ACCOUNTANTS ONE 2012 ACCOUNTING UPDATE FEBRUARY 22, 2012 Presented by Chris Rouse Windham Brannon,...

66

ACCOUNTANTS ONE 2012 ACCOUNTING UPDATE FEBRUARY 22, 2012 Presented by Chris Rouse Windham Brannon, PC

-

Upload

audrey-glenn -

Category

Documents

-

view

214 -

download

0

Transcript of ACCOUNTANTS ONE 2012 ACCOUNTING UPDATE FEBRUARY 22, 2012 Presented by Chris Rouse Windham Brannon,...

ACCOUNTANTS ONE 2012 ACCOUNTING UPDATE

FEBRUARY 22, 2012

Presented by

Chris Rouse

Windham Brannon, PC

• Questions, Questions, QuestionsoWhat’s going on at FASB?oWill IFRS be adopted?oWill all operating leases be capitalized?oWhen are we going to have “Little GAAP”?oWill the balance sheet still balance?oWhere have all the VIEs gone?oWhen is revenue “earned”?oWhat is equity?

• Pot Pourri of Other New Standards

2012 ACCOUNTING UPDATE

Topics To Be Covered

2

• Board members

Leslie Seidman (Chair) Larry Smith Tom LinsmeierIndustry Public Accounting EducationDir Acctg Policy & Stds Former EITF Chair Derivatives Expertise(JP Morgan) (KPMG) (Michigan State)

2012 ACCOUNTING UPDATE

What’s Going On At FASB?

3

• Board members

Russell Golden Marc SiegelPublic Accounting IndustryEITF Chair/FASB Staff Forensic Accounting(Deloitte & Touche) (RiskMetrics Group)

2012 ACCOUNTING UPDATE

What’s Going On At FASB?

4

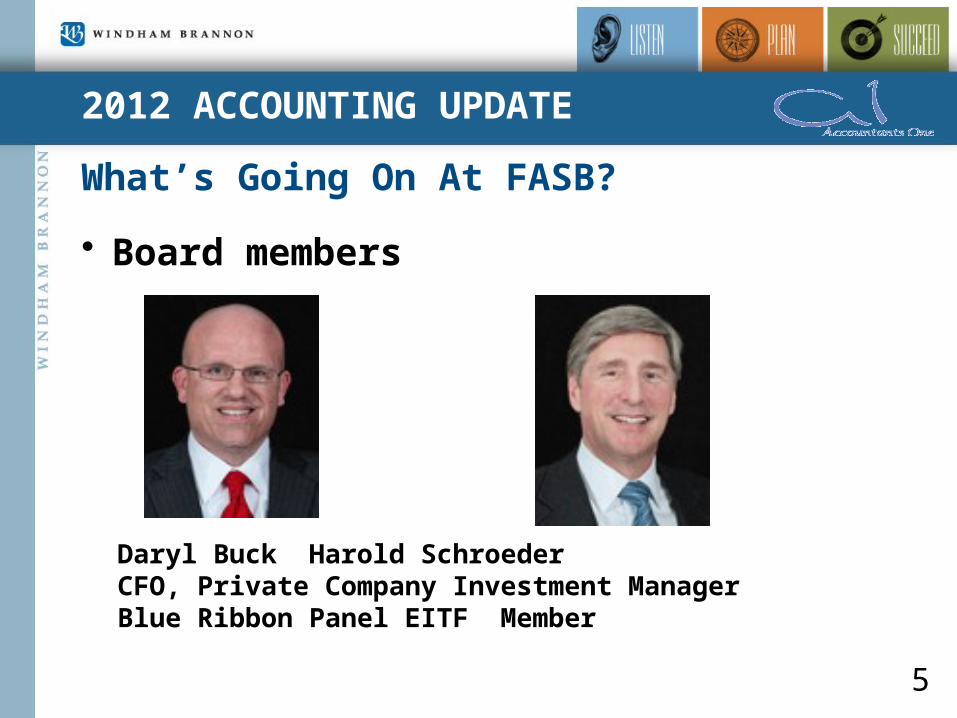

• Board members

Daryl Buck Harold SchroederCFO, Private Company Investment ManagerBlue Ribbon Panel EITF Member

2012 ACCOUNTING UPDATE

What’s Going On At FASB?

5

2012 ACCOUNTING UPDATE

Will IFRS be adopted, rendering all our GAAP accounting skills obsolete?

6

• FASB continues to advance Convergence with international accounting standardso All recent FASB Standards reflect convergence

with IFRSo FASB believes international standards are best

for worldwide marketso Pressure for convergence is moving faster than

FASB anticipatedo Conceptual Framework focus is on private

sector

2012 ACCOUNTING UPDATE

Will IFRS be adopted, rendering all our GAAP accounting skills obsolete?

7

• Uncertainty regarding completion of projects remaining on MOU

• Both FASB and IASB have said there will be no future projects once current agenda is completed

2012 ACCOUNTING UPDATE

Will IFRS be adopted?

8

• In 2008, SEC proposed Roadmap for potential use of IFRS by US issuers beginning 2014

• In 2009, both SEC and Congress expressed concerns about progress on the Roadmap

• In 2010, SEC said prior Roadmap timing is no longer in play – Work Plan adopted

• In 2011, SEC said progress on Work Plan is slower than expected

2012 ACCOUNTING UPDATE

Will IFRS be adopted?

9

• SEC “Work Plan” examines 6 areas impacted by adoption of IFRS by US companiesoConsistency of applicationo Independence of IASBo Investor understanding of IFRSo Impact on US laws and regulationso Impact on preparerso Impact on auditors

2012 ACCOUNTING UPDATE

Will IFRS be adopted?

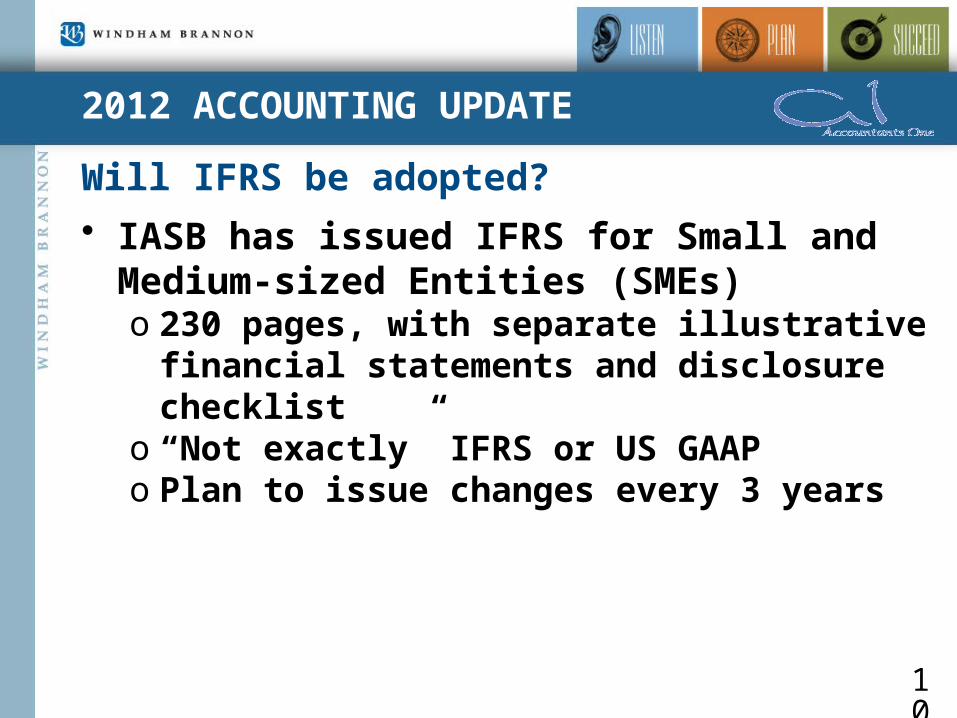

10

• IASB has issued IFRS for Small and Medium-sized Entities (SMEs)o 230 pages, with separate illustrative financial

statements and disclosure checklisto “Not exactly” IFRS or US GAAPo Plan to issue changes every 3 years

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized? Will the entire balance sheet become “fair valued”?

11

• Overarching principle – A right to useo Leasing is a financing transactiono Recognize lease payment obligation and

leased asset on balance sheeto Includes all leases of tangible assets, not

just property leases Board is still considering software and

inventory leaseso Existing leases would be recognized

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

12

• Lessee accountingo Lease obligation recognized at present value

Contingent payments that are likely to occur would be included

Indexed changes would be recognized as they occur

Lease term includes non-cancellable period plus renewal periods when “significant economic incentive” to renew is present

Discount rate is rate charged by lessor or lessee’s incremental borrowing rate

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

13

• Lessee accountingo Lease asset recognized at obligation plus

direct costso Subsequent changes reflected as they

occur In earnings if change arises from current

or prior periods In obligation (and asset) if related to

future periods

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

14

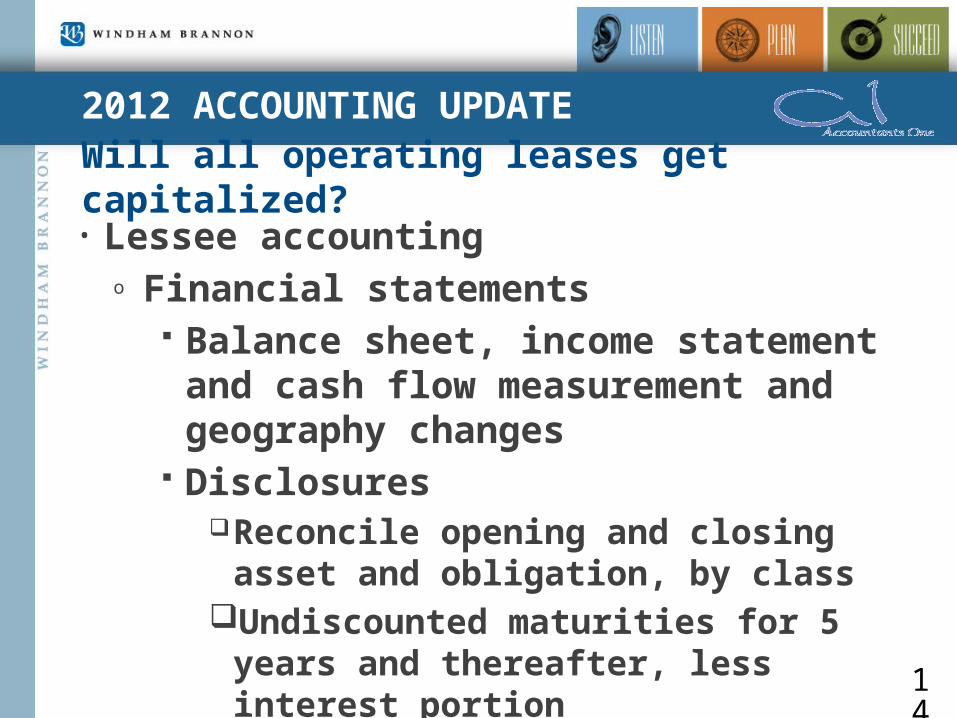

• Lessee accountingo Financial statements

Balance sheet, income statement and cash flow measurement and geography changes

DisclosuresReconcile opening and closing asset and

obligation, by classUndiscounted maturities for 5 years and

thereafter, less interest portion

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

15

• Lessee accountingo Disclosures

Lease expense in tabular format, including AmortizationInterestVariable payments not in amortizationExpense for any non-capitalized leases

Future commitment for services or non-asset component of leases

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

16

• Lessor accountingo A dual model

Performance obligation approach for financing transactions

De-recognition approach for sale transactions

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

17

• Lessor accountingo Performance obligation approach

Applies when lessor retains risks and rewards of asset

Recognize asset for contractual terms, plus contingent rentals, renewals, termination payments, etc

Changes as lease payments are made Recognize liability to provide asset

Amortize based on pattern of use (revenue)Straight line if no pattern

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

18

• Lessor accountingo Performance obligation approach

Recognize interest income using effective interest method

Reassess estimates each reporting periodRecognize changes in lease terms on balance

sheetChanges in contingent/index payments added

to asset and liability Included in current period revenue if effects

prior or current period

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

19

• Lessor accountingo Performance obligation approach

Leased asset remains on booksDepreciation/amortization in accordance

with GAAP

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

20

• Lessor accountingo De-recognition approach

When ownership transfers at end of lease, or when there is a bargain purchase option

Recognize receivable and sale revenue De-recognize asset and recognize cost of sales

Amount is based on relationship of fair values of receivable and asset

Residual is not accreted While similar to current sales-type lease,

amounts are determined differently

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

21

• Lessor accountingo De-recognition approach

Reassess upon change in lease terms Contingent/index cash flows are recognized in

revenue On balance sheet, present lease receivable

separately from other financial assets

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

22

• Lessor accountingo De-recognition approach

Any residual asset is presented separately within that asset’s class

Income statement depends on lessor’s business

Financing business – net lease income and expense on one line

Seller business – separate lines for lease income and expense

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

23

• Sale- Leasebackso Recognized as two transactionso “Control” criteria in revenue recognition ED

would determine if sale occurredo Accounted for as (1) sale of “whole” asset, and

(2) lease of a right-to-use underlying asset

2012 ACCOUNTING UPDATE

Will all operating leases get capitalized?

24

• The Devil is in the detailso Second exposure draft due out “soon”

Some key lessor items still being discussed Second ED may still have some tentative

positionso Preparing financial statement preparerso Preparing auditorso Preparing financial statement users

2012 ACCOUNTING UPDATE

When are we going to have “Little GAAP” for smaller companies?

25

• FASB is considering GAAP Differences vs. Separate GAAP approach o Criteria considers different user needs

Differences in user access to information Cost/Benefit considerations Small/Large business vs. Public/Nonpublic

businessNote – FASB does not believe there is a lack of

investor users for non-public entities• FASB has named a staff-member to oversee all

nonpublic entity issues

2012 ACCOUNTING UPDATE

When are we going to have “Little GAAP”?

26

• Small Business Advisory Committee formed in 2004o Purpose is to obtain more active involvement

by the business community in accounting standards Representatives include public and non-

public companieso Twenty members representing users,

preparers and auditorso Meets twice a year, discusses issues and

submits recommendations to the Board

2012 ACCOUNTING UPDATE

When are we going to have “Little GAAP”?

27

• Private Company Financial Reporting Committee started in 2007o Joint initiative of FASB and AICPAo Purpose is to provide recommendations to

FASB on accounting standards for privately held companies

2012 ACCOUNTING UPDATE

When are we going to have “Little GAAP”?

28

• Private Company Financial Reporting Committeeo Has submitted over 40 recommendations on

specific standards eg, has issues with revenue from contracts

exposure draft eg, is supportive of the lease accounting

exposure draft Says FASB continues to show an

unwillingness to consider and approve measurement, recognition or presentation differences

2012 ACCOUNTING UPDATE

When are we going to have “Little GAAP”?

29

• Blue Ribbon Panel on Private Company Accounting formed in 2010o Joint initiative of AICPA and FAFo Purpose is to address how accounting

standards can best meet the needs of users of private company financial statements Lack of relevance for many users of private

company financials Overall complexity concerns private

company preparers

2012 ACCOUNTING UPDATE

When are we going to have “Little GAAP”?

30

• Blue Ribbon Panel on Private Company AccountingoRecommended near-term exceptions and

modifications to US GAAP for private companies rather than a separate, self-contained GAAP for private companies Recommended a separate private company

accounting standards board to address both existing and new standards

2012 ACCOUNTING UPDATE

When are we going to have “Little GAAP”?

31

• Blue Ribbon Panel on Private Company AccountingoReport submitted in January 2011 – see it at

http://www.accountingfoundation.org

• In late 2011, the FAF rejected the Panel’s recommendation in favor of increasing FASB staff and input to FASB from non-public entity groups

• AICPA has asked FAF to reconsider separate standard setting body for non-public entities

2012 ACCOUNTING UPDATE

Will the balance sheet still balance?

32

• FASB Project; Financial Statement Presentationo Tentative conclusion is a full set of financial

statements is comparative information for two full years, consisting of statements of: 3 years of financial position 2 years of earnings and comprehensive

income 2 years of cash flows 2 years of changes in equity

2012 ACCOUNTING UPDATE

Will the balance sheet still balance?

33

• FASB Project; Financial Statement Presentationo All statements would classify accounts as

operating (business), financing and investing Format is similar to current cash flow

statement See examples in Attachments

2012 ACCOUNTING UPDATE

Where have all the VIE’s gone?

34

• Improving VIE disclosures – ASU 2009-17 et alo Redefines primary beneficiary in qualitative

manner The Power to direct the activities of the VIE

that significantly impacts the VIE’s economic performance“Power” relates to management, not

governance

2012 ACCOUNTING UPDATE

Where have all the VIE’s gone?

35

• Improving VIE disclosureso Redefines primary beneficiary in qualitative

manner (cont) The obligation to absorb losses or receive

benefits that could be potentially significant to the VIE

Also assess whether the PB has implicit financial responsibility to ensure the VIE operates as designed

Requires ongoing re-assessment of whether entity is PB of VIE

2012 ACCOUNTING UPDATE

Where have all the VIE’s gone?

36

• Related party “trap” still in playo“… in determining the primary

beneficiary, a variable interest holder will consider its related party interests as its own”

oTie Breaker rule says the Primary Beneficiary is the entity that is most closely associated with the VIE

2012 ACCOUNTING UPDATE

Where have all the VIE’s gone?

37

• Disclosures about cash flows, financial position and performanceo How they are accounted foro Fair values in tabular formo Balance sheet and income statement

locationso Notional amounts of derivative instruments

2012 ACCOUNTING UPDATE

Where have all the VIE’s gone?

38

• Disclosures about cash flows, financial position and performanceo How they affect financial position, financial

performance and cash flows Existence and nature of contingent features Timing and likelihood Cash effects Credit risk related contingencies Potential effect on liquidity

o Additional disclosures required to increase transparency of PB’s involvement with VIEs

2012 ACCOUNTING UPDATE

Where have all the VIE’s gone?

39

• The Devil Is In The Detailso Disclosures significantly exceeds those for

entities consolidated because of majority ownership

o Determining whether an entity is a VIE is a complex process and should not be undertaken “off the top of your head”

o Determining who is the PB is a complex process and …

• Effective for years ending after 11-15-10, and interim periods within that year

2012 ACCOUNTING UPDATE

When is Revenue “Earned”?

40

• Overarching Principles in Current Standardso Persuasive evidence of an arrangement

exists Documentation required

o The fee is fixed or determinable No clear definition, but several examples Overarching principle – Cannot be

dependent on future events

2012 ACCOUNTING UPDATE

When is Revenue “Earned”?

41

• Overarching Principles in Current Standardso Delivery or performance has occurred

Identifiable deliverables Seller has fulfilled obligation Proportional performance deliverables

recognizedo Collectability is reasonably assured

Determined at time of revenue recognition Factors for determining bad debt reserves

are applicable

2012 ACCOUNTING UPDATE

When is Revenue “Earned”?

42

• Revenue recognition; Milestone method (ASU 2010-17)o Applies only to R&D vendorso Applies to payments earned upon achievement

of milestoneso In the absence of specific relevant GAAP,

provides good accounting concepts for project-type services

2012 ACCOUNTING UPDATE

When is Revenue “Earned”?

43

• Revenue recognition; Revenue arrangements that include software (ASU 2009-14)o Changed prior GAAP for recognizing revenue

for sales of tangible products that include software essential to the functionality of the tangible product Clarifies what guidance should be used to

measure revenue for product and software, not when to recognize it

Includes revenue recognition for post-contract services and undelivered software

2012 ACCOUNTING UPDATE

When is Revenue “Earned”?

44

• Revenue recognition; Multiple deliverables (ASU 2009-13)o Divide arrangements into separate units and

recognize revenue based on relative selling prices

o Selling prices are determined using vendor-specific objective evidence

o Effective beginning after 6-15-2010

2012 ACCOUNTING UPDATE

When is Revenue “Earned”?

45

• Revenue recognition exposure drafto Uses “contract” basis

“Contract” is an understanding, and does not have to be in writing

Identify rights and obligations of contracts with customers

Determine transaction price(s) Allocate transaction price to performance

obligations Recognize revenue when performance

obligation is satisfied

2012 ACCOUNTING UPDATE

When is Revenue “Earned”?

46

• Revenue recognition exposure drafto Performance obligations

Single performance obligation if entity integrates goods or services into a single item

Accounted for as multiple performance obligations if pattern of transfer is different for different goods or services, and …Each good or service has a distinct

function

2012 ACCOUNTING UPDATE

When is Revenue “Earned”?

47

• Revenue recognition exposure drafto Measurement

Multiple obligations would be measured on basis of relative standalone selling prices of the goods or services

o Next steps Re-expose a revised draft (imminent) Comment period 60-90 days Final standard in summer 2012 Effective date periods after 12-15-??

2012 ACCOUNTING UPDATE

What is “Equity”?

48

• Financial Instruments with Characteristics of Equityo Basic ownership approach

Only the most residual claim would be equity Approach preferred by FASB Currently the approach used in International

Financial Reporting Standardso Ownership-Settlement approach

Adds Perpetual and Indirect Ownership Interests to Basic Ownership Interests in equity

2012 ACCOUNTING UPDATE

What is “Equity”?

49

• Financial Instruments with Characteristics of Equityo Reassessed Expected Outcomes approach

Would include instruments that change in fair value with changes in Basic Ownership instruments

2012 ACCOUNTING UPDATE

Pot Pourri

50

• Loans in 401(k) plans (ASU 2010-25)o Participant loans in 401(k) plans are not

investments and will be carried at unpaid principal balance plus accrued interest

o Effective for 2010 financial statements

2012 ACCOUNTING UPDATE

Pot Pourri

51

• Disclosures about credit quality (ASU 2010-20)o Applies to financing receivables

Does not apply to trade receivables due in less than one year, or financing receivables carried at fair value

2012 ACCOUNTING UPDATE

Pot Pourri

52

• Disclosures about credit quality (ASU 2010-20)o Purpose is to improve user information about

credit quality Nature of credit risk inherent in portfolio How credit risk is analyzed and assessed in

determining the allowance for credit losses Changes, and their reasons, in allowances Many new disclosures

o Effective for issuers 12-15-10, and for non-issuers 12-15-11

2012 ACCOUNTING UPDATE

Pot Pourri

53

• Improving fair value disclosures (ASU 2010-06)o Users requested greater level of disaggregated

information and more robust disclosures Disclose separately amounts of significant

transfers in and out of Levels 1 and 2, including reasons

For Level 3, disclose separately information about purchases, sales, issuances and settlements (ie, gross, not net)

2012 ACCOUNTING UPDATE

Pot Pourri

54

• Improving fair value disclosures (ASU 2010-06)o Provide fair value measurement disclosures for

each class of assets and liabilities carried at fair value Recognizes that judgment is required –

consider user needso Disclosure of valuation technique for Level 2

increased Separately for “similar” vs “identical”

2012 ACCOUNTING UPDATE

Pot Pourri

55

• Additional Fair Value Disclosures – ASU 2011-04o Part of Convergence project – not many

changes, and they are not significanto Clarifies that blockage factor is not

appropriate, but control premium “may” be appropriate

2012 ACCOUNTING UPDATE

Pot Pourri

56

• Additional Fair Value Disclosureso Additional level 3 disclosures

Valuation process used Sensitivity information Fair value categories for items not

measured at fair value but for which fair value is disclosed

2012 ACCOUNTING UPDATE

Pot Pourri

57

• Consider user needs when preparing fair value disclosureso Creditor needs are different than investor

needs – cover botho Level 2 – comparable/active, or

identical/inactiveo Level 3 – Describe key assumptions and

estimates• Use a Great disclosure checklist

o FASB ASC 820-10-50; Fair Value Disclosures

2012 ACCOUNTING UPDATE

Pot Pourri

58

• Fair Value of Private Investment Partnerships (ASU 2009-12)o Applies to investments in entities that permit

redemption at specified times at net asset value determined using fair value accounting

o Provides guidance as to how to use reported net asset value in determining fair value

o Would be classified as Level 2; Identical security in inactive market Disclose observable and unobservable data

2012 ACCOUNTING UPDATE

Pot Pourri

59

• Other Comprehensive Income (ASU 2011-05)o Required to be on income statement or

separate statement Re-title Statement of Income to

Statement of Comprehensive Incomeo Effective years beginning after 12-15-2011

for publics, and 12-15-2012 for non-publicso Board has tweaked reclassification

adjustment provisions in ASU 2011-12

2012 ACCOUNTING UPDATE

Pot Pourri

60

• Some on Healthcare Entitieso Display and disclosure of revenue and bad

debts (ASU 2011-07)o Gross up malpractice insurance claims and

recoveries (2010-24)o Measuring charity care (at cost)-(2010-23)

2012 ACCOUNTING UPDATE

Pot Pourri

61

• More on financial instrumentso Disclosure of gross information about assets

and liabilities that have been offset (2011-11)o Credit quality of financing receivables (2010-

20)o Loan pool modifications (2010-18)o Troubled debt restructurings (2011-02)

2012 ACCOUNTING UPDATE

Pot Pourri

62

• A couple on goodwill and other intangibleso Making qualitative assessment of goodwill

impairment (ASU 2011-08) Annually consider whether it is more likely

than not that goodwill fair value is less than carrying amount

Negative change in economic conditionsNegative change in financial performance

2012 ACCOUNTING UPDATE

Pot Pourri

63

• A couple on goodwill and other intangibleso Making qualitative assessment … (cont)

Annually consider … (cont) Negative change in management,

personnel, customers, etc Others listed

o If qualitative assessment “passes”, no need to perform 2-step test

2012 ACCOUNTING UPDATE

Pot Pourri

64

• Goodwillo Testing goodwill impairment when investment

is negative (ASU 2010-28) When carrying value is negative, presumably

fair value exceeds carrying amount, so technically the impairment test is not called for

Revised Standard requires a Step 2 test of goodwill impairment, which may result in additional negative investment

Note previous discussion of ASU 2011-08

2012 ACCOUNTING UPDATE

Pot Pourri

65

• Complete listing of Accounting Standards Updates for 2012 – 2010 in Exhibit to slide deck

o 2012; None issued at 2/15/2012o 2011; # 01 – 12o 2010; # 01 – 29 o 2009; # 01 – 17

• Visit http://www.fasb.org/jsp/FASB/Page/SectionPage&cid=1176156316498

2012 ACCOUNTING UPDATE

In Conclusion…

• Monitor the FASB web site (www.fasb.org)

• Monitor the AICPA web site (www.aicpa.org)

• Call Chris Rouse at

Windham Brannon 404-898-2000

Bon Auditpetite! 66