ACA 2015: Ready, Set, Comply - The Benefit Companies · -14- ACA 2015: Ready, Set, Comply The...

79

-1- ACA 2015: Ready, Set, Comply Bottom Line Driven Health Benefits Planning ACA 2015: Ready, Set, Comply Jeffery A. Schultz Phone: 262.207.1999 ext. 112 Email: [email protected] Vice President, BeneCo of Wisconsin Innovation. Dedication. Knowledge. Purpose. Integrity. Vision. Talent. Results.

Transcript of ACA 2015: Ready, Set, Comply - The Benefit Companies · -14- ACA 2015: Ready, Set, Comply The...

-1- ACA 2015: Ready, Set, Comply

Bottom Line Driven Health Benefits Planning

ACA 2015: Ready, Set, Comply

Jeffery A. Schultz Phone: 262.207.1999 ext. 112

Email: [email protected] Vice President, BeneCo of Wisconsin

Innovation. Dedication. Knowledge. Purpose. Integrity. Vision. Talent. Results.

-2- ACA 2015: Ready, Set, Comply

Who We Are

BeneCo of Wisconsin, Inc.:

A member of The Benefit Companies, a privately held company.

Have been providing insurance and employee benefits consulting since 1971.

A full service benefits firm serving over 1,200 companies and organizations ranging from 10 to 50,000 employees.

Headquartered in Brookfield, WI with additional Wisconsin offices in Green Bay, and Plymouth.

-3- ACA 2015: Ready, Set, Comply

Jeff Schultz Vice President BeneCo of Wisconsin

Justin Andaloro Manager of Marketing & Communications BeneCo of Wisconsin

-4- ACA 2015: Ready, Set, Comply

Ground Rules

Some questions may fall under

Haven't read,

Haven't heard,

Guidance not released

Just don’t know…

-5- ACA 2015: Ready, Set, Comply

Top Questions

1. Do the Applicable Large Employer penalties apply to me…and when?

2. What’s the cost of terminating coverage and paying the penalty?

3. Is my plan affordable as defined by the law?

4. Which affordability safe harbor should we use?

5. What does the look back and stability periods mean for eligibility?

6. Will my plan headcount increase or decrease and what are the implications?

7. How does ACA influence my wellness plan?

8. How can I use exchanges and subsidies to my plan’s advantage?

9. Will I have to pay the Cadillac Tax?

10. What do I need to know about 6055 and 6056 reporting requirements?

-6- ACA 2015: Ready, Set, Comply

#1 Do the Applicable Large Employer penalties apply to me…and when?

-7- ACA 2015: Ready, Set, Comply

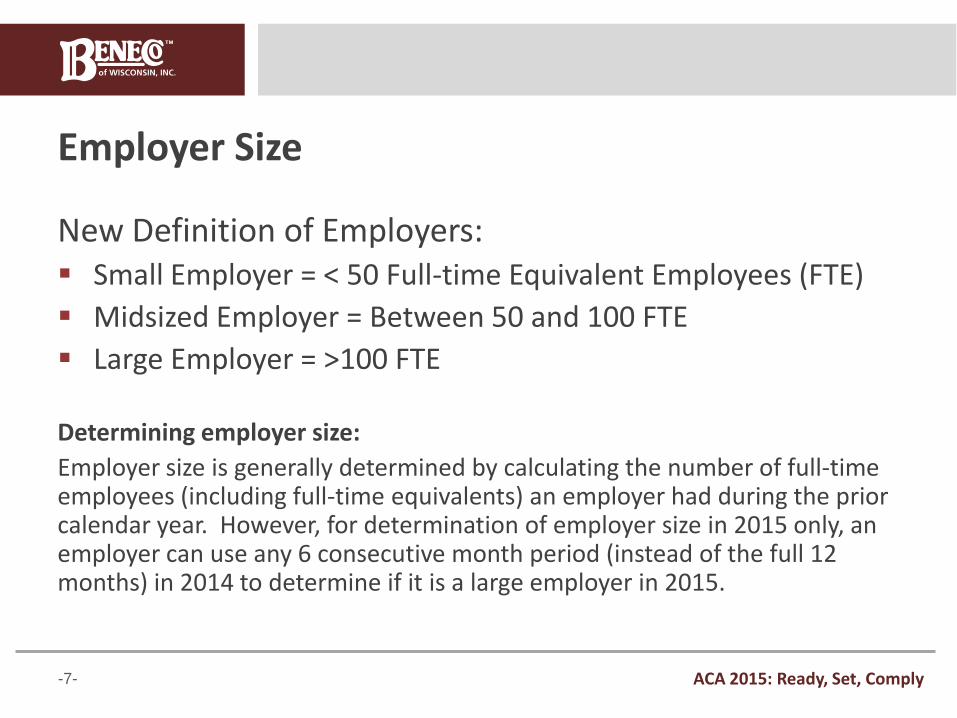

Employer Size

New Definition of Employers: Small Employer = < 50 Full-time Equivalent Employees (FTE)

Midsized Employer = Between 50 and 100 FTE

Large Employer = >100 FTE

Determining employer size:

Employer size is generally determined by calculating the number of full-time employees (including full-time equivalents) an employer had during the prior calendar year. However, for determination of employer size in 2015 only, an employer can use any 6 consecutive month period (instead of the full 12 months) in 2014 to determine if it is a large employer in 2015.

-8- ACA 2015: Ready, Set, Comply

When do the 4980(a) and 4980(b) penalties apply?

Employer Size When ACA Applies

Small Employer 2-49 FTE N/A

Midsized Employer 50-99 Depends: 2015-2016

Large Employer 100+ 2015

*Calendar year transition relief applies to both Midsized and Large employers

-9- ACA 2015: Ready, Set, Comply

Transition Relief for SOME Midsized Employers

The penalty is delayed until the first day of an employer’s 2016 plan year for midsized employers IF:

Maintenance of Workforce and Aggregate Hours of Service: The employer does not

reduce its workforce during the period of February 9, 2014 to December 31, 2014 solely to qualify (reductions in workforce for “bona fide” business reasons are permissible);

Maintenance of Previously Offered Health Coverage: For the period of February 9, 2014 until the end of the employer’s 2015 plan year, the employer does not eliminate or materially reduce any health coverage it offered as of February 9, 2014

“Material” reduction means a 5% or greater reduction in the dollar amount of the employer contribution towards individual premiums, or any reduction in the percentage of the employer’s share.

The employer must certify that it satisfies these conditions on a form to be provided by

the IRS

-10- ACA 2015: Ready, Set, Comply

Non-Calendar Year Plans Generally, plans that have non-calendar year plans will receive transition relief to avoid the employer mandate penalties until the start of their plan first plan year rather than 1/1/2015. To qualify:

Plan had to be a non-calendar year plan on 12/27/2012 and the plan date has not been changed after 12/27/2012 (for example, the employer has not pushed the beginning of plan year from May 1st to December 1st).

Different types of employees are provided different relief.

Eligible Employees under plan’s eligibility terms as of 2/9/2014

Generally, these employees receive transition relief as long as they are offered affordable coverage that meets Minimum Actuarial Value no later than the first day of the plan year beginning in 2015

Employees not eligible under plan’s eligibility terms as of 2/9/2014 provided…(Next slide)

-11- ACA 2015: Ready, Set, Comply

Non-Calendar Year Plans Non-Eligible Employees as of 2/9/14 Generally, these employees receive transition relief as long the employer offered or provided a significant percentage of employees coverage AND they are offered affordable coverage that meets Minimum Actuarial Value no later than the first day of the plan year beginning in 2015. Significant Percentage Rule #1: At least ¼ of all of the employer’s employees were covered as of any date from

February 10, 2013 to February 9, 2014; or At least 1/3 of all of the employer’s employees were offered coverage during the

most recent open enrollment period that ended before February 9, 2014 Significant Percentage Rule #2

At least 1/3 of all of the employer’s full-time employees were covered as of any date from February 10, 2013 to February 9, 2014; or

At least ½ of all of the employer’s full-time employees were offered coverage during the most recent open enrollment

-12- ACA 2015: Ready, Set, Comply

Non-Calendar Year Plans

Example:

ABC Company has 1000 employees with a 5/1 plan year.

They provide coverage that meets Minimum Actuarial Value, but the coverage is not affordable for 200 of the employees on 5/1/2015.

ABC company has an exposure of $250 per month for each of these 200 employees beginning on January 1, 2015 because the coverage offered on 5/1/2015 is not affordable.

-13- ACA 2015: Ready, Set, Comply

#2 What’s the cost of terminating coverage and paying the penalty?

-14- ACA 2015: Ready, Set, Comply

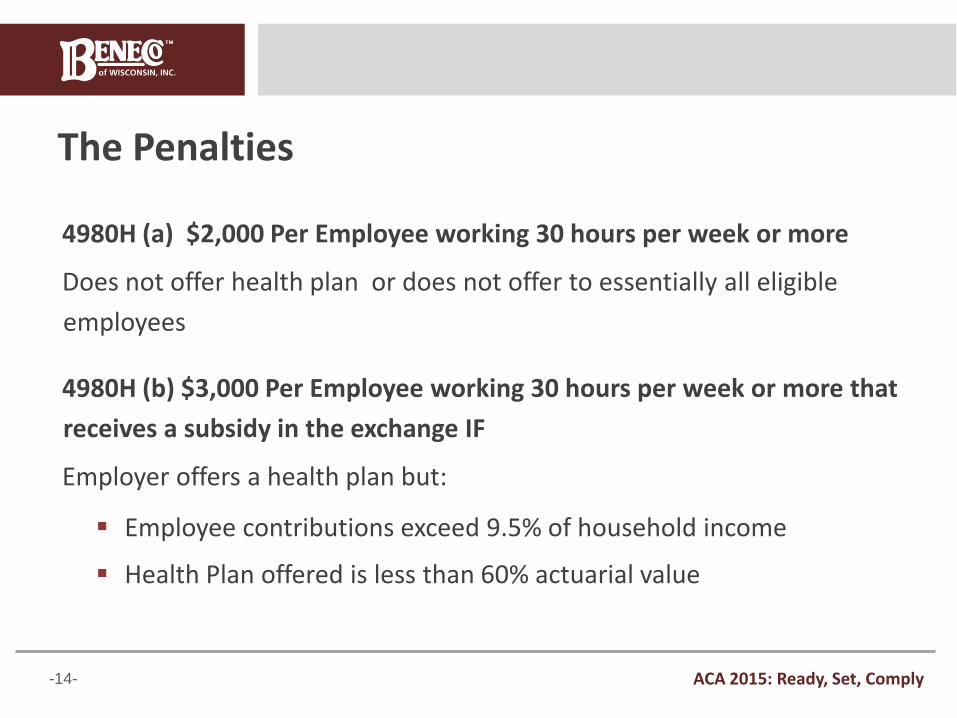

The Penalties

4980H (a) $2,000 Per Employee working 30 hours per week or more

Does not offer health plan or does not offer to essentially all eligible

employees

4980H (b) $3,000 Per Employee working 30 hours per week or more that

receives a subsidy in the exchange IF

Employer offers a health plan but:

Employee contributions exceed 9.5% of household income

Health Plan offered is less than 60% actuarial value

-15- ACA 2015: Ready, Set, Comply

Cost of Terminating Coverage For Mid & Large Employers

The penalty is $2,000 x FTEs (Less 30 Ees) if at least one FTE received premium tax credit.

Employers with 100+ FTE subtract 80 employees for 2015 only.

IE; A group with 200 employees. (200-80)=120 X 2000 = $240,000 in penalties.

If the employer does not offer coverage to 95% of their population working 30 hours per week or more, is seen as not offering coverage at all. 70% for 2015.

-16- ACA 2015: Ready, Set, Comply

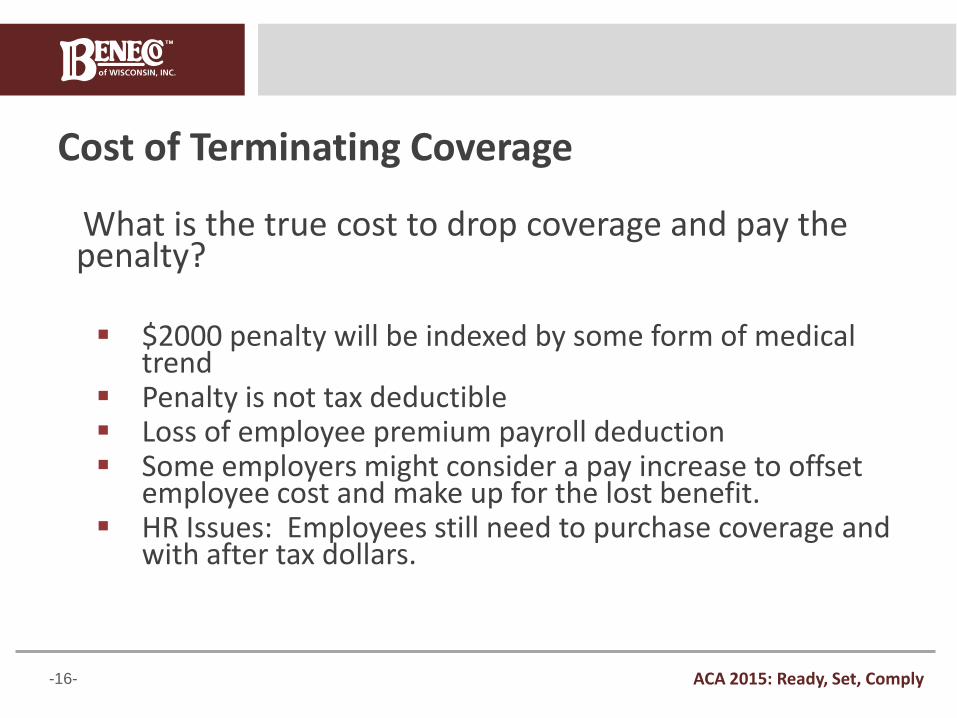

Cost of Terminating Coverage

What is the true cost to drop coverage and pay the penalty? $2000 penalty will be indexed by some form of medical

trend Penalty is not tax deductible Loss of employee premium payroll deduction Some employers might consider a pay increase to offset

employee cost and make up for the lost benefit. HR Issues: Employees still need to purchase coverage and

with after tax dollars.

-17- ACA 2015: Ready, Set, Comply

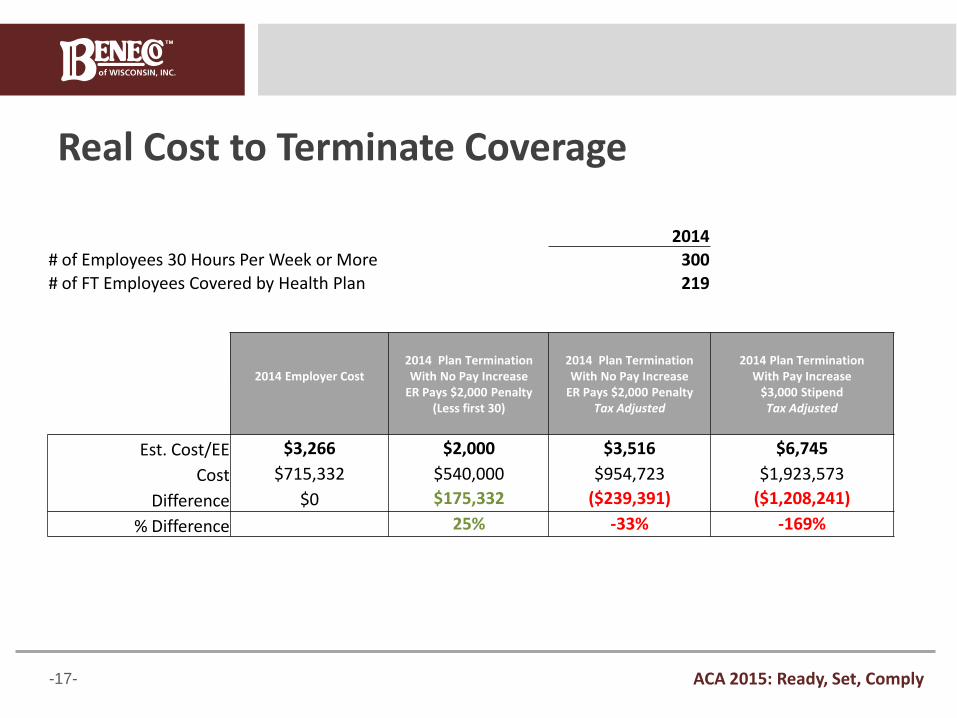

Real Cost to Terminate Coverage

2014 # of Employees 30 Hours Per Week or More 300 # of FT Employees Covered by Health Plan 219

2014 Employer Cost

2014 Plan Termination With No Pay Increase

ER Pays $2,000 Penalty (Less first 30)

2014 Plan Termination With No Pay Increase

ER Pays $2,000 Penalty Tax Adjusted

2014 Plan Termination With Pay Increase

$3,000 Stipend Tax Adjusted

Est. Cost/EE $3,266 $2,000 $3,516 $6,745

Cost $715,332 $540,000 $954,723 $1,923,573

Difference $0 $175,332 ($239,391) ($1,208,241)

% Difference 25% -33% -169%

-18- ACA 2015: Ready, Set, Comply

#3 Is my plan affordable as defined by the law?

-19- ACA 2015: Ready, Set, Comply

What is considered Affordable?

Two ways to look at Affordability

The Employee side in terms of getting subsidies

The Employer side in terms of paying penalties

For Employers:

Each employee must be tested

Cannot average incomes

Has to be affordable for employees at 30+ hours per week.

Lower wage/higher contribution likely issues

-20- ACA 2015: Ready, Set, Comply

Which Premium to Use Premium is measured at 9.5% of income for SINGLE coverage

Measured on the lowest cost single plan that meets minimum actuarial value.

Assumes that employees do not achieve the wellness requirements, regardless of their achievement status.

As shown below, affordability is based on $600 as the employee contribution for all employees, even if they are paying $120.

Monthly Premiums

Wellness Participant Wellness Achiever Wellness Leader

Score 86-100

No Participation

(COBRA Rates) Score 0-50

Score 51-60

Score 61-70

Score 71-85 or

Improve by 5+

Employee $600.00 $300.00 $240.00 $180.00 $150.00 $120.00 Employee + Spouse $1,050.00 $525.00 $420.00 $315.00 $262.50 $210.00

Employee + Child(ren) $900.00 $450.00 $360.00 $270.00 $225.00 $180.00 Family $1,300.00 $650.00 $520.00 $390.00 $325.00 $260.00

-21- ACA 2015: Ready, Set, Comply

The Safe Harbors

Affordability originally intended to be measured on household income.

Safe harbors were provided to measure on an employee only level

Federal Poverty Line Safe Harbor

W-2 Wages Safe Harbor

Rate of pay Safe Harbor

-22- ACA 2015: Ready, Set, Comply

Federal Poverty Line Safe Harbor

2014 FPL is $11,670 for a single

Assume all employees earn 100% of poverty level

Calculate contribution against the $11,670 FPL

Employers can set their premium at $92.38 regardless of employee’s income and be considered affordable.

$11,670 X 9.5% =$1108.65 or $92.38 Per Month Employee Premium is $600 per month. FAIL

-23- ACA 2015: Ready, Set, Comply

W-2 Wages Safe Harbor

Uses the employee’s W-2 income (box1) for the current year.

Does not include pre-tax contributions for 401(k) or cafeteria plans.

Employee earning $30,000 has $3600 of pretax contributions. W-2 Box 1 = $30,000-$3,600 = $26,400

$26,400 X 9.5% =$2,508 or $209.00 Per Month Employee Premium is $600 per month. FAIL

-24- ACA 2015: Ready, Set, Comply

W-2 Wages Safe Harbor

Uses the employee’s W-2 income (box1) for the current year.

Does not include pre-tax contributions for 401(k) or cafeteria plans.

Employee earning $30,000 has $3600 of pretax contributions. W-2 Box 1 = $30,000-$3,600 = $26,400

$26,400 X 9.5% =$2,508 or $209.00 Per Month Employee Premium is $600 per month. FAIL

-25- ACA 2015: Ready, Set, Comply

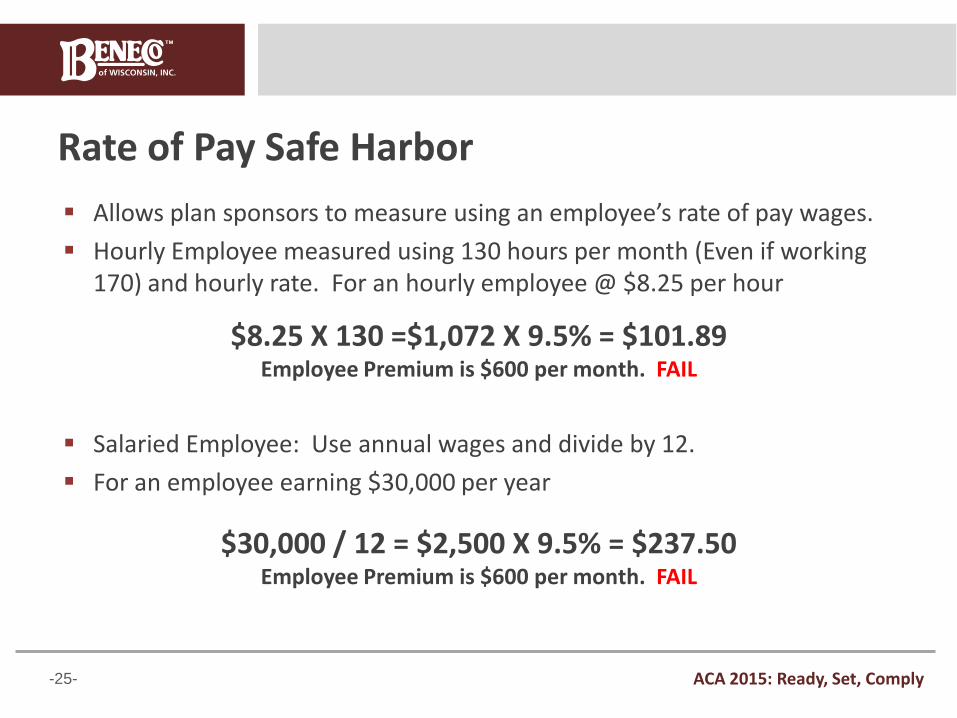

Rate of Pay Safe Harbor

Allows plan sponsors to measure using an employee’s rate of pay wages.

Hourly Employee measured using 130 hours per month (Even if working 170) and hourly rate. For an hourly employee @ $8.25 per hour

Salaried Employee: Use annual wages and divide by 12.

For an employee earning $30,000 per year

$8.25 X 130 =$1,072 X 9.5% = $101.89 Employee Premium is $600 per month. FAIL

$30,000 / 12 = $2,500 X 9.5% = $237.50 Employee Premium is $600 per month. FAIL

-26- ACA 2015: Ready, Set, Comply

#4 Which affordability safe harbor should we use?

-27- ACA 2015: Ready, Set, Comply

Safe Harbor Considerations

Considerations FPL W-2 Rate of Pay

High % of 40 hour per week hourly employees x x

High % of Variable Hour Employees x x

High % of Pre-Tax Deductions x x

Low Paid Tipped or Commissioned Employees x x

Need to institute a Safe Harbor Plan x x

Have a single premium higher than $92.38 x x

*These are general suggestions for discussion purposes only

-28- ACA 2015: Ready, Set, Comply

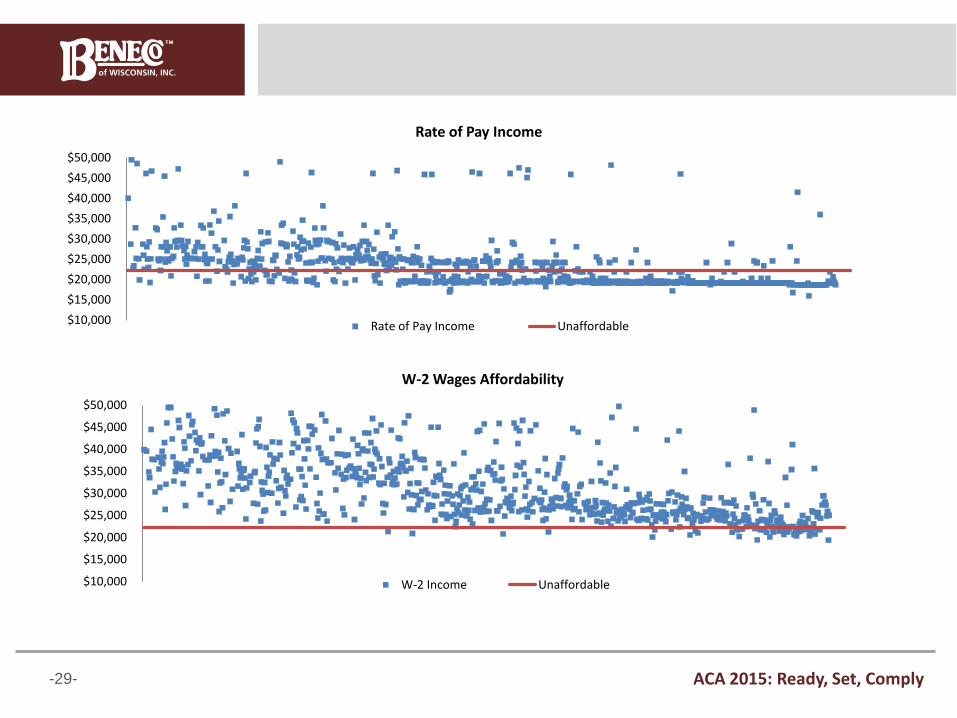

How Many Employees are Unaffordable under each Safe Harbor?

Rate of Pay W-2 Wages

Number of Eligible and Unaffordable 400 120

Average Wage $31,500 $36,887

Average Max Premium For Those Unaffordable $167 $168

-29- ACA 2015: Ready, Set, Comply

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

Rate of Pay Income

Rate of Pay Income Unaffordable

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

W-2 Wages Affordability

W-2 Income Unaffordable

-30- ACA 2015: Ready, Set, Comply

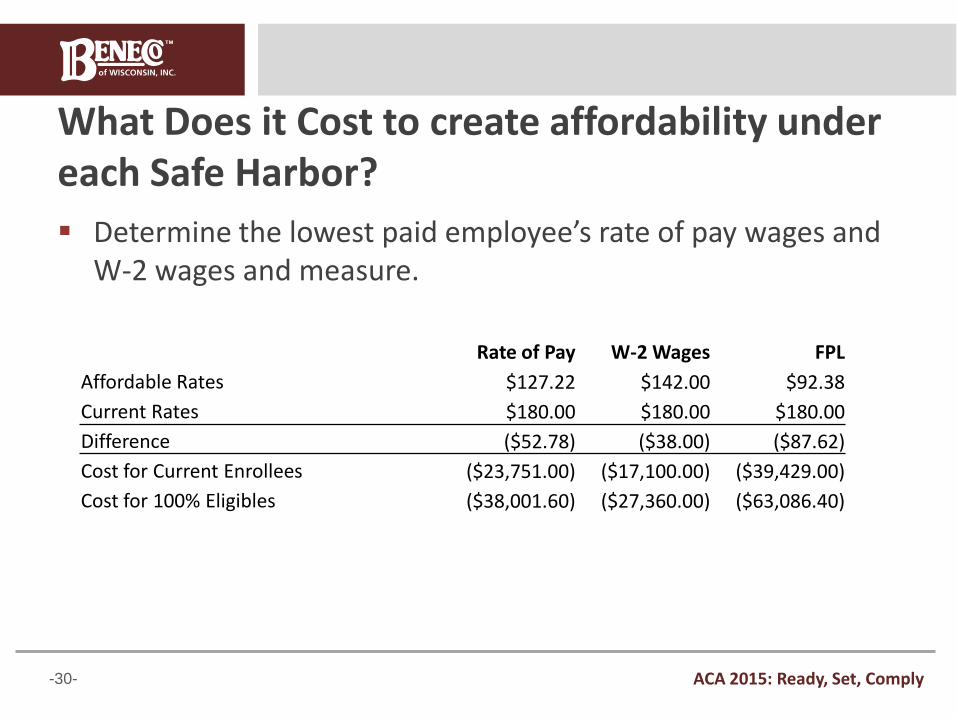

What Does it Cost to create affordability under each Safe Harbor?

Determine the lowest paid employee’s rate of pay wages and W-2 wages and measure.

Rate of Pay W-2 Wages FPL

Affordable Rates $127.22 $142.00 $92.38

Current Rates $180.00 $180.00 $180.00

Difference ($52.78) ($38.00) ($87.62)

Cost for Current Enrollees ($23,751.00) ($17,100.00) ($39,429.00)

Cost for 100% Eligibles ($38,001.60) ($27,360.00) ($63,086.40)

-31- ACA 2015: Ready, Set, Comply

#5 What does the look back and stability periods mean for eligibility?

-32- ACA 2015: Ready, Set, Comply

The Options to Measure Eligibility

30 Hours per week is the new eligibility standard. Determine Hours worked by the following methods:

Monthly measurement period

Look Back and Stability Period

-33- ACA 2015: Ready, Set, Comply

The Monthly Measurement Period

Default measurement method under the Affordable Care Act. AKA: Doing Nothing.

Generally, this method requires employers to offer coverage to any employee for any month in which that employee works 130 hours.

Challenging method to implement: At the beginning of the month the employer does not

know how many hours the employee will work At the end of the month once the employer has made the

determination, it is too late to offer the employee coverage.

-34- ACA 2015: Ready, Set, Comply

The Safe Harbor: Types of Employees New Hires

Full-Time Employees: Employee that is reasonably expected to work 30 hours per

week or more during the initial measurement period.

Variable Hour Employees: An employee that cannot be determined at the

employees start date if the employee is reasonably expected to average 30 hours per week or more during the initial measurement period.

Part-Time Employees: Employee has a reasonable expectation on the start date

that an employee will be employed on average less than 30 hours per week.

Seasonal Employees: Typically works for a period of six months or less, and that

period should begin each calendar year in approximately the same part of the year, such as summer or winter.

Ongoing Employees: All employees that have completed their initial measurement

period.

-35- ACA 2015: Ready, Set, Comply

The Safe Harbor: Ongoing Employees

Standard Measurement Period 10/15/14 to 10/14/15

10/15/13 10/15/14 1/1/15 1/1/16 10/15/15

Standard Measurement Period 10/15/13 to 10/14/14

Admin Period 10/15/14 to 12/31/14

Standard Stability Period 1/1/15 to 12/31/15

Admin Period 10/15/15 to 12/31/15

Standard Stability Period

1/1/16 to 12/31/16

For all ongoing employees the employer may use a Measurement and Stability period to determine if an employee works more that 30 hours per week. In this example, the employer uses a 12 month stability period with a standard measurement period beginning October 15th.

If the employee averages more than 30 hours per week during the Standard Measurement Period, the employer must treat them as a full-time employee in the Standard Stability Period and offer them coverage for the full length of the period. The Administrative Period is a period of no more than 90 days where the employer can make a determination of the employee’s status and notify them of their eligibility.

-36- ACA 2015: Ready, Set, Comply

Standard Measurement Period 10/15/15 to 10/14/16

5/1/14 10/15/14 5/1/15 6/1/15 10/15/15 1/1/16

Initial Measurement Period 5/1/14 to 4/30/15

6/1/16 1/1/17

Initial Stability Period 6/1/15 to 5/31/16

10/15/16

Standard Measurement Period 10/15/14 to 10/14/15

Admin Period 10/15/15 to 12/31/15

Standard Stability Period 1/1/16 to 12/31/16

Admin Period 10/15/16 to 12/31/16

Standard Stability Period

1/1/17 to 12/31/17

Admin Period 5/1/15 to 5/31/15

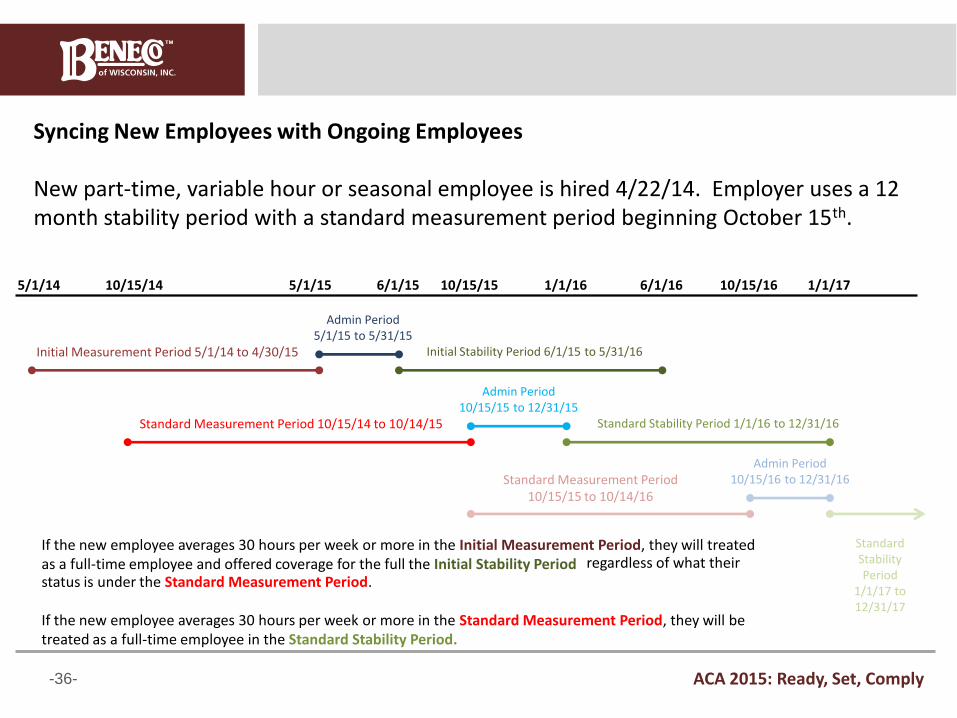

Syncing New Employees with Ongoing Employees New part-time, variable hour or seasonal employee is hired 4/22/14. Employer uses a 12 month stability period with a standard measurement period beginning October 15th.

If the new employee averages 30 hours per week or more in the Initial Measurement Period, they will treated as a full-time employee and offered coverage for the full the Initial Stability Period regardless of what their status is under the Standard Measurement Period. If the new employee averages 30 hours per week or more in the Standard Measurement Period, they will be treated as a full-time employee in the Standard Stability Period.

-37- ACA 2015: Ready, Set, Comply

Transition Relief for 2015

Transition Relief: Shorter “look-back” period permitted leading up to 2015 stability period.

While the look-back measurement period must generally be the same length as the stability period, for the 2014 to 2015 cycle, employers may use a measurement period as short as 6 months leading up to a 12 month stability period. To take advantage of this transition relief, the measurement period must

begin no later than July 1, 2014

For employees hired during or after this special short Measurement Period, an employer with a 12-month Initial Stability Period will have to track their hours during a 12-month Initial Measurement Period.

-38- ACA 2015: Ready, Set, Comply

#6 Will my plan headcount increase or decrease and what are the implications?

-39- ACA 2015: Ready, Set, Comply

Potential In Migration

Current Employer Spend $538,960

Current Average Cost Per Employee On Plan: ($538,960 / 83) $6,493

Current or Newly Eligible 180

Currently on Plan 83

Current Participation 46%

Potential Additions 97

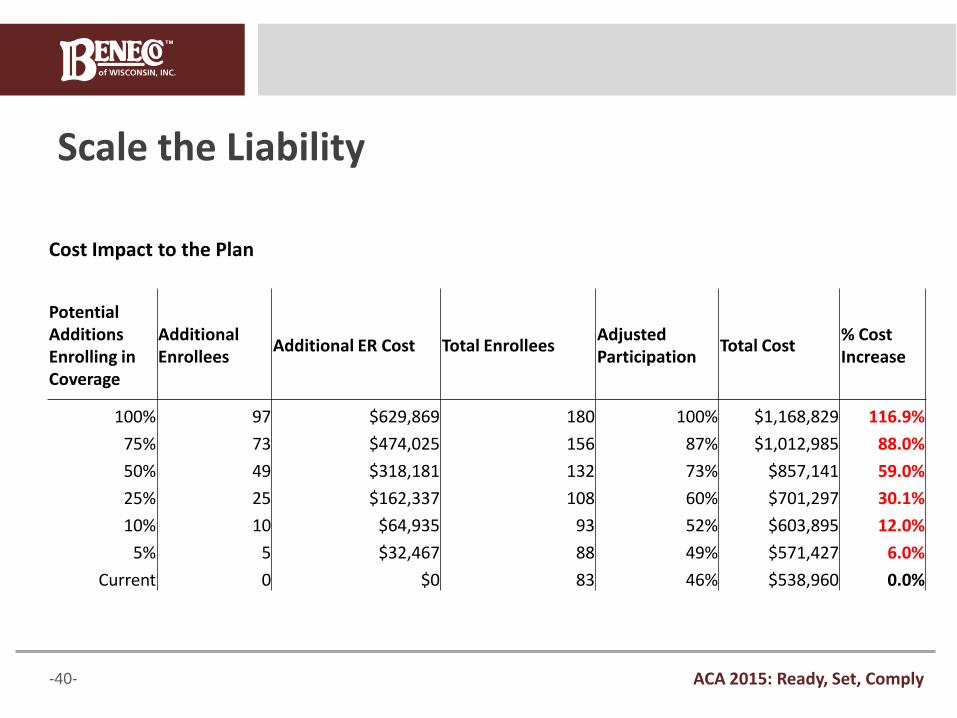

-40- ACA 2015: Ready, Set, Comply

Scale the Liability

Cost Impact to the Plan

Potential Additions Enrolling in Coverage

Additional Enrollees

Additional ER Cost Total Enrollees Adjusted Participation

Total Cost % Cost Increase

100% 97 $629,869 180 100% $1,168,829 116.9%

75% 73 $474,025 156 87% $1,012,985 88.0%

50% 49 $318,181 132 73% $857,141 59.0%

25% 25 $162,337 108 60% $701,297 30.1%

10% 10 $64,935 93 52% $603,895 12.0%

5% 5 $32,467 88 49% $571,427 6.0%

Current 0 $0 83 46% $538,960 0.0%

-41- ACA 2015: Ready, Set, Comply

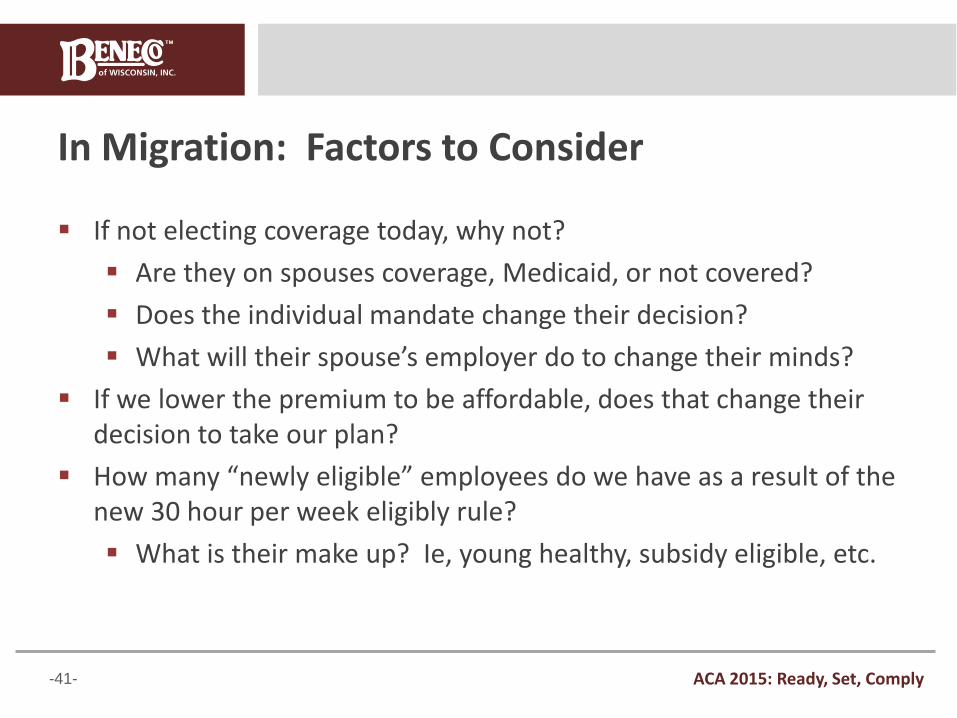

In Migration: Factors to Consider

If not electing coverage today, why not?

Are they on spouses coverage, Medicaid, or not covered?

Does the individual mandate change their decision?

What will their spouse’s employer do to change their minds?

If we lower the premium to be affordable, does that change their decision to take our plan?

How many “newly eligible” employees do we have as a result of the new 30 hour per week eligibly rule?

What is their make up? Ie, young healthy, subsidy eligible, etc.

-42- ACA 2015: Ready, Set, Comply

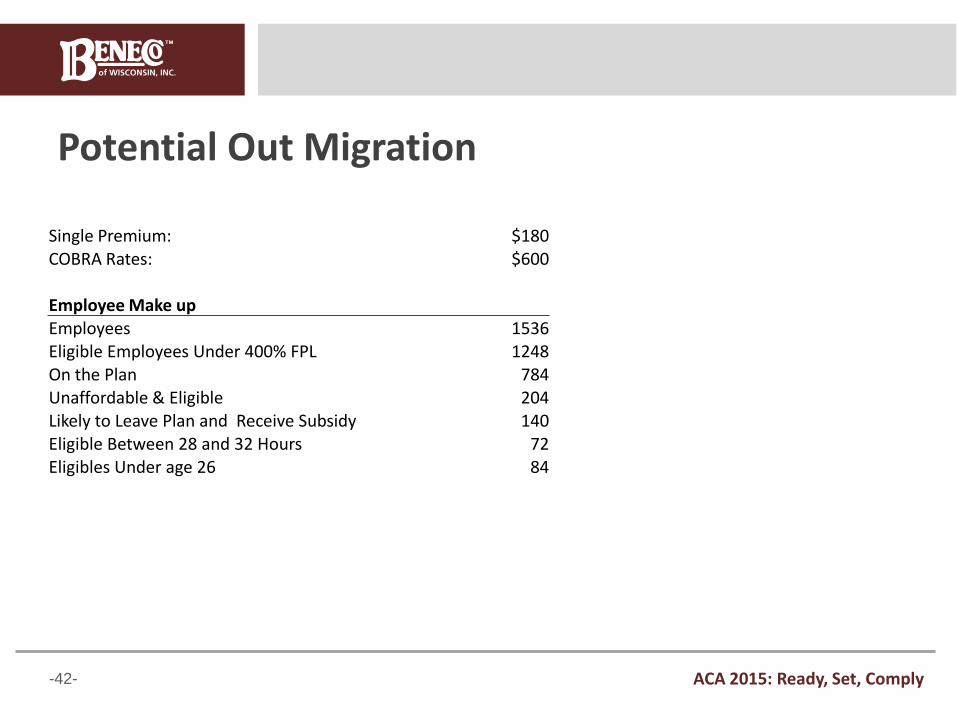

Potential Out Migration

Single Premium: $180 COBRA Rates: $600

Employee Make up Employees 1536 Eligible Employees Under 400% FPL 1248 On the Plan 784 Unaffordable & Eligible 204 Likely to Leave Plan and Receive Subsidy 140 Eligible Between 28 and 32 Hours 72 Eligibles Under age 26 84

-43- ACA 2015: Ready, Set, Comply

Potential Out Migration

$5,000.00

$15,000.00

$25,000.00

$35,000.00

$45,000.00

$55,000.00

$65,000.00

$75,000.00

$85,000.00

$95,000.00

Income

Unaffordable

Subsidy Eligible

Likely to Take Subsidy

100% FPL

138% FPL

-44- ACA 2015: Ready, Set, Comply

#7 How does ACA influence my wellness plan?

-45- ACA 2015: Ready, Set, Comply

What ACA Allows: Outcomes Based Wellness

COBRA Rates Current 30% Total

Premium Total Premium Annual Contribution Surcharge Achiever Non-Achiever Difference Single $600 $120 $180 $120 $300 $2,160 Family $1,300 $260 $390 $260 $650 $4,680

-46- ACA 2015: Ready, Set, Comply

What ACA Allows: Tobacco -Outcomes Based Wellness

COBRA Rates Current 50% Total

Premium Total Premium Annual

Contribution Surcharge Achiever Non-Achiever Difference Single $600 $120 $300 $120 $420 $3,600

Family $1,300 $260 $650 $260 $910 $7,800

-47- ACA 2015: Ready, Set, Comply

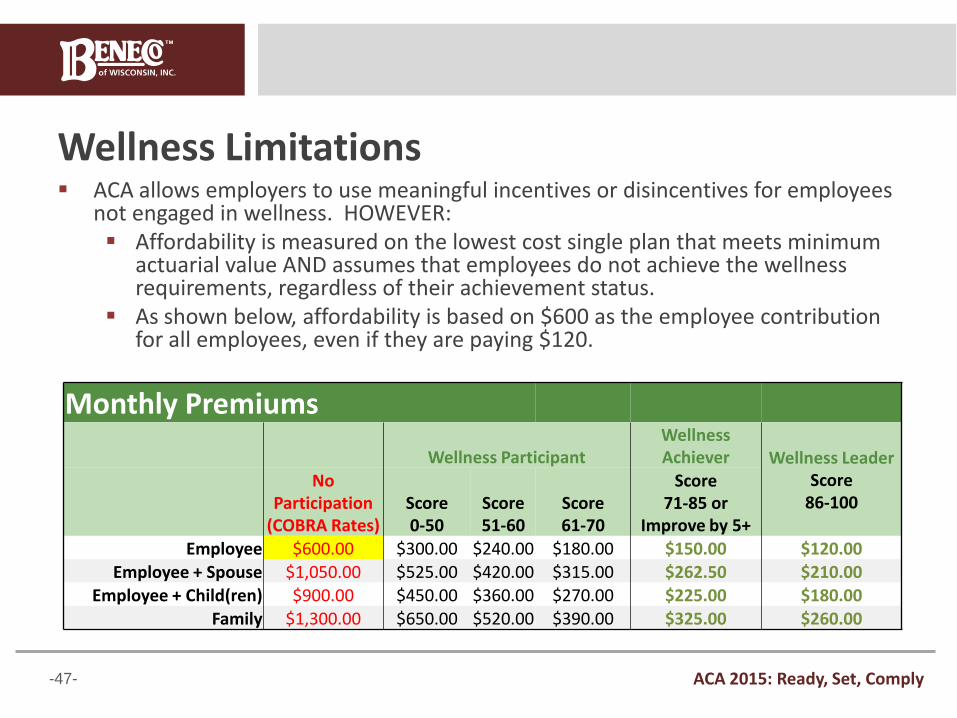

Wellness Limitations ACA allows employers to use meaningful incentives or disincentives for employees

not engaged in wellness. HOWEVER: Affordability is measured on the lowest cost single plan that meets minimum

actuarial value AND assumes that employees do not achieve the wellness requirements, regardless of their achievement status.

As shown below, affordability is based on $600 as the employee contribution for all employees, even if they are paying $120.

Monthly Premiums

Wellness Participant Wellness Achiever Wellness Leader

Score 86-100

No Participation

(COBRA Rates) Score 0-50

Score 51-60

Score 61-70

Score 71-85 or

Improve by 5+

Employee $600.00 $300.00 $240.00 $180.00 $150.00 $120.00 Employee + Spouse $1,050.00 $525.00 $420.00 $315.00 $262.50 $210.00

Employee + Child(ren) $900.00 $450.00 $360.00 $270.00 $225.00 $180.00 Family $1,300.00 $650.00 $520.00 $390.00 $325.00 $260.00

-48- ACA 2015: Ready, Set, Comply

How do we keep a Robust wellness program with Affordability Challenges?

The employer has three choices:

Have little to no wellness incentives to stay affordable.

Offer coverage that is intentionally unaffordable for some and strategically pay some penalties

Create a “Safe Harbor” plan that satisfies the affordability requirements and minimum actuarial value requirements.

-49- ACA 2015: Ready, Set, Comply

The Safe Harbor Plan

A second plan allows an employer to use maximum incentives on Plan Option 1, and pass all the ACA tests on Plan Option 2.

Only offered to singles Dependent Children @ COBRA rates. No Spouses.

No Wellness Close to 60% Actuarial Value Employees who either do not participate or achieve in the wellness

program are likely: Highest risk or lowest engaged employees. They will either:

Pay a higher premium Consider the Safe Harbor Plan

-50- ACA 2015: Ready, Set, Comply

Safe Harbor Plan Funding Options

Set premium at Federal Poverty Line Safe Harbor $92.38 Set premium to be affordable for the lowest rate of pay wage

Why rate of pay wage and not W-2? Set premium at 9.4% of the employee’s rate of pay wage Run the numbers:

Lowest Premium to be Affordable $127.22

Average 9.4% of all Singles Ees $193.42

Average 9.4% Premium of likely Ees $138.22

FPL Safe Harbor $92.38

-51- ACA 2015: Ready, Set, Comply

Advantages and Disadvantages

Potential Employer Advantages

Employer will remain immunized from penalties

Employer can deploy a robust wellness strategy

Higher risk or non-participant employees subsidize their cost either through increased premium or through plan design.

Potential Employer Disadvantages

High risk employees will remain on the plan.

High risk employees will remain dis-engaged in wellness

-52- ACA 2015: Ready, Set, Comply

#8 How can I use exchanges and subsidies to my plan’s advantage?

-53- ACA 2015: Ready, Set, Comply

Plans have 3 Strategies

Employers have three strategies when benefits planning:

Drop coverage and pay the penalty = $2,000

Offer coverage and make sure the plan is affordable and meets MV to avoid penalties

Offer coverage that is unaffordable for some and strategically pay some penalties =$3,000

-54- ACA 2015: Ready, Set, Comply

Who is Subsidy Eligible

In Wisconsin employees between 100% of FPL and 400% of FPL IF the employer either doesn’t offer a plan or doesn’t offer a plan that meets Minimum Value or the single rate exceeds 9.5% of the employee’s household income. Other states 138%-400% FPL.

FPL guidelines for 2014

Household Size 100% 133% 150% 200% 300% 400%

1 $11,670 $15,521 $17,505 $23,340 $35,010 $46,680

2 $15,730 $20,921 $23,595 $31,460 $47,190 $62,920

3 $19,790 $26,321 $29,685 $39,580 $59,370 $79,160

4 $23,850 $31,721 $35,775 $47,700 $71,550 $95,400

-55- ACA 2015: Ready, Set, Comply

Subsidies in the Exchange Subsidies are not insignificant

Do you have wellness incentives/penalties that extend beyond the following?

What if we incentivized the lowest risk employees to stay on our plan?

Age 30 60 30 45

Family Single Single Family 4 Family 5

Wage $10 / Hour 30

Hours Per Week $10 / Hour 30 Hours

Per Week $21 / Hour 40

Hours Per Week $5,000 Per

month

Income $15,600 $15,600 $45,000 $60,000

Health Insurance Premium $3,127 $7,171 $9,381 $11,982

Subsidy $2,634 $6,678 $6,731 $7,832

Annual Premium $493 $493 $2,650 $4,150

Monthly Premium $41 $41 $221 $346

Information from Kasier Subsidy Calculator

-56- ACA 2015: Ready, Set, Comply

High Risks Members bring Significant Cost

-57- ACA 2015: Ready, Set, Comply

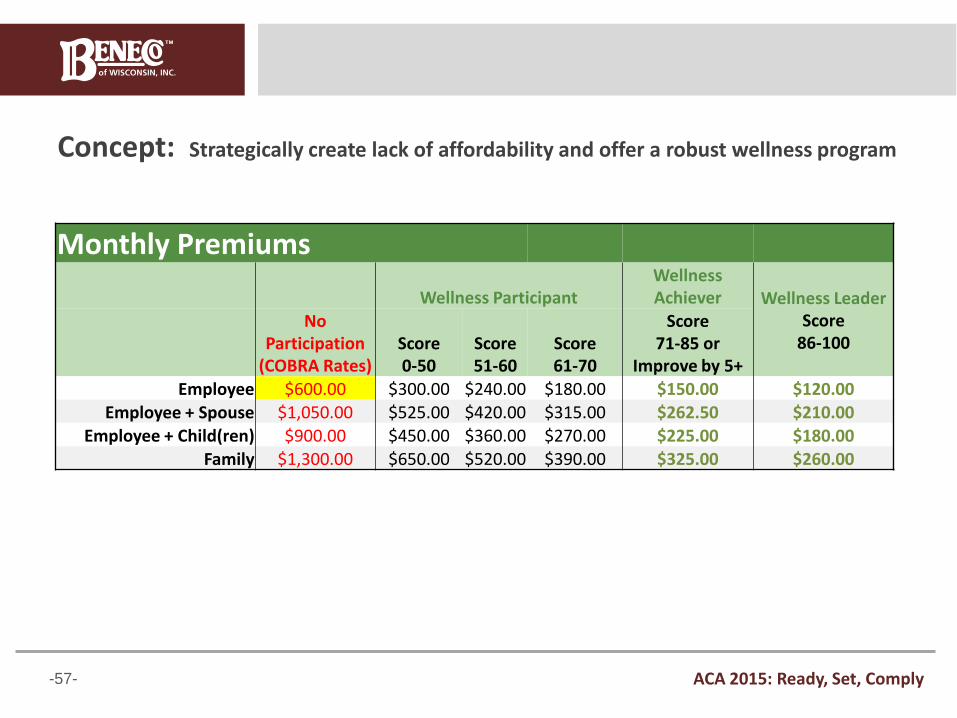

Concept: Strategically create lack of affordability and offer a robust wellness program

Monthly Premiums

Wellness Participant Wellness Achiever Wellness Leader

Score 86-100

No Participation

(COBRA Rates) Score 0-50

Score 51-60

Score 61-70

Score 71-85 or

Improve by 5+ Employee $600.00 $300.00 $240.00 $180.00 $150.00 $120.00

Employee + Spouse $1,050.00 $525.00 $420.00 $315.00 $262.50 $210.00 Employee + Child(ren) $900.00 $450.00 $360.00 $270.00 $225.00 $180.00

Family $1,300.00 $650.00 $520.00 $390.00 $325.00 $260.00

-58- ACA 2015: Ready, Set, Comply

Impact on Employees

Certain employees will be eligible for subsidies

Employees who either do not participate or achieve are likely

Highest risk or lowest engaged employees. They will either:

Pay a higher premium

Consider other coverage options. We now have those options. Some quite affordable.

Exchange and non exchange plans will likely be LESS costly for highest risk employees considering significant wellness surcharges

Likely subsidy eligible

Subsidy “sweet spot” up to 300% of FPL

Employees will gravitate towards the less expensive coverage

-59- ACA 2015: Ready, Set, Comply

Potential Advantages and Disadvantages to Employer

Potential Advantages

Employer will remain immunized from penalties in most cases.

Employer can deploy a robust wellness strategy

Higher risk or non-participant employees will likely migrate out of plan

Employer loses high risk individuals

Win/Win so long as employer costs are not less than $5000 PEPY. (Tax adjusted Penalty =$5,000)

Potential Disadvantages

Employer will likely pay penalties on those migrating

Significant analysis must be done prior to implementation

Will not work for younger, lower paid groups

Needs to work within your culture

-60- ACA 2015: Ready, Set, Comply

#9 Will I have to pay the Cadillac Tax?

-61- ACA 2015: Ready, Set, Comply

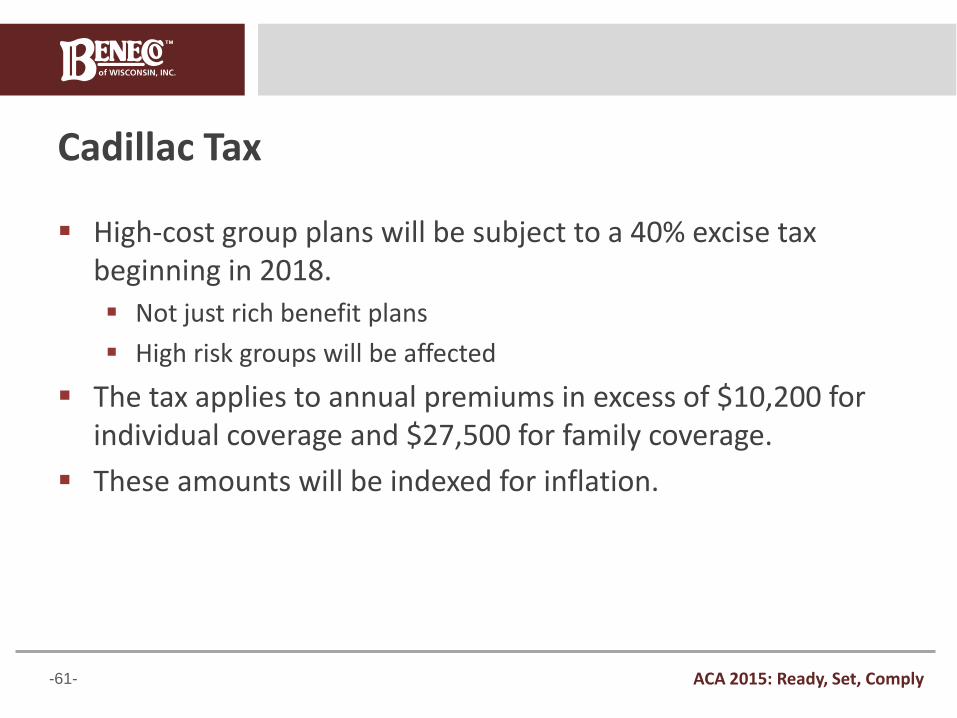

Cadillac Tax

High-cost group plans will be subject to a 40% excise tax beginning in 2018.

Not just rich benefit plans

High risk groups will be affected

The tax applies to annual premiums in excess of $10,200 for individual coverage and $27,500 for family coverage.

These amounts will be indexed for inflation.

-62- ACA 2015: Ready, Set, Comply

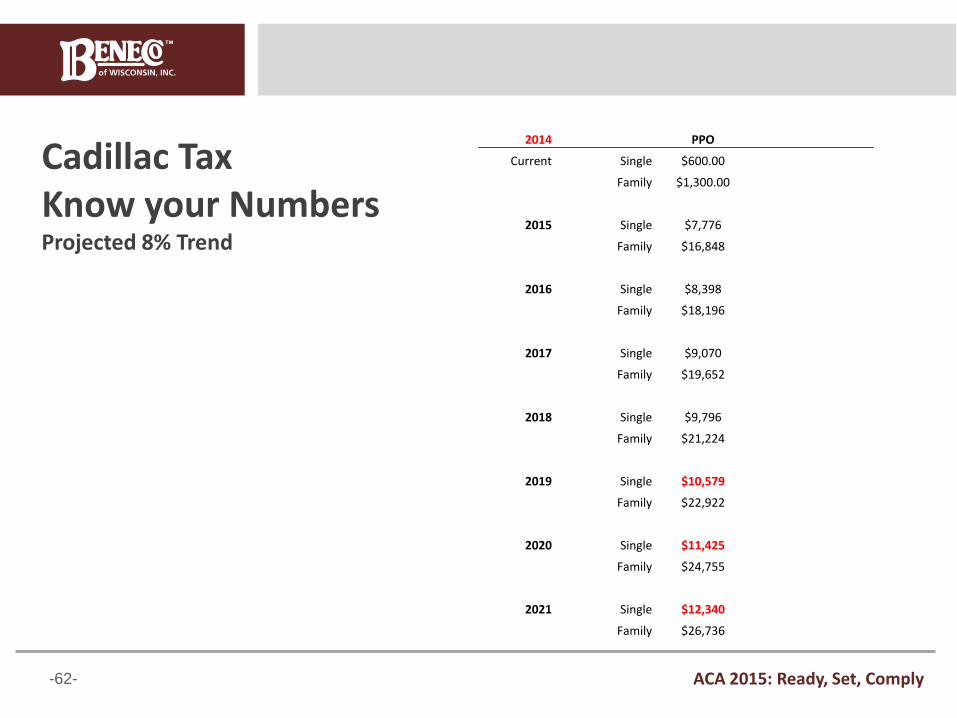

Cadillac Tax Know your Numbers Projected 8% Trend

2014 PPO

Current Single $600.00

Family $1,300.00

2015 Single $7,776

Family $16,848

2016 Single $8,398

Family $18,196

2017 Single $9,070

Family $19,652

2018 Single $9,796

Family $21,224

2019 Single $10,579

Family $22,922

2020 Single $11,425

Family $24,755

2021 Single $12,340

Family $26,736

-63- ACA 2015: Ready, Set, Comply

#10 What do I need to know about 6055 and 6056 reporting requirements?

-64- ACA 2015: Ready, Set, Comply

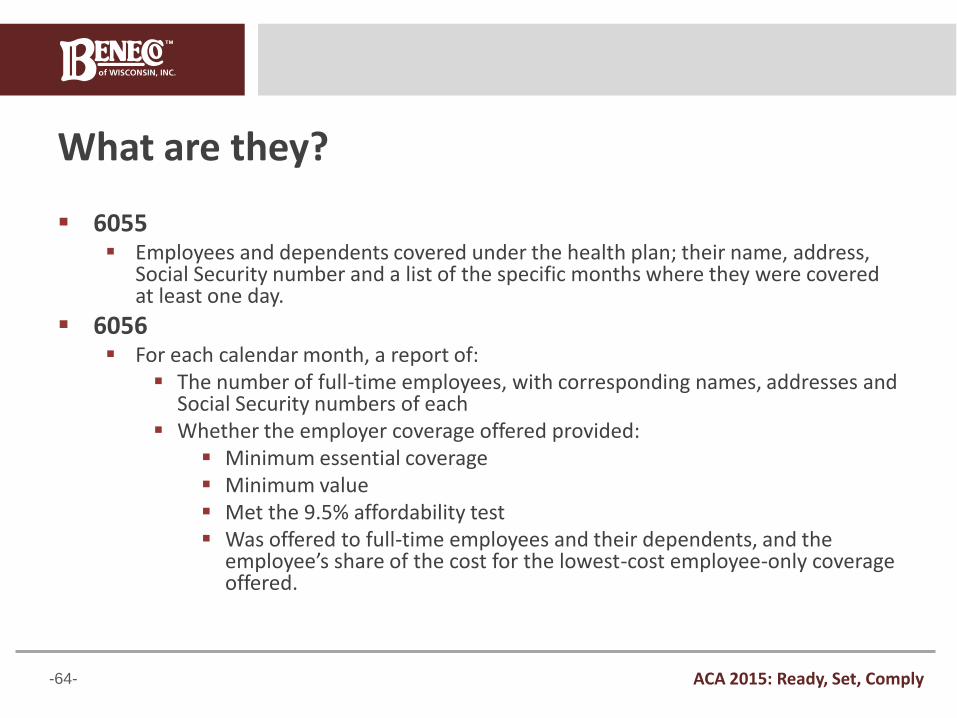

What are they?

6055 Employees and dependents covered under the health plan; their name, address,

Social Security number and a list of the specific months where they were covered at least one day.

6056 For each calendar month, a report of:

The number of full-time employees, with corresponding names, addresses and Social Security numbers of each

Whether the employer coverage offered provided: Minimum essential coverage Minimum value Met the 9.5% affordability test Was offered to full-time employees and their dependents, and the

employee’s share of the cost for the lowest-cost employee-only coverage offered.

-65- ACA 2015: Ready, Set, Comply

Simplified Filing Options

Qualified Offer (No need to provide monthly details)

Employer offers MEC that provides minimum actuarial value for all months during the year in which an employee was full-time.

The cost of single coverage can be not more than FPL level for affordability purposes

Must be offered to spouse and dependents

A 6056 will still need to be filled for all other employees.

-66- ACA 2015: Ready, Set, Comply

Simplified Filing Options

98 Percent Offers

An employer can certify that it offered MEC and Minimum Value coverage that is affordable to 98 percent or more of its full-time employees (and their dependents) does not have to determine whether each employee is a full-time employee, or report the total number of employees reported on the 6056 return

For purposes of this simplified option, coverage is affordable if it meets any of the affordability safe harbors under Section 4980H (Employer Shared Responsibility).

-67- ACA 2015: Ready, Set, Comply

What Do I Do Now?

-68- ACA 2015: Ready, Set, Comply

What needs to be done? Be Tactical and Strategic

Tactical Be accurate and timely with compliance Know the tasking and timelines Enlist the appropriate resources

Strategic Know your group Know your risk Model probable scenarios Create risk enhancement /preservation incentives Understand the $$ involved in pay or play Leverage ACA to your advantage

-69- ACA 2015: Ready, Set, Comply

What do I do Now?

Audit, Assess, Analyze, Communicate and Decide

Conduct Analyses: Maximum plan changes allowed under grandfather provision. Maximum employee contribution changes allowed under grandfather

provision. Net cost of remaining grandfathered vs. eliminating grandfathered

plan. Eligibility requirement cost impact. Subsidy eligibility analysis. Medicaid eligibility analysis. Probable subsidy and Medicaid eligible IN/OUT migration. Affect on risk pool due to subsidy eligible migration Cadillac tax projection.

-70- ACA 2015: Ready, Set, Comply

What needs to be done?

Be Strategic; Audit, Assess, Analyze, Communicate and Decide

Decide

On a 3-5 year strategy based on

Your test answers

Affordability

Culture

Moving the ACA levers to your advantage

-71- ACA 2015: Ready, Set, Comply

Pulling it all together creating a long term plan

ABC Co Health Insurance Pro forma March 2013

2013 2014 2015 2016 2017 2018 Plan Design

Ded 1000/3000 1250/3750 1250/3750 1500/4500 1500/4500 2000/6000 Coins 90/70 90/70 90/70 90/70 90/70 90/70 OOP 2000/6000 2500/7500 2500/7500 3000/9000 3000/9000 4000/12000

Estimated Actuarial Value 84% 80% 80% 80% 80% 75%

Employee Contributions 15% 15% 20% 23% 25% 25%

Wellness Incentives 5% 10% 10% 10% 10% 10%

Cost

Total cost $3,080,250 $3,385,760 $3,588,906 $3,876,019 $4,186,100 $4,437,266

Employer Cost $3,080,250 $3,047,184 $3,230,015 $3,294,616 $3,558,185 $3,549,813

% Change -1.1% 6.0% 2.0% 8.0% -0.2%

Employee Cost $0 $338,576 $358,891 $581,403 $627,915 $887,453

% Change 6.0% 62.0% 8.0% 41.3% Number of covered employees 452 452 452 452 452 452 Cost per employee per year $6,845 $7,491 $7,940 $8,575 $9,261 $9,817

% Change 9.4% 6.0% 8.0% 8.0% 6.0% COBRA Rates Monthly

8%/6% Single $401 $425 $451 $487 $526 $557 Family $1,040 $1,102 $1,169 $1,262 $1,363 $1,445

Annualized

Single $4,812 $5,101 $5,407 $5,839 $6,306 $6,685 Family $12,480 $13,229 $14,023 $15,144 $16,356 $17,337

Cadillac Tax Threshold Single $10,200

Family $27,500 Excise tax $0 $0 $0 $0 $0 $0

-73- ACA 2015: Ready, Set, Comply

We are grateful AM 620 WTMJ has asked BeneCo to host a radio series to educate listeners on how best to tackle the ins and outs of the Affordable Care Act (ACA). Focused primarily on educating: Business Owners, CEO's, CFO's and HR professionals; we will help them determine if ACA is a "Top 3" or "Top 30" business priority. Tune in to hear us discuss critical ACA challenges to business on September 27, from 3-4pm. Be sure to listen for the advertisements!

-74- ACA 2015: Ready, Set, Comply

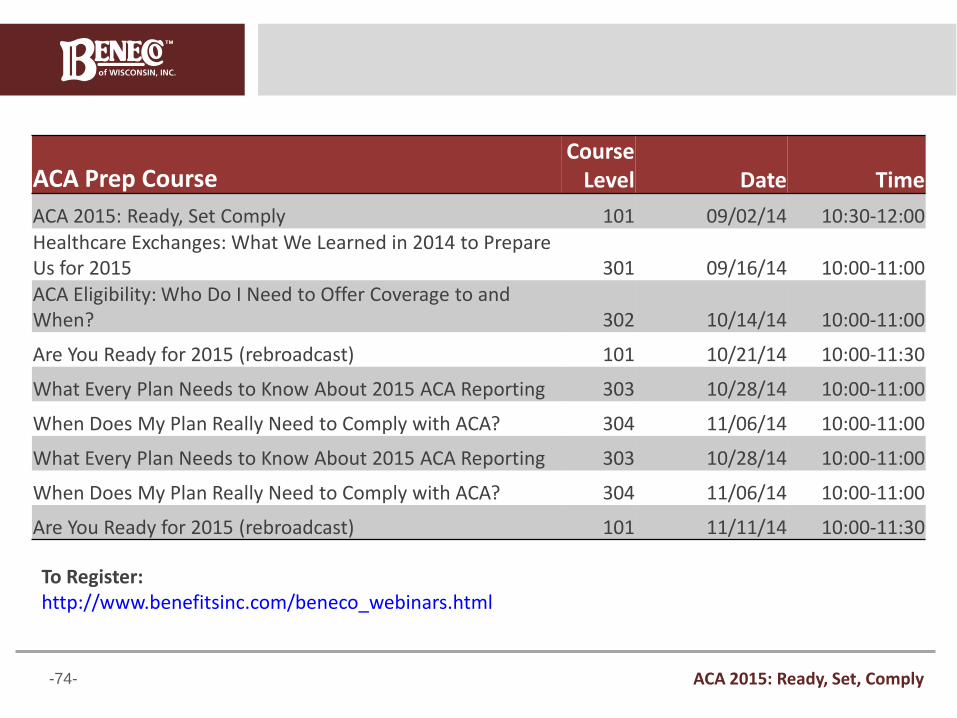

ACA Prep Course Course

Level Date Time

ACA 2015: Ready, Set Comply 101 09/02/14 10:30-12:00 Healthcare Exchanges: What We Learned in 2014 to Prepare Us for 2015 301 09/16/14 10:00-11:00 ACA Eligibility: Who Do I Need to Offer Coverage to and When? 302 10/14/14 10:00-11:00

Are You Ready for 2015 (rebroadcast) 101 10/21/14 10:00-11:30

What Every Plan Needs to Know About 2015 ACA Reporting 303 10/28/14 10:00-11:00

When Does My Plan Really Need to Comply with ACA? 304 11/06/14 10:00-11:00

What Every Plan Needs to Know About 2015 ACA Reporting 303 10/28/14 10:00-11:00

When Does My Plan Really Need to Comply with ACA? 304 11/06/14 10:00-11:00

Are You Ready for 2015 (rebroadcast) 101 11/11/14 10:00-11:30

To Register: http://www.benefitsinc.com/beneco_webinars.html

-75- ACA 2015: Ready, Set, Comply

ACA Prep Course Course

Level Date Time What You Need to Know to Pass a DOL Audit (rebroadcast) 300 09/23/14 10:00-11:00 Cadillac Tax: Creating a Glide Path to Minimize the 2018 Excise Tax (rebroadcast) 314 09/30/14 10:00-11:00 Top Five Most Inaccurate Assumptions About ACA and How to Avoid Them (rebroadcast) 301 10/07/14 10:00-11:00 Wellness Based Incentives: Creating Culturally Sensitive Outcome Based Premium Differentials (rebroadcast) 312 11/20/14 10:00-11:00

To Register: http://www.benefitsinc.com/beneco_webinars.html

-76- ACA 2015: Ready, Set, Comply

ACA Impact Study

ACA Impact Study How will ACA impact my organization? What do I need to plan for?

Free initial consultation Fee for service basis based on plan complexity ACA Sustainability Analysis How do I create a long term sustainable ACA cost strategy and

still comply? Fee for service basis based on plan complexity

-77- ACA 2015: Ready, Set, Comply

Ask us about Haiti… The work: Orphan care and sponsorship, tent

city refugee relocation and community development, microenterprise other ministry opportunities

To get more info or engaged in some way drop us a email, or for a glimpse of the work go to www.newlife4kids.org or www.missiondiscovery.org

2014 Upcoming trips: October

-78- ACA 2015: Ready, Set, Comply

Jeff Schultz Vice President BeneCo of Wisconsin 262-207-1999 ext 112 [email protected]

Justin Andaloro Manager of Marketing & Communications BeneCo of Wisconsin 262-207-1999 ext 114 [email protected]

For Follow up Information or Questions

To Register for upcoming webinars: http://www.benefitsinc.com/beneco_webinars.html

-79- ACA 2015: Ready, Set, Comply

Questions?