Account Documentation Series: Compliance & Due Diligence ...

77

PRESENTED BY MARY-LOU HEIGHES COMPLIANCE PLUS, INC. [email protected] JANUARY 2017 Compliance & Due Diligence at Account Opening 1

Transcript of Account Documentation Series: Compliance & Due Diligence ...

P R E S E N T E D B Y

M A R Y - L O U H E I G H E S

C O M P L I A N C E P L U S , I N C .

m h e i g h e s @ c u a s k m e . c o m

J A N U A R Y 2 0 1 7

Compliance & Due Diligence at Account Opening

1

Disclaimer 2

This presentation is designed to provide accurate and authoritative information in

regard to the subject matter covered. The handouts, visuals, and verbal information

provided are current as of the webinar date. However, due to an evolving

regulatory environment, Financial Education & Development, Inc. does not

guarantee that this is the most-current information on this subject after that time.

Webinar content is provided with the understanding that the publisher is not

rendering legal, accounting, or other professional services. Before relying on the

material in any important matter, users should carefully evaluate its accuracy,

currency, completeness, and relevance for their purposes, and should obtain any

appropriate professional advice. The content does not necessarily reflect the views

of the publisher or indicate a commitment to a particular course of action. Links to

other websites are inserted for convenience and do not constitute endorsement of

material at those sites, or any associated organization, product, or service.

Sponsors

Alabama Bankers Association

Arkansas Community Bankers

California Community Banking Network

Independent Bankers of Colorado

Florida Bankers Association

Community Bankers Association of Georgia

Community Banker Association of Illinois

Indiana Bankers Association

Community Bankers of Iowa

Community Bankers Association of Kansas

Kentucky Bankers Association

Maine Bankers Association

Community Bankers of Michigan

Independent Community Bankers of Minnesota

Missouri Independent Bankers Association

Montana Independent Bankers Association

Nebraska Independent Community Bankers

Independent Comm. Bankers Assoc. of New Mexico

Independent Bankers Assoc. of New York State

Independent Community Banks of North Dakota

Community Bankers Association of Ohio

Community Bankers Association of Oklahoma

Pennsylvania Association of Comm. Bankers

Independent Banks of South Carolina

Independent Comm. Bankers of South Dakota

Tennessee Bankers Association

Independent Bankers Association of Texas

Vermont Bankers Association

Virginia Association of Community Banks

Community Bankers of Washington

Community Bankers of West Virginia

Wisconsin Bankers Association

Directed by The Community Bankers Webinar Network

3

Today’s Presenter 4

Mary-Lou Heighes, Compliance Plus, Inc.

Mary-Lou Heighes is President and founder of Compliance Plus, Inc., which has assisted financial institutions with the development of compliance programs since 2000. She provides compliance training for trade associations and financial institutions. Mary-Lou has been an instructor at regulatory compliance schools, conducts dozens of webinars, and speaks at numerous conferences throughout the country.

Involved with financial institutions since 1989, Mary-Lou has over 20 years’ compliance experience. Before starting Compliance Plus in 2000, she spent five years working as a loan officer, marketer, and collector. She also worked at a state trade association for seven years providing compliance assistance and advising on state and federal legislative issues that affect financial institutions.

Topics

Customer Identification Program

Customer Due Diligence

Identity Theft Red Flags

Office of Foreign Assets Control

Signature Cards

Disclosures

5

PATRIOT Act Identification

Every financial institution is required to identify every

accountholder with whom they have a “formal banking

relationship” (i.e., Customer Identification Program)

Must have a “reasonable belief” that they know the people

who have accounts are who they say they are

Must have an idea of the types of activities accountholders

will engage in (i.e., Customer Due Diligence)

6

CIP Notification

Notice must be posted wherever accounts are opened – in person, by mail, online, etc.

Important Information About Procedures For Opening A New Account

To help the government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens an account.

What this means for you: when you open an account, we will ask for your name, address, date of birth, and other information that will allow us to identify you. We may also ask to see your driver’s license or other identifying documents.

7

Who is the Customer for CIP?

Natural person – the person

Formal business – the business

May also need to do it on the owner(s) and signer (May 2018)

Sole proprietor – the person

An UTMA account – the custodian

An account established using a power of attorney

If principal is incapacitated – the attorney in fact

If the principal is not incapacitated – the principal

A formal trust or estate – the trust or estate

May also need to do CIP on the trustor, trustee, or executor depending on whether the account/party is considered higher risk

8

Customer Identification Program (CIP)

4 required pieces of information (natural person):

Name

Date of birth

Physical address

Home, work

Description of location

Next of kin

Taxpayer identification (or other identifying number)

US person = Social Security number

Non-US person = SSN, individual taxpayer identification number or other number tied to a government issued document

9

Additional Information

The institution may collect additional information as needed

Occupation is often collected at account opening

Will facilitate completion of Currency Transaction and Suspicious Activity Reports (SARs)

Helps in investigations

Is this information kept current?

10

Documentary Verification for CIP

Documentary: non-expired, government-issued

document showing nationality or residence and

bearing a photograph or similar safeguard, such as a:

Passport or passport card

State-issued driver’s license or identification

Other government issued document

Can use any government ID specified in your

CIP program

11

Non-Documentary Verification for CIP

Non-documentary can be anything spelled out in your written program, for example:

Expired government-issued documents

Credit or consumer report

Utility bill

Paycheck stub

Employee ID

Etc.

Useful for minors or anyone lacking government ID

Cannot go outside the institution’s written program

12

Customer Identification for Businesses

For businesses and other accounts held by non-natural persons:

Name

Physical address

Taxpayer identification number (EIN usually)

Documentary verification

Based on form of business – articles of incorporation, certificate of partnership, etc.

Whatever is in your written program

13

Verifying Information

You must be able to verify enough information to

form a true belief of who the person is that is

opening the account.

This does not mean that every single piece of

information must be verified.

Refer to your written procedures for direction.

14

Clarifying Discrepancies

If your procedures call for clarifying discrepancies –

for example name and SSN don’t match

Follow written procedures

(may include additional documentation)

If you have satisfied the requirement that you have

formed a true belief that the person or entity is who

they say they are, then the process is complete

15

Additional Documentation

Additional documentation may be required if the

institution needs it to clarify discrepancies or form a

reasonable belief as to the person’s identity

Credit report

Utility or other bills

Lease or rental agreements

Etc.

16

CIP Conclusions

If you are unable to reach a reasonable belief that the

person is who they say they are during the CIP process, the

written CIP program should specify what action you are to

take regarding the account

CIP is only conducted once per accountholder, unless the

institution later determines that it no longer has a

reasonable belief that the person is who they say

For businesses, the beneficial ownership form will need to be

completed for every new account regardless of current

account ownership/relationship (May 2018)

17

Account Opening Procedures

Your procedures should address all the different ways accounts may be established:

In person

Online

By mail

By phone

Through third parties

The methods for establishing identity may vary based on how the account is opened

18

Remote Opening

For accounts opened by mail, phone, or online

Procedures for establishing identity

Out-of-wallet questions

Information from consumer reports

Third-party verification services

IRS TIN-matching program

Will you be receiving government-issued identification?

What about signatures?

For fraud purposes, check signing, indorsements

19

Due Diligence

Anticipate the type of activities in which accountholders will engage

The higher the risk of the accountholder, the more due diligence is needed

Lower risk = CIP information and normal monitoring

Higher risk = above plus additional information concerning the accountholder and transactional information up front

20

Due Diligence for Business Accounts

In addition to the regular due diligence, financial

institutions must obtain CIP information on any owner

of a business that has 25% or more ownership; and the

same information over the person with direct control

or management of the business

There is a model form for this purpose.

21

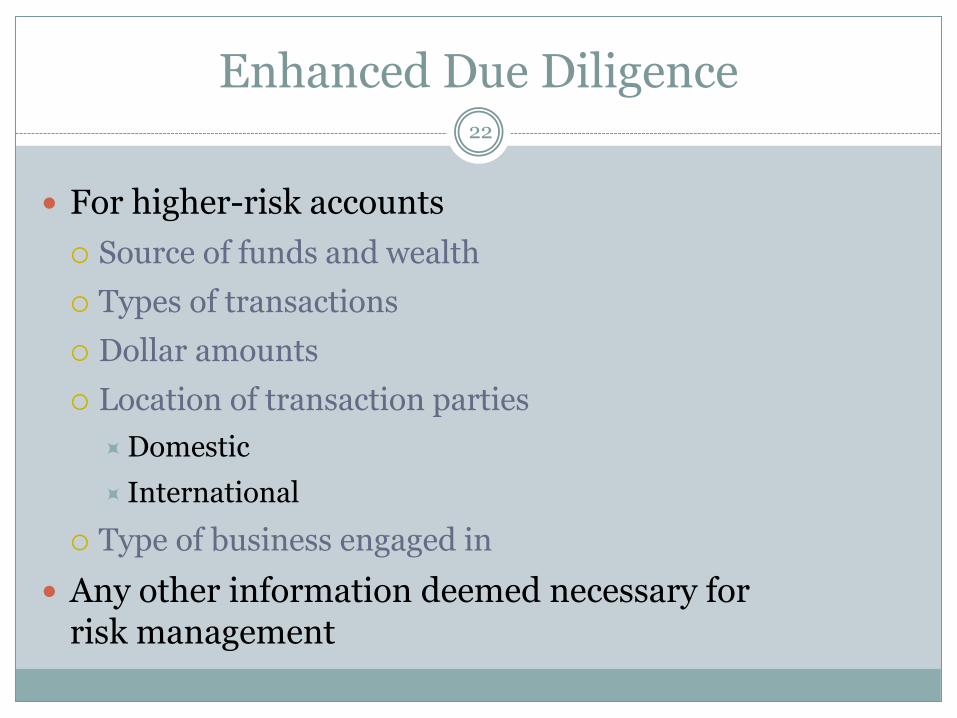

Enhanced Due Diligence

For higher-risk accounts

Source of funds and wealth

Types of transactions

Dollar amounts

Location of transaction parties

Domestic

International

Type of business engaged in

Any other information deemed necessary for risk management

22

Consumer Reports

It is permissible to run a consumer report on anyone establishing an account?

If the consumer gives written permission, or

Otherwise has a legitimate business need for the information in connection with a business transaction that is initiated by the consumer

Credit report, ChexSystems/Qualifile, etc.

23

Denial Based on Consumer Report

If denying an account or services based on information

in a consumer report, adverse action notice is needed.

Name, address, and toll-free number for the

consumer reporting agency.

If credit score was used, must include the score.

24

Prescreens

If using a consumer report run at account opening to

determine whether the consumer qualifies for other

products and services beyond the one he or she requested

Considered a “prescreen” where credit is involved

Requires a “firm offer of credit”

25

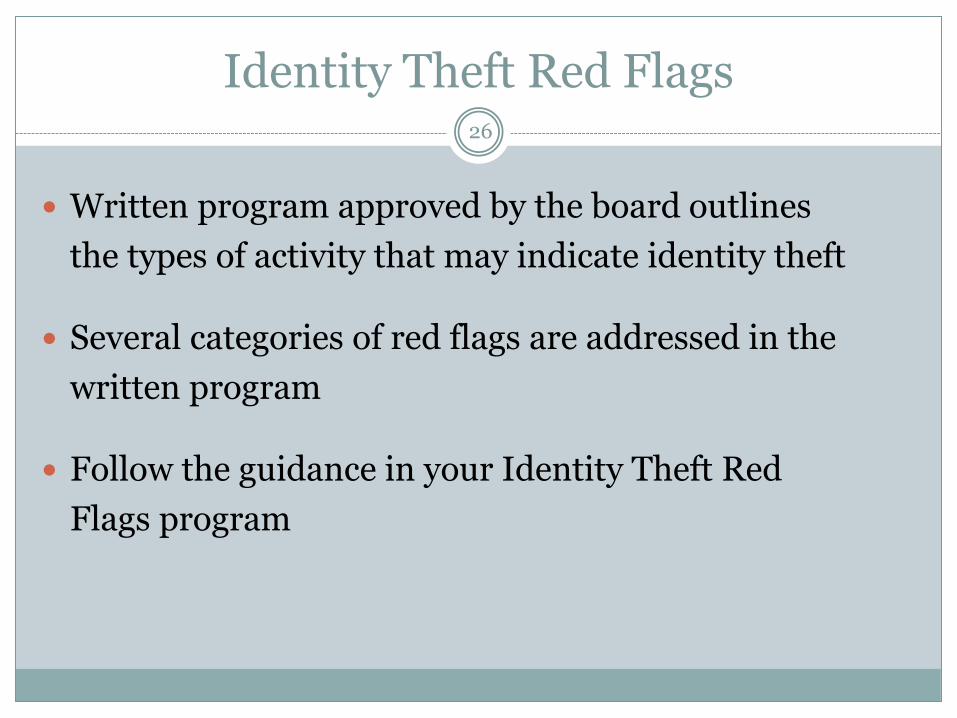

Identity Theft Red Flags

Written program approved by the board outlines

the types of activity that may indicate identity theft

Several categories of red flags are addressed in the

written program

Follow the guidance in your Identity Theft Red

Flags program

26

Red Flags at Account Opening

A fraud or active duty alert is included with a consumer report.

A consumer reporting agency provides a notice of credit freeze in

response to a request for a consumer report.

A consumer reporting agency provides a notice of

address discrepancy.

Documents provided for identification appear to have been

altered or forged.

The photograph or physical description on the identification is

not consistent with the appearance of the applicant or

customer presenting the identification.

27

Suspicious Documents

Other information on the identification is not consistent

with information provided by the person opening a new

covered account or customer presenting the identification.

Other information on the identification is not consistent

with readily accessible information that is on file with the

financial institution or creditor, such as a signature card or

a recent check.

An application appears to have been altered or forged,

or gives the appearance of having been destroyed and

reassembled.

28

Suspicious Information

Personal identifying information provided is inconsistent when

compared against external information sources used by the

financial institution or creditor. For example:

The address does not match any address in the consumer report; or

The Social Security number (SSN) has not been issued, or is listed on

the Social Security Administration’s Death Master File.

Personal identifying information provided by the customer is not

consistent with other personal identifying information provided

by the customer. For example, there is a lack of correlation

between the SSN range and date of birth.

29

Suspicious Information

The person opening the covered account or the customer fails to provide all required personal identifying information on an application or in response to notification that the application is incomplete.

Personal identifying information provided is not consistent with personal identifying information that is on file with the financial institution or creditor.

For financial institutions and creditors that use challenge questions, the person opening the covered account or the customer cannot provide authenticating information beyond that which generally would be available from a wallet or consumer report.

30

Identity Theft and Business

Identity theft can occur on business accounts,

fiduciary accounts, any type of account.

Look for suspicious business paperwork, lack of

paperwork on the business.

Resistance to providing documentation, unwillingness

to answer questions about the business.

31

Identity Theft Reporting

If you believe that an attempt at identity theft has

been made, it should be reported to management

and usually the Bank Secrecy Act Officer.

Identity theft is reportable on a Suspicious

Activity Report.

32

Red Flags During Account Opening

Fraudulent identification information

ID theft or Active Duty Alert on credit report

Use of incorrect/false Social Security number

Deceased, not issued yet, name or DOB mismatch

Stated income not supported

No credit report

False income statements/paystubs

Unable to locate using contact information

False addresses/employer

33

Address Discrepancies

If a credit report shows an address different than

what was provided, you should verify address prior

to providing a credit account or a new plastic card.

34

Office of Foreign Assets Control

Once a reasonable belief is formed that this is the true

identity of the person, the name must be checked

against the lists maintained by the Office of Foreign

Assets Control.

These lists are people, places, entities, foundations, and

others that no one in the U.S. can do business with.

Parties to the account should be checked against the

OFAC list as specified in your written procedures.

35

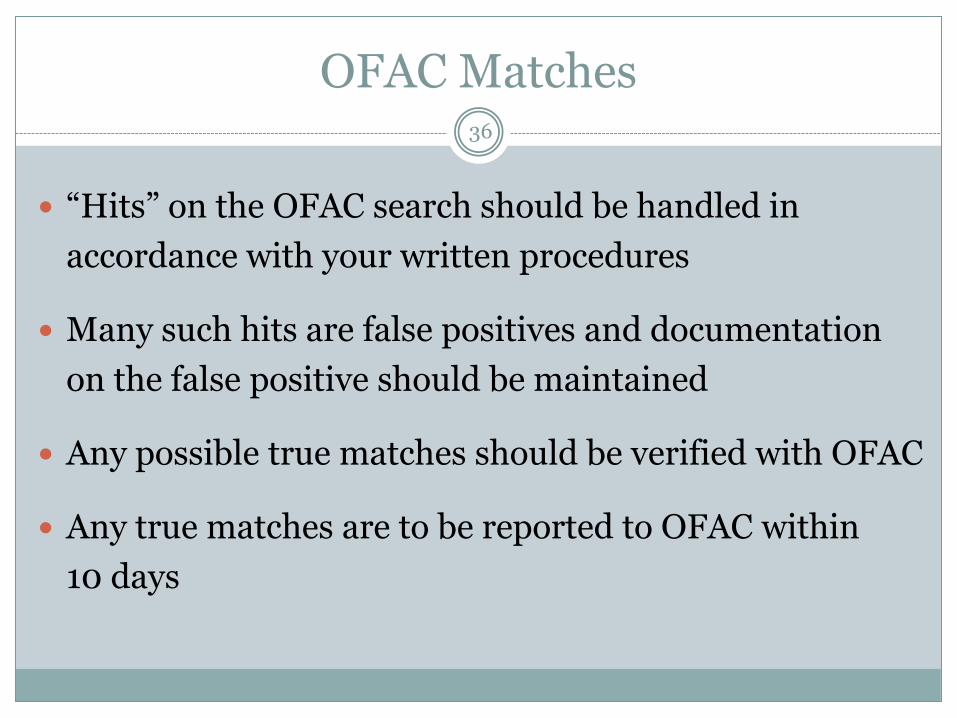

OFAC Matches

“Hits” on the OFAC search should be handled in

accordance with your written procedures

Many such hits are false positives and documentation

on the false positive should be maintained

Any possible true matches should be verified with OFAC

Any true matches are to be reported to OFAC within

10 days

36

Question Break

37

Signature Cards

Based on type of ownership

Individual

Joint (with or without right of survivorship)

Trust (formal requires special signature card?)

With pay-on-death beneficiaries

Sole proprietorship?

Formal business, organization, or association

Fiduciary capacity (power of attorney, conservatorship, rep. payee)

Uniform Transfer to Minors

IRAs

38

Individual Accounts

One owner

Signs signature card

May name a beneficiary or pay on death payee

Use owner’s Social Security number if US person

If one US person on account, must use SSN to report to Internal Revenue Service

Non-US person may have SSN, ITIN, or other identifying number

May provide W-8BEN

39

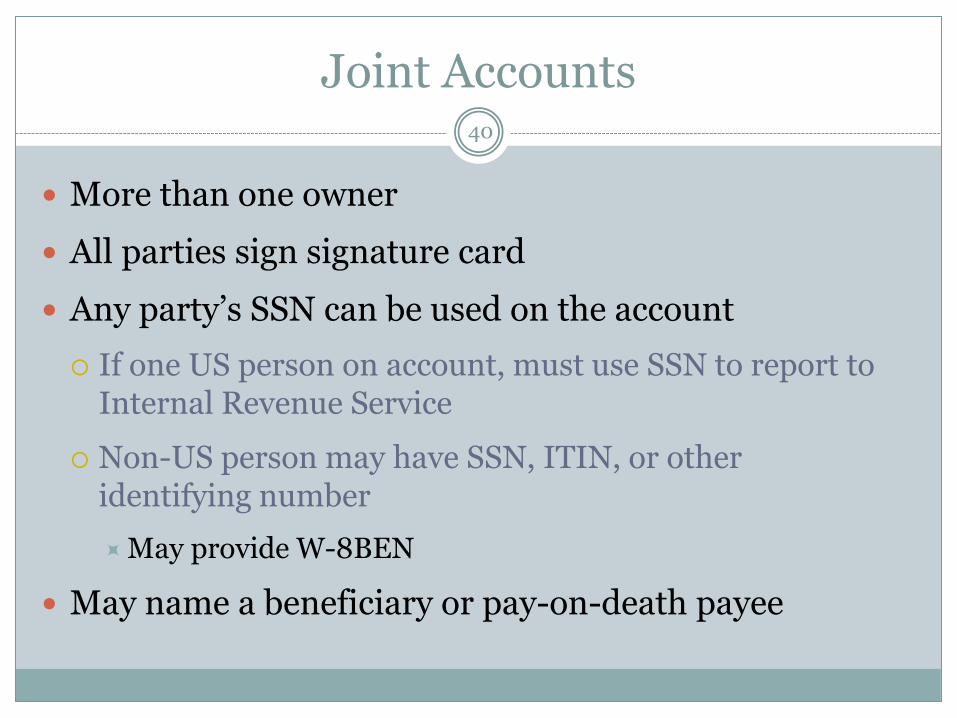

Joint Accounts

More than one owner

All parties sign signature card

Any party’s SSN can be used on the account

If one US person on account, must use SSN to report to Internal Revenue Service

Non-US person may have SSN, ITIN, or other identifying number

May provide W-8BEN

May name a beneficiary or pay-on-death payee

40

Trust Accounts

Should have a special signature card/account agreement for formal trusts

Trustors create the trust but are not signers on the account

Trustees are nominated by trustors to manage trust assets

They sign the signature card but are not owners of the account, they are merely agents

Trustors may name themselves as trustees

Beneficiaries of the trust may be named

41

Sole Proprietorships

Usually one owner

Owner signs signature card

May have other authorized signers

Use owner’s Social Security number (IRS encourages SSN even if they have an EIN)

If using another name (DBA) what is required as proof according to policy/procedures?

42

Formal Legal Entity

Use name of formal entity

Resolution or other documentation on who is authorized to sign

Authorized signers not necessarily owners

Use taxpayer identification number of legal entity

Does resolution or other documentation have limitations on signers?

43

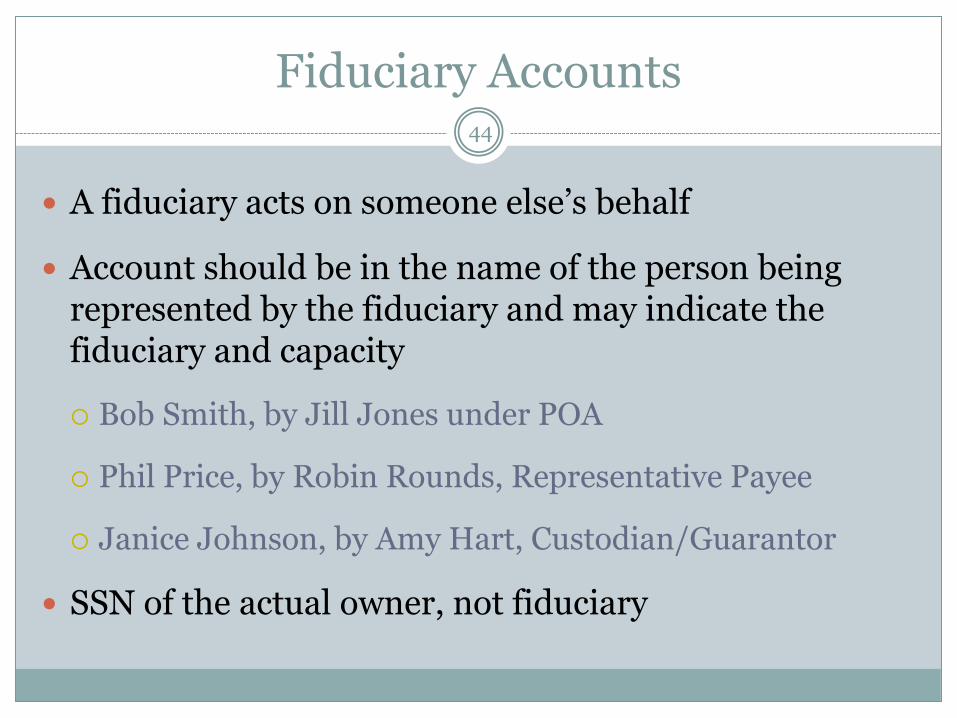

Fiduciary Accounts

A fiduciary acts on someone else’s behalf

Account should be in the name of the person being represented by the fiduciary and may indicate the fiduciary and capacity

Bob Smith, by Jill Jones under POA

Phil Price, by Robin Rounds, Representative Payee

Janice Johnson, by Amy Hart, Custodian/Guarantor

SSN of the actual owner, not fiduciary

44

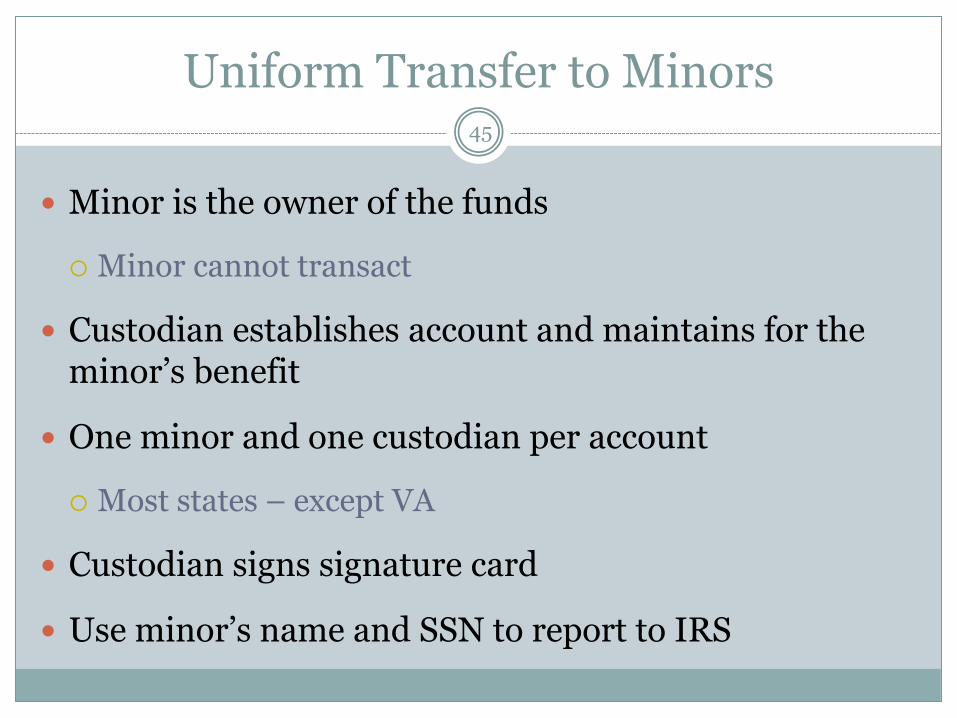

Uniform Transfer to Minors

Minor is the owner of the funds

Minor cannot transact

Custodian establishes account and maintains for the minor’s benefit

One minor and one custodian per account

Most states – except VA

Custodian signs signature card

Use minor’s name and SSN to report to IRS

45

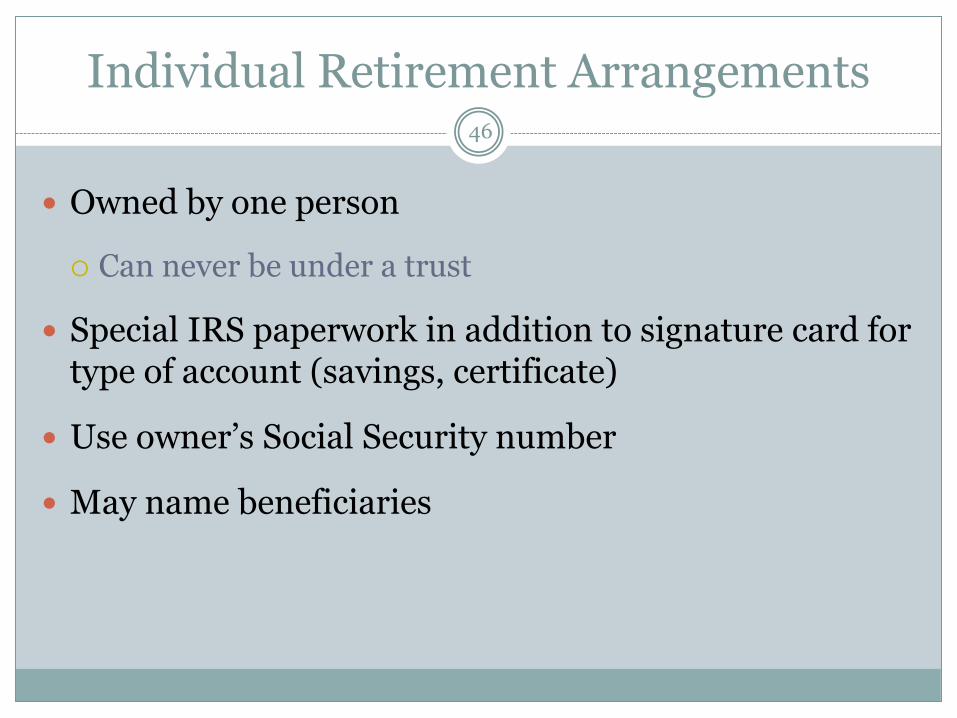

Individual Retirement Arrangements

Owned by one person

Can never be under a trust

Special IRS paperwork in addition to signature card for type of account (savings, certificate)

Use owner’s Social Security number

May name beneficiaries

46

IRS Rules on Reporting

The name and taxpayer identification number must match

W-9 form for certification or substitute W-9 on the signature card

If on the signature card, either a separate signature line for the certification or a statement that the IRS does not require signer to agree to any terms

W-8BEN for non-US persons if requested

47

48

Whose Tax ID?

For this type of account:

Individual

Two or more individuals (joint account)

Custodian account of a minor (Uniform Gift to Minors Act)

a. The usual revocable savings trust (grantor is also trustee)

b. So-called trust account that is not a legal or valid trust under state law

Sole proprietorship or disregarded entity owned by an individual

Give name and SSN of:

The individual

The actual owner of the account or, if combined funds, the first individual on the account

The minor

The grantor-trustee

The actual owner

The owner

49

Whose Tax ID?

For this type of account: Grantor trust filing under Optional

Form 1099 Filing Method 1

Disregarded entity not owned by an individual

A valid trust, estate, or pension trust

Corporation or LLC electing corporate status on Form 8832 or Form 2553

Association, club, religious, charitable, educational, or other tax-exempt organization

Give name and SSN of: The grantor

Give name and EIN of: The owner

Legal entity

The corporation

The organization

50

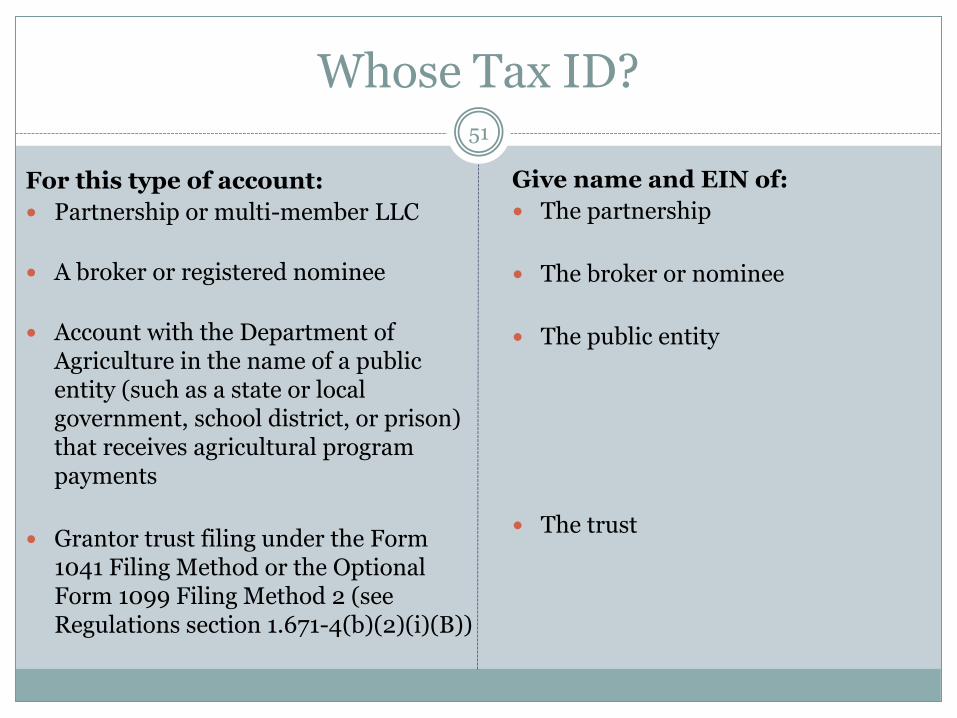

Whose Tax ID?

For this type of account:

Partnership or multi-member LLC

A broker or registered nominee

Account with the Department of Agriculture in the name of a public entity (such as a state or local government, school district, or prison) that receives agricultural program payments

Grantor trust filing under the Form 1041 Filing Method or the Optional Form 1099 Filing Method 2 (see Regulations section 1.671-4(b)(2)(i)(B))

Give name and EIN of:

The partnership

The broker or nominee

The public entity

The trust

51

Required Disclosures

Truth in Savings

Your ability to withdraw funds (check holds)

Regulation D – transaction limitations

Regulation E – electronic funds transfers

Home banking

Bill payer

Audio response

Debit cards/ATM cards

52

Truth in Savings

Provided at account opening

In person, online

For accounts opened by phone

Mailed within 10 business days

Disclosure of terms and conditions related to the account:

Opening deposit, minimum balance requirements

Payment of interest or dividends, when paid

Fees and rates of interest or dividends

Features of certificates and time accounts

53

Overdraft Privilege/Courtesy Pay

Disclose the categories of transactions that may incur an overdraft fee – this means all debits, not just checks

For example, “overdraft fees may apply to any overdraft created by check, draft, withdrawals, ATM withdrawals, or other electronic means” or

You may incorporate a list of transactions and fees

Disclose fees

Disclose when items might not be paid

54

Account Agreement and Disclosure

In addition to regulatory requirements, the

disclosures contain contractual terms and

conditions of the account

Needs to be provided when account is opened

and is often referenced in the signature card

55

Contractual Terms and Conditions

Termination of account

Accountholder in good standing

Calculation and payment of interest/dividends

Account ownership

Terms and conditions of each type of account

Transaction limitations

Privacy (may be separate notice)

Funds Availability (may be separate notice)

Additional contractual terms

Joint and several liability

Stop payments

Postdating

Stale dating

Endorsement of checks

Truncation of checks

Returned checks/provisional credit

Overdraft privilege conditions

Change of address

Dormant accounts/escheat

Authorization for consumer report

Negative credit report notice

Choice of law

56

Your Ability to Withdraw Funds

Regulation CC: check holds

Provided before (at the time) a transaction (checking) account is opened

Specifies the time period that funds from deposits will be held

Includes normal and exception holds

Holds for new accounts

Any funds held beyond the timeframe specified would receive notice at time a hold is placed

Notice also posted where deposits are accepted

57

Transaction Limitations

Regulation D: limitation on transactions

Usually incorporated into the Truth in Savings Account Agreement and Disclosure

Discloses the limitation of certain transaction from non-transaction (savings) accounts

Maximum of 6 per month or statement cycle – checks and drafts to a third party, debit card, ACH debits, POS, home banking, bill payer, audio response, overdrafts

58

Electronic Funds Transfer

Disclosure required at the time an electronic service is requested or before the first EFT can be made from an account

Outlines the rights and liabilities of the institution and the accountholder

Specific error resolution procedures

Institution contact info, business days

Types of transactions, limitations on transactions

Sharing of information

Fees (including fees charged by others), documentation

Stop payments

59

What is an EFT?

Any transfer of funds that is initiated through an electronic terminal telephone, computer for the purpose of ordering, instructing, or authorizing a financial institution to debit or credit a consumer’s account:

Point of sale; automated teller machines

Direct deposits or withdrawals

Transfers initiated by telephone

Debit card transactions whether or not initiated through a terminal

Check conversions to ACH

Home banking, bill payer, mobile banking

60

Issuance of Access Device

Access device = card, code, or pin

Can be solicited – at the request of the accountholder

Can be unsolicited if:

Not validated at the time

Explanation of how to validate or dispose of

Accompanied by the required disclosures

Validated only in response to an oral or written request by the accountholder

61

Opt In for Overdraft Fees

For ATM and one-time debit card transactions

May include information about other types of transactions that may overdraw account

Consumer must opt-in before a fee can be charged for overdrawing an account

Does not include overdrafts from savings or lines of credit

Provide notice at account opening or upon request for service

62

Opt-In Notice 63

Remote Deposit Capture (RDC)

Consumer’s ability to deposit checks remotely

Not covered by Regulation CC – check holds

Hold timeframes should be disclosed in RDC disclosure and if longer than regular holds, redisclosed often in a manner the consumer is likely to notice

Risk assessment recommended to determine who qualifies for the service, and restrictions or limitations on allowable deposits

Disclosure of terms, limitations, and conditions of RDC use provided at time service is made available (upon request, activation, etc.)

64

Privacy Notice

Federal privacy notice to be provided at account opening

Describes what information about the consumer is collected

Describes what information is shared by the institution and with whom

May provide an opt out from sharing

65

66

Insurance on Accounts

Every federally-insured financial institution must make available a written explanation regarding federal deposit insurance

Provided upon request of accountholder

Disclosures/information available to download online

Privately insured institutions must disclose that accounts are not federally insured on signature cards and statements

67

Providing Disclosures Electronically

Federal law: Electronic Signatures in Global and National Commerce Act (E-SIGN)

State law: Uniform Electronic Transactions Act (UETA)

Both specify how documents required to be in writing may be provided electronically

All the consumer protection regulations allow electronic disclosures if following E-SIGN

68

Requirements of E-SIGN

Cannot require opting in

Cannot automatically opt people in

Pre-disclosure

System requirements, ability to download or print, costs for paper

disclosures, costs to discontinue electronic disclosures, keeping

institution informed of contact information, which products and

services it relates to

Consent – affirmative, demonstrable consent

“consents electronically, or confirms his or her consent

electronically, in a manner that reasonably demonstrates that the

consumer can access information in the electronic form that will be

used to provide the information that is the subject of the consent”

69

Business vs. Consumer

Business accounts are not covered by certain consumer protection regulations:

Truth in Savings

Regulation E

Privacy

The regulations relating to business accounts:

Membership

Identity Theft Red Flags

Regulation CC

Regulation D

Insurance on accounts

CIP/BSA/OFAC

70

Electronic Security Concerns 71

Financial institutions are often liable for unauthorized transactions

Electronic services, RDC, and other means of access pose significant risks

Financial institutions are encouraged to use multi-factor authentication,

particularly in high-risk or high-dollar transactions

Accountholders should be encouraged to:

Select robust passwords (not easy to guess)

Use unique passwords (no duplicates)

Some security experts go so far as to recommend that accountholders do

not answer security questions correctly making it more difficult for

identity thieves to correctly guess security answers

Example: Q. Where did you go to school?

(info on FB, Linked In, professional profile) A. Mushroom

Bank Secrecy Act

Risk assessment determines what constitutes

higher risk for money laundering:

Remote account opening

EFT and RDC services

Red flags at account opening

Internal controls are the policies, procedures, and

processes designed to mitigate the identified risks

72

BSA Account Opening Red Flags

An accountholder uses unusual or suspicious identification documents that cannot be readily verified.

An accountholder provides an individual tax identification number after having previously used a Social Security number.

An accountholder uses different tax identification numbers with variations of his or her name.

An accountholder’s home or business telephone is disconnected.

73

BSA Account Opening Red Flags

A business is reluctant, when establishing a new account, to provide complete information about the nature and purpose of its business, anticipated account activity, prior banking relationships, the names of its officers and directors, or information on its business location.

The accountholder’s background differs from that which would be expected on the basis of his or her business activities.

An accountholder makes frequent or large transactions and has no record of past or present employment experience.

74

Suspicious Activity Report Categories

Identification/Documentation

a. Changes spelling or arrangement of name

b. Multiple individuals with same or similar identities

c. Provided questionable or false documentation

d. Refused or avoided request for documentation

e. Single individual with multiple identities

z. Other (specify type of suspicious activity in space provided)

75

Question Break

76

77

Thanks for Attending!

F O R Q U E S T I O N S , P L E A S E C O N T A C T :

M A R Y - L O U H E I G H E S

C O M P L I A N C E P L U S , I N C .

M H E I G H E S @ C U A S K M E . C O M