ACC 4 Assets Part II

18

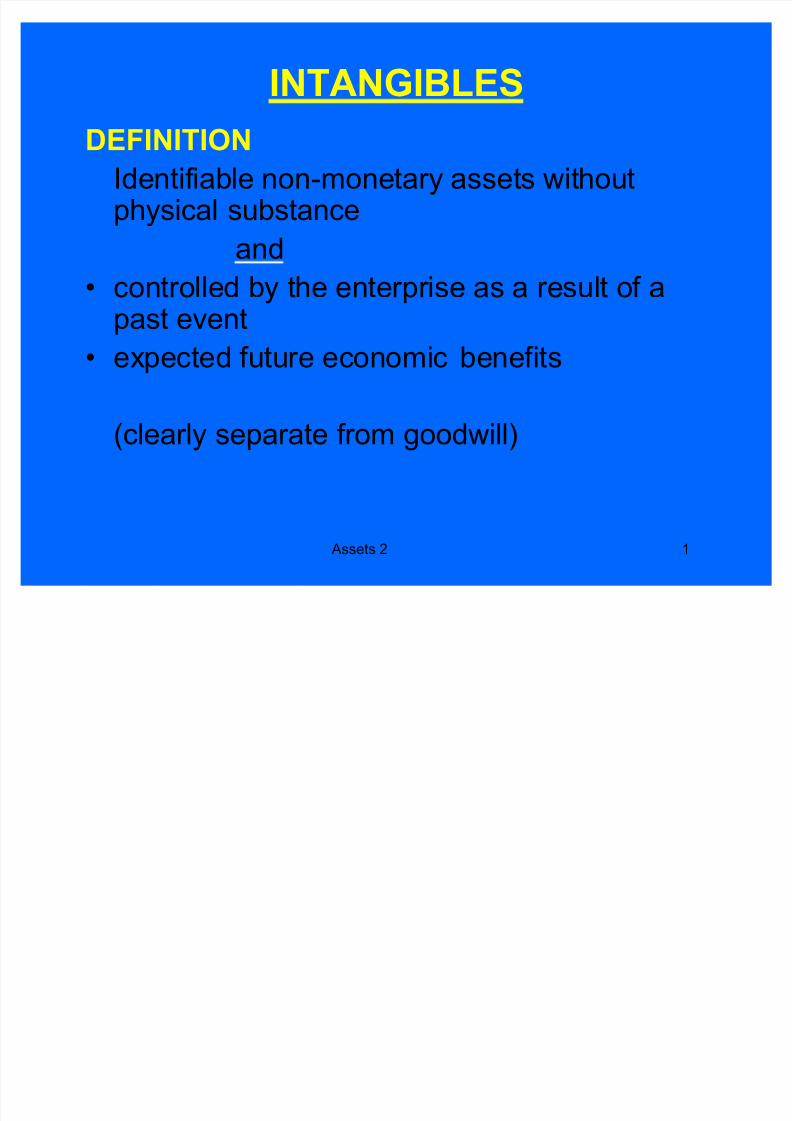

Assets 2 1 INTANGIBLES DEFINITION Ide ntif iable non-mone tary asset s withou t physical substance and contro lle d by t he enterpr ise as a re sul t o f a past event expected future economic benefits (clearly separate from goodwill)

Transcript of ACC 4 Assets Part II

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 1/18

Assets 2 1

INTANGIBLES

DEFINITION

Identifiable non-monetary assets withoutphysical substance

and

controlled by the enterprise as a result of apast event

expected future economic benefits

(clearly separate from goodwill)

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 2/18

Assets 2 2

INTANGIBLES

RECOGNITION probable that economic benefits will flow

cost can be reliably measured

MEASUREMENT

Initially at cost

± Separate acquisition

± Business combination

± Internally generated

Research is expensed

Development costs are capitalised if six conditions met

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 3/18

Assets 2 3

INTANGIBLES

ALWAYS EXPENSE:

- Research costs

- Pre-opening costs (unless PPE)

- Establishment costs

- Training costs- Advertising

- Relocation/restructuring

- Internally generated:

- Customer lists- Brands,

- Mastheads, Publishing titles

- Goodwill

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 4/18

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 5/18

Assets 2 5

INTANGIBLES

IMPAIRMENT

Apply principles on impairment

Recoverable amount estimated at each balance

date for intangibles:

± not yet in use

± Indefinite life intangibles

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 6/18

Assets 2 6

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 7/18

Assets 2 7

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 8/18

Assets 2 8

NON-CURRENT ASSETS HELD

FOR SALE

Non-current asset (or disposal group) wherecarrying amount will be recovered through sale.

MEASUREMENT

at the lower of: fair value less costs to sell, and

carrying amount.

TREATMENT

Held for sale¶s not depreciated

Separate presentation on balance sheet of

assets & liabilities

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 9/18

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 10/18

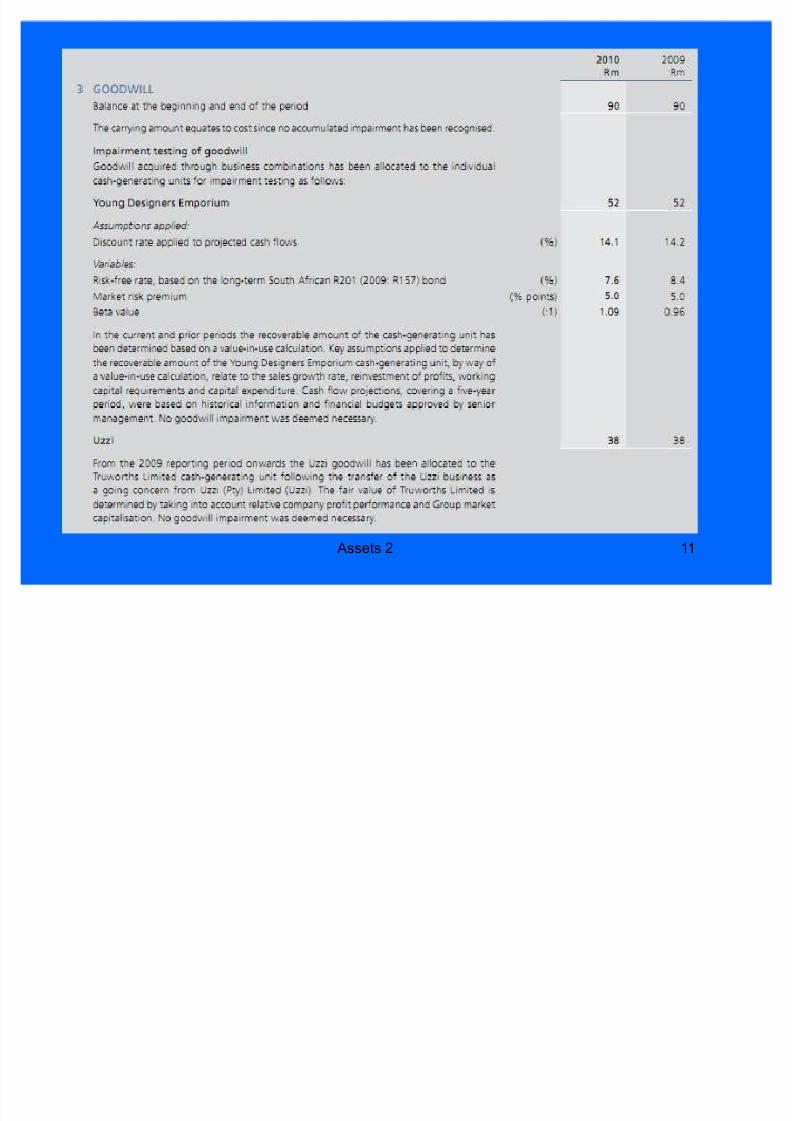

Assets 2 10

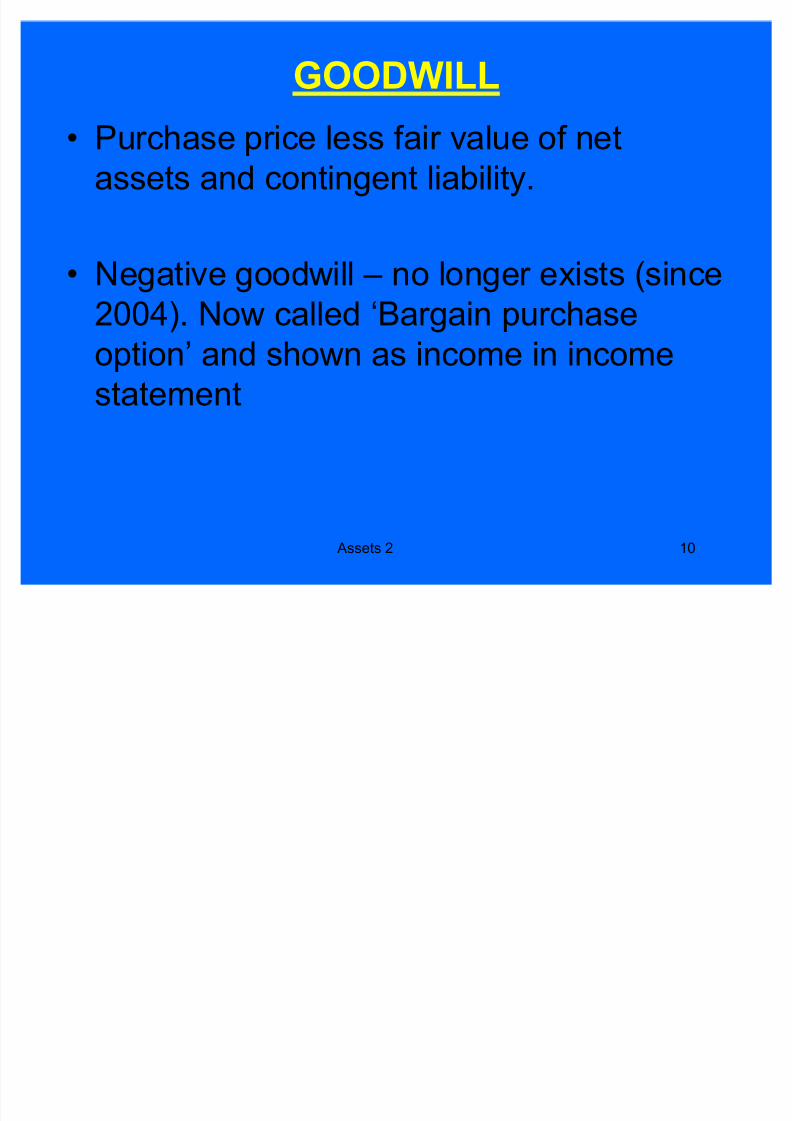

GOODWILL

Purchase price less fair value of netassets and contingent liability.

Negative goodwill ± no longer exists (since2004). Now called µBargain purchase

option¶ and shown as income in income

statement

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 11/18

Assets 2 11

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 12/18

Assets 2 12

SPUR 2006

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 13/18

Assets 2 13

SPUR 2006

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 14/18

14

FULL GOODWILL METHOD

Not a policy choice !!!

Sub has net assets of R4m

Parent pays R3m for 60% of business

Fair value of 40% is R1.8m

100% 60% 40%

NAV 4 000 2 400 1 600

Cost 3 000 1 800

Goodwill 600 200

Current status 2009

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 15/18

Assets 2 15

INVENTORIES

DEFINITION

Assets held for sale in the ordinary course of

business, in the process of production for such

sale, or in the form of materials or supplies to be

consumed in the production process or inrendering of services.

COST

= purchase price + costs incurred in bringing the

inventories to their present location and condition.

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 16/18

Assets 2 16

INVENTORIES

Lower of Cost or Net realisable value

FIFO, Weighted average, LIFO, Standard cost and Retailmethod

Cost of inventory expense incl:

± cost of units sold

± unallocated overheads ± abnormal wastage costs

± write down to NRV

± reversal of write down

Disclose: ± cost of sales

± write-downs & reversals of write downs

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 17/18

Assets 2 17

8/3/2019 ACC 4 Assets Part II

http://slidepdf.com/reader/full/acc-4-assets-part-ii 18/18

DISTELL 2010

Assets 2 18