Accounting & Financial Statement Analysis: Making it Real! By: Ms. Eborn Virtual Enterprise-...

43

Accounting & Financial Statement Analysis: Making it Real! By: Ms. Eborn Virtual Enterprise- Accounting I

-

Upload

colleen-richards -

Category

Documents

-

view

219 -

download

1

Transcript of Accounting & Financial Statement Analysis: Making it Real! By: Ms. Eborn Virtual Enterprise-...

Accounting & Financial Statement Analysis: Making it Real!

By: Ms. Eborn

Virtual Enterprise- Accounting I

What is Accounting?

The Language of Business Standard Rules for Measuring Firm’s

Performance Assessing Performance is important to: The Firm’s Office Managers & Employees

(Measures Performance in different geographic locations)

Investors (Current & Potential Shareholders) Lenders (Banks) General Public (Communication to Public

Arena)

Why is Accounting Important?

Make Corporate Decisions Make Investment Decisions (Mutual

Funds looking to invest in companies) Facilitates Corporate and Investment

Decision (Assessment & Comparison)

Who Uses Accounting?

Federal Government Non-Profit Organizations Small Businesses Corporations

Standardized U.S. Accounting Regulations (GAAP)

Generally Accepted Accounting Principles (GAAP) How does it work?

U.S. Governmental Agency called Securities and Exchange Commission (SEC) authorizes the Financial Accounting Standards Board (FASB) to determine U.S. Accounting Rules

FASB communicates these Rules by issuing Statements of Financial Accounting Standards (SFAS). These statements make up the U.S. Accounting rules known as GAAP.

Purpose of GAAP?

Serve as Guidelines for Financial accounting, to insure that business present their financial information on a fair, consistent, and straightforward basis.

U.S. companies must be prepared according to U.S. GAAP.

What is IFRS?

There has been a convergence between the standards for the U.S. and other countries.

In 2001, IASC committee was replaced by the International Accounting Standards Board (IASB). IASB has 14 Board Members that were selected by IASC. IASB (the parent foundation) is solely responsible for developing IFRS.

In 2002, FASB & IASB agreed to work together toward a convergence between GAAP & IFRS, but there still remains differences.

In 2005, all EU countries adopted International Financial Reporting Standards (IFRS). In addition, accounting standards for many countries outside of Europe, including Japan.

Assessment: Fully write out Assessment: Fully write out questions & answers on questions & answers on your paperyour paper

Select letter and all answers that apply. Select letter and all answers that apply. There may be more than one answer.There may be more than one answer.

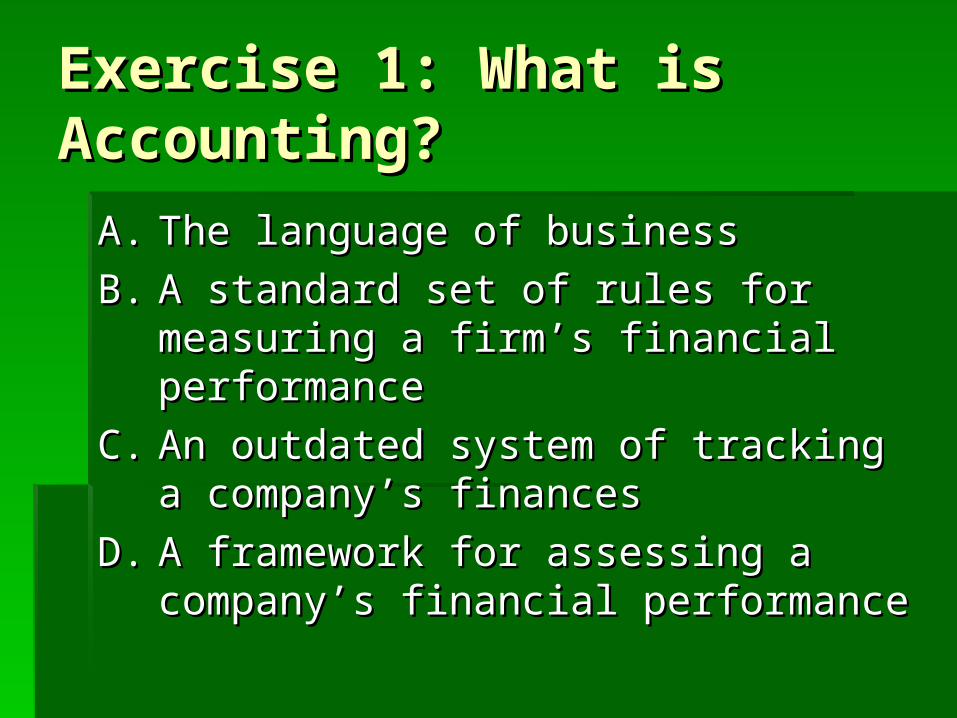

Exercise 1: What is Exercise 1: What is Accounting?Accounting?

A.A. The language of businessThe language of business

B.B. A standard set of rules for measuring a A standard set of rules for measuring a firm’s financial performancefirm’s financial performance

C.C. An outdated system of tracking a An outdated system of tracking a company’s financescompany’s finances

D.D. A framework for assessing a company’s A framework for assessing a company’s financial performancefinancial performance

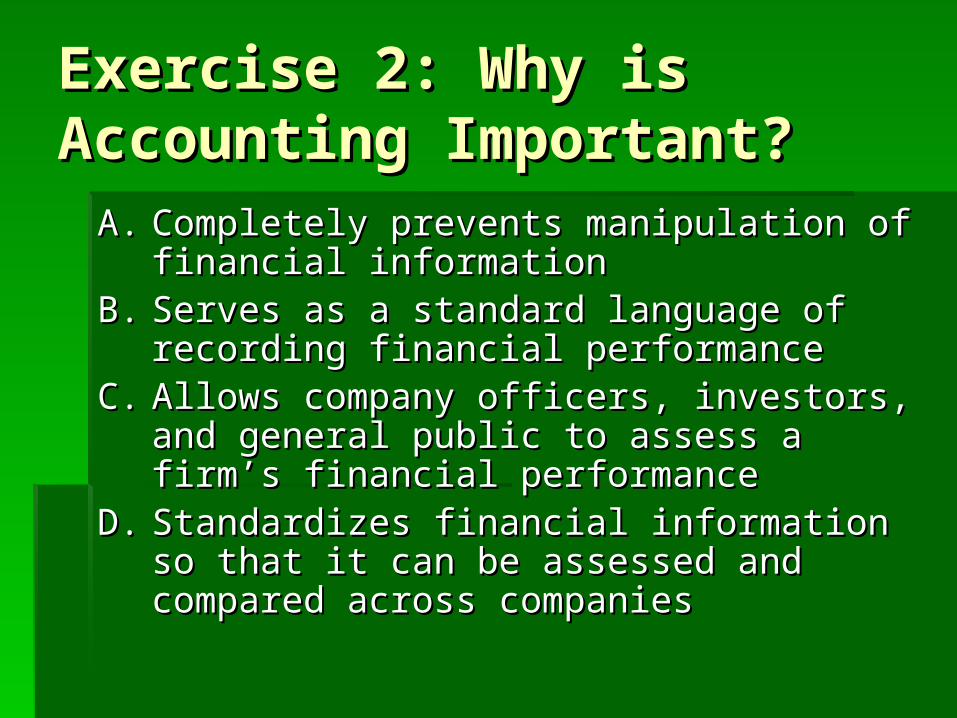

Exercise 2: Why is Exercise 2: Why is Accounting Important?Accounting Important?

A.A. Completely prevents manipulation of financial Completely prevents manipulation of financial informationinformation

B.B. Serves as a standard language of recording Serves as a standard language of recording financial performancefinancial performance

C.C. Allows company officers, investors, and Allows company officers, investors, and general public to assess a firm’s financial general public to assess a firm’s financial performanceperformance

D.D. Standardizes financial information so that it Standardizes financial information so that it can be assessed and compared across can be assessed and compared across companiescompanies

Exercise 3: What does Exercise 3: What does GAAP Stand For?GAAP Stand For?

A.A. Generally Accepted Accounting Generally Accepted Accounting Performance Performance

B.B. General Accounting Accepted PracticesGeneral Accounting Accepted Practices

C.C. Generally Accepted Accounting Generally Accepted Accounting Practices Practices

Exercise 4: Accounting Exercise 4: Accounting Regulations-GAAP Is:Regulations-GAAP Is:

A.A. Rules and Regulations governing Rules and Regulations governing accountingaccounting

B.B. Developed by the SEC on behalf of Developed by the SEC on behalf of FASBFASB

C.C. Communicated through issuance of Communicated through issuance of Statements of Financial Accounting Statements of Financial Accounting Standards (SFAS)Standards (SFAS)

D.D. All of the aboveAll of the above

Exercise 5: IFRS-International Exercise 5: IFRS-International Financial Reporting Standards Financial Reporting Standards (IFRS) are:(IFRS) are:

A.A. Rules and regulations governing Rules and regulations governing international accountinginternational accounting

B.B. Developed by FASB and used by all EU Developed by FASB and used by all EU countriescountries

C.C. Converging with U.S. GAAP, but a Converging with U.S. GAAP, but a number of difference still existnumber of difference still exist

D.D. Converging with U.S. GAAP, with both Converging with U.S. GAAP, with both accounting systems set to be identical by accounting systems set to be identical by 20102010

What is Depreciation Expense?

A method where a long-term fixed asset (purchases that are expected to provide benefits for the company for a period of 1 year or more)

This is spread over a future period (number of years) when these assets are expected to be in service & help generate Revenue for a company.

Depreciation quantifies the wear & tear (from use & passage of time) of the physical asset through a systematic decrease (depreciation) of the assets’ book (historical value).

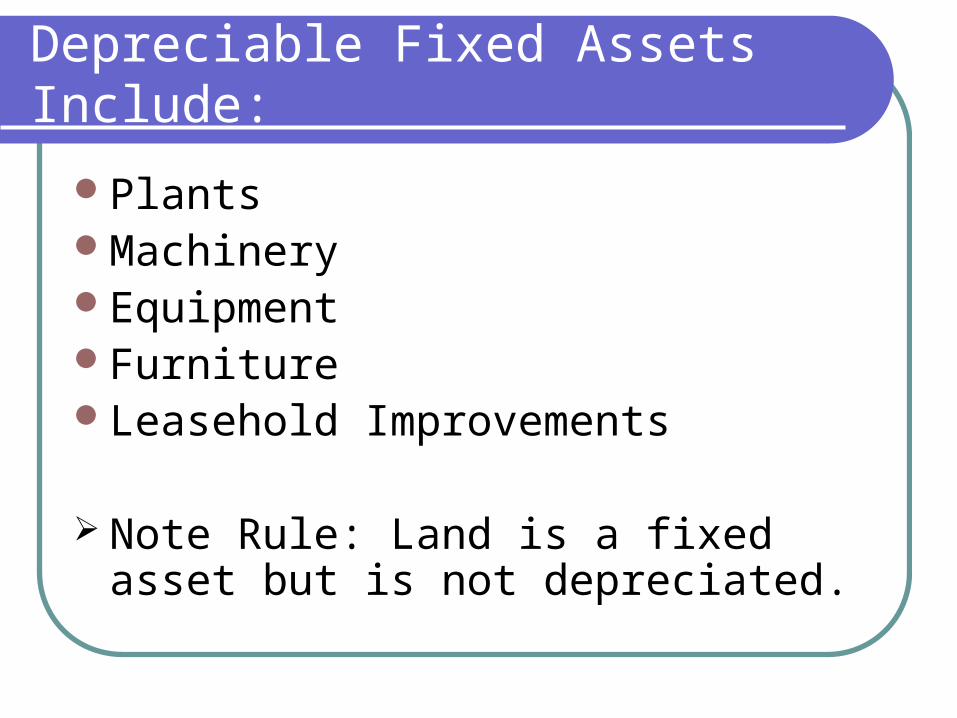

Depreciable Fixed Assets Include:

PlantsMachineryEquipmentFurnitureLeasehold Improvements

Note Rule: Land is a fixed asset but is not depreciated.

Major Asset Classes & Their Typical Useful Lives:

Building & Improvements: 5-50 YearsFixtures & Equipment 5-12 YearsTransportation Equipment 2-5 YearsInternally Developed Software: 3 YearsLand: Not Depreciated

Assessment: Fully write out Assessment: Fully write out questions & answers on questions & answers on your paperyour paper

Select letter and all answers that apply. Select letter and all answers that apply. There may be more than one answer.There may be more than one answer.

Depreciation Exercise 9: Depreciation Exercise 9: Which of the Following Which of the Following Needs to be Depreciated?Needs to be Depreciated?A.A. WarehouseWarehouse

B.B. Administrative WagesAdministrative Wages

C.C. Office FurnitureOffice Furniture

D.D. Power PlantPower Plant

E.E. Land used to build a supermarketLand used to build a supermarket

Depreciation Exercise 9 SolutionDepreciation Exercise 9 Solution

A. WarehouseA. Warehouse

C. Office FurnitureC. Office Furniture

D. Power PlantD. Power Plant

Depreciation Expense:Depreciation Expense:Bonus QuestionBonus Question

What is Depreciation Expense in your own What is Depreciation Expense in your own words?words?

Operating Operating Expenses Expenses Estimating MonthlyEstimating MonthlyDemand, Expenses Demand, Expenses & Overhead & Overhead

Identify & Estimate Operating Expenses

• In business, an expense is defined as the use of an asset.

• In other words, as you expend your assets to run and operate your business venture, the dollar value of those assets are noted on an Income Statement as expenses.

• The more expenses you have, the less profit you make and the less taxes you pay.

Operating Expenses - use of your assets & services to produce

revenue. Some specific, common examples are:

• Cost of Goods Sold (non-cash expense)

• Rent (cash expense)

• Prepaid Insurance (non-cash expense)

• Wages & Salaries (cash expense

How Expenses are How Expenses are Categorized on the Income Categorized on the Income Statement Statement

Expenses usually are put into one of two categories:Expenses usually are put into one of two categories: Cost of Goods Sold (CGS)Cost of Goods Sold (CGS) - direct labor & materials. These - direct labor & materials. These

vary/change as your sales volume increases or decreases. The vary/change as your sales volume increases or decreases. The are the use of your asset called inventory. CGS is usually a non-are the use of your asset called inventory. CGS is usually a non-cash expense. The cash was expended in months past to buy the cash expense. The cash was expended in months past to buy the inventory. The amount of the inventory sold each month inventory. The amount of the inventory sold each month (expended or used up) is the expense you show on the Income (expended or used up) is the expense you show on the Income Statement.Statement.

OverheadOverhead - all other expenses of operating your business. These - all other expenses of operating your business. These tend to be fixed. They tend not to change as your sales volume tend to be fixed. They tend not to change as your sales volume changes in the short run. They may be cash or non-cash changes in the short run. They may be cash or non-cash expenses.expenses.

Overhead Includes:Overhead Includes:

operating expenses - rent, insurance operating expenses - rent, insurance selling expenses - commissions, mileage selling expenses - commissions, mileage administrative expenses - management administrative expenses - management

salaries, office expensessalaries, office expenses

DemandDemand - estimate of future sales measured in - estimate of future sales measured in customers, units, or dollars. Your actual customers, units, or dollars. Your actual demand is called demand is called sales revenue sales revenue on an Income on an Income Statement.Statement.

Why Estimate Demand, Why Estimate Demand, Expenses & Overhead? Expenses & Overhead?

determine total dollar amount needed to start your determine total dollar amount needed to start your business business

determine appropriate type of financing determine appropriate type of financing assess risk, feasibility, and personal investment assess risk, feasibility, and personal investment have better information to help make decisions have better information to help make decisions set appropriate price set appropriate price manage controllable expenses manage controllable expenses assure profitability assure profitability manage cash flowmanage cash flow

Income Statements Income Statements

Income statements vary in style, However, Income statements vary in style, However, there are parts to an Income Statement that there are parts to an Income Statement that help us separate activities and categories for help us separate activities and categories for tracking and managing our sales and tracking and managing our sales and expenses.expenses.

In the simplest form, an Income statement is In the simplest form, an Income statement is three linesthree lines

RevenueRevenue-Expenses-Expenses= profit/loss= profit/loss

Elements of an Income Elements of an Income Statement Statement

The most important element is your The most important element is your Sales RevenueSales Revenue or just or just revenue. This is the measure of success of your business and revenue. This is the measure of success of your business and marketing strategies. This is the top of the Income Statement.marketing strategies. This is the top of the Income Statement.

REVENUEREVENUE = P x Q (your selling price times quantity sold or = P x Q (your selling price times quantity sold or demand in units)demand in units)

DEMANDDEMAND = Quantity of: = Quantity of: Units (measured in hours, items sold, gallons, meals served, etc.) Units (measured in hours, items sold, gallons, meals served, etc.) Customers (individuals, groups, businesses, etc.) Customers (individuals, groups, businesses, etc.) $ (dollar value of the units demanded)$ (dollar value of the units demanded)

The next section of an Income Statement shows the inventory The next section of an Income Statement shows the inventory expended in producing those sales. This figure includes items expended in producing those sales. This figure includes items given away, lost, damaged and sold.given away, lost, damaged and sold.

Most Important Element Most Important Element is Sales Revenue or is Sales Revenue or RevenueRevenue

This is the top of the Income Statement.This is the top of the Income Statement. REVENUEREVENUE = P x Q (your selling price times quantity sold or = P x Q (your selling price times quantity sold or

demand in units)demand in units) DEMANDDEMAND = Quantity of: = Quantity of: Units (measured in hours, items sold, gallons, meals served, etc.) Units (measured in hours, items sold, gallons, meals served, etc.) Customers (individuals, groups, businesses, etc.) Customers (individuals, groups, businesses, etc.) $ (dollar value of the units demanded)$ (dollar value of the units demanded)

The next section of an Income Statement shows the inventory The next section of an Income Statement shows the inventory expended in producing those sales. This figure includes items expended in producing those sales. This figure includes items given away, lost, damaged and sold.given away, lost, damaged and sold.

CGS = Cost of Goods SoldCGS = Cost of Goods Sold

portion of portion of inventoryinventory sold or otherwise sold or otherwise used up to produce sales used up to produce sales

cost of making or buying the product soldcost of making or buying the product sold

The sales revenue minus CGS gives us The sales revenue minus CGS gives us our our gross profitgross profit, that is profit before , that is profit before accounting for operating expenses and accounting for operating expenses and taxes.taxes.

GROSS PROFIT = Revenue GROSS PROFIT = Revenue less CGSless CGS

(gross profit before operating expenses and (gross profit before operating expenses and taxes)taxes)

OPERATING EXPENSESOPERATING EXPENSES = Expenses to run = Expenses to run the business and generate sales the business and generate sales

PROFIT/LOSSPROFIT/LOSS = the bottom line before taxes = the bottom line before taxes

Operating Expenses and Operating Expenses and Overhead Overhead

Operating expenses are the expenses to Operating expenses are the expenses to produce your sales and to run the business. produce your sales and to run the business. They usually recur each month with slight They usually recur each month with slight fluctuations.fluctuations.

There are two types:There are two types: Selling Expenses - may vary with demand; Selling Expenses - may vary with demand;

often thought of a variable expenses often thought of a variable expenses General & Administrative Expenses - likely General & Administrative Expenses - likely

constant; often referred to as fixed costs or constant; often referred to as fixed costs or overheadoverhead

Sales Revenue Sales Revenue

Revenue equalsRevenue equals price x quantity price x quantity demanded. We need to use our demanded. We need to use our estimated demand and estimated selling estimated demand and estimated selling price to calculate Revenue. Total price to calculate Revenue. Total Revenue = P x QRevenue = P x Q

Selling Price = CGS + FCC + ProfitSelling Price = CGS + FCC + Profit

How the Selling Price is Determined

Total Costs CGS $5

+ Overhead/unit $14

(Fixed Cost Contribution)

$ Markup +Target Profit $6

Selling Price = $25

When and How Much Revenue?

There are two methods for determining when and how much revenue to record on an Income Statement. (1) Accrual versus(2) Cash accounting methods

Cash accounting means that you consistently record sales when the cash is received from the customer. Consequently, you must also record expenses when the cash is paid to vendors and suppliers.

Accrual accounting means that you consistently record sales when the deal is struck and the goods are delivered to the customer. Consequently, you must also record expenses when the deal is struck and the supplies are received from the vendors and suppliers.

For example: suppose you had the following

sales chart for a typical month Sales Revenue: Cash sales = $35,000

Accounts Receivable= 15,000 Total Sales Revenue = $50,000

What is our Revenue for our Income Statement and tax liability? By Cash accounting it is $35,000 By Accrual accounting it's $50,000

NOTE: The bank would want to see $50,000 to give us a loan.We would like the $35,000 for a lower tax liability.

Typical Income Statement

http://www.cabrillo.edu/~dambrosini/188Web/images/incomesams.gif

Review the following sample Income Statement

Task: Re-create the next example of an Income Statement on Excel

Income Statement Exercise

Use the following data to make both an Income Statement and a Cash Flow Statement for the same time period.

Cash Sales $ 15,000Credit Sales 10,000CGS 10,000Rent 3,000Depreciation, buildings 1,000Advertising 1,000Payroll 2,500

The company was started with a $100,000 loan and an investment of $100,000.

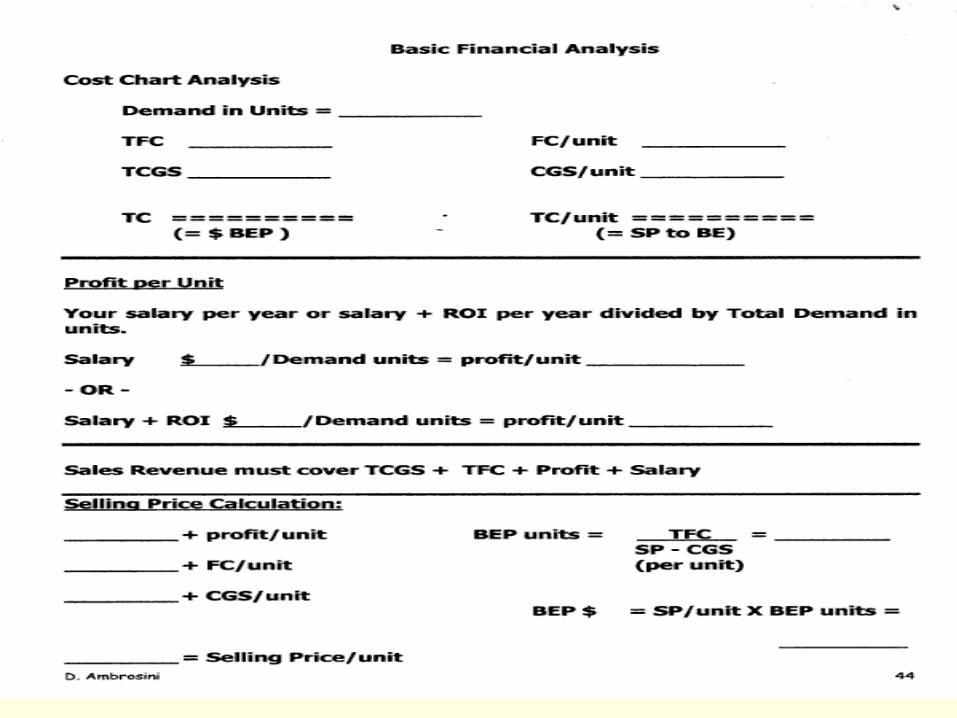

Basic Financial Analysis

Create the next form on Excel http://www.cabrillo.edu/~dambrosini/

188Web/classsessions/operatingcosts.htm

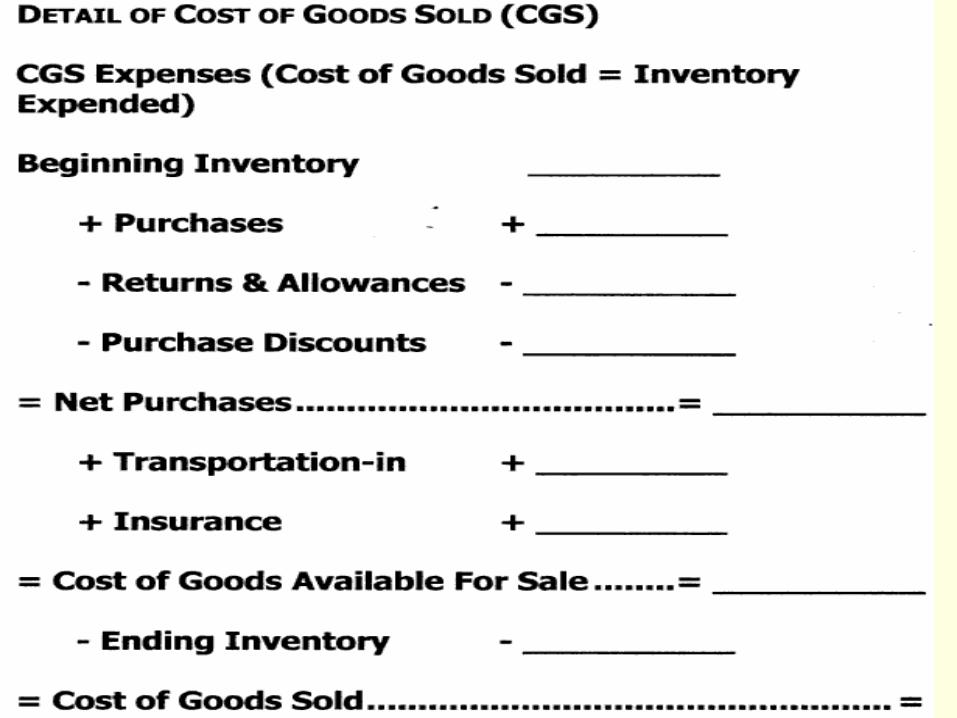

Cost of Goods Sold

Cost of Goods Sold can be complicated to calculate. The following example illustrates the components of CGS.

Create the next form on Excel