. Price is determined by discounting expected future cash flows.

Dechow et al [1998] find that earnings is a better predictor of future cash flows than is cash

flows itself. That investors revise their expectation of future cash flows based on current

earnings is well established. As such, while price-earnings ratios should capture the market’s

sensitivity to earnings news, they will also capture the discount rate the market applies to

future cash flows. I therefore include the market risk premium to control for the discount rate

and to allow the PE ratio to be interpreted as a measure of the sensitivity of price to earnings

news.

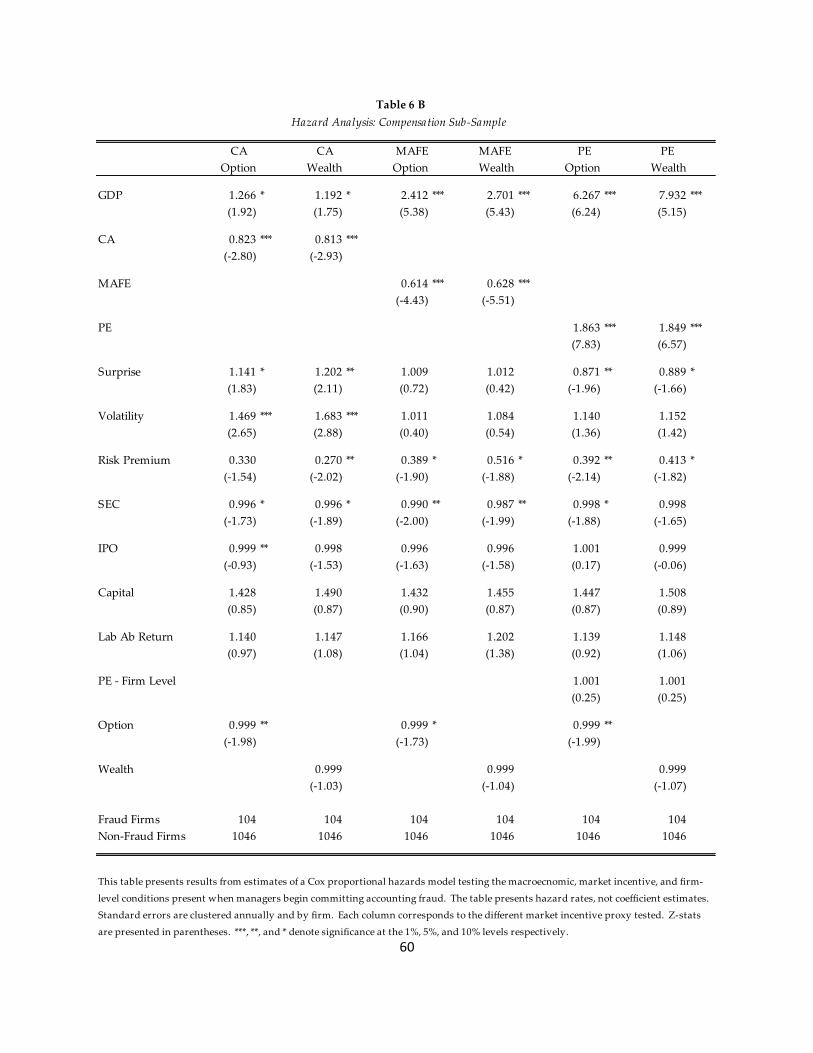

The results I obtain for Hypothesis 2, which are presented in Tables 6A and 6B, are

strong for all three proxies for market wide incentives. The hazard rates for covariance

asymmetry (CA), median absolute forecast error (MAFE), and price-earnings ratio (PE) are all

significant in the predicted directions. The proxies are significant at the 1 percent level in every

estimation except for one, that is, the MAFE in Table 6A, which is significant at 10 percent. The

results for Hypothesis 2 suggest that managers are more willing to commit accounting fraud

when share price is determined more by firm-level news than by market news. Ceteris paribus

34

it is reasonable to expect that as the market places more weight on managerial ability, more

managers will commit accounting fraud.

The results also suggest that managers will be more likely to commit accounting fraud in

periods wherein earnings are easier to predict. Several interpretations are consistent with this

result: on the one hand, it could be managers are penalized more severely for falling short in

periods wherein earnings are easier to predict; on the other, it could be that, in periods wherein

earnings are more difficult to predict, managers have several plausible explanations for their

failure to meet performance expectations. It could also be that managers feel more comfortable

borrowing from the future in periods wherein performance is easier to predict.

Finally, I find that more managers start to commit accounting fraud in periods of high

price sensitivity to short-term earnings news. This finding is consistent with the predictions

made in Benmelech et al [2010]. Both the penalty for reporting poor performance and the

benefit of exceeding expectation are generally higher when news has a stronger effect on price.

I include in this model the PE ratios of individual firms to discern whether increases in the

individual fraud firms’ PE ratios drive the significance on the aggregate PE ratio. Ultimately, I

find that the firm PE ratio is insignificant, while the aggregate PE ratio is positive and

significant. This finding suggests that what creates the strongest incentives to misreport for

managers is economy wide price sensitivity to news. Incentives for managers to commit fraud

are high when all firms in the economy have high expectations built into their share price.

35

Results for the risk premium, the SEC budget, IPO, capital, and lagged abnormal returns

are similar in direction and significance to those reported in Tables 5A and 5B. Results for

macroeconomic volatility are consistent across Tables 5A and 6A, but not across Tables 5B and

6B. Volatility is highly correlated with the market incentive proxies analyzed in Table 6, which

could explain the inconsistent results for this variable. Results for GDP surprise are similar to

the results for volatility – they are consistent across the A tables, but not across the B tables. The

reduced number of fraud firm observations in the B tables could lead to a lack of power to

detect weaker relations.

Macroeconomic variables are often correlated with multiple forces. Though the market

wide incentive proxies arguably do capture market wide incentives, they may also be correlated

with other factors that could influence a manager’s decision to commit accounting fraud. Two

related explanations for time-variance in accounting fraud are changes in the detection

environment and changes in the litigation environment. Though it is not clear in what direction

either would be correlated with my sample of accounting fraud, it is possible that they affect a

manager’s decision to commit fraud in the same way I argue market wide incentives do. In

periods wherein monitors exert high effort, it is reasonable to assume that a higher proportion

of accounting fraud will be detected. If this is true and if, in addition, periods wherein monitors

exert high effort are correlated with periods of strong aggregate performance, then an increase

in the number of detected cases of accounting fraud in these periods could derive from an

increased detection rate and not from an increase in the number of managers reporting

fraudulently. While measuring effort empirically is difficult, most theoretical research finds

36

that monitoring effort actually decreases during periods of strong aggregate performance. This

finding argues against the conclusion that increases in AAERs during periods of high

performance derive from an increased detection rate of accounting fraud.

On the other hand, if monitors do in fact reduce their effort during good times, then one

could argue that their reduced effort increases the true number of fraud firms in the economy,

which in turn may explain part of the increase in detected cases of accounting fraud. Again, the

difficulty in measuring effort makes this hypothesis hard to test or refute. Dyck et.al. [2007]

find that whistleblowers detect more cases of accounting fraud than other agents do. Further,

they find that a large amount of accounting fraud is detected by agents that are not employed as

monitors; they note in particular that the media and analysts detect a reasonable number of

fraud cases. It is not clear whether the benefits one stands to gain from breaking a big story or

the ethics and/or willingness of a lower level employee to speak up vary much over time, or are

correlated with market covariance asymmetry or price-earnings ratios. Whistleblowers in

particular do not monitor the firm per se and tend to uncover fraudulent activity simply in the

course of doing their job. If the effort levels of agents that detect the vast majority of accounting

fraud cases do not vary over time, then the detection environment is less likely to be a concern

in this setting.

The evidence suggests that the SEC budget effectively controls for changes in the

litigation environment. The relation between accounting fraud and the SEC budget is negative

and significant in almost every estimation, which is consistent with fewer managers committing

accounting fraud in periods wherein the SEC has more resources at its disposal. Controlling for

37

changes in the detection environment is more difficult. The SEC budget should control for the

SEC’s resources for detecting accounting fraud, but as mentioned above, many other agents

detect accounting fraud. Moreover, data on the corporate governance characteristics of firms or

measures of abnormal audit fees are only available from the late 1990s onward and can be

calculated only for approximately 10 percent of the fraud firms in my sample.

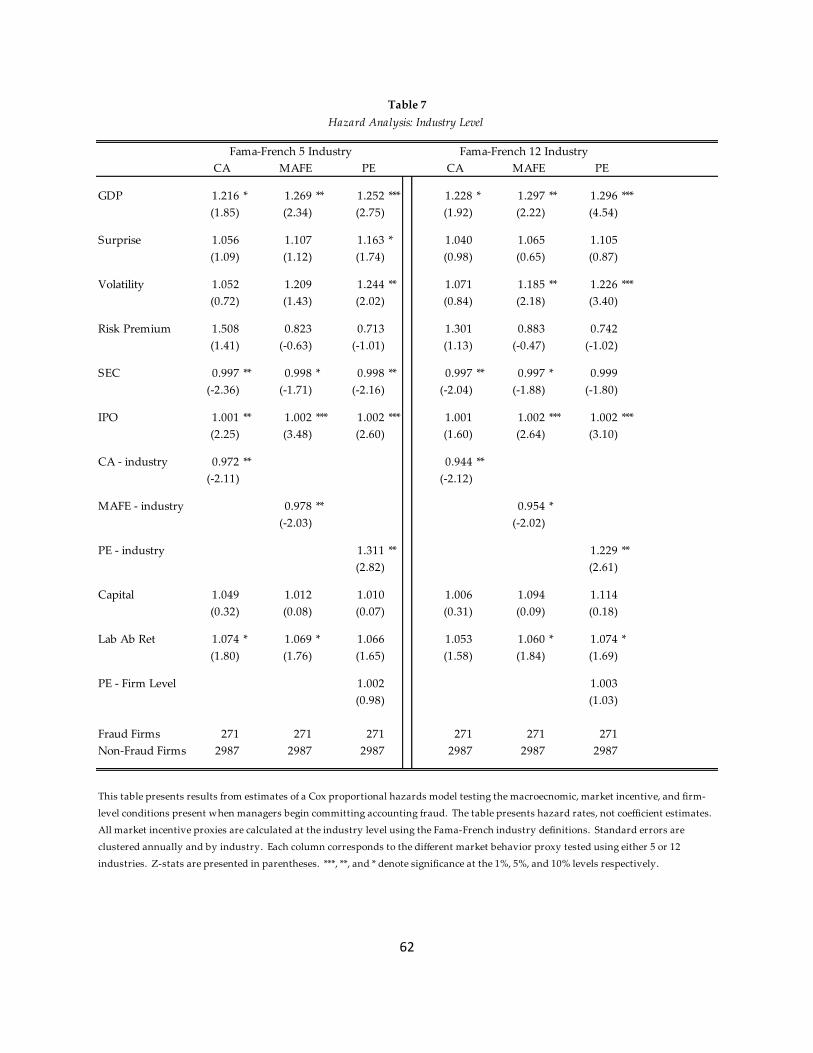

To reduce the likelihood that the statistical significance of the proxies for market wide

incentives derives from correlated omitted variables, I recalculate each of these proxies at the

industry level using the Fama-French 5 and 12 industry definitions and re-estimate the hazards

models. Doing so increases the cross-sectional variation in the proxies which should in and of

itself increase the reliability of the results. Assuming the cross-sectional variation reduces the

likelihood that the market incentive proxies also serve as proxies for changes in either the

detection or litigation environments, then these recalculations provide more support for the

market wide incentive hypothesis. As presented in Table 7, the results support Hypothesis 2.

The industry-level proxies for market wide incentives are statistically significant in the

predicted directions. To conclude that these results are driven by changes in detection or

litigation, I would need to find that the effort to detect accounting fraud or the propensity to

litigate for each separate industry changes with the proxies for market incentives measured at

the industry level. At the very least, such a finding is far less plausible than when the proxies

are measured at the economy level. The standard errors in Table 7 are clustered by industry

and by year. The control variables exhibit behavior similar to that reported in Table 6A. The

38

coefficient on the risk premium switches signs in the CA model (but is not significant); all other

variables behave similarly.

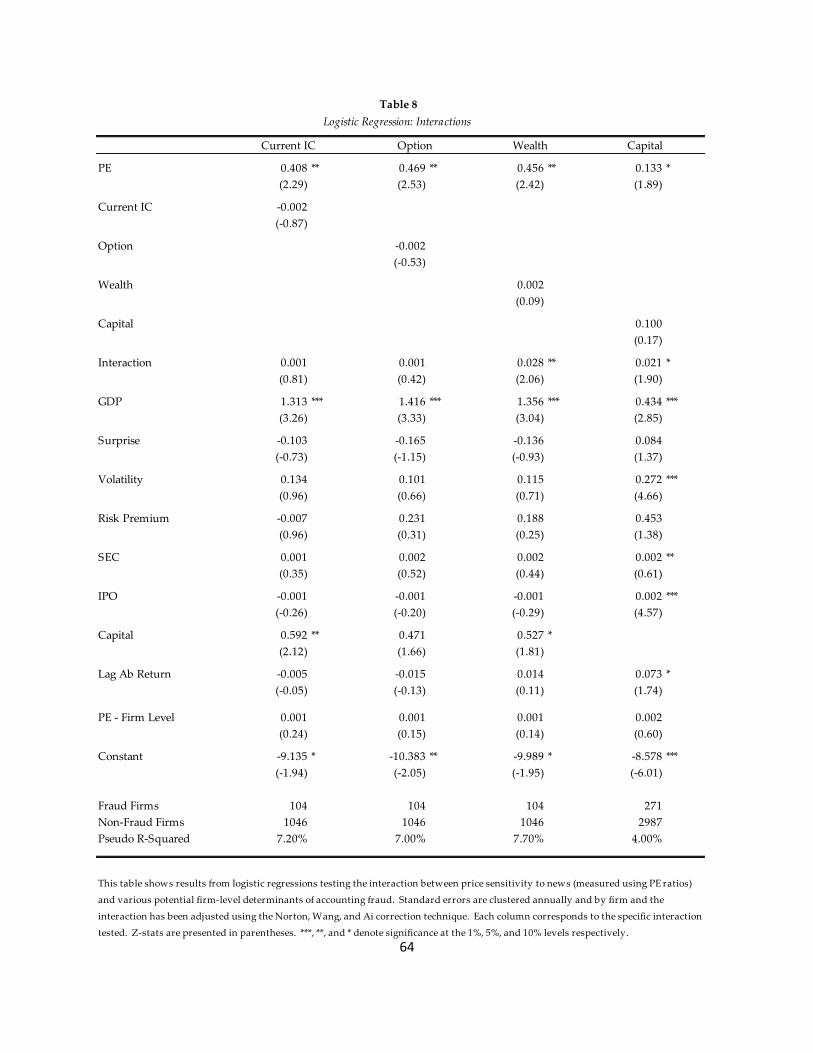

I use logistic regressions to test Hypotheses 3 and 4, namely, that the relations between

accounting fraud and incentive compensation and accounting fraud and raising capital,

respectively, are stronger in periods wherein price is highly sensitive to news. The evidence

presented in Table 8 supports Hypothesis 3. In general, the relation between CEO incentive

compensation or CEO net worth and the propensity to observe new cases of accounting fraud is

negative, as it is in Tables 5 and 6. However, when I interact the relation with PE ratios and test

the delta of all CEO shares held, it becomes positive and significant at the 5 percent level. These

findings are consistent with those of Benmelech et al [2010] and support the conclusion that a

CEO’s wealth positively influences their decision to commit accounting fraud in periods

wherein share price, and by extension wealth, is highly sensitive to short-term earnings news.

The difference in significance between shares held and options held could reflect a lack of

accuracy in the Execucomp values for total options/shares held. A superior approach would be

to calculate the CEO option delta using the Core and Guay [2002] methodology. I will make

this change in an updated version of this paper so that I can test a more accurate measure of

delta and the relation between CEO wealth and accounting fraud.

The evidence presented in Table 8 also supports Hypothesis 4. The relation between

raising capital and accounting fraud is positive and significant at the 10 percent level in periods

wherein price is highly sensitive to news. This result might explain the inconsistent results

found in the literature that study this question. Because the significance of this result is

39

relatively low, I re-estimate this regression substituting the net amount of new financing raised,

deflated by total assets, for the actual issuance indicator. This interaction coefficient is also

significant at the 10 percent level. Dechow et al [2010] use both of these measures in their initial

analysis but find stronger predictive power for the actual issuance indicator variable.

The results presented in Table 8 serve two purposes. First, they show the conditions

present when the incentives created by CEO compensation and a firm’s need to raise external

capital are strong enough to prompt more managers to commit accounting fraud. This aspect of

the results supports recent research on these firm-level determinants and can explain why past

studies have often reported contradictory results. Second, they show two of the channels

through which market wide incentives in the form of price sensitivity to news can influence

managers.

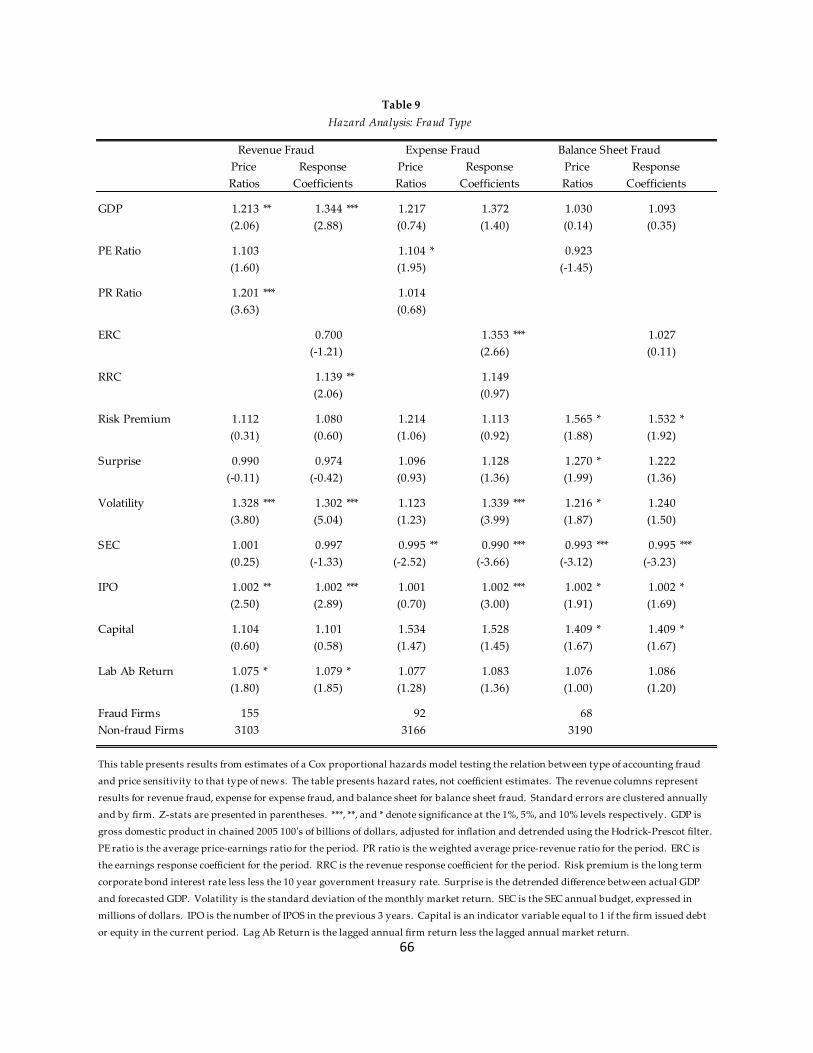

Table 9 presents the results of testing the differential effect of market incentives on fraud

type and provides further support for the Hypothesis 2. If capital and labor market incentives

are a primary determinant of accounting fraud, then we should observe a differential effect

when looking at different sources of incentives. In Table 9, I split fraud into three types -

revenue fraud, expense fraud, and balance sheet (i.e., non-income statement) fraud - and

analyze each using survival analysis. If revenue fraud is positively associated with price

sensitivity to revenue news, but expense fraud and balance sheet fraud are not, then I can

conclude more confidently that the results are driven by the sensitivity to news and not by

changes in the detection or litigation environments. In this table, the dependent variable takes a

value of 1 in periods wherein a manager commits accounting fraud of a certain type. For

40

example, in the revenue columns, fraud is equal to 1 if a manager commits revenue fraud and 0

otherwise.15 I measure the sensitivity of price to news using price-earnings and price-revenue

ratios and earnings response and revenue response coefficients. I did not include expense

measures because of their near perfect negative correlation with revenue measures.

Overall, results suggest that the type of fraud committed is related to sensitivity to news

of that type. Revenue fraud is positively and significantly associated with both the price-

revenue ratio and the revenue response coefficient, but not with the price-earnings ratio or the

earnings response coefficient. Expense fraud, on the other hand, shows the opposite results; it

is significantly associated with sensitivity to earnings news, but not with sensitivity to revenue

news. Expense fraud appears to be related to the portion of earnings news not related to

revenue news. Balance sheet fraud is not related to the sensitivity of price to news at all; given

that balance sheet fraud does not change earnings or revenues, this is to be expected.

Consistent with the notion that growth is valued in boom or high growth periods, the relation

between GDP and revenue fraud is positive and significant. The relation between GDP and

expense fraud is not significant.

Most cases of balance sheet fraud involve overstating reserves or improperly removing

debt from the balance sheet. One motivation for committing this type of accounting fraud is to

appear less debt constrained and less risky. Accounting fraud of this type is more beneficial in

15

The number of fraud firm observations across the three models does not equal 271 because of overlaps in the

type of fraud. In many cases, managers commit more than one type of fraud at a time. In untabulated results, I re-

estimate the hazard models, this time using firms that commit only one type of accounting fraud. While my results

are marginally stronger, this restriction significantly reduces the size of my sample.

41

periods wherein the risk of default is higher. Balance sheet fraud is positive and significantly

related to the default risk premium while revenue and expense fraud are not. This finding

further suggests that the relation between the incentive proxies and accounting fraud is driven

by changes in market wide incentives. Together, the results in Table 9 suggest that different

types of accounting fraud have different determinants.

These results suggest that studying the relation between all forms of accounting fraud

and market or firm-level determinants is not always the appropriate research design. To

properly test certain relations, the researcher may need to separate accounting fraud into

subgroups. It is possible that even my earlier tests which find significant relations between

accounting fraud and market covariance asymmetry and price-earnings ratios may sacrifice the

level of understanding we can gain from them. Table 3 reports that revenue fraud is negatively

correlated with covariance asymmetry, whereas expense fraud and balance sheet fraud are not.

Similarly, revenue fraud appears to be motivated by the component of PE ratios driven by

revenues whereas expense fraud appears motivated by the component that is not. Further,

balance sheet fraud does not appear to be motivated by PE ratios at all. Just as the total strength

of incentives managers have to misreport can vary over time, so too can the source of those

incentives.

6. Robustness Checks

My robustness tests are primarily intended to validate the proxies for market wide

incentives and to strengthen Hypothesis 2. Each proxy is measured in a second way and

42

retested in the same models. I use the r-squared from the following annual regression,

_ _firm return market return as an alternative measure of covariance asymmetry; this

proxy captures how well the market return explains firm returns each year. I use the

percentage of firms that fail to meet their consensus median analyst forecast as another measure

of the information environment and the predictability of earnings. This proxy captures how

often firms report earnings below their forecast, rather than capturing the magnitude of forecast

errors. Finally, I use an annual earnings response coefficient as another measure of the

sensitivity of share price to earnings news.

Untabulated results show that the additional market wide incentive proxies are

significant in the predicted directions. These results also suggest that the significant results I

find for the initial proxies are not likely the result of how the variables are constructed. These

results are available upon request. Further, including the hypothesized firm-level predictors of

accounting fraud from Dechow et al [2010] does not eliminate the significant predictive power

of the market incentive proxies. While this paper focuses on determinants of fraud and is not

attempting to create a prediction model, it is comforting to know that firm-level variables

cannot be used to explain the observed relation between macro variables and accounting fraud.

7. Future Work

The primary extension of this paper is to further develop the fraud type and differential

effects analysis. Having several clear and testable predictions supported by economic theory

will more strengthen the conclusion of my current analysis. Developing more proxies that

43

measure market wide incentives from different sources will strengthen the results presented in