ACCOUNTABILITY PERFORMANCE REPORTING …Accountability, performance reporting, comprehensive audit -...

381

A CCOUNTABILITY , P ERFORMANCE R EPORTING , C OMPREHENSIVE A UDIT - A N I NTEGRATED P ERSPECTIVE by G U Y L E C L E R C W. D AV I D M O Y N A G H J E A N -P I E R R E B O I S C L A I R H U G H R. H A N S O N

Transcript of ACCOUNTABILITY PERFORMANCE REPORTING …Accountability, performance reporting, comprehensive audit -...

ACCOUNTABILIT Y,PERFORMANCE

REPORTING,COMPREHENSIVE

AUDIT -AN INTE G RATED PERSPECTIVE

b y

G U Y L E C L E R C

W . D A V I D M O Y N A G H

J E A N - P I E R R E B O I S C L A I R

H U G H R . H A N S O N

Accountability, performance reporting, comprehensive audit - an integrated perspective

Copyright © 1996 CCAF-FCVI Inc.

All rights reserved. No part of this publication may be repro-duced, stored in a data base or retrieval system, or transmitted, inany form or by any means, electronic, mechanical, photocopying,recording, or otherwise, without the prior written permission ofthe publisher, CCAF-FCVI Inc.

Published byCCAF-FCVI Inc.55 Murray St., Suite 210Ottawa, CANADAK1N 5M3(613) 241-6713 Fax (613) 241-6900

ISBN 0-919557-47-3

Printed and bound in Canada.Design and layout by Paul Edwards Design. Print coordination by Poirier Litho.

This book is available in French under the title: Reddition de comptes, rapports sur la performance et vérification intégrée - une vue d’ensemble.Translation by Traduction Nicole Plamondon.

Canadian Cataloguing in Publication Data:

Main entry under title:Accountability, performance reporting, comprehensive

audit - an integrated perspective

Issued also in French under title: Reddition de comptes, rapports sur la performance et vérification intégrée - une vue d’ensembleIncludes bibliographical references and index.ISBN 0-919557-47-3

1. Auditing. 2. Organizational Effectiveness.I. CCAF-FCVI Inc.

HF5667.A26 1996 657’.45 C96-900071-S

TABLE OF CONTENTS

PART I. ACCOUNTABILITY.................................................................................1INTRODUCTION .............................................................................................................................3

SECTION 1. ACCOUNTABILITY’S CONTEXT—GOVERNANCE ............................................7

CHAPTER 1. GOVERNANCE—DEFINITIONS AND ISSUES ...............................................................8GOVERNANCE VERSUS MANAGEMENT ........................................................................9GOVERNANCE STRUCTURES......................................................................................10SOME RELATED CONCEPTS........................................................................................10DEMOCRACY .............................................................................................................12THE NATURE OF A CONSTITUTION...........................................................................13ESSENTIAL CHARACTERISTICS OF GOOD GOVERNANCE............................................14

CHAPTER 2. GOVERNANCE IN CANADA.......................................................................................15THE FORM OF GOVERNMENT IN CANADA................................................................15THE ROLE OF ELECTED REPRESENTATIVES................................................................21INFLUENCES ON POLICY IN A DEMOCRACY...............................................................22SOME IMPLICATIONS OF FEDERALISM .......................................................................25GOVERNMENT IN OTHER COUNTRIES ......................................................................26PRIVATE SECTOR GOVERNANCE ................................................................................27GOOD GOVERNANCE — A COMMON GOAL..............................................................31

CHAPTER 3. THE LANGUAGE OF GOVERNANCE AND ACCOUNTABILITY.....................................33VOCABULARY AND TERMINOLOGY ............................................................................33RULES AND DISCRETION ...........................................................................................33DISCRETIONARY POWERS ..........................................................................................35BUREAUCRATIZATION................................................................................................35INDEPENDENCE.........................................................................................................36NEUTRALITY..............................................................................................................38AUTONOMY...............................................................................................................39SUBSIDIARITY ............................................................................................................40STEWARDSHIP............................................................................................................40VICARIOUS RESPONSIBILITY ......................................................................................41MANAGEMENT AND ADMINISTRATION .....................................................................41

SECTION 2. ACCOUNTABILITY—ISSUES & PRACTICE.....................................................43

CHAPTER 4. THE MEANING OF ACCOUNTABILITY ......................................................................44ACCOUNTABILITY DEFINED.......................................................................................44ACCOUNTABILITY—MANY CONTEXTS, MANY FORMULATIONS .................................44THE ROOT OF ACCOUNTABILITY...............................................................................47DEMONSTRATING ACCOUNTABILITY.........................................................................50EXTERNAL INDUCEMENT FOR ACCOUNTABILITY ......................................................50THE ENVIRONMENT FOR ACCOUNTABILITY..............................................................54AUTONOMY AND ACCOUNTABILITY ..........................................................................56DIMENSIONS OF ACCOUNTABILITY ...........................................................................57IN SUMMARY .............................................................................................................59

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E

CHAPTER 5. ACCOUNTABILITY OBLIGATIONS..............................................................................61THE TRADITIONAL VIEW...........................................................................................62THE DEBATE..............................................................................................................62ACCOUNTABILITY OF PUBLIC SERVANTS....................................................................66

CHAPTER 6. ACCOUNTABILITY IN CERTAIN OTHER CIRCUMSTANCES ........................................71ACCOUNTABILITY IN THE PRIVATE SECTOR...............................................................71DIFFERENCE BETWEEN PRIVATE- AND PUBLIC-SECTOR ACCOUNTABILITY ................71GOVERNMENT IN AND OUT OF BUSINESS.................................................................71ACCOUNTABILITY IN A MONOPOLY...........................................................................73THE PRIVATE NONPROFIT SECTOR............................................................................73

CHAPTER 7. CONTROL AND CONTROLS......................................................................................75CONTROL..................................................................................................................75CONTROL AND THE CHANGE IN ORGANIZATIONAL CULTURE..................................75TWO MODELS OF MANAGEMENT..............................................................................76IMPROPERLY CONTROLLED DELEGATION—STREET-LEVEL BUREAUCRATS.................77DELEGATION AND THE DIFFICULTY OF “LETTING GO” ............................................79

CONCLUSION ...............................................................................................................................80KNOW THE BUSINESS ................................................................................................80ORGANIZATIONAL KNOWLEDGE CHECKLIST.............................................................81

APPENDIX. ..................................................................................................................................84A CASE OF CHANGE IN MANAGERIAL CULTURE ......................................................84INCREASED MINISTERIAL AUTHORITY AND ACCOUNTABILITY.................................84PUBLIC SERVICE 2000 ...............................................................................................88SHARED MANAGEMENT AGENDA (SMA)..................................................................89WAS CONTROL LOST?................................................................................................91THE TRANSITION CONTINUES ..................................................................................92THE MANAGERIAL REVOLUTION: CULTURAL AND PROCEDURAL ..............................92

PART II—PERFORMANCE REPORTING ............................................................95

INTRODUCTION ...........................................................................................................................97

SECTION 1. THE THEORETICAL BASIS FOR PERFORMANCE REPORTING......................103

CHAPTER 8. EXISTING REPORTING PRACTICES .........................................................................104PUBLIC-SECTOR REPORTING MECHANISMS .............................................................104PRIVATE-SECTOR PERFORMANCE REPORTING .........................................................109SOME RECENT INITIATIVES IN REPORTING ON PERFORMANCE...............................110

CHAPTER 9. CONCEPTUAL ISSUES IN PERFORMANCE REPORTING............................................116THE CENTRAL ISSUES ..............................................................................................116PERFORMANCE AND EFFECTIVENESS.......................................................................116VALUE FOR MONEY .................................................................................................116THE EFFECTIVENESS DILEMMA ...............................................................................120EFFECTIVENESS AND THE ACHIEVEMENT OF GOALS...............................................121SOME APPROACHES TO EFFECTIVENESS...................................................................124LISTS OF ATTRIBUTES OF EFFECTIVENESS ...............................................................125SENSITIVITY OF THE NOTION OF EFFECTIVENESS...................................................129CHARACTERISTICS OF GOOD REPORTING...............................................................130ABOUT REPRESENTATIONS ......................................................................................132

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E

SECTION 2. PRINCIPLES AND GUIDELINES FOR PERFORMANCE REPORTING................135

CHAPTER 10. AN EFFECTIVENESS-REPORTING FRAMEWORK ....................................................136BACKGROUND .........................................................................................................136MANAGEMENT REPRESENTATIONS ..........................................................................137ATTRIBUTES OF EFFECTIVENESS..............................................................................138GUIDELINES FOR MAKING REPRESENTATIONS ON THE ATTRIBUTES.......................145NEED FOR EXTERNAL REVIEW.................................................................................148

CHAPTER 11. PRELIMINARY CONSIDERATIONS IN REPORTING EFFECTIVENESS........................150OVERALL PERSPECTIVE............................................................................................150DETERMINING IF THE ORGANIZATION IS READY TO PROCEED...............................151SETTING REALISTIC EXPECTATIONS.........................................................................153DECIDING WHERE TO FOCUS INITIAL EFFORTS ......................................................153DECIDING WHO OUGHT TO PARTICIPATE...............................................................154MANAGING THE OVERALL PROCESS ........................................................................158DEVELOPING MANAGEMENT REPRESENTATIONS.....................................................159DETERMINING WHERE AND WHEN TO REPORT REPRESENTATIONS........................160

CHAPTER 12. IMPLEMENTING AN EFFECTIVENESS-REPORTING PROJECT .................................162OVERVIEW OF THE PROCESS ...................................................................................162PHASE I—INITIAL ENGAGEMENT OF THE CEO/SENIOR MANAGEMENT.................163PHASE II—DECIDING WHERE TO FOCUS AND HOW TO PROCEED .........................172PHASE III—PREPARING FOR AND BEGINNING IMPLEMENTATION ..........................175PHASE IV—REFINING THE INITIAL MANAGEMENT REPRESENTATIONS ..................187PHASE V—WRITING THE MANAGEMENT-REPRESENTATIONS REPORT....................190PHASE VI—TABLING THE REPORT WITH THE GOVERNING BODY..........................191PHASE VII—AUDIT OF REPRESENTATIONS ON EFFECTIVENESS..............................192

CONCLUSION .............................................................................................................................193ELEMENTS OF A GOOD PERFORMANCE-MANAGEMENT SYSTEM..............................193ELEMENTS OF GOOD PERFORMANCE MEASURES.....................................................195

APPENDIX — EXHIBITS ..............................................................................................................196EXHIBIT A ...............................................................................................................196EXHIBIT B ...............................................................................................................197EXHIBIT C...............................................................................................................200EXHIBIT D ..............................................................................................................203EXHIBIT E ...............................................................................................................209EXHIBIT F ...............................................................................................................210EXHIBIT G...............................................................................................................213

PART III COMPREHENSIVE AUDIT .................................................................217

INTRODUCTION .........................................................................................................................219

SECTION 1. BACKGROUND............................................................................................221

CHAPTER 13—UNDERSTANDING AUDIT...................................................................................222RELATIONSHIP TO ACCOUNTING ............................................................................222DEFINITIONS OF AUDIT ..........................................................................................224CHARACTERISTICS OF AUDIT ..................................................................................224

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E

CHAPTER 14—UNDERSTANDING COMPREHENSIVE AUDIT ......................................................226HISTORICAL DEVELOPMENT ...................................................................................226THE COMPREHENSIVE AUDIT CONCEPT .................................................................228NON-AUDIT FORMS OF PRACTICE...........................................................................232

CHAPTER 15—THREE APPROACHES TO COMPREHENSIVE AUDIT ............................................234AN EVOLVING CONCEPT .........................................................................................234AUDIT REPORTING ON MANAGEMENT SYSTEMS AND PRACTICES ...........................236AUDIT ATTESTATION TO MANAGEMENT REPRESENTATIONS ON PERFORMANCE ....237AUDIT REPORTING ON PERFORMANCE ...................................................................241

SECTION 2. GENERAL CONSIDERATIONS ......................................................................243

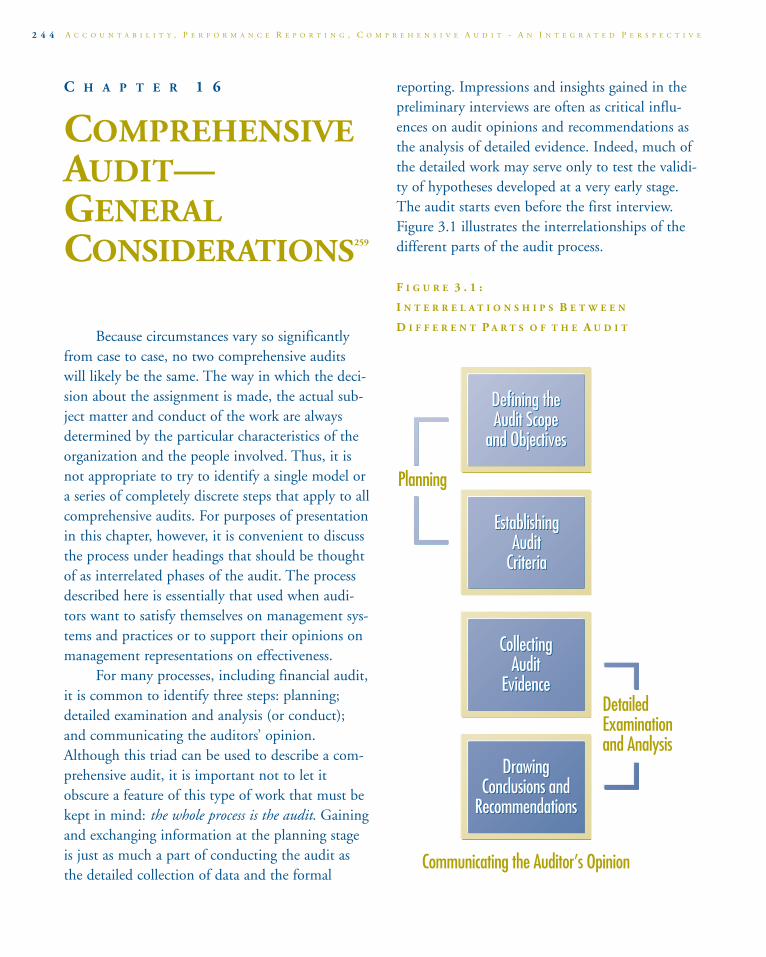

CHAPTER 16—COMPREHENSIVE AUDIT—GENERAL CONSIDERATIONS ...................................244THREE KEY VARIABLES.............................................................................................245FOCUS OF EXAMINATIONS.......................................................................................247DECIDING THE SUBJECT FOR AUDIT.......................................................................248

SECTION 3. COMPREHENSIVE AUDIT PRACTICE...........................................................251

CHAPTER 17—CONDUCTING COMPREHENSIVE AUDITS ..........................................................252PLANNING THE AUDIT ............................................................................................252THE CONDUCT PHASE ............................................................................................262THE COMPREHENSIVE AUDIT REPORT ....................................................................267

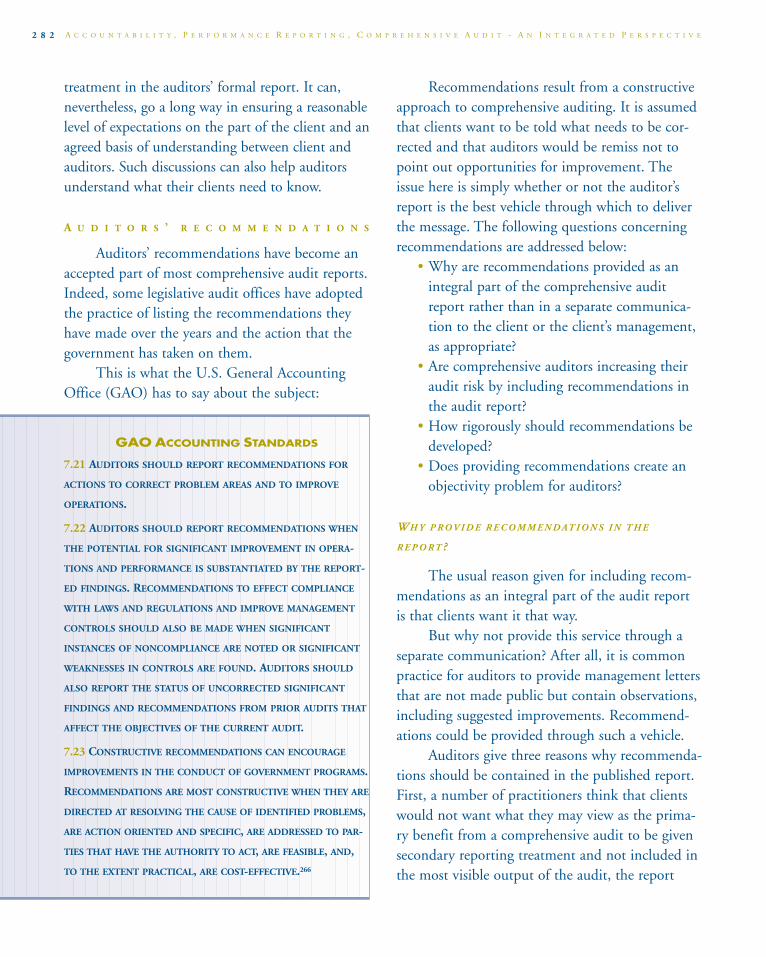

CHAPTER 18—COMPREHENSIVE AUDIT—REPORTING ISSUES..................................................271INTRODUCTION ......................................................................................................271SCOPE......................................................................................................................271ASSURANCE .............................................................................................................271SIGNIFICANCE .........................................................................................................276AUDITORS’ RECOMMENDATIONS ............................................................................282FAIR AND BALANCED REPORTING ...........................................................................284

CHAPTER 19—AUDIT CRITERIA ................................................................................................286WHAT ARE AUDIT CRITERIA?...................................................................................286SUITABILITY OF CRITERIA........................................................................................287USING AUDIT CRITERIA...........................................................................................288SOURCES OF AUDIT CRITERIA .................................................................................289

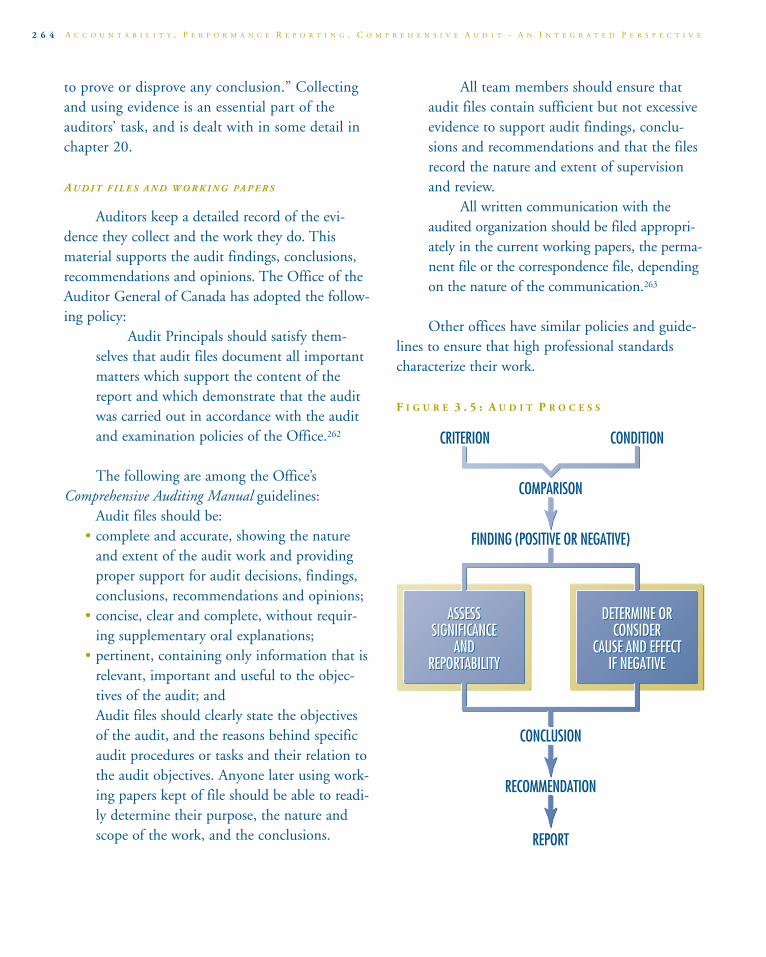

CHAPTER 20—EVIDENCE ..........................................................................................................291WHAT IS EVIDENCE? ...............................................................................................291STANDARDS OF VFM-RELATED AUDIT EVIDENCE...................................................291EVIDENCE FACTORS TO CONSIDER IN PLANNING ...................................................293RELIANCE AS A FORM OF EVIDENCE .......................................................................293METHODS OF GATHERING AUDIT EVIDENCE..........................................................295AUDIT PROCESS AND EVIDENCE..............................................................................295

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E

SECTION 4. OTHER KEY CONSIDERATIONS..........................................................297

CHAPTER 21—INTERNAL AUDIT ...............................................................................................298WHAT IS INTERNAL AUDITING? ..............................................................................298CLIENT FOR INTERNAL AUDITING ..........................................................................299SENIOR MANAGEMENT SUPPORT.............................................................................300LEADERSHIP AND STAFFING ....................................................................................301ORGANIZATIONAL ARRANGEMENTS FOR INTERNAL AUDITING .............................302INTERNAL AUDIT REPORTS......................................................................................310

CHAPTER 22—OTHER REVIEW PROCESSES—COORDINATION & RELIANCE............................312COORDINATION AND COOPERATION......................................................................312RELIANCE ................................................................................................................313PLANNING FOR RELIANCE .......................................................................................313DEVELOPING A TENTATIVE STRATEGY FOR RELIANCE.............................................319OPTIMIZING PLANNED RELIANCE POTENTIAL ........................................................320TIMING ...................................................................................................................321CHANGES IN TENTATIVE RELIANCE STRATEGIES .....................................................322PLACING RELIANCE .................................................................................................322REPORTING ON RELIANCE.......................................................................................324OTHER FORMS OF REVIEW......................................................................................325

CHAPTER 23—STANDARDS AND QUALITY ASSURANCE.............................................................332VALUE-FOR-MONEY AUDIT STANDARDS ..................................................................332QUALITY ASSURANCE ..............................................................................................340AUDIT MANUALS .....................................................................................................340REVIEW PROCESSES .................................................................................................340STAFFING.................................................................................................................342

CHAPTER 24—PROFILE OF THE COMPREHENSIVE AUDITOR ....................................................343COMPREHENSIVE AUDIT LEADERS...........................................................................344MANAGEMENT FUNCTIONS AND SYSTEMS..............................................................345THE AUDIT TEAM....................................................................................................347

CONCLUSION .............................................................................................................................349INDEX.........................................................................................................................................352

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E

HARRY ALLEN, GEORGE ANDERSON, ROBERT ANDERSON, RODNEY ANDERSON, ALAN ANDREWS, DOUGLAS ARCHER, JIM ARMSTRONG,PETER ARMSTRONG, MARTA ARNALDO, ROLAND ARPIN, PHILLIP ASPINALL, JOHN ASTLE, JOHN ATKINSON, JOYCE BAILEY, NATALIE BALKO,ALAN BARNARD, DAVID BARNES, PETER BARNES, MARIA BARRADOS, DOUGLAS BARRINGTON, JOHN BART, WILLIAM BARTON, GILLESBÉDARD, CLAUDE BÉGIN, KENNETH BELBECK, CAROL BELLRINGER, BRUCE BENNETT, JEAN BERNARD, LIBA BERRY, HUGUETTEBERTRAND, DAVID BIGNEY, BOB BLACK, RALPH BLACK, ANDY BOEHM, JEAN-PIERRE BOISCLAIR, SHIRLEY BOISCLAIR, ANDRÉ BOLDUC,HUGH BOLTON, DAVID BONHAM, WILLIAM BRADSHAW, JOHN BRADT, FRANCINE BRAZEAU, GUY BRETON, ROBERT BROMLEY, JAMESBROPHY, DONALD BROWN, NEIL BROWN, JUDY BURNS, RICHARD BUSKI, BRIAN CAINE, JAMES CAIRNCROSS, DOUG CAMERON, FRANCESCAMERON, HEATHER CAMPBELL, DENIS CARO, MARCEL CARON, CHARLES CARRIERE, JOHN CARSON, CLAUDE CARTER, EDWARD CASE, MARLENE CATTERALL, HOWARDC H A N , M I K E C H A R L T O N , R H É A L C H A T E L A I N , WA R R E NCH I P PI N D A L E, GA I L CH R I S T I E ,IAN CLARK, TOM CLOSSON, JIMC LU F F, C A RO L CO D O R I , J O H NC O L E , B A R R Y C O O P E R S M I T H ,PE N I N A CO O PE R S M I T H, BR I A NC O R B I S H L E Y, PAU L C O R M I E R ,KAREN CORNELIUS, CATHERINECORNELL, JEAN COWPERTHWAITE,R O B E R T C U M M I N G S , J A M E SC U R R I E , J O H N C U R R I E , J A M E SC U T T , K E I T H D A L G L I S H ,FRANCINE DALPHOND, THOMASDALTON, ALEXANDER DAVIDSON,CATHIE DAVIS, COLIN DEACON,DENIS DESAUTELS, PETER DEY,G A R Y D I C K I N S O N , E L W Y ND I C K S O N , A L A N D I LW O R T H ,M A R I L Y N D O L E N K O , E N D R ED O L H A I , E L I Z A B E T HD O M B R O S K I E , B I L L D R O V E R ,R AY M O N D D U B O I S , A L I S TA I RDUFF, VIVIANE DUNN, GORDONDUNNET, KENNETH DYE, WALLYEAMER, PAUL EDWARDS, ROBERTAELLIS, ROBERT ELTON, BRENDAE P R I L E , W I L L I A M FA R L I N G E R ,ROBIN FARQUHAR, TOM FARRELL,LYNN FAUCHER, JUDY FERGUSON,MARY FERGUSON-PARÉ, PENELOPEF I L I A T R A U LT- M A C D O N A L D ,

E L I Z A B E T H F L E E T , C E C I LFLEMING, JEAN-PIERRE FORTIN,PAUL FORTUGNO, C.E.S. FRANKS,ALISTAIR FRASER, RONALD GAGE,RICHARD GAGNÉ, IDA GARRETT,DONALD GASS, YVAN GAUDETTE,Y V E S G AU T H I E R , H E L E N G AY,F R A N K G E L I N , M U R R AY G I L L ,ALAN GILLMORE, FRED GINGELL,R O B E R T G I R O U X , J E A N - PA U LGOBEIL, ROBERT GOBEIL, BERNIEG O R M A N , L O U I S G O S S E L I N ,MA RC E L GO U L E T, TR E N T GOW,D O N A L D G R A C E Y, K AT H E R I N EG R A H A M , A L A N G R A T I A S ,C H R I S T O P H E R G R E E N , J O A NGREEN, PETER GREGORY, RONALDG R E Y, R O D G E R G U I N N , R O YG U N N , K E N N E T H G U N N I N G ,ERNEST HALL, LYLE HANDFIELD,J A C K H A N N A , J O H N H A N N A ,H U G H H A N S O N , W I L L I A MH A R K E R , M A RY- J A N E H A R R I S ,RICHARD HARRIS, JIM HAWKES,JOHN HAYES, ROBERT HAYWARD,B R Y A N H E L D , P E T E R H E L D ,JACQUES HENRICHON, STEPHENHE R B E RT, RAY HE S S I O N, JO H NHICKMAN, JANET HOFSTETTER,J O H N H O L D S T O C K , G O R D O NHUDSON, JOE HUDSON, FRANKH U G H E S , RO N H U N T I N G T O N ,CA RO L I N E HU P É, JE A N HU R S T,

OLE INGSTRUP, FRED JAAKSON, JOHN JACKSON, CRAIG JAMES, JOCK JARDINE, KATHERINE JAST, WARREN JOHNSON, DIANE JOLY,FRANÇOIS JOLY, MALCOLM JORDAN, GUYLAINE JUTEAU, TIM KAPTEIN, JOHN KELLY, RONALD KIGGINS, JOSEPH KIRCHNER, ANNEKIRKALDY, PAUL LABBÉ, HUGUETTE LABELLE, FRANÇOIS LACASSE, ROGER LACHANCE, PATRICK LAFFERTY, JEAN-GUY LALIBERTÉ, ROBERTLALONDE, JACQUES LAMONDE, CLAUDE LAMOUREUX, MARVIN LAMOUREUX, JEAN-MARIE LAMPRON, ERIC LANDE, WILLIAM LANGDON,SPENCER LANTHIER, GÉRARD LAROSE, GASTON LATULIPPE, VICTOIN LAURIN, LUC LAVOIE, GUY LECLERC, GUY LEFEBVRE, KENLEISHMAN, JULIAN LEMIEUX, DAVID LEVINE, DOUGLAS LEWIS, JAMES LIBBEY, FULVIO LIMONGELLI, ALWYN LLOYD, ROBERT LORD, CAROLASHFIELD LOUGHREY, JOHN LYNCH, NANCY LYNCH, HOWARD LYONS, ANDREW MACDONALD, DUNBAR MACDONALD, LYMAN MACINNIS,MICHAEL MACKENZIE, DAVID MACKINNON, JANICE MACKINNON, R.D. MACLEAN, HARVEY MACLEOD, ELIZABETH MACRAE, PAUL-ANDRÉ MALO, CLAYTON MANNESS, LORNA MARSDEN, ELIZABETH MARSHALL, BRIAN MARSON, ALAN MARTIN, GUY MARTIN, RITAMATHERS, SUNNY MATHIESON, LES MCADAMS, MARY MCBRIDE, HENRY MCCANDLESS, TOM MCCANN, JAMES MCCRINDELL, NEVINMCDIARMID, LEONARD MCGIMPSEY, JOSEPH MCGRATH, MICHAEL MCLAUGHLIN, DORIS MCMULLAN, EDWARD MCNAMARA, HUGHMCROBERTS, GILES MEIKLE, LARRY MEYERS, JIM MILES, RICHARD MINEAU, NICK MISHCHENKO, MARCEL MIVILLE-DÉCHÊNE,ROLLANDE MONTSION, DONALD MOORS, ELAINE MORASH, RAYMOND MORCEL, GEORGE MORFITT, ERMA MORRISON, DAVID MOYNAGH,DAVID MUIR, TERESA MURPHY, WAYNE MURPHY, BEV ANN MURRAY, MELISSA NAPIER-ANDREWS, NIGEL NAPIER-ANDREWS, KARENNELSON, EUGENE NESMITH, EDWARD NETTEN, DAVID NEUMANN, PETER NEWDICK, CLIFFORD NORDAL, PAUL NORTHOVER, ELAINE ORR,JAMES OTTERMAN, JOHN PALMER, RICHARD PALMER, PIERRE-ANDRÉ PARÉ, GARY PEALL, LEWIS PERINBAM, ERIK PETERS, JEAN PICARD,LAURENT PICARD, LISE PISTONO, NICOLE PLAMONDON, BERNIE POIRIER, JOYCE POTTER, COLIN POTTS, ED POWELL, ERROL PRICE,DOROTHY PRINGLE, ROBERT PROSSER, ROSS QUANE, MICHEL RACINE, WILLIAM RADBURN, PAUL RAMSEY, ANNE RANDELL, DAVIDRATTRAY, MICHAEL RAYNER, ANGUS REE, PATRICK REID, PAUL REINHART, BRIAN REINKE, STANLEY REMPLE, ROBERT RENNIE, ARTHURROBERGE, PAUL ROBINSON, RONALD ROBINSON, LUCIE ROCHETTE, DOUGLAS ROGERS, HARRY ROGERS, LAWRENCE ROSEN, EDWARDROWE, TERRY RUSSELL, LEONARD RUTMAN, VINOD SAGHAL, ALINE SAINT-AMAND, DONALD SALMON, ROY SALMON, KARN SANDY,DONALD SCOTT, NORMAN SCOTT, RONA SHAFFRAN, JOHN SHARPE, PETER SIMEONI, SONJA SINCLAIR, HAR SINGH, JON SINGLETON,ALISTAIR SKINNER, WILLIAM SLOAN, JACK SMITH, STUART SMITH, KIMBERLEY SPEEK, GEORGE STEPHENSON, ESTHER STERN, KENNETHSTEVENSON, MARGARET STOCKTON, WAYNE STREILOFF, CLAUDE TAYLOR, GAIL TAYLOR, ROBERT TAYLOR, JOHN THOMPSON, HUGH TIDBY,MARTHA TORY, SEYMOUR TRACHIMOVSKY, ALEC TRAFFORD, GUY TRUDEL, PETER TRUEMAN, ROBERT TURNBULL, NATALIE UMIASTOWSKI,PETER VALENTINE, PETER VAUGHAN, CHARLES VINCENT, DIANA VOSSELER, EDWARD WAITZER, ROSS WALKER, JOSIE WALSH, RONALDWARME, JOHN WATSON, SUSAN WATSON, JAMES WAUGH, BARRIE WEBB, LINDA WEEKS, MICHAEL WEIR, SUZANNE WERHAR-SEEBACH,DAVID WHITE , STAN WHITELEY, NICOLE WIECZOREK, PETER WILEY, ALAN WILLIS, GEOFFREY WILSON, JOHN WILSON, PETER WILSON,ALAN WINBERG, ANDREW WINGATE, DOUGLAS WOOD, BRENT WORTMAN, JAMES WRIGHT, GEORGINA WYMAN, DONALD YEOMANS,CARMAN YOUNG, DON YOUNG, DONALD M. YOUNG, DAVID ZUSSMAN, AND THE 119 CCAF INTERNATIONAL GRADUATE FELLOWS.

THIS BOOK IS DEDICATED TO:

THE GENIUS AND MEMORY OF THE LATE

J A M E S J . M A C D O N E L L

CCAF’S FOUNDING CHAIRMAN (1980-83),

WHOSE INTELLECT AND ENERGY CREATED THE VISION

AND POINTED THE WAY,

a n d

G O R D O N H . C O W P E R T H W A I T E

CCAF CHAIRMAN (1983-93),

WHOSE DISTINGUISHED LEADERSHIP SUSTAINED THE

VISION AND ADDED TO IT NEW DIMENSION AND

SIGNIFICANCE,

a n d

ALL THOSE WHO HAVE WORKED TO CREATE

THE BODY OF KNOWLEDGE AND EXPERIENCE

WHICH THIS BOOK REFLECTS.

INTRODUCTION

Students of comprehensive auditing and prac-titioners or clients newly engaged in this area ofaudit practice are faced with a formidable chal-lenge.

Existing literature on comprehensive audit-ing is both diverse and fragmented, oftenapproaching the subject in terms of a specificaspect of practice—or in relation to a specifictime period—or through the perspective, policiesand procedures of a specific audit organization.Rarely has the literature ventured into an exami-nation of the accountability context within whichcomprehensive auditors operate and the perspec-tives and roles of other key stakeholders to theaccountability process—that is, those who governand manage our institutions. Indeed, many gener-al texts on auditing start from the assumptionthat the practitioner already has a knowledge ofthis accountability environment.

Thus, those who are new to comprehensiveauditing face the difficult task of having tosearch far, wide and long for basic informationand discussion on such matters. The onus hasbeen on them to identify and envelop all thesesources of knowledge and practice, sort out thecontemporary from the passé, fill in the blanks,and somehow pull it all together and make theright connections.

This book seeks to remedy this problem. Itmakes no assumption that readers already possess athorough grasp of the subject of accountability andrelated reporting principles. Instead, it deals withthese matters extensively. It provides readers withthe basic concepts, frameworks, tools and practiceguidelines they need to begin their learning orcareers in the area of comprehensive auditing. It is,however, more than a collection of pieces of

knowledge and experience. The structure and con-tent of this book reflect an important underlyingphilosophy and perspective. Simply stated, the phi-losophy is this: the defining role of audit is to servean accountability relationship, and thus, to trulyunderstand comprehensive auditing one must lookbeyond the borders of technical practice. It isessential to be knowledgeable about the broaderaccountability context and the roles and perspec-tives of those who operate within it. Having suchknowledge permits practitioners to identify theaudit approaches that will add the greatest value inthe circumstances, assess the implications of suchapproaches for the actions of other key stakehold-ers in the accountability process and explain theconsequences.

In this respect, this book is an extension ofCCAF itself. The foundation’s perspective is that ifaccountability is going to work properly, both par-ties to the accountability relationship—governingbodies and management—and the auditor whoserves this accountability relationship, play impor-tant and interdependent roles. The research andeducation work of CCAF—supported by theefforts of its members—is designed to help allthree parties achieve their mutual interest inimproving performance and accountability.

The book is divided into three parts. Part Ideals with the subject of accountability. It takes thereader through a wide-ranging and thoughtfulexamination of underlying theory, concepts andprinciples, and it connects these matters to con-temporary thinking and practice in the areas ofgovernance and management. We felt compelled todevelop this material since, to be well-positioned topractise comprehensive auditing, the practitionermust first acquire a thorough knowledge of thebusiness, an essential aspect of which is theaccountability environment. The discussion thatPart I gives to these issues is, we believe, unique inscope and character.

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E I

Part II focuses on performance reporting. Itprovides an overview of existing reporting practicesin the public and private sectors, noting a numberof recent initiatives in Canada and globally. Itmakes the case that concepts like performance andeffectiveness should be viewed as multidimension-al, arguing that this is necessary in order torespond to the reality of today’s accountability anddecision-making environment. Ideally, it is man-agement, not the auditor, that is in the best posi-tion to report (make representations) on the per-formance or effectiveness of the organization. Andif management does take on this responsibility,then the auditor plays a key role in providingassurance to the governing body (those to whommanagement reports) about the fairness and com-pleteness of the information management has pro-vided. Part II describes a framework of twelveattributes that is useful as a basis for such perfor-mance reporting. Drawing on actual practice inapplying this framework, key considerations arediscussed and a strategy for implementation is sug-gested. Audit practitioners need to have a thoroughappreciation of such performance reporting con-cepts and strategies if they are to conduct theirassurance role or, possibly, if they are called uponto provide such information to the governing bodydirectly, in the absence of management taking onthis reporting responsibility.

Part III provides an extensive review of com-prehensive audit theory and practice. It examinesseveral basic factors that influence the nature of theaudit process and product. Three approaches ormodels of comprehensive auditing, and relatedconsiderations and implications, are also discussed.Most important for readers to know is that com-prehensive audit is not a one-size-fits-all proposi-tion. Moreover, what these different approachesentail, and how they are explained and implement-ed, is very much linked to matters discussed in ear-lier parts of the book. Part III also provides an

overview of the issues and factors practitionersneed to keep in mind, and the methods theyemploy, in conducting a comprehensive audit.Several key professional practice issues are given in-depth treatment, among them, reporting, audit cri-teria and evidence, existing standards of practiceand quality assurance. The links between compre-hensive audit and internal audit are also examined.

All three parts of the book emphasize thatthere is no universal template or panacea. There arechoices. What the book seeks to do is provide read-ers with a basic understanding of what these choic-es are and how they are interconnected. It gives thereader a starting point and set of considerationsfrom which to assess the relative merits of thesechoices in the circumstances concerned. And itsuggests frameworks and strategies that can behelpful to the practitioner in engaging those whogovern and manage the enterprise and, ultimately,in implementing the decisions that result from thisprocess.

Educators in the areas of management, publicadministration and audit will find this book help-ful as a basic reference text around which to devel-op a program of study for their students. Moreexperienced comprehensive auditors will also findaspects of it useful—in reinforcing existingapproaches, and perhaps in other ways, by addingnew ideas and perspectives to their work.

This textbook is based on almost two decadesof practice in the field of comprehensive auditing.It flows from the thinking and experience of sever-al dozens of leading practitioners and researchers.It is the product of four individuals. First to men-tion is Guy Leclerc, former Deputy ComptrollerGeneral of Canada and for two years a researchassociate with CCAF. His efforts were joined bythose of W. David Moynagh, CCAF’s director ofresearch and Jean-Pierre Boisclair, the foundation’spresident. Hugh R. Hanson played a key role aswriter and as editor-in-chief ensuring that all the

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V EI I

pieces fit together. Liba Berry copyedited the book,Nicole Plamondon translated it into French, andSuzanne Seebach, Director, Operations &Communications, coordinated production andpublication arrangements. All the members ofCCAF’s secretariat played an important supportingrole in the development of this textbook. Withoutthe efforts of all these people, this project wouldnot have been possible.

A senior advisory panel was also establishedto provide strategic advice on a number of impor-tant policy issues relating to the focus of the bookand the development of key positions taken withinit. Comprising this panel were: Guy Breton,Auditor General of Quebec; Carol Bellringer,Provincial Auditor of Manitoba; Alexander M.Davidson, managing partner of Accounting andAuditing, Coopers & Lybrand; Denis Desautels,Auditor General of Canada; J. Colin Potts, partner,Deloitte & Touche; and Carman L. Young,Auditor of the Bank of Canada and former chair-man of the board of the Institute of InternalAuditors. The perspective and wisdom that thesedistinguished individuals brought to their rolemade a major contribution to this initiative.

The foundation’s board of governors andexecutive relied on CCAF’s Research Committee toprovide a rigourous professional challenge of con-tent. In exercising this role, all members of thecommittee played a critical part in the develop-ment of this volume. It has benefitted greatly fromtheir insights and suggestions.

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E I I I

P A R T I

ACCOUNTABILITY

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E 1

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E2

TO SERVE… AND PRESENT MY TRUE ACCOUNT…

J O H N M I L T O N , S O N N E T X V I ,

O N H I S B L I N D N E S S

P A R T 1

ACCOUNTABILITY

I N T R O D U C T I O N

Effective audit practice starts with a thoroughunderstanding of the context within which theclient and other key stakeholders operate. Thiscontext involves both the governance and manage-ment process, and the accountability arrangementsthat bind them together.

There has been much discussion aboutaccountability. Accountability implies responsibilityand public trust. The contemporary emphasis is oneverybody’s assuming responsibility and beingaccountable. Saying it, however, does not necessari-ly make it so. So many situations and circum-stances demand that public officials and people ingeneral be inspired by a sense of demonstrableresponsibility, and yet it is the lack of accountabili-ty or its inadequacy that drives the current dis-course on the subject. What characterizes the dis-cussion is that beyond the utterance of the word,there is so often little explanation as to what ismeant by it.

The word accountability evokes, to some, a setof lofty ideals intuitively and eminently sensible.To others, it is a normal expectation from anyoneentrusted with a responsibility. Still others see inthe word an element of confrontation.

The concept of accountability draws itsmeaning from a diverse body of literature in theareas of political science, religion, philosophy, soci-ology, management science, and public administra-tion. Each of these disciplines has somethingimportant to say on the subject. What is said, how-ever, often has a one-dimensional quality and is

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E 3

couched in the language of that discipline. Addedtogether, an almost surrealistic picture of the sub-ject of accountability emerges.

Trying to apply simple logic to bring thepieces into focus often leads to oversimplification.In much of the management literature, account-ability is assumed, relegated to the status of a tech-nical, bureaucratic process, and then quickly dis-patched in favour of other topics. Indeed, account-ability does include process elements, but it alsoinvolves a wide range of values, beliefs, attitudes,and behaviours, which are important determinantsof the nature and endurance of accountabilityarrangements.

Part I of this book focuses on the subject ofaccountability and related issues of governance andcontrol. While it identifies the key elements of theliterature, it also attempts to go deeper, explainingthe varied interpretations those concepts are givenand how they can be connected. For the practition-er to provide professional advice and products inthe service of improving accountability, it is impor-tant to understand the subtleties, and sometimesthe contradictions, associated with the subject andwith the perspectives and strategies that governors,management and other stakeholders bring to bearin their respective accountability relationships.

The context of accountability is governance,another term that has recently gained currency.Public sector—and corporate—governance isunder stress. Ineffective governance processes arebarriers to an organization’s effective performance.An efficient and accountable management cannotensure good performance if those responsible forthe direction of the organization cannot or will notperform their duties appropriately.

In dealing with the subject of governance inthis first section of the book the purpose is not toprovide a definitive and exhaustive explanation ofthe concept; rather, it is to impart a sense of theculture and characteristics of governance. It

attempts to discover basic principles that will helpthe reader understand the concept in various situa-tions.

Chapter 1 provides a general context, explor-ing conceptual issues, offering examples of philo-sophical approaches to the subject of governance.The second chapter deals with governance in boththe public and private sectors. It describes the gov-ernment structures in Canada to provide gover-nance and some of the constraints under whichgovernment operates. Reference is also made to theform of government in other countries. Chapter 2also explains the responsibilities of directors of cor-porations whose securities are issued to the public.

Chapter 3 examines some of the conceptssurrounding both governance and accountability,and explains various terms that are used in thatcontext.

Chapter 4 discusses the concept of account-ability. This general discussion tries to give thereader an understanding of the theory and some ofthe issues involved in establishing an effectiveaccountability regime.

Chapter 5 addresses the concept of ministeri-al responsibility and its diverse interpretations.These differing views introduce the reader to thesubtleties involved in issues of this nature.

Chapter 6 describes accountability in suchcontexts as the private sector, monopolies, andthe nonprofit sector. The differences among thevarious accountability regimes highlight thecomplexity of the application of the concept ofaccountability.

Control and controls are the subject ofChapter 7. Two polar approaches to control in anorganization are discussed, as well as the operationof controls in certain circumstances.

The conclusion of Part I stresses the impor-tance of knowledge of governance and accountabil-ity issues to audit practitioners and those involvedin performance reporting. It contains a checklist of

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E4

questions that the leader of a comprehensive oughtto be able to answer in respect of the client’s gover-nance and accountability arrangements.

The Appendix uses the government ofCanada to illustrate the complex issues surround-ing control and controls, and the major attemptsto improve its systems. This emphasis on theCanadian government is not meant to exalt it overother institutions; it is used as an illustration ofcontrol and controls because it is big, complex,well-documented, and is observed and commentedupon considerably more than others. And it con-tains all the dilemmas in accountability facingother institutions.

P A R T 1 – A C C O U N T A B I L I T Y 5

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E6

S E C T I O N 1

ACCOUNTABILITY’SCONTEXT–

GOVERNANCE

P A R T I . A C C O U N T A B I L I T Y 7

THE WORD GOVERNANCE COMES FROM THE GREEK WORD

KYBERNAN, TO DIRECT THE COURSE OF A SHIP, OR TO STEER

THE SHIP. THE ROMANS BORROWED THE WORD AS GUBERNARE

AND IT EVENTUALLY CROSSED THE ENGLISH CHANNEL AS

GOVERNOR, A STEERMAN OR A PILOT. IN FRENCH, THE

RUDDER OF A SHIP IS CALLED A GOUVERNAIL. IN THE

FAMILIAR LANGUAGE OF POLITICS IN THE UNITED STATES, ONE

HEARS OCCASIONAL REFERENCE TO “STEERING THE SHIP OF

STATE,” A METAPHOR FOR GOVERNANCE.1

C H A P T E R 1

GOVERNANCE—DEFINITIONS ANDISSUES

Governance is an elegant word summarizingthe all-embracing concept of authority and control,of governing. Recently, the term has appeared withincreasing frequency in the literature of manage-ment and public administration. Recognition of itscrucial importance to effective public administra-tion and prosperous private enterprises has givengovernance its current prominence as an issue. Itsrecognition has even spawned research institutes2

and caused existing organizations to gain a betterunderstanding of the concept and to review theirgovernance practices.

Depending on the context, the word gover-nance may be used to describe a variety of notions:

• the art of governing: the concepts and methodsinvolved in governance, (for example, parlia-mentary or presidential, unitary or federated,military or civilian, authoritarian versusdemocratic, in the case of governments);

• the exercise of authority: the use of power, theprocess of governance;

• the structure of authority: the arrangement—hierarchical, bureaucratic—for governance totake place; and

• the jurisdiction: the area in which the govern-ing body has authority.

The highly generic and detailed definition ofgovernance developed by Dr. Duncan Sinclair toguide an academic medical centre is applicable toany governing body:

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E8

Governance is the exercise of authority,direction and control. It can be thought of asthe right and responsibility to determine thepurposes and principles by which an organi-zation will function and then to arrange forits management accordingly. The purposes arewhat the organization seeks to accomplish;the principles are the context, the value sys-tem, within which it operates. Governancedeals with what an organization is to do andis, therefore, highly focused on planning, set-ting goals and objectives, and on the develop-ment of policies to guide the organizationand monitor its progress toward implementa-tion of its plans. Provided that the governingbody has confidently arranged for effectivemanagement of the organization, the primaryfocus of governance should be on the long-term—the organization’s mission, values,policies, goals, objectives and, for public sec-tor institutions… its accountability under theterms of its implicit social contract.3

A DEFINITION OF GOVERNANCE

(IN THE NONPROFIT CONTEXT)

GOVERNANCE IS THE FULFILLMENT OF RESPONSIBLE OWNER-

SHIP ON BEHALF OF THE COMMUNITY.4

DEFINITION OF GOVERNANCE

(USED IN THE WORLD BANK)

FROM A GENERAL DEFINITION OF GOVERNANCE AS “THE EXER-

CISE OF AUTHORITY, CONTROL, MANAGEMENT, POWER OF

GOVERNMENT,” THE WORLD BANK HAS FORMULATED A MORE

RELEVANT DEFINITION FOR ITS PURPOSES: “THE MANNER IN

WHICH POWER IS EXERCISED IN THE MANAGEMENT OF A

COUNTRY’S ECONOMIC AND SOCIAL RESOURCES FOR

DEVELOPMENT.”5

G O V E R N A N C E V E R S U S

M A N A G E M E N T

Elaborating on his definition, DuncanSinclair contrasted governance with management:

Governance is where the buck stops. Butgovernance is something quite different frommanagement. Governors cannot and shouldnot attempt to manage organizations whosepolicies they control.

Management is the act, art or manner ofcontrolling or conducting affairs, the skillfuluse of means to accomplish a defined pur-pose. If governance has to do with what anorganization is to do, management deals withhow it does it. Management, in our complicat-ed world with all its rules and regulations,requires expertise, experience and highlydeveloped sophisticated skills. It is (or shouldbe) a very professional activity that governorshave to ensure is firmly in place to serve theneeds and execute the plans of their organiza-tion. Just as governors should not try to man-age their organizations, so should managersnot try to provide them with governance.Managers are accountable to governors.6

In Canada, the exercise of authority over pub-lic hospitals has given rise to public debate.Clarification of this issue came from Ontariowhere a ministerial committee suggested that newlegislation define governance and specify the dis-tinction between governance and management.The committee suggested that governance, in thePublic Hospitals Act, be defined as :

The exercise, by the hospital’s board ofdirectors, of authority, direction and controlover the hospital.

The fundamental responsibilities of thehospital board are to ensure that the hospitalfulfills its purposes and principles, its social

P A R T I . C H A P T E R 1 . G O V E R N A N C E – D E F I N I T I O N S A N D I S S U E S 9

contract and its objectives for patient caremanagement, quality of programs and ser-vices, fiscal integrity and long-term viability.

Management’s responsibility is to devel-op and implement the strategies and pro-grams to achieve the principles, purposes,goals and objectives set by the board.

There are shades of gray separating gov-ernance from management. The differencebetween them, however, is that the board’sauthority derives from both the hospital cor-poration and the community, whereas man-agement’s authority derives from the board towhich it is accountable. Procedures should bedeveloped to enable the hospital corporationand the community to assess the effectivenessof the hospital’s governance, and to provide abasis for public scrutiny of the hospital’s ful-fillment of its social contract.7

G O V E R N A N C E S T R U C T U R E S

Institutionalized governance is exercisedthrough a governing body that has the power ofscrutiny or direction, such as a board of directorsor governors, a regulatory body, a cabinet in itsexecutive role, a city council, or a legislative assem-bly. The form that a governance structure takesdepends on a number of factors. It may, for exam-ple, be established by legislation or honoured tradi-tion. Different structures suit different organiza-tions. In any event, how things happen within aformal governance structure will be influenced bythe human factor—the personalities, talents, anddesires of the people involved.

Michael Atkinson defines governance struc-tures as:

The informal and patterned ways inwhich different institutions and actors inter-act within particular political and administra-tive settings to develop policy goals, select

among means, cope with uncertainty andcontroversy, and foster legitimacy and supportfor policies.8

S O M E R E L A T E D C O N C E P T S

To better understand the general nature ofgovernance and the structures through which it ispractised, it is useful to touch on some key philo-sophical underpinnings.

C I V I L G OV E R N A N C E A N D L I B E R T Y

Much of the concept of civil governancederives from the theory of the manner in whichthe state relates to its population. Civil governanceis related to civil liberty.9 The contrast is naturalliberty, which implies absolute freedom to do whatone wants to do. Civil liberty also means freedomof action, but only as long as it does not harm the“common good” and does not infringe on someoneelse’s liberty. Political liberty is the freedom to par-ticipate in civil governance by voting, holding pub-lic office, and expressing one’s political opinions inpublic.

The translation of the concept of civil gover-nance into social and political arrangements pro-vides the basis of a constitution from which thelaws of the land can be promulgated. It has alsoengendered social contracts, compacts, covenants,and citizen’s charters. Let’s explore these notions,starting with the social contract.

S O C I A L C O N T R AC T

The concept of a social contract has beenarticulated by philosophers like Thomas Hobbes,John Locke, and others. The term is most oftenassociated with the eighteenth-century Frenchthinker Jean-Jacques Rousseau. He imagined astate in which free citizens, acting freely, wouldrelinquish part of their freedom to the state.

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E1 0

Participatory democracy would characterize theprocess. In our present context, however, the termdoes not apply to a document binding two partiesin a set of mutual obligations, but rather to a polit-ical arrangement describing the relations between agovernment or a major public institution and thecommunity it serves. The social contract becomes apromise, an undertaking, a declaration, in effect an“unwritten agreement between society and thosewho seek to serve it.”10

S O C I A L C O M PAC T

People in the labour movement may relate tothe expression “social compact” as a variant of asocial contract. A compact is an agreement betweenindividuals or groups; contract essentially means thesame thing, except the term is used to describe theformal document reflecting the compact.

In the word compact was the connotation ofan agreement between factions that choose to lookat each other as equals. The term has somewhatmodified its meaning through time. The domina-tion of the government of Upper Canada by aclique of like-minded people at the turn of thenineteenth century was called the Family Compact;so was the expression describing the alliance in theearly 1700s between the Bourbon rulers of Franceand those of Spain. More recently, in 1974, theBritish Labour government promised price subsi-dies, and price and dividend controls to tradeunions, in exchange for restrained wage demands.Social compact was the name given to theproposal.

THE MAYFLOWER COMPACT, CONTRARY TO WHAT IS SO

OFTEN THOUGHT TODAY, DOES NOT REALLY SUGGEST A

SOCIAL CONTRACT OF INDEPENDENT AND EQUAL PEO-

PLE CONSTITUTING BY CONSENT THEIR OWN SOVEREIGN

AND REPRESENTATIVE GOVERNMENT FOR THE PURPOSE

OF THE PROTECTION OF THEIR OWN LIBERTIES AND

PROPERTY. ON THE CONTRARY: THE COMPACT IS ONE

FORMED AMONG PEOPLE WHO CHARACTERIZE THEIR

STATUS AS THAT OF “LOYALL SUBJECTS”, OF “OUR

DREAD SOVERAIGNE LORD, KING JAMES.” THEIR GUID-

ING PURPOSE, THEY DECLARED, WAS TWOFOLD: “THE

GLORIE OF GOD,” I.E. THE “ADVENCEMENTE OF THE

CHRISTIAN FAITH,” AND “THE HONOR OF OUR KING &

COUNTRIE.”11

COV E N A N T

In the United States, the Constitution isoften regarded as a covenant, a term borrowedfrom the Bible and sometimes deemed to be justanother word for social contract. However, notonly is the Constitution viewed as having intellec-tual origins (in the sense of getting agreement onthe most appropriate political system), but it is alsoseen as spiritually inspired and grounded in reli-gious ethics. In this sense, the framers of theConstitution are said to have brought forward acovenant, not merely a social contract.12

C I T I Z E N ’ S C H A R T E R

In the United Kingdom, a citizen’s charterwas tabled in Parliament in 1991. It focused on thepromise of raising the quality of public services andmaking them responsive to the needs of citizens. Inintroducing the charter, Prime Minister JohnMajor was specific about the intent:

How we will, for example, be introduc-ing guaranteed minimum waiting times for

P A R T I . C H A P T E R 1 . G O V E R N A N C E – D E F I N I T I O N S A N D I S S U E S 1 1

hospital operations. How we will require allschools to provide parents with reports. HowBritish Rail will be introducing new compen-sation schemes for poor service. How thosewho regulate electricity, water, gas andtelecommunications will be given the samestrong powers to insist on good service stan-dards for the customer. How we will toughenup inspection and audit, relate pay moreclosely to performance, and provide the citi-zen with more and better information.13

In the mind of the prime minister, the charteris not limited to improving the quality of service:“The citizen’s charter is about giving more powerto the Citizen,” insisting, however, that citizenshave responsibilities—as parents, as taxpayers—aswell as entitlements. There are four themes in thecharter: quality, choice, standards, and value. Thespirit of the citizen’s charter, which covers thewhole of the public service, is present in the char-ter drawn by a large number of government agen-cies. Those public declarations usually state thepromise, the commitments, the rights of the citi-zens, but some of them include the role and oblig-ations of citizens. For instance, the Job SeekersCharter insists that people applying for a job keepappointments on time.

Closing the loop in the accountability undera social contract, or an arrangement under anyother name, is not an easy step, as it generally con-sists of an agreement between the government andthe governed, which is the population at large. Thelatter cannot effectively organize to represent them-selves and negotiate with equal cohesion and con-sistency. It may well be, however, that the terms ofthe U.K. Citizen’s Charter are such that redress isavailable for mal- and nonfeasance by the govern-ment authority concerned.

The promises made by a political party that issuccessful in an election is an informal charter—a

commitment to do certain things while in office. Ifcitizens think that the government has not lived upto its implied commitment, they have to wait forthe next election to show their displeasure.

D E M O C R A C Y

Democracy is a form of government that rec-ognizes the right of all members of society to influ-ence political decisions, either directly or indirectly.

In a direct democracy, power is exerciseddirectly by the people: clearly, this is possible onlywhere the population is small. In representativedemocracies—which is what modern democraciesare—political decisions are taken by citizens elect-ed by the people to be their representatives.

The central institution of a modern democra-cy is a representative legislature in which decisions

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E1 2

THE LANGUAGE OF DEMOCRACY

WHAT, SIR, IS THE GENIUS OF DEMOCRACY? LET ME READ

THAT CLAUSE OF THE BILL OF RIGHTS OF VIRGINIA, WHICH

RELATES TO THIS: 3D CL. “THAT GOVERNMENT IS OR OUGHT

TO BE INSTITUTED FOR THE COMMON BENEFIT, PROTECTION,

AND SECURITY OF THE PEOPLE, NATION, OR COMMUNITY:

OF ALL THE VARIOUS MODES AND FORMS OF GOVERNMENT,

THAT IS BEST WHICH IS CAPABLE OF PRODUCING THE

GREATEST DEGREE OF HAPPINESS AND SAFETY, AND IS MOST

EFFECTUALLY SECURED AGAINST THE DANGER OF MAL-

ADMINISTRATION, AND THAT WHENEVER ANY GOVERNMENT

SHALL BE FOUND INADEQUATE, OR CONTRARY TO THESE

PURPOSES, A MAJORITY OF THE COMMUNITY HATH AN

UNDUBITABLE, UNALIENABLE AND INDEFEASIBLE RIGHT TO

REFORM, ALTER, ABOLISH IT, IN SUCH MANNER AS SHALL BE

JUDGED MOST CONDUCIVE TO THE PUBLIC WEAL.” THIS, SIR,

IS THE LANGUAGE OF DEMOCRACY: THAT A MAJORITY OF THE

COMMUNITY HAVE A RIGHT TO ALTER THEIR GOVERNMENT

WHEN FOUND TO BE OPPRESSIVE.14

P A T R I C K H E N R Y , 1 7 8 8

are taken by majority vote. The characteristics ofsuch a democracy are regular elections, free choiceof candidates, universal suffrage, freedom to orga-nize rival political parties, independence of thejudiciary, freedom of speech, freedom of the press,and respect for civil liberties and minority rights.

T H E N A T U R E O F A C O N S T I T U T I O N

A constitution defines the fundamental valuesand rules of a society.

THE ESSENCE OF A CONSTITUTION

[A CONSTITUTION] IS CONCERNED WITH WHAT IS DONE TO MAKE

SOCIETY INTO A PROPERLY STRUCTURED, CONTINUOUS LIVING BODY,

SO THAT THE POLITICAL ACTION OF WHICH THAT SOCIETY IS

CAPABLE CAN BE EFFICIENTLY AND EFFECTIVELY CONDUCTED.

MACHINERY, YES. BUT ALSO THOUGHT, THE DOCTRINE, THE

TEACHING, THE CONVENTIONAL NOTIONS. WHAT DOES THE SOCIETY

THINK ITS GOVERNMENT IS, HOW DOES IT TREAT IT, WHAT DOES IT

DO TO AMEND IT? WHAT FORMS OF CHANGE ARE POSSIBLE, WHAT

REFORMS...?15

[T]HE CONSTITUTION OF AN ORGANIZATION IS ITS FUNDAMENTAL

NORMATIVE STRUCTURE… A SET OF AGREEMENTS AND UNDER-

STANDINGS WHICH DEFINE THE LIMITS AND GOALS OF THE GROUP

(COLLECTIVITY) AS WELL AS THE RESPONSIBILITIES AND RIGHTS OF

THE PARTICIPANTS STANDING IN DIFFERENT RELATIONS TO IT.16

A constitution is often conceived of as a char-ter, a declaration or text outlining the nature of agovernment or other organization. A country’s con-stitution specifies how power will be shared amongthe people, the legislative and executive bodies, andthe judiciary. It has legal precedence over all otherlaws of the land. It is the basic law used to inter-pret all other laws.

Not all countries have written constitutions.Great Britain is the leading example of a countrywith an unwritten constitution. But it is unwrittenonly in the sense that there is no single documentreferred to as the constitution:

There are in fact various laws of consti-tutional significance, and there is a great cor-pus of authoritative constitutional writing inwhich scholars and lawyers discuss the consti-tution as it is, and as they think it ought tobe. It remains true, however, that a numberof important constitutional practices are fol-lowed with rigidity although they are nothingmore than conventions. The fact that Britaindoes not have a formally written constitutionis thus not of a great significance for the prac-tice of government and politics. A bindingauthoritative constitution does exist andpoliticians and public administrators are noless constitutional in their behavior than theircounterparts in those countries which dohave a formally designated document.17

ON THE NATURE OF A CONSTITUTION

THE CONSTITUTION APPEARS TO BE A RESTRAINT WHEN IN

FACT IT IS NONE AT ALL… SIR, I WILL NOT DECLAIM, AND SAY

ALL MEN ARE DISHONEST; BUT I THINK THAT, IN FORMING A

CONSTITUTION, IF WE PRESUME THIS, WE SHALL BE ON THE

SAFEST SIDE… MANY MILLIONS OF MONEY HAVE BEEN PUT

INTO THE HANDS OF GOVERNMENT, WHICH HAVE NEVER BEEN

ACCOUNTED FOR, THE ACCOUNTS ARE NOT SETTLED YET, AND

HEAVEN ONLY KNOWS WHEN THEY WILL BE.18

M E L A N C T O N S M I T H

A N T I - F E D E R A L I S T , 1 7 8 8

Concepts such as rights and responsibilities,power sharing, representation, participation andinfluence, which, as noted above, are rooted in

P A R T I . C H A P T E R 1 . G O V E R N A N C E – D E F I N I T I O N S A N D I S S U E S 1 3

such notions as social contract, democracy, andconstitution, are very much a part of the gover-nance equation in relation to our public- and pri-vate-sector institutions. Earlier, key definitionaland structural aspects were highlighted. Let us nowexamine a set of characteristics that, taken together,provide a framework for looking at the quality ofgovernance. The discussion will return to theseissues as it delves further into the subjects of gover-nance and accountability and the arrangementsthat bind them.

E S S E N T I A L C H A R A C T E R I S -

T I C S O F G O O D G O V E R N A N C E

Governance can be either good or bad, assidu-ous or negligent. Good governance displays a desireto move away from exercise of authority throughcontrols which may be effective but ephemeral,towards exercise of leadership which is at onceeffective, inspiring, continuous, and lasting.

To govern well implies the application offoresight, knowledge, understanding, and judg-ment, as well as considerable trust. Affirmation of

power and imposition of rigorous controls are leastlikely to be used in enlightened governance. As acorollary, good governance is very demanding ofaccountability.

But what is good governance and how will weknow we have it? The following are key characteris-tics of good governance.19 We know we have goodgovernance when governing bodies:

• comprise people with necessary knowledge,ability, and commitment to fulfill theirresponsibilities;

• understand their purposes and whose intereststhey represent;

• understand the objectives and strategies of theorganizations they govern;

• understand what constitutes reasonable infor-mation for good governance and obtain it;

• once informed, are prepared to ensure thatthe organization’s objectives are met and thatperformance is satisfactory; and

• fulfill their accountability obligations to thosewhose interests they represent by reporting ontheir organization’s performance.

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E1 4

1 SEE RICHARD LEDERER, “LANGUAGE-HATS IN THE RING, (THE PARLANCE OF POLITICS),” DELTA AIRLINES SKY MAGAZINE, NOVEMBER 1992, 128.2 THE INSTITUTE ON GOVERNANCE IN OTTAWA AND THE INSTITUTE OF CORPORATE DIRECTORS IN TORONTO, FOR INSTANCE.3 DUNCAN SINCLAIR, DEAN OF MEDICINE, QUEEN’S UNIVERSITY, “GOVERNANCE OF THE ACADEMIC MEDICAL CENTRE,” IN ACMC FORUM, VOL. XX, NO. 4, 12.4 R. J. UMBDENSTOCK, W. M. HAGEMAN AND B. AMNDSON, “THE FIVE CRITICAL AREAS FOR EFFECTIVE GOVERNANCE OF NOT-FOR-PROFIT HOSPITALS,” HOSPITALS AND HEALTH SERVICES

ADMINISTRATION, NO. 35, 1990, 481-92.5 THE WORLD BANK, GOVERNANCE AND DEVELOPMENT (WASHINGTON, D.C.: THE WORLD BANK, 1992), 3.6 SINCLAIR, “GOVERNANCE OF THE ACADEMIC MEDICAL CENTRE,” 12.7 ONTARIO MINISTRY OF HEALTH, INTO THE 21ST CENTURY, ONTARIO PUBLIC HOSPITALS, REPORT OF THE STEERING COMMITTEE, PUBLIC HOSPITALS ACT REVIEW (TORONTO: ONTARIO

MINISTRY OF HEALTH, FEBRUARY 1992), ES-3.8 MICHAEL M. ATKINSON, GOVERNING CANADA, INSTITUTIONS AND PUBLIC POLICY (TORONTO: HARCOURT BRACE JOVANOVICH CANADA INC., 1993), GLOSSARY.9 SEE MICHAEL G. KAMMEN, THE ORIGINS OF THE AMERICAN CONSTITUTION (TORONTO: PENGUIN BOOKS, 1986), IX.10 THIS CHARACTERIZATION OF THE SOCIAL CONTRACT IS FROM WHITE, KERR AND J. E. CONNELLY, “THE MEDICAL SCHOOL’S MISSION AND THE POPULATION’S HEALTH,” ANNALS OF

INTERNAL MEDICINE, DECEMBER 1991, VOL. 115, NO. 12, AS CITED IN UNIVERSITY OF OTTAWA HEALTH SCIENCES COMPLEX STRATEGIC PLANNING PROCESS DISCUSSION PAPER, HEALTHY

DIRECTIONS (OTTAWA: UNIVERSITY OF OTTAWA HEALTH SCIENCES COMPLEX, 1992), 53.11 THOMAS L. PANGLE, “THE CONSTITUTION’S HUMAN VISION,” THE PUBLIC INTEREST, NO. 86, WINTER 1987, 79.12 IRVING KRISTOL, “THE SPIRIT OF ‘87,” THE PUBLIC INTEREST, IBID., 5.13 TREASURY, THE CITIZEN’S CHARTER: RAISING THE STANDARD (LONDON: HMSO, CM 1599, JULY 1991), 1.14 SPEECH OF PATRICK HENRY IN THE VIRGINIA RATIFYING CONVENTION, JUNE 5, 1788, AS CITED IN THE AMERICAN CONSTITUTION, FOR AND AGAINST, THE FEDERALIST AND ANTI-

FEDERALIST PAPERS, J. R. POLE, ED. (NEW YORK: HILL AND WANG, 1987), 119.15 G. R. ELTON, THE FUTURE OF THE PAST (CAMBRIDGE: CAMBRIDGE UNIVERSITY PRESS, 1968), 24-25, AS CITED IN PETER HENNESSY, WHITEHALL (NEW YORK: THE FREE PRESS, 1989), 11-

12.16 M. N. ZALD, POWER IN ORGANIZATIONS (NASHVILLE: VANDERBILT UNIVERSITY PRESS, 1970), 225.17 J. E. KINGDOM, ED., THE CIVIL SERVICE IN LIBERAL DEMOCRACIES, AN INTRODUCTORY SURVEY, (LONDON: ROUTLEDGE, 1990), 11. 18 THE AMERICAN CONSTITUTION, BACK PAGE.19 CCAF, IN SEARCH OF EFFECTIVE GOVERNANCE, VIDEO SCRIPT, 1994, 15.

FEDERATION VERSUS CONFEDERATION

THE SEMANTICS OF CONSTITUTIONAL ARRANGEMENTS CAN BE

TRICKY. MANY AUTHORITIES MAKE A DISTINCTION BETWEEN A

FEDERATION AND A CONFEDERATION. IN A FEDERATION, IN

THEIR VIEW, THE COMMON GOVERNMENT HAS ASCENDENCY

OVER THE GOVERNMENTS OF THE STATES COMPRISING IT; IT IS

SUPREME. IN A CONFEDERATION, THE EMPHASIS IS ON THE

SOVEREIGNTY AND AUTONOMY OF EACH CONSTITUENT STATE

AND IS USUALLY FORMED TO ACHIEVE EFFICIENCY IN EXTER-

NAL PURPOSES—DEFENSE, INTERNATIONAL TRADE, EXTERNAL

AFFAIRS. THE FEDERAL SYSTEM IN CANADA HAS ENOUGH OF

BOTH TO SATISFY LARGE ELEMENTS OF THE TWO DEFINITIONS.

THE FATHERS OF CONFEDERATION HAVE GIVEN US A FEDERAL

GOVERNMENT, AND THE PROVINCES, OVER 125 YEARS, HAVE

DISPLAYED DIFFERENT POINTS OF VIEW ABOUT THEIR UNDER-

STANDING OF WHAT EXACTLY CANADA IS.

NATIONAL VERSUS FEDERAL

WE MIGHT ADD A FATHER OF THE U.S. CONSTITUTION AND

THE FOURTH PRESIDENT OF THE UNITED STATES, JAMES

MADISON’S DISTINCTION 20 BETWEEN NATIONAL AND FEDERAL

WHICH, IN A WAY, EXPLAINS WHY THE MEECH LAKE AGREE-

MENT HAD TO BE RATIFIED BY EVERY PROVINCE REGARDLESS

OF ITS POPULATION INSTEAD OF BY THE MAJORITY OF THE

POPULATION IN THE COUNTRY. IF THE CONSTITUTION IS

NATIONAL IN CHARACTER, THE SUPREME AND ULTIMATE

AUTHORITY WOULD RESIDE IN THE MAJORITY OF THE PEOPLE

OF CANADA; IF IT IS FEDERAL, THE CONCURRENCE OF EACH

PROVINCE WOULD BE ESSENTIAL TO EVERY ALTERATION OF THE

CONSTITUTION THAT WOULD BE BINDING ON ALL. THIS

IMPLIES A DIFFERENT UNDERSTANDING OF FEDERAL THAN IS

GIVEN ABOVE.

C H A P T E R 2

GOVERNANCE INCANADA

Canada’s constitution contains both writtenand unwritten elements. We inherited from GreatBritain an accumulation of constitutional decisions,precedents, and practices defining governmentauthority. The British North America Act of 1867(BNA Act) granted Canada its independence and isthe basis for the written part of the constitution. Ithas been formally renamed the Constitution Act,1867, and has been amended several times, mostrecently by the Constitution Act, 1982, which con-tains the Canadian Charter of Rights and Freedoms.An important part of the Canadian constitutiondivides the totality of governmental powers betweenthe provinces and the federal government, a pointof controversy over the decades. It also containsprovisions for such matters as periodic elections (atleast every five years) that are essential to ensure acontinuing democracy.

The Canadian constitution sets out broadlythe nature of our government. It draws heavily onthe Westminster (British) model, and the princi-ples of parliamentary government apply equally tothe federal government and the provinces. Thepositions of prime minister and premier do notappear in the written constitution, nor does theterm cabinet. They are elements of the unwrittenpart of the constitution, but no less important tothe essential working of Canadian governments.

T H E F O R M O F G O V E R N M E N T

I N C A N A D A

The Crown is the sovereign authority—thatis, head of state—in Canada’s system of govern-

P A R T I . S E C T I O N 1 . A C C O U N T A B I L I T Y ’ S C O N T E X T — G O V E R N A N C E 1 5

ment. The Crown is represented at the federal levelby a governor-general, who as a public figure isvery active, but within the system of governmentplays a largely ceremonial role. The governor-gen-eral takes advice from the Privy Council ofCanada, more precisely from its operational part,the cabinet headed by the prime minister. At theprovincial level, a lieutenant-governor representsthe Crown and takes advice from the provincialexecutive council.

CANADA HAS ADOPTED FROM GREAT BRITAIN THE

WESTMINSTER MODEL OF PARLIAMENTARY GOVERN-

MENT. IT HAS A PARLIAMENT IN THE FORM OF A BICAM-

ERAL ASSEMBLY, CONSISTING OF AN APPOINTED

SENATE,21 AND AN ELECTED HOUSE OF COMMONS. THE

FORMAL ROLE OF PARLIAMENT IS THAT OF LEGISLATION,

BUT MOST LEGISLATION IS FRAMED BY THE CABINET,

WHICH IS ABLE TO RELY ON THE SUPPORT OF ITS PARTY

MAJORITY IN THE HOUSE OF COMMONS, SO THAT THE

EFFECTIVE ROLE OF THE HOUSE IS ONE OF SCRUTINIZ-

ING THE EXECUTIVE, AND PROVIDING A FORUM FOR

POLITICAL DEBATE.22

THE MOST IMPORTANT DETERMINANTS OF CONTROL

AND USE OF POWER IN THE CANADIAN PARLIAMENTARY

SYSTEM ARE THE POLITICAL PARTIES. ELECTIONS ARE

MORE A MATTER OF VOTERS CHOOSING BETWEEN PAR-

TIES AND PARTY LEADERS THAN BETWEEN INDIVIDUAL

CANDIDATES. THE WINNING PARTY BECOMES THE GOV-

ERNMENT, WITH A MONOPOLY OVER EXECUTIVE POWER

AND DOMINATION OF PARLIAMENT. WITHIN THE HOUSE

OF COMMONS, THE BASIC STRUCTURE OF PROCEEDINGS

IS THE ADVERSARIAL FORMAT OF CONTEST AND DEBATE

BETWEEN THE GOVERNMENT AND OPPOSITION PARTIES.23

T H E P R I M E M I N I S T E R A N D T H E C A B I N E T

The prime minister and the cabinet of minis-ters are not directly elected to those positions bythe people, though they are usually popularly elect-ed as members of the House of Commons. Theprime minister is usually the leader of the politicalparty that won the majority of seats in the last elec-tion. In turn, the cabinet is chosen by the primeminister from among his or her supporters in theHouse of Commons and the Senate.24

Executive power is really in the hands of cabi-net led by the prime minister. Interestingly, “nei-ther of these are actually mentioned in the BNAAct. The origins of the Canadian cabinet lie in thePrivy Council, a body formally charged with thefunction of advising the Governor-General. Oncechosen, cabinet members formally gain theirauthority by being sworn in as members of thisCouncil. Though remaining privy councillors forlife, but they lose their executive authority oncethey cease to be members of the cabinet.”25

THE WORD EXECUTIVE

THE WORD EXECUTIVE IS DERIVED FROM THE LATIN VERB

EXSEQUI, TO FOLLOW THROUGH OR TO CARRY OUT. IN THE

PRIVATE SECTOR, CORPORATE EXECUTIVES HEADED BY A CHIEF

EXECUTIVE OFFICER (CEO) CARRY OUT THE WILL OF THE

BOARD OF DIRECTORS. IN PRIVATE FAMILY MATTERS, EXECU-

TORS OF ESTATES FOLLOW THE WISHES OF DECEASED TESTA-

TORS. IN OUR GOVERNMENT, THE WORD EXECUTIVE REFERS

TO THE CABINET AND BUREAUCRACY: THE EXECUTIVE ARM OF

GOVERNMENT. THE MOST SENIOR NONELECTED OFFICIAL IN

THE PRIVY COUNCIL OFFICE IS THE CLERK OF THE PRIVY

COUNCIL AND HOLDS THE SIMULTANEOUS TITLE SECRETARY

TO THE CABINET. FARTHER DOWN THE HIERARCHY ARE OFFI-

CIALS WITH THE TITLE EXECUTIVE DIRECTOR.

A C C O U N T A B I L I T Y , P E R F O R M A N C E R E P O R T I N G , C O M P R E H E N S I V E A U D I T - A N I N T E G R A T E D P E R S P E C T I V E1 6

By convention, the great majority of cabinetmembers are chosen from the House of Commons.The reason is that the ministers can then beaccountable to the elected chamber; the Senate isconsidered an inferior forum in which to holdministers to account.

COLLECTIVE RESPONSIBILITY

IN CANADA’S SYSTEM OF GOVERNMENT, CABINET MINISTERS

ARE NOT ONLY ACCOUNTABLE FOR THEIR OWN PORTFOLIOS,

THEY ALSO HAVE A COLLECTIVE RESPONSIBILITY AS MEMBERS

OF THE GOVERNMENT. THE CABINET ASSUMES RESPONSIBILITY

FOR THE POLICIES AND PERFORMANCE OF ITS GOVERNMENT.

INDIVIDUAL MINISTERS HAVE THE TASK OF MESHING THEIR

INDIVIDUAL ACCOUNTABILITY WITH RESPECT TO THEIR OWN

DEPARTMENTAL POLICIES AND PROGRAMS WITH THEIR COL-

LECTIVE RESPONSIBILITIES AS MINISTERS OF THE CROWN IN

SUPPORT OF THEIR OWN GOVERNMENT.