Accounting for Insurance Contracts - sias.at · Italian GAAP Austrian GAAP German ... Insurance...

47

willistowerswatson.com Accounting for Insurance Contracts IFRS 4 and US-GAAP 5 th April 2018 Thorsten Wagner © 2018 Willis Towers Watson. All rights reserved.

Transcript of Accounting for Insurance Contracts - sias.at · Italian GAAP Austrian GAAP German ... Insurance...

willistowerswatson.com

Accounting for Insurance Contracts

IFRS 4 and US-GAAP

5th April 2018

Thorsten Wagner

© 2018 Willis Towers Watson. All rights reserved.

willistowerswatson.com 2© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Agenda

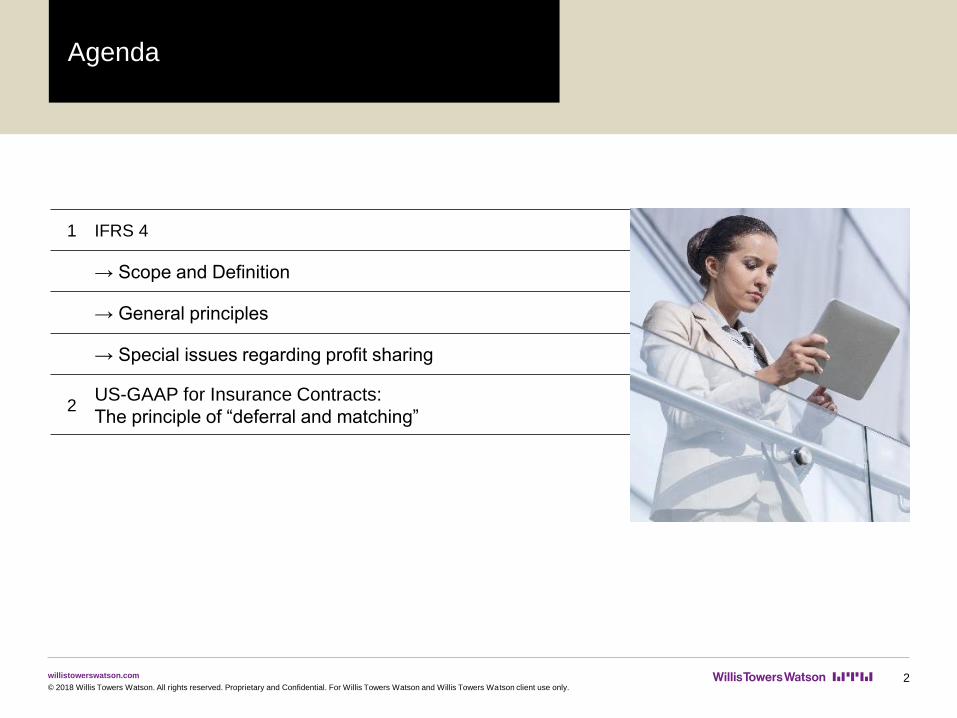

1 IFRS 4

→ Scope and Definition

→ General principles

→ Special issues regarding profit sharing

2US-GAAP for Insurance Contracts:

The principle of “deferral and matching”

willistowerswatson.com

IFRS 4: Introduction

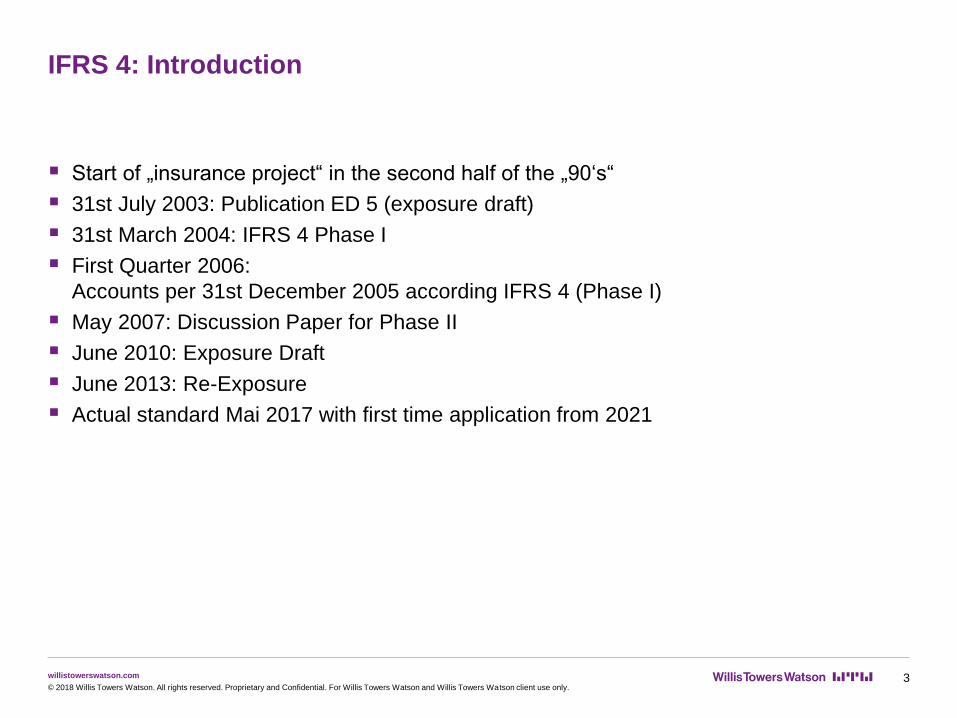

Start of „insurance project“ in the second half of the „90‘s“

31st July 2003: Publication ED 5 (exposure draft)

31st March 2004: IFRS 4 Phase I

First Quarter 2006:

Accounts per 31st December 2005 according IFRS 4 (Phase I)

May 2007: Discussion Paper for Phase II

June 2010: Exposure Draft

June 2013: Re-Exposure

Actual standard Mai 2017 with first time application from 2021

3© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: Introduction

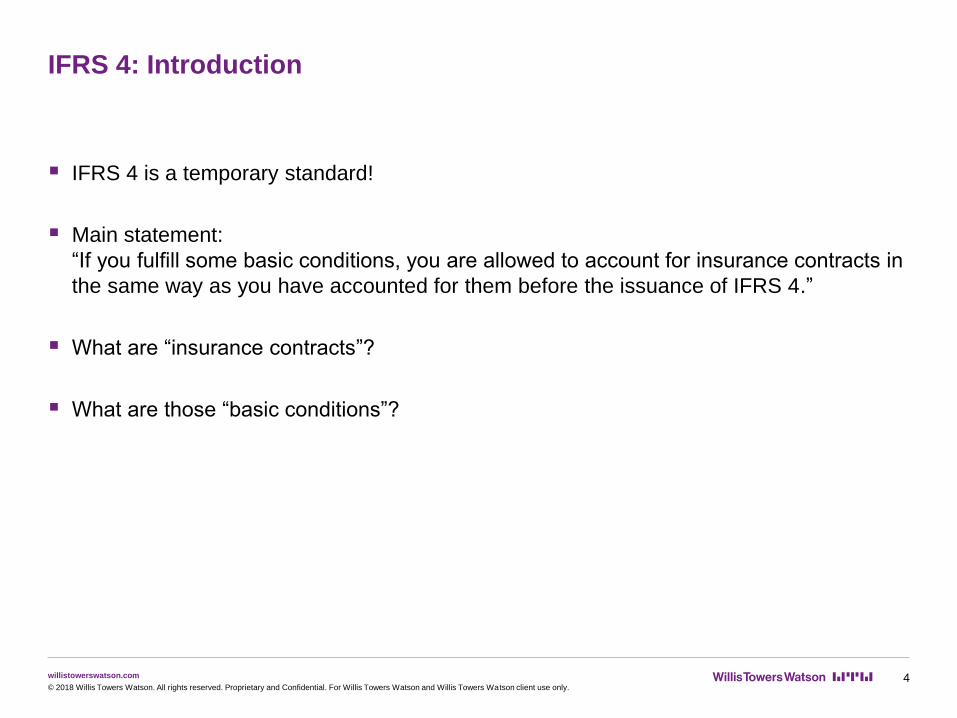

IFRS 4 is a temporary standard!

Main statement:

“If you fulfill some basic conditions, you are allowed to account for insurance contracts in

the same way as you have accounted for them before the issuance of IFRS 4.”

What are “insurance contracts”?

What are those “basic conditions”?

4© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: Introduction

But first of all:

What does it mean - for example for an international insurance company … ?

5© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: Introduction

6© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

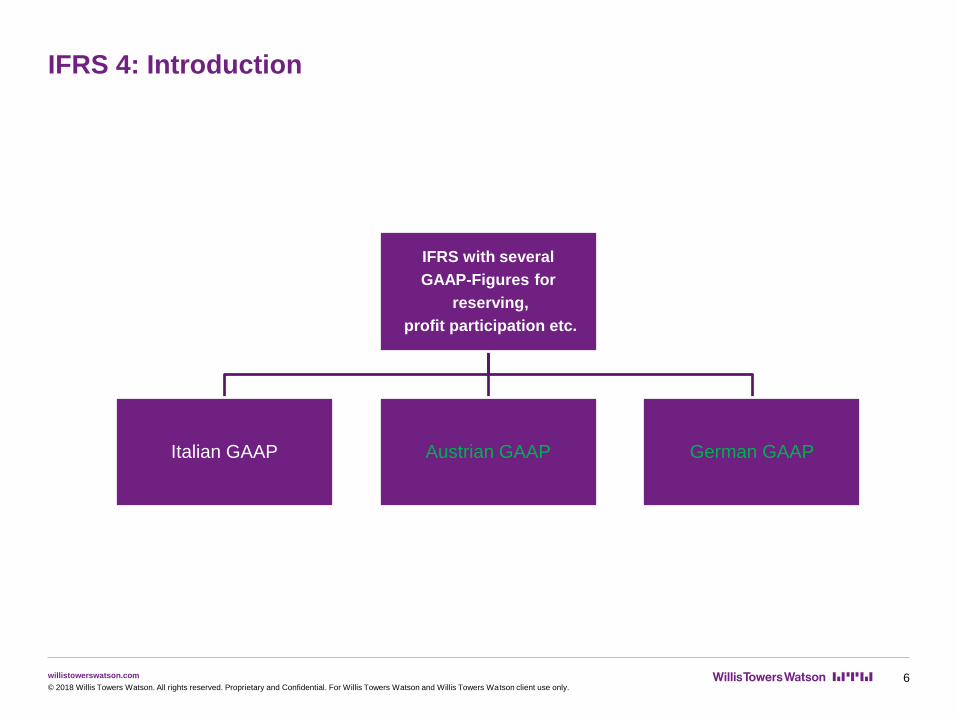

IFRS with several

GAAP-Figures for

reserving,

profit participation etc.

Italian GAAP Austrian GAAP German GAAP

willistowerswatson.com

IFRS 4: Scope

Basically will be unchanged in Phase II

(Re-) Insurance contracts (Re: activ and ceded)

financial instruments with a DPF:

“discretionary participation feature“

IFRS 4 shall not be applied for:

insurance companies in general

financial guarantees

accounting for the policyholder (except ceded re-insurance)

product warranties issued directly (manufacturer, dealer,…)

employee benefit plans (IAS 19 / IAS 26)

7© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: Definition

Definition “Insurance Contract“

significant insurance risk

compensation in case of a specified uncertain future event (insured event)

insured event has to affect the policyholder adversely

insured event may only occur in future periods

(e.g. not in the first five years but afterwards)

8© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: Definition

9© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

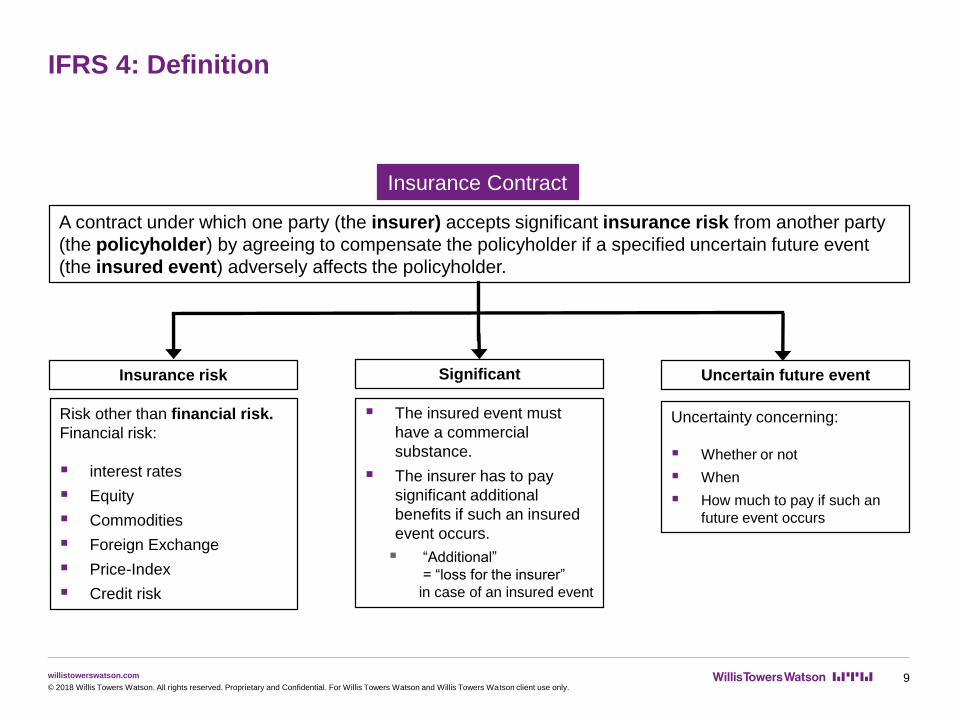

Insurance Contract

A contract under which one party (the insurer) accepts significant insurance risk from another party

(the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event

(the insured event) adversely affects the policyholder.

Uncertain future eventSignificantInsurance risk

Uncertainty concerning:

Whether or not

When

How much to pay if such an

future event occurs

The insured event must

have a commercial

substance.

The insurer has to pay

significant additional

benefits if such an insured

event occurs.

“Additional”

= “loss for the insurer”

in case of an insured event

Risk other than financial risk.

Financial risk:

interest rates

Equity

Commodities

Foreign Exchange

Price-Index

Credit risk

willistowerswatson.com

IFRS 4: Classification

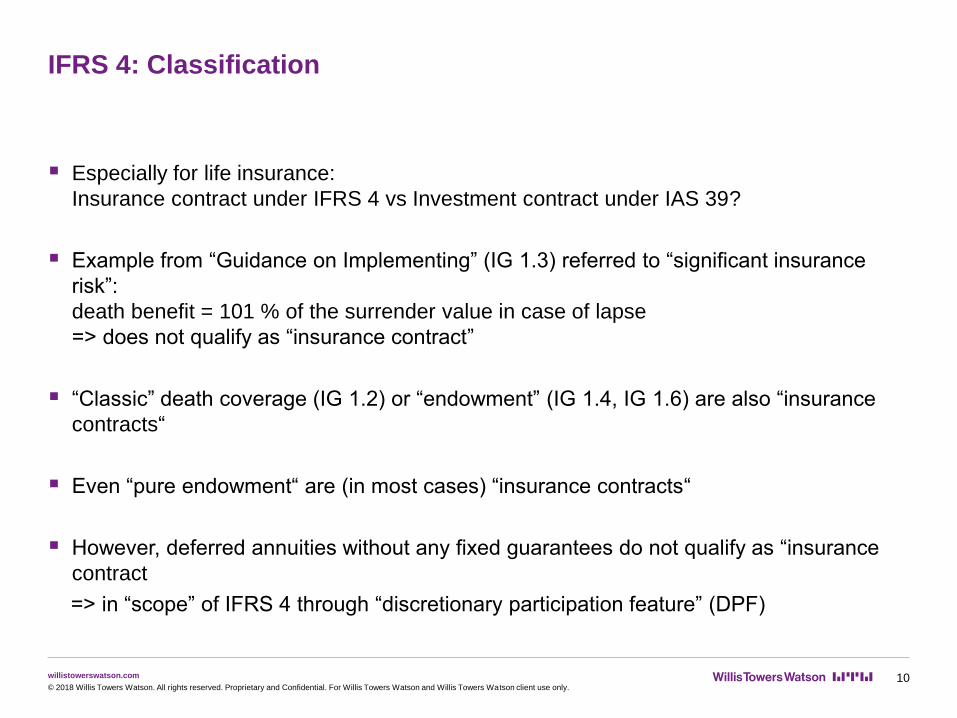

Especially for life insurance:

Insurance contract under IFRS 4 vs Investment contract under IAS 39?

Example from “Guidance on Implementing” (IG 1.3) referred to “significant insurance

risk”:

death benefit = 101 % of the surrender value in case of lapse

=> does not qualify as “insurance contract”

“Classic” death coverage (IG 1.2) or “endowment” (IG 1.4, IG 1.6) are also “insurance

contracts“

Even “pure endowment“ are (in most cases) “insurance contracts“

However, deferred annuities without any fixed guarantees do not qualify as “insurance

contract

=> in “scope” of IFRS 4 through “discretionary participation feature” (DPF)

10© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: Classification

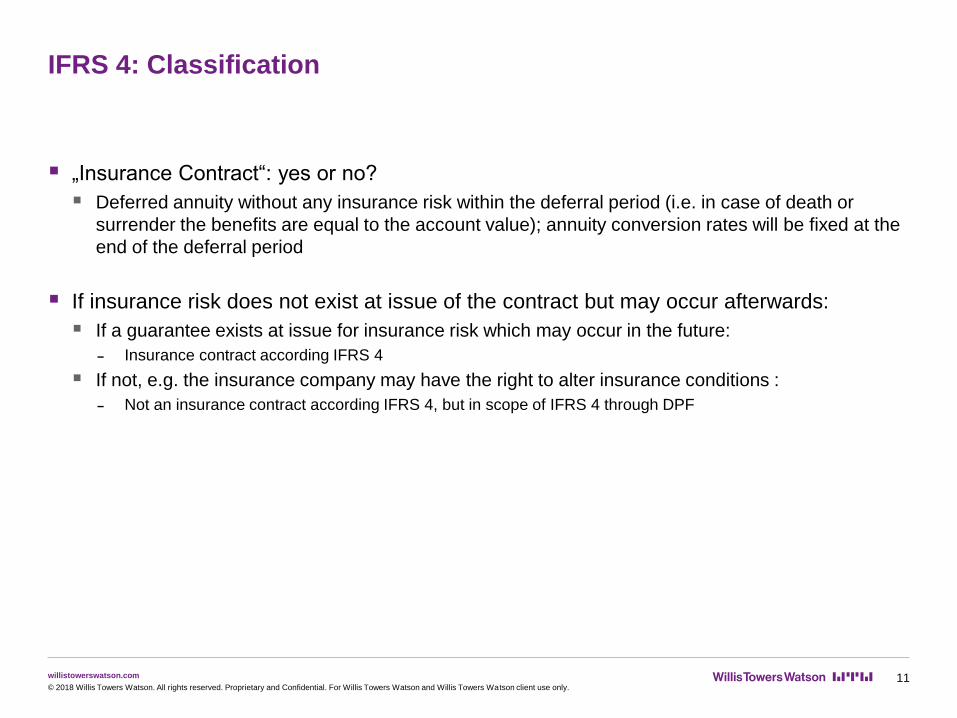

„Insurance Contract“: yes or no?

Deferred annuity without any insurance risk within the deferral period (i.e. in case of death or

surrender the benefits are equal to the account value); annuity conversion rates will be fixed at the

end of the deferral period

If insurance risk does not exist at issue of the contract but may occur afterwards:

If a guarantee exists at issue for insurance risk which may occur in the future:

Insurance contract according IFRS 4

If not, e.g. the insurance company may have the right to alter insurance conditions :

Not an insurance contract according IFRS 4, but in scope of IFRS 4 through DPF

11© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: “Accounting Policies”

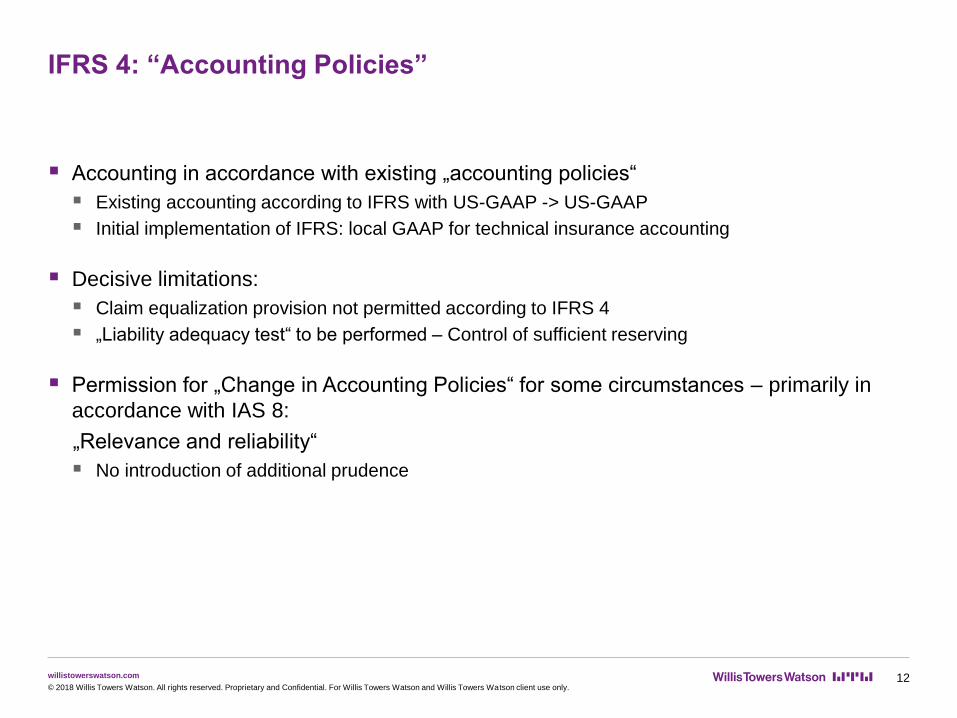

Accounting in accordance with existing „accounting policies“

Existing accounting according to IFRS with US-GAAP -> US-GAAP

Initial implementation of IFRS: local GAAP for technical insurance accounting

Decisive limitations:

Claim equalization provision not permitted according to IFRS 4

„Liability adequacy test“ to be performed – Control of sufficient reserving

Permission for „Change in Accounting Policies“ for some circumstances – primarily in

accordance with IAS 8:

„Relevance and reliability“

No introduction of additional prudence

12© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

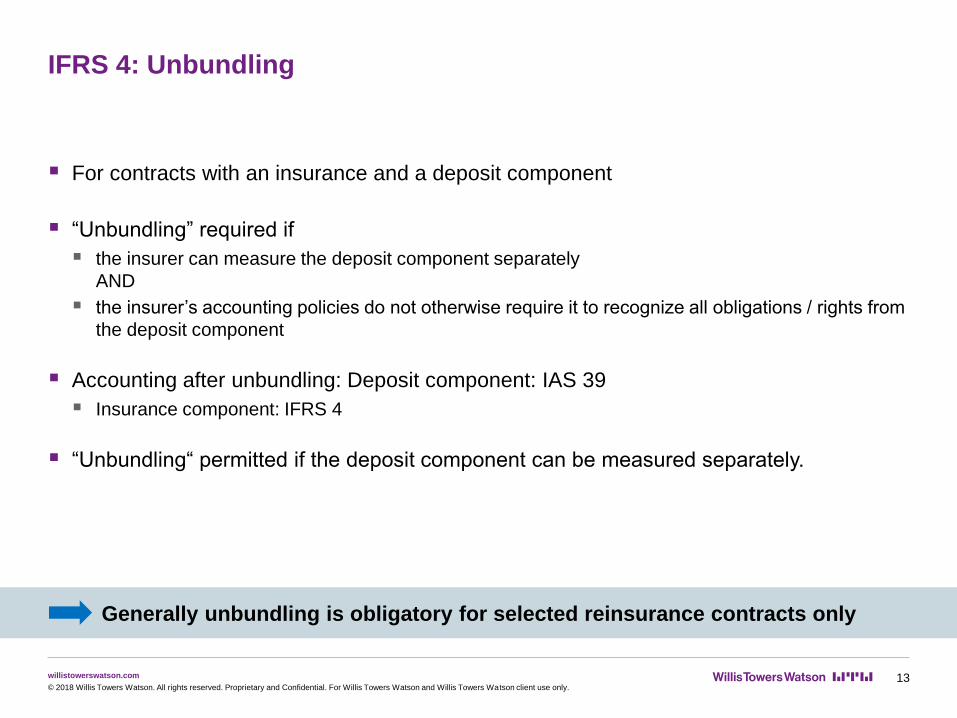

IFRS 4: Unbundling

For contracts with an insurance and a deposit component

“Unbundling” required if

the insurer can measure the deposit component separately

AND

the insurer’s accounting policies do not otherwise require it to recognize all obligations / rights from

the deposit component

Accounting after unbundling: Deposit component: IAS 39

Insurance component: IFRS 4

“Unbundling“ permitted if the deposit component can be measured separately.

13© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Generally unbundling is obligatory for selected reinsurance contracts only

willistowerswatson.com

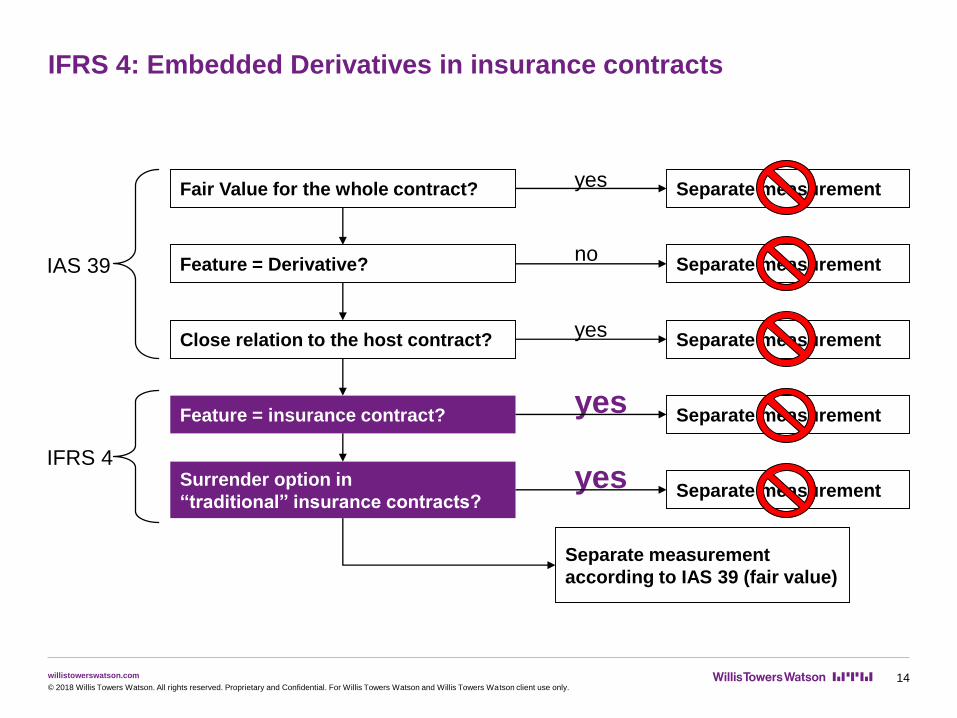

IFRS 4: Embedded Derivatives in insurance contracts

14© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Fair Value for the whole contract?

Feature = Derivative?

Close relation to the host contract?

Feature = insurance contract?

Surrender option in

“traditional” insurance contracts?

Separate measurement

Separate measurement

according to IAS 39 (fair value)

no

yes

yes

yes

yes

Separate measurement

Separate measurement

Separate measurement

Separate measurement

IAS 39

IFRS 4

willistowerswatson.com

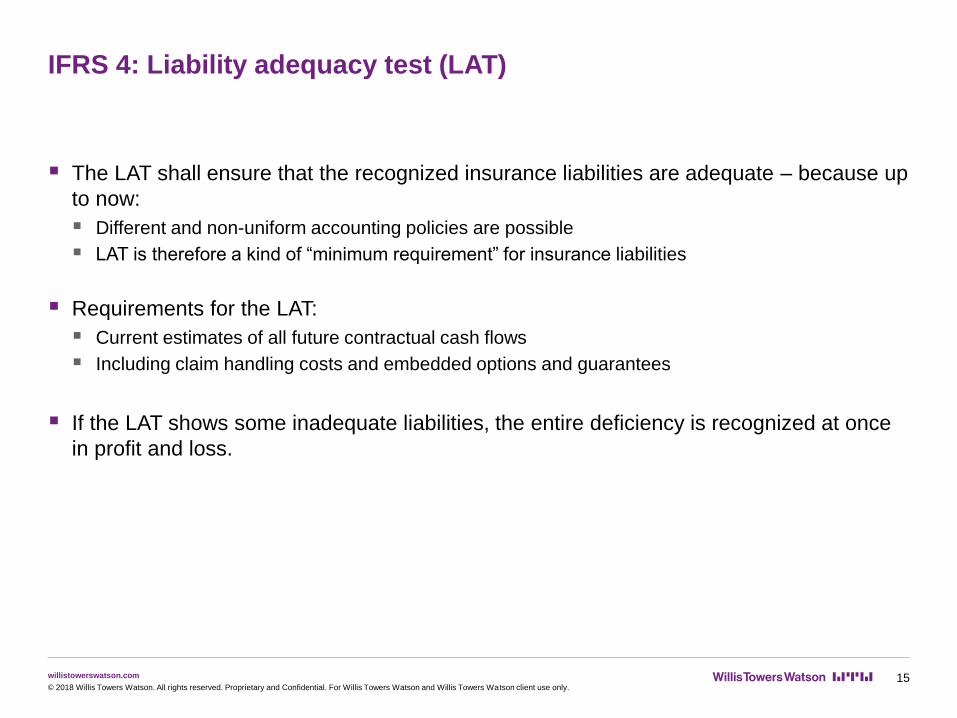

IFRS 4: Liability adequacy test (LAT)

The LAT shall ensure that the recognized insurance liabilities are adequate – because up

to now:

Different and non-uniform accounting policies are possible

LAT is therefore a kind of “minimum requirement” for insurance liabilities

Requirements for the LAT:

Current estimates of all future contractual cash flows

Including claim handling costs and embedded options and guarantees

If the LAT shows some inadequate liabilities, the entire deficiency is recognized at once

in profit and loss.

15© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

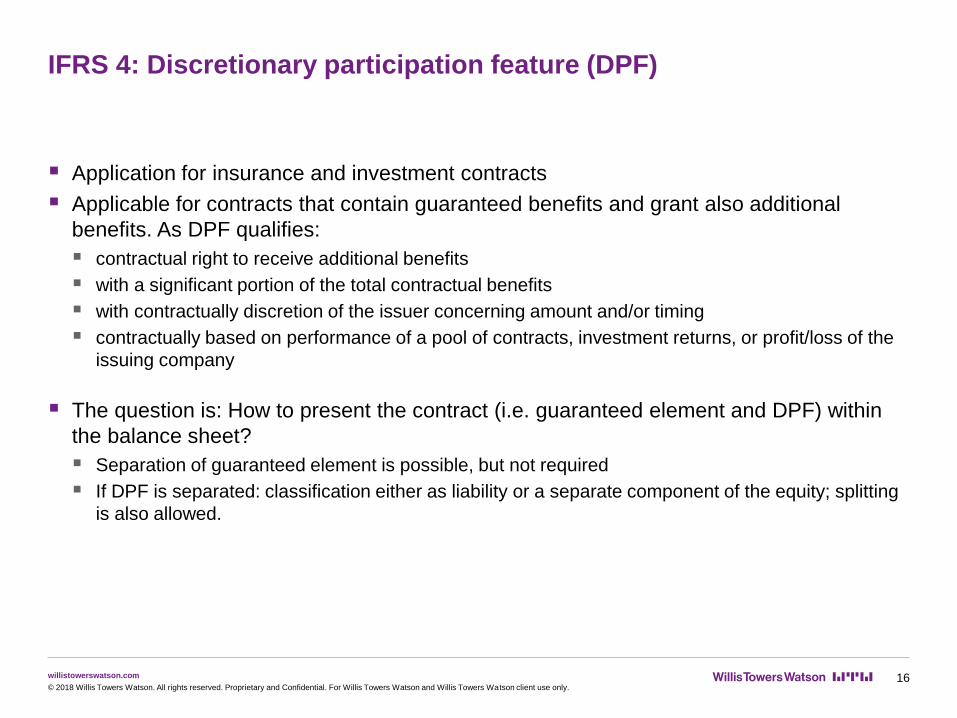

IFRS 4: Discretionary participation feature (DPF)

Application for insurance and investment contracts

Applicable for contracts that contain guaranteed benefits and grant also additional

benefits. As DPF qualifies:

contractual right to receive additional benefits

with a significant portion of the total contractual benefits

with contractually discretion of the issuer concerning amount and/or timing

contractually based on performance of a pool of contracts, investment returns, or profit/loss of the

issuing company

The question is: How to present the contract (i.e. guaranteed element and DPF) within

the balance sheet?

Separation of guaranteed element is possible, but not required

If DPF is separated: classification either as liability or a separate component of the equity; splitting

is also allowed.

16© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

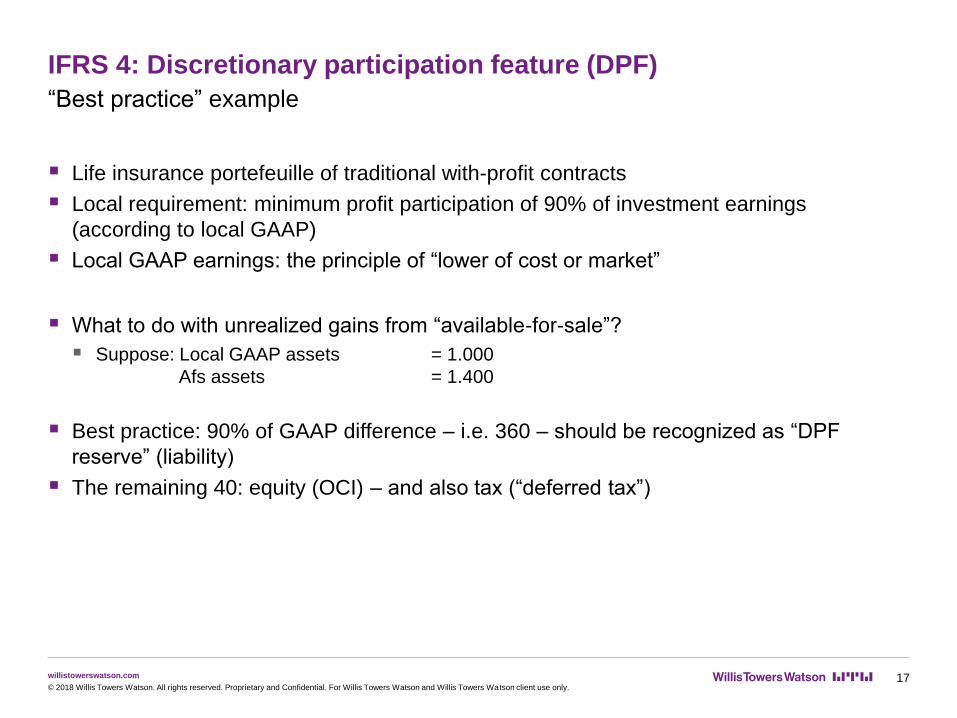

IFRS 4: Discretionary participation feature (DPF)

“Best practice” example

Life insurance portefeuille of traditional with-profit contracts

Local requirement: minimum profit participation of 90% of investment earnings

(according to local GAAP)

Local GAAP earnings: the principle of “lower of cost or market”

What to do with unrealized gains from “available-for-sale”?

Suppose: Local GAAP assets = 1.000

Afs assets = 1.400

Best practice: 90% of GAAP difference – i.e. 360 – should be recognized as “DPF

reserve” (liability)

The remaining 40: equity (OCI) – and also tax (“deferred tax”)

17© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

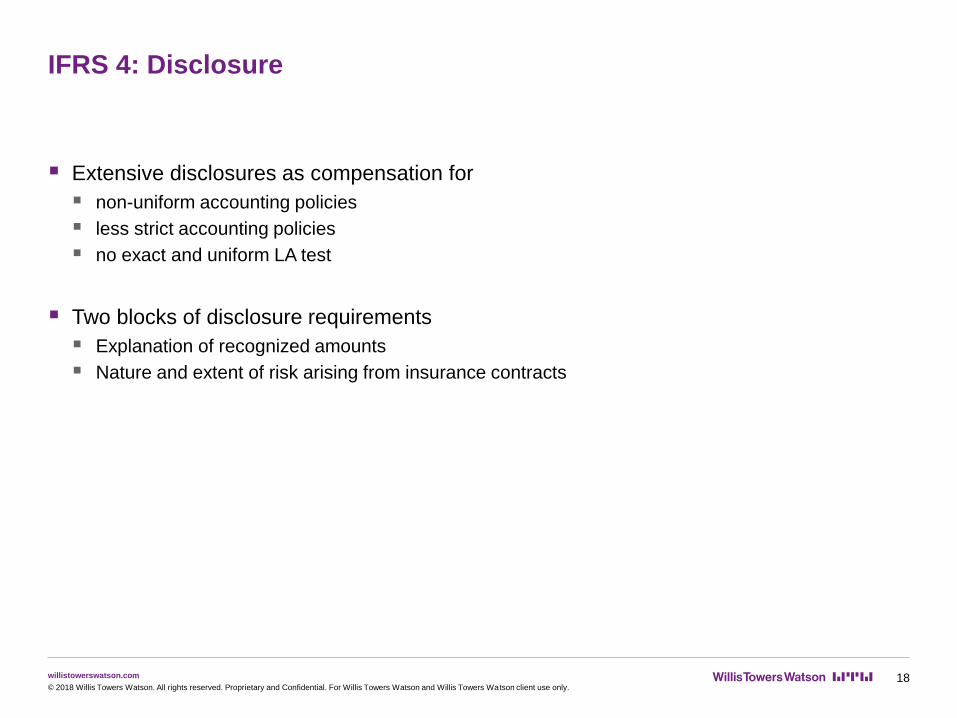

IFRS 4: Disclosure

Extensive disclosures as compensation for

non-uniform accounting policies

less strict accounting policies

no exact and uniform LA test

Two blocks of disclosure requirements

Explanation of recognized amounts

Nature and extent of risk arising from insurance contracts

18© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: Disclosure

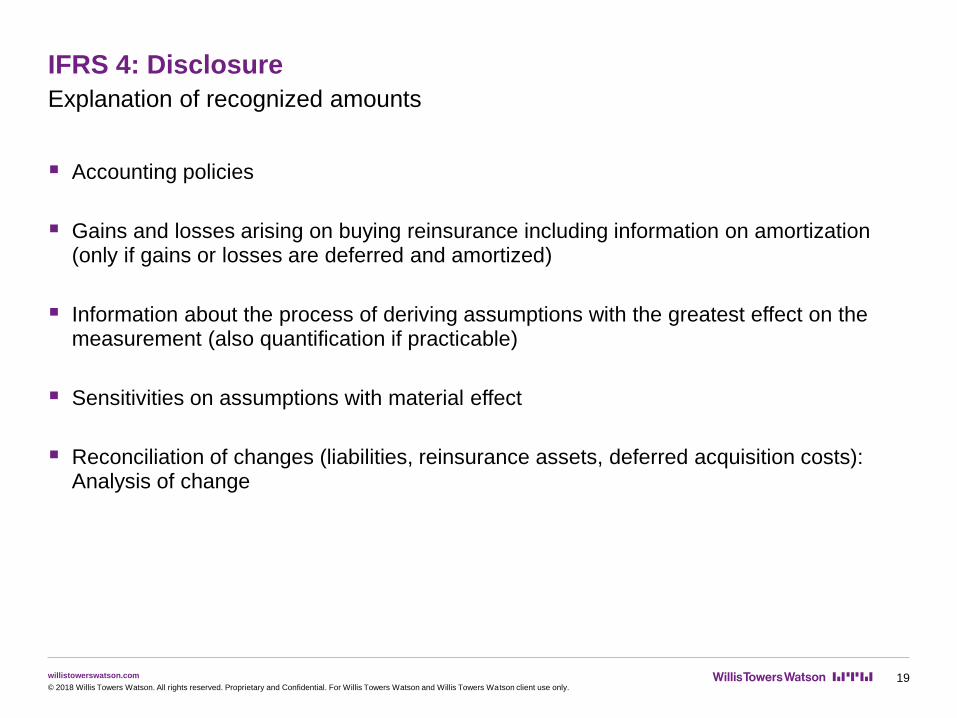

Explanation of recognized amounts

Accounting policies

Gains and losses arising on buying reinsurance including information on amortization (only if gains or losses are deferred and amortized)

Information about the process of deriving assumptions with the greatest effect on the measurement (also quantification if practicable)

Sensitivities on assumptions with material effect

Reconciliation of changes (liabilities, reinsurance assets, deferred acquisition costs): Analysis of change

19© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

IFRS 4: Disclosure

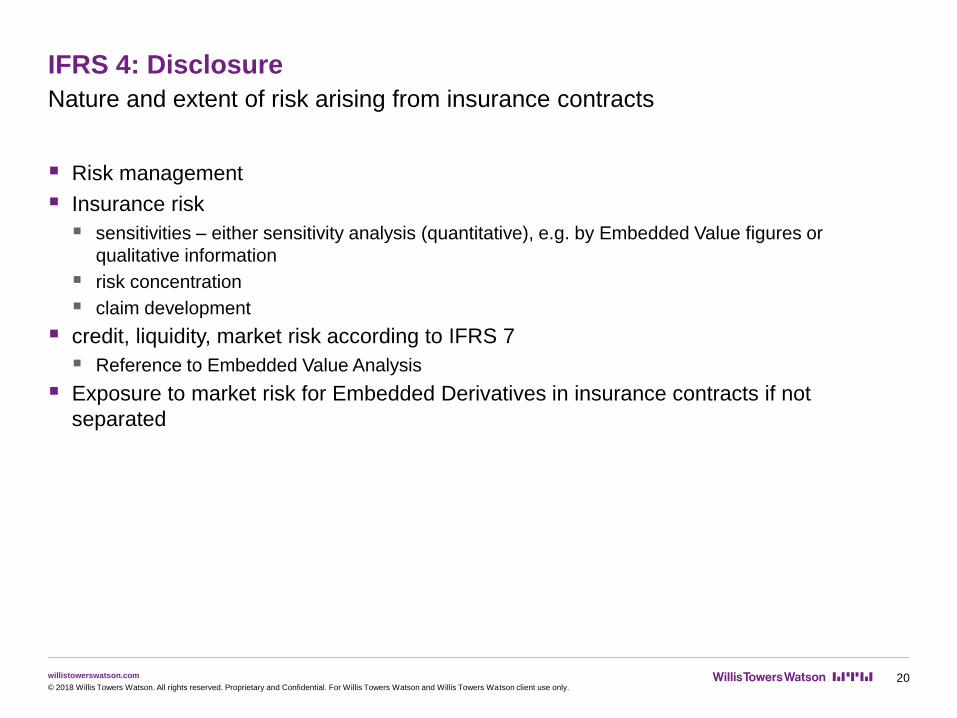

Nature and extent of risk arising from insurance contracts

Risk management

Insurance risk

sensitivities – either sensitivity analysis (quantitative), e.g. by Embedded Value figures or

qualitative information

risk concentration

claim development

credit, liquidity, market risk according to IFRS 7

Reference to Embedded Value Analysis

Exposure to market risk for Embedded Derivatives in insurance contracts if not

separated

20© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com 21© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Agenda

1 IFRS 4

→ Scope and Definition

→ General principles

→ Special issues regarding profit sharing

2US-GAAP for Insurance Contracts:

The principle of “deferral and matching”

willistowerswatson.com

US-GAAP: Deferral and matching

Expenses will be recognized according to profit-recognition of the corresponding asset

acquired.

Revenue will be recognized according to the benefit provided.

Amortization over the term of risk acceptance in relation to expected “margins”:

There are several margin concepts in place

=> different amortization pattern for different kind of contracts

Aim: smooth and steady profit and loss recognition

22© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

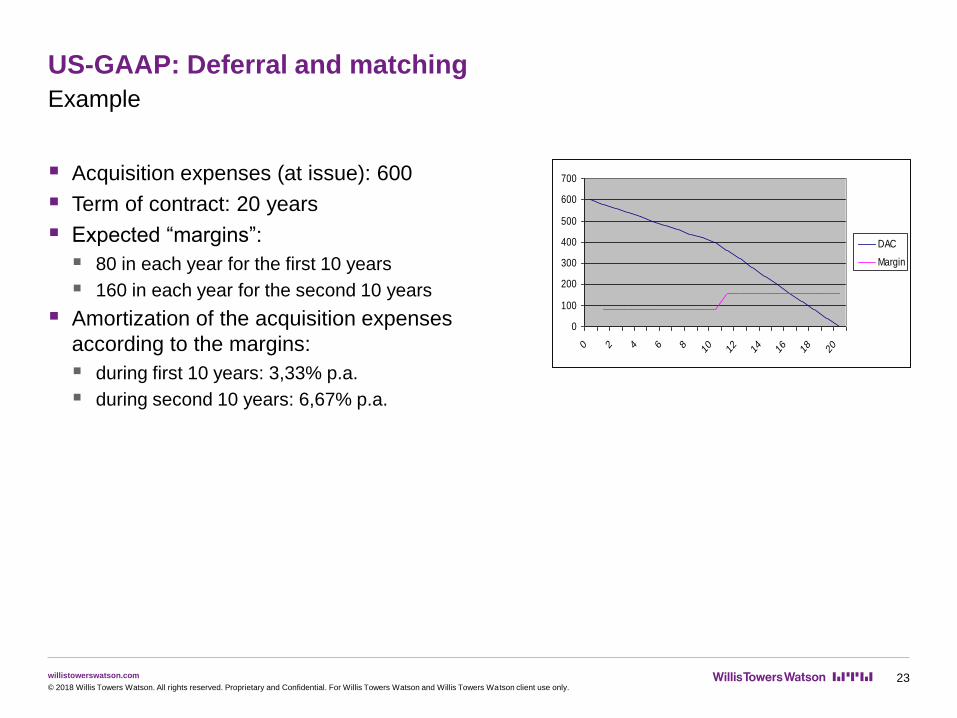

US-GAAP: Deferral and matching

Example

Acquisition expenses (at issue): 600

Term of contract: 20 years

Expected “margins”:

80 in each year for the first 10 years

160 in each year for the second 10 years

Amortization of the acquisition expenses

according to the margins:

during first 10 years: 3,33% p.a.

during second 10 years: 6,67% p.a.

23© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

0

100

200

300

400

500

600

700

0 2 4 6 8 10 12 14 16 18 20

DAC

Margin

willistowerswatson.com

US-GAAP: Deferral and matching

Which expenses and revenues will be amortized with such a margin concept?

Expenses:

acquisition costs => deferred acquisition cost: DAC

terminal dividends => liability for terminal dividend: LTD

present value of future profits (PVFP) of acquired insurance contracts

Revenue:

unearned revenue => unearned revenue reserve: URR

Deferral and matching is only applicable for a small part of expenses and revenue

We will also have to consider other matters, e.g. calculation of claim reserves, life insurance

liabilities, premium recognition etc.

24© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

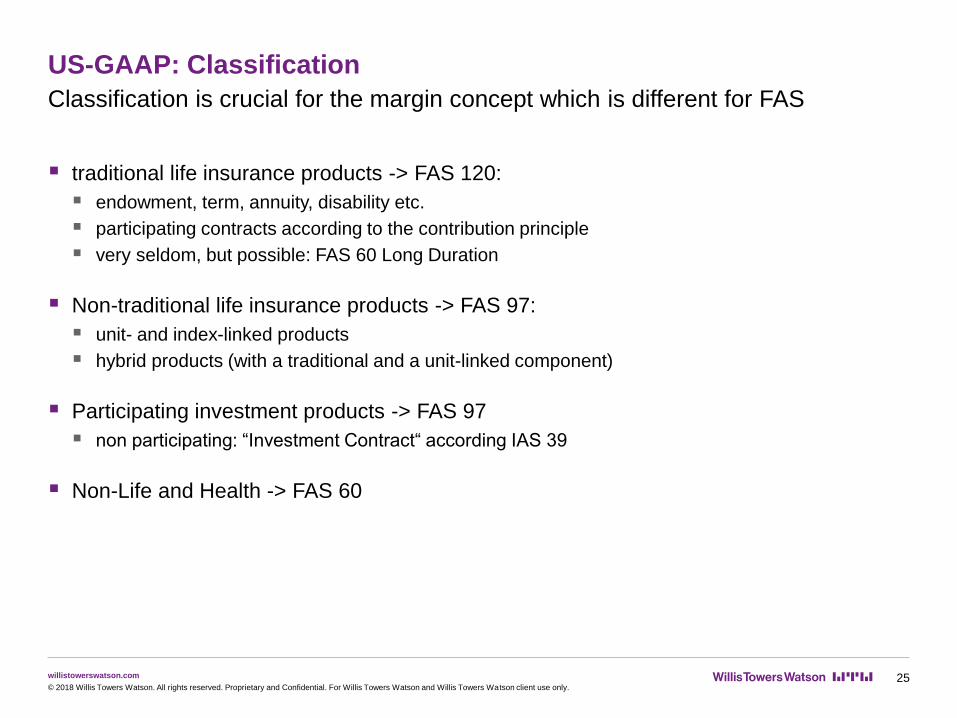

US-GAAP: Classification

Classification is crucial for the margin concept which is different for FAS

traditional life insurance products -> FAS 120:

endowment, term, annuity, disability etc.

participating contracts according to the contribution principle

very seldom, but possible: FAS 60 Long Duration

Non-traditional life insurance products -> FAS 97:

unit- and index-linked products

hybrid products (with a traditional and a unit-linked component)

Participating investment products -> FAS 97

non participating: “Investment Contract“ according IAS 39

Non-Life and Health -> FAS 60

25© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

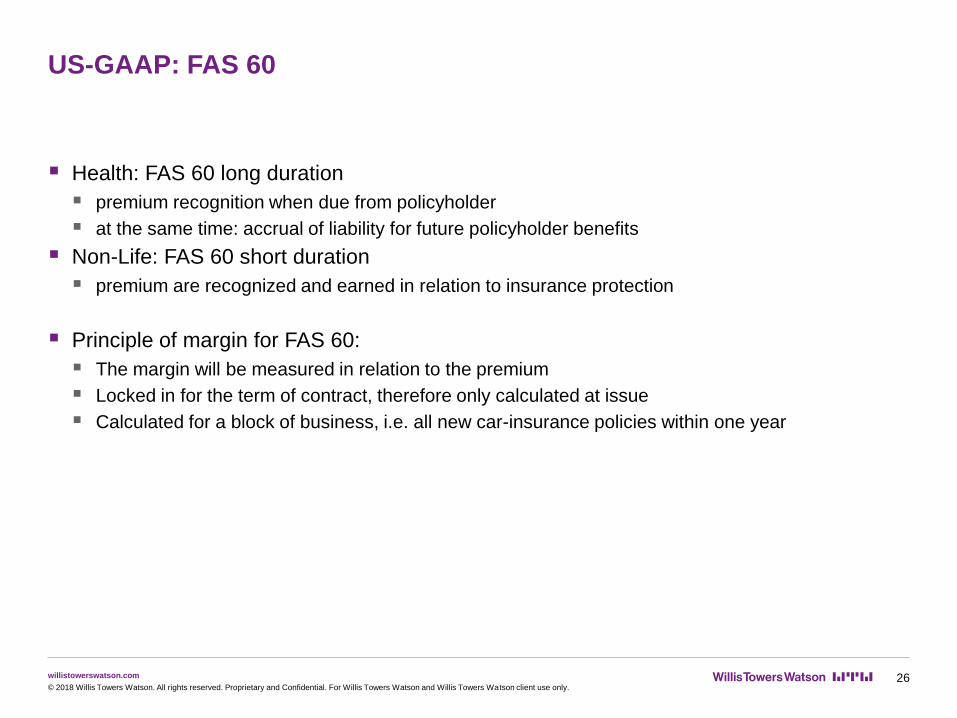

US-GAAP: FAS 60

Health: FAS 60 long duration

premium recognition when due from policyholder

at the same time: accrual of liability for future policyholder benefits

Non-Life: FAS 60 short duration

premium are recognized and earned in relation to insurance protection

Principle of margin for FAS 60:

The margin will be measured in relation to the premium

Locked in for the term of contract, therefore only calculated at issue

Calculated for a block of business, i.e. all new car-insurance policies within one year

26© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

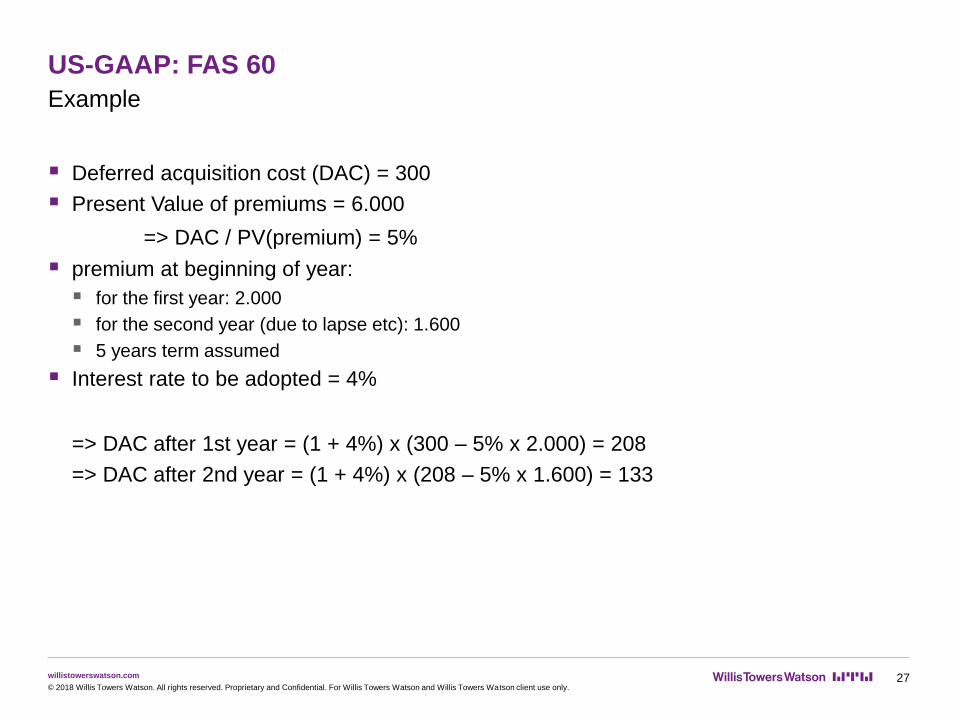

US-GAAP: FAS 60

Example

Deferred acquisition cost (DAC) = 300

Present Value of premiums = 6.000

=> DAC / PV(premium) = 5%

premium at beginning of year:

for the first year: 2.000

for the second year (due to lapse etc): 1.600

5 years term assumed

Interest rate to be adopted = 4%

=> DAC after 1st year = (1 + 4%) x (300 – 5% x 2.000) = 208

=> DAC after 2nd year = (1 + 4%) x (208 – 5% x 1.600) = 133

27© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: FAS 60

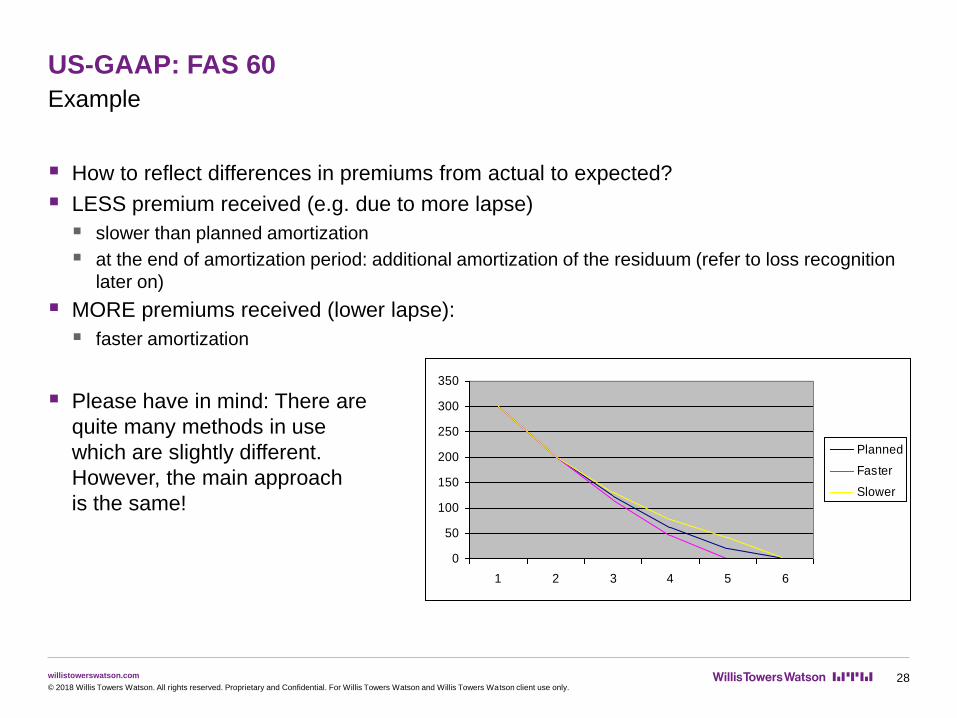

Example

How to reflect differences in premiums from actual to expected?

LESS premium received (e.g. due to more lapse)

slower than planned amortization

at the end of amortization period: additional amortization of the residuum (refer to loss recognition

later on)

MORE premiums received (lower lapse):

faster amortization

Please have in mind: There are

quite many methods in use

which are slightly different.

However, the main approach

is the same!

28© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

0

50

100

150

200

250

300

350

1 2 3 4 5 6

Planned

Faster

Slower

willistowerswatson.com

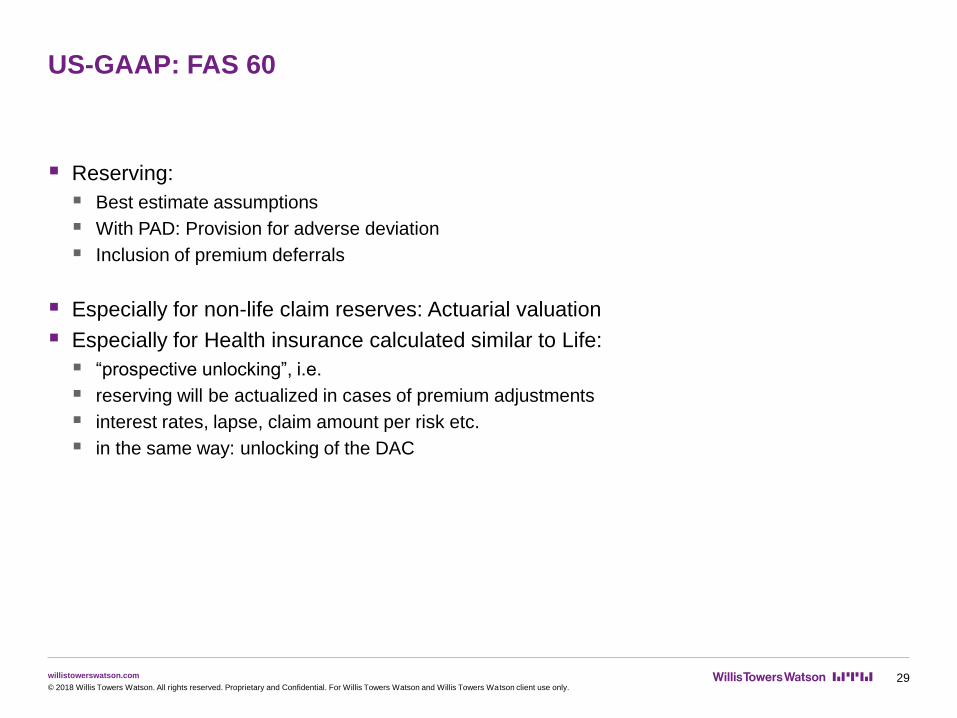

US-GAAP: FAS 60

Reserving:

Best estimate assumptions

With PAD: Provision for adverse deviation

Inclusion of premium deferrals

Especially for non-life claim reserves: Actuarial valuation

Especially for Health insurance calculated similar to Life:

“prospective unlocking”, i.e.

reserving will be actualized in cases of premium adjustments

interest rates, lapse, claim amount per risk etc.

in the same way: unlocking of the DAC

29© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: FAS 120 and FAS 97

Deferral and matching similar for FAS 120 and FAS 97

Before we will deal with the deferral and matching items

let’s see how the other balance sheet items are dealt with

…….

30© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

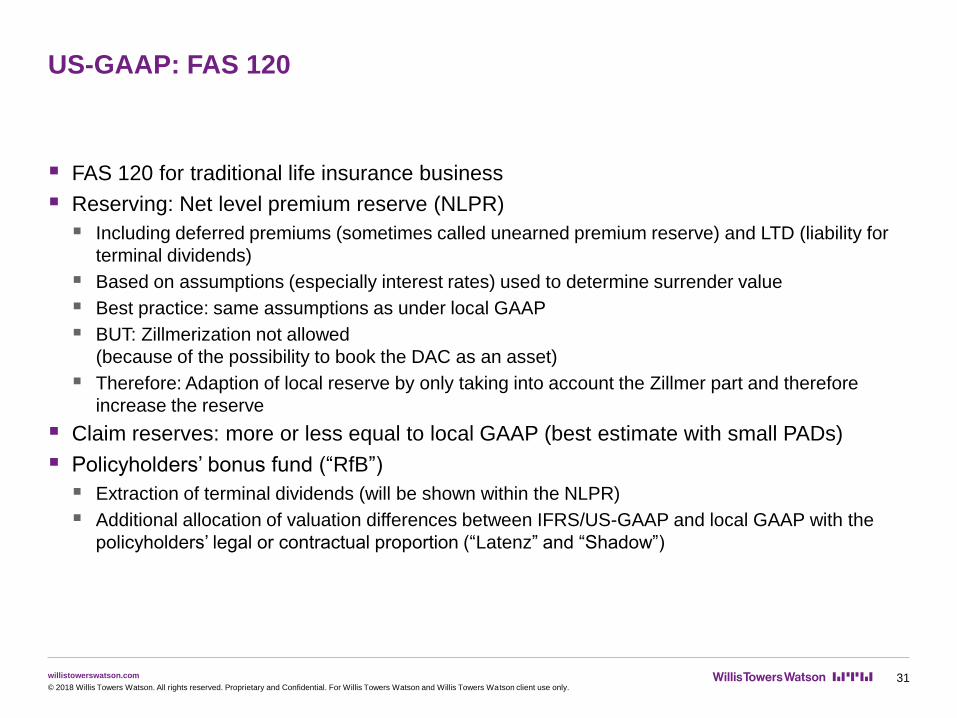

US-GAAP: FAS 120

FAS 120 for traditional life insurance business

Reserving: Net level premium reserve (NLPR)

Including deferred premiums (sometimes called unearned premium reserve) and LTD (liability for

terminal dividends)

Based on assumptions (especially interest rates) used to determine surrender value

Best practice: same assumptions as under local GAAP

BUT: Zillmerization not allowed

(because of the possibility to book the DAC as an asset)

Therefore: Adaption of local reserve by only taking into account the Zillmer part and therefore

increase the reserve

Claim reserves: more or less equal to local GAAP (best estimate with small PADs)

Policyholders’ bonus fund (“RfB”)

Extraction of terminal dividends (will be shown within the NLPR)

Additional allocation of valuation differences between IFRS/US-GAAP and local GAAP with the

policyholders’ legal or contractual proportion (“Latenz” and “Shadow”)

31© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

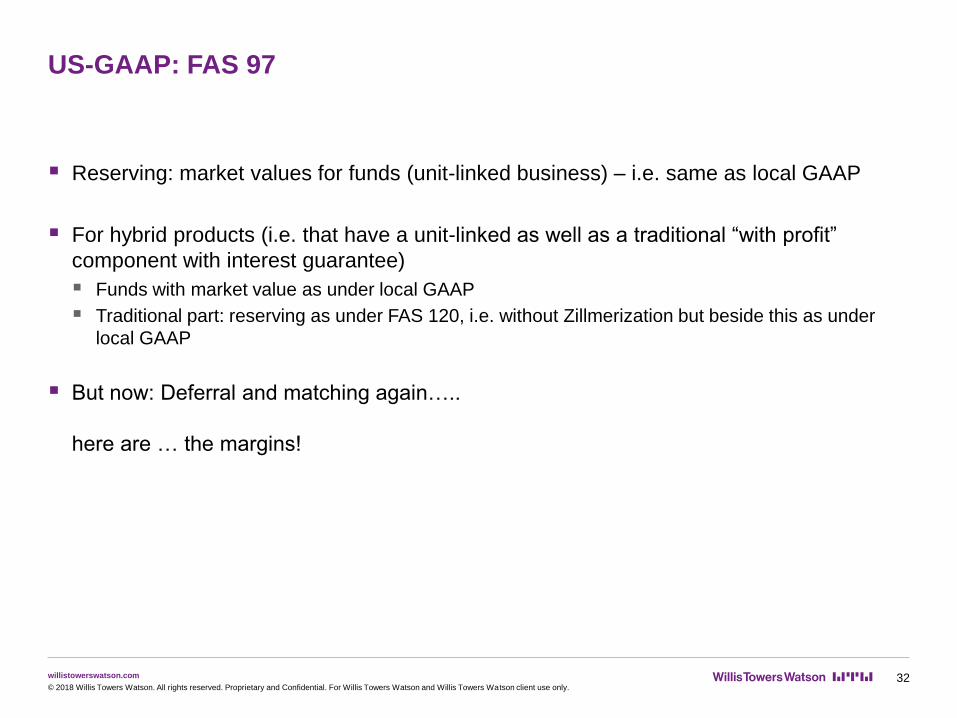

US-GAAP: FAS 97

Reserving: market values for funds (unit-linked business) – i.e. same as local GAAP

For hybrid products (i.e. that have a unit-linked as well as a traditional “with profit”

component with interest guarantee)

Funds with market value as under local GAAP

Traditional part: reserving as under FAS 120, i.e. without Zillmerization but beside this as under

local GAAP

But now: Deferral and matching again…..

here are … the margins!

32© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

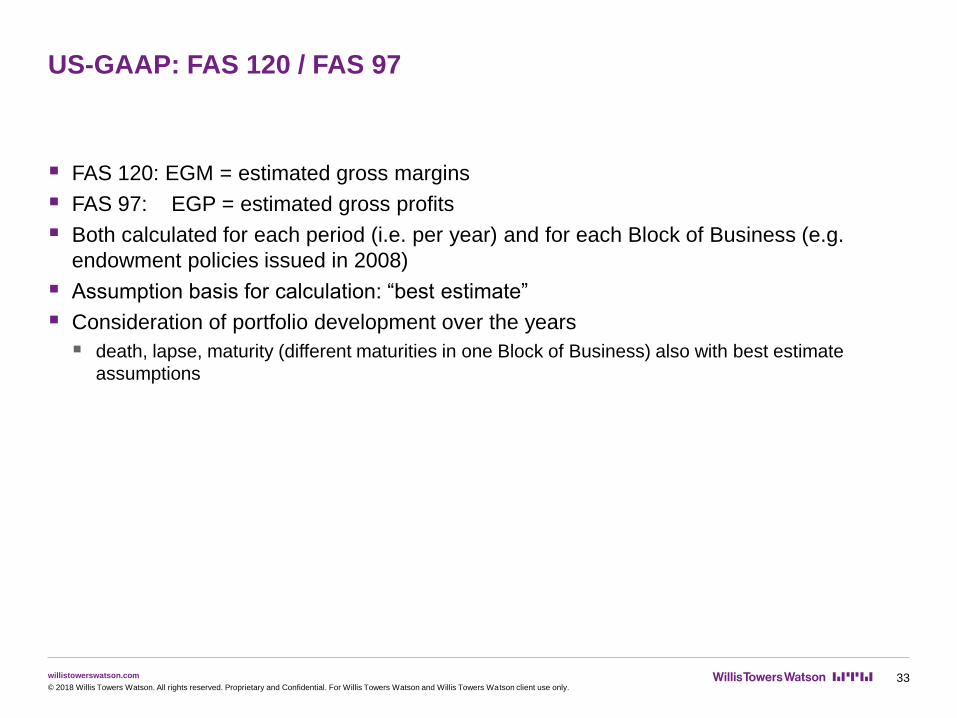

US-GAAP: FAS 120 / FAS 97

FAS 120: EGM = estimated gross margins

FAS 97: EGP = estimated gross profits

Both calculated for each period (i.e. per year) and for each Block of Business (e.g.

endowment policies issued in 2008)

Assumption basis for calculation: “best estimate”

Consideration of portfolio development over the years

death, lapse, maturity (different maturities in one Block of Business) also with best estimate

assumptions

33© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

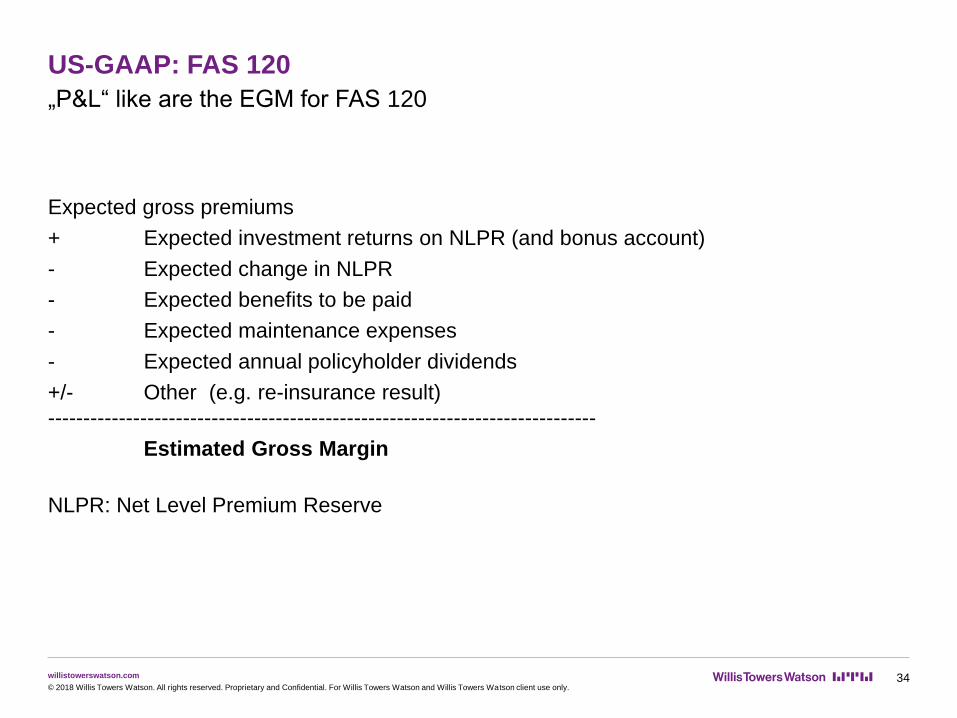

US-GAAP: FAS 120

„P&L“ like are the EGM for FAS 120

Expected gross premiums

+ Expected investment returns on NLPR (and bonus account)

- Expected change in NLPR

- Expected benefits to be paid

- Expected maintenance expenses

- Expected annual policyholder dividends

+/- Other (e.g. re-insurance result)

-----------------------------------------------------------------------------

Estimated Gross Margin

NLPR: Net Level Premium Reserve

34© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

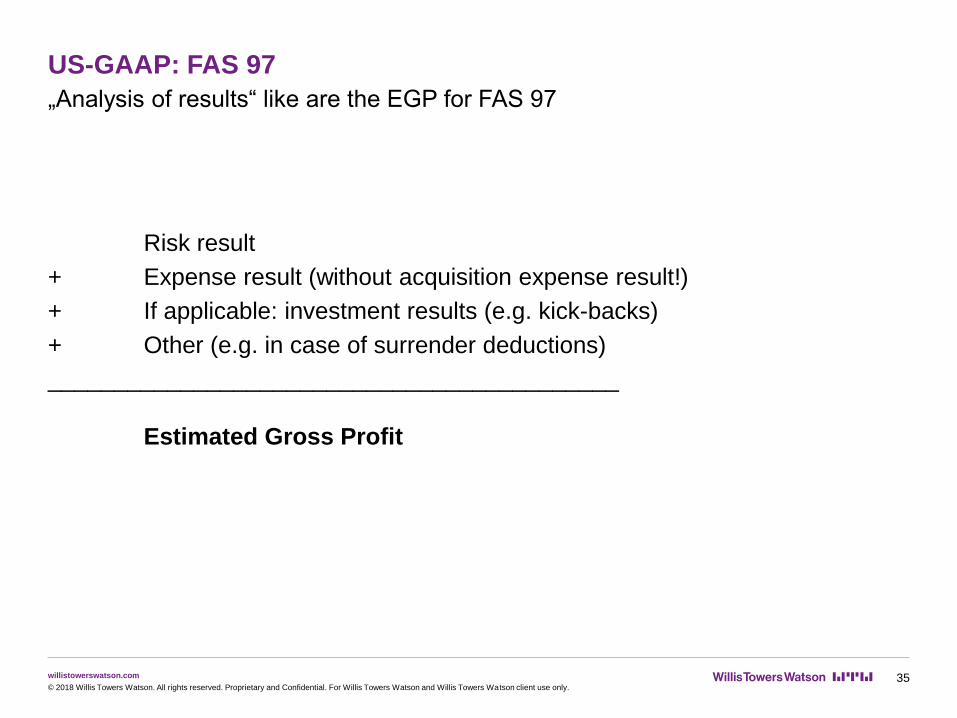

US-GAAP: FAS 97

„Analysis of results“ like are the EGP for FAS 97

Risk result

+ Expense result (without acquisition expense result!)

+ If applicable: investment results (e.g. kick-backs)

+ Other (e.g. in case of surrender deductions)

___________________________________________

Estimated Gross Profit

35© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: FAS 120 / FAS 97

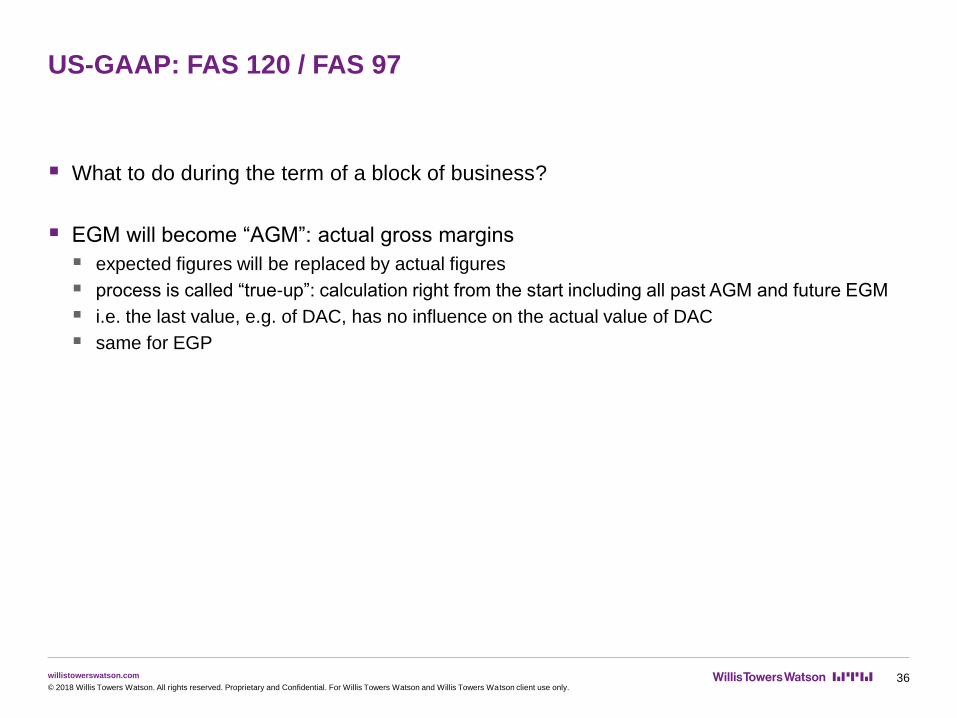

What to do during the term of a block of business?

EGM will become “AGM”: actual gross margins

expected figures will be replaced by actual figures

process is called “true-up”: calculation right from the start including all past AGM and future EGM

i.e. the last value, e.g. of DAC, has no influence on the actual value of DAC

same for EGP

36© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

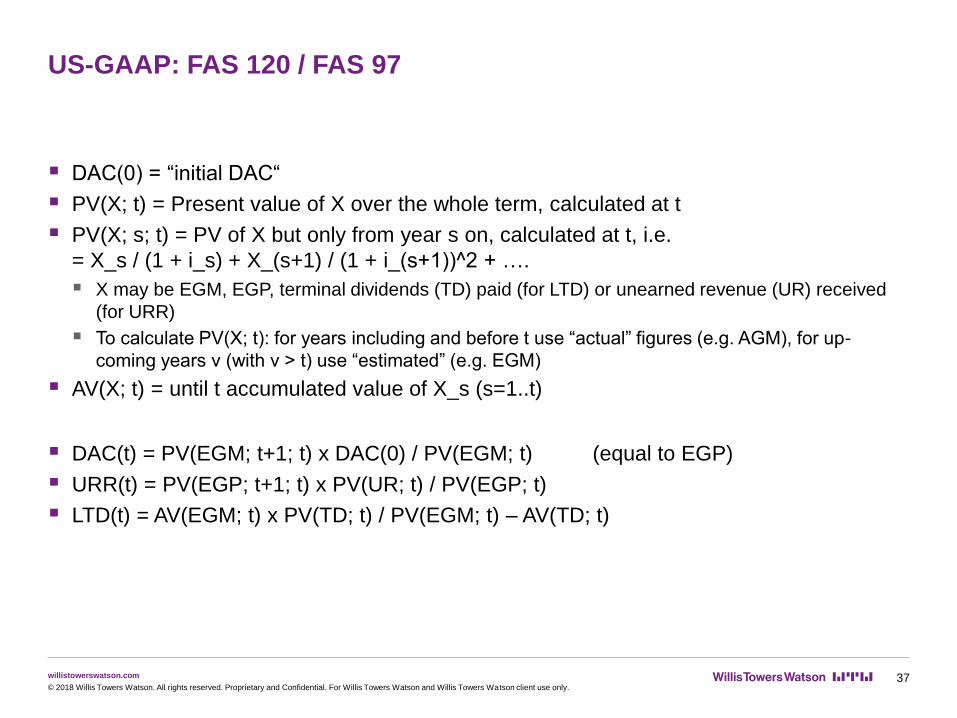

US-GAAP: FAS 120 / FAS 97

DAC(0) = “initial DAC“

PV(X; t) = Present value of X over the whole term, calculated at t

PV(X; s; t) = PV of X but only from year s on, calculated at t, i.e.

= X_s / (1 + i_s) + X_(s+1) / (1 + i_(s+1))^2 + ….

X may be EGM, EGP, terminal dividends (TD) paid (for LTD) or unearned revenue (UR) received

(for URR)

To calculate PV(X; t): for years including and before t use “actual” figures (e.g. AGM), for up-

coming years v (with v > t) use “estimated” (e.g. EGM)

AV(X; t) = until t accumulated value of X_s (s=1..t)

DAC(t) = PV(EGM; t+1; t) x DAC(0) / PV(EGM; t) (equal to EGP)

URR(t) = PV(EGP; t+1; t) x PV(UR; t) / PV(EGP; t)

LTD(t) = AV(EGM; t) x PV(TD; t) / PV(EGM; t) – AV(TD; t)

37© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

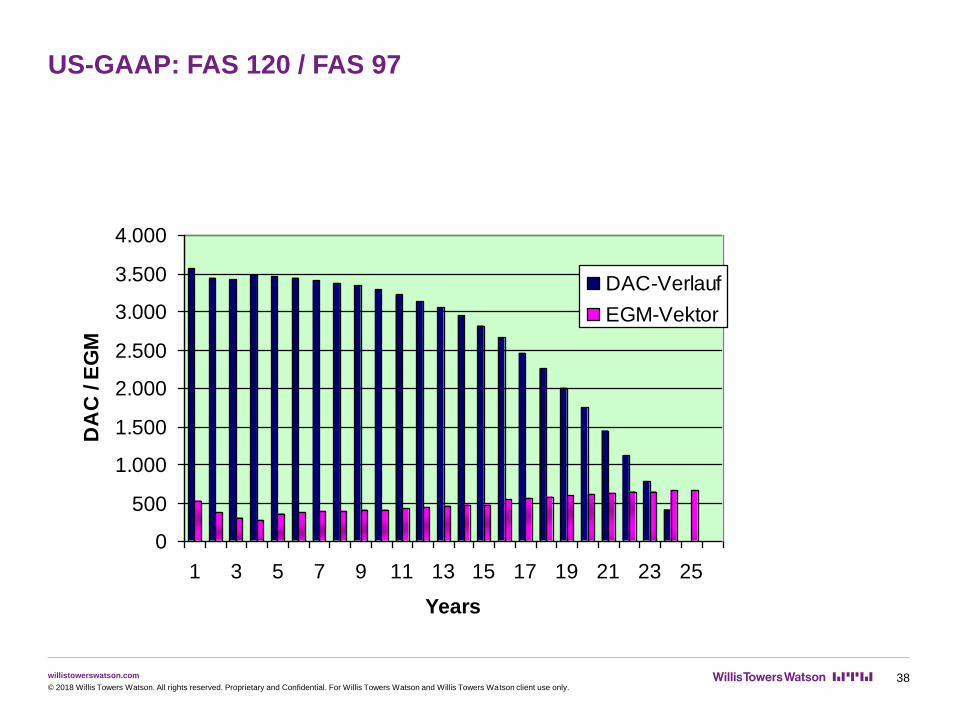

US-GAAP: FAS 120 / FAS 97

38© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

1 3 5 7 9 11 13 15 17 19 21 23 25

Years

DA

C / E

GM

DAC-Verlauf

EGM-Vektor

willistowerswatson.com

US-GAAP: True-up according to FAS 120 / FAS 97

True-up: EGM / EGP update

Hence, change within the depending amounts: DAC, PVFP, URR, TBR

Change impacts often unpredictable, because of model complexity

Interaction of substantial assumptions:

Interest surplus participation of the policyholder

Return on capital investments

39© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: FAS 120 / FAS 97

Example: “True-up” of DAC for traditional life insurance

Initial DAC: DAC(0) = 1.000

EGM, calculated at t = 0: constant over whole term (20 years) = 100 p.a.

Discount rate = 0%, i.e. linear amortization of DAC planned at issue

AGM of first 10 years equal to EGM: 100 p.a.

=> DAC after 10 years BEFORE True-up: 500

True-up of future EGM (i.e. for the second ten years):

Case A: 50 p.a.

Case B: 200 p.a.

Calculation including the whole term yields:

Amortization of initial DAC during the first 10 years:

Case A: 2/3 = (10 * 100) / (10 * 100 + 10 * 50) of initial DAC

Case B: 1/3 = (10 * 100) / (10 * 100 + 10 * 200) of initial DAC

DAC after True-up: Case A = 333 vs. Case B = 667

40© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: FAS 120 / FAS 97

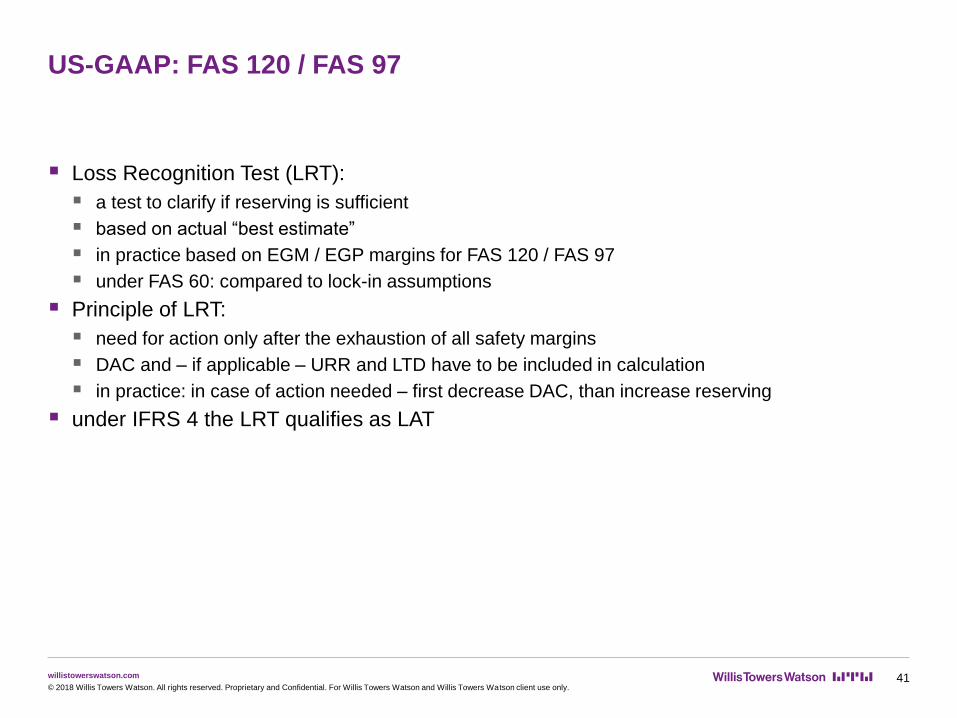

Loss Recognition Test (LRT):

a test to clarify if reserving is sufficient

based on actual “best estimate”

in practice based on EGM / EGP margins for FAS 120 / FAS 97

under FAS 60: compared to lock-in assumptions

Principle of LRT:

need for action only after the exhaustion of all safety margins

DAC and – if applicable – URR and LTD have to be included in calculation

in practice: in case of action needed – first decrease DAC, than increase reserving

under IFRS 4 the LRT qualifies as LAT

41© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: FAS 120 / FAS 97

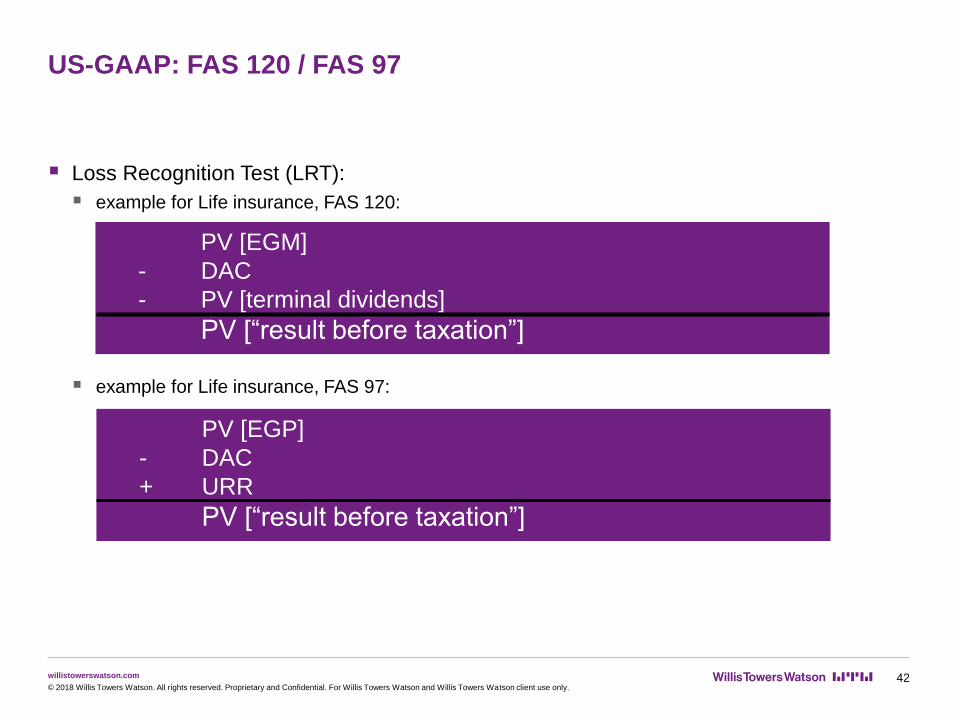

Loss Recognition Test (LRT):

example for Life insurance, FAS 120:

example for Life insurance, FAS 97:

42© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

PV [EGM]

- DAC

- PV [terminal dividends]

PV [“result before taxation”]

PV [EGP]

- DAC

+ URR

PV [“result before taxation”]

willistowerswatson.com

US-GAAP: FAS 97

FAS 97: Different approach to recognize premiums in P&L

idea / opinion: savings premiums which are invested in a fund are not under risk and responsibility

of the insurance company

therefore, that’s a “pass-through premium”

which should not be recognized as income!

Big difference to many local GAAP in which the whole premium will be recognized as

income

Consequently under FAS 97:

increase of the reserve due to saving premiums are not shown as expense

benefits are only shown as expense if exceeding the fund value (again: pass-through feature!)

decrease of the reserve due to benefits are not shown as income

43© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: Accounting for differences between IFRS/US-GAAP and local

GAAP

There may occur many differences between local GAAP and IFRS/US-GAAP figures

DAC, reserving, LTD, URR

IAS 39: accounting for assets (“available for sale” etc…)

Others like e.g. IAS 19, pension obligation

However, for with-profit business (“discretionary participation” under IFRS 4) the profit

participation will be linked (in most cases) to local GAAP figures

Consequently, there is a problem to be solved:

Which part of the differences between local GAAP and IFRS/US-GAAP should be

accounted for as

Equity (and corresponding deferred taxes)?

Policyholder bonus reserve?

44© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: Accounting for differences between IFRS/US-GAAP and local

GAAP

Which part of the differences between local GAAP and IFRS/US-GAAP should be

accounted for as

Equity (and corresponding deferred taxes)?

Policyholder bonus reserve?

In general: Build up a policyholder bonus reserve for GAAP differences to the amount of

that portion on which the policyholders have a right to receive a participation

Often “best practice”: approximations as e.g. “90%”

What to do if GAAP difference sum up to a negative amount – i.e. a charge to

policyholder bonus reserve?

“Best practice”: permitted up to the amount of the non-allocated (“free”) part of the statutory

policyholder bonus reserve

45© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: Accounting for differences between IFRS/US-GAAP and local

GAAP

Example:

Consider the following insurance company which offers only traditional with-profit

contracts with an obligation of a participation rate of 90% on all results based on

statutory GAAP.

local reserve = 18.500

=> no Zillmerization under US-GAAP => NLPR = 19.500

statutory assets related to acquisition costs = 300 (“Zillmer”-asset) => DAC = 1.500

local reserve for terminal dividends = 560

(e.g. the so-called “SÜAF” in Germany which is part of the whole policyholder bonus reserve,

called RfB)

=> LTD = 1.000

unearned premium reserve (under both GAAP) = 140

local book value of assets = 21.000

=> all classified as “available for sale” under IAS 39 => 22.000

46© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

US-GAAP: Accounting for differences between IFRS/US-GAAP and local

GAAP

Example:

47© 2018 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

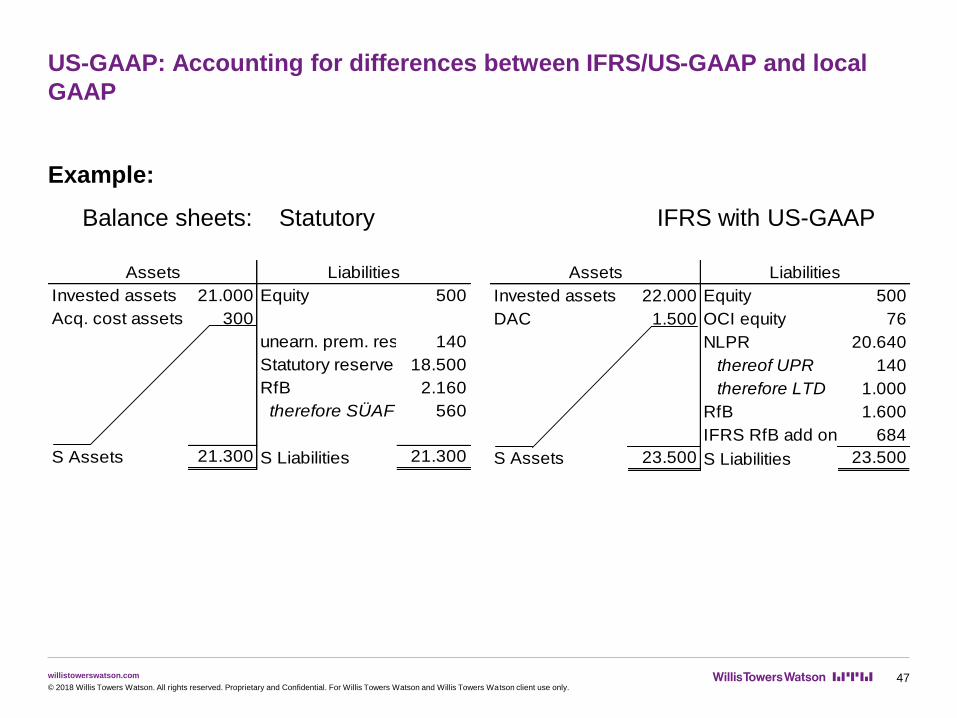

Balance sheets: Statutory IFRS with US-GAAP

Invested assets 22.000 Equity 500

DAC 1.500 OCI equity 76

NLPR 20.640

thereof UPR 140

therefore LTD 1.000

RfB 1.600

IFRS RfB add on 684

S Assets 23.500 S Liabilities 23.500

Assets Liabilities

Invested assets 21.000 Equity 500

Acq. cost assets 300

unearn. prem. res. 140

Statutory reserve 18.500

RfB 2.160

therefore SÜAF 560

S Assets 21.300 S Liabilities 21.300

Assets Liabilities