Accounting & Auditing Year in Review · Accounting & Auditing Year in Review. May 19-22, 2019 •...

168

Monday, May 20, 2019 Los Angeles, California Accounting & Auditing Year in Review May 19-22, 2019 • Los Angeles, California 113 th Annual Conference Learn more by visiting us at gfoa.org • #GFOA2019 Melinda Gildart, CPA, MBA Controller, Chicago Public Schools R. Kinney Poynter, CPA Executive Director, National Association of State Auditors, Comptrollers, and Treasurers David A. Vaudt, CPA Chairman, Governmental Accounting Standards Board Michele Mark Levine, CPA Director, Technical Services Center, Government Finance Officers Association

Transcript of Accounting & Auditing Year in Review · Accounting & Auditing Year in Review. May 19-22, 2019 •...

Monday, May 20, 2019Los Angeles, California

Accounting & Auditing Year in Review

May 19-22, 2019 • Los Angeles, California113th Annual Conference

Learn more by visiting us at gfoa.org • #GFOA2019

Melinda Gildart, CPA, MBAController, Chicago Public Schools

R. Kinney Poynter, CPAExecutive Director, National Association of State Auditors, Comptrollers, and Treasurers

David A. Vaudt, CPAChairman, Governmental Accounting Standards Board

Michele Mark Levine, CPADirector, Technical Services Center, Government Finance Officers Association

SESSION AGENDA

I. Auditing Year In ReviewII. GASB Research & Technical

Agenda UpdateIII.Accounting Year In Review

2

I. Auditing Year in Review

2019 GFOA Annual ConferenceLos Angeles, CaliforniaMay 20, 2019

R. Kinney Poynter, Executive Director

Today’s Audit Agenda

• OMB Uniform Guidance• GAO’s Government Auditing Standards: 2018 Revision• AICPA – Current Issues• Other Emerging Issues

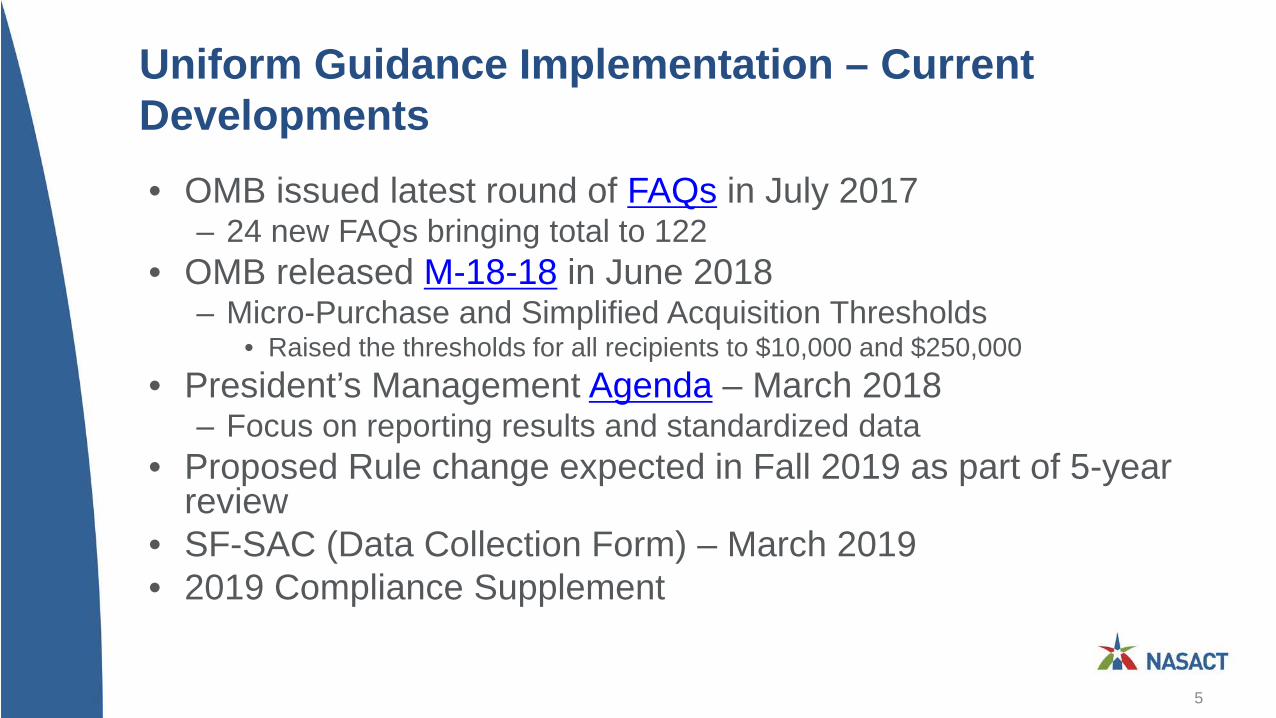

Uniform Guidance Implementation – Current Developments • OMB issued latest round of FAQs in July 2017

– 24 new FAQs bringing total to 122• OMB released M-18-18 in June 2018

– Micro-Purchase and Simplified Acquisition Thresholds• Raised the thresholds for all recipients to $10,000 and $250,000

• President’s Management Agenda – March 2018– Focus on reporting results and standardized data

• Proposed Rule change expected in Fall 2019 as part of 5-year review

• SF-SAC (Data Collection Form) – March 2019• 2019 Compliance Supplement

5

Implementation Issue: Pension and OPEB Costs Allowability

• Section 200.431(g)(3)– “For entities using accrual based accounting, the cost assigned

to each fiscal year is determined in accordance with GAAP”• GASB 68 calculated pension costs differ from the amounts funded

– HHS DCA is currently allowing amounts funded in excess of GASB 68 amount (but awaiting OMB guidance)

– OMB hopes to release a proposed revision in summer 2018• Similar issue for OPEB costs

6

Implementation Issue: Leases

• Section 200.465(c)(5)– “Rental costs under leases which are required to be treated

as capital leases under GAAP are allowable only up to the amount that would be allowed had the non-Federal entity purchased the property on the date the lease agreement was executed.”

• GASB 87 establishes a single model for lease accounting, and eliminates all distinctions between operating and capital leases

– How will the provisions of UG that specifically reference GAAP capital leases be applied?

– Will UG’s capitalization threshold of $5,000 apply?

7

2019 SF-SAC (Data Collection Form)• Released twice for comments

– Published for comments in Federal Register on April 3, 2018

– Published for comments in Federal Register on November 6, 2018

• Final form approved by March 25, 2019– Release on Internet Data Entry System (IDES) in May 2019

• New form is to be used for audits covering fiscal periods ending in 2019, 2020, and 2021

8

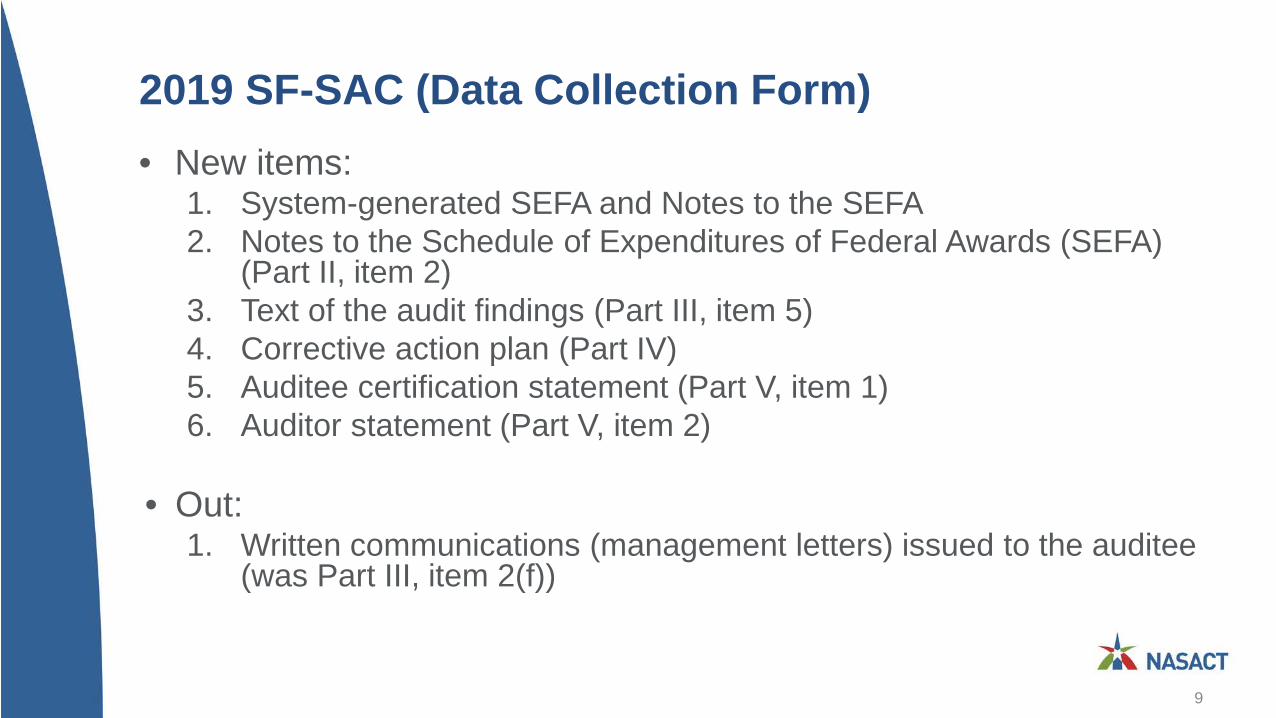

2019 SF-SAC (Data Collection Form)• New items:

1. System-generated SEFA and Notes to the SEFA2. Notes to the Schedule of Expenditures of Federal Awards (SEFA)

(Part II, item 2)3. Text of the audit findings (Part III, item 5)4. Corrective action plan (Part IV)5. Auditee certification statement (Part V, item 1) 6. Auditor statement (Part V, item 2)

• Out:1. Written communications (management letters) issued to the auditee

(was Part III, item 2(f))

9

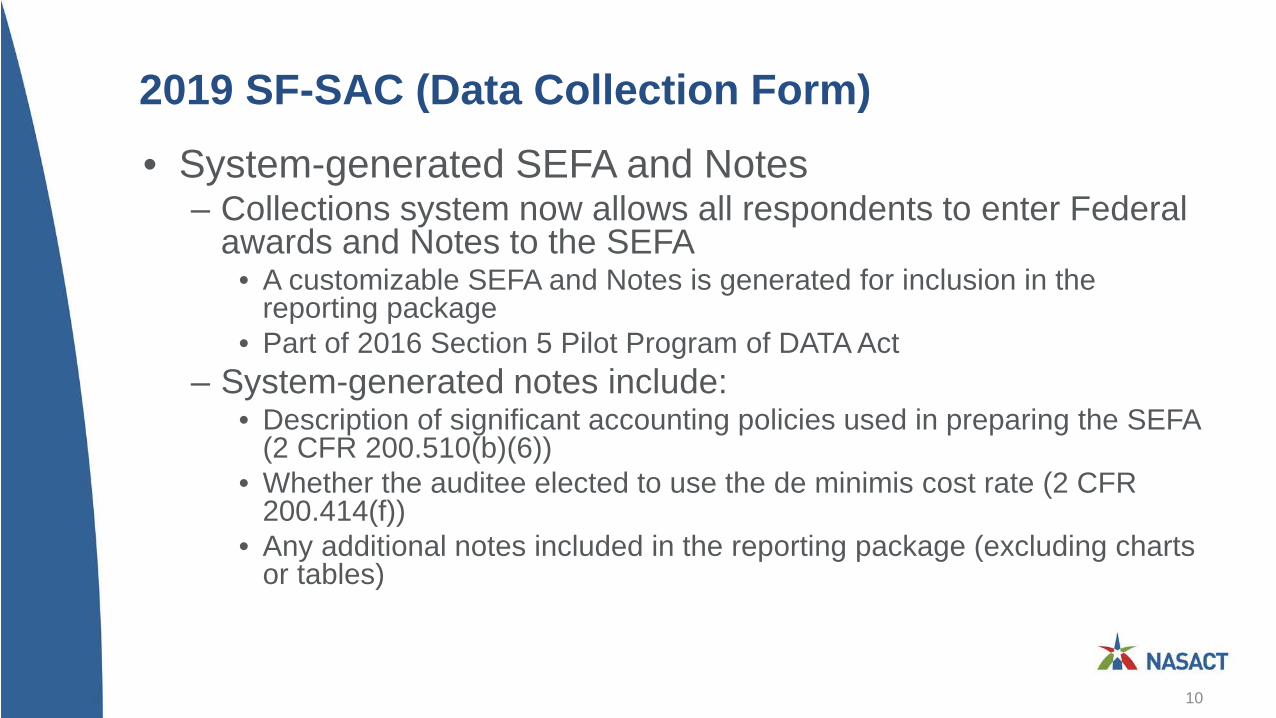

2019 SF-SAC (Data Collection Form)• System-generated SEFA and Notes

– Collections system now allows all respondents to enter Federal awards and Notes to the SEFA

• A customizable SEFA and Notes is generated for inclusion in the reporting package

• Part of 2016 Section 5 Pilot Program of DATA Act– System-generated notes include:

• Description of significant accounting policies used in preparing the SEFA (2 CFR 200.510(b)(6))

• Whether the auditee elected to use the de minimis cost rate (2 CFR 200.414(f))

• Any additional notes included in the reporting package (excluding charts or tables)

10

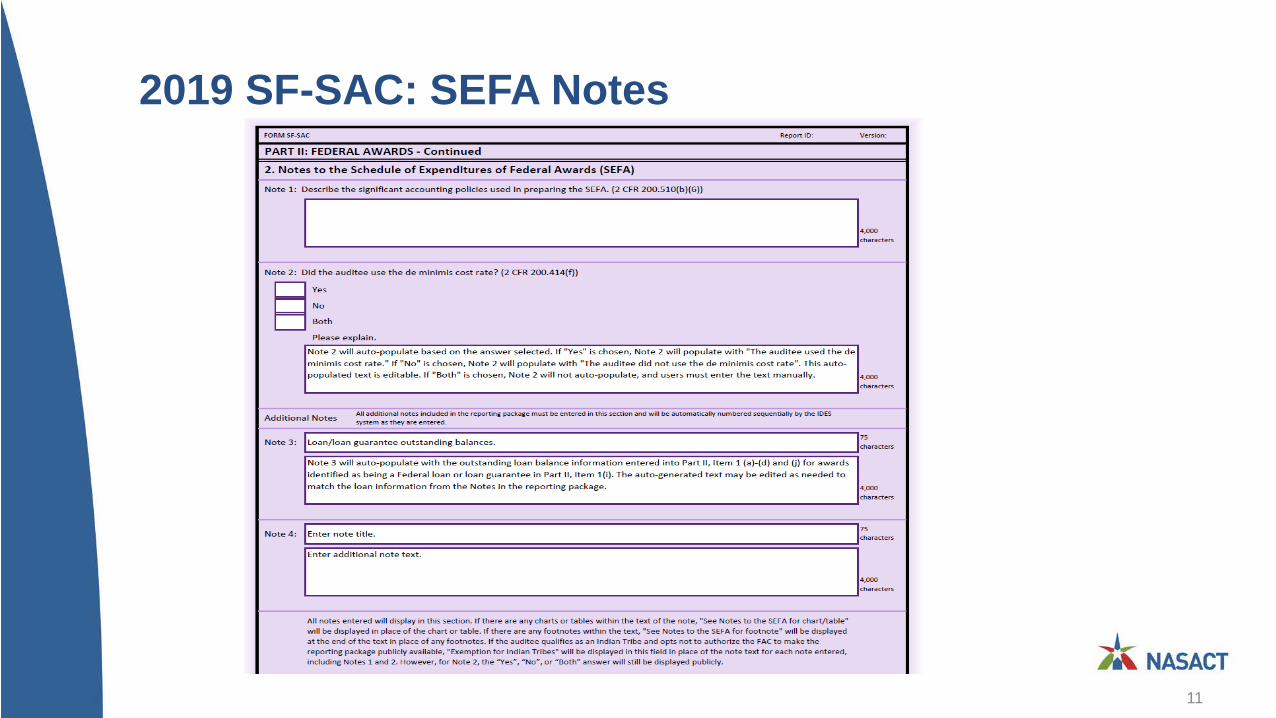

2019 SF-SAC: SEFA Notes

11

2019 SF-SAC (Data Collection Form)• Text of Audit Findings (Part III, item 5)

– Information obtained from Schedule of Findings and Questioned Costs• Audit finding reference numbers from Part III, Item 4(e) will be auto-generated in

Part III, Item 5(a)• For findings related to more than one program, the text must only be entered once

by audit finding reference number• Enter full, detailed text and the auditee’s response(s) excluding any charts or

tables– May copy and paste text from the reporting package

• If there are any charts or tables, enter– See “Schedule of Findings and Questioned Costs for chart/table” in the place of the chart or

table within the text• Similar treatment for any footnotes within the text• Do not enter “See reporting package” for all other text

12

2019 SF-SAC: Audit Findings

13

2019 SF-SAC (Data Collection Form)• Corrective Action Plan (Part IV)

– Information is obtained from the auditee’s CAP• Audit finding reference numbers from Part III, Item 4(e) will be auto-generated in

Part III, Item 5(a)• For findings related to more than one program, the text must only be entered once

by audit finding reference number• Enter full, detailed text of the corrective action plan, including any header

information (such as name of contact person and anticipated completion date) and excluding any charts or tables

– May copy and paste text from the reporting package• If there are any charts or tables, enter

– See “Corrective Action Plan for chart/table” in place of the chart or table within the text• Similar treatment for any footnotes within the text• Do not enter “See reporting package” for all other text

14

2019 SF-SAC: Corrective Action Plan

15

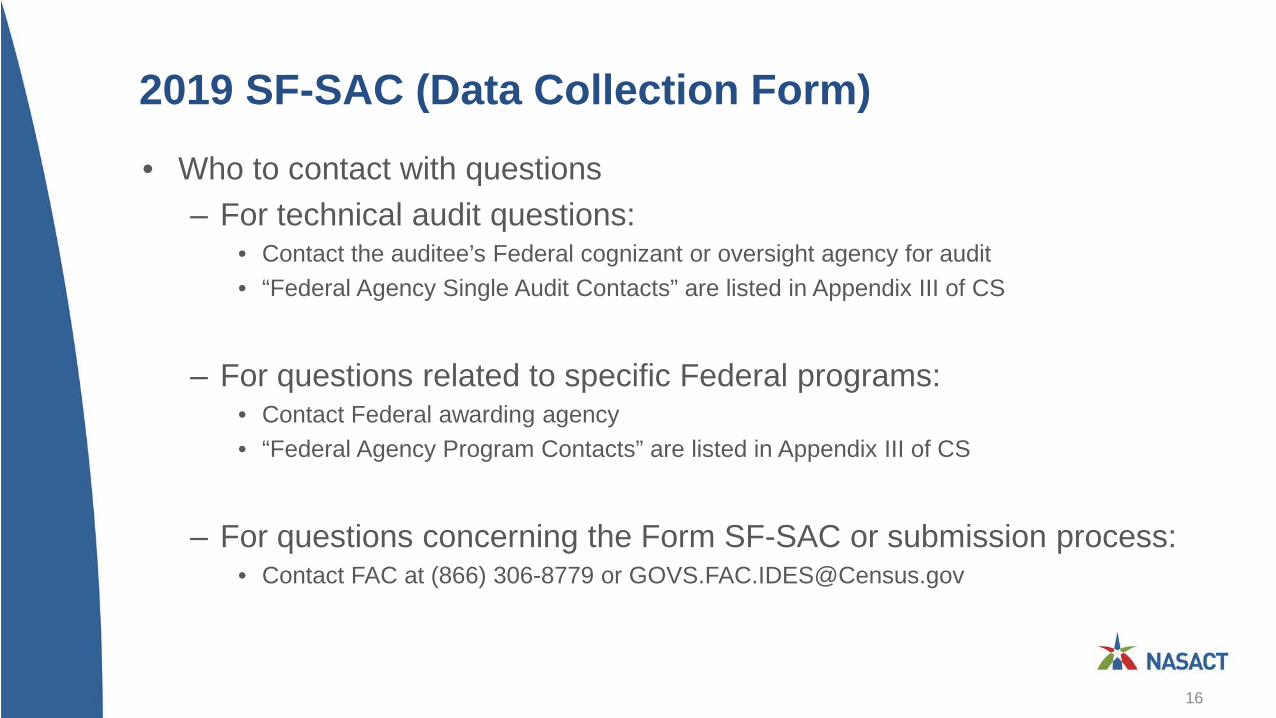

2019 SF-SAC (Data Collection Form)• Who to contact with questions

– For technical audit questions:• Contact the auditee’s Federal cognizant or oversight agency for audit• “Federal Agency Single Audit Contacts” are listed in Appendix III of CS

– For questions related to specific Federal programs:• Contact Federal awarding agency• “Federal Agency Program Contacts” are listed in Appendix III of CS

– For questions concerning the Form SF-SAC or submission process:• Contact FAC at (866) 306-8779 or [email protected]

16

2019 Compliance Supplement• OMB is considering some interesting concepts:

– 20 percent of agency programs are being examined for scrubbing and streamlining

– Compliance review areas limited to 6 compliance areas (“pick six”)• All 12 compliance areas remain applicable• Program specific• Rotate on a year to year basis• Key practice issue

– What is the auditor’s responsibility for a compliance type marked with an “N,” but yet has a direct and material effect on the program?

– Will the auditor still have to test this type of compliance in order to issue an opinion on the program’s compliance?

– Timing:• Vett Draft started in December 2018; last round of programs received April 2019• Final in ??

17

Government Auditing Standards: 2018 Revision

Government Auditing Standards

• 2018 Government Auditing Standards Revision (aka, Yellow Book or GAGAS)

• Exposure Draft was issued on April 5, 2017– 95 comment letters with over 1,700

individual comments received• Final version issued July 17, 2018

– First revision since 2011

19

Summary of Key Changes

• New format and organization • Common terms and definitions• Independence threats related to preparing financial

statements• Updates to independence guidance• Competence of auditors• Guidance for CPE requirements• Competence of specialists• Peer review requirements

20

Summary of Key Changes

• Quality control and monitoring of quality• Internal control: financial audits and examination

engagements• Internal control: performance audits• New considerations for addressing waste• Standards for reviews of financial statements• Criteria for performance audits• Management assertions

21

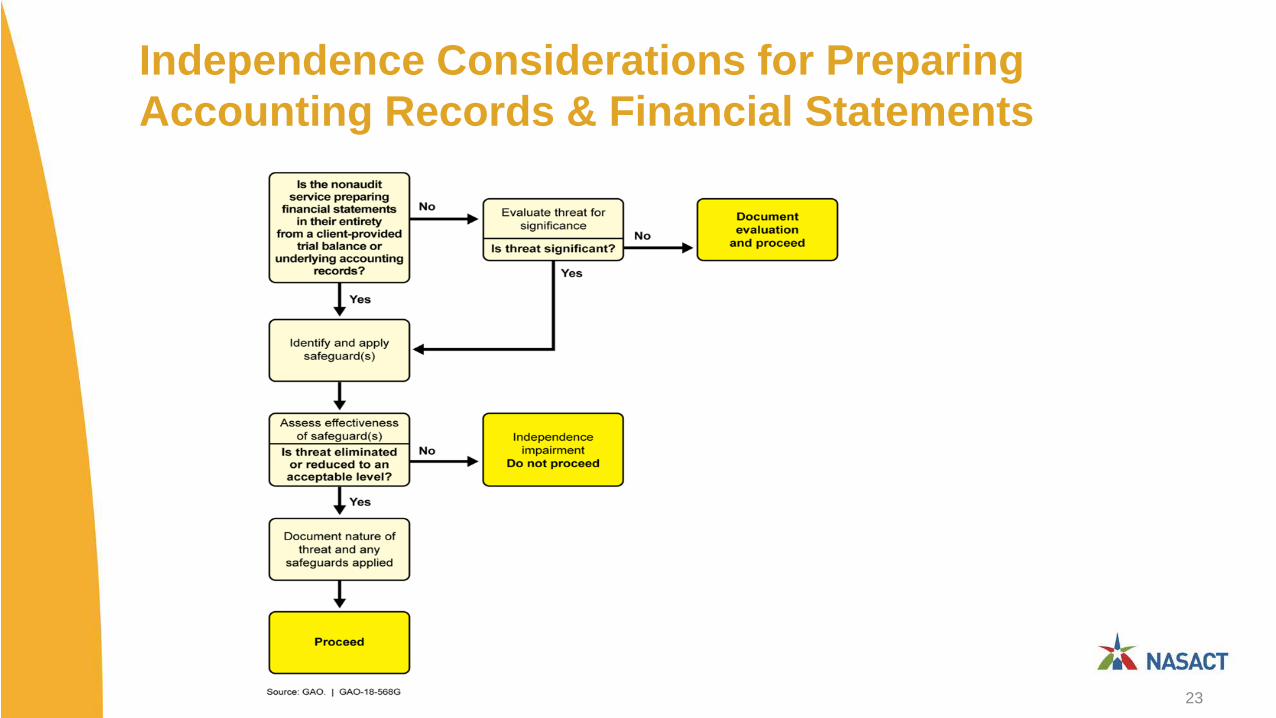

Independence Threats Related to Preparing Financial Statements & Accounting Records

Nonaudit services performed by auditors related to financial statements and accounting records either:

Impair Independence

Are Significant Threats

The auditor prepares financial statements in their entirety (para. 3.88).OR The auditor determines that a service related to preparing financial statements or accounting records is a significant threat (para. 3.93).

Are Threats • Evaluate threat and document evaluation (para. 3.90).• Typing, formatting, printing, binding: not likely significant (para.

3.95)

No change from 2011 Yellow Book (para. 3.87)

Document the threats and safeguards applied to eliminate and reduce threats to an acceptable level (para. 3.33).ORDecline to perform the service (para. 3.88).

22

Independence Considerations for Preparing Accounting Records & Financial Statements

23

Additional Updates to Independence Guidance

• Added application guidance to define management's “Skills, Knowledge and Experience” (SKE) an indicator is management’s ability to recognize a material error (para. 3.79)

• Updated application guidance to clarify that certain services provided by government audit organizations would generally not create threats to independence allowability of certain functions such as investigations (para. 3.72)

24

CPE Requirements and Guidance

• Removed the 4-hour GAGAS Qualification CPE requirement proposed in the exposure draft

• Added application guidance related to obtaining GAGAS specific CPE each time a new Yellow Book revision is issued (para. 4.19)

25

Competence of Specialists• Engagement team should determine whether specialists are qualified

and competent in their areas of specialization (para. 4.12)

• External specialists are not subject to Yellow Book CPE requirements (para. 4.30)

• Internal specialists who are not involved in planning, directing, performing engagement procedures, or reporting are not subject to Yellow Book CPE requirements (para. 4.30)

• IT auditors are considered auditors and thus are subject to the CPE requirements (para. 4.13)

26

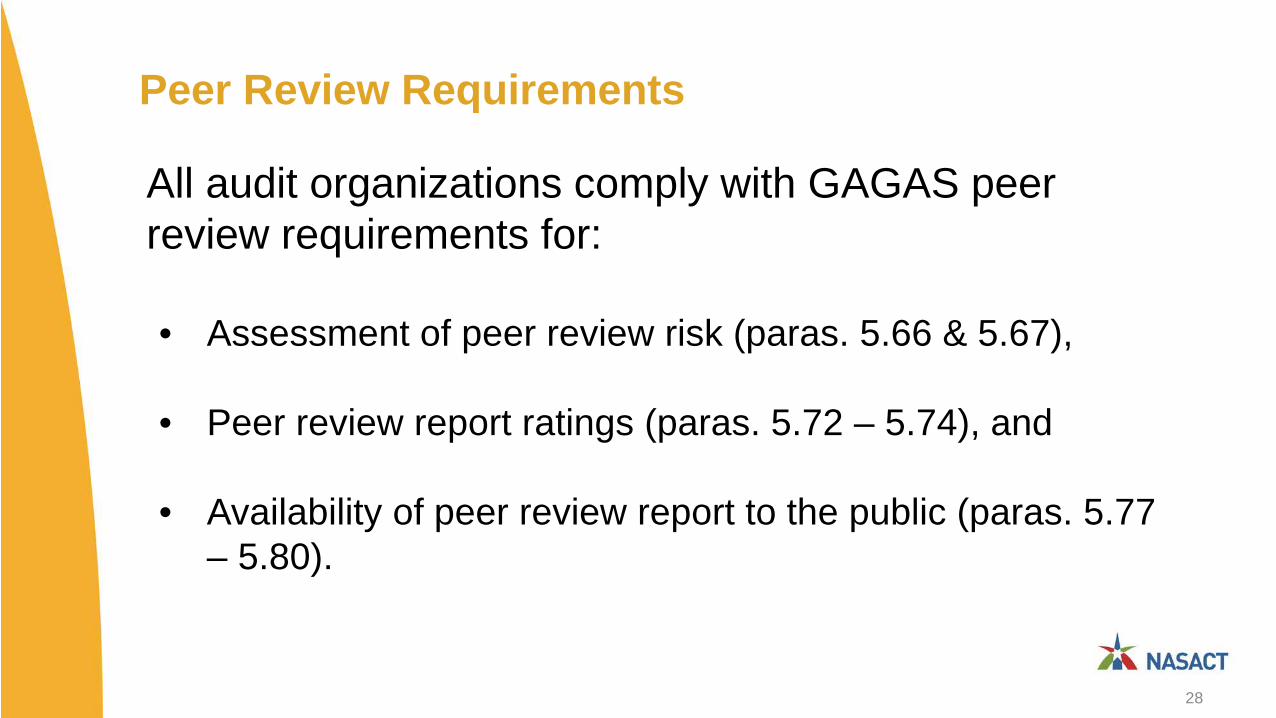

Peer Review Requirements

Peer review section differentiates requirements for those audit organizations affiliated with a recognized organization.

Audit organization affiliated with a

recognized organization?

Yes

No

27

Peer Review Requirements

All audit organizations comply with GAGAS peer review requirements for:

• Assessment of peer review risk (paras. 5.66 & 5.67),

• Peer review report ratings (paras. 5.72 – 5.74), and

• Availability of peer review report to the public (paras. 5.77 – 5.80).

28

Peer Review Requirements: Not Affiliated

Audit organizations not affiliated with a recognized organization also comply with additional GAGAS peer review requirements in areas including:• Peer review scope (para. 5.82) • Peer review intervals (para. 5.84) • Written agreement for peer review (para. 5.86)• Peer review team (para. 5.89) • Report content (para. 5.91) and• Audit organization’s response to the peer review report (paras.

5.93 – 5.94)

29

Waste and Abuse

• Auditor considerations related to waste and abuse are intended to be consistent

• Auditors are not required to perform procedures to detect waste or abuse

• Evaluating internal control in a government environment may include consideration of internal control deficiencies that result in waste or abuse

(paras. 6.20, 7.22, & 8.119)

30

Effective Date

• 2018 Revision is effective for- Financial audits, attestation engagements, and reviews of financial statements for periods ending on or after June 30, 2020, and

- Performance audits beginning on or after July 1, 2019• Early implementation is not permitted

31

Where to Find the Yellow Book

• The Yellow Book is available on GAO’s website at:www.gao.gov/yellowbook

• For technical assistance, contact us at:[email protected] call (202) 512-9535

32

AICPA Current Issues

AICPA – Current Exposure Drafts• Auditor Reporting

– Exposure Draft issued in November 2017• Proposes four new SASs• Also includes proposed amendments Addressing Disclosures in

the Audit of Financial Statements• 297 pages!

– Current Status:• Voted final in January 2019; SAS expected in spring

34

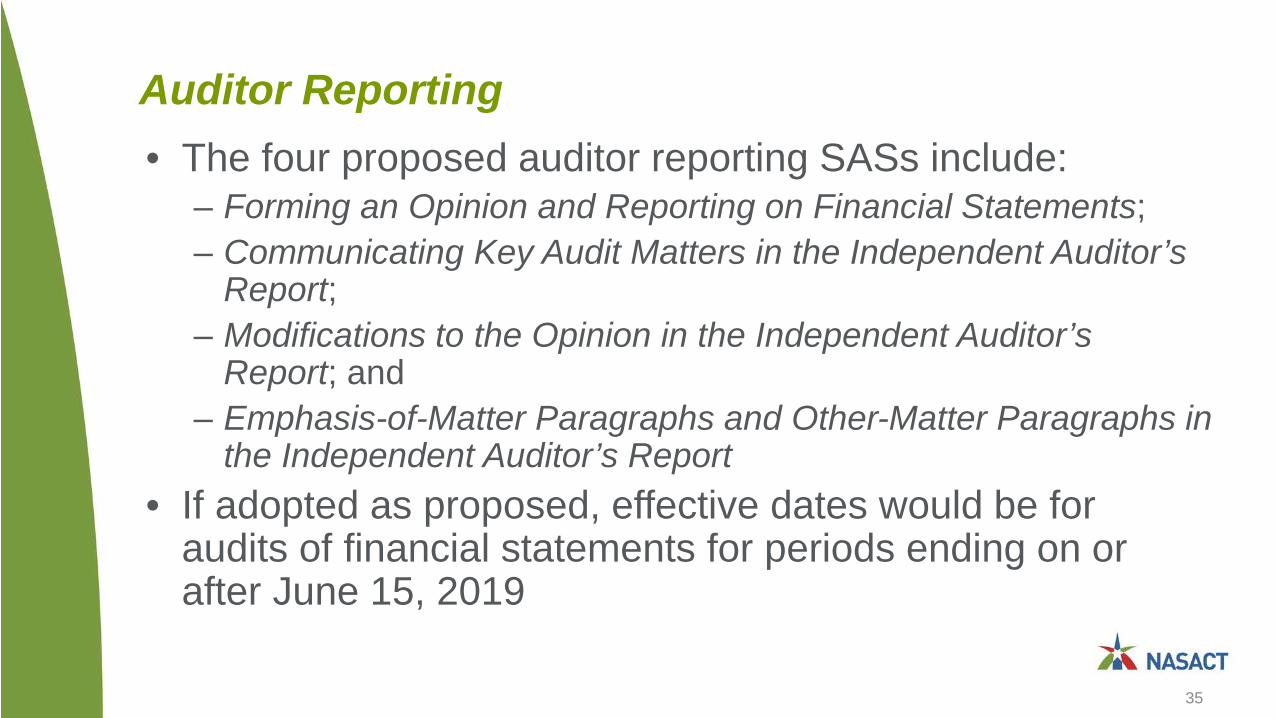

Auditor Reporting • The four proposed auditor reporting SASs include:

– Forming an Opinion and Reporting on Financial Statements;– Communicating Key Audit Matters in the Independent Auditor’s

Report;– Modifications to the Opinion in the Independent Auditor’s

Report; and– Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs in

the Independent Auditor’s Report• If adopted as proposed, effective dates would be for

audits of financial statements for periods ending on or after June 15, 2019

35

Auditor Reporting

• Key changes:– Moving the opinion to the first paragraph– Adding an affirmative statement about the auditor’s

independence and compliance with ethical responsibilities– New Section

• AU-C 701, Communicating Key Audit Matters in the Independent Auditor’s Report

• Required for issuers (of securities); however, might be required by nonissuers if required by law, regulation, or contractual agreement (e.g., included in the terms of the audit engagement)

36

AICPA Professional Ethics Division: State and Local Government Entities

• Exposure Draft issued July 7, 2017– Formerly Entities Included in State and Local

Government Financial Statements (ET sec. 1.224.020)– Addresses a member’s (of the AICPA) independence

with respect to entities that are required to be included in a state or local government’s financial reporting entity

• Exposure Draft issued January 11, 2019– Addresses questions about overall clarity

37

State and Local Government Entities (2017)

• Makes use of terms downstream, upstream and brother-sister entities– Downstream: refers to those entities that are “below” the f/s attest

client in its organization structure• e.g., financial statement attest client is the primary government, funds and component

units to be evaluated are those required to be included in the primary government’s financial reporting entity

– Upstream: refers to those entities that are “above” the f/s attest client• e.g., financial statement attest client is a fund or component unit

– Brother-sister: refers to other funds and component units that the member does not provide attest services to but are included in the same upstream financial reporting entity as the financial statement attest client

38

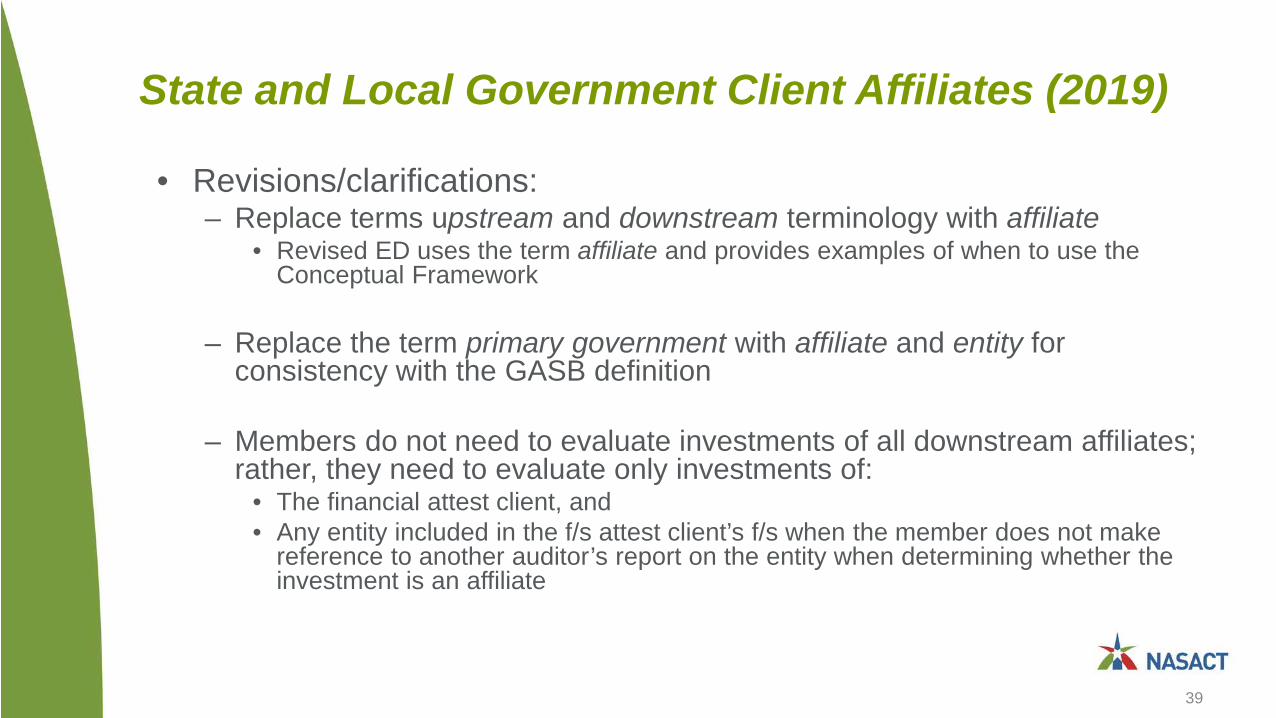

State and Local Government Client Affiliates (2019)

• Revisions/clarifications:– Replace terms upstream and downstream terminology with affiliate

• Revised ED uses the term affiliate and provides examples of when to use the Conceptual Framework

– Replace the term primary government with affiliate and entity for consistency with the GASB definition

– Members do not need to evaluate investments of all downstream affiliates; rather, they need to evaluate only investments of:

• The financial attest client, and• Any entity included in the f/s attest client’s f/s when the member does not make

reference to another auditor’s report on the entity when determining whether the investment is an affiliate

39

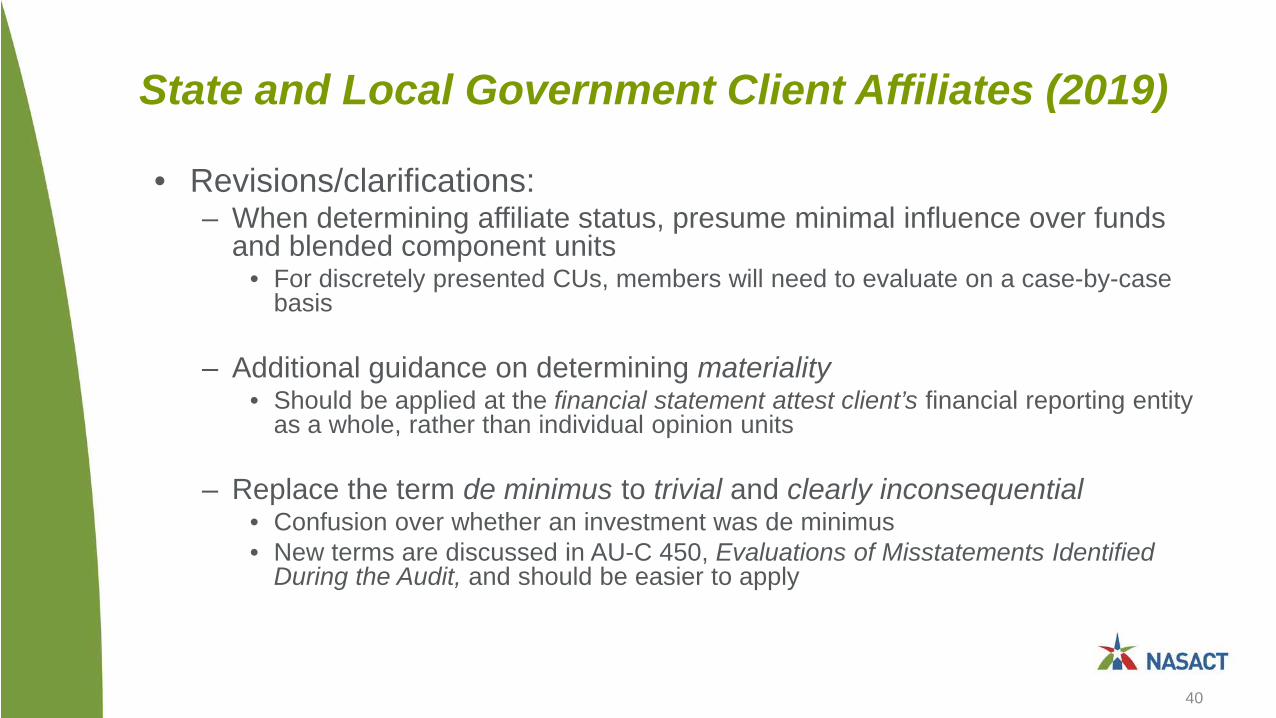

State and Local Government Client Affiliates (2019)

• Revisions/clarifications:– When determining affiliate status, presume minimal influence over funds

and blended component units• For discretely presented CUs, members will need to evaluate on a case-by-case

basis

– Additional guidance on determining materiality• Should be applied at the financial statement attest client’s financial reporting entity

as a whole, rather than individual opinion units

– Replace the term de minimus to trivial and clearly inconsequential• Confusion over whether an investment was de minimus• New terms are discussed in AU-C 450, Evaluations of Misstatements Identified

During the Audit, and should be easier to apply

40

State and Local Government Client Affiliates (2019)

• Effective Date– PEEC recommends the interpretation be effective one year

after adoption• Early implementation allowed

• Current status– PEEC will review in May 2019– AICPA plans to issue a number of educational tools to assist

members with implementation, including:• Flowcharts - affiliate consideration for entities and investments• Practice aid including an electronic checklist (Excel)• FAQs and slides• Courses at conferences

41

Other Emerging Issues

Increasing Transparency: The Continuing Story• FFATA (2006)

– Ongoing monthly reporting of Federal awards and contracts at prime/first-tier sub levels

• DATA (2014)– Amends FFATA– Now fully operational at Federal level

• GREAT (2018)– Proposed legislation to further DATA

43

GREAT Act

• The Grant Reporting Efficiency and Agreements Transparency (GREAT) Act– Continuation of the vision of the DATA Act– Requires data structure (taxonomy) to cover all the data

elements required of recipients of federal funds

44

GREAT Act

• House and Senate bills in 2018 had same requirements:– Establish government-wide data standards for information related to

federal awards reported by recipients of federal awards (within 1 year)

– Issue guidance to grantmaking agencies on how to utilize new technologies and implement new data standards into existing reporting practices with minimum disruption (within 2 years)

– Amends the Single Audit Act to provide for grantee audits to be reported in an electronic format consistent with the data standards (guidance to be issued within 2 years)

45

GREAT Act• Legislative Update

– 2018 (115th Congress)• House (H.R. 4887)

– Passed House on September 26, 2018• Senate (S. 3484)

– Homeland Security & Government Affairs Committee passed on September 26, 2018

– Did not move to full Senate vote– 2019 (116th Congress)

• House (H.R. 150)– Passed unanimously on January 17, 2019

• Senate– Still waiting for companion bill

46

Questions or Comments?R. Kinney Poynter, [email protected](859) 276-1147

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

The views expressed in this presentation are those ofOfficial positions of the GASB are reached only after extensive due process and deliberations.

GASB UpdateMay 20, 2019David A. Vaudt, GASB Chairman

113th Annual Conference

Mr. Vaudt.

Current Technical Agenda Projects

49

Financial Reporting Model Reexamination

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Preliminary Views:Financial Reporting Model Improvements

50

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

What:

•The Board proposed improvements to the financial reporting model―Statements 34, 35, 37, 41, and 46, and Interpretation 6

Why:

•A review of those standards found that they generally were effective, but that there were aspects that could be significantly improved

When:

•Comment deadline was February 15, 2019

Preliminary Views:Financial Reporting Model Improvements

51

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Lack of conceptual consistency in recognition of assets and liabilities

Lack of conceptual foundation from which to develop standards for complex transactions

Some consider it ineffective in conveying that the information is related to fiscal accountability (rather than operational accountability)

• Focuses on financial resources rather than on economic resources• Shorter time perspective than information in government-wide financial

statements

Lack of consistency in short-term perspective

Concerns with Existing Reporting of Governmental Funds

52

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Pre-Agenda Research Started April 2013

Added to Current Technical Agenda September 2015

Invitation to Comment Issued December 2016

Preliminary Views Issued September 2018

Public Hearings March 5, 12 & 14, 2019

User Forums March 6 & 14, 2019

Redeliberations Begin June 2019

Exposure Draft Expected June 2020

Project Timeline

53

Revenue and Expense Recognition

54

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

What:

•The Board is redeliberating stakeholder input on an Invitation to Comment as part of developing a comprehensive model for recognition of revenues and expenses

Why:

•Guidance for exchange transactions is limited; guidance for nonexchange transactions could be improved and clarified

When:

•Redeliberations began in June 2018

Revenue and Expense Recognition

55

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

The project scope broadly encompasses revenue and expense recognition but excludes the following:

Project Scope

56

Topics with guidance developed considering the current conceptual framework

Topics related to financial instruments

Topics related to transactions arising from recognition of capital assets or certain liabilities

For example, pensions and other post-employment benefits

For example, investments, derivatives, leases, and insurance

For example, depreciation, asset retirement obligations, and pollution remediation obligations

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Classification is the process of identifying the type of transaction

(for example, is the transaction exchange

or nonexchange?)

Recognition is the process of determining what element should be reported and when (for

example, recognize revenue when earned)

Measurement is the process of determining the amount to report for

the element (not addressed in the

Invitation to Comment)

Revenue and Expense Recognition Models

57

The are three components of a revenue and expense recognition model

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Exchange/Nonexchange Model

58

Classification

Recognition

Measurement

Is the transaction an exchange?

Measurement was not addressed in the Invitation to Comment but is expected to be addressed in a later due process document.

Earnings recognition approach:

• Government controls a resource, or incurs an obligation to sacrifice a resource,

and• The change in net assets is not

applicable to a future period

Provisions of Statement 33:

• Derived tax revenue• Imposed nonexchange revenue• Government-mandated

nonexchange transaction• Voluntary nonexchange

transaction

YES NO

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

A performance obligation is a promise in a binding arrangement between a government and another party to provide distinctgoods or services to a specific beneficiary.

Performance Obligation Definition

59

A binding arrangement is a

legally enforceable mutual

understanding between a

government and another party.

Another party can be a customer, a

vendor, a resource provider, an

employee, and so on.

Distinct goods or services are separately

identifiable and can provide

benefits on their own.

A specific beneficiary would be identifiable and distinguished from the general public.

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Performance Obligation/No Performance Obligation Model

60

Classification

Recognition

Measurement

Does the transaction contain a performance obligation?

Measurement is not addressed in the Invitation to Comment but is expected to be addressed in a later due process document.

Performance recognition approach:

• Determine consideration• Allocate consideration to performance

obligation(s)• Recognize revenue or expense as each

performance obligation is satisfied (at a point in time or over time) and the transaction is applicable to the reporting period(s)

Provisions of Statement 33:

• Derived tax revenue• Imposed nonexchange revenue• Government-mandated

nonexchange transaction• Voluntary nonexchange

transaction

YES NO

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

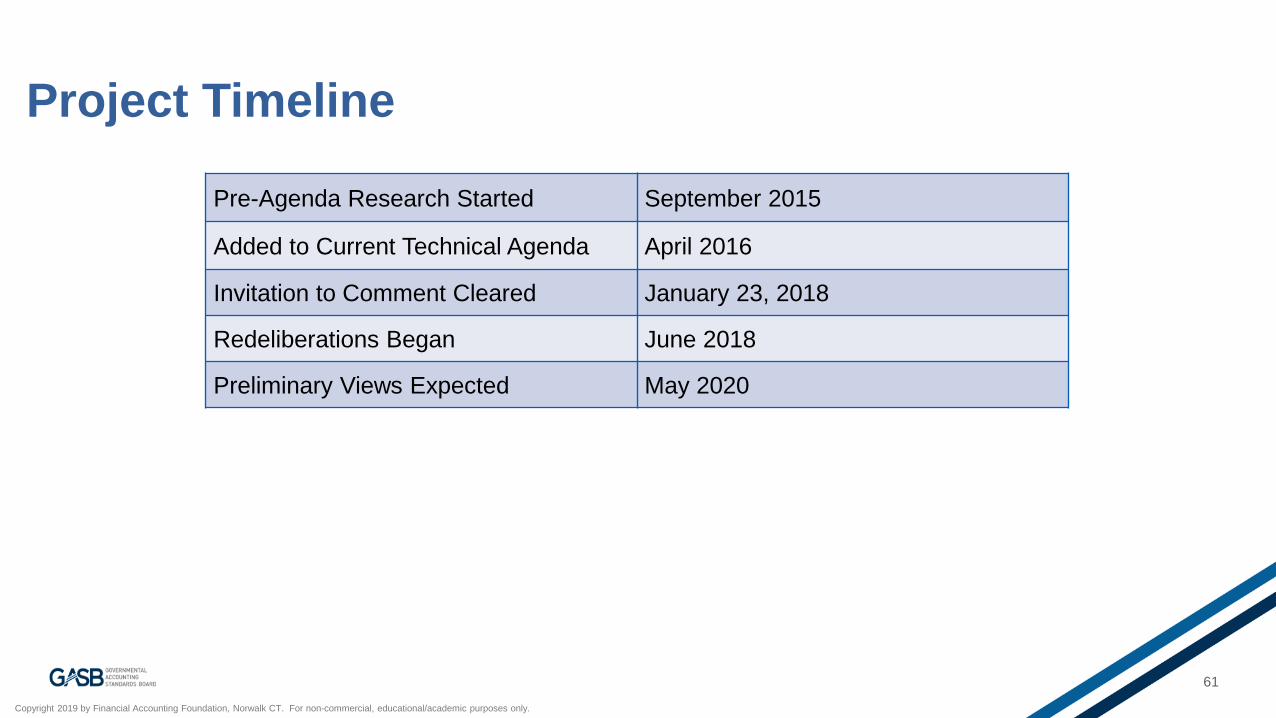

Pre-Agenda Research Started September 2015

Added to Current Technical Agenda April 2016

Invitation to Comment Cleared January 23, 2018

Redeliberations Began June 2018

Preliminary Views Expected May 2020

Project Timeline

61

Deferred Compensation Plans: Reexamination of Statement 32

62

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

What:

•The GASB has added a project to consider improvements to Statement 32 on IRC Section 457 plans

Why:

•Statement 32 became effective in 1999 and the relevant portions of the IRC have changed significantly since then

When:

•Deliberations began in April 2019

Deferred Compensation Plans

63

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

What standards should be applied to Section 457 plans that meet the definition of a pension plan – Statement 32, as amended, or the pension standards (Statements 67, 68, and 73, as amended)?

Key Issue to Be Considered

64

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

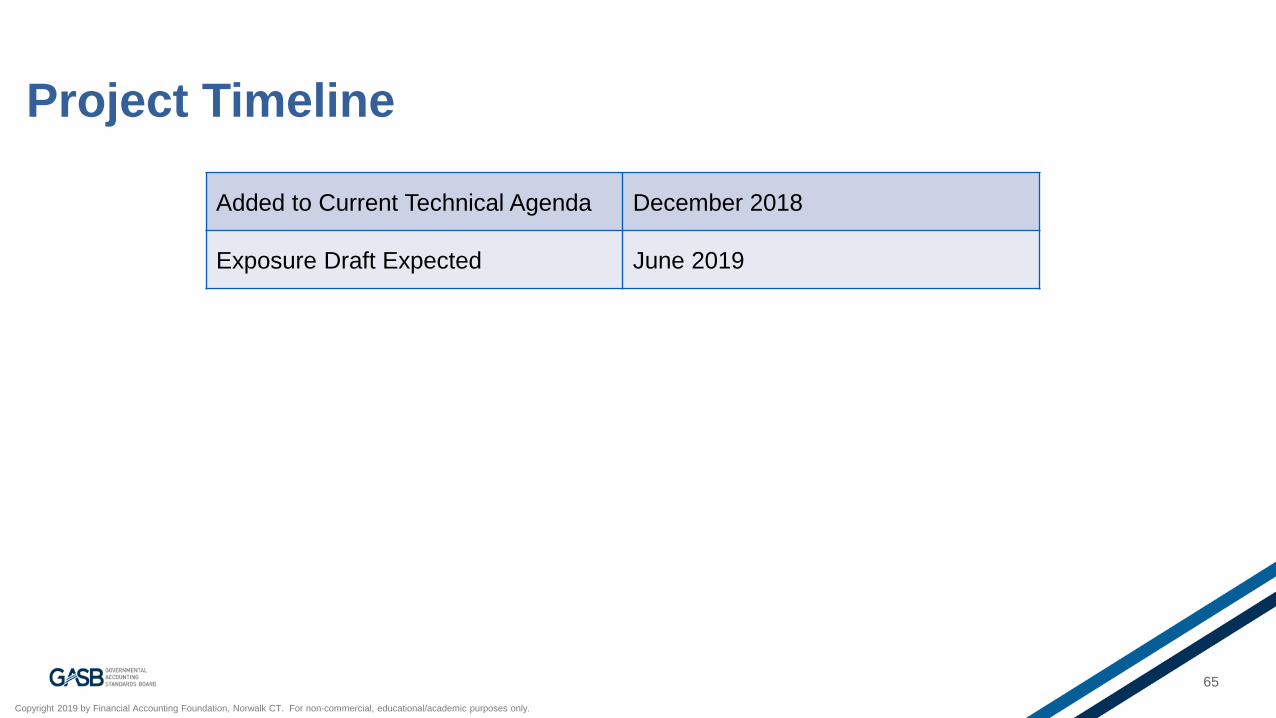

Added to Current Technical Agenda December 2018

Exposure Draft Expected June 2019

Project Timeline

65

Omnibus

66

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

What:

•The Board added an Omnibus project in December 2018

Why:

•Omnibus projects are used to address issues in multiple pronouncements that, individually, would not justify a separate project

When:

•An Exposure Draft is expected to be considered in June 2019

Omnibus Project

67

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Effective Date of Statement 87: Should the effective date of Statement 87 be changed from reporting periods beginning after December 15, 2019, to fiscal years beginning after that date?

•Definition of Collections: Should the definition in Statement 34 of “collections” be amended to reflect the updates introduced by the American Alliance of Museums?

•Intra-Entity Transfers of Assets: Should the guidance in Statement 48 be clarified to address how the transfer of assets reported by the primary government at historical cost be reflected in the financial statements?

•Certain Effects of Statement 84: Should the term “control” introduced by the Statement be replaced in instances when the guidance could be applied to the assessment of certain potential fiduciary component units associated with pensions and OPEB?

Topics to Be Considered

68

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

•Available to Be Issued: Should the concept of a financial report being “available to be issued” be introduced in determining subsequent events?

•Exceptions to Acquisition Value: Should Statement 69 be amended to exclude the use of acquisition value for measuring asset retirement obligations?

•Technical Correction to Statement 72: Should Statement 72 be amended to correct a misidentified paragraph reference to Statement 62, as amended?

•Reinsurance Recoveries: Should inconsistencies in how the insurance accounting standards refer to a netting provision for recoveries from reinsurers and excess insurers be resolved?

Topics to Be Considered (continued)

69

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Added to Current Technical Agenda December 2018

Deliberations Began January 2019

Exposure Draft Expected June 2019

Project Timeline

70

Secured Overnight Financing Rate – London Interbank Offered Rate Replacement

71

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

What:

•The Board added a project to consider amending existing standards that reference LIBOR

Why:

•LIBOR – which is included as a reference rate in billions of dollars of financial instruments, including derivatives –effectively sunsets in 2021

When:

•Deliberations began in April 2019

SOFR – LIBOR Replacement

72

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

How should the replacement of LIBOR be addressed: (1) by replacing existing citations of LIBOR with SOFR or other new reference rates or (2) by describing the characteristics of an acceptable reference rate?

•If the latter, what are the characteristics of an acceptable reference rate?

•Do the circumstances related to the revision or replacement of derivative instruments in response to the end of LIBOR merit an exception to the hedge accounting termination provision of Statement 53, similar to exception in Statement 64?

Topics to Be Considered

73

Copyright 2019 by Financial Accounting Foundation, Norwalk CT. For non-commercial, educational/academic purposes only.

Added to Current Technical Agenda December 2018

Exposure Draft Expected August 2019

Project Timeline

74

Questions?

Visit www.gasb.org

75

III. ACCOUNTING YEAR IN REVIEW

76

AGENDAA. Overview of Upcoming ImplementationsB. New Pronouncements

Three new statements One new implementation guide

C. Exposure DraftsTwo new implementation guide EDsOne new statement ED

D. Review of Selected Guidance Becoming Effective in Fiscal Year 2019 [time permitting]

77

WHEN DOES MY GOVERNMENT NEED TO IMPLEMENT …?New Statements Implement for Fiscal Years Ending*

Statement #

Effective forPeriods Beginning After

March 31st June 30th September 30th

& October 31stDecember 31st

GASB 83 6/15/2018 2020 2019 2019 2019

GASB 84 12/15/2018 2020 2020 2020 2019

GASB 87 12/15/2019 2021 2021 2021 2020

GASB 88 6/15/2018 2020 2019 2019 2019

GASB 89 12/15/2019 2021 2021 2021 2020

GASB 90 12/15/2018 2020 2020 2020 2019

GASB 91 12/15/2020 2022 2022 2022 2021

78

* Early implementation is encouraged for all of these statements. For interim reporting, standards are effective for interim periods of the first FYE (Omnibus may change this for GASB 89).

WHEN DOES MY GOVERNMENT NEED TO IMPLEMENT …?

New Implementation Guidance Implement for Fiscal Years Ending*Guide Effective For

Periods Beginning After

March 31st June 30th September 30th

& October 31stDecember

31st

2018-1 CIG Update

6/15/2018 2020 2019 2019 2019

2019-1 CIG Update

6/15/2019 2021 2020 2020 2020

2019-2 FiduciaryActivities **

12/15/2018 2020 2020 2020 2019

2019-3 Leases ** 12/15/2019 2021 2021 2021 2020

79

* Early implementation is encouraged if related statements have been implemented. For interim reporting, guidance is effective for interim periods of the first FYE** Expected to be issued in June, 2019

PART B: NEW PRONOUNCEMENTS

1. GASB Statement No. 89, Accounting for Interest Cost Incurred before the End of a Construction Period

2. GASB Statement No. 90, Majority Equity Interests – an amendment of GASB Statements No. 14 and No. 61

3. GASB Statement No. 91, Conduit Debt 4. GASB Implementation Guide No. 2019-1, Implementation

Guidance Update – 2019

80

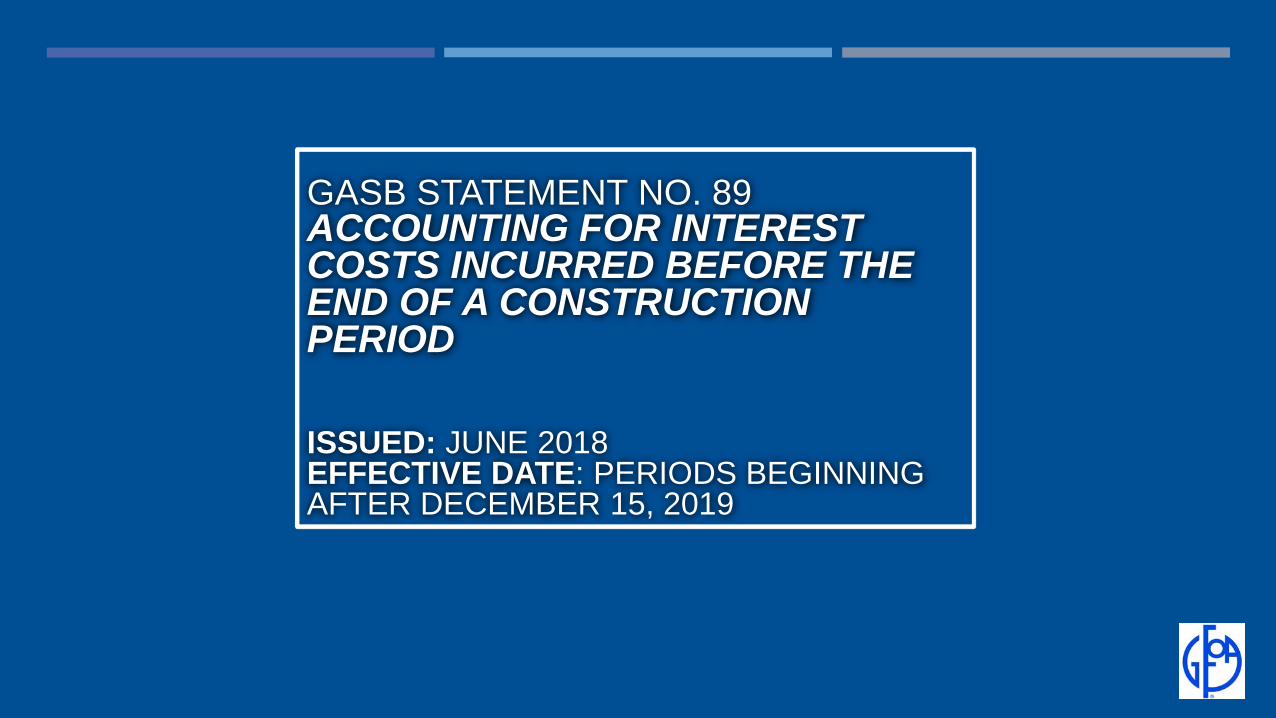

GASB STATEMENT NO. 89 ACCOUNTING FOR INTEREST COSTS INCURRED BEFORE THE END OF A CONSTRUCTION PERIOD

ISSUED: JUNE 2018EFFECTIVE DATE: PERIODS BEGINNING AFTER DECEMBER 15, 2019

82

INTEREST INCURRED ON CAPITAL PROJECTS

Capitalizing interest in BTAs

83

Economic Resources Measurement Focus –Interest is an expense in the period incurred

Current Financial Resources Measurement Focus – Interest is an expenditure when due and payable

IMPLEMENTATIONEffective - periods beginning after December

15, 2019Early implementation is encouragedProspective from beginning of period

implemented• No need to back-out previously capitalized

interest84

GASB STATEMENT NO. 90 ACCOUNTING AND FINANCIAL REPORTING FOR MAJORITY EQUITY INTERESTS

ISSUED: AUGUST 2018EFFECTIVE DATE: PERIODS BEGINNING AFTER DECEMBER 15, 2018

GASB 90 - EQUITY INTEREST

A financial interest in a legally separate organization represented by shares of stock or otherwise having an explicit, measurable right to net resources of an organization, usually based on an investment* of financial or capital resources by a government

86* As in a contribution or exchange, not an investment per in GASB 72/Cod. Sec. I50.

EQUITY INTEREST (CONT.)A government has an explicit, measurable

right to net resources of an entity if the• Government has a present or future claim to net

resources, and• Government’s share is determinable

Excludes residual interests in assets that may revert to a government upon dissolution of an entity

87

Government’s Share > 50% = MEI

88

OVERVIEW

MEI INVESTMENT DETERMINATIONAn investment asset is one that

• A government holds primarily for income or profit, and

• Has a present service capacity based solely on ability to generate or be sold for cash

[Cod Sec I50, Investments/GASB 72]89

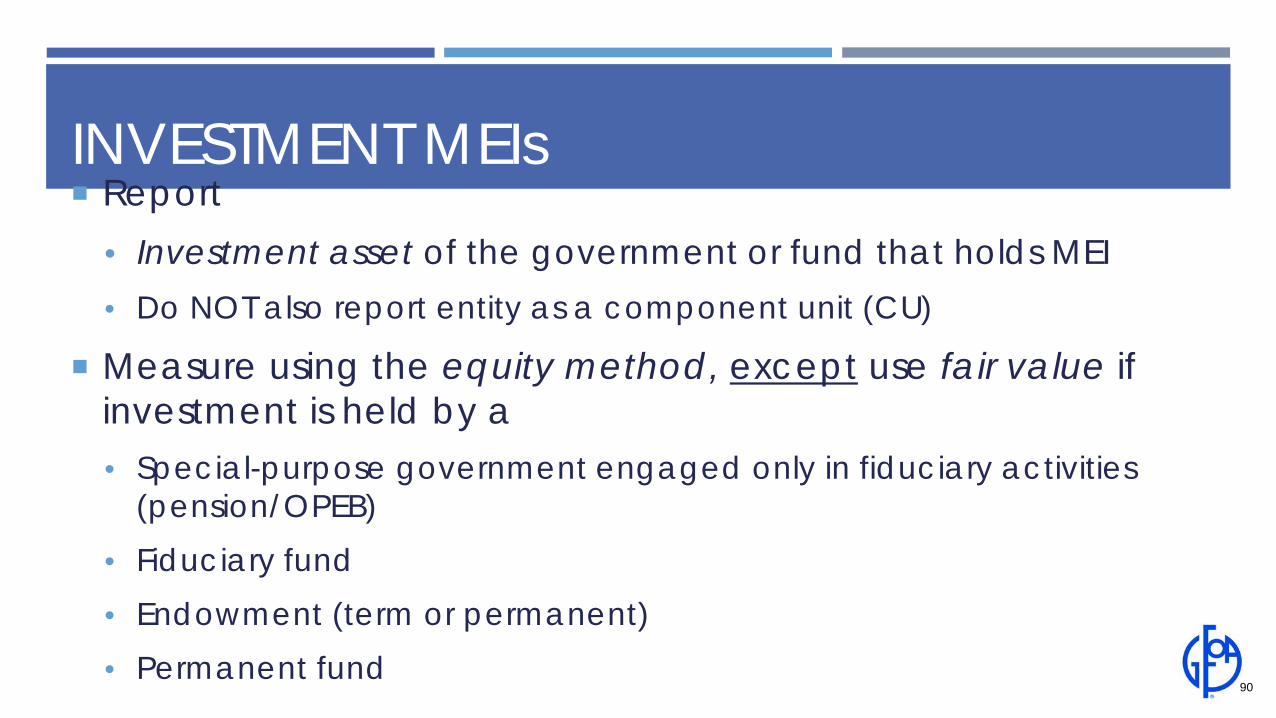

INVESTMENT MEIs Report

• Investment asset of the government or fund that holds MEI• Do NOT also report entity as a component unit (CU)

Measure using the equity method, except use fair value if investment is held by a• Special-purpose government engaged only in fiduciary activities

(pension/OPEB)• Fiduciary fund• Endowment (term or permanent)• Permanent fund

90

NON-INVESTMENT MEIs Report• Non-investment asset of the government or fund that

holds MEI (e.g. equity in utility company)• A CU because non-investment MEI = financial

accountabilityo If blended CU, eliminate asset and CU net position

Measure – If MEI < 100%• Economic Resources – Equity method• Current Financial Resources – Report only current financial

resources (payables & receivables between government d th CU)

91

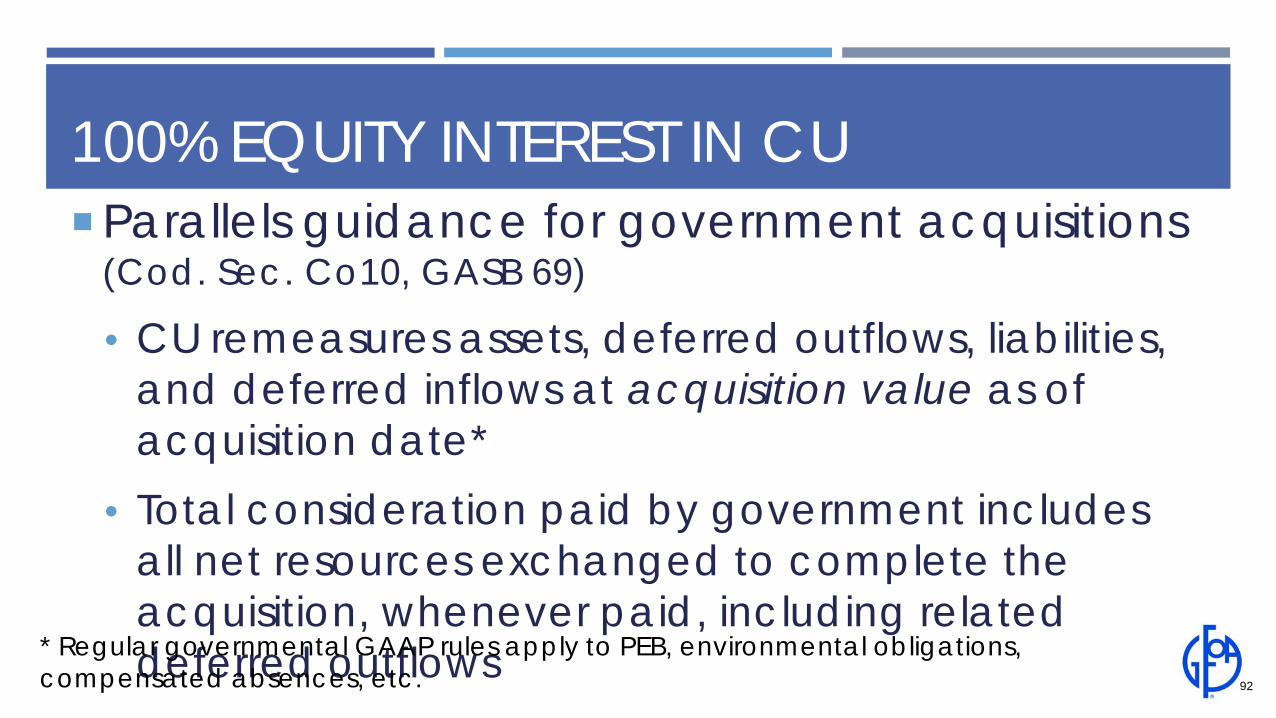

100% EQUITY INTEREST IN CUParallels guidance for government acquisitions

(Cod. Sec. Co10, GASB 69)

• CU remeasures assets, deferred outflows, liabilities, and deferred inflows at acquisition value as of acquisition date*

• Total consideration paid by government includes all net resources exchanged to complete the acquisition, whenever paid, including related deferred outflows

92

* Regular governmental GAAP rules apply to PEB, environmental obligations, compensated absences, etc.

100% EQUITY INTEREST IN CU (CONT.)

Net position acquired by government = net position of CU after re-measurement

And…CU’s flows statement includes only post-

acquisition activity

93

IMPLEMENTATION Effective - periods beginning after December 15,

2018 Early implementation is encouraged Retroactive implementation - restatement of

beginning net position of First period presented, or Earliest period restated and explain reason for not

restating earlier period(s)

94

GASB STATEMENT NO. 91 CONDUIT DEBT OBLIGATIONS

ISSUED: MAY 2019EFFECTIVE DATE: PERIODS BEGINNING AFTER DECEMBER 15, 2020

96

Conduit Debt Issuer Commitment

s

Associated Arrangement

s

CONDUIT DEBT

A debt instrument issued in the name of a state or local government (the “issuer”) that is for the benefit of a third party that is primarily liable for the repayment of the debt instrument (the “third-party obligor”).

97

CONDUIT DEBT CRITERIATo be conduit debt, all five criteria must be met:1. At least 3 parties

a) Issuerb) Third-party obligor (obligor)*c) Debt holder or trustee*

2. Issuer and obligor not part of same reporting entity

98

* There may be more than one of these

CONDUIT DEBT CRITERIA (CONT.)Conduit debt criteria (cont.):3. Debt not a parity bond or cross collateralized

with other debt of issuer4. The obligor (or its agent) – not the issuer –

ultimately receives the proceeds of the debt5. The obligor – not the issuer – is primarily

obligated for the payment of all debt service99

ISSUERS’ COMMITMENTSLimited[All issuers]

• Maintain Tax-exempt Status, and

• Use Obligor-provided Resources (if any) for Debt Service

• May also facilitate payments from Obligor to Debt Holders/Bond Trustees

Additional[Some issuers]

• Moral Obligation Pledge

• Appropriation Pledge

• Financial Guarantee*

• Pledging own revenue or assets

Voluntary[Some issuers]

• Voluntarily requests an appropriation for a debt service payment

• Voluntarily makes a debt service payment

Commitments to support debt if obligor is or will be unable

Decides to support debt - without having an obligation to do so - if obligor is or will be unable * Issuer should provide conduit debt disclosures not nonexchange financial guarantee

ISSUER LIABILITY RECOGNITION

Conduit Debt – Do Not Recognize Liability to Support Debt Service Payment –

Recognize when it is more likely than not (likelihood > 50%) that the issuer will support one or more debt service payments for conduit debt

101

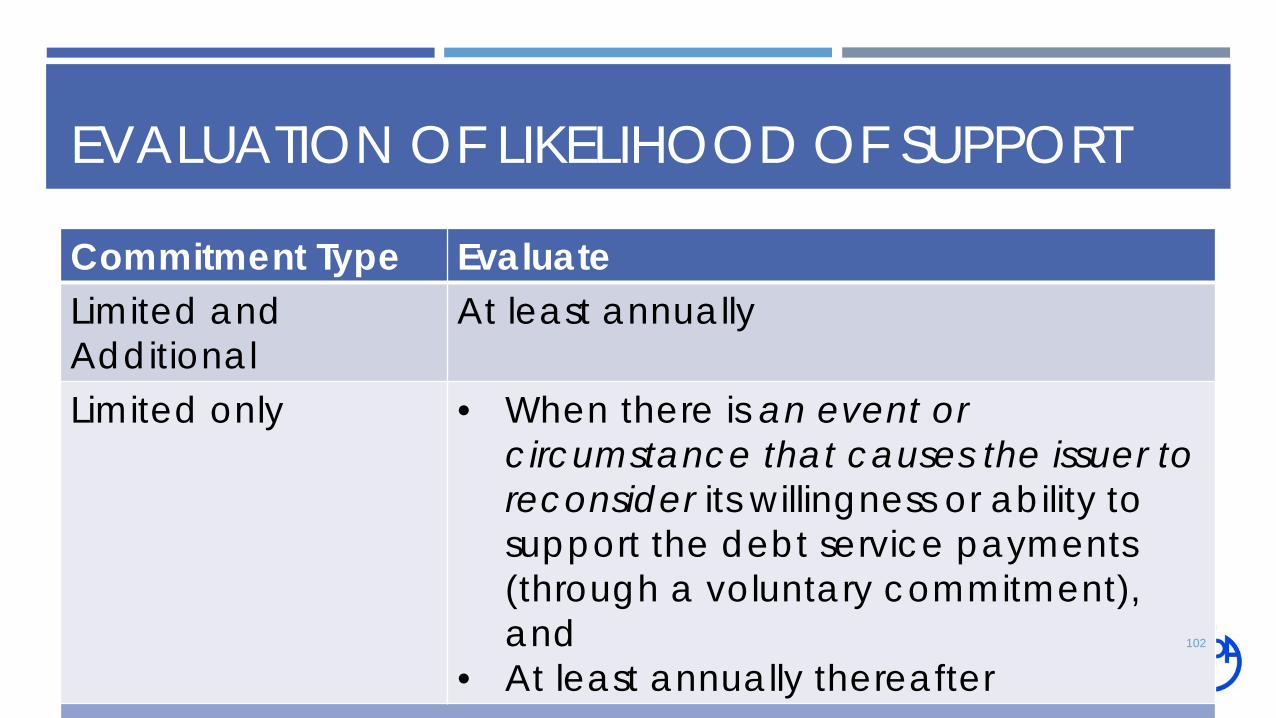

EVALUATION OF LIKELIHOOD OF SUPPORT

Commitment Type EvaluateLimited and Additional

At least annually

Limited only • When there is an event or circumstance that causes the issuer to reconsider its willingness or ability to support the debt service payments (through a voluntary commitment), and

• At least annually thereafterl t i Q lit ti t ( l t lid )

102

QUALITATIVE FACTORS - OBLIGOR

If Obligor:• Initiates process of bankruptcy or financial

reorganization• Breaches a debt-contract provision related to

conduit debt (rate covenants, coverage ratios, default or delinquency in payments)

• Experiences significant financial difficulty (laundry list of examples in statement)

103

QUALITATIVE FACTORS – PROJECT

If Project that is expected to provide funding for debt service is:• Terminated• The subject of litigation that would negatively affect

project

104

QUALITATIVE FACTORS – ISSUER

If Issuer has: • Concern that default on conduit debt would affect

its one access to capital • History of fulfilling additional commitments

(including voluntary support)• Ability or willingness to support debt service

105

LIABILITY TO SUPPORT DEBT SERVICE –ECONOMIC RESOURCES MFIssuer recognizes a liability and a related expense if it is More likely than not that issuer will support debt

serviceMeasure liability –

Discounted PV of best estimate of future payments to support debt • If no best estimate, discounted PV of the

minimum of a range of estimates 106

LIABILITY TO SUPPORT DEBT SERVICE –CURRENT FINANCIAL RESOURCES MFIssuer recognizes a governmental fund liability to support debt service payments and a related expenditure if it is both:More likely than not that issuer will need to

support debt service, and Debt service payment is due and payable

107

ASSOCIATED ARRANGEMENTSCommonly referred to as “leases” but excluded

from GASB’s lease accounting standardAttributes (must have all):

• Construction/acquisition of the capital asset financed by the conduit debt

• Issuer retains title to the capital asset from inception• Payments from obligor cover conduit debt service• Payment schedule coincides with conduit debt service

108

ACCOUNTING FOR ASSOCIATED ARRANGEMENTS If meet definition of a Service Concession

Arrangement, follow that guidance (Cod Sec S30 / GASB 60)

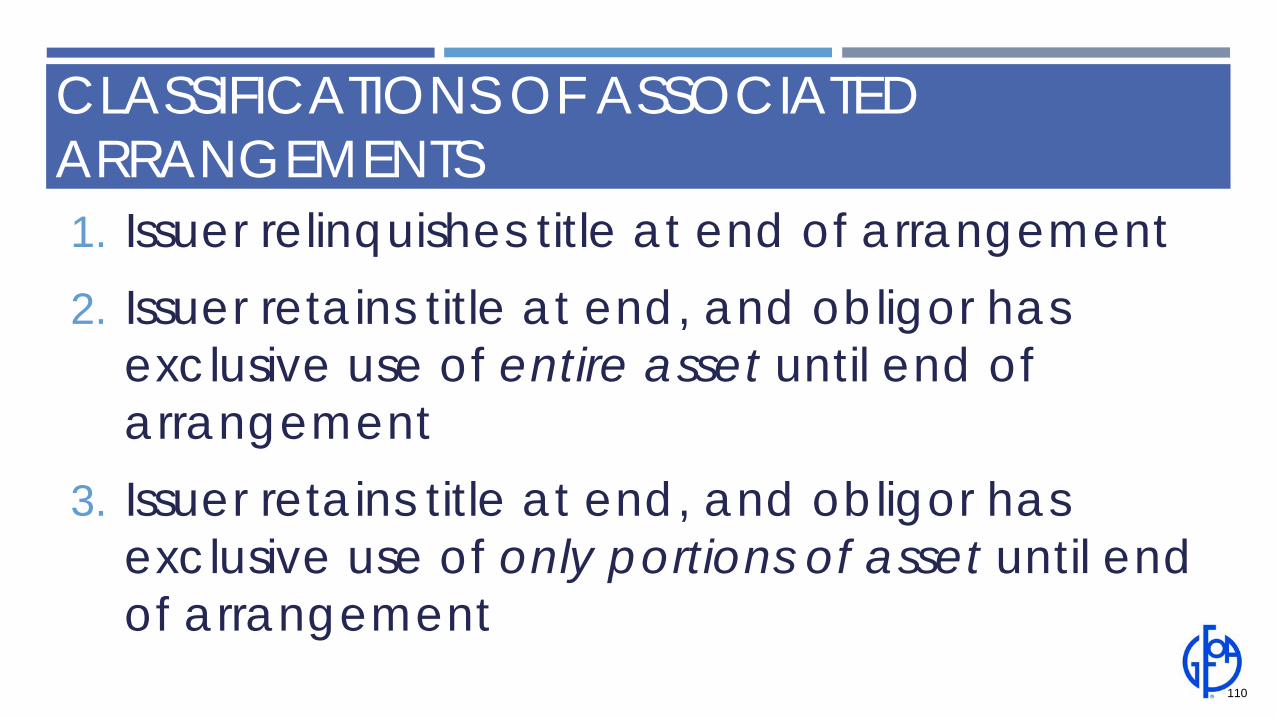

Otherwise, accounting different for each of three (3) classifications of associated arrangements, depending on:• Whether issuer relinquishes title to asset at end of

arrangement• Whether obligor has exclusive use of all or only a

portion of the capital asset during term of arrangement 109

CLASSIFICATIONS OF ASSOCIATED ARRANGEMENTS1. Issuer relinquishes title at end of arrangement2. Issuer retains title at end, and obligor has

exclusive use of entire asset until end of arrangement

3. Issuer retains title at end, and obligor has exclusive use of only portions of asset until end of arrangement

110

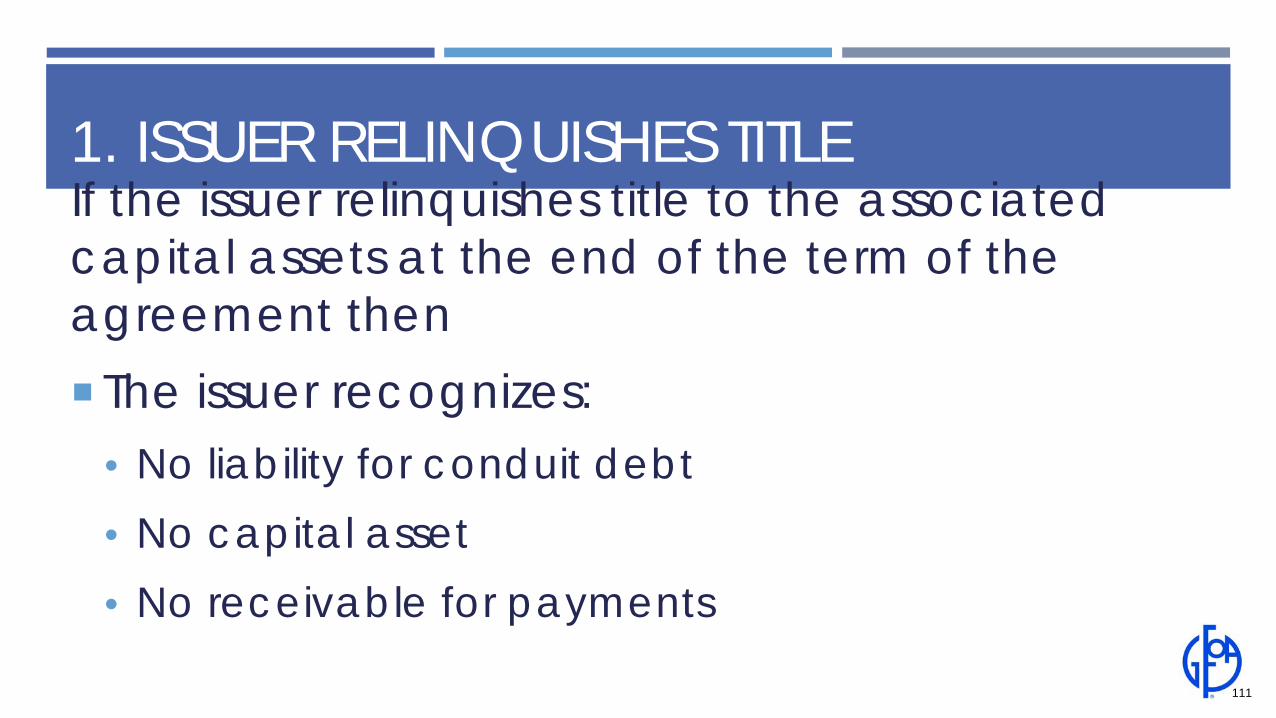

1. ISSUER RELINQUISHES TITLEIf the issuer relinquishes title to the associated capital assets at the end of the term of the agreement then The issuer recognizes:

• No liability for conduit debt• No capital asset• No receivable for payments

111

2. ISSUER RETAINS TITLE & OBLIGOR HAS USE OF ENTIRE ASSETIf issuer does not relinquish title at end and obligor has exclusive use of the entire capital asset during the term then: At inception of associated arrangement, issuer recognizes:

• No liability for conduit debt

• No receivable for payments

• No capital asset

At end of associated arrangement, issuer recognizes• Capital asset at acquisition value and an inflow of resources (revenue) in

same amount112

3. ISSUER RETAINS TITLE & OBLIGOR HAS USE OF PORTIONS OF ASSETIf issuer does not relinquish title at end and obligor has exclusive use of only portion(s) of capital asset during the term then:

At inception of associated arrangement, issuer recognizes: No liability for conduit debt No receivable for payments The entire capital asset at acquisition value, and a deferred inflow of

resources for same amount

Over the life of the associated arrangement, issuer recognizes Reduction of deferred inflow and an inflow of resources (revenue) in

a systematic and rational manner113

NOTE DISCLOSURES – ALL ISSUERS General descriptions of the issuer’s:

• Conduit debt obligations• Limited commitment(s)• Voluntary commitment(s)• Additional commitments, if any, including:o Legal authority and limits for extending the commitment(s)o Length of time of commitment(s)o Arrangements for recovering payments from obligors, if any

• Aggregate outstanding principal of all conduit debt obligations with the same type of commitments (limited commitments only, additional commitments by type, voluntary commitments by type) 114

NOTE DISCLOSURES – ISSUERS REPORTING LIABILITIES TO SUPPORT DEBT SERVICE Brief description of timing of recognition and measurement

of liability, including:

Cumulative amount of payments made on recognized liability, if any

Amounts expected to be recovered, if any115

NOTE: An issuer that makes a financial guarantee as an additional commitment should provide conduit debt – not nonexchange financial guarantee disclosures

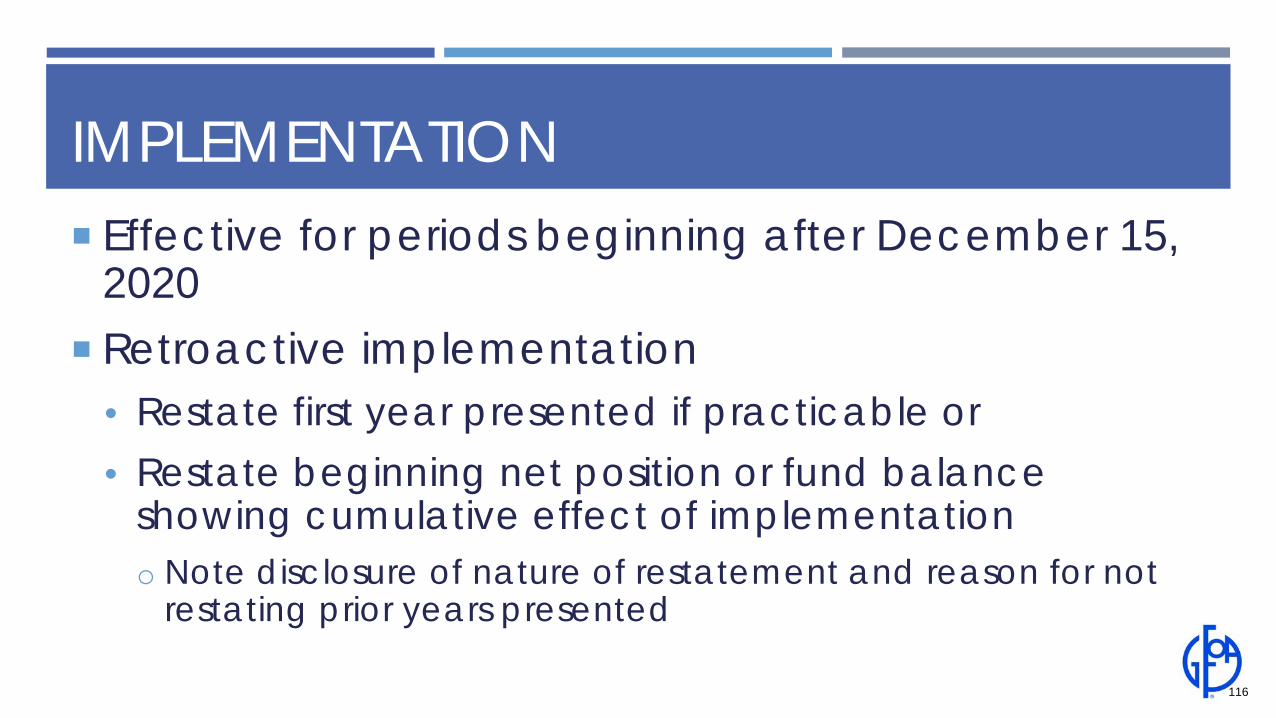

IMPLEMENTATION Effective for periods beginning after December 15,

2020 Retroactive implementation

• Restate first year presented if practicable or • Restate beginning net position or fund balance

showing cumulative effect of implementationo Note disclosure of nature of restatement and reason for not

restating prior years presented

116

GASB IMPLEMENTATION GUIDE NO. 2019-1, IMPLEMENTATION GUIDANCE UPDATE – 2019

ISSUED: APRIL 2019EFFECTIVE DATE: PERIODS BEGINNING AFTER JUNE 15, 2019

14 NEW Q&As Pension & OPEB - 4 Terminations of Hedge Derivatives – 1 Disaster Grant & Insurance Recovery – 2 Intra-Entity Transfers – 2 Nonspendable Governmental Fund Balance Calculation – 1 Tax Abatement Disclosures – 1 Irrevocable Split Interest Agreements – 3

118

BOND INDEX RATES IN PEB

Pension and OPEB plans and employers measurement of PEB liabilities that use a yield or index rate:

Rates used must be as of the measurement dateAverage of rates/indexes from different dates

may not be used 119

OPEB IMPLICIT RATE SUBSIDIESRetiree subsidies implicit in premiums paid for active employees between the measurement date and the end of the employer’s reporting period should be included in the calculation of deferred outflows of resources related to OPEB contributions made during that period.

120

TERMINATIONS OF EFFECTIVE HEDGING DERIVATIVESDeferred inflows or outflows of resources related to an interest rate swap that was an effective hedge are recognized as resources flows (gains or losses) on the date that the derivative terminates. If settlement (payment) will be made in the

future, the government recognizes the amount receivable or payable. 121

DISASTER GRANT RECOGNITIONA government should not recognize a grant receivable prior to the execution of a grant agreement, even if: Eligible expenditures have been incurredA presidential disaster declaration and

funding agreement are in place The grant agreement is executed prior to

issuance of F/S 122

INSURANCE RECOVERYInsurance recoveries for storm damage clean-up costs in a governmental fund should be either:Netted against clean-up expenditures if

realized or realizable (insurer acknowledges coverage) in the same year

Reported as other financing sources, or extraordinary items, if first realized or realizable in subsequent period(s) 123

INTRA-ENTITY TRANSFERS

Assets transferred within a reporting entity must be reported by the transferee at the transferor’s carrying value. No mark-up to market value, even if

transferee intends to hold the transferred asset as an investment or to sell.

124

GOVERNMENTAL FUND BALANCE

Long-term portion of governmental fund receivables that are reported as deferred inflows are not included in nonspendable fund balance.

125

TAX ABATEMENT DISCLOSURESThe existence of alternate tax incentives or agreements does not factor into the calculation of a government’s disclosed forgone tax revenue.

126

IRREVOCABLE SPLIT-INTEREST AGREEMENTS (ISAs)Government’s remainder interest is a contribution to a permanent fund:

Reported as two separate transactions: Establishment of ISA:

Government recognizes deferred inflow

Termination of ISA: Government recognizes establishment of the permanent fund. 127

IRREVOCABLE SPLIT-INTEREST AGREEMENTS (ISAs) (CONT.)

If Government’s lead interest is reported in a governmental fund, then the fund recognizes a fund liability for the remainder interest

128

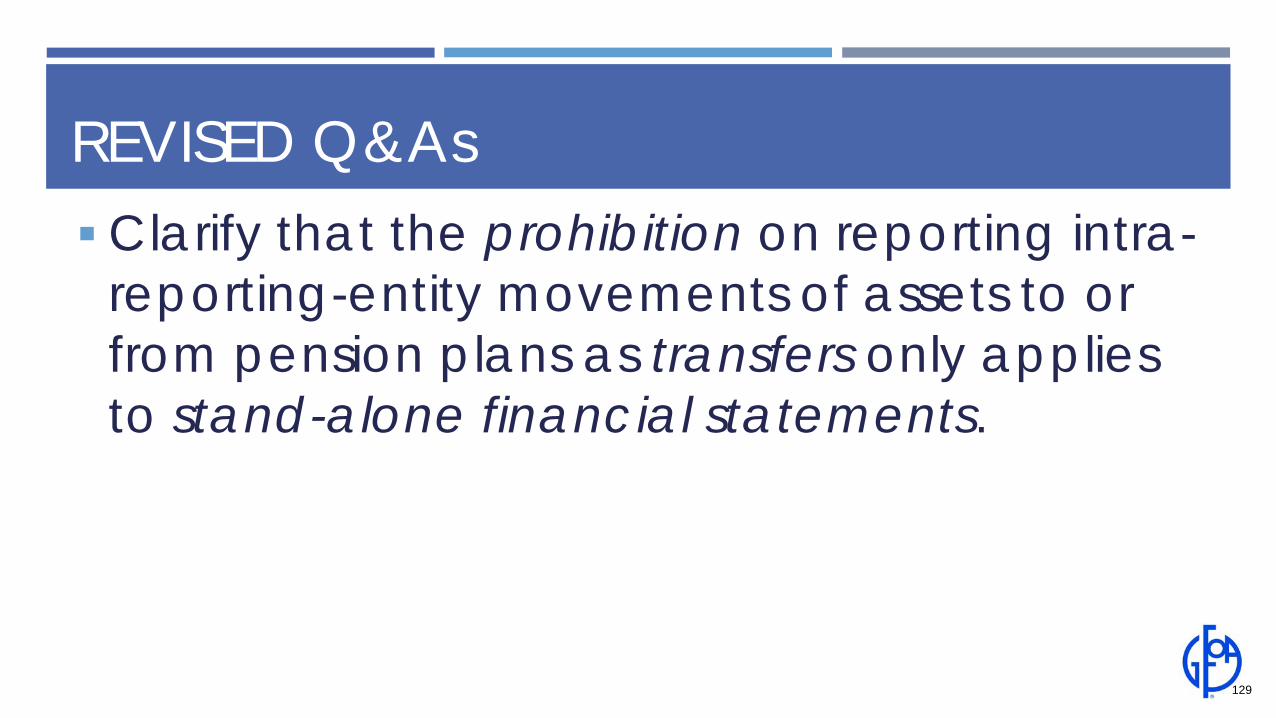

REVISED Q&AsClarify that the prohibition on reporting intra-

reporting-entity movements of assets to or from pension plans as transfers only applies to stand-alone financial statements.

129

REVISED Q&As (CONT.) Clarify debt service to maturity disclosure

requirements for variable rate debt for which there is an effective hedging derivative• Disclosure debt service requirements – and a

separate column showing the effect of the swap – assuming continuation of current rates on both the debt and the swap

• Despite the fact that the fair value of the swap is based on expected future rates, not current rates)

130

REVISED Q&As (CONT.)

131

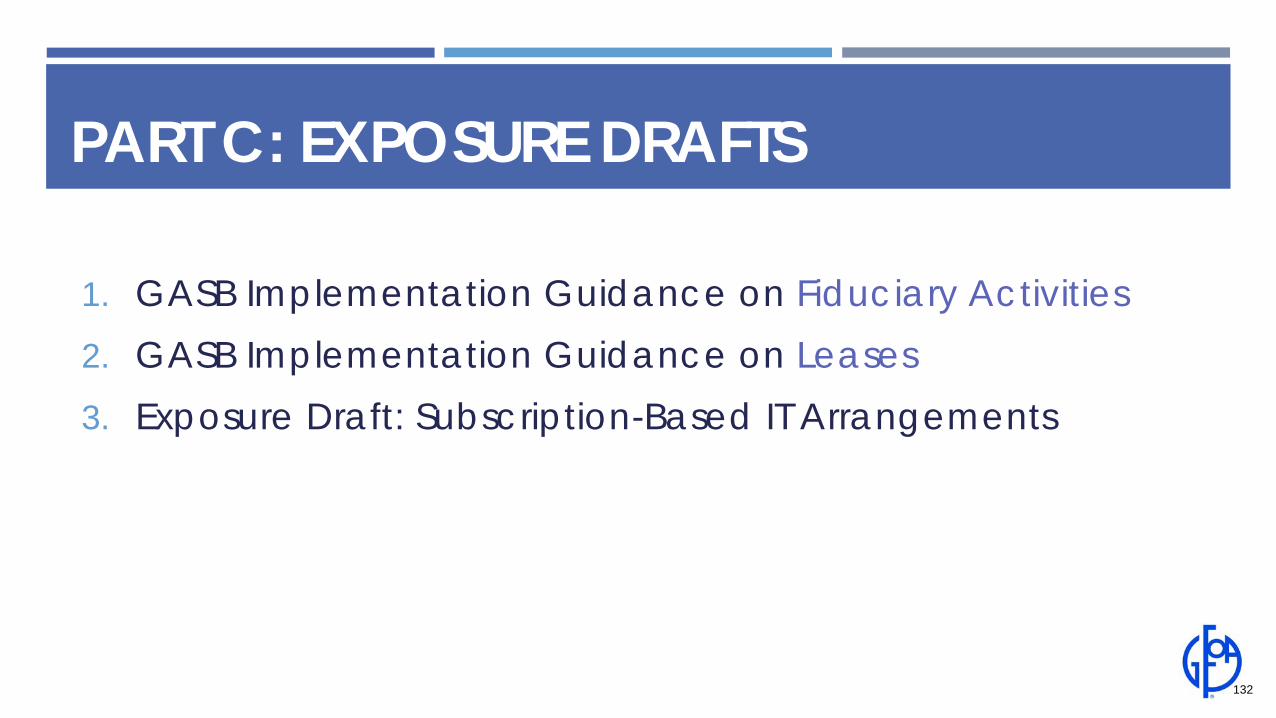

PART C: EXPOSURE DRAFTS

1. GASB Implementation Guidance on Fiduciary Activities2. GASB Implementation Guidance on Leases3. Exposure Draft: Subscription-Based IT Arrangements

132

GASB EXPOSURE DRAFT PROPOSED IMPLEMENTATION GUIDE – FIDUCIARY ACTIVITIES

ED ISSUED: DECEMBER 2018FINAL IG EXPECTED ISSUANCE : JUNE 2019PROPOSED EFFECTIVE DATE: PERIODS BEGINNING AFTER DECEMBER 15, 2018.

NEW Q&As53 New Q&AsIdentifying Fiduciary Activities

• Component Units (CUs)oSeparate legal entities – 3 oFinancial accountability – 5

• PEB Arrangements that are not CUs – 1 134

NEW Q&AS (CONT.) Identifying Fiduciary Activities (cont.)

• Other Fiduciary Activities (i.e., Non-CU, Non-PEB) oGeneral distinctions fiduciary/non-fiduciary – 7 o Individual v. organizational beneficiaries – 5 oAdministrative involvement – 9 oDirect financial involvement – 1oControl of assets – 5 oOwn-source revenue – 4

135

NEW Q&AS (CONT.)

Fiduciary Fund Types – 7 Fiduciary Financial Statements

• Statement of fiduciary net position – 1 • Statement of changes in fiduciary net position

disaggregation exceptions – 3 • Reporting Fiduciary CUs – 3

136

REVISED Q&A

3 Revised Q&As Clarifications and improved alignment with

GASB 84

137

GFOA’S COMMENTS Generally believe guidance to be clear and

beneficial, • Especially Q&As specific to schools (student activity fees)

Requested clarifications/additional guidance:• Clarifying distinction in accounting for shared revenue v.

taxes or fees collected on behalf of another government• Providing additional examples pertaining to unclaimed or

escheat property• Distinguishing between disaggregated presentation and

aggregated reporting permitted as an exception for funds normally held in a custodial capacity for less than 3 months. 138

GASB EXPOSURE DRAFT PROPOSED IMPLEMENTATION GUIDE – LEASES

ED ISSUED: FEBRUARY 2019FINAL IG EXPECTED ISSUANCE : JUNE 2019PROPOSED EFFECTIVE DATE: PERIODS BEGINNING AFTER JUNE 15, 2019

NEW Q&AS80 New Q&As Scope and Applicability – 13Determining Lease Term – 9 Identifying Short-term Leases – 4Contracts that Transfer Ownership – 2

140

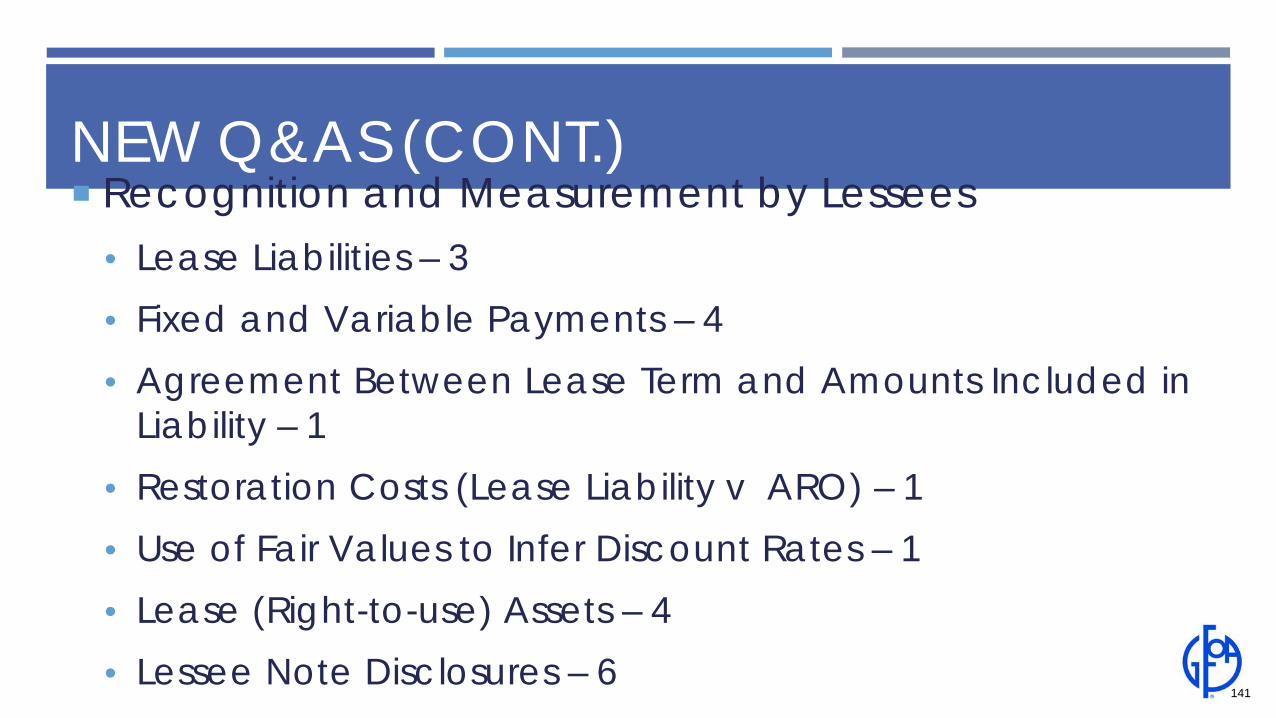

NEW Q&AS (CONT.) Recognition and Measurement by Lessees

• Lease Liabilities – 3 • Fixed and Variable Payments – 4 • Agreement Between Lease Term and Amounts Included in

Liability – 1 • Restoration Costs (Lease Liability v ARO) – 1 • Use of Fair Values to Infer Discount Rates – 1 • Lease (Right-to-use) Assets – 4 • Lessee Note Disclosures – 6

141

NEW Q&AS (CONT.) Recognition and Measurement by Lessors

• Leases that are Investments – 1 • Certain Regulated Leases – 1 • Lease Receivables – 3 • Deferred Inflows of Resources – 2 • Underlying Assets – 2 • Lessor Note Disclosures – 2 • Other – 2

142

NEW Q&AS (CONT.) Lease Incentives – 2 Leases with Multiple Components – 5 Contract Combinations – 2 Lease Modifications and Terminations – 6 Sale- and Lease-Leaseback Transactions – 4 Intra-entity Leases – 1 Effective Date and Transition – 2

143

GFOA’S COMMENTSGenerally believe guidance to be specific and

helpful Requested clarifications/additional guidance: From perspective of governmental lessors To assist in estimating or inferring lease interest rates for

lessees Related to regulated leases About software that is inseparable from leased

hardware144

GASB EXPOSURE DRAFT PROPOSED STATEMENT SUBSCRIPTION-BASED INFORMATION TECHNOLOGY ARRANGEMENTS

ED ISSUED: MAY 2019COMMENT PERIOD ENDS: AUGUST 23, 2019PROPOSED EFFECTIVE DATE: FISCAL YEARS BEGINNING AFTER JUNE 15, 2021 AND REPORTING PERIODS THEREAFTER

Subscription Based Information Technology Arrangements (SBITAs)

LeaseInternally Generat

ed Software

146

SBITA

SUBSCRIPTION-BASED INFORMATION TECHNOLOGY ARRANGEMENTS (SBITAs)

Definition: A contract that conveys control of the right to use another party’s hardware, software, or a combination of both, including information technology (IT) infrastructure as specified in a contract for a period of time in an exchange or an exchange-like transaction

147

SBITAs AND THEIR COUSINS: LEASES

SBITAA contract that conveys control of the right to use another party’s hardware, software, or a combination of both, including IT infrastructure as specified in a contract for a period of time in an exchange or an exchange-like transaction

LeaseA contract that conveys control of the right to use another entity’s nonfinancial asset as specified in the contract for a period of time in an exchange or exchange-like transaction

148

SBITAs AND THEIR COUSINS: LEASES

SBITAA contract that conveys control of the right to use another party’s hardware, software, or a combination of both, including IT infrastructure as specified in a contract for a period of time in an exchange or an exchange-like transaction

LeaseA contract that conveys control of the right to use another entity’s nonfinancial asset as specified in the contract for a period of time in an exchange or exchange-like transaction

149

SBITAs AND THEIR COUSINS: LEASES

SBITAA contract that conveys control of the right to use another party’s hardware, software, or a combination of both, including IT infrastructure as specified in a contract for a period of time in an exchange or an exchange-like transaction

LeaseA contract that conveys control of the right to use another entity’s nonfinancial asset as specified in the contract for a period of time in an exchange or exchange-like transaction

Major Difference: Governments are only expected to be in the “lessee” role – No “lessor equivalent”

accounting guidance

150

EXCLUDED

Governments that provide the right to use their hardware or software to other entities through SBITAs

Service Concession Arrangements (GASB 60; Cod. Sec. 30)

Arrangements that grant a perpetual license to use a vendor’s software (Cod Sec 1400.142-153, Intangible Assets/GASB 51,)

151

SUBSCRIPTION-BASED INFORMATION TECHNOLOGY ARRANGEMENTS (SBITAs) (CONT.)

Party whose IT hardware/infrastructure and/or software is being used:

• SBITA vendor (≈ lessor) IT hardware/infrastructure and/or software that

is the subject of the contract:

• Underlying hardware or software152

SIMILAR TO LEASES Subscription term calculationWhen reassessment of lease term is required Short term SBITAs – 12 months or less max termDiscount rate

153

SUBSCRIPTION LIABILITY MEASUREMENT

Fixed payments Variable payments dependent on

an index or rate (as of commencement)

Variable payments that are fixed in substance

Payments for SBITA termination penalties if the term reflects the exercise of an option for which there is a penalty

Subscription contract incentives receivable

Other payments to SBITA vendor that the government is reasonably certain to be required to pay

Present value of payments expected to be required during the contract term, including:

154

SUBSCRIPTION ASSET Measure - sum of :

• Initial measurement of subscription liability• Subscription payments made to SBITA vendor at or before

beginning of the lease term • Capitalizable implementation costs

Amortize in a systematic and rational manner over the shorter of:• Subscription term • Useful life of the underlying hardware or software

155

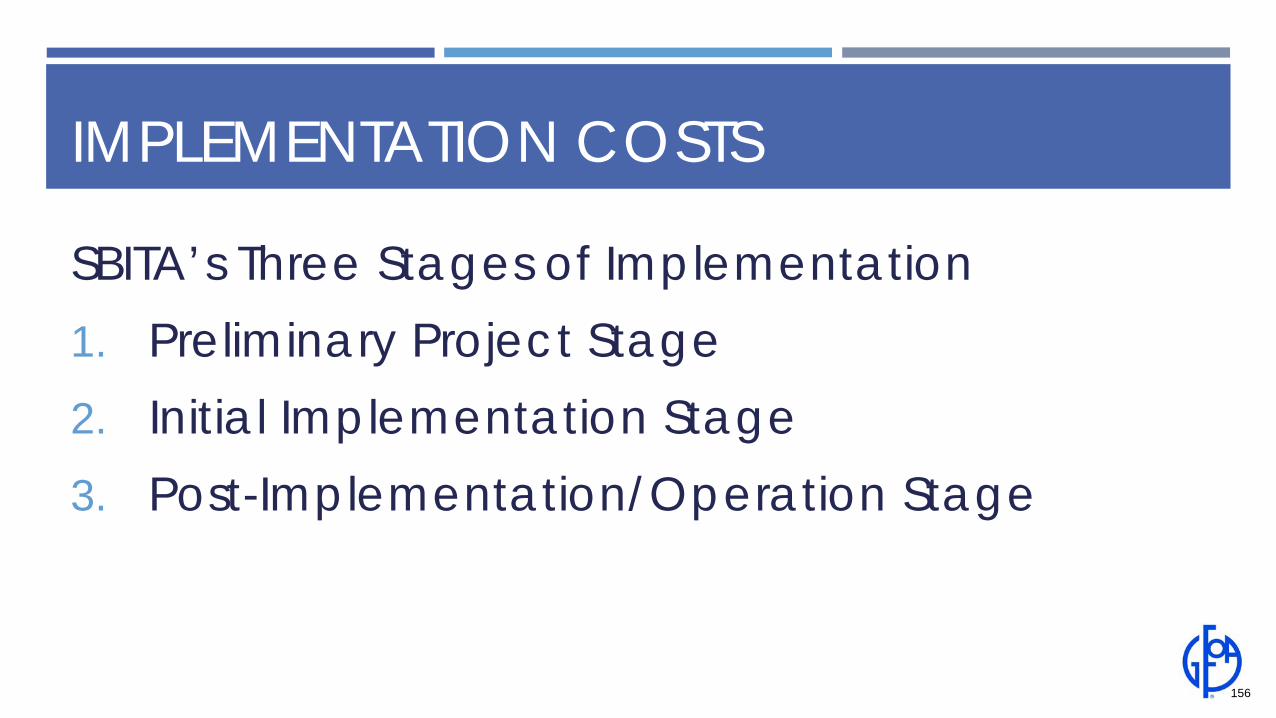

IMPLEMENTATION COSTS

SBITA’s Three Stages of Implementation1. Preliminary Project Stage2. Initial Implementation Stage3. Post-Implementation/Operation Stage

156

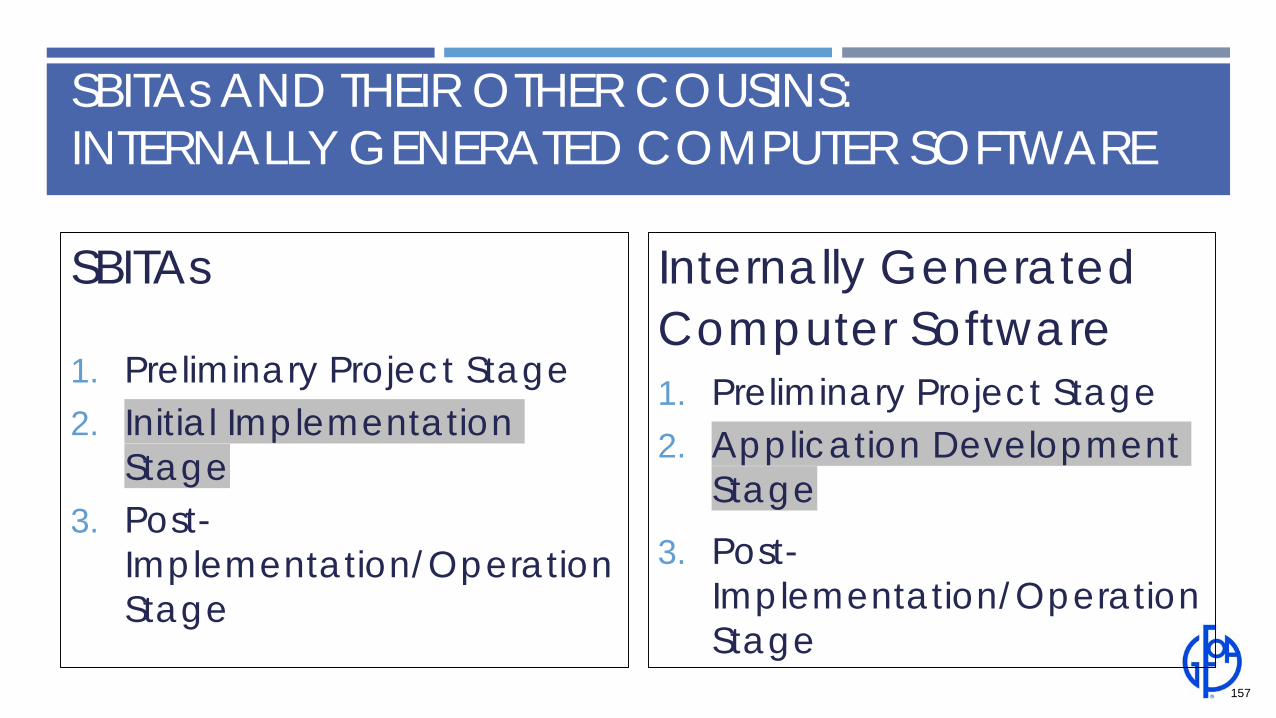

SBITAs AND THEIR OTHER COUSINS: INTERNALLY GENERATED COMPUTER SOFTWARE

SBITAs

1. Preliminary Project Stage2. Initial Implementation

Stage3. Post-

Implementation/Operation Stage

Internally Generated Computer Software1. Preliminary Project Stage2. Application Development

Stage3. Post-

Implementation/Operation Stage

157

CAPITAL ELIGIBILITY VERY LIMITEDExpense all costs incurred before: Determination of project

objective and the nature of service capacity of subscription

Demonstration of feasibility of subscription

Demonstration of intent, ability and effort to enter i b i i

And, those criteria are not met until: Preliminary project stage

activities are completed Management authorizes

and commits to funding at least the first fiscal year of the SBITA

158

IMPLEMENTATION COSTS -CAPITALIZABLE

SBITA’s Three Stages of Implementation1. Preliminary Project Stage – Expense2. Initial Implementation Stage – Capitalize as

part of subscription asset3. Post-Implementation/Operation Stage –

Expense159

OTHER COSTS

Outlays, in addition to subscription payments, for SBITA already in operation should be capitalized only if they result in either: Increased functionality (new tasks) Increased efficiency (higher level of service)

160

ALSO SIMILAR TO LEASE GUIDANCE

SBITA vendor paid incentives SBITA contracts with multiple components SBITA contract combinations SBITA contract modifications and terminationsNote disclosures

161

PART D: GUIDANCE EFFECTIVE 2019 GASB Statement No 83, Certain Asset Retirement

Obligations GASB Statement No. 84,* Fiduciary Activities GASB Statement No. 88, Certain Disclosures Related to

Debt, including Direct Borrowings and Direct Placements GASB Statement No. 90, * Majority Equity Interests GASB Implementation Guide No. 2018-1, Implementation

Guidance Update - 2018 162

* Effective for Calendar FYEs 2019; Other FYEs 2020

GASB STATEMENT NO. 88 [COD. A10]DISCLOSURES RELATED TO DEBT,INCLUDING DIRECT BORROWINGS AND DIRECT PLACEMENTS

ISSUED: MARCH 2018EFFECTIVE DATE: PERIODS BEGINNING AFTER JUNE 15, 2018

GASB 88Establishes new note disclosure requirements

for long term debt, including direct borrowings and placements.

Effective for reporting periods beginning after June 15, 2018. Earlier application is encouraged.

164

DEFINITION OF DEBT

A liability that arises from a contractual obligation to pay cash (or other assets that may be used in lieu of cash) in one or more payments to settle an amount that is fixed at the date the contractual obligation is established. Excludes:

• Leases (except for contracts reported as a financed purchase of the underlying asset)

• accounts payable

165

ADDITIONAL DISCLOSURESAmount of unused lines of creditAssets pledged as collateral for debt Terms specified in debt agreements related to

significant:• Events of default with finance-related consequences, • Termination events with finance-related

consequences, and • Subjective acceleration clauses.

166

ADDITIONAL DISCLOSURES (CONT.)

Separate information in debt disclosures for Direct borrowings and direct placement debt Other debt

167

QUESTIONS OR COMMENTS?

168

Government Finance Officers Association Technical Services Center(312) 977-0700