Acc 290 acc290

46

ACC 290 The Latest Version A+ Study Guide Entire Course https://uopcourses.com/category/acc-290/ ACC 290 Week 1 Assignment WileyPLUS Assignment Click Assignment: Week 1 Assignment within WileyPLUS to complete the following exercises: DO IT! 1-3 Exercise 1-3 Exercise 1-4 Exercise Excel E 2-4 IFRS 2-4 Resource: WileyPLUS Click Assignment: Week 1 Assignment within WileyPLUS to complete the following exercises: DO IT! Review 1-3 Exercise 1-3 Exercise 1-4 Exercise 2-4 IFRS 2-4

-

Upload

goodcoursehelp -

Category

Education

-

view

42 -

download

1

Transcript of Acc 290 acc290

ACC 290 The Latest Version A+ Study Guide

Entire Course

https://uopcourses.com/category/acc-290/

ACC 290 Week 1 Assignment WileyPLUS Assignment

Click Assignment: Week 1 Assignment within WileyPLUS to complete the

following exercises:

DO IT! 1-3

Exercise 1-3

Exercise 1-4

Exercise Excel E 2-4

IFRS 2-4

Resource: WileyPLUS

Click Assignment: Week 1 Assignment within WileyPLUS to complete the

following exercises:

DO IT! Review 1-3

Exercise 1-3

Exercise 1-4

Exercise 2-4

IFRS 2-4

ACC 290 Week 2 Assignment WileyPLUS Assignment

Resource: WileyPLUS

Click Assignment: Week 2 Assignment within WileyPLUS to complete the

following exercises:

BYP 2-2

IFRS 2-6

Exercise 3-4

BYP 3-2

IFRS 3-2

Problem 3-5

Problem 3-6

Resource: WileyPLUS

Click Assignment: Week 2 Assignment within WileyPLUS to complete the

following exercises:

BYP 2-2

IFRS 2-6

Exercise 3-4

Exercise 3-8

Exercise 3-10

BYP 3-2

IFRS 3-2

Problem 3-5A

Problem 3-6A

ACC 290 Week 3 Assignment WileyPLUS Assignment

Resource: WileyPLUS

Click Assignment: Week 3 Assignment within WileyPLUS to complete the

following exercises:

Brief Exercise 4-1

Problem 4-2A

Problem 4-3A

BYP 4-1

IFRS Practice Question 1

IFRS Practice Question 2

IFRS Practice Question 3

IFRS Practice Question 4

Resource: WileyPLUS

Click Assignment: Week 3 Assignment within WileyPLUS to complete the

following exercises:

Brief Exercise 4-1

Problem 4-2A

Problem 4-3A

BYP 4-1

IFRS Practice Question 1

IFRS Practice Question 2

IFRS Practice Question 3

IFRS Practice Question 4

ACC 290 Week 4 Assignment WileyPLUS Assignment

Resource: WileyPLUS

Click Assignment: Week 4 Assignment within WileyPLUS to complete the

following exercises:

Problem 4-8A

BYP 5-1

BYP 5-2

Question 2

Brief Exercise 5-1

Brief Exercise 5-2

IFRS 5-2

IFRS 5-4

Practice Question 1

Practice Question 2

Practice Question 3

Resource: WileyPLUS

Click Assignment: Week 4 Assignment within WileyPLUS to complete the

following exercises:

Problem 4-8A

Brief Exercise 5-1

Brief Exercise 5-2

BYP 5-1

BYP 5-2

IFRS 5-2

IFRS 5-4

Practice Question 1

Practice Question 2

Practice Question 3

ACC 290 Week 5 Assignment WileyPLUS Assignment

Resource: WileyPLUS

Click Assignment: Week 5 Assignment within WileyPLUS to complete the

following exercises:

IFRS Practice Question 1

IFRS Practice Question 2

Brief Exercise 6-5

Brief Exercise 6-7

BYP 6-1

BYP 6-2

Brief Exercise 7-4

Brief Exercise 7-6

Resource: WileyPLUS

Click Assignment: Week 5 Assignment within WileyPLUS to complete the

following exercises:

IFRS Practice Question 1

IFRS Practice Question 2

Brief Exercise 6-5

Brief Exercise 6-7

BYP 6-1

BYP 6-2

Brief Exercise 7-4

Brief Exercise 7-6

ACC 290 Comparing IFRS to GAAP Paper

Write a 700- to 1,050-word summary of your team’s discussion regarding

IFRS versus. GAAP. The summary should be structured in a

subject-by-subject format. Include an introduction and a conclusion. Your

discussion should include the answers to the following:

IFRS 2-1: In what ways does the format of a statement of financial or

position under IFRS often differ from a balance sheet presented under GAAP?

IFRS 2-2: Do the IFRS and GAAP conceptual frameworks differ in

terms of the objective of financial reporting? Explain.

IFRS 2-3: What terms commonly used under IFRS are synonymous

with common stock and balance sheet?

IFRS 3-1: Describe some of the issues the SEC must consider in

deciding whether the United States should adopt IFRS.

IFRS 4-1: Compare and contrast the rules regarding revenue

recognition under IFRS versus GAAP.

IFRS 4-2: Under IFRS, do the definitions of revenues and expenses

include gains and losses? Explain.

IFRS 7-1: Some people argue that the internal control requirements of

the Sarbanes-Oxley Act (SOX) of 2002 put U.S. companies at a competitive

disadvantage to companies outside the United States. Discuss the competitive

implications (both pros and cons) of SOX.

Format your paper consistent with APA guidelines.

Use your Financial Accounting text and at least two additional

scholarly-reviewed references.

Click the Assignment Files tab to submit your assignment.

ACC 290 WileyPLUS Final Examination

Resource: WileyPLUS

Click Assignment: Final Examination within WileyPLUS to complete the

exam. You are allowed one attempt to complete the exam. Results are auto

graded and sent to your instructor.

(Note. Final Examination questions are adapted from Financial Accounting:

Tools for Business Decision Making.)

Question 1

Your answer is correct.

Jackson Company recorded the following cash transactions for the year:

Paid $135,000 for salaries.

Paid $60,000 to purchase office equipment.

Paid $15,000 for utilities.

Paid $6,000 in dividends.

Collected $245,000 from customers.

What was Jackson’s net cash provided by operating activities?

$110,000

$35,000

$89,000

$95,000

Question 2

Your answer is correct.

Which of the following describes the classification and normal balance of the Unearned

Rent Revenue account?

Revenues, credit

Liability, credit

Expense, debit

Asset, debit

Question 3

Your answer is correct.

Posting

should be performed in account number order.

accumulates the effects of journalized transactions in the individual accounts.

involves transferring all debits and credits on a journal page to the trial balance.

is accomplished by examining ledger accounts and seeing which ones need updating

Question 4

Your answer is correct.

The following is selected information from L Corporation for the fiscal year ending

October 31, 2014.

Cash received from customers $300,000

Revenue earned 390,000

Cash paid for expenses 170,000

Cash paid for computers on November 1, 2013 that will be used for 3 years 48,000

Expenses incurred including any depreciation 216,000

Proceeds from a bank loan, part of which was used to pay for the computers 100,000

Based on the accrual basis of accounting, what is L Corporation’s net income for the

year ending October 31, 2014?

$220,000

$174,000

$204,000

$158,000

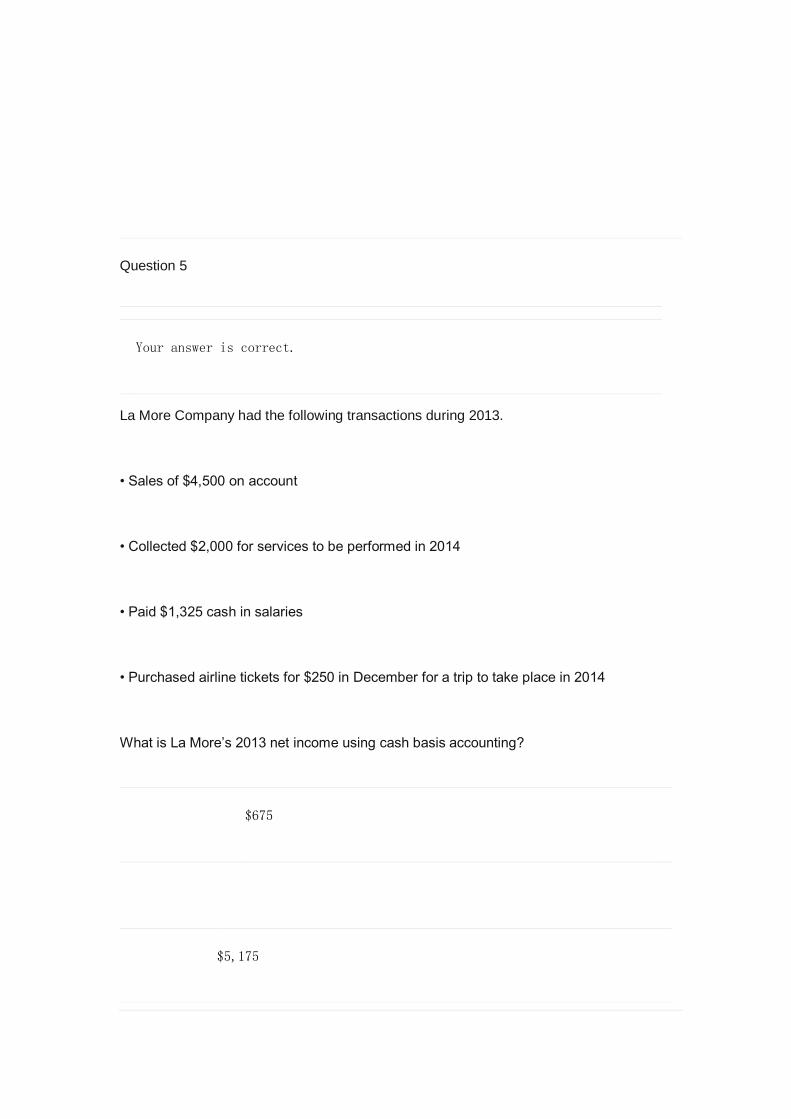

Question 5

Your answer is correct.

La More Company had the following transactions during 2013.

• Sales of $4,500 on account

• Collected $2,000 for services to be performed in 2014

• Paid $1,325 cash in salaries

• Purchased airline tickets for $250 in December for a trip to take place in 2014

What is La More’s 2013 net income using cash basis accounting?

$675

$5,175

$425

$4,925

Question 6

Your answer is correct.

Which one of the following is not a justification for adjusting entries?

Adjusting entries are necessary to bring the general ledger accounts in line with the budget.

Adjusting entries are necessary to ensure that the revenue recognition principle is followed.

Adjusting entries are necessary to ensure that the expense recognition principle is followed.

Adjusting

entries are necessary to enable financial statements to be in conformity with GAAP.

Question 7

Your answer is correct.

The Vintage Laundry Company purchased $6,500 worth of laundry supplies on

June 2 and recorded the purchase as an asset. On June 30, an inventory of

the laundry supplies indi-cated only $1,000 on hand. The adjusting entry that

should be made by the company on June 30 is:

debit Laundry, $1,000

; credit Laundry Supplies Expense, $1,000.

debit Laundry Expense, $5,500; credit Laundry Supplies, $5,500.

debit Laundry Expense, $1,000; credit Laundry Supplies, $1,000.

debit Laundry, $5,500; credit Laundry Supplies Expense, $5,500.

Question 8

Your answer is correct.

Similarities between International Financial Reporting Standards (IFRS) and

U.S. GAAP in-clude all of the following except

Cash-basis accounting is not in accordance with either IFRS or U.S. GAAP.

The form and content of financial statement

s are very similar under IFRS and U.S. GAAP.

Both IFRS and U.S. GAAP allow revaluation of items such as land and buildings to fair value.

Both IFRS and U.S. GAAP divide the eco

nomic life of companies into artificial time periods.

Question 9

Your answer is correct.

Conway Company purchased merchandise inventory with an invoice price of

$9,000 and credit terms of 2/10, n/30. What is the net cost of the goods if

Conway Company pays within the discount period?

$8,820

$8,100

$8,280

$9,000

Question 10

Your ans

wer is correct.

Stan’s Market recorded the following events involving a recent purchase of

inventory:

Received goods for $90,000, terms 2/10, n/30.

Returned $1,800 of the shipment for credit.

Paid $450 freight on the shipment.

Paid the invoice within the discount period.

As a result of these events, the company’s inventory

increased by $86,877.

increased by $88,650.

increased by $86,886.

increased by $86,436.

Question 11

Your answer is correct.

Financial information is presented below:

Operating expenses

$36,000

Sal

es revenue

150,000

Cost of goods sold105,000

Gross profit would be

$114,000.

$24,000.

$36,000.

$45,000.

Question 12

Your answer is correct.

At December 31, 2014 Mohling Company’s inventory records indicated a balance of

$602,000. Upon further investigation it was determined that this amount included the

following:

$112,000 in inventory purchases made by Mohling shipped from the seller

12/27/14 terms FOB destination, but not due to be received until January 2nd

$74,000 in goods sold by Mohling with terms FOB destination on December

27th. The goods are not expected to reach their destination until January 6th

$6,000 of goods received on consignment from Dollywood Company

What is Mohling’s correct ending inventory balance at December 31, 2014?

$484,000

$490,000

$596,000

$410,000

Question 13

Your answer is correct.

Olympus Climbers Company has the following inventory data:

July 1

Beginning inventory

20 units at $19

$380

7

Purchases

70 units at $20

1,400

22

Purchases

10 units at $22

220

$2,000

A physical count of merchandise inventory on July 30 reveals that there are 32 units on

hand. Using the FIFO inventory method, the amount allocated to cost of goods sold for

July is

$620.

$1,380.

$660.

$1,340.

Question 14

Your answer is correct.

If companies have identical inventoriable costs but use different inventory flow

assumptions when the price of goods have not been constant, then the

ending inventory of the companies will be identical.

net income of the companies will be identical.

cost of goods sold of the companies will be identical.

cost of goods purchased during the year will be identical.

Question 15

Your answer is correct.

Jenks Company developed the following information about its inventories in applying the

lower of cost or market (LCM) basis in valuing inventories:

Product

Cost

Market

A

$57,000

$60,000

B

40,000

38,000

C

80,000

81,000

If Jenks applies the LCM basis, the value of the inventory reported on the balance sheet

would be

$175,000.

$181,000.

$177,000.

$179,000.

Question 16

Your answer is correct.

The following information was available for Bowyer Company at December 31,

2014: beginning inventory $90,000; ending inventory $70,000; cost of goods

sold $880,000; and sales $1,200,000. Bowyer’s inventory turnover ratio in

2014 was

11.0 times.

15.0 times.

12.6 times.

9.8 times.

Question 17

Your answer is correct.

Use the following data to determine the total dollar amount of assets to be classified as

property, plant, and equipment.

Eddy Auto Supplies

Balance Sheet

December 31, 2014

Cash

$84,000

Accounts payable $110,000

Accounts

receivable

80,000

Salaries and wages payable 20,000

Inventory

140,000

Mortgage payable 180,000

Prepaid insurance

60,000

Total liabilities $310,000

Stock Investments

170,000

Land

190,000

Buildings $226,000

Common stock $240,000

Less: Accumulated

depreciation

(40,000) 186,000

Retained earnings 500,000

Trademarks

140,000

Total

stockholders’ equity

$740,000

Total assets

$1,050,000

Total

liabilities and stockholders’

equity

$1,050,000

$556,000

$686,000

$516,000

$376,000

Question 18

Your answer is correct.

Accounting information is relevant to business decisions because it

confirms prior expectations.

is prepared on an annual basis.

is neutral in its representations.

has been verified by external audit.

Question 19

Your answer is correct.

Howard Company had a transaction that caused a $5,000 increase in both

assets and total liabilities. This transaction could have been a(n)

repayment of a $5,000 bank loan.

purchase of office equipment for $12,000, paying $7,000 cash and issuing a note payable for

the balance.

investment of $5,000 cash in the business by the stockholders.

purchase of office equipment for $5,000 cash.

Question 20

Your answer is correct.

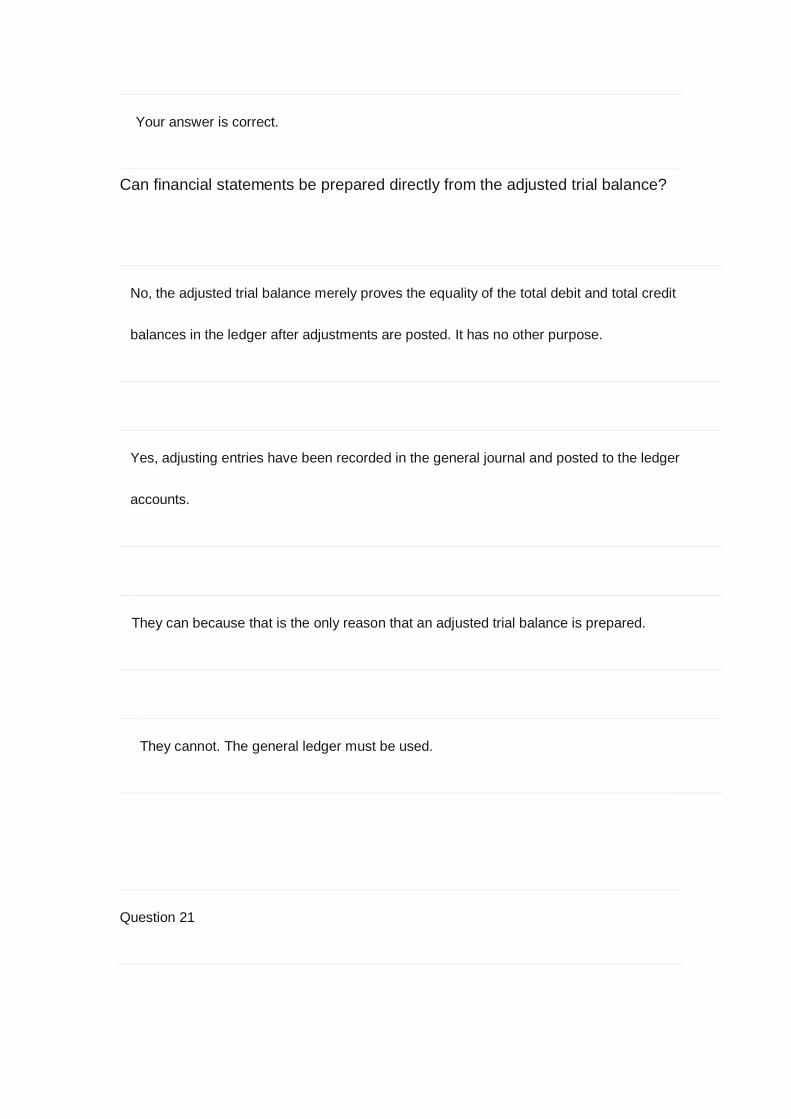

Can financial statements be prepared directly from the adjusted trial balance?

No, the adjusted trial balance merely proves the equality of the total debit and total credit

balances in the ledger after adjustments are posted. It has no other purpose.

Yes, adjusting entries have been recorded in the general journal and posted to the ledger

accounts.

They can because that is the only reason that an adjusted trial balance is prepared.

They cannot. The general ledger must be used.

Question 21

Which trial balance will consist of the greatest number of accounts?

Adjusted trial balance

Post-closing trial balance

Trial balance

All of these answer choices will contain the same number of accounts.

Question 22

Your answer is correct.

All of the following are required steps in the accounting cycle except:

preparing a work sheet.

preparing an adjusted trial balance.

preparing a post-closing trial balance.

journalizing and posting closing entries.

Question 23

Your answer is correct.

A sales discount does not

provide the purchaser with a cash saving.

increase a contra revenue account.

increase an operating expense account.

reduce the amount of cash received from a credit sale.

Question 24

Your answer is correct.

American Importers reports net income of $50,000 and cost of goods sold of $450,000.

If the company’s gross profit rate was 40%, net sales were

$750,000.

$1,125,000.

$825,000.

$1,175,000.

Question 25

Your answer is correct.

The manager of Weiser is given a bonus based on net income before taxes. The net

income after taxes is $35,700 for FIFO and $29,400 for LIFO. The tax rate is 30%. The

bonus rate is 20%. How much higher is the manager’s bonus if FIFO is adopted instead

of LIFO?

$1,800

$9,000

$6,300

$12,600

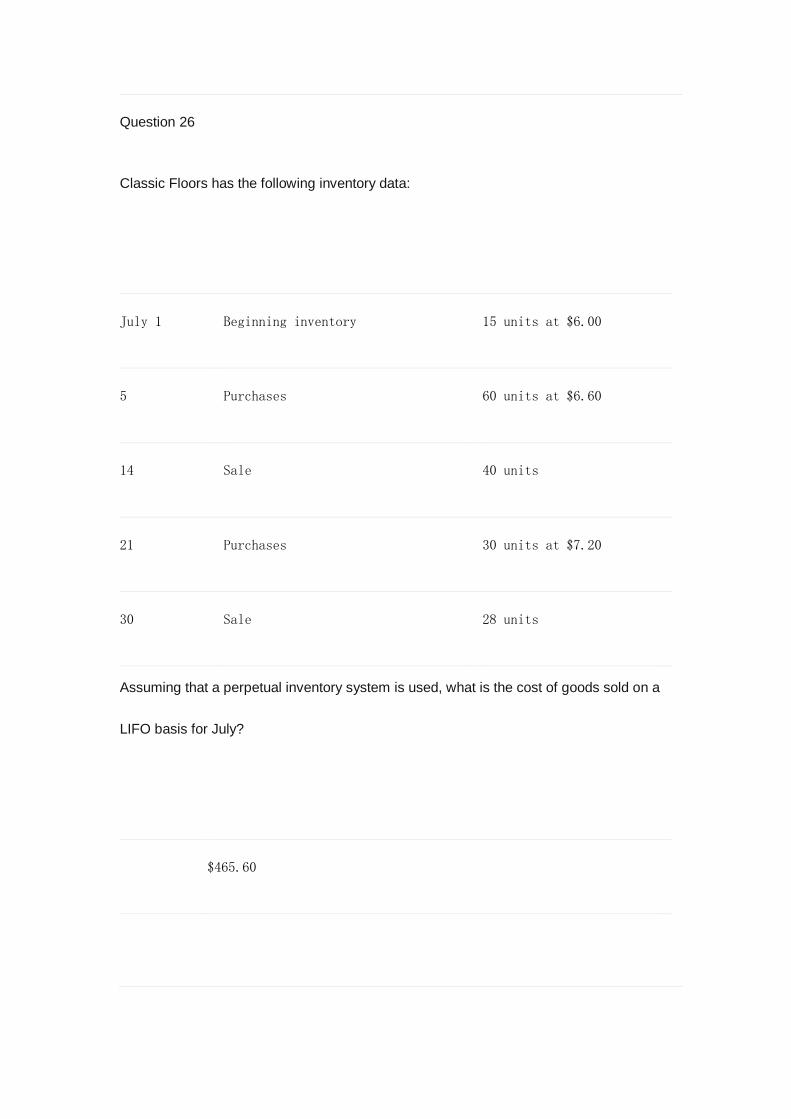

Question 26

Classic Floors has the following inventory data:

July 1

Beginning inventory

15 units at $6.00

5

Purchases

60 units at $6.60

14

Sale

40 units

21

Purchases

30 units at $7.20

30

Sale

28 units

Assuming that a perpetual inventory system is used, what is the cost of goods sold on a

LIFO basis for July?

$465.60

$236.40

$702.00

$348.00

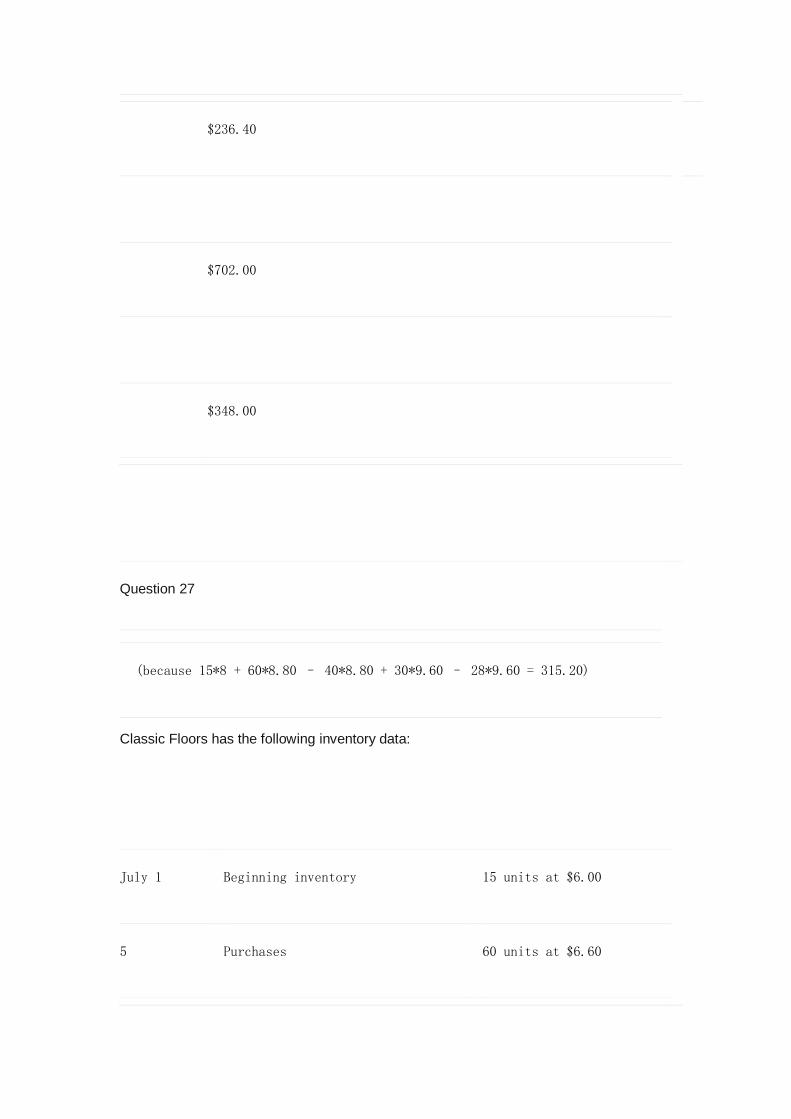

Question 27

(because 15*8 + 60*8.80 – 40*8.80 + 30*9.60 – 28*9.60 = 315.20)

Classic Floors has the following inventory data:

July 1

Beginning inventory

15 units at $6.00

5

Purchases

60 units at $6.60

14

Sale

40 units

21

Purchases

30 units at $7.20

30

Sale

28 units

Assuming that a perpetual inventory system is used, what is the value of ending

inventory on a LIFO basis for July?

$702.00

$354.00

$236.40

$465.60

Question 28

Your answer is correct.

Which of the following is not one of the main factors that contribute to fraudulent

activity?

Opportunity.

Incompatible duties.

Financial pressure.

Rationalization.

Question 29

Your answer is correct.

What is the rationale for the internal control principle, segregation of duties?

Segregation of duties causes companies to hire more employees and thus it supports

the economy.

History has shown that employees are generally dishonest and thus cannot be entrusted

with performing related duties.

Control is most effective when only one person is responsible for a give task.

The work of one employee should, without duplication of effort, provide a reliable

basis for evaluating the work of another employee.

Question 30

Your answer is correct.

Under IFRS

comparative prior-period information is not required, but financial statements must be provided

annually.

comparative prior-period information must be presented, but financial statements need not be

provided annually.

comparative prior-period information is not required, but financial statements need not be

provided annually.

comparative prior-period information must be presented, and financial statements must be

provided annually.