accounting

3

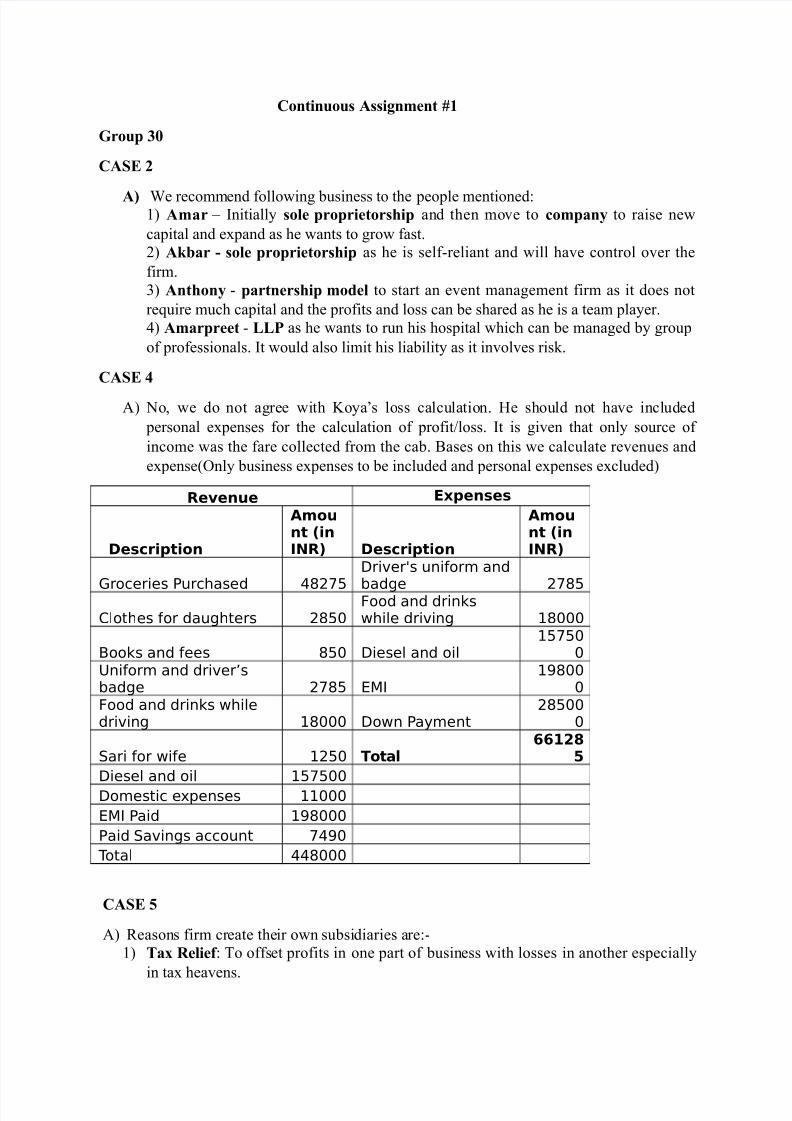

Continuous Assignment #1 Group 30 CASE 2 A) We recommend following business to the people mentioned: 1) Amar – Initially sole proprietorship and then mo ve to company to raise new capital and expand as he wants to grow fast. 2) Akbar - sole proprietorship as he is selfreliant and will have control over the firm. !) Anthony partnership moel to start an event management firm as it does not re"uire much capital and the profits and loss can be shared as he is a team player. #) Amarpreet !!" as he wants to run his hospital which can be managed by group of professionals. It would also limit his liability as it involves ris$. CASE %) &o' we do not agree wi th (oya s loss calcu latio n. *e should not have incl uded personal expenses for the calculation of profit+loss. It is given that only source of income was the fare collected from the cab. ,ases on this we calculate revenues and expense-nly business expenses to be included and personal expenses excluded) Revenue Expenses Description Amou nt (in INR) Description Amou nt (in INR) Groceries Purchased 48275 Driver's uniform and badge 2785 Clothes for daughters 2850 Food and drins !hile driving "8000 #oos and fees 850 Diesel and oil "5750 0 $niform and driver%s badge 2785 &( ")800 0 Food and drins !hile driving "8000 Do!n Pa*ment 28500 0 +ari for !ife "250 Total 66128 5 Diesel and oil "57500 Domestic e,-enses ""000 &( Paid ")8000 Paid +avings account 74)0 . otal 448000 CASE $ %) /eason s firm cr eate the ir own subsi diaries a re: 1) %a& 'elie( : 0o offset profits in one part of busin ess with losses in another especially in tax heavens.

-

Upload

ankit-goel -

Category

Documents

-

view

4 -

download

0

description

accounting

Transcript of accounting

7/18/2019 accounting

http://slidepdf.com/reader/full/accounting-56d4b01baa0c9 1/3

Continuous Assignment #1

Group 30

CASE 2

A) We recommend following business to the people mentioned:1) Amar – Initially sole proprietorship and then move to company to raise new

capital and expand as he wants to grow fast.

2) Akbar - sole proprietorship as he is selfreliant and will have control over the

firm.

!) Anthony partnership moel to start an event management firm as it does not

re"uire much capital and the profits and loss can be shared as he is a team player.

#) Amarpreet !!" as he wants to run his hospital which can be managed by group

of professionals. It would also limit his liability as it involves ris$.

CASE

%) &o' we do not agree with (oyas loss calculation. *e should not have included

personal expenses for the calculation of profit+loss. It is given that only source of

income was the fare collected from the cab. ,ases on this we calculate revenues and

expense-nly business expenses to be included and personal expenses excluded)

Revenue Expenses

Description

Amount (inINR) Description

Amount (inINR)

Groceries Purchased 48275

Driver's uniform and

badge 2785

Clothes for daughters 2850Food and drins!hile driving "8000

#oos and fees 850 Diesel and oil"5750

0$niform and driver%sbadge 2785 &(

")8000

Food and drins !hiledriving "8000 Do!n Pa*ment

285000

+ari for !ife "250 Total66128

5

Diesel and oil "57500

Domestic e,-enses ""000

&( Paid ")8000

Paid +avings account 74)0

.otal 448000

CASE $

%) /easons firm create their own subsidiaries are:

1) %a& 'elie( : 0o offset profits in one part of business with losses in another especially

in tax heavens.

7/18/2019 accounting

http://slidepdf.com/reader/full/accounting-56d4b01baa0c9 2/3

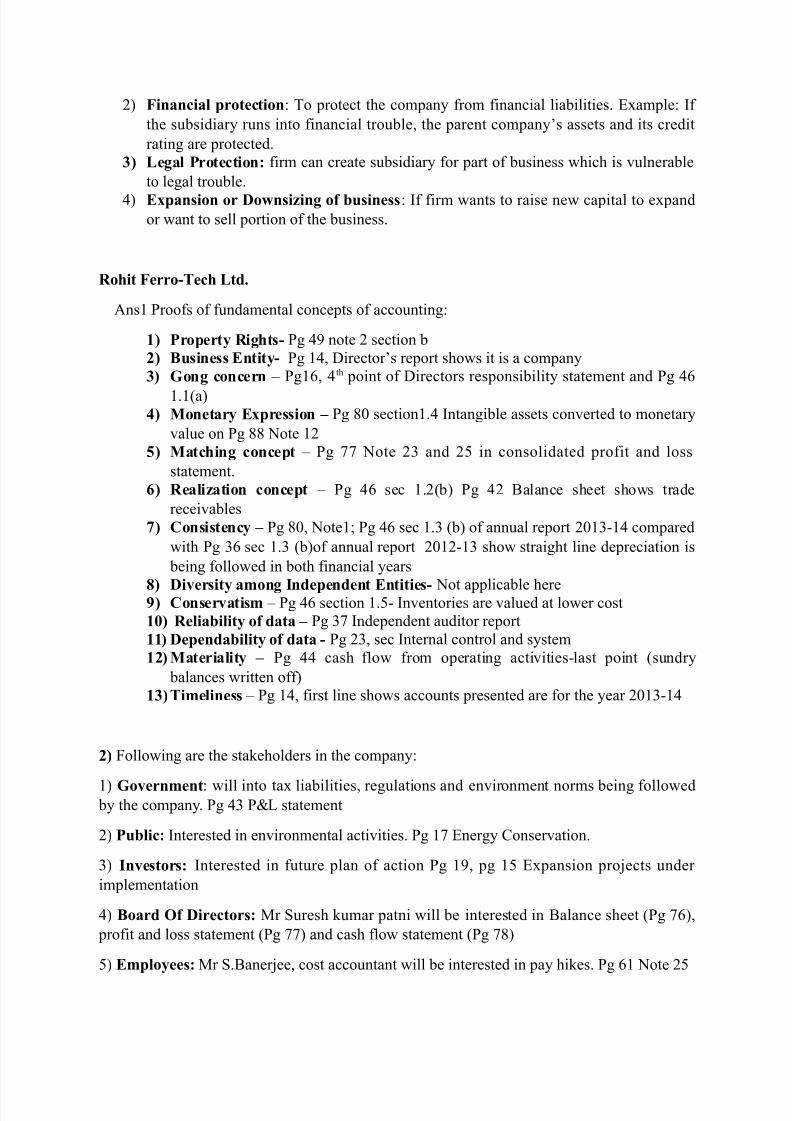

2) inancial protection: 0o protect the company from financial liabilities. xample: If

the subsidiary runs into financial trouble' the parent companys assets and its credit

rating are protected.

3) !egal "rotection* firm can create subsidiary for part of business which is vulnerable

to legal trouble.

#) E&pansion or +o,nsiing o( business: If firm wants to raise new capital to expandor want to sell portion of the business.

'ohit erro-%ech !t.

%ns1 roofs of fundamental concepts of accounting:

1) "roperty 'ights- g #3 note 2 section b

2) /usiness Entity- g 1#' 4irectors report shows it is a company

3) Gong concern – g15' #th point of 4irectors responsibility statement and g #5

1.1-a)) onetary E&pression g 67 section1.# Intangible assets converted to monetary

value on g 66 &ote 12

$) atching concept – g 88 &ote 2! and 29 in consolidated profit and loss

statement.

) 'ealiation concept – g #5 sec 1.2-b) g #2 ,alance sheet shows trade

receivables

) Consistency g 67' &ote1 g #5 sec 1.! -b) of annual report 271!1# compared

with g !5 sec 1.! -b)of annual report 27121! show straight line depreciation is

being followed in both financial years

4) +i5ersity among 6nepenent Entities- &ot applicable here7) Conser5atism – g #5 section 1.9 Inventories are valued at lower cost

10) 'eliability o( ata g !8 Independent auditor report

11) +epenability o( ata - g 2!' sec Internal control and system

12) ateriality g ## cash flow from operating activitieslast point -sundry

balances written off)

13) %imeliness – g 1#' first line shows accounts presented are for the year 271!1#

2) ;ollowing are the sta$eholders in the company:

1) Go5ernment: will into tax liabilities' regulations and environment norms being followed by the company. g #! <= statement

2) "ublic* Interested in environmental activities. g 18 nergy >onservation.

!) 6n5estors* Interested in future plan of action g 13' pg 19 xpansion pro?ects under

implementation

#) /oar 8( +irectors* @r Auresh $umar patni will be interested in ,alance sheet -g 85)'

profit and loss statement -g 88) and cash flow statement -g 86)

9) Employees* @r A.,aner?ee' cost accountant will be interested in pay hi$es. g 51 &ote 29

7/18/2019 accounting

http://slidepdf.com/reader/full/accounting-56d4b01baa0c9 3/3

5) E9uity Analyst an un anagers* Interested in credit rating -pg 19)' share

performance and corporate debt restructuring -g 19)

8) Customers* Interested in $nowing the ability to fulfil orders eg. steel industry

6) Suppliers an 8ther Creitors* Interested in profitability and improvements of the

company. g 17 and pg#2