Accounting - CE Workshops · Moral obligations refer to a duty or obligation that "is sanctioned by...

50

Accounting

-

Upload

nguyenminh -

Category

Documents

-

view

214 -

download

0

Transcript of Accounting - CE Workshops · Moral obligations refer to a duty or obligation that "is sanctioned by...

Accounting

Dr. Nitish Singh (PhD/MBA/MA) Professor, Boeing Institute of International Business, St. Louis University Compliance Consultant, IntegTree LLC. E-mail: [email protected]

Copyright © Nitish Singh 2015 onwards All Rights Reserved. The Complete Document is copyrighted. Unauthorized Reproduction and Distribution is Prohibited. The program module was developed by Professor Nitish Singh, Saint Louis University, USA Published By: The Localization Institute All material presented in these online modules is only for internal educational use and cannot be reproduced, stored or transmitted in any form or by any means, without the written permission of the course leader. Permission request can be sent to Professor Nitish Singh: [email protected] The information contained in these online modules has been obtained from various academic and professional sources, which we believe to be reliable. However, neither its completeness nor accuracy can be guaranteed. Recommendations and opinions are based on our interpretation of available information. References for the presentation are available upon request

About The Presenter: Dr. Nitish Singh • Published more than 55 papers, presented at 70+

conferences and authored 4 books. I have educated executives from AT&T, Boeing, British Sky Broadcasting, Bunge, Dunken Brands, Emirates National Oil, Johnson Controls, Monsanto, Northern Trust, Novartis, Suncor, Verisign, Weatherford, Wells Fargo, and many more.

• Recently published a Compliance Handbook which covers the development and implementation of compliance

programs (Compliance Management: A How-to Guide for Executives, Lawyers, and Other Compliance Professionals).

• LINK to the Book: www.integtree.com/book

3

Disclaimer: This material is confidential and proprietary to IntegTree LLC © and may not be reproduced, published or disclosed to others without the express written authorization of IntegTree LLC. IntegTree LLC is not a law firm and is not engaged in providing legal or other similar professional advice or services. In providing our services, IntegTree LLC attempts to provide its clients with “effective practices” in light of then-current laws and regulations. IntegTree’s services should not replace advice from your in-house or outside counsel or their opinions concerning best company practices.

Doing the Right Thing Can a business allow its employees to indulge in unethical behavior like

stealing from the company or perpetuating

an atmosphere of lies and deceit?

Can a business indulge in unscrupulous acts with complete immunity from reprisal?

Can a business afford to lose the trust of its customers that takes years to build?

Can a business sell defective products or services and expect no consumer backlash?

5

Can You Bear the Consequences? The lack of ethical considerations can result in some serious negative outcomes:

1. Lack of organizational trust 2. Dishonesty 3. Fraud/criminal acts 4. Work place harassment/discrimination/bullying 5. Exaggerated risk of employee misconduct 6. Reputational harm 7. Loss of productivity 8. Low employee morale 9. Monetary Fines 10. Lawsuits 11. Personal and company bankruptcy 12. Jail time!

6

Let them Burn…

7

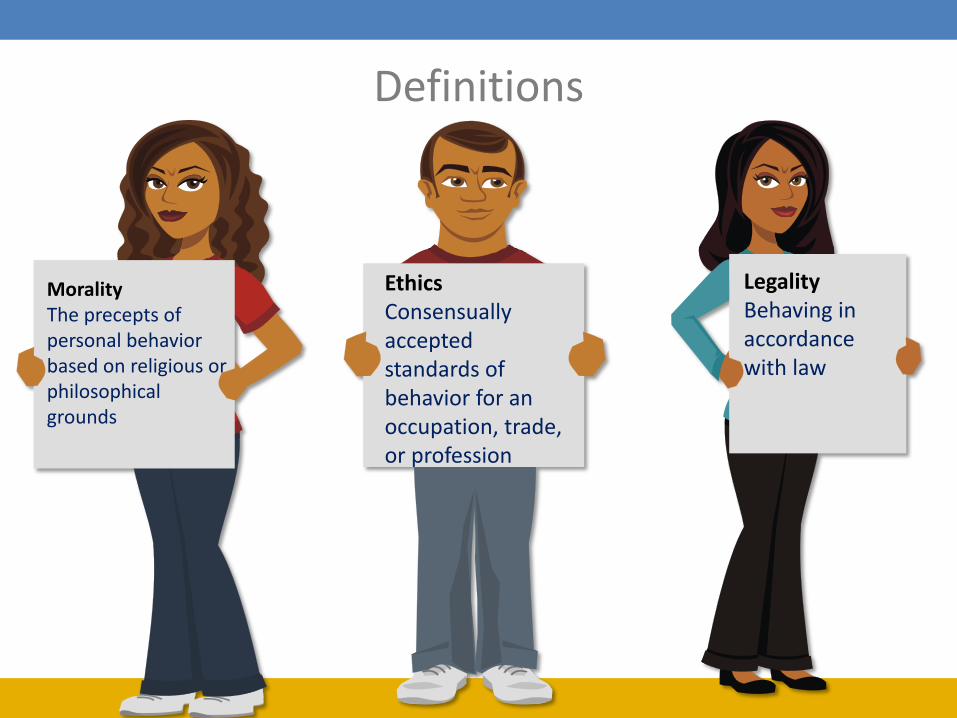

Definitions

Morality The precepts of personal behavior based on religious or philosophical grounds

Ethics Consensually accepted standards of behavior for an occupation, trade, or profession

Legality Behaving in accordance with law

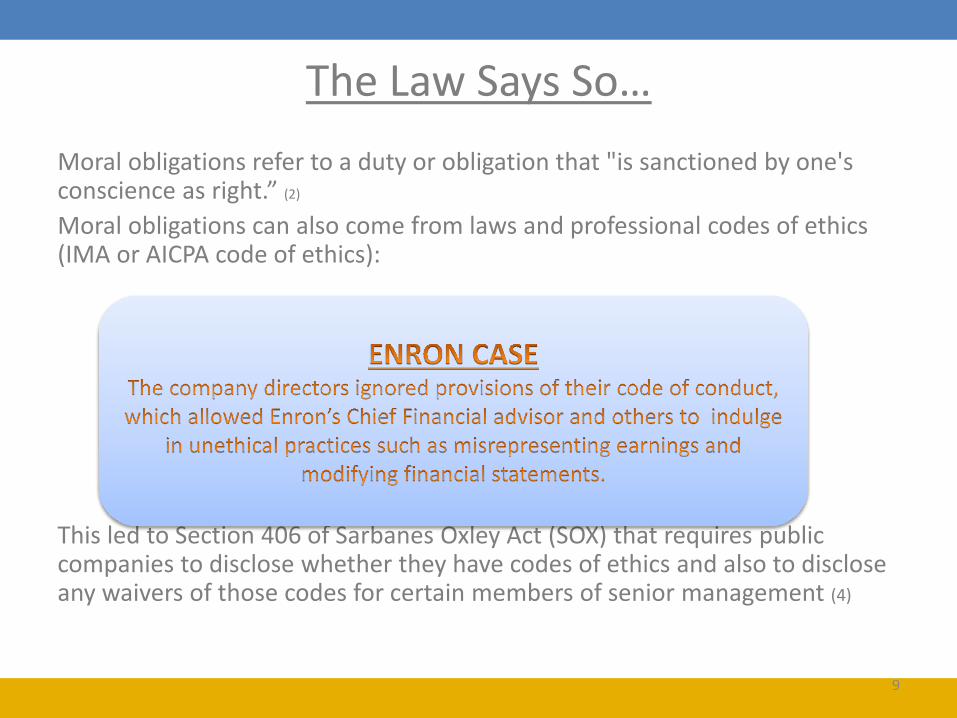

The Law Says So… Moral obligations refer to a duty or obligation that "is sanctioned by one's conscience as right.” (2)

Moral obligations can also come from laws and professional codes of ethics (IMA or AICPA code of ethics): This led to Section 406 of Sarbanes Oxley Act (SOX) that requires public companies to disclose whether they have codes of ethics and also to disclose any waivers of those codes for certain members of senior management (4)

9

The Law Says So…

Sarbanes Oxley requires public companies to disclose whether they have adopted a code of ethics/conduct. These codes of ethics are important pillars for facilitating ethical decision making

The Federal Sentencing Guidelines for Organizations (FSGO) also encourages ethical decision making in organizations by having organizations establish a culture of ethical conduct and compliance with the laws

10

Moral Imagination

• Moral imagination demands that we abandon the myopic view of short-term profits and embrace a wider appreciation of the impact we have on diverse constituencies over time

11

Ethics: The consensually accepted standards of behavior for an occupation, trade, or profession

Morality: The precepts of personal behavior based on religious or philosophical grounds

Ethical Traits: honesty, responsibility, reliability, fairness, respect for others, compassion, accountability and integrity

12

Is it Moral or Immoral?

• How do we come to an understanding of what is moral or ethical?

• Is our understanding of morals superior to others?

• Shall we impose our morals and ethics on other cultures?

• Is there a set of universal ethics?

13

Universal Values

• Universal Values imply that there are a set of morals or ethics that are universal and that everybody is capable of following them

• Cultural imperialism implies that one particular set of national or cultural code of conduct or set of moral principles is superior to all others

• Problem with universalism: a universal value has to be of same value or worth, and be acceptable to all at every time and in every situation

14

STEAK ANYONE ?

15

Relativism • Based on the relativistic point of view that there is no absolute right

or wrong

• Aligned to this view is the idea of Cultural Relativism, wherein the morals and ethics are not universal, but rather culturally determined

• If cultural relativism is to be taken at face value and followed in the world, then it would be impossible to criticize what goes on morally and ethically in different cultures at different times (Mitchell, 2003)

Can you give some examples?

16

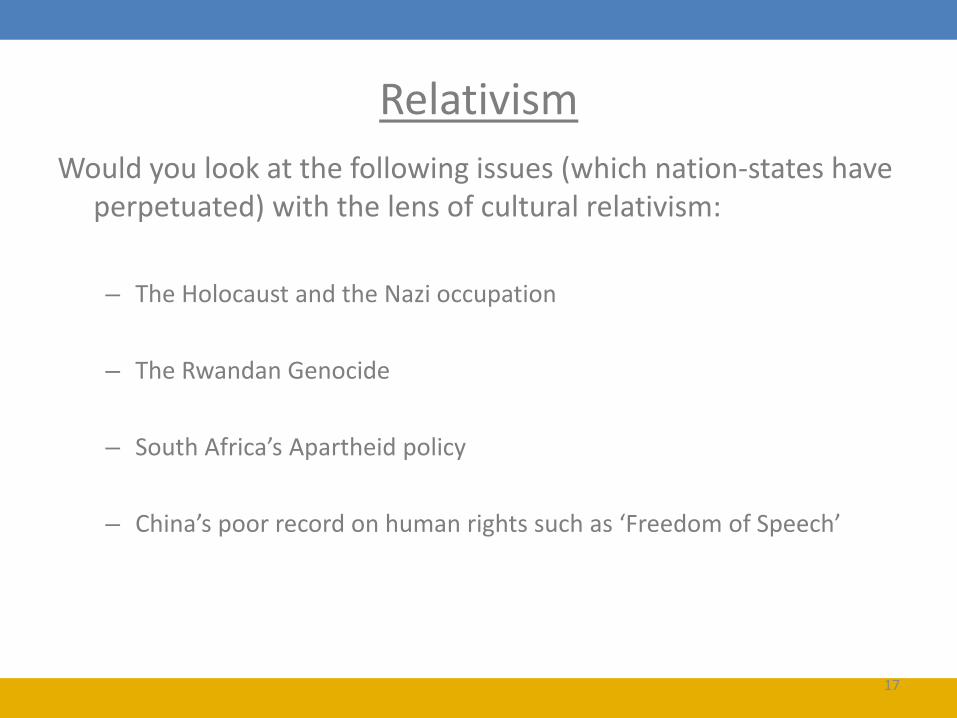

Relativism Would you look at the following issues (which nation-states have

perpetuated) with the lens of cultural relativism:

– The Holocaust and the Nazi occupation

– The Rwandan Genocide

– South Africa’s Apartheid policy – China’s poor record on human rights such as ‘Freedom of Speech’

17

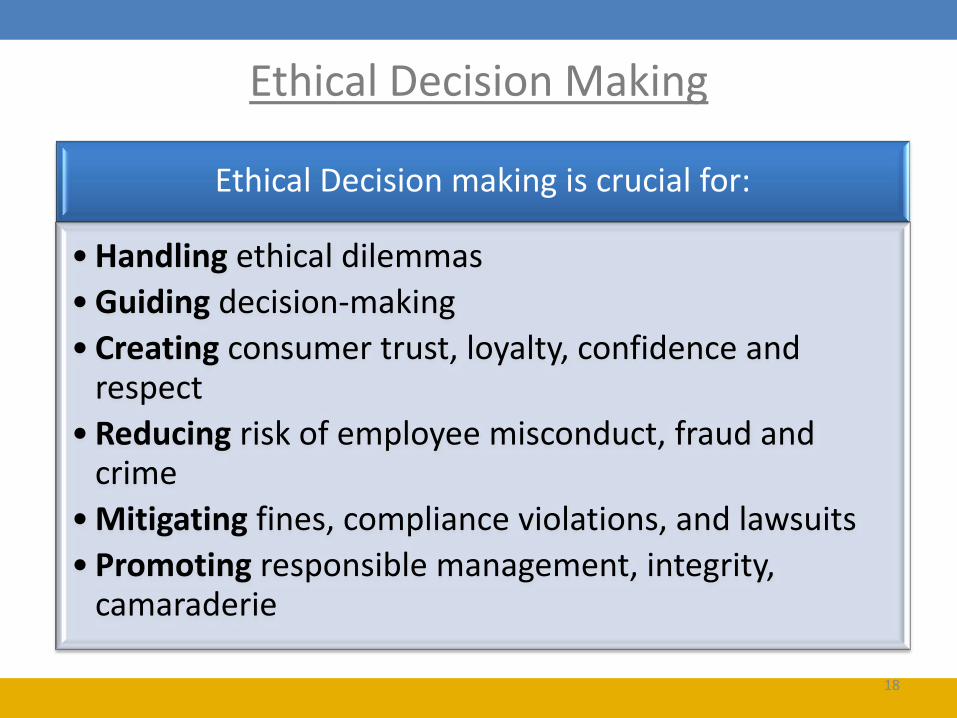

Ethical Decision Making

Ethical Decision making is crucial for:

• Handling ethical dilemmas • Guiding decision-making • Creating consumer trust, loyalty, confidence and

respect • Reducing risk of employee misconduct, fraud and

crime • Mitigating fines, compliance violations, and lawsuits • Promoting responsible management, integrity,

camaraderie

18

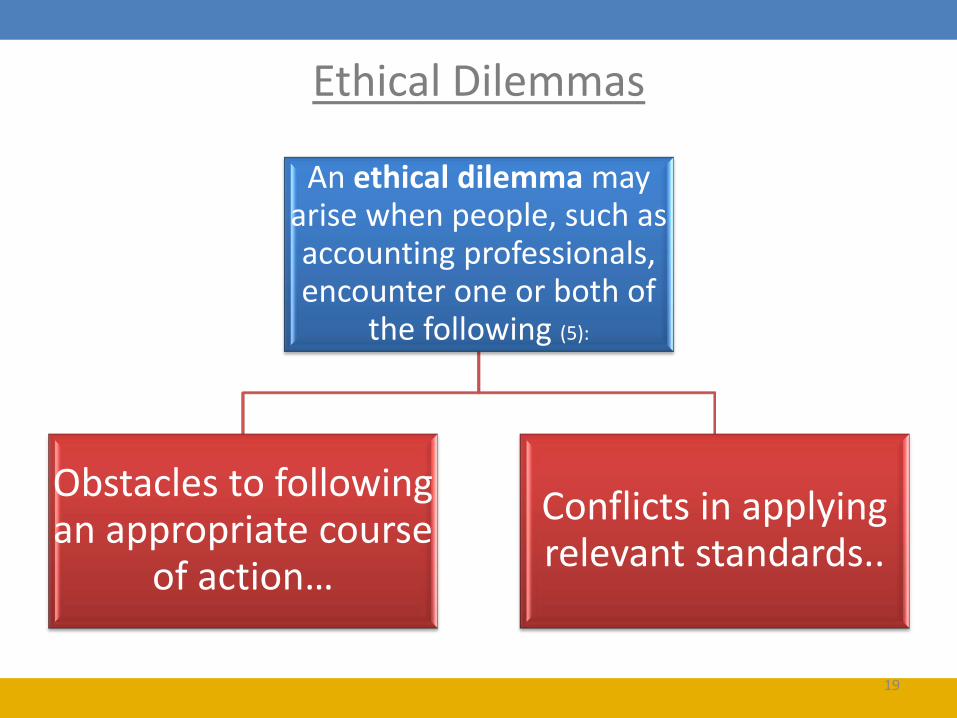

Ethical Dilemmas

An ethical dilemma may arise when people, such as accounting professionals, encounter one or both of

the following (5):

Obstacles to following an appropriate course

of action…

Conflicts in applying relevant standards..

19

The AICPA: Resolving Ethical Conflicts (5)

!

22

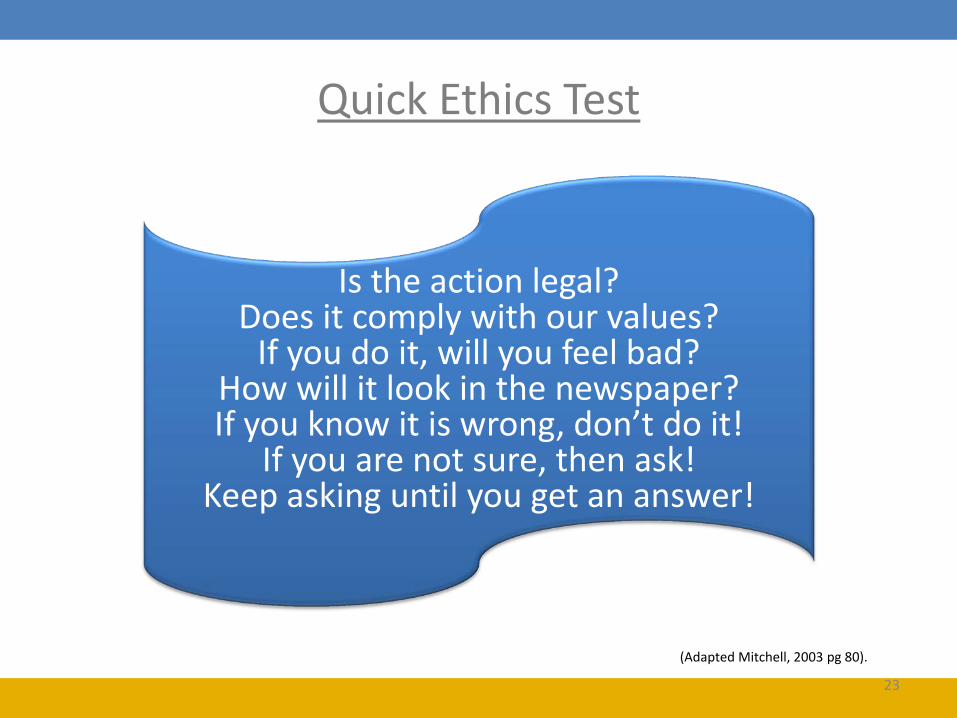

Quick Ethics Test

(Adapted Mitchell, 2003 pg 80).

Is the action legal? Does it comply with our values?

If you do it, will you feel bad? How will it look in the newspaper? If you know it is wrong, don’t do it!

If you are not sure, then ask! Keep asking until you get an answer!

23

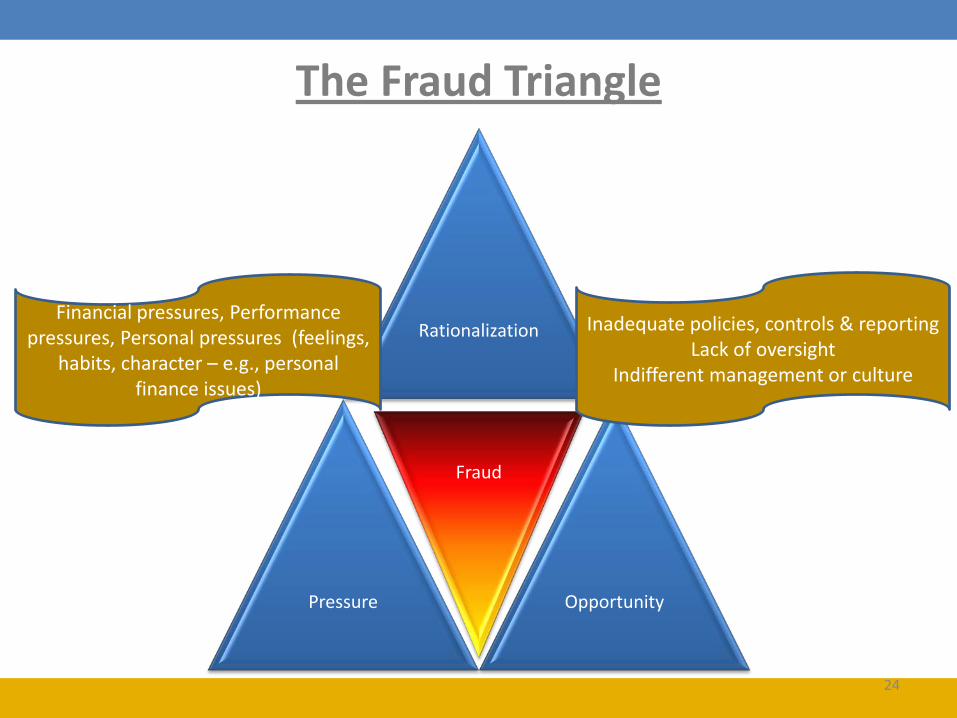

The Fraud Triangle

Rationalization

Pressure

Fraud

Opportunity

Inadequate policies, controls & reporting Lack of oversight

Indifferent management or culture

Financial pressures, Performance pressures, Personal pressures (feelings,

habits, character – e.g., personal finance issues)

24

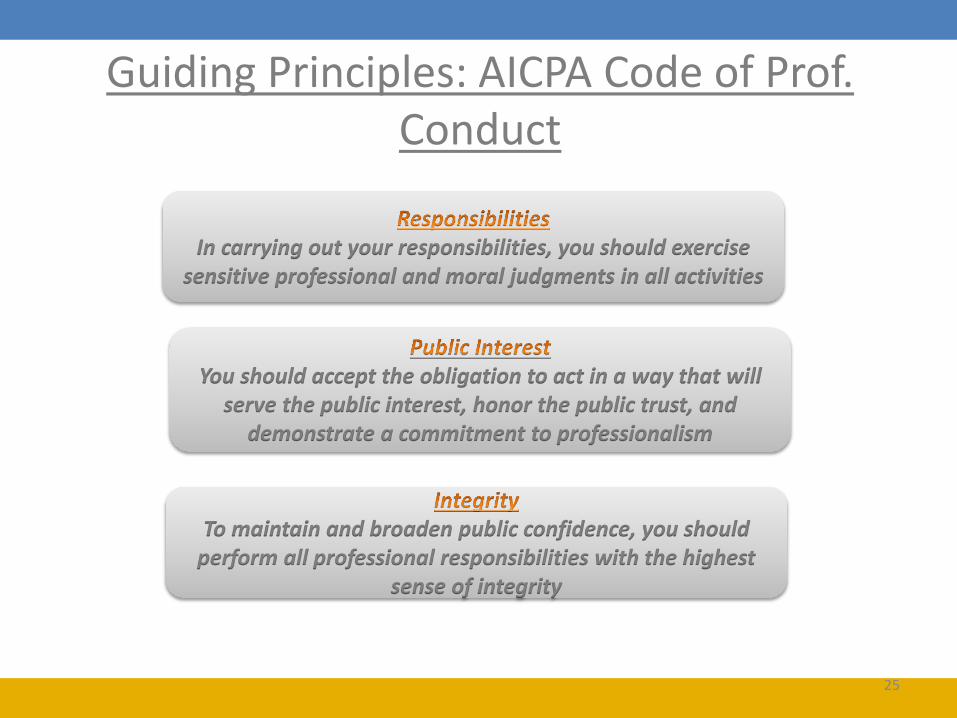

Guiding Principles: AICPA Code of Prof.

Conduct

In carrying out your responsibilities, you should exercise sensitive professional and moral judgments in all activities

You should accept the obligation to act in a way that will serve the public interest, honor the public trust, and

demonstrate a commitment to professionalism

To maintain and broaden public confidence, you should perform all professional responsibilities with the highest

sense of integrity

25

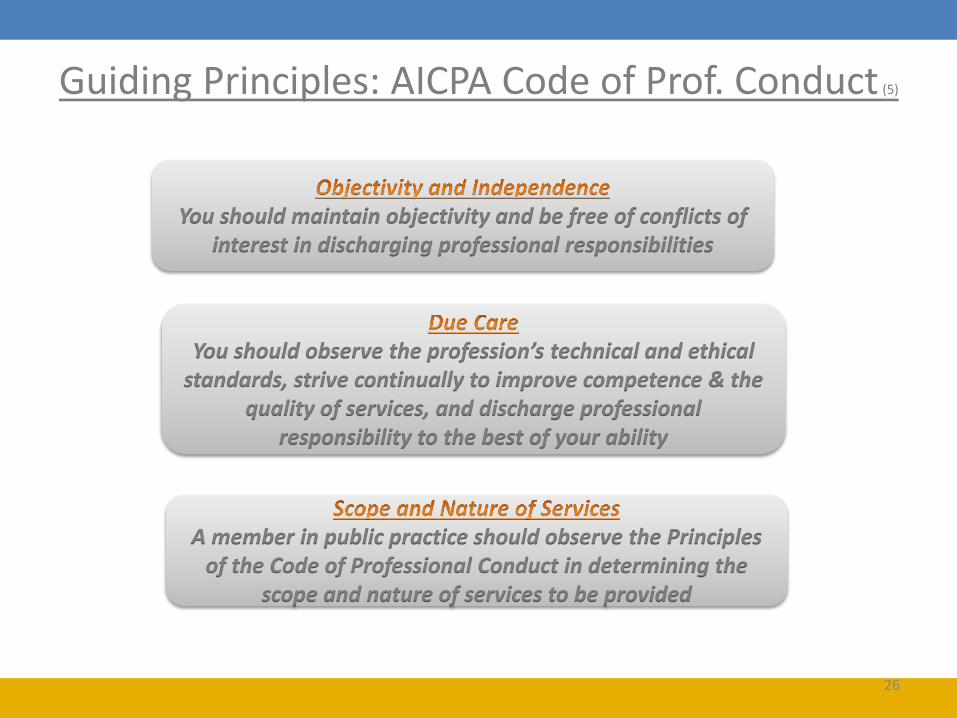

Guiding Principles: AICPA Code of Prof. Conduct (5)

You should maintain objectivity and be free of conflicts of interest in discharging professional responsibilities

You should observe the profession’s technical and ethical standards, strive continually to improve competence & the

quality of services, and discharge professional responsibility to the best of your ability

A member in public practice should observe the Principles of the Code of Professional Conduct in determining the

scope and nature of services to be provided

26

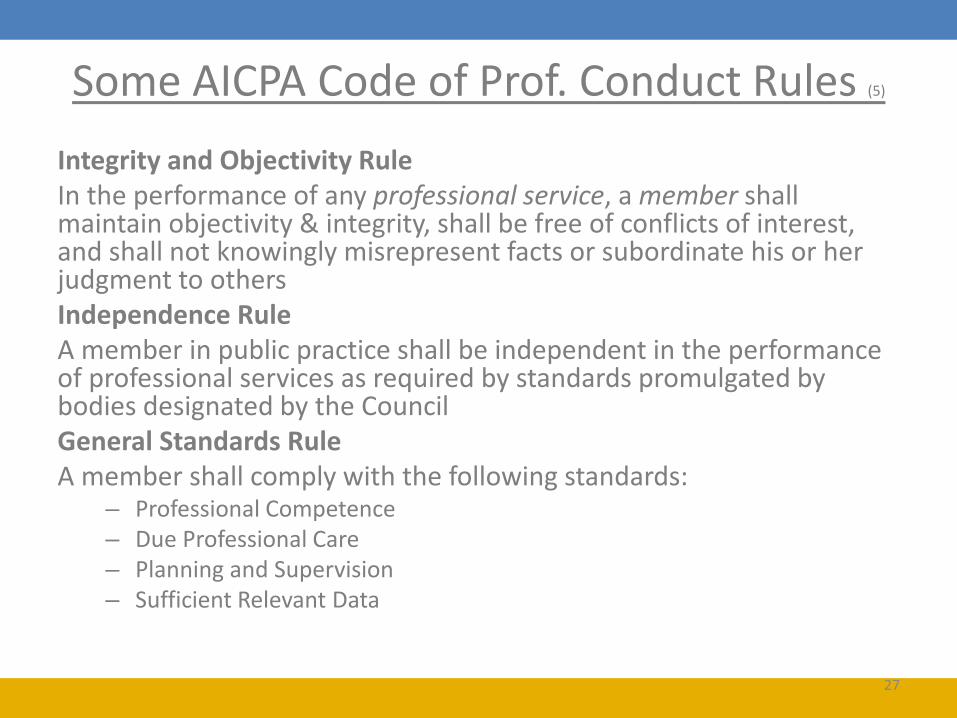

Some AICPA Code of Prof. Conduct Rules (5)

Integrity and Objectivity Rule In the performance of any professional service, a member shall maintain objectivity & integrity, shall be free of conflicts of interest, and shall not knowingly misrepresent facts or subordinate his or her judgment to others Independence Rule A member in public practice shall be independent in the performance of professional services as required by standards promulgated by bodies designated by the Council General Standards Rule A member shall comply with the following standards:

– Professional Competence – Due Professional Care – Planning and Supervision – Sufficient Relevant Data

27

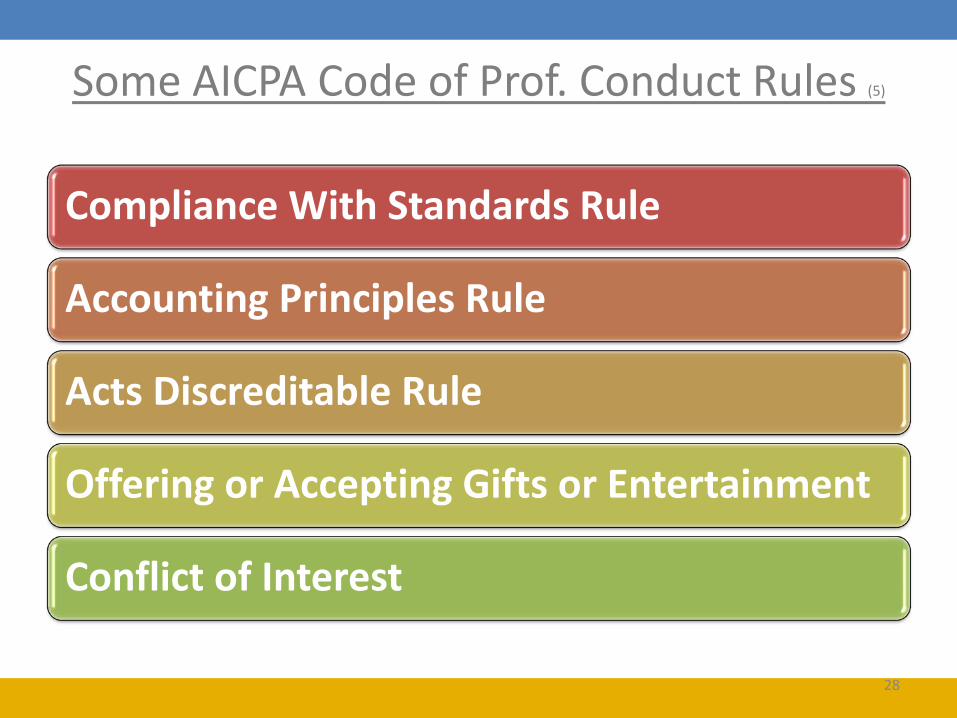

Some AICPA Code of Prof. Conduct Rules (5)

Compliance With Standards Rule

Accounting Principles Rule

Acts Discreditable Rule

Offering or Accepting Gifts or Entertainment

Conflict of Interest

28

Deloitte Vice-Chairman Caught Insider Trading (6) • Deloitte & Touche LLP Vice-Chairman Tom Flanagan

sentenced to 21 months in prison for insider trading

• He used insider information to trade on client’s stock between 2005-2008 – over $400,000 in profits, and shared that information with his son [6]. Tom Flanagan received 21 months in prison, in addition to fines and penalties [7]

30

Real World Examples of Unethical Behavior

Sherry Hunt – Whistleblower at Citigroup

• She was tasked with uncovering fraud and avoiding mal-investments [8] Her concerns about Citigroup’s mortgage unit were not addressed even after discussing the issues with Citigroup HR and Ethics[9]

• According to Hunt, executives buried her discoveries, and she was told that the number of defective/bad loans would need to be reduced or it would be “your asses on the line.” [3]

• Rather than engage in dishonest behavior, Hunt sued – joined by the Department of Justice. Citigroup did not dispute the allegations, and settled the case. It is worth noting that, according to Hunt, Citigroup executives engaged in this cover-up and intimidation “before, during and after the financial crisis, and even into 2012.” [3] So, despite reforms, this type of unethical behavior is still prevalent in the financial industry

31

Ethical Considerations: Fiduciary Duties

• A fiduciary duty is a legal duty to act solely in another party's interests.

• A fiduciary should set aside his/her personal interests for those of the principal

• Fiduciary may not profit from the relationship with the principals unless fiduciary has the principals' express informed consent

• And avoid any conflicts of interests between fiduciary and the principal.

Real World Application for Financial Advisors

The Fiduciary Rule

33

Very Brief History – Employee Retirement Income Security Act of 1974 (ERISA)

• Minimum standards and federal income tax rules for private pension plans

• Required disclosure of certain financial information, standards of conduct for

fiduciaries, etc.

• Private sector plans must follow Financial Accounting Standards Board (FASB )requirements.

• Primary cause for passage: concerns about under-funded pension plans and shady vesting requirements.

• However increasingly retirement funding is self-directed and there is movement away from defined pension plans.

• Focus is on updating the definition of “fiduciary investment advice” under ERISA to extend protections to more self-directed retirement vehicles.

• In essence – expand the definition of fiduciary to those who provide investment advice or recommendations to ERISA plans and IRAs.

34

Concerns • Distilled to a single quote: “[a]nd the challenge we've got is right now,

there are no uniform rules of the road that require retirement advisors to act in the best interests of their clients -- and that's hurting millions of working and middle-class families. There are a lot of very fine financial advisors out there, but there are also financial advisors who receive backdoor payments or hidden fees for steering people into bad retirement investments that have high fees and low returns. So what happens is these payments, these inducements incentivize the broker to make recommendations that generate the best returns for them, but not necessarily the best returns for you.” – President Barrack Obama, Save our Retirement Coalition Speech – February 23, 2015 – AARP HQ

• Full Details available in the report: • The Effects of Conflicted Investment Advice on Retirement

Savings - by Council of Economic Advisers

35

Taking a Step Back: Specific Components of a Fiduciary

• Legal and ethical concept – A fiduciary holds confidence and trust of the principal – Broadly requires the party to act in the best interest of the principal – Specific standards and rules depending on circumstances – e.g., in

Corporate Law: • “Duty of Care” -- requires ‘reasonable standards of care’ –

no acts or omissions to cause harm – be informed, no negligence.

• “Duty of Loyalty” – addresses conflict of interest – maintain principal’s interest over agent’s

• “Duty of Good Faith” – must act as a ‘reasonably prudent’ person would.

– Examples include: • Trustee/Beneficiary • Corporate Director/Shareholder

36

Broad Strokes

• To what standard do we hold those who offer financial advice?

• Not a philosophical “how many angels can dance on the head of a pin” type of question – as in so many areas of ethics, one that has measurable, concrete, real-world impact.

37

Political Turmoil

• President Trump asked the Department of Labor to review the rule in early February 2017.

• In May 2017, Labor Secretary Alexander Acosta stated “[r]espect for the rule of law leads us to the conclusion that this date cannot be postponed.”

38

Where We Are At

• Some elements went into effect June 9th – However enforcement provisions are not in effect until Jan 1st 2018 – Investment advisers are now considered fiduciaries and are held to the “impartial conduct standard”.

– According to the US Department of Labor Conflict of Interest FAQs for the ‘Transition Period’ (June 9,

2017 – January 1, 2018) – this standard can be broken down into two major components:

• Prudence Standard – “the advice must meet a professional standard of care as specified in the text of the exemption”; and

• Loyalty Standard – “the advice must be based on the interests of the customer, rather than the competing financial interest of the adviser or firm”

• Advisors can “charge no more than reasonable compensation” • And they can “[m]ake no misleading statements about investment transactions,

compensation, and conflicts of interest“ • “Best-Interest Contract Exemption” (BICE) – can receive commissions in perhaps

grey-area conflict situations, provided acting in best interest of client and not mispresent choices

39

Broader Concerns

• The American College of Financial Services conducted the “Retirement Income Planning Quiz” in 2014 – interviewing over 1,000 individuals between the ages of 60 and 75 with at least 100k in assets.

• Only 19% passed the quiz – no one received a 90% or higher. – Largely confused by concepts such as:

• The relationship between interest rate rises and the value of bond funds

• Annuities • The “4%” rule (i.e., the ‘safe’ withdrawal of 4% of your

retirement account per year – to avoid depleting your savings prematurely).

40

Some Ethical Questions

• What kind of actual disclosures are possible if the subject matter is so foreign to a client? – By analogy, in medicine, the concept of “informed consent” exists –

the patient or their guardian must understand the risks and benefits associated with a procedure. You have an ethical (and legal) right to the information required to make reasonable decisions about your health….

– Should it translate into financial matters?

– If so, how does this translate into financial matters?

41

What Do You Think? – Can clients operate with this kind of ‘informed consent’ if they lack a

rudimentary understanding of the field in which they are operating?

– How much understanding does a client need to have to waive a conflict of interest (i.e., is there a difference between disclosing facts/relationships, and insuring a client appreciates the facts/relationships)?

– Who has the responsibility to educate the client? The client? The adviser? The government?

– Are some conflicts ethically non-waivable, regardless of disclosure?

– More broadly: are regulatory standards stringent enough, or do they often fall short of our ethical duties?

42

Additional Resources and Perspectives on the Fiduciary Rule

• http://www.estateplan-hc.org/Hampden%20DOL%20Rule%20Presntation.pdf

• https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/faqs/retirement-plans-and-erisa-consumer

• https://www.forbes.com/sites/ashleaebeling/2015/04/14/dol-issues-proposed-fiduciary-rule-2015-version/#62109c5c4927

• http://www.thinkadvisor.com/2017/06/23/how-dol-fiduciary-rule-can-boost-advisors-profits

43

Some Related Ethical Considerations for Attorneys

ABA Rule 1.8 (a) (Excerpts) (14)

A lawyer shall not enter into a business transaction with a client or knowingly acquire an ownership, possessory, security or other pecuniary interest adverse to a client unless: • the transaction and terms on which the lawyer acquires the interest

are fair and reasonable to the client and are fully disclosed and transmitted in writing in a manner that can be reasonably understood by the client;

• the client is advised in writing of the desirability of seeking and is given a reasonable opportunity to seek the advice of independent legal counsel on the transaction; and

• the client gives informed consent, in a writing signed by the client, to the essential terms of the transaction and the lawyer's role in the transaction, including whether the lawyer is representing the client in the transaction.

44

Why Good People Sometimes Do Unethical Things

1. Short term gain and short term thinking 2. Lack of knowledge around acceptable business practices 3. Lack of proper code of ethics 4. Yielding to temptation 5. Thrill seeking 6. Low moral expectations at a workplace 7. Peer pressure 8. Acceptable industry practice - because everyone does it! 9. If big guys are doing it…It's my company, and I can do whatever I want!" 10. If it is not illegal then it is ethical 11. If it is for the greatest good 12. Competitive rivalry 13. Personal problems 14. Just a small and one time mistake? Or if the $$ amount is small it's

alright! 15. There are worse things than what I did 16. Deep rooted culture of mistrust

45

Why Should I Be Ethical?

1. Happiness comes from ethical growth 2. Doing good makes you feel good 3. Moral growth give you purpose in life 4. Repercussions of unethical behavior not only impact you but your

family, friends and colleagues 5. Less likely to get in trouble and decreased vulnerability 6. Sense of integrity and conviction 7. Ethical character is infectious 8. People want to do business with and be friends with people who

are ethical and trustworthy 9. Spiritual and emotional rewards 10. Be a role model to others 11. Generates respect and self-respect 12. Creates optimism and dispels FEAR 13. Who knows--Might get to meet JESUS!

46

Conclusion • Ethical behavior is rewarding in and of itself (intrinsically

rewarding).

• Ethical behavior can result in greater profitability and business success over the long run (extrinsically rewarding).

• Ethical behavior can help you avoid prison and lawsuits.

• A lawyer and accountant’s value to an enterprise is inexorably linked to the ethical orientation of the practitioner. You are bulwarks against fraud and corruption, and guardians of transparency and honest reporting.

47

Conclusion

Ethical behavior is rewarding in

and of itself

Ethical behavior results in

profitability and business success

Ethical behavior can help avoid

prison and lawsuits.

A accountant’s value to an

enterprise is inexorably linked

to ethical orientation

48

References and Notes 1. Picture credit for slide 6. https://c2.staticflickr.com/8/7442/11898617276_b54556deff_h.jpg 2. Nancy B. Kurland, Sales Agents and Clients: Ethics, Incentives, and a Modified Theory of Planned Behavior, 49 Hum. Rel. 51,

59 (1996) [hereinafter Kurland, Sales Agents] 3. Langenderfer, Harold Q., and Joanne W. Rockness. "Integrating ethics into the accounting curriculum." Accounting Ethics:

Theories of accounting ethics and their dissemination 2.1 (2006): 346. & cross reference 4. http://corporate.findlaw.com/law-library/corporate-ethics-and-sarbanes-oxley.html 5. The AICPA Code of Professional Conduct

http://www.aicpa.org/Research/Standards/CodeofConduct/DownloadableDocuments/2014December15CodeOfProfessionalConduct.pdf

6. Former Deloitte vice chairman get 21 months for insider trading (Chicago Tribune) http://articles.chicagotribune.com/2012-10-26/business/chi-former-deloitte-insider-trading-20121026_1_deloitte-partner-insider-thomas-flanagan

7. http://www.bloomberg.com/news/articles/2012-10-26/exdeloitte-partner-gets-21-months-for-insider-trades-1 8. http://www.bloomberg.com/news/articles/2012-05-31/woman-who-couldn-t-be-intimidated-by-citigroup-wins-31-million 9. http://www.reuters.com/article/2012/02/17/us-citigroup-whistleblower-idUSTRE81G06Y20120217 10. http://dealbook.nytimes.com/2013/04/09/kpmg-said-to-resign-as-herbalifes-auditor-over-investigation/?_r=0 11. http://ir.herbalife.com/releasedetail.cfm?ReleaseID=755276 12. http://www.icaew.com/~/media/corporate/files/technical/ethics/ethical%20case%20studies/ccabeg%20case%20studies%2

0accountants%20public%20practice.ashx 13. https://www.law.cornell.edu/wex/fiduciary_duty 14. http://www.americanbar.org/groups/professional_responsibility/publications/model_rules_of_professional_conduct/rule_1

_8_current_clients_specific_rules.html 15. https://www.forbes.com/sites/jamiehopkins/2017/06/14/new-fiduciary-rule-for-financial-advisors-moves-the-needle-but-

in-which-direction/#30656b964caa 16. Additional sources available upon request.

49

Additional Resources

• The Book- Compliance Management:

http://www.integtree.com/book/

• The Corporate Ethics and Compliance Professors’ Blog and Newsletter Mailing List

• www.ethicsresources.org

• Is It A Bribe or Is It A Gift? Facilitating Ethical Decision Making

• www.integtree.com/courseware/

• Bribe or Gift Checklist • www.integtree.com/checklist/

50