Accenture hf s-blueprint-report-telecom-operations-as-a-service-excerpt

58

The Services Research Company Pareekh Jain Research Director [email protected] HfS Blueprint Report Telecom Operations As-a-Service Excerpt for Accenture May 2016

-

Upload

silas-musakali -

Category

Technology

-

view

51 -

download

0

Transcript of Accenture hf s-blueprint-report-telecom-operations-as-a-service-excerpt

The Services Research Company

Pareekh JainResearch [email protected]

HfS Blueprint Report

Telecom Operations As-a-ServiceExcerpt for Accenture

May 2016

©2016 HfSResearch Ltd. Proprietary │Page2Excerpt forAccenture

TOPIC PAGE

ExecutiveSummary 3

TelecomOperationsAs-a-Service 8

Research Methodology 23

KeyMarketDynamics 28

ServiceProviderGrid 44

ServiceProviderProfile 48

Market Wrap-UpandRecommendations 50

About theAuthor 56

Table of Contents

Executive Summary

©2016 HfSResearch Ltd. Proprietary │Page4Excerpt forAccenture

Introduction to the HfS Blueprint Report: Telecom Operations As-a-Service

n The Telecom Operations As-a-Service HfS Blueprint Report is a new look at the evolving marketfor network, fulfilment, billing and assurance services. This Blueprint builds on the 2014 HfSTelecom Operations Services Blueprint to look in greater detail at the outsourcing of this criticalbusiness function for telecom (wireless and wireline) and cable firms and the adoption of the 8Ideals of As-a-Service delivery in this market as well.

n The HfS Blueprint now includes profiles and assessments of eight service providers of TelecomOperations As-a-Service. For the first time, CSS Corp and Aegis are included.

n Unlike other quadrants and matrices, the HfS Blueprint identifies relevant differentials betweenservice providers across a number of facets in twomain categories: innovation and execution.

n For this report, HfS has increased the attention paid to innovation criteria in particular andadopted the new 2016 Blueprint Grid layout to assess service providers. This Grid nowrecognizes up-and-coming service providers (High Potentials) that are scoring higher oninnovation criteria than on execution criteria as the providers build these practices. The Gridincludes a new group of established, high-execution service providers (Execution Powerhouses)that have built effective delivery operations but need to innovate capabilities and offeringsfurther. They are in addition to the pre-existing rankings for highest overall performance(Winners Circle) and strong combined innovation and execution performance (High Performers).

©2016 HfSResearch Ltd. Proprietary │Page5Excerpt forAccenture

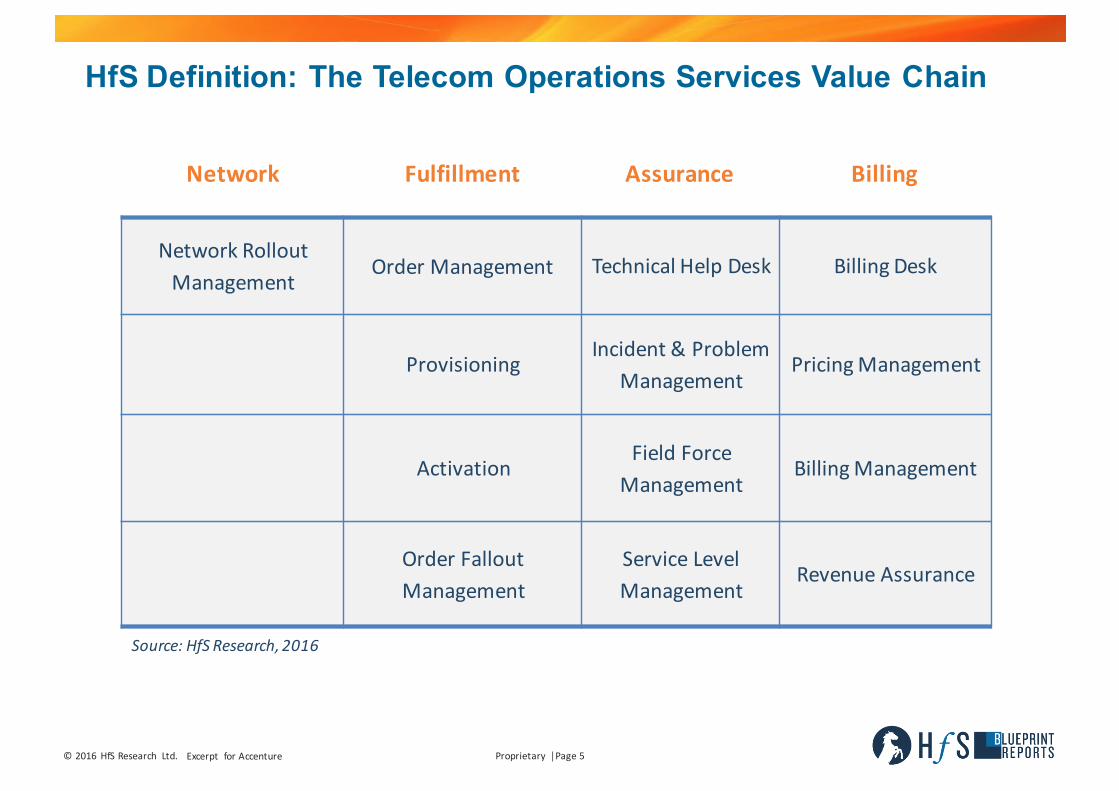

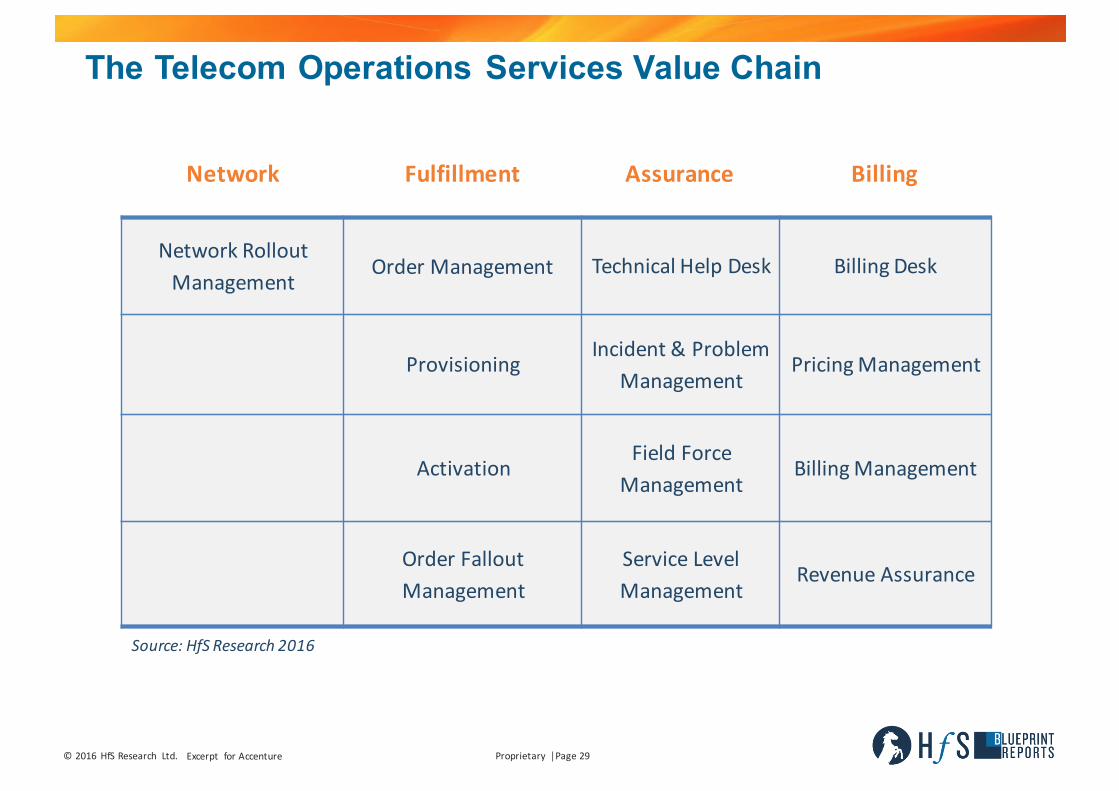

HfS Definition: The Telecom Operations Services Value Chain

Network Fulfillment Assurance Billing

NetworkRolloutManagement

OrderManagement TechnicalHelpDesk BillingDesk

ProvisioningIncident&Problem

ManagementPricingManagement

ActivationFieldForce

ManagementBillingManagement

OrderFalloutManagement

Service LevelManagement

RevenueAssurance

Source:HfSResearch,2016

©2016 HfSResearch Ltd. Proprietary │Page6Excerpt forAccenture

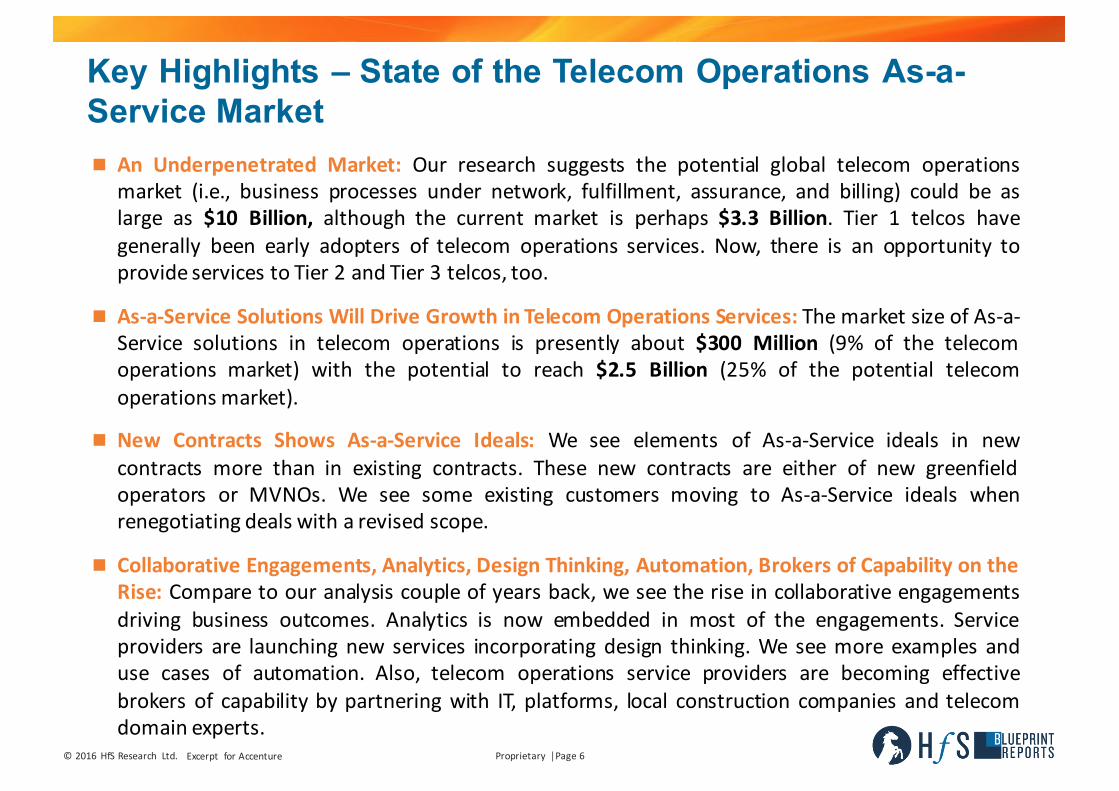

Key Highlights – State of the Telecom Operations As-a-Service Marketn An Underpenetrated Market: Our research suggests the potential global telecom operations

market (i.e., business processes under network, fulfillment, assurance, and billing) could be aslarge as $10 Billion, although the current market is perhaps $3.3 Billion. Tier 1 telcos havegenerally been early adopters of telecom operations services. Now, there is an opportunity toprovide services to Tier 2 and Tier 3 telcos, too.

n As-a-Service Solutions Will Drive Growth in Telecom Operations Services: The market size of As-a-Service solutions in telecom operations is presently about $300 Million (9% of the telecomoperations market) with the potential to reach $2.5 Billion (25% of the potential telecomoperations market).

n New Contracts Shows As-a-Service Ideals: We see elements of As-a-Service ideals in newcontracts more than in existing contracts. These new contracts are either of new greenfieldoperators or MVNOs. We see some existing customers moving to As-a-Service ideals whenrenegotiating deals with a revised scope.

n Collaborative Engagements, Analytics, Design Thinking, Automation, Brokers of Capability on theRise: Compare to our analysis couple of years back, we see the rise in collaborative engagementsdriving business outcomes. Analytics is now embedded in most of the engagements. Serviceproviders are launching new services incorporating design thinking. We see more examples anduse cases of automation. Also, telecom operations service providers are becoming effectivebrokers of capability by partnering with IT, platforms, local construction companies and telecomdomain experts.

©2016 HfSResearch Ltd. Proprietary │Page7Excerpt forAccenture

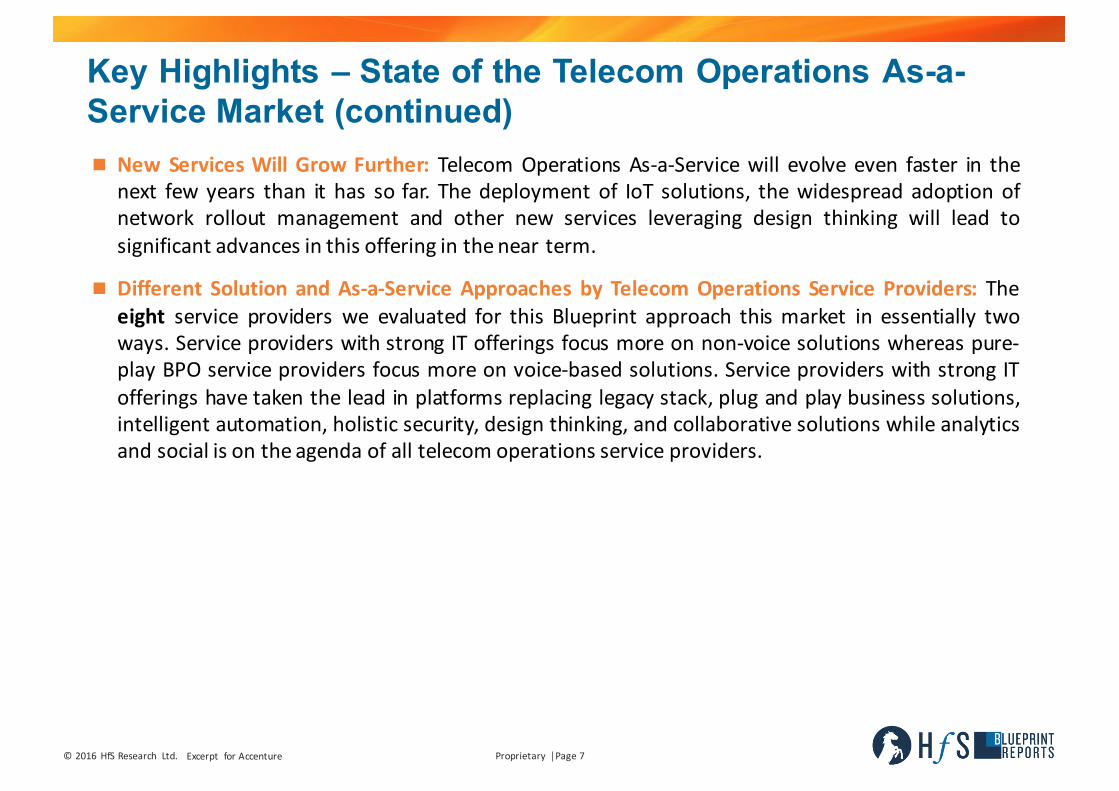

Key Highlights – State of the Telecom Operations As-a-Service Market (continued)n New Services Will Grow Further: Telecom Operations As-a-Service will evolve even faster in the

next few years than it has so far. The deployment of IoT solutions, the widespread adoption ofnetwork rollout management and other new services leveraging design thinking will lead tosignificant advances in this offering in thenear term.

n Different Solution and As-a-Service Approaches by Telecom Operations Service Providers: Theeight service providers we evaluated for this Blueprint approach this market in essentially twoways. Service providers with strong IT offerings focus more on non-voice solutions whereas pure-play BPO service providers focus more on voice-based solutions. Service providers with strong ITofferings have taken the lead in platforms replacing legacy stack, plug and play business solutions,intelligent automation, holistic security, design thinking, and collaborative solutions while analyticsand social is on the agenda of all telecom operations service providers.

Telecom Operations As-a-Service

©2016 HfSResearch Ltd. Excerpt forAccenture

TOOLS/INFRASTRUCTURE GOVERNANCE

Welcome to the As-a-Service EconomyHfSusestheword“economy”toemphasizethattheemergingnextphaseofoutsourcingisamoreflexible,outcomefocusedwayofengagingandmanagingresourcestodeliverservices.OperatingintheAs-a-ServiceEconomymeansarchitectinguseofincreasinglymatureoperatingmodels,enablingtechnologiesandtalenttodrivetargetedbusinessoutcomes.Thefocusisonvaluetotheconsumer.

I.THEOPTIMUMOPERATINGMODEL

Outsourcing|SharedServicesGBS|BPaaS/SaaS/IaaS|Crowdsourcing

II.EMPOWERINGTALENTTOMAKEITALL

POSSIBLECapabilitiesoverSkills|

DefiningOutcomes|Creativity|DataScience

IV.TECHNOLOGYTOAUGMENTKNOWLEDGELABOR

Digitization&RoboticAutomation|Analytics|Mobility|SocialMedia|CognitiveComputing

III.ABURNINGPLATFORMFORCHANGE

GlobalizationofLabor|High-growthEmergingMarkets|

DisruptiveBusinessModels|Consumerization

AS-A-SERVICEECONOMY

Agility|CollaborationOne-to-Many|OutcomeFocus

Plug-and-PlayServices

©2016 HfSResearch Ltd. Excerpt forAccenture

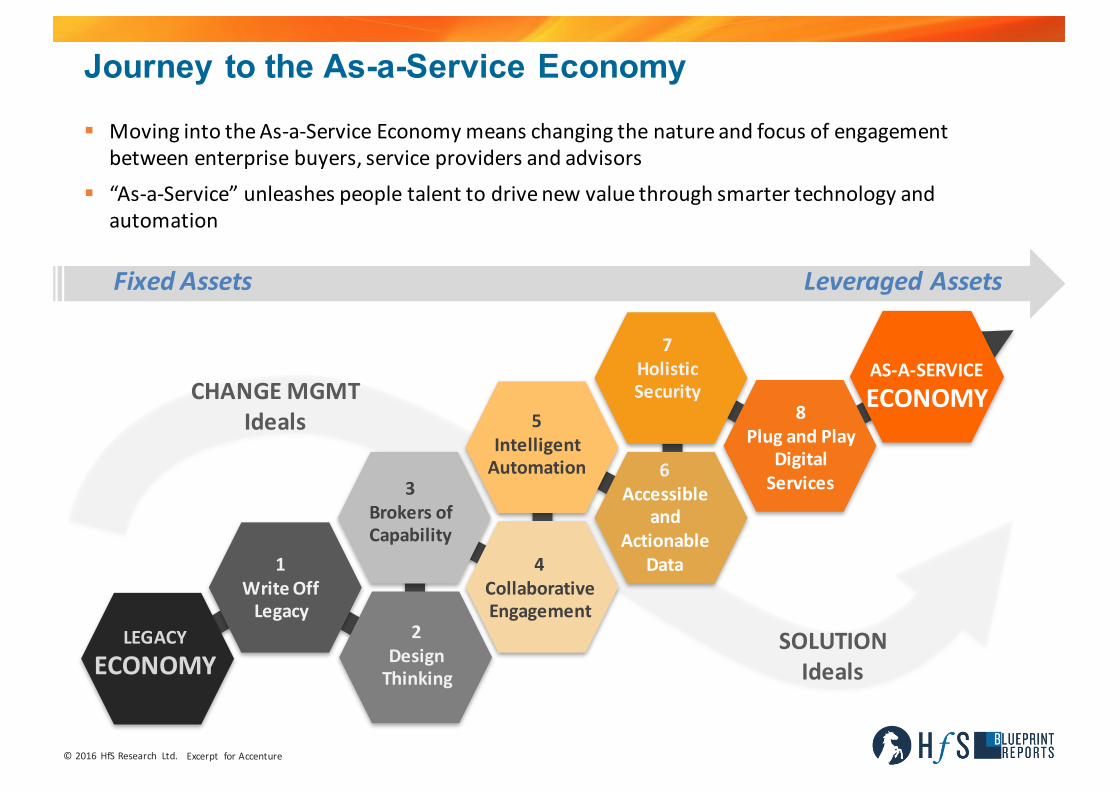

FixedAssetsLeveragedAssets

2DesignThinking

3BrokersofCapability

1WriteOffLegacy

4CollaborativeEngagement

7HolisticSecurity

5IntelligentAutomation 6

Accessibleand

ActionableData

8PlugandPlay

DigitalServices

SOLUTIONIdeals

LEGACYECONOMY

AS-A-SERVICEECONOMYCHANGEMGMT

Ideals

§ MovingintotheAs-a-ServiceEconomymeanschangingthenatureandfocusofengagementbetweenenterprisebuyers,serviceprovidersandadvisors

§ “As-a-Service”unleashespeopletalenttodrivenewvaluethroughsmartertechnologyandautomation

Journey to the As-a-Service Economy

©2016 HfSResearch Ltd. Proprietary │Page11Excerpt forAccenture

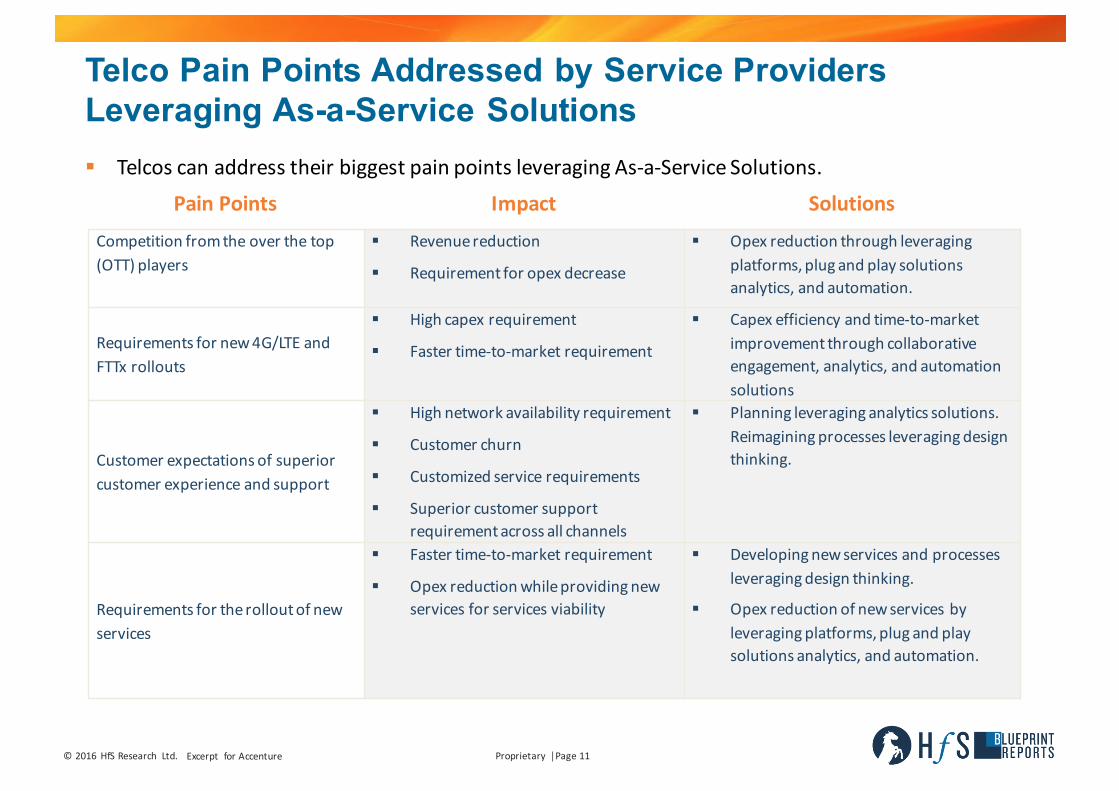

Telco Pain Points Addressed by Service Providers Leveraging As-a-Service Solutions

PainPoints Impact SolutionsCompetitionfromtheoverthetop(OTT)players

§ Revenuereduction

§ Requirementforopexdecrease

§ Opexreductionthroughleveragingplatforms,plug andplaysolutionsanalytics,andautomation.

Requirementsfornew4G/LTEandFTTx rollouts

§ Highcapexrequirement

§ Fastertime-to-marketrequirement

§ Capexefficiencyandtime-to-marketimprovementthrough collaborativeengagement,analytics,andautomationsolutions

Customerexpectationsofsuperiorcustomerexperienceandsupport

§ Highnetworkavailabilityrequirement

§ Customerchurn

§ Customizedservicerequirements

§ Superiorcustomersupportrequirementacrossallchannels

§ Planningleveraginganalyticssolutions.Reimaginingprocessesleveragingdesignthinking.

Requirementsfortherolloutofnewservices

§ Fastertime-to-marketrequirement

§ Opexreductionwhileprovidingnewservicesforservicesviability

§ Developingnewservicesandprocessesleveragingdesignthinking.

§ Opexreductionofnewservicesbyleveragingplatforms,plug andplaysolutions analytics,andautomation.

§ TelcoscanaddresstheirbiggestpainpointsleveragingAs-a-ServiceSolutions.

©2016 HfSResearch Ltd. Proprietary │Page12Excerpt forAccenture

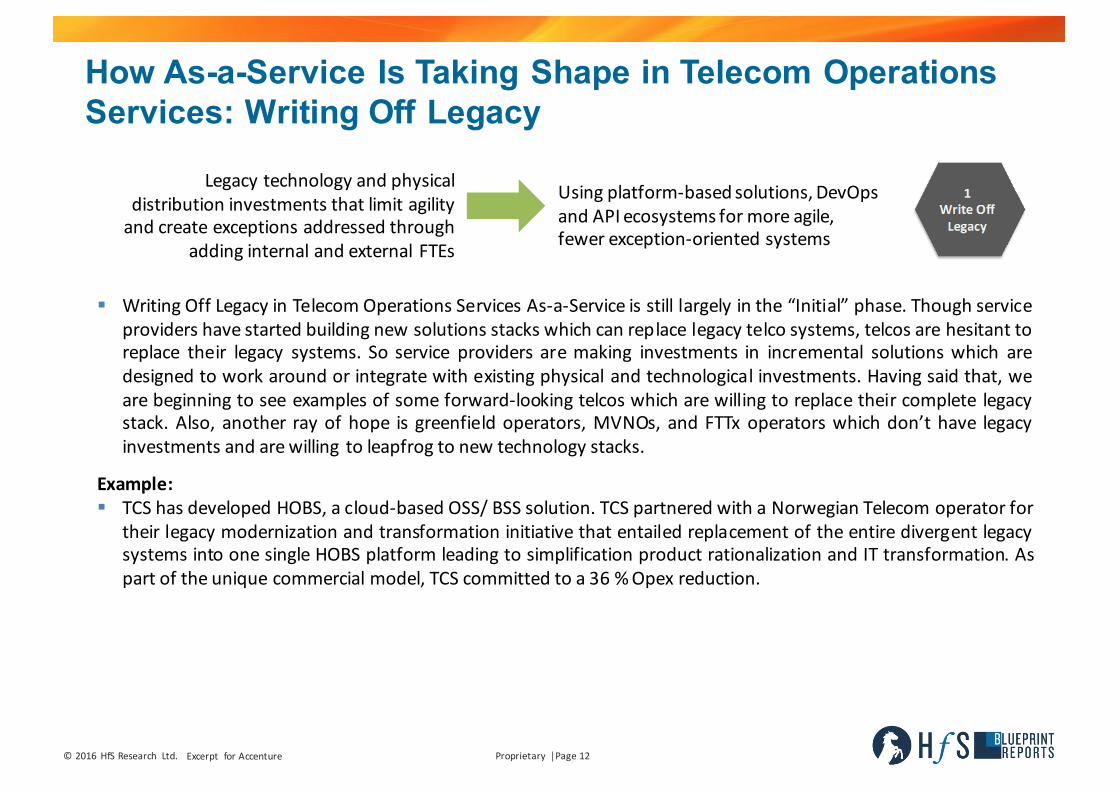

How As-a-Service Is Taking Shape in Telecom Operations Services: Writing Off Legacy

Legacytechnologyandphysicaldistributioninvestments thatlimitagilityandcreate exceptionsaddressedthrough

addinginternalandexternalFTEs

Usingplatform-basedsolutions,DevOpsandAPIecosystemsformoreagile,fewerexception-orientedsystems

§ Writing Off Legacy in Telecom Operations Services As-a-Service is still largely in the “Initial” phase. Though serviceproviders have started building new solutions stacks which can replace legacy telco systems, telcos are hesitant toreplace their legacy systems. So service providers are making investments in incremental solutions which aredesigned to work around or integrate with existing physical and technological investments. Having said that, weare beginning to see examples of some forward-looking telcos which are willing to replace their complete legacystack. Also, another ray of hope is greenfield operators, MVNOs, and FTTx operators which don’t have legacyinvestments and arewilling to leapfrog to new technology stacks.

Example:§ TCS has developed HOBS, a cloud-based OSS/ BSS solution. TCS partnered with a Norwegian Telecom operator for

their legacy modernization and transformation initiative that entailed replacement of the entire divergent legacysystems into one single HOBS platform leading to simplification product rationalization and IT transformation. Aspart of the unique commercial model, TCS committed to a 36 %Opex reduction.

©2016 HfSResearch Ltd. Proprietary │Page13Excerpt forAccenture

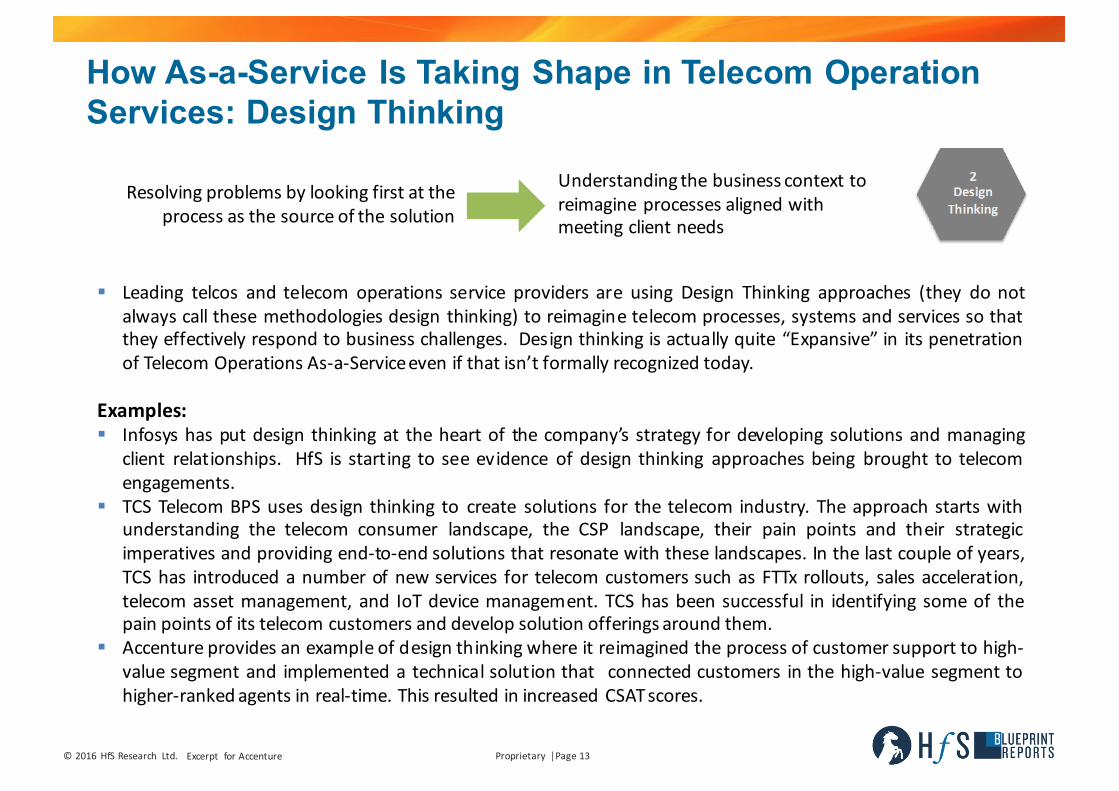

How As-a-Service Is Taking Shape in Telecom Operation Services: Design Thinking

Resolvingproblemsbylookingfirstattheprocessasthesourceofthesolution

Understandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds

§ Leading telcos and telecom operations service providers are using Design Thinking approaches (they do notalways call these methodologies design thinking) to reimagine telecom processes, systems and services so thatthey effectively respond to business challenges. Design thinking is actually quite “Expansive” in its penetrationof Telecom Operations As-a-Serviceeven if that isn’t formally recognized today.

Examples:§ Infosys has put design thinking at the heart of the company’s strategy for developing solutions and managing

client relationships. HfS is starting to see evidence of design thinking approaches being brought to telecomengagements.

§ TCS Telecom BPS uses design thinking to create solutions for the telecom industry. The approach starts withunderstanding the telecom consumer landscape, the CSP landscape, their pain points and their strategicimperatives and providing end-to-end solutions that resonate with these landscapes. In the last couple of years,TCS has introduced a number of new services for telecom customers such as FTTx rollouts, sales acceleration,telecom asset management, and IoT device management. TCS has been successful in identifying some of thepain points of its telecom customers and develop solution offerings around them.

§ Accenture provides an example of design thinking where it reimagined the process of customer support to high-value segment and implemented a technical solution that connected customers in the high-value segment tohigher-rankedagents in real-time. This resulted in increased CSATscores.

©2016 HfSResearch Ltd. Proprietary │Page14Excerpt forAccenture

How As-a-Service Is Taking Shape in Telecom Operations Services: Brokers of Capability

Focusinggovernanceandoperationsstaffonmanagingtotheletterofthecontractandthedecimalpointsofservice levels

Orientinggovernancetosourceexpertisefromallavailablesources,bothinternallyandexternally,toaddresscapabilitygaps

§ Brokers of capability is the ability of a service provider to source expertise from all available sources, bothexternally and internally to address client requirements. It helps service providers to identify current andanticipated needs to deliver business results and to manage capability effectively to deliver those outcomes.Telecom operations service providers work with the variety of players in the ecosystem – consulting firms, ITservices firms, telecom experts, field partners, construction companies, etc. We see this Ideal as “Extensively”available in today’smarket.

Examples:§ TCS provides clients with a wide breadth of expertise in support of the telecom operations. TCS has partnerships

with local field and construction companies in different geographies and it leverages them to provide totalnetwork rollout solutions to telcos. It also brings the telecom domain expertise of telecom companies of TataGroup and offers them on demand in its engagements. Finally, TCS also uses its expertise in IT services, Networkservices and telecom platforms in delivering a total solution to telcos.

§ Accenture has developed a structured platform-led crowdsourcing approach for tapping external and internalcapabilities on demand for its engagement (Accenture Liquid Workforce). Accenture has developed a compellingvision and roadmap of how telcos can transform to become integrated digital service providers (IDSPs) tocompete in the digital economy. The Operations team is working with other Accenture Growth Platforms(Strategy, Digital) in delivering on the IDSPpromise.

§ Other broad-based service providers such as Tech Mahindra, Wipro, Infosys also leverage capabilities in IT andBPO in telecom engagements.

©2016 HfSResearch Ltd. Proprietary │Page15Excerpt forAccenture

How As-a-Service Is Taking Shape in Telecom Operations Services: Collaborative Engagement

§ The key to a sustainable outsourcing engagement is collaboration. Traditionally, business process outsourcingwork has been directive from service buyers to service providers and managed strictly by procurementorganizations. As telcos are facing the threat of survival in the digital world, they are leveraging telecomoperations service providers more strategically. HfS is seeing a move over time to more collaborationengagement where trust and experience are in place, often through shared outcomes and results. The adoptionof practices of collaborative engagement is “Expansive” in Telecom Operations today.

Examples:§ TCS employs a three-level model of collaborative engagement with strategic discussions at the senior

management level, the tactical collaboration between operational managers (supported by a CustomerEngagement Portal) and operational reviews at the day-to-day level. This coupled with its ValueBPS™ approach,which aligns telcos’ strategic objectives with key business metrics, TCS delivers on strategic business outcomessuch as telecom revenue and margin metrics, NPS, time to market, opex and capex reduction, etc.

§ Accenture contracts and manages its telecom engagements with the focus on governance, business outcomesand co-innovation. It has a three-layer approach to governance ensuring tactical, operational and strategicissues and opportunities with a near-, mid-and long-term focus are proactively managed. Clients pointed totangible business outcomes such as capex efficiency, process efficiency, cost reduction, customer satisfaction,delivered by Accenture.

Evaluatingrelationshipsonbaselinesofcost,effortandlabor

Ensuringrelationshipsarecontractedtodrivesustainedexpertiseandoutcomes

©2016 HfSResearch Ltd. Proprietary │Page16Excerpt forAccenture

How As-a-Service Is Taking Shape in Telecom Operations Services: Intelligent Automation

Operatingfragmentedprocessesacrossmultipletechnologieswithsignificant

manualinterventions

Usingofautomationandcognitivecomputingtoblendanalytics,talentandtechnology

§ Intelligent Automation leveraging RPA, autonomics, cognitive and analytics is gaining the interest of telcos. Mostof the early automation case studies in telco business process delivery came from either order management orcustomer support. We have lately observed automation examples in other telco processes such as networkdesign, billing audits, field force management, incident and problem management. Almost all service providersare now offering automation solutions either on their own platforms or leveraging third party solutions. Theadoption of intelligent automation is “Expansive” in Telecom Operations today.

Examples:§ Wipro has a comprehensive approach to intelligent automation in telecom operations combing automation and

analytics. Wipro calls it Cognitive RPA which combines the power of analytics with robotic automation and candeliver a combined improvement of cycle times by higher than 25%, additional operational cost reduction by35% over the traditional approach. Wipro has successfully leverage intelligent automation in several telcoengagements.

§ Accenture Operations is committed to bringing higher levels of automation to all of its engagements. Last yearthe total impact of all automation solutions was a 14 percent productivity improvement. In telecom operations,Accenture’s automation initiatives cover complete value chain including network, fulfillment, assurance andbilling.

©2016 HfSResearch Ltd. Proprietary │Page17Excerpt forAccenture

AUTOMATION

• ServiceDeskandWebChatAutomation:IncreasingproductivityofL1supportwithautomatedtools.Theuseofrobotstoanswersimplequeriesandrepetitivequestions.

• FieldForceAutomation:Enablingfieldtechnicianstoworkeffectivelybyautomatingsomeoftheirprocessesandprovidingtechnicalandoperationalexpertiseondemand.UsingGoogleGlasstoautomatevideotransferofnetworkrepairandautomateticketclosure.Usingautomationtoreducefalseorghosttickets,thusreducingthemeantimetorepair.

• NetworkDrawingAutomation:Reducingnetworkdrawingtimebyautomatingnetworkdiagramproductionandanalysisprocess.

• OrderManagementandProvisioningAutomation:Performingautomaticqualitychecksinordermanagementandprovisioningprocesses,thussavingactivationtime.

• BillingAutomation:Automatingthemajorityofauditchecksinthebillingprocess,thusreducingFTEeffortandAHT.

• AutomatedSelf-Care:Automatedtechnicalscanforsubscribers,toidentifyissuesthatcouldimpedeserviceperformance.

• ApplicationAutomation:Provideaunifiedorsinglescreen/sourceofinformationtoagentsbyeliminatingswitchingfromscreentoscreen.Provideaunifiedapplicationtotheworkforceinthefieldbyintegratingotherapplicationsfortheworkforceinthefield.

Automation Examples in Telecom Operations As-a-Service

©2016 HfSResearch Ltd. Proprietary │Page18Excerpt forAccenture

How As-a-Service Is Taking Shape in Telecom Operations Services: Accessible and Actionable Data

Performingad-hocanalysisonunstructureddatawithlittleintegrationor

businesscontext

Applyinganalyticstechnologies,processesandresourcestorelevantdatasetstoderiveinsightsthatcanhelpimproveanenterprise

§ Taking advantage of Accessible and Actionable Data is at the very heart of Telecom As-a-Service operations.Telcos were the early adopter for actionable analytics when they started leveraging analytics to reduce customerchurn. Now analytics is leveraged across all telecom processes including network, fulfillment, assurance, andbilling for deriving insights and that either the service provider and/or the telco can act upon to improve thebusiness. This Ideal is “Extensive” in its application within the current Telecom Operations Services As-a-Servicemarket.

Examples:§ Accenture has embedded analytics in 100% of telecom operations engagements. Accenture combines financial,

business/operations, network and customer analytics in a holistic way. Accenture’s analytics team hasdeveloped analytics apps for telecom operations e.g. Incident Management, Ticket Triage and Intelligent OrderManagement. These apps are customizable per client requirement and reduce time to generate insights.

§ TCS has comprehensive analytics offerings and offers analytic solutions across the telecom value chain to helptelcos increase sales, decrease operational cost, reduce churn and fraud, and improve risk management. TCSalso has filed two patents for telecom analytics framework recently.

©2016 HfSResearch Ltd. Proprietary │Page19Excerpt forAccenture

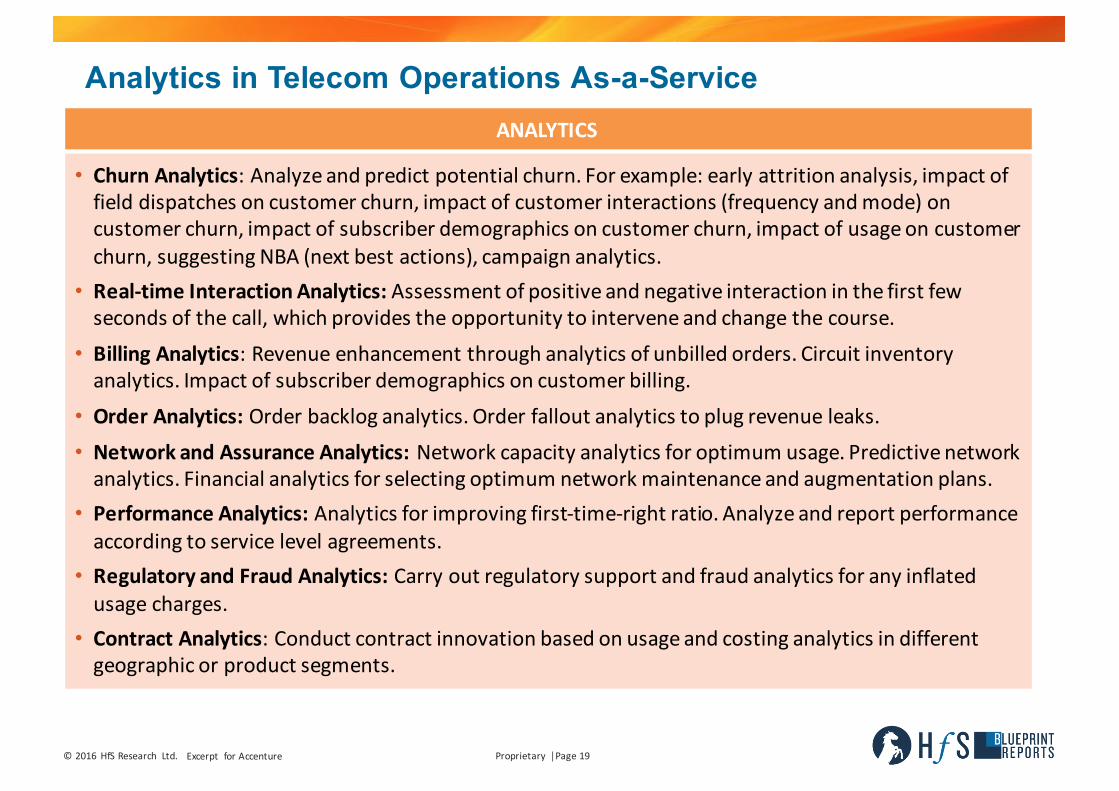

ANALYTICS

• ChurnAnalytics:Analyzeandpredictpotentialchurn.Forexample:earlyattritionanalysis,impactoffielddispatchesoncustomerchurn,impactofcustomerinteractions(frequencyandmode)oncustomerchurn,impactofsubscriberdemographicsoncustomerchurn,impactofusageoncustomerchurn,suggestingNBA(nextbestactions),campaignanalytics.

• Real-timeInteractionAnalytics:Assessmentofpositiveandnegativeinteractioninthefirstfewsecondsofthecall,whichprovidestheopportunitytointerveneandchangethecourse.

• BillingAnalytics:Revenueenhancementthroughanalyticsofunbilledorders.Circuitinventoryanalytics.Impactofsubscriberdemographicsoncustomerbilling.

• OrderAnalytics:Orderbackloganalytics.Orderfalloutanalyticstoplugrevenueleaks.• NetworkandAssuranceAnalytics:Networkcapacityanalyticsforoptimumusage.Predictivenetworkanalytics.Financialanalyticsforselectingoptimumnetworkmaintenanceandaugmentationplans.

• PerformanceAnalytics:Analyticsforimprovingfirst-time-rightratio.Analyzeandreportperformanceaccordingtoservicelevelagreements.

• RegulatoryandFraudAnalytics: Carryoutregulatorysupportandfraudanalyticsforanyinflatedusagecharges.

• ContractAnalytics:Conductcontractinnovationbasedonusageandcostinganalyticsindifferentgeographicorproductsegments.

Analytics in Telecom Operations As-a-Service

©2016 HfSResearch Ltd. Proprietary │Page20Excerpt forAccenture

How As-a-Service Is Taking Shape in Telecom Operations Services: Holistic Security

Respondingreactivelywithpost-eventfixes.Little focusonend-to-endprocess

valuechains

Proactivelymanagingdigitaldataacrossservicechainofpeople,systemsandprocesses

§ Holistic Security is a critical element in telecom operations as telecom operations are highways on whichenterprise and customer data flows. However, it is handled by the separate specialized group which is often partof IT or network practices. From BPO service providers, we don’t hear much about holistic security. We believesecurity services should be part of the total solution and aligned to BPO or operations group too. In IoT world,the data will explode and telecom operations group will be the critical part of delivering holistic securitysolutions to telcos. We are observing that a couple of service providers are beginning to align their securitypractices with operations group and this trend will become extensive over time.

Example:§ Accenture has 360° approach addresses spectrum of security across people, processes, technology. Accenture’s

Security practice is part of Accenture Operations. The core value proposition for combining security withoperations team is collaborations. This is true both within the security team and through the locational synergywith Accenture’s existing cloud, analytics, automation, and operations staff already located in Bangalore. We’rehopeful this collaboration will result in a greater level of system awareness by all parties, and potential decreasethe time to plan foror respond to cyber threats.

§ CSS Corp is a niche service provider offering network and assurance services to telecom customers. Along withthis, it also has enterprise security practicewhich is aligned with assurance or tech support practice. As they aredeveloping tech support solution for IoT they are also aligning them with security solutions for potential threatsof cyber crime in IoT.

©2016 HfSResearch Ltd. Proprietary │Page21Excerpt forAccenture

How As-a-Service Is Taking Shape in Telecom Operations Services: Plug and Play Digital Business Services

Undertakingcomplexandoftenpainfultechnologytransitionstoreachasteady

state

Plugginginto“readytogo”businessoutcome–focused,people,processandtechnologywithsecuritymeasures

§ Telecom operations service providers have started partnering with clients in developing and deploying Plug andPlay Digital Business Services. As telcos are hesitant to replace their legacy systems, service providers aremakinginvestments in incremental solutions which are designed to work around or integrate with existing physical andtechnological investments. Typically, they have taken the form of point solutions for order management, billingmanagement, problem or incident management, contact center, social media, revenue assurance, analytics, etc.We see these solutions as being at the “Expansive” stage of development with significant progress forecastedover the next few years as telcos becomemore comfortablewith these solutions.

Example:§ Tech Mahindra has developed an in-house Carexa platform which consists of in-house tools such as OrderVu,

OrderFix, Socio, Tecnico, and Uno and also third party tools. Tech Mahindra offers business process as a service(BPaaS) to the telcos on Carexa platforms. OrderFix is a cloud-based order orchestration platform, OrderVuhelps plug revenue leakage, Socio helps in social media support, Tecnico helps in remote technical support, andUno is automation.

§ The TCS platform components are built with a modular design instead of monolithic applications. Takingsystems based approach platform solutions cater to entire processes rather than just point applications. Thisenables customers to “pick-and-choose” services and applications from platform portfolio. TCS has integratedits differentpoint solutions with its flagship OSS/BSS solutionHOBS.

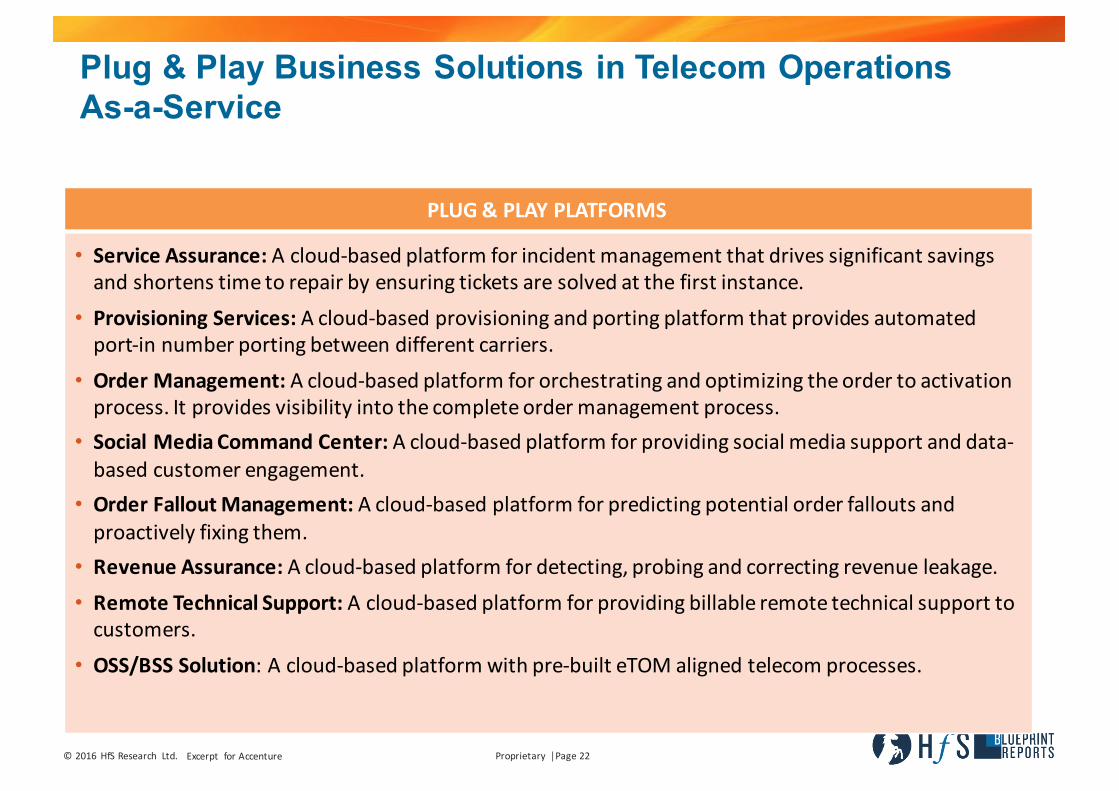

©2016 HfSResearch Ltd. Proprietary │Page22Excerpt forAccenture

PLUG&PLAYPLATFORMS

• ServiceAssurance:Acloud-basedplatformforincidentmanagementthatdrivessignificantsavingsandshortenstimetorepairbyensuringticketsaresolvedatthefirstinstance.

• ProvisioningServices:Acloud-basedprovisioningandportingplatformthatprovidesautomatedport-innumberportingbetweendifferentcarriers.

• OrderManagement:Acloud-basedplatformfororchestratingandoptimizingtheordertoactivationprocess.Itprovidesvisibilityintothecompleteordermanagementprocess.

• SocialMediaCommandCenter:Acloud-basedplatformforprovidingsocialmediasupportanddata-basedcustomerengagement.

• OrderFalloutManagement: Acloud-basedplatformforpredictingpotentialorderfalloutsandproactivelyfixingthem.

• RevenueAssurance:Acloud-basedplatformfordetecting,probingandcorrectingrevenueleakage.• RemoteTechnicalSupport:Acloud-basedplatformforprovidingbillableremotetechnicalsupporttocustomers.

• OSS/BSSSolution:Acloud-basedplatformwithpre-builteTOMalignedtelecomprocesses.

Plug & Play Business Solutions in Telecom Operations As-a-Service

Research Methodology

©2016 HfSResearch Ltd. Proprietary │Page24Excerpt forAccenture

Blueprint Research MethodologyDataSummaryn DatawascollectedinQ12016andQ22016,covering

buyers,providersandadvisors/influencers ofTelecomOperationsServices.

n Morethan500datapointswerecollected,covering8majorserviceproviders.

ParticipatingServiceProviders

ThisReportIsBasedOn:

n TalesfromtheTrenches:Interviewswereconductedwithbuyerswhohaveevaluatedserviceprovidersandexperiencedtheservices.Someweresupplied byserviceproviders,butmanyinterviewswereconductedbyHfSExecutiveCouncilmembersandparticipantsinourextensivemarketresearch.

n Sell-SideExecutiveBriefings:Structureddiscussions withserviceproviderswereintendedtocollectdatanecessarytoevaluateinnovation,executionandmarketshare,anddealcounts.

n PubliclyAvailableInformation:Financialdata,websiteinformation,presentationsgivenbyseniorexecutivesandothermarketingcollateralwereevaluated.

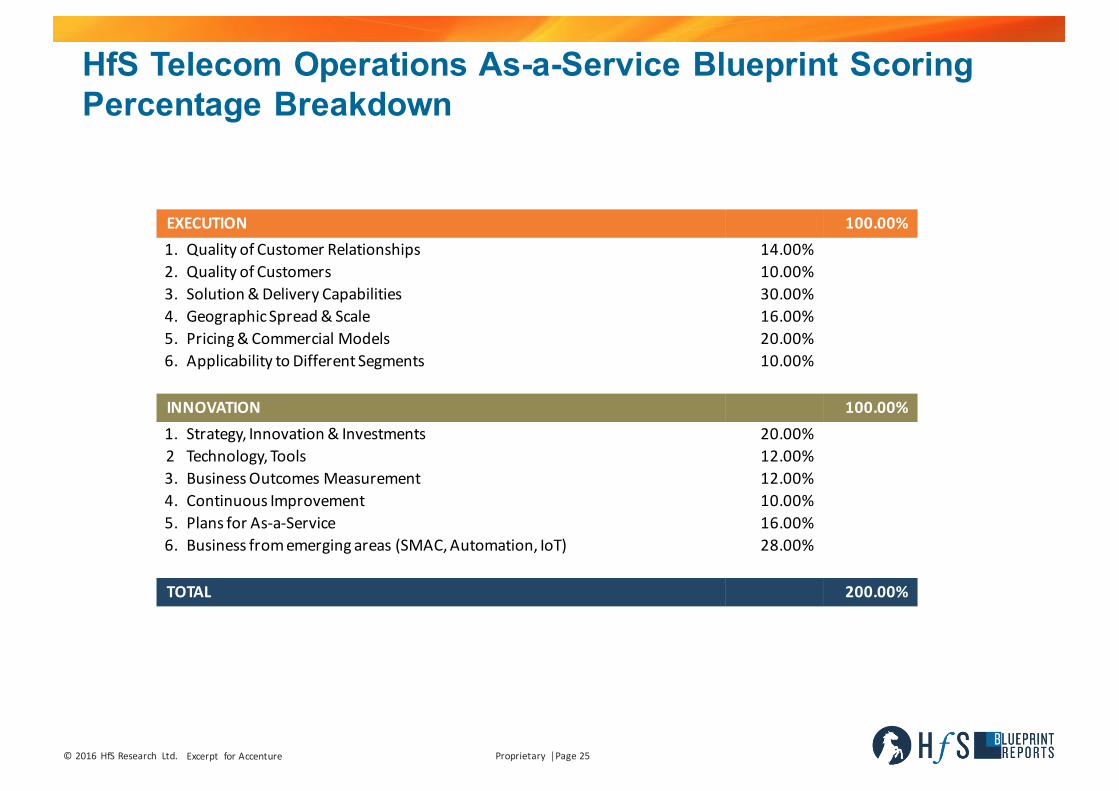

©2016 HfSResearch Ltd. Proprietary │Page25Excerpt forAccenture

HfS Telecom Operations As-a-Service Blueprint Scoring Percentage Breakdown

EXECUTION 100.00%1. Quality ofCustomerRelationships 14.00%2. QualityofCustomers 10.00%3. Solution&DeliveryCapabilities 30.00%4. GeographicSpread&Scale 16.00%5. Pricing&CommercialModels 20.00%6. ApplicabilitytoDifferent Segments 10.00%

INNOVATION 100.00%1. Strategy,Innovation&Investments 20.00%2 Technology,Tools 12.00%3. BusinessOutcomesMeasurement 12.00%4. ContinuousImprovement 10.00%5. PlansforAs-a-Service 16.00%6. Businessfromemergingareas(SMAC,Automation,IoT) 28.00%

TOTAL 200.00%

©2016 HfSResearch Ltd. Proprietary │Page26Excerpt forAccenture

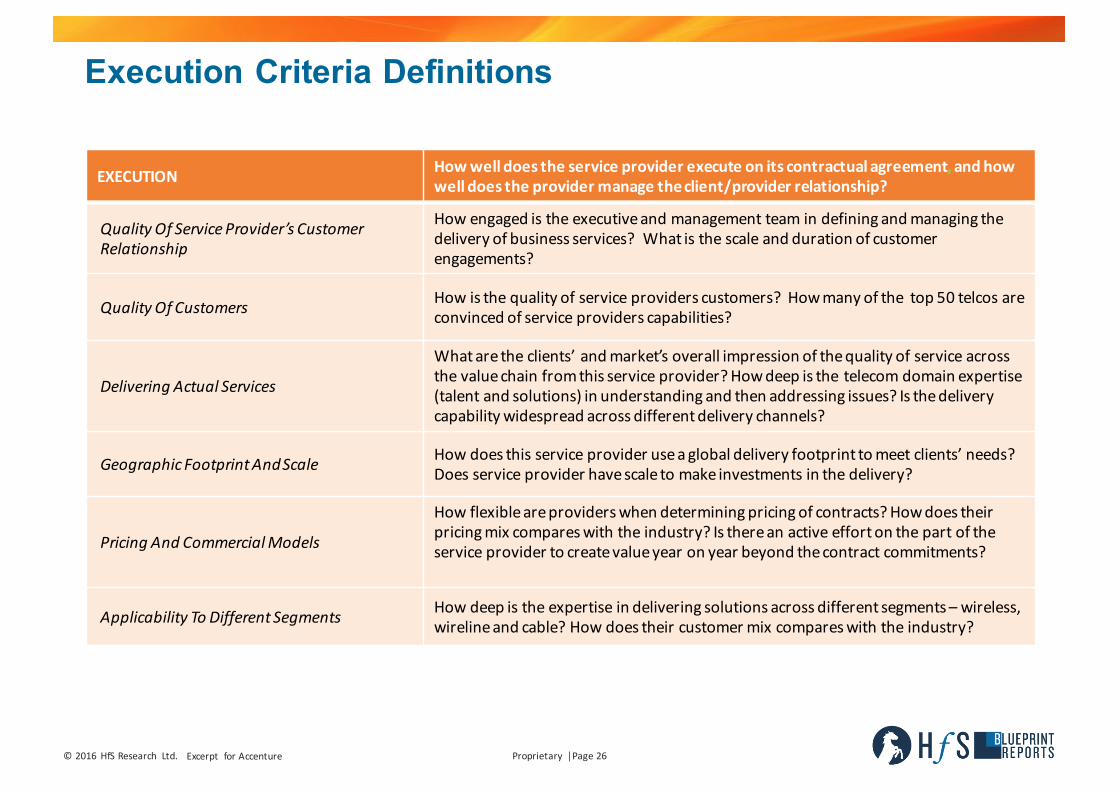

Execution Criteria Definitions

EXECUTION Howwelldoestheserviceproviderexecuteonitscontractualagreement,andhowwelldoestheprovidermanagetheclient/providerrelationship?

QualityOfServiceProvider’sCustomerRelationship

Howengagedis theexecutiveandmanagementteamindefiningandmanagingthedeliveryofbusinessservices?Whatisthescaleanddurationofcustomerengagements?

QualityOfCustomers Howisthequalityofserviceproviderscustomers?Howmanyofthetop50telcosareconvincedofserviceproviderscapabilities?

DeliveringActualServices

Whatarethe clients’andmarket’soverallimpressionofthequalityofserviceacrossthevaluechainfromthisserviceprovider?Howdeep isthetelecomdomainexpertise(talentandsolutions)inunderstandingandthenaddressingissues?Isthedeliverycapabilitywidespreadacrossdifferentdeliverychannels?

GeographicFootprintAndScale Howdoesthisserviceprovideruseaglobaldeliveryfootprinttomeetclients’needs?Doesserviceproviderhavescaletomakeinvestmentsinthedelivery?

Pricing AndCommercialModels

Howflexibleareproviderswhendeterminingpricingofcontracts?Howdoestheirpricingmixcompareswiththeindustry?Isthereanactiveeffortonthepartoftheserviceprovidertocreatevalueyearonyearbeyondthecontractcommitments?

ApplicabilityToDifferent Segments Howdeep istheexpertiseindeliveringsolutionsacrossdifferentsegments– wireless,wirelineandcable?Howdoestheircustomer mixcompareswiththeindustry?

©2016 HfSResearch Ltd. Proprietary │Page27Excerpt forAccenture

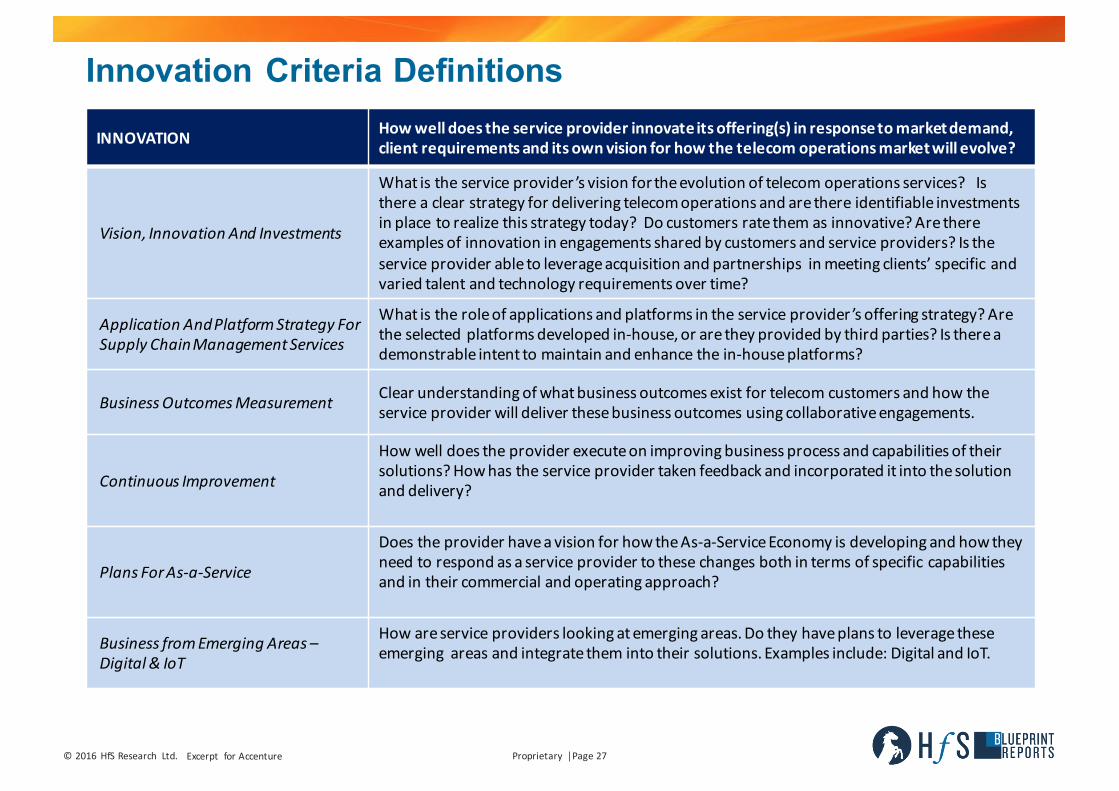

Innovation Criteria Definitions

INNOVATION Howwelldoestheserviceproviderinnovateitsoffering(s)inresponsetomarketdemand,clientrequirements anditsownvisionforhowthetelecomoperationsmarketwillevolve?

Vision, InnovationAndInvestments

Whatistheserviceprovider ’svision fortheevolutionoftelecomoperationsservices?Isthereaclearstrategyfordeliveringtelecomoperationsandarethereidentifiableinvestmentsinplacetorealizethisstrategytoday?Docustomersratethemasinnovative?Arethereexamplesofinnovationinengagementssharedbycustomersandserviceproviders?Istheserviceproviderabletoleverageacquisitionandpartnerships inmeetingclients’specificandvariedtalentandtechnologyrequirementsovertime?

Application AndPlatformStrategyForSupplyChainManagementServices

Whatistheroleof applicationsandplatformsintheserviceprovider ’sofferingstrategy?Aretheselectedplatformsdevelopedin-house,oraretheyprovidedbythirdparties?Isthereademonstrableintenttomaintainandenhancethein-houseplatforms?

BusinessOutcomesMeasurement Clearunderstandingofwhatbusinessoutcomesexistfortelecomcustomersandhowtheserviceproviderwilldeliverthesebusinessoutcomes usingcollaborativeengagements.

ContinuousImprovement

Howwelldoestheproviderexecuteonimprovingbusinessprocessandcapabilitiesoftheirsolutions?Howhas theserviceprovidertakenfeedbackandincorporateditintothesolutionanddelivery?

PlansForAs-a-Service

DoestheproviderhaveavisionforhowtheAs-a-ServiceEconomy isdevelopingandhowtheyneedtorespondasaserviceprovidertothesechangesbothintermsofspecificcapabilitiesandintheircommercialandoperatingapproach?

BusinessfromEmergingAreas–Digital&IoT

Howareserviceproviderslookingatemergingareas.Dotheyhaveplanstoleveragetheseemergingareasandintegratethemintotheirsolutions.Examplesinclude:DigitalandIoT.

Key Market Dynamics

©2016 HfSResearch Ltd. Proprietary │Page29Excerpt forAccenture

The Telecom Operations Services Value Chain

Network Fulfillment Assurance Billing

NetworkRolloutManagement

OrderManagement TechnicalHelpDesk BillingDesk

ProvisioningIncident&Problem

ManagementPricingManagement

ActivationFieldForce

ManagementBillingManagement

OrderFalloutManagement

Service LevelManagement

RevenueAssurance

Source:HfSResearch2016

©2016 HfSResearch Ltd. Proprietary │Page30Excerpt forAccenture

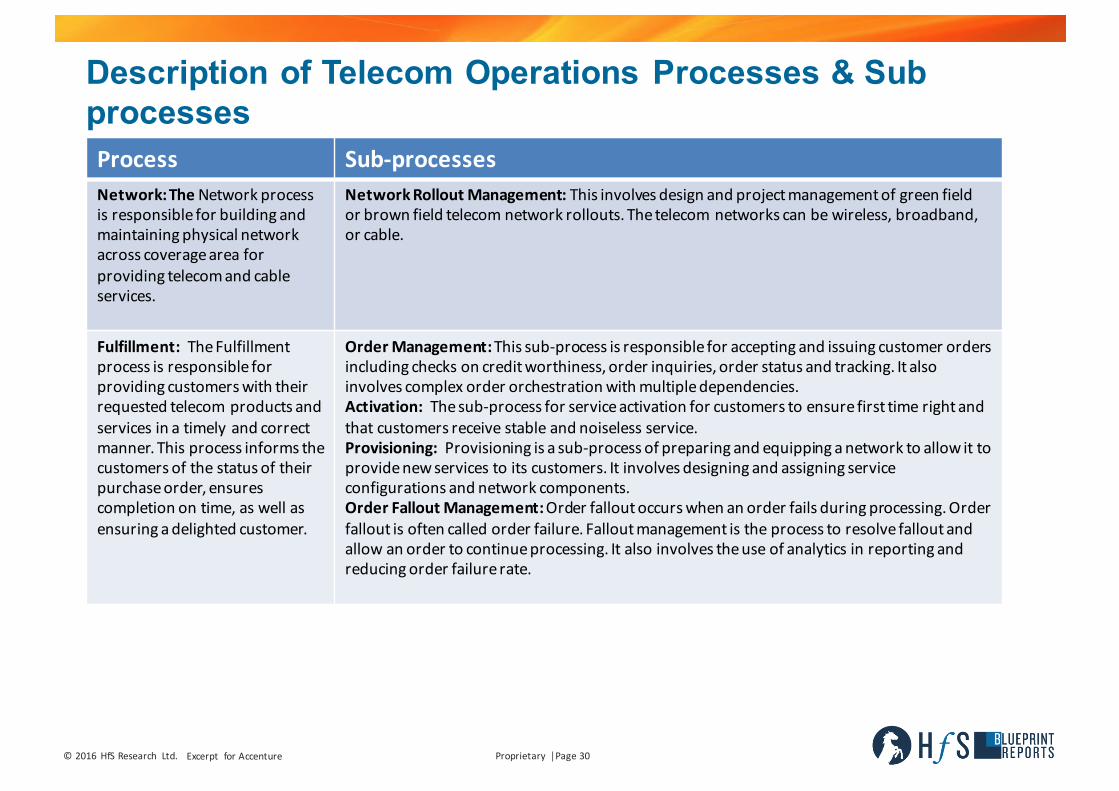

Description of Telecom Operations Processes & Sub processesProcess Sub-processesNetwork:TheNetworkprocessisresponsibleforbuildingandmaintainingphysicalnetworkacrosscoverageareaforprovidingtelecomandcableservices.

NetworkRolloutManagement:Thisinvolvesdesignandprojectmanagementofgreenfieldorbrownfieldtelecomnetworkrollouts.Thetelecomnetworkscanbewireless,broadband,orcable.

Fulfillment: TheFulfillmentprocessisresponsibleforprovidingcustomerswiththeirrequestedtelecomproductsandservicesinatimelyandcorrectmanner.Thisprocessinformsthecustomersofthestatusoftheirpurchaseorder,ensurescompletionontime,aswellasensuringadelightedcustomer.

OrderManagement:Thissub-processisresponsibleforacceptingandissuingcustomerordersincludingchecksoncreditworthiness,orderinquiries,orderstatusandtracking.Italsoinvolvescomplexorderorchestrationwithmultipledependencies.Activation: Thesub-processforserviceactivationforcustomerstoensurefirsttimerightandthatcustomersreceivestableandnoiselessservice.Provisioning: Provisioningisasub-processofpreparingandequippinganetworktoallowittoprovidenewservicestoitscustomers.Itinvolvesdesigningandassigningserviceconfigurationsandnetworkcomponents.OrderFalloutManagement:Orderfalloutoccurswhenanorderfailsduringprocessing.Orderfalloutisoftencalled orderfailure. Falloutmanagement istheprocesstoresolvefalloutandallowanordertocontinueprocessing. Italsoinvolvestheuseofanalyticsinreportingandreducingorderfailurerate.

©2016 HfSResearch Ltd. Proprietary │Page31Excerpt forAccenture

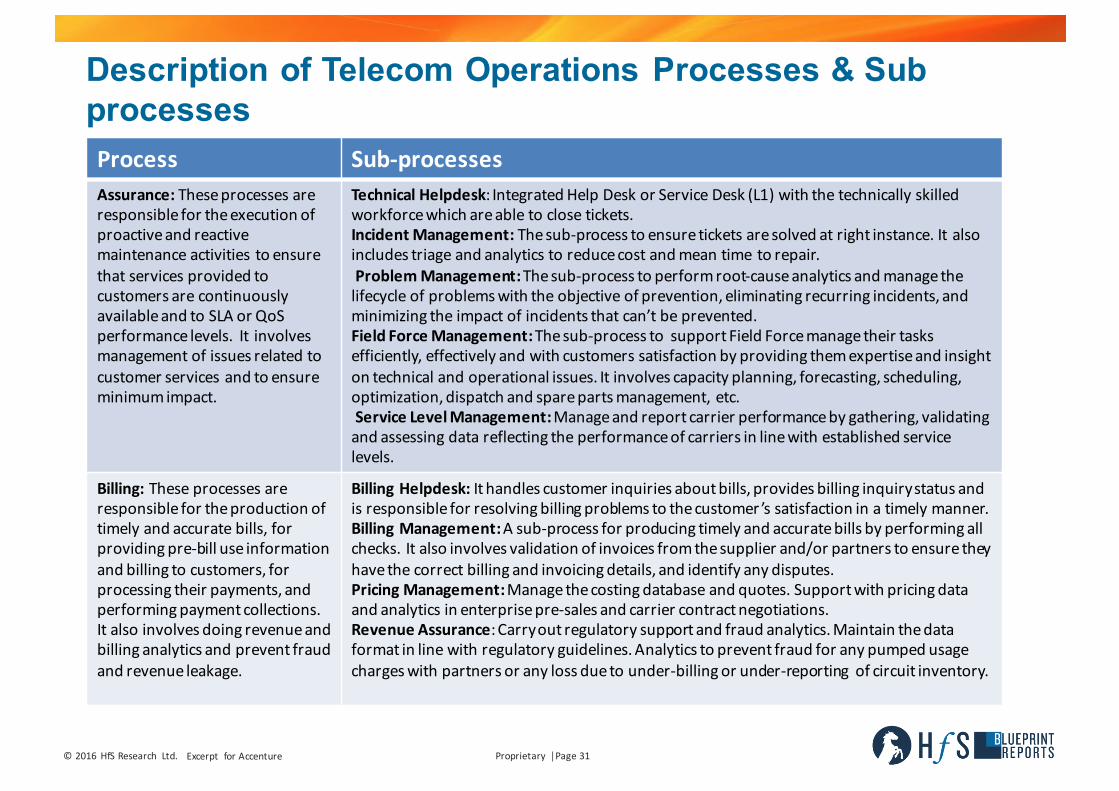

Description of Telecom Operations Processes & Sub processesProcess Sub-processesAssurance:TheseprocessesareresponsiblefortheexecutionofproactiveandreactivemaintenanceactivitiestoensurethatservicesprovidedtocustomersarecontinuouslyavailableandtoSLAorQoSperformancelevels.It involvesmanagementofissuesrelatedtocustomerservicesandtoensureminimumimpact.

TechnicalHelpdesk:IntegratedHelpDeskorServiceDesk(L1)withthetechnicallyskilledworkforcewhichareabletoclosetickets.IncidentManagement: Thesub-processtoensureticketsaresolvedatrightinstance.Italsoincludestriageandanalyticstoreducecostandmeantimetorepair.ProblemManagement:Thesub-processtoperformroot-causeanalyticsandmanagethelifecycleofproblemswiththeobjectiveofprevention,eliminatingrecurringincidents,andminimizingtheimpactofincidentsthatcan’tbeprevented.FieldForceManagement:Thesub-processtosupportFieldForcemanagetheirtasksefficiently,effectivelyandwithcustomerssatisfactionbyprovidingthemexpertiseandinsightontechnicalandoperationalissues.Itinvolvescapacityplanning,forecasting,scheduling,optimization,dispatchandsparepartsmanagement,etc.ServiceLevelManagement:Manageandreportcarrierperformancebygathering,validatingandassessingdatareflectingtheperformanceofcarriersinlinewithestablishedservicelevels.

Billing:Theseprocessesareresponsiblefortheproductionoftimelyandaccuratebills,forprovidingpre-billuseinformationandbillingtocustomers,forprocessingtheirpayments,andperformingpaymentcollections.Italsoinvolvesdoingrevenueandbillinganalyticsandpreventfraudandrevenueleakage.

BillingHelpdesk: Ithandlescustomerinquiriesaboutbills,providesbillinginquirystatusandisresponsibleforresolvingbillingproblemstothecustomer ’ssatisfactioninatimelymanner.BillingManagement:Asub-processforproducingtimelyandaccuratebillsbyperformingallchecks. Italsoinvolvesvalidationofinvoicesfromthesupplierand/orpartnerstoensuretheyhavethecorrectbillingandinvoicingdetails,andidentifyanydisputes.PricingManagement:Managethecostingdatabaseandquotes.Supportwithpricingdataandanalyticsinenterprisepre-salesandcarriercontractnegotiations.RevenueAssurance:Carryoutregulatorysupportandfraudanalytics.Maintainthedataformatinlinewithregulatoryguidelines.Analyticstopreventfraudforanypumpedusagechargeswithpartnersoranylossduetounder-billingorunder-reportingofcircuitinventory.

©2016 HfSResearch Ltd. Proprietary │Page32Excerpt forAccenture

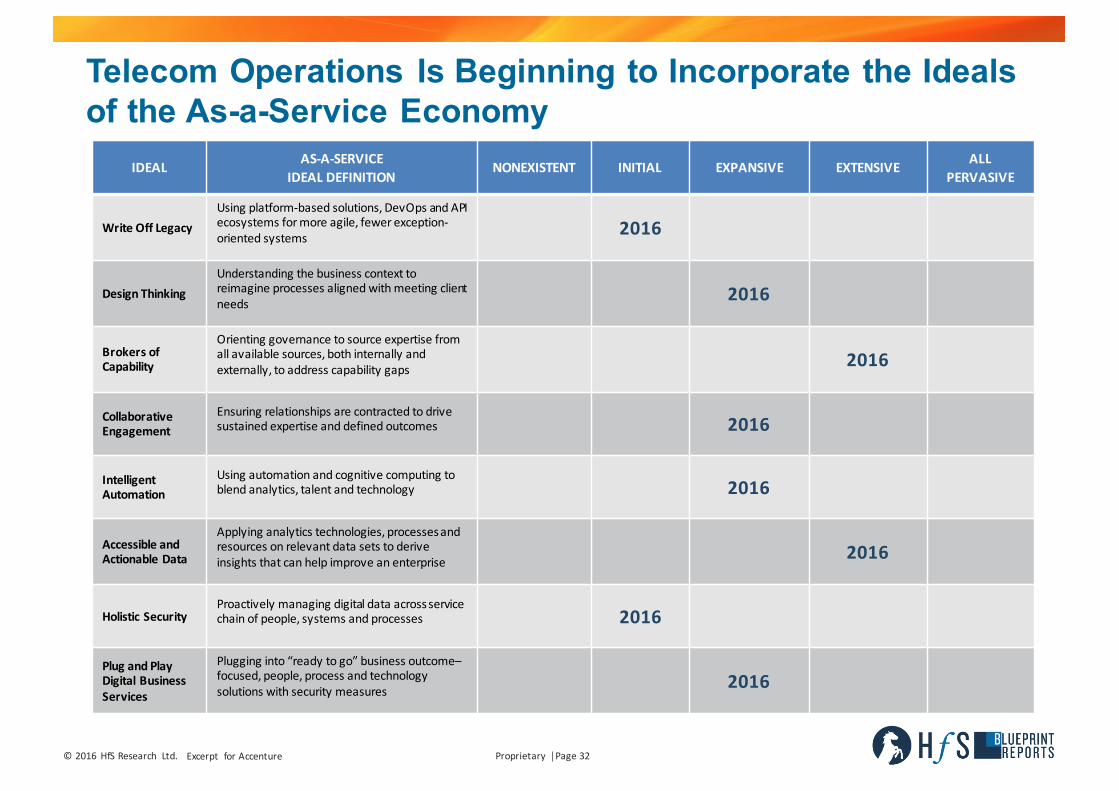

Telecom Operations Is Beginning to Incorporate the Ideals of the As-a-Service Economy

IDEAL AS-A-SERVICEIDEALDEFINITION

NONEXISTENT INITIAL EXPANSIVE EXTENSIVE ALLPERVASIVE

WriteOffLegacyUsingplatform-basedsolutions,DevOpsandAPIecosystemsformoreagile,fewerexception-orientedsystems 2016

DesignThinkingUnderstandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds 2016

Brokers ofCapability

Orientinggovernance tosourceexpertisefromallavailablesources,bothinternallyandexternally,toaddresscapabilitygaps 2016

CollaborativeEngagement

Ensuring relationshipsarecontractedtodrivesustainedexpertiseanddefinedoutcomes 2016

IntelligentAutomation

Using automationandcognitivecomputingtoblendanalytics,talentandtechnology 2016

AccessibleandActionableData

Applyinganalyticstechnologies,processesandresourcesonrelevantdatasetstoderiveinsightsthatcanhelpimproveanenterprise 2016

HolisticSecurityProactivelymanagingdigitaldataacrossservicechainofpeople,systemsandprocesses 2016

Plug andPlayDigitalBusinessServices

Plugginginto“readytogo”business outcome–focused, people,processandtechnologysolutionswithsecuritymeasures 2016

©2016 HfSResearch Ltd. Proprietary │Page33Excerpt forAccenture

Multi-Dimension Analysis* of Telecom Operations Services

Customers

GeographyServiceOfferings

TelecomOperationsServices

Training

CustomerRelationships

CustomerQuality

* Basedonparticipatingserviceprovider’sdata

PricingOnshorevs.Offshore

©2016 HfSResearch Ltd. Proprietary │Page34Excerpt forAccenture

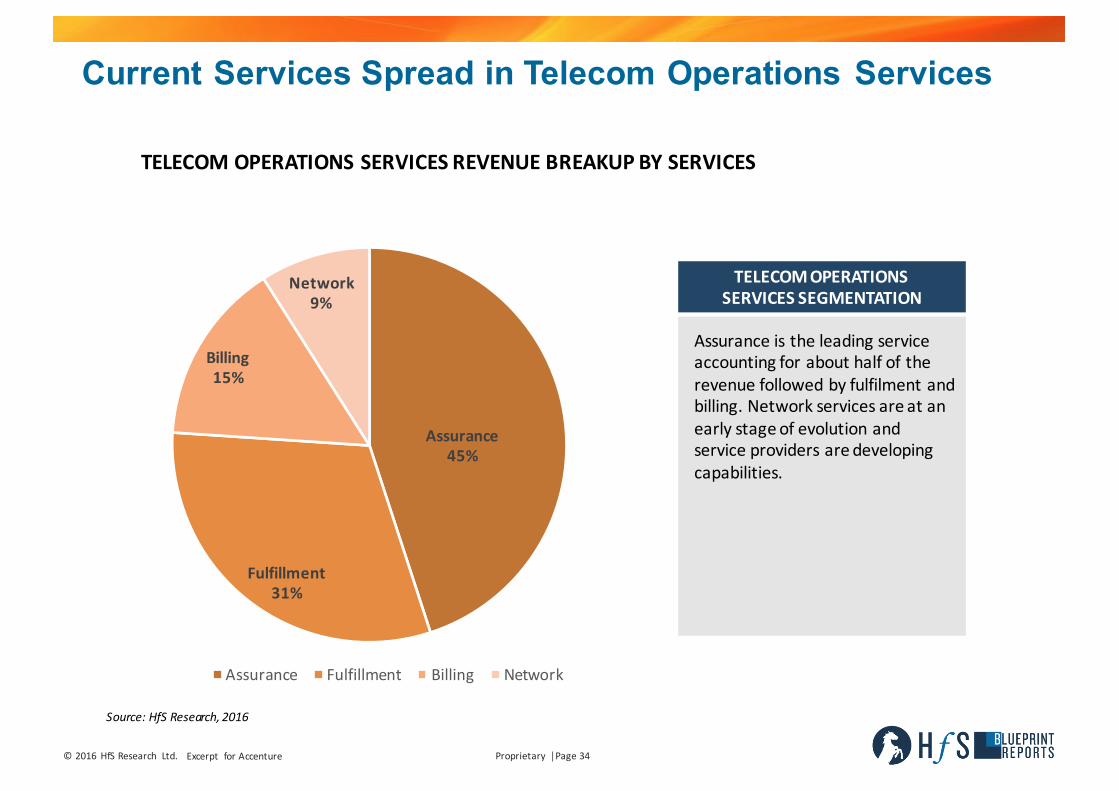

Current Services Spread in Telecom Operations Services

TELECOMOPERATIONSSERVICESSEGMENTATION

Assuranceistheleadingserviceaccountingforabouthalfoftherevenuefollowedbyfulfilmentandbilling.Networkservicesareatanearlystageofevolutionandserviceprovidersaredevelopingcapabilities.

Source:HfSResearch,2016

Assurance45%

Fulfillment31%

Billing15%

Network9%

Assurance Fulfillment Billing Network

TELECOMOPERATIONSSERVICESREVENUEBREAKUPBYSERVICES

©2016 HfSResearch Ltd. Proprietary │Page35Excerpt forAccenture

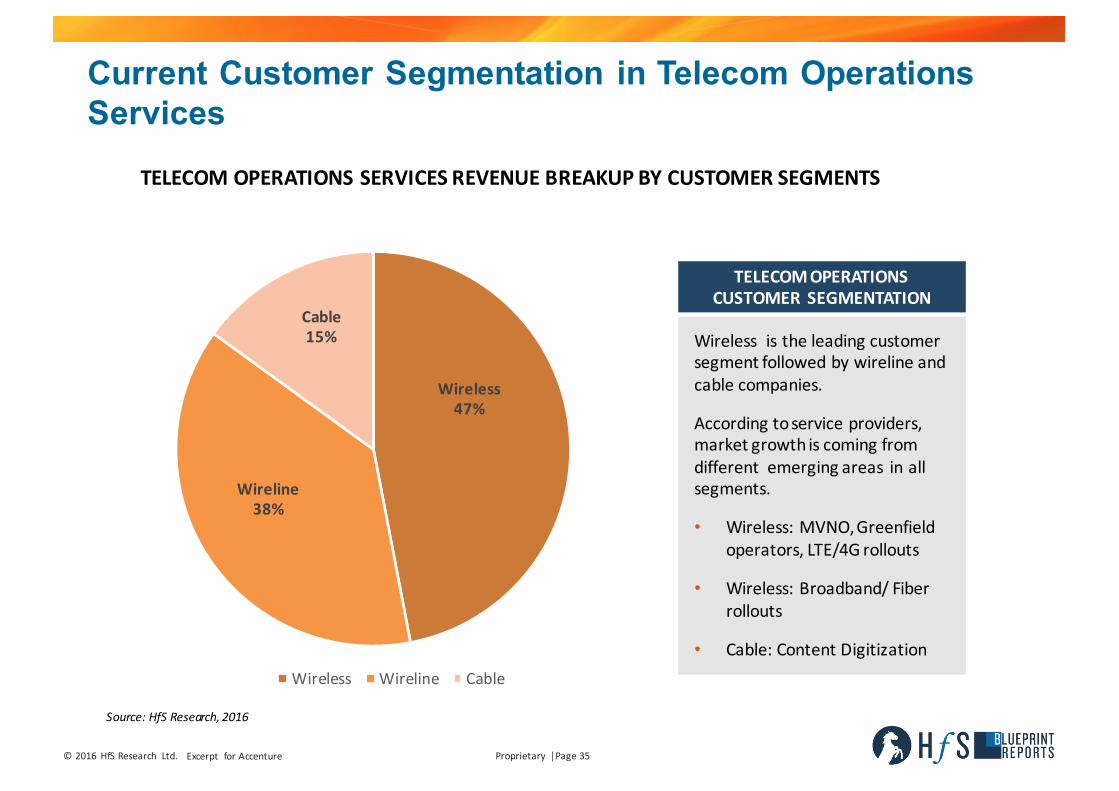

Current Customer Segmentation in Telecom Operations Services

TELECOMOPERATIONSCUSTOMERSEGMENTATION

Wirelessistheleadingcustomersegmentfollowedbywirelineandcablecompanies.

Accordingtoserviceproviders,marketgrowthiscomingfromdifferentemergingareasinallsegments.

• Wireless:MVNO,Greenfieldoperators,LTE/4Grollouts

• Wireless:Broadband/Fiberrollouts

• Cable:ContentDigitization

TELECOMOPERATIONSSERVICESREVENUEBREAKUPBYCUSTOMERSEGMENTS

Source:HfSResearch,2016

Wireless47%

Wireline38%

Cable15%

Wireless Wireline Cable

©2016 HfSResearch Ltd. Proprietary │Page36Excerpt forAccenture

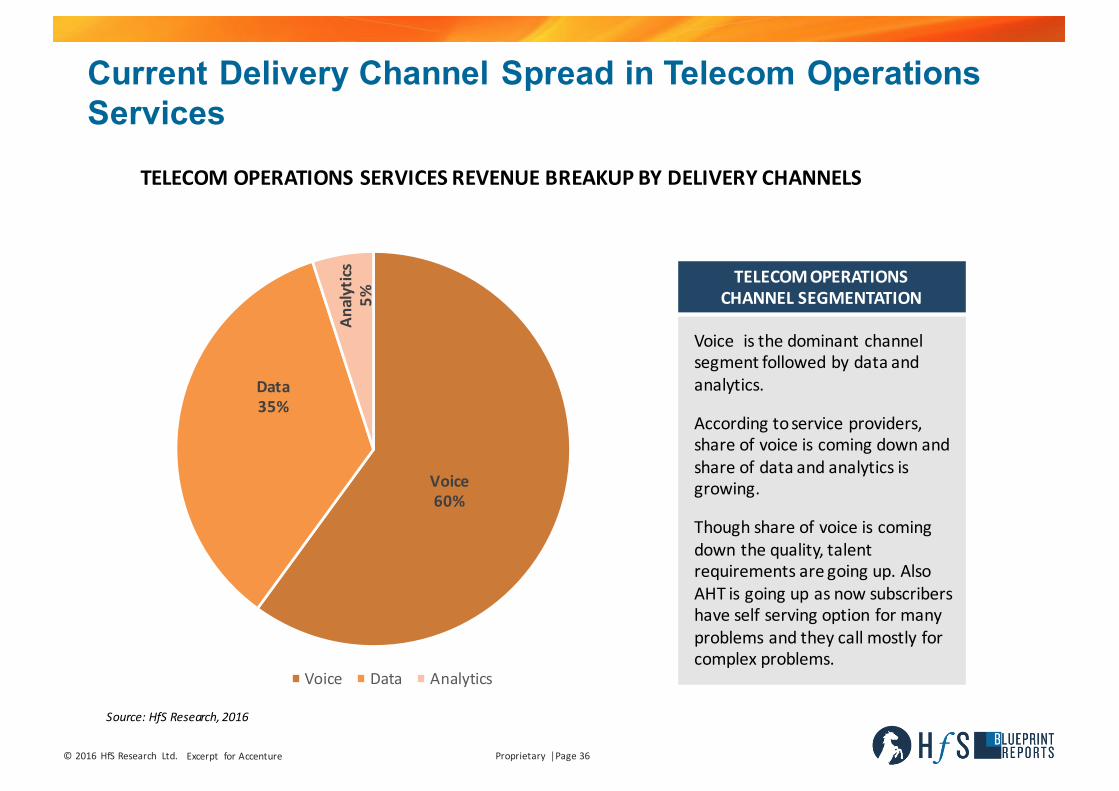

Current Delivery Channel Spread in Telecom Operations Services

TELECOMOPERATIONSCHANNEL SEGMENTATION

Voiceisthedominantchannelsegmentfollowedbydataandanalytics.

Accordingtoserviceproviders,shareofvoiceiscomingdownandshareofdataandanalyticsisgrowing.

Thoughshareofvoiceiscomingdownthequality,talentrequirementsaregoingup.AlsoAHTisgoingupasnowsubscribershaveselfservingoptionformanyproblemsandtheycallmostlyforcomplexproblems.

TELECOMOPERATIONSSERVICESREVENUEBREAKUPBYDELIVERYCHANNELS

Source:HfSResearch,2016

Voice60%

Data35%

Analytics

5%

Voice Data Analytics

©2016 HfSResearch Ltd. Proprietary │Page37Excerpt forAccenture

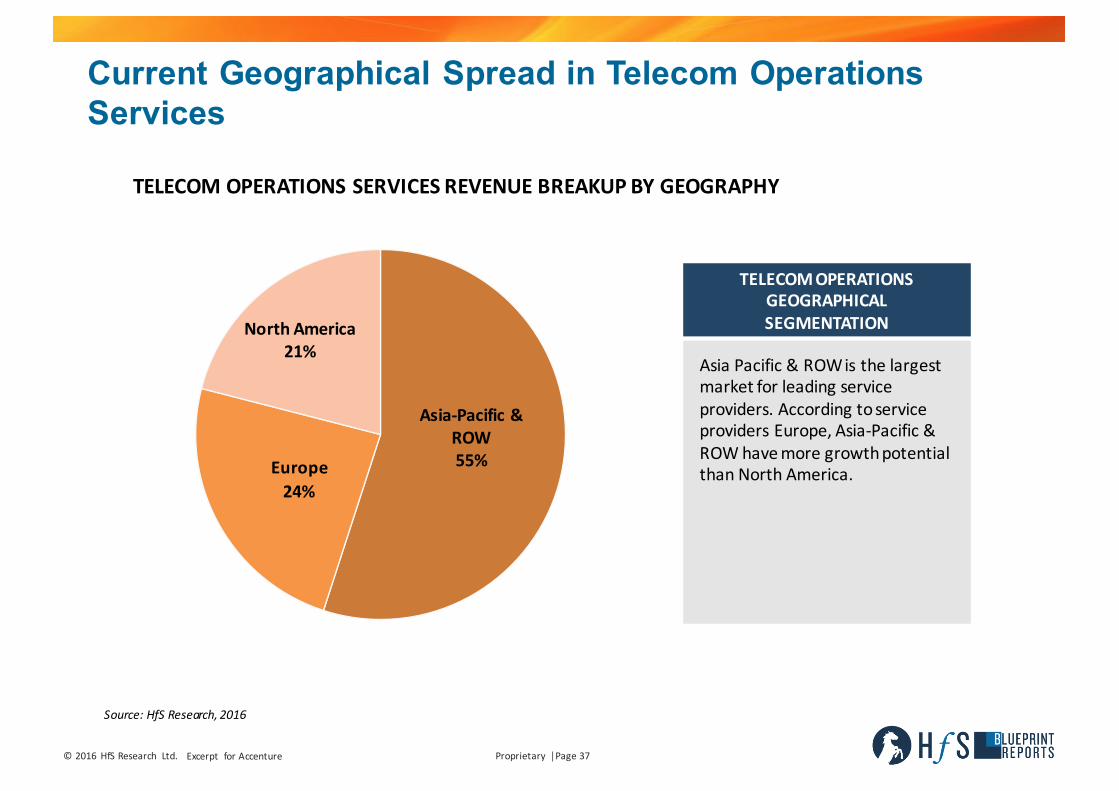

Current Geographical Spread in Telecom Operations Services

TELECOMOPERATIONSGEOGRAPHICALSEGMENTATION

AsiaPacific&ROWisthelargestmarketforleadingserviceproviders.AccordingtoserviceprovidersEurope,Asia-Pacific&ROWhavemoregrowthpotentialthanNorthAmerica.

TELECOMOPERATIONSSERVICESREVENUEBREAKUPBYGEOGRAPHY

Asia-Pacific&ROW55%Europe

24%

NorthAmerica21%

Source:HfSResearch,2016

©2016 HfSResearch Ltd. Proprietary │Page38Excerpt forAccenture

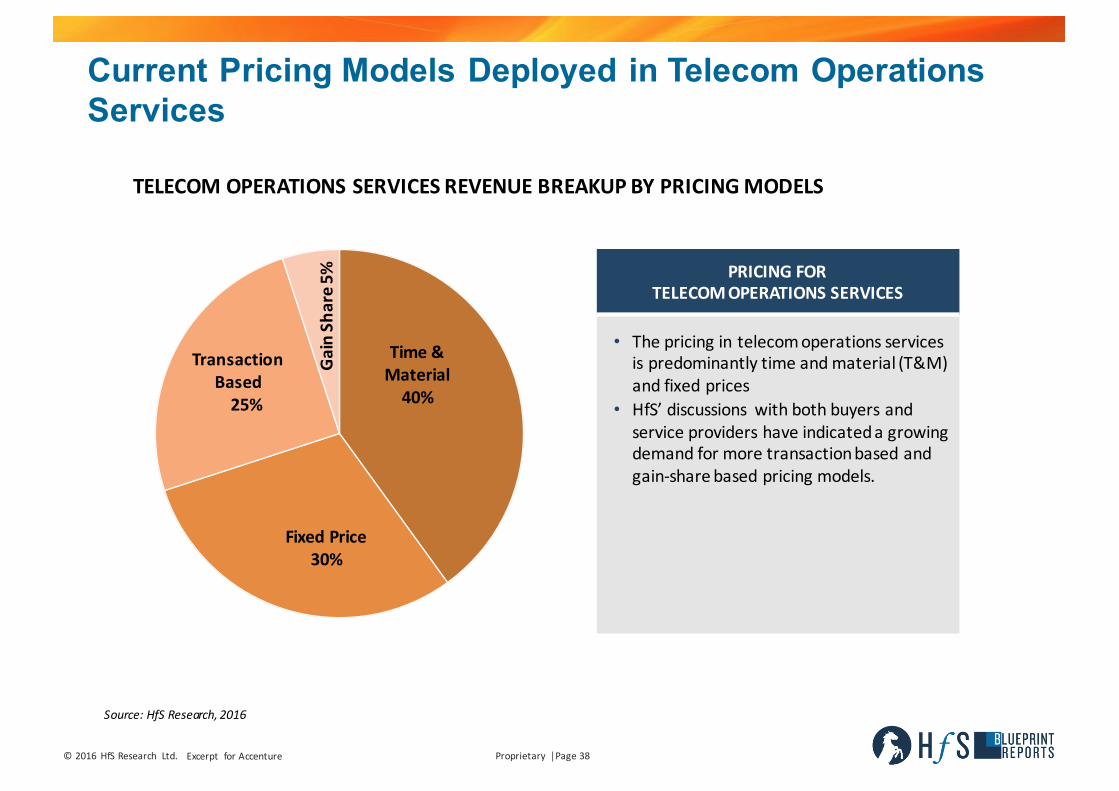

Current Pricing Models Deployed in Telecom Operations Services

TELECOMOPERATIONSSERVICESREVENUEBREAKUPBYPRICINGMODELS

Source:HfSResearch,2016

Time&Material40%

FixedPrice30%

TransactionBased25%

GainSh

are5

% PRICINGFORTELECOMOPERATIONSSERVICES

• Thepricingintelecomoperationsservicesispredominantlytimeandmaterial(T&M)andfixedprices

• HfS’discussions withbothbuyersandserviceprovidershaveindicatedagrowingdemandformoretransactionbasedandgain-sharebasedpricingmodels.

©2016 HfSResearch Ltd. Proprietary │Page39Excerpt forAccenture

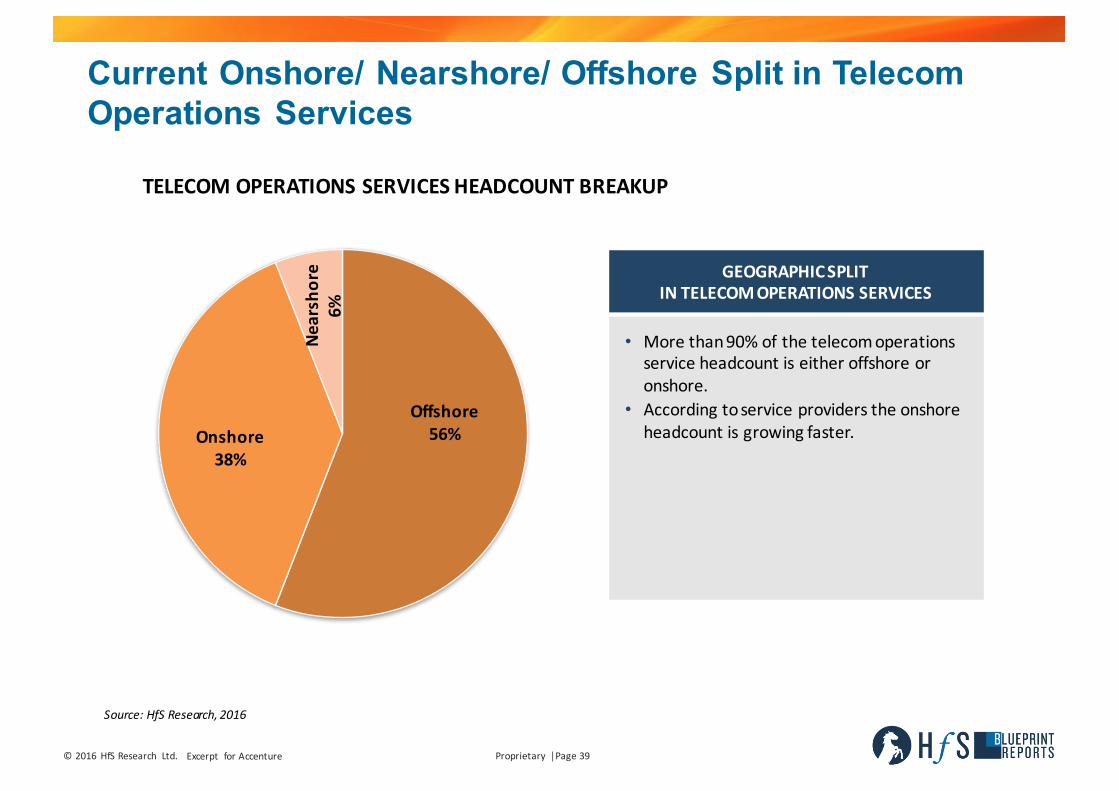

Current Onshore/ Nearshore/ Offshore Split in Telecom Operations Services

GEOGRAPHICSPLITINTELECOMOPERATIONSSERVICES

• Morethan90%ofthetelecomoperationsserviceheadcountiseitheroffshoreoronshore.

• Accordingtoserviceproviderstheonshoreheadcountisgrowingfaster.

TELECOMOPERATIONSSERVICESHEADCOUNTBREAKUP

Source:HfSResearch,2016

Offshore56%Onshore

38%

Nearshore

6%

©2016 HfSResearch Ltd. Proprietary │Page40Excerpt forAccenture

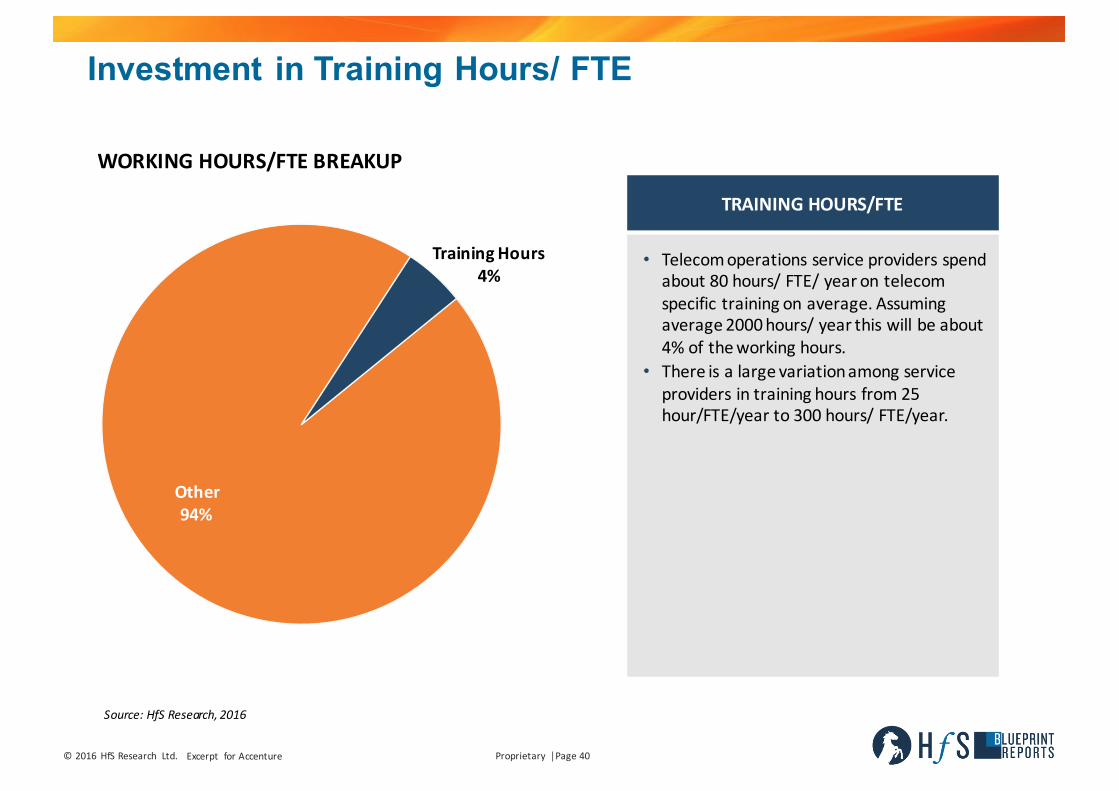

Investment in Training Hours/ FTE

TRAINING HOURS/FTE

• Telecomoperationsserviceprovidersspendabout80hours/FTE/yearontelecomspecifictrainingonaverage.Assumingaverage2000hours/yearthiswillbeabout4%oftheworkinghours.

• Thereisalargevariationamongserviceprovidersintraininghoursfrom25hour/FTE/yearto300hours/FTE/year.

WORKINGHOURS/FTEBREAKUP

Source:HfSResearch,2016

Other94%

TrainingHours4%

©2016 HfSResearch Ltd. Proprietary │Page41Excerpt forAccenture

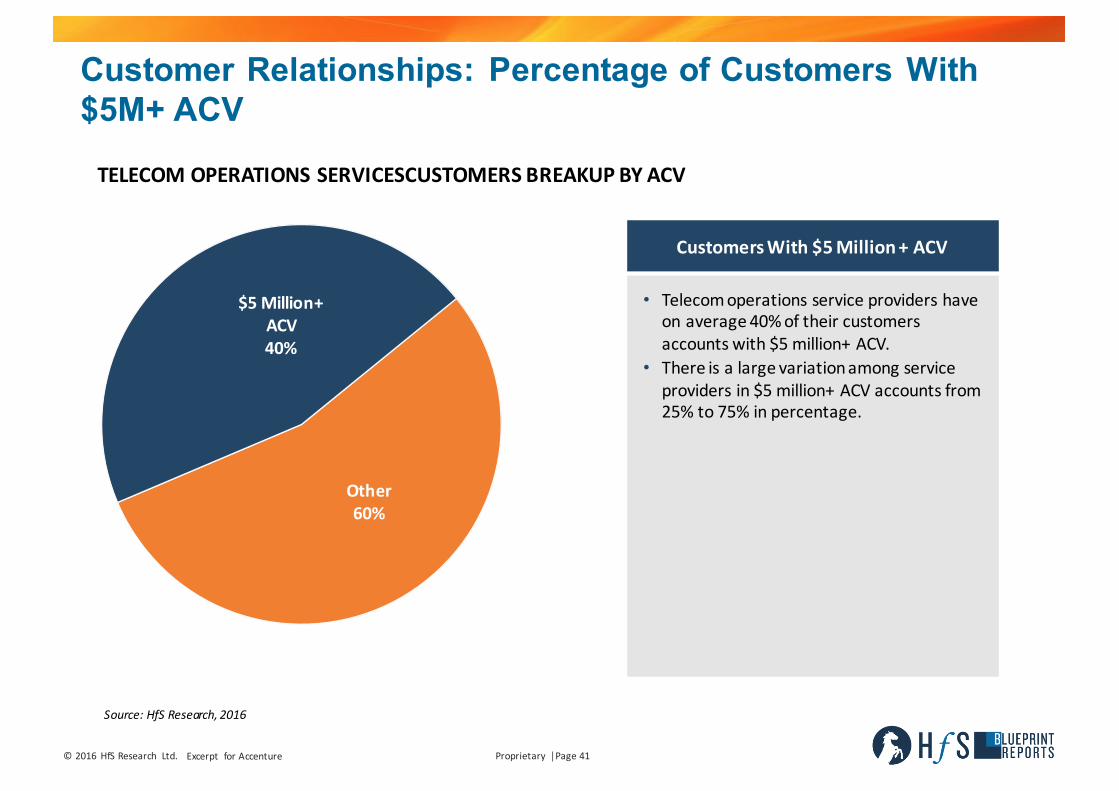

Customer Relationships: Percentage of Customers With $5M+ ACV

CustomersWith$5Million+ACV

• Telecomoperationsserviceprovidershaveonaverage40%oftheircustomersaccountswith$5million+ACV.

• Thereisalargevariationamongserviceprovidersin$5million+ACVaccountsfrom25%to75%inpercentage.

TELECOMOPERATIONSSERVICESCUSTOMERSBREAKUPBYACV

Source:HfSResearch,2016

Other60%

$5Million+ACV40%

©2016 HfSResearch Ltd. Proprietary │Page42Excerpt forAccenture

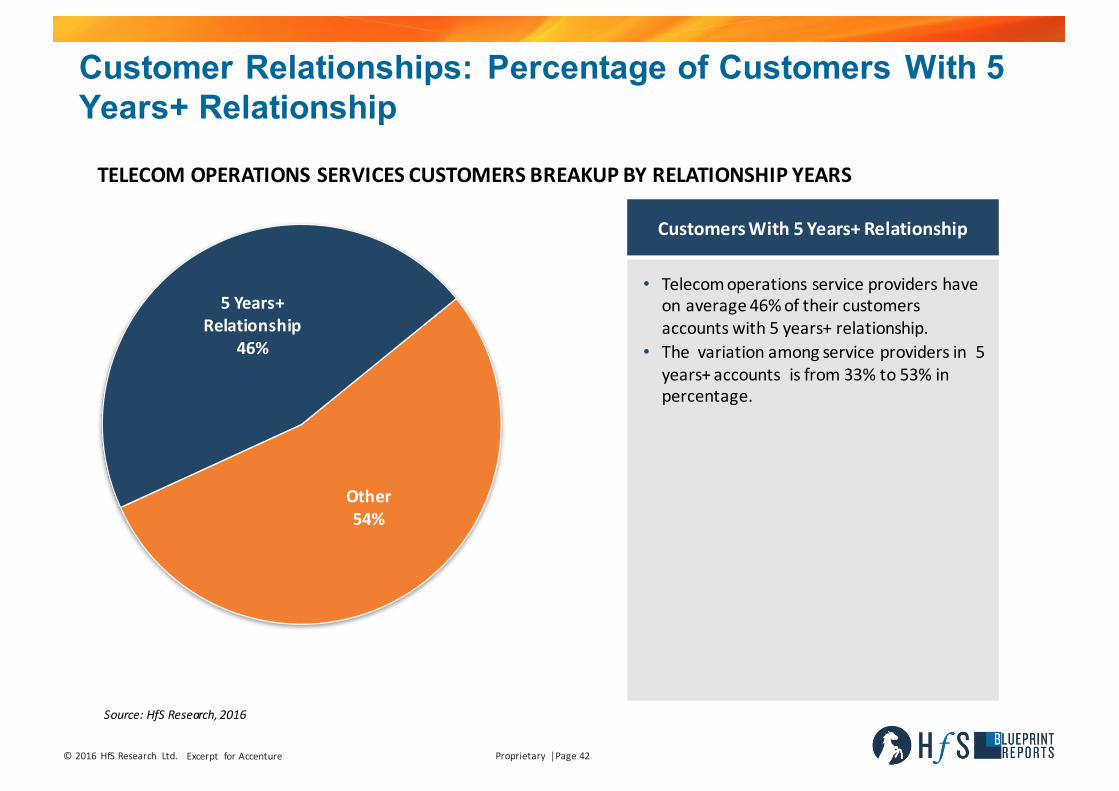

Customer Relationships: Percentage of Customers With 5 Years+ Relationship

CustomersWith5Years+Relationship

• Telecomoperationsserviceprovidershaveonaverage46%oftheircustomersaccountswith5years+relationship.

• Thevariationamongserviceprovidersin5years+accountsisfrom33%to53%inpercentage.

TELECOMOPERATIONSSERVICESCUSTOMERSBREAKUPBYRELATIONSHIPYEARS

Source:HfSResearch,2016

Other54%

5Years+Relationship

46%

©2016 HfSResearch Ltd. Proprietary │Page43Excerpt forAccenture

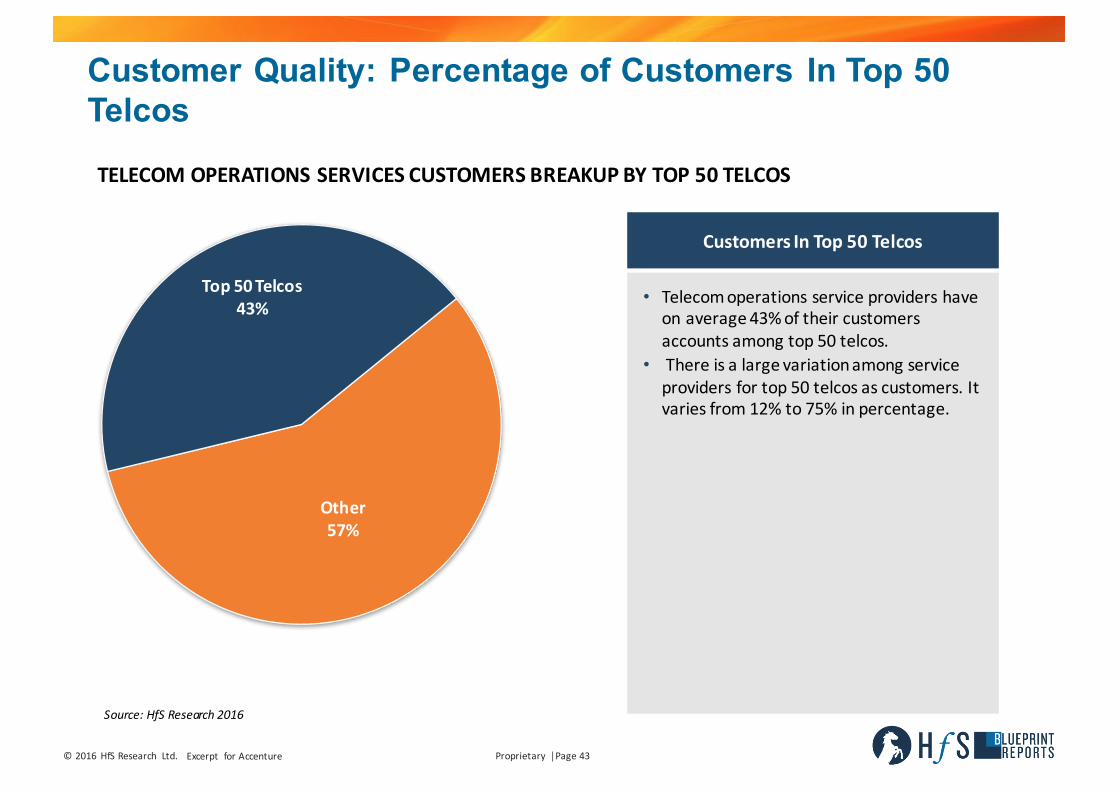

Customer Quality: Percentage of Customers In Top 50 Telcos

Customers InTop50Telcos

• Telecomoperationsserviceprovidershaveonaverage43%oftheircustomersaccountsamongtop50telcos.

• Thereisalargevariationamongserviceprovidersfortop50telcosascustomers.Itvariesfrom12%to75%inpercentage.

TELECOMOPERATIONSSERVICESCUSTOMERSBREAKUPBYTOP50TELCOS

Source:HfSResearch2016

Other57%

Top50Telcos43%

Service Provider Grid

©2016 HfSResearch Ltd. Proprietary │Page45Excerpt forAccenture

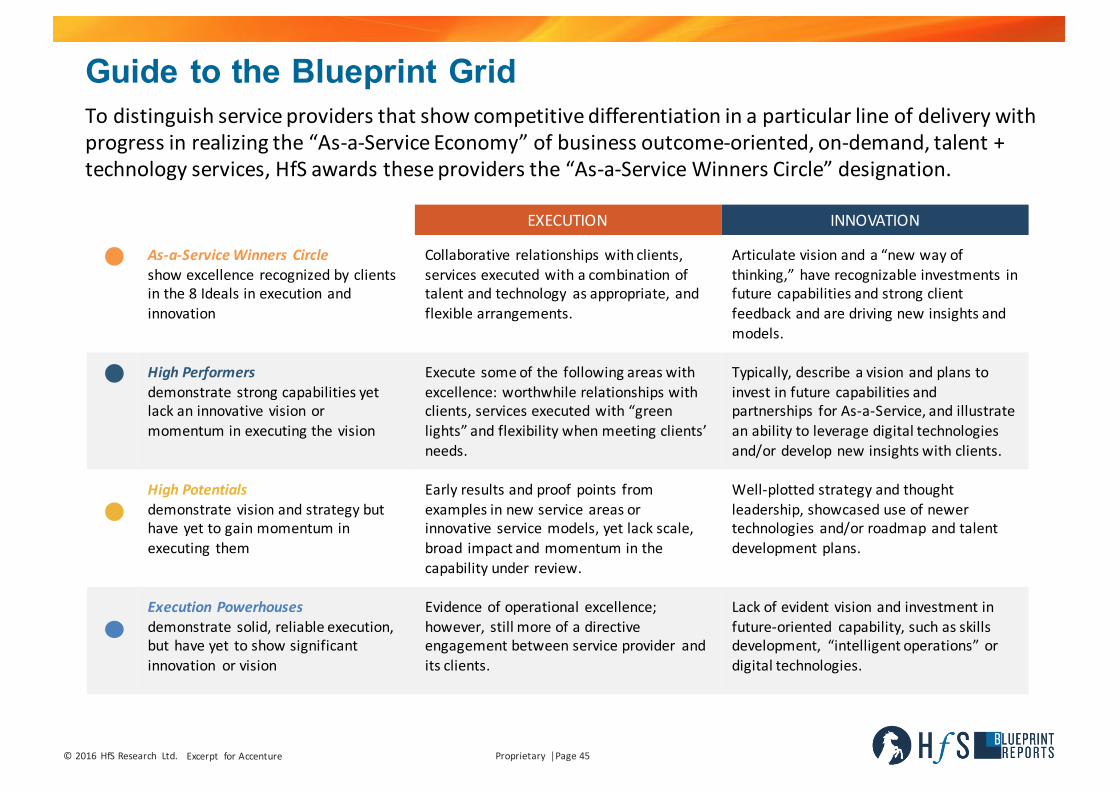

Todistinguishserviceprovidersthatshowcompetitivedifferentiationinaparticularlineofdeliverywithprogressinrealizingthe“As-a-ServiceEconomy”ofbusinessoutcome-oriented,on-demand,talent+technologyservices,HfSawardstheseprovidersthe“As-a-ServiceWinnersCircle”designation.

Guide to the Blueprint Grid

EXECUTION INNOVATION

As-a-ServiceWinners Circleshowexcellence recognizedbyclientsinthe8Idealsin executionandinnovation

Collaborative relationshipswithclients,servicesexecutedwithacombinationoftalentandtechnology asappropriate,andflexiblearrangements.

Articulatevisionanda“newwayofthinking,”haverecognizableinvestments infuturecapabilities and strongclientfeedbackand aredrivingnewinsights andmodels.

HighPerformersdemonstratestrongcapabilitiesyetlackaninnovativevisionormomentuminexecutingthevision

Executesomeofthe followingareaswithexcellence:worthwhilerelationshipswithclients,servicesexecutedwith“greenlights”andflexibilitywhenmeetingclients’needs.

Typically, describeavisionandplanstoinvestinfuturecapabilitiesandpartnerships forAs-a-Service,andillustratean abilitytoleveragedigitaltechnologiesand/ordevelop newinsightswithclients.

High Potentialsdemonstratevisionandstrategybuthaveyettogainmomentuminexecuting them

Earlyresultsandproof points fromexamplesinnewserviceareasorinnovativeservicemodels,yetlackscale,broad impactandmomentuminthecapabilityunder review.

Well-plotted strategyandthoughtleadership,showcaseduseofnewertechnologiesand/orroadmapandtalentdevelopmentplans.

ExecutionPowerhousesdemonstratesolid,reliableexecution,buthaveyet toshowsignificantinnovation orvision

Evidence ofoperationalexcellence;however, stillmoreofadirectiveengagementbetweenserviceprovider anditsclients.

Lack ofevidentvisionandinvestmentinfuture-oriented capability,suchasskillsdevelopment, “intelligentoperations”ordigitaltechnologies.

©2016 HfSResearch Ltd. Proprietary │Page46Excerpt forAccenture

INNOVA

TION

EXECUTION

ExcellentatInnovationandExecutionInvestinginInnovationtoChange

BuildingAllCapabilities ExecutionIsAheadofInnovation

AS-A-SERVICEWINNER’SCIRCLE

EXECUTIONPOWERHOUSES

HIGHPOTENTIALS

HIGHPERFORMERS

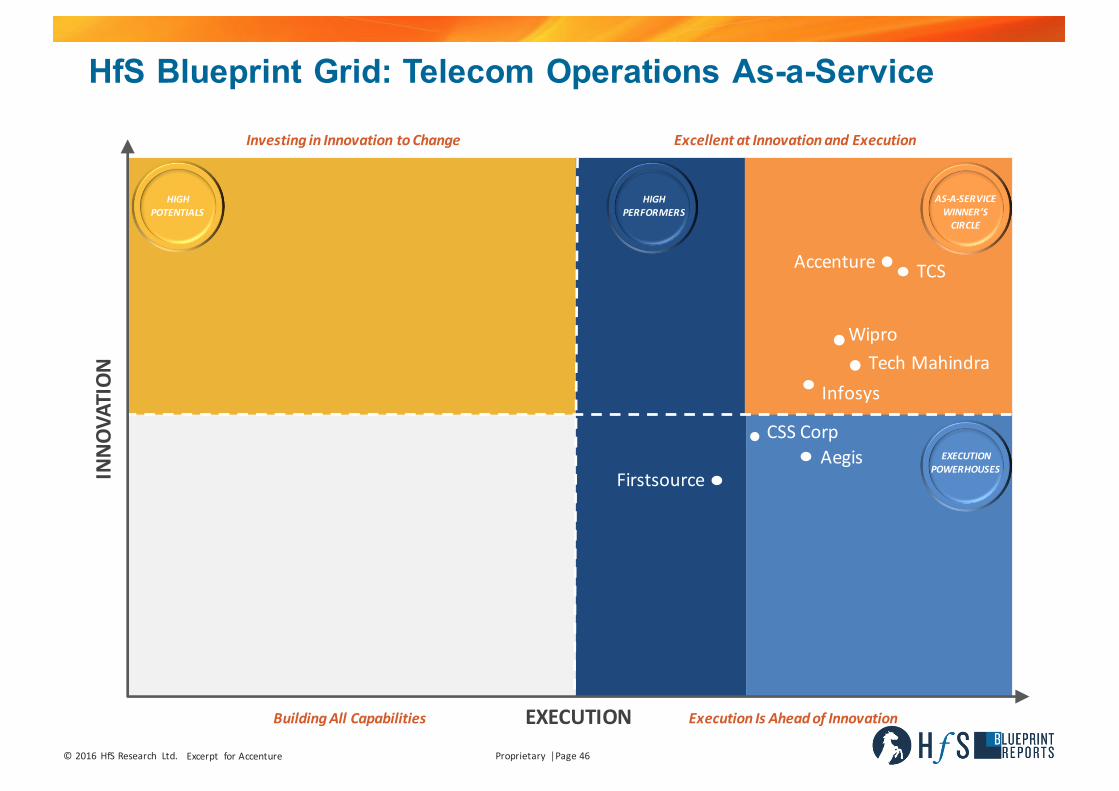

HfS Blueprint Grid: Telecom Operations As-a-Service

Accenture TCS

AegisCSSCorp

Firstsource

Infosys

WiproTechMahindra

©2016 HfSResearch Ltd. Proprietary │Page47Excerpt forAccenture

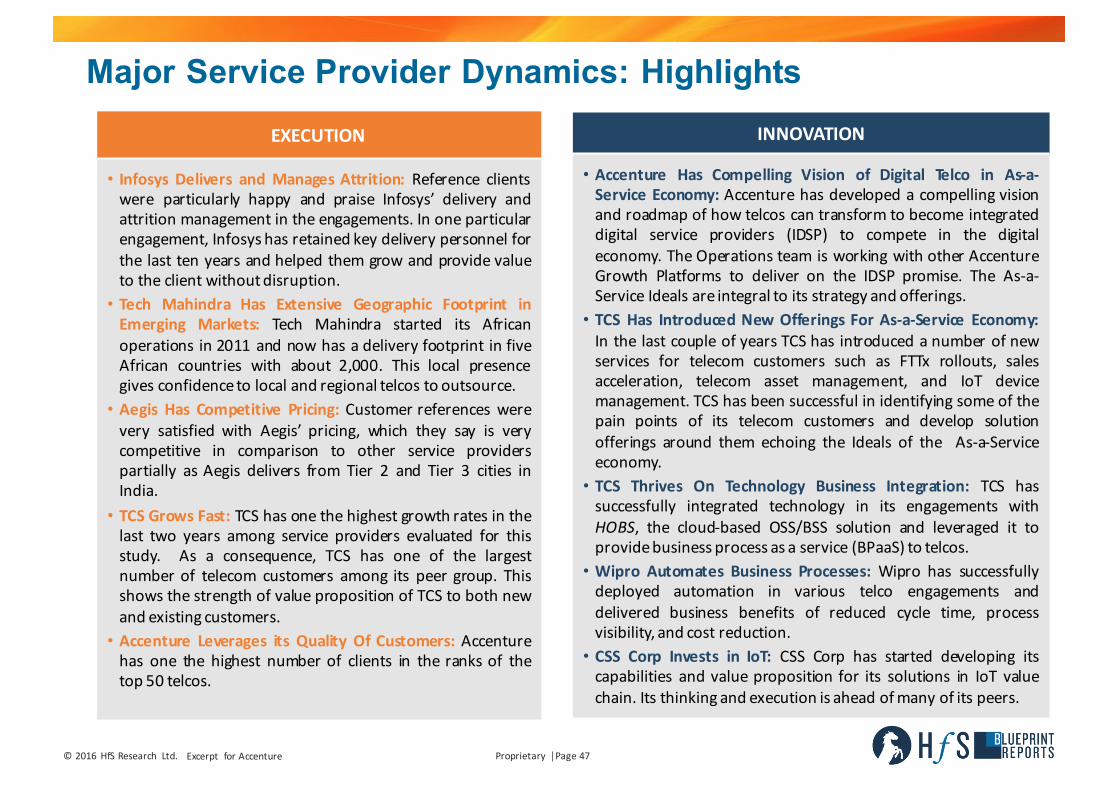

Major Service Provider Dynamics: HighlightsEXECUTION

• Infosys Delivers and Manages Attrition: Reference clientswere particularly happy and praise Infosys’ delivery andattrition management in the engagements. In one particularengagement, Infosys has retained key delivery personnel forthe last ten years and helped them grow and provide valueto the client withoutdisruption.

• Tech Mahindra Has Extensive Geographic Footprint inEmerging Markets: Tech Mahindra started its Africanoperations in 2011 and now has a delivery footprint in fiveAfrican countries with about 2,000. This local presencegives confidenceto local and regional telcos to outsource.

• Aegis Has Competitive Pricing: Customer references werevery satisfied with Aegis’ pricing, which they say is verycompetitive in comparison to other service providerspartially as Aegis delivers from Tier 2 and Tier 3 cities inIndia.

• TCS Grows Fast: TCS has one the highest growth rates in thelast two years among service providers evaluated for thisstudy. As a consequence, TCS has one of the largestnumber of telecom customers among its peer group. Thisshows the strength of value proposition of TCS to both newand existing customers.

• Accenture Leverages its Quality Of Customers: Accenturehas one the highest number of clients in the ranks of thetop 50 telcos.

INNOVATION

• Accenture Has Compelling Vision of Digital Telco in As-a-Service Economy: Accenture has developed a compelling visionand roadmap of how telcos can transform to become integrateddigital service providers (IDSP) to compete in the digitaleconomy. The Operations team is working with other AccentureGrowth Platforms to deliver on the IDSP promise. The As-a-Service Ideals are integral to its strategy and offerings.

• TCS Has Introduced New Offerings For As-a-Service Economy:In the last couple of years TCS has introduced a number of newservices for telecom customers such as FTTx rollouts, salesacceleration, telecom asset management, and IoT devicemanagement. TCS has been successful in identifying some of thepain points of its telecom customers and develop solutionofferings around them echoing the Ideals of the As-a-Serviceeconomy.

• TCS Thrives On Technology Business Integration: TCS hassuccessfully integrated technology in its engagements withHOBS, the cloud-based OSS/BSS solution and leveraged it toprovidebusiness process as a service (BPaaS) to telcos.

• Wipro Automates Business Processes: Wipro has successfullydeployed automation in various telco engagements anddelivered business benefits of reduced cycle time, processvisibility, and cost reduction.

• CSS Corp Invests in IoT: CSS Corp has started developing itscapabilities and value proposition for its solutions in IoT valuechain. Its thinking and execution is ahead ofmany of its peers.

Service Provider Profile

StrongCapabilities/ MatureOffering- PresenceofOfferingsinmajoritysubcategories,>$10million

Developing Capabilities

Yet toDeveloporMinimal<$1million

©2016 HfSResearch Ltd. Proprietary │Page49Excerpt forAccenture

Accenture

Relevant Acquisitions/Partnerships Key Clients Global Operations Centers Proprietary Technologies / Platforms

Acquisitions:• Acquity Group (2013)• Fjord (2013)• i4C (2014)• FusionX (2015)

Partnerships:• Alcatel-Lucent/ Nokia, Cisco, Huawei, Oracle,SAP,ServiceNow, Vlocity

Top 50 Telcos as Clients: 23

Clients: 30+ telecom BPO clients including:• Dutch Telco• Australian Telco• European Telco• USTelco• Brazilian Telco• Danish Telco

Telecom BPOHeadcount (In-Scope): 5,000 -6,000 estimated byHfS

Locations: 15+ telecom BPO deliverycenter locations including:

• North America: US• Europe: Czech Republic, Poland, Slovakia,• APAC: Australia,India, Philippines• ROW: Argentina, Brazil

• Accenture Operations Global Productivity Hub(GPH): In-house application for productivitymonitoring and control

• Accenture Operations App Exchange: In-houserepository for automation

• Accenture Operations App Explorer: In-housetools for analytics

• Accenture Liquid Workforce: Acrowdsourcing-inspired platform and initiative

• Accenture Intelligent OrderManagement(IOM): Tool for ordermanagement analytics

Strengths Challenges

• Vision of Digital Telco in As-a -Service Economy : Accenture ha s developed acompelli ng visi on and roadmap of how tel cos can tra nsform to become i ntegrateddigital service provi ders (IDSPs) t o compete i n the digital e conomy. The Operati onsteam is working with other Accenture Growt h Platforms (Strategy, Digital) indelivering on the IDSP promise . Accent ure ha s been i nvesting i n and developingtools and technology for telecom digital operations. It aims to gradually transformtelcos’ business toward digital operations, where an increasi ng proporti on of thebusi ness processes can be delivered as BPaaS. The As-a -Service ideal s are integralto its strategy and offerings.

• Delivery of Services f or All Pr ocesses: Accent ure has a depth of client experiencesand capabilities across all telecom operati ons sub-processes of network,ful fillment, a ssura nce, and billing. Clients poi nted to example s of transformativesolutions in all areas and to a deep bench of skilled delivery resour ces. Customerreferences have confirmed that they also bene fited fr om automation and analyticscapabilities of Accenture in the last couple of years.

• Analytics and Experi ence of Deliver ing Business Outcomes: Accent ure hasdemonstrated its strong analytics credentials with a large number of case studies.Clients pointed to Accenture’s focus on tangible business outcomes such as capexeffi ciency, pr ocess e ffi ciency, cost reducti on, customer satis fa ction, andcompliance in the engagements.

• Quality Of Cust omers: Accenture ha s one the hig hest number of clients in theranks of the top 50 telcos.

• Moving Beyond Tier 1 Te lcos: Accent ure’s strategy is to work wit hthe G2000. Out of its 30+ telco customers, 23 are among top 50telcos. While the quality of clients is A ccenture’ s strengt h, ther e is a nopportunity for Accenture to engage with Tier 2 and Tier 3 tel cos wit hthe right value proposition.

• Getting Best Out of Accenture : Refer ence cli ents have pointed outthat Accent ure’s BPO delivery is sometimes constrained due to ITissues. I f IT i s not managed by Accent ure, the BPO team may have t odo temporary work ar ounds whi ch can impact t he delivery ofbusi ness out comes. In the opini on of several clients, it will bebene fi cial for both clients a nd Accenture i f both IT and BPO ar emanag ed by Accenture. The Accenture team can be more proa ctivein conveying the value pr oposition of si ngle sour ce IT and BPO t ostakehol ders. This will also hel p Accent ure to a ccelerate thedepl oyment of i ntelligent a utomation int o customer engagements a swell as accelerate their As-a-Service strategy.

Businessoutcomes–focusedglobalserviceproviderwithcompellingAs-a-Servicevisionandafullsetofofferingsintelecom

Winner’s CircleBlueprintLeadingHighlights

• Customer Quality – Number of Top50Telcos asCustomer

• Delivery– AllProcesses AcrossValueChain

• Plans for As-a-Service• Innovation - Examples• Business Outcomes Measurement

Network

Fulfillment

Assurance

Billing

Wireless

Wireline/ Broadband

Cable

Market Wrap-Up and Recommendations

©2016 HfSResearch Ltd. Proprietary │Page51Excerpt forAccenture

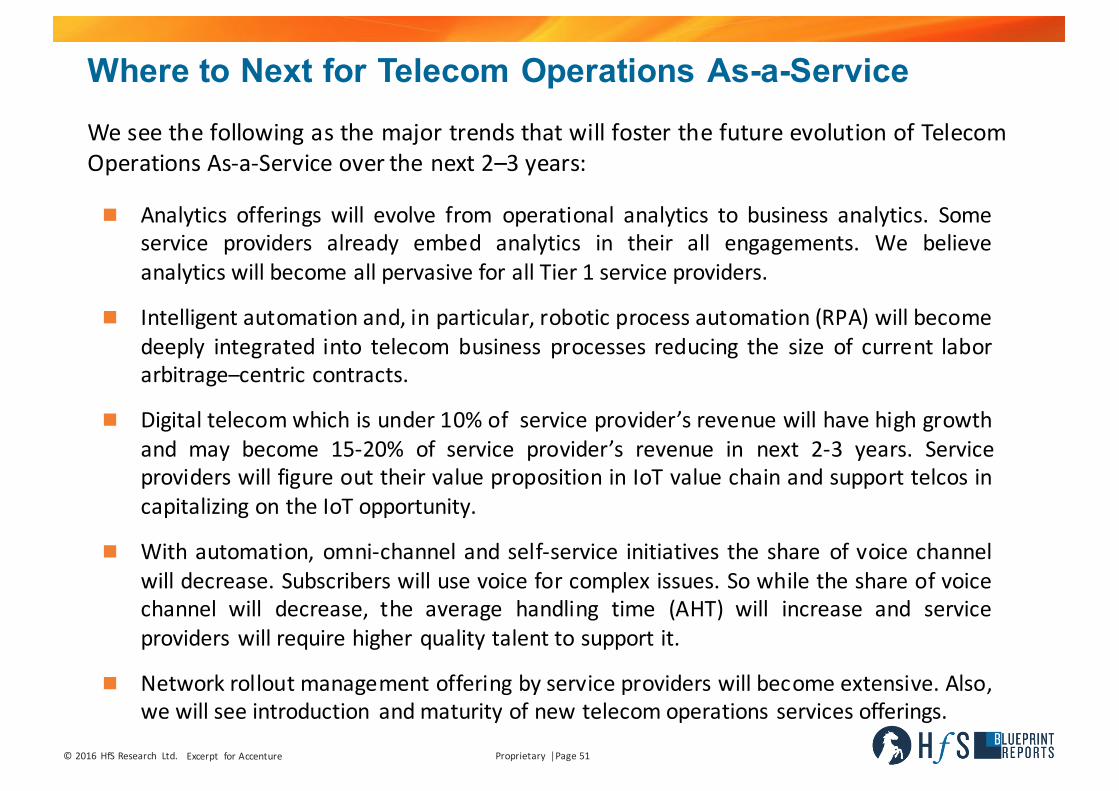

Where to Next for Telecom Operations As-a-Service

n Analytics offerings will evolve from operational analytics to business analytics. Someservice providers already embed analytics in their all engagements. We believeanalytics will become all pervasive for all Tier 1 service providers.

n Intelligent automation and, in particular, robotic process automation (RPA) will becomedeeply integrated into telecom business processes reducing the size of current laborarbitrage–centric contracts.

n Digital telecomwhich is under 10% of service provider’s revenue will have high growthand may become 15-20% of service provider’s revenue in next 2-3 years. Serviceproviders will figure out their value proposition in IoT value chain and support telcos incapitalizing on the IoT opportunity.

n With automation, omni-channel and self-service initiatives the share of voice channelwill decrease. Subscribers will use voice for complex issues. So while the share of voicechannel will decrease, the average handling time (AHT) will increase and serviceproviders will require higher quality talent to support it.

n Network rollout management offering by service providers will become extensive. Also,we will see introduction and maturity of new telecom operations services offerings.

We see the following as the major trends that will foster the future evolution of TelecomOperations As-a-Service over the next 2–3 years:

©2016 HfSResearch Ltd. Proprietary │Page52Excerpt forAccenture

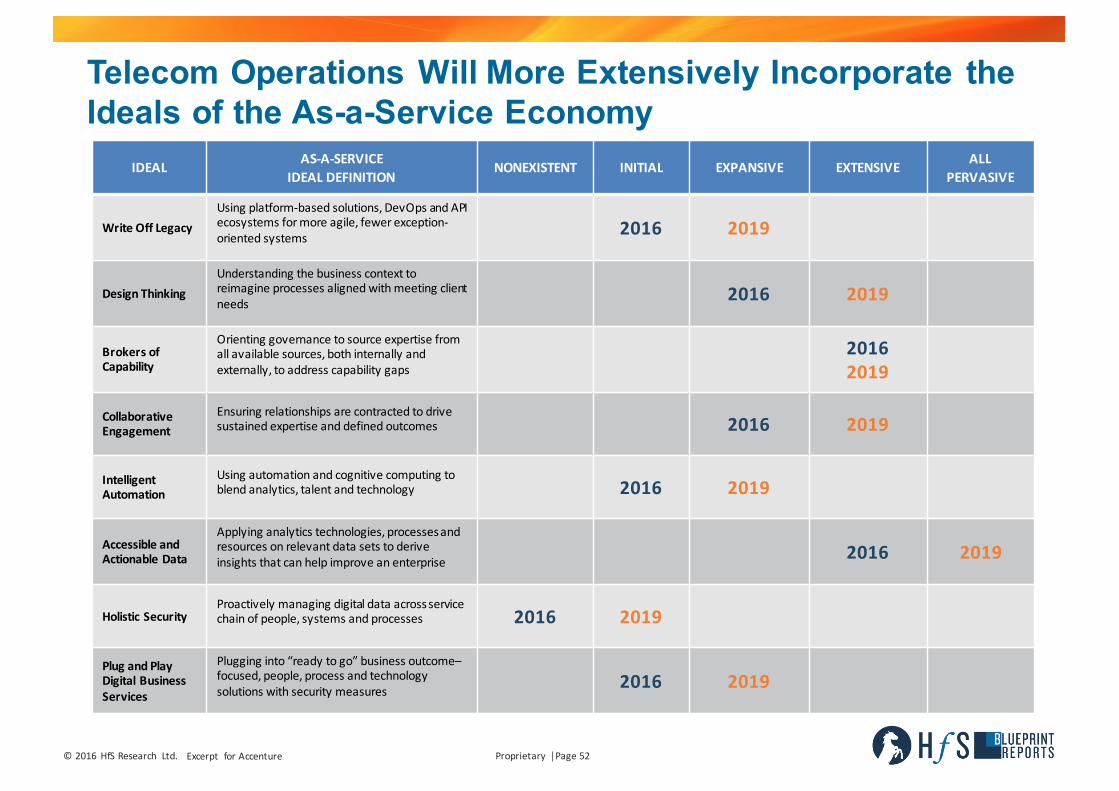

Telecom Operations Will More Extensively Incorporate the Ideals of the As-a-Service Economy

IDEAL AS-A-SERVICEIDEALDEFINITION

NONEXISTENT INITIAL EXPANSIVE EXTENSIVE ALLPERVASIVE

WriteOffLegacyUsingplatform-basedsolutions,DevOpsandAPIecosystemsformoreagile,fewerexception-orientedsystems 2016 2019

DesignThinkingUnderstandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds 2016 2019

Brokers ofCapability

Orientinggovernance tosourceexpertisefromallavailablesources,bothinternallyandexternally,toaddresscapabilitygaps

20162019

CollaborativeEngagement

Ensuring relationshipsarecontractedtodrivesustainedexpertiseanddefinedoutcomes 2016 2019

IntelligentAutomation

Using automationandcognitivecomputingtoblendanalytics,talentandtechnology 2016 2019

AccessibleandActionableData

Applyinganalyticstechnologies,processesandresourcesonrelevantdatasetstoderiveinsightsthatcanhelpimproveanenterprise 2016 2019

HolisticSecurityProactivelymanagingdigitaldataacrossservicechainofpeople,systemsandprocesses 2016 2019

Plug andPlayDigitalBusinessServices

Plugginginto“readytogo”business outcome–focused, people,processandtechnologysolutionswithsecuritymeasures 2016 2019

©2016 HfSResearch Ltd. Proprietary │Page53Excerpt forAccenture

2016-17 Recommendations: Buyers

n Increase the Trust Collaboration: Push your service provider(s) to be more collaborative, more visionary, moreinclusive and share with you. In turn, provide that same approach to the service provider(s). Realizing thebusiness outcomes is easier in a close partnership than in a closed-off zero-sum mindset relationship. So, workwith your service provider(s) in a manner that facilitates long-term success as well and ask for it in return.

n Rethink Your Legacy Stack: OTT players are already eating your lunch. Don’t let legacy technology hold you backin your transformation for the digital era. Service providers are capable of delivering on new technology stack,but it is the perception of buyers about the robustness of new technologies and about the capability of serviceproviders which is holding them back. Ask service providers about case studies of early adopters, develop thebusiness case and get service providers skin in the gamewhile leveraging new technologies to remain relevant inthe digital era.

n Test Digital and IoT Implications: Building further on the above recommendation, ask your service provider(s)for insight into how Digital, the IoT and other innovations are likely to impact the telecom business processesyou have in place today whether the service provider delivers them or not. Use quarterly business reviews(QBRs) and other interactions with your service provider(s) to review their vision for the evolution of telecomoperations.

n Rethink About Captive and Local Outsourcing: Our research shows that only about one-third of potentialtelecom operations market is outsourced to large and mid-size service providers. The rest of the potentialmarket is served by in-house operations, captives or small local service providers. In-house centers and smalllocal service providers might not have scale and expertise to invest in analytics, automation and other As-a-Service initiatives. While, most large and mid-size service providers are either investing or have plans to invest inthese initiatives. By leveraging large and mid-size service providers, buyers can get best out of their operations.

©2016 HfSResearch Ltd. Proprietary │Page54Excerpt forAccenture

2016-17 Recommendations: Buyers (continued)

n Move Faster and Deeper to As-a-Service Offerings from Service Providers: Keep pushing your serviceprovider(s) to move to an As-a-Service model that goes beyond labor arbitrage to include and offer you abroader set of choices for what solutions you adopt and how they interact with your own retained organization.Don’t settle for a long-term fixed model of solution delivery for telecom operations services, but push yourservice provider(s) to be flexible and agile so that future services offerings better align to your own potentialfuture needs.

n Adopt Design Thinking: Don’t dismiss design thinking as something that is a fad with little benefit for your ownoperations. The opportunities to sit down with your service provider(s) to better understand the businesscontext in which your current processes operate and what can be done to realign or reimagine these processesto achieve different and/orbetter results is always an exercise worthundertaking.

n Greenfield Service Providers and MVNOs can Leapfrog into As-a-Service: Greenfield service providers andMVNOs which doesn’t have any legacy constraint and get best out of telecom service providers and use them toreimagine process, reduce time to market, and make themselves foolproof in As-a-Service Economy.

©2016 HfSResearch Ltd. Proprietary │Page55Excerpt forAccenture

2016-17 Recommendations: Service Providers

n Scale-up Innovation: Overall, buyers ratings of service providers were lowest on getting value from serviceprovider led innovation initiatives. Most buyers feel that service providers can do better at innovation. Fewbuyers complain that service providers are becoming complacent and either not reimagining the supportprocesses with design thinking, technology, analytics, automation or not doing fast enough.

n Move Further to As-a-Service Offering Design and Execution: At HfS, we are strong believers in the rapidmove of BPO away from legacy “lift and shift” models toward an As-a-Service solution design and deliveryworld. This is especially true for telecom operations, which has always had some embodiment of the 8 Idealsof As-a-Service in how service providers have sold and delivered the offering. That said, there is stillsignificant opportunity to move this further forward and bring a more modular yet end-to-end solution stack

n Prepare for the Rise of the IoT and Digital: They might not be mainstream technologies, but Digital and theIoT are becoming that way. Research labs, consulting teams and SI units inside each major service providerare working with clients around these technologies today. However, the lessons learned may not yet havemade their way over to the telecom operations group running day-to-day operations. Put aside investmentfunds this year to encourage that collaboration so that as a service provider you can share these sameinsights with clients.

n Develop New Service Offerings: Telcos are facing serious threat from OTTs and need all the help they can getin making themselves relevant in the digital era. Service providers can understand their pain-points and usedesign thinking to develop new service offerings which will make telcos competitive and relevant to theirsubscribers.

n Move Beyond Tier 1 and English-Speaking Telcos: Most of the telco customers are either tier-one (top 50telcos) or are from English speaking countries. There are good opportunities with Tier 2 and Tier 3 telcos andbeyond English speaking countries which service providers should also target.

About the Author

©2016 HfSResearch Ltd. Proprietary │Page57Excerpt forAccenture

Pareekh JainResearchDirector,Bangalore,India

Overview• Morethan10years’businessexperienceinbuyside,advisory,anddeliveryintheglobaloutsourcingindustryacrosstheUS,Europe,andAsia.

• CoverageareasinHfSaretelecombusinessoperations,engineeringservices,andoutsourcingdeals.

• AuthorofthebookWhoIsThatLady?• Astrategist,researcher,andwriter.

PreviousExperience• BusinessPlanningManager(AsiaPacific),EmersonNetworkPower• Manager,OutsourcingAdvisory,NeoGroup• SoftwareEngineer,GeometricGlobal

Education• MBA,IndianInstituteOfManagement(IIM),Bangalore,India• B.Tech,IndianInstituteOfTechnology(IIT),Delhi,India

[email protected]@pareekhjain

©2016 HfSResearch Ltd. Proprietary │Page58Excerpt forAccenture

About HfS ResearchHfSResearch isTheServicesResearchCompany™—theleadinganalystauthorityandglobalcommunityforbusinessoperationsandITservices.Thefirmhelpsenterprisesvalidatetheirglobaloperatingmodelswithworld-classresearchandpeernetworking.

HfSResearchcoinedthetermTheAs-a-ServiceEconomy toillustratethechallengesandopportunitiesfacingenterprisesneedingtore-architecttheiroperationstothriveinanageofdigitaldisruption,whilegrapplingwithanincreasinglycomplexglobalbusinessenvironment.HfScreatedtheEightIdealsofBeingAs-a-Service asaguidingframeworktohelpservicebuyersandprovidersaddressthesechallengesandseizetheinitiative.

Withspecificfocusonthedigitizationofbusinessprocesses,intelligentautomationandoutsourcing,HfShasdeepindustryexpertise inhealthcare,lifesciences,retail,manufacturing,energy, utilities, telecommunications andfinancialservices. HfSusesitsgroundbreakingBlueprintMethodology™toevaluatetheabilityofserviceandtechnologyproviderstoinnovateandexecutetheEightIdeals.

HfSfacilitatesathrivinganddynamicglobalcommunityofmorethan100,000activesubscribers,whichaddsrichnesstoitsresearch.Inaddition,HfSholdsseveralServiceLeadersSummits everyyear,bringingtogetherseniorservicebuyers,providersandtechnologysuppliersinanintimateforumtodevelopcollective recommendationsfortheindustryandadddepthtothefirm’sresearchpublicationsandanalystofferings.

Nowinits tenthyearofpublication,HfSResearch’sacclaimedblogHorsesforSources isthemostwidelyreadandtrusteddestinationforunfetteredcollective insight,researchandopendebateaboutsourcingindustryissuesanddevelopments.HorsesforSourcesandtheHfSnetworkofsitesreceivemorethanamillionwebvisitsayear.

HfSwasnamedAnalystFirmoftheYearfor2016,alongsideGartnerandForrester,byleadinganalystobserverInfluencerRelations.