Absa AgriBusiness Presenter name Subject Agrimark trends Agric outlook 2 October 2008 Disclaimer:...

50

Absa AgriBusiness Presenter name Subject Agrimark trends Agric outlook 2 October 2008 Disclaimer: Although everything has been done to ensure the accuracy of the information, the Bank takes no responsibility for actions or losses that might occur due to the usage of this information.

-

Upload

lester-riley -

Category

Documents

-

view

213 -

download

0

Transcript of Absa AgriBusiness Presenter name Subject Agrimark trends Agric outlook 2 October 2008 Disclaimer:...

Absa AgriBusiness

Presenter nameSubject

Agrimark trends

Agric outlook

2 October 2008

Disclaimer: Although everything has been done to ensure the accuracy of the information, the Bank takes no responsibility for actions or losses that might occur due to the usage of this information.

Absa AgriBusiness

Agricultural outlook - Content

• General market trends

• Field crops– Maize, Wheat, Sunflower, Soya

• Fibre – Cotton, Wool, Mohair

• Livestock– Poultry, Pork, Beef, Mutton, Dairy Ostrich

• Vegetables– Tomato, Potato, Cabbage, Carrots

Absa AgriBusiness

Absa AgriBusiness

Economic market principals with in agriculture

Comments• South African farmers face a 60% plus price exposure

to the outside world and are therefore by implication global players in a global market.

• They therefore have very little control over pricing levels and tend to be price takers, with prices ranging between import parity and export parity depending on local supply and demand resulting in increased price volatility

• Factors influencing prices over which they have no control are international production trends, international farming subsidies, exchange rates, import and export tariffs.

• Production risk due to nature also contributes to production volatility which in turn lead to an increase in price volatility

• Framers therefore have to manage PRICE and PRODUCTION if they want to make a success of their business

SA Rainfall trends

0

200

400

600

800

1000

Rain

(mm

)

Rain 3 yr Avg Long-term Avg

SA Agricultural's Exposure to the International Market

05,000

10,00015,00020,00025,00030,00035,00040,00045,000

1980 1985 1990 1995 2000 2005

(R '0

00

)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Exports Imports Import + Exports as % of GPV

SA yellow maize prices (R/ton

200

700

1,200

1,700

2,200

2,700

3,200

3,700

J an-03 J an-04 J an-05 J an-06 J an-07 J an-08 J an-09 J an-10

Import Parity Export Parity Domestic

Absa AgriBusiness

New Market environment – Technology is changing the world

Pointers

• Demand technology

• Taste enhancement / Packaging / Presentation / Time value enhancements

• Variety, safety and convenience is taken as a given

• Information technology

• Connectivity

• Here now attitude

• Transport technology

• World is becoming a smaller place

• Delivery just in time

• Storage technology

• Improved shelf life

• No more seasonality

• Production technology

• GMO’s - Selection / fertilizers etc.

• Productivity enhancement

Absa AgriBusiness

Agric Cost curve

Absa AgriBusiness

Economic market principles within agriculture

Cost curve

In the long term agriculture is experiencing a cost curve of approximately 3% per annum (The price of Farming requisites increases faster than producer prices however for 2008/09 season we expect a cost curve of more than 30%

To survive this, farmers need to become more productive (increase output in relation to inputs) this is mainly done by:

• Improving production efficiencies (use of technology)• Value adding• Lowering fixed costs (economies of scale)

World agriculture is poised to enter a new growth phase that will be much greater than colonization and industrialization.

• During the period of industrialization after the second world war, agricultural production expanded exponentially, compared to the growth in population (due to the development of fertilizer and production machinery).

• Production of coarse grains, beef and mutton however peak during mid eighties as these commodities were mainly dependent on the availability of natural resources. Commodities like poultry and pork continued to grow as they were able to utilize surplus coarse grains.

• Production has however once again since the mid nineties started to increase due to advances in geo-technology (GMOS etc.)

The net effect of the above is that production volumes will continue to increase thus improving the survival potential of agriculture in general

Agricultural Cost Curve

-2

0

2

4

6

8

10

12

14

1980 1985 1990 1995 2000 2005

Producer price index Farming requisites

Maize yield

-

1.00

2.00

3.00

4.00

5.00

6.00

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

(to

n/h

a)

World yields SA yields

Maize yield

-

1.00

2.00

3.00

4.00

5.00

6.00

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

(to

n/h

a)

World yields SA yields

Absa AgriBusiness

Agricultural economic indicators

Farm income and expenditure trends (R million)

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

69/70 73/74 77/78 81/82 85/86 89/90 93/94 97/98 01/02 05/06 09/10

Yearly Farm Debt commitment Expenditure on inputsGross producer income Net Farm incomeValue of Fixed Assets 50% margin

Absa AgriBusiness

Economic market principals with in agriculture

World agriculture commodity prices to increase substantial over the medium term.

There are two main driving forces at work that will have a positive impact on agricultural commodity prices namely:

• Global WarmingSentiment around global warming is driving legislature around the world to continuously push for the implementation of so-called carbon friendly legislation. As agriculture is the prime beneficiary this type of legislation (due to the ability of plants to extract carbon from the air) new markets will place upward pressure on agricultural commodity prices. Agriculture could however never produce enough energy to replace all fossil fuels.

Crude oil price and production trends

50,000.0

55,000.0

60,000.0

65,000.0

70,000.0

75,000.0

80,000.0

85,000.0

1975 1980 1985 1990 1995 2000 2005 2010

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

AVG Barrel / Day Price ($/B)

Hong Kong repatriated to China

Iran / Iraq

• Demand for Food and Energy

During the late nineties Capitalism replaced Communism as economic system in the world (signs of the time where the collapse of the Berlin wall in ’98 the repatriation of Hong Kong in to China in ‘99)

This led to an exponential economic growth in Eastern European, Middle East and Asian countries with a resulting increase in the buying power of these consumers, hence the growth in demand for food and energy

Absa AgriBusiness

Grain industry outllok

Absa AgriBusiness

Absa AgriBusiness

Agricultural outlook - Content

• General market trends

• Field crops– Maize, Wheat, Sunflower, Soya

• Fibre – Cotton, Wool, Mohair

• Livestock– Poultry, Pork, Beef, Mutton, Dairy Ostrich

• Vegetables– Tomato, Potato, Cabbage, Carrots

Absa AgriBusiness

World maize trends

World maize price and stock trends International maize price trends (US$/ton)

0

200000

400000

600000

800000

1000000

1988 1991 1994 1997 2000 2003 2006 2009

0

50

100

150

200

250

300

350

Consumption Production

Stocks Price

(US $/t)('000 ton)

60

110

160

210

260

310

360

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

White Yellow

FAO, USDA - Economic Research Services, USDA - Agricultural Marketing Services

Absa AgriBusiness

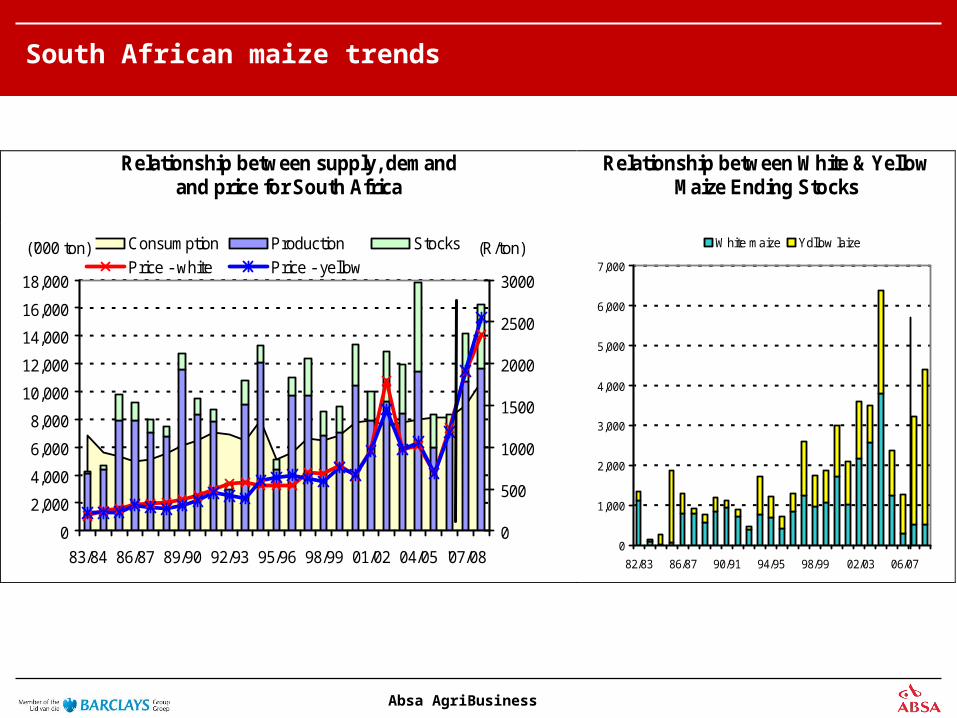

South African maize trends

Relationship between supply, demand and price for South Africa

Relationship between White & Yellow Maize Ending Stocks

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

83/84 86/87 89/90 92/93 95/96 98/99 01/02 04/05 '07/08

0

500

1000

1500

2000

2500

3000

Consumption Production Stocks

Price - white Price - yellow(R/ton)('000 ton)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

82/83 86/87 90/91 94/95 98/99 02/03 06/07

White maize Ydllow laize

Absa AgriBusiness

SA Yellow maize price trends

SA Yellow maize prices (R/ton) Ending stocks for Yellow maize ('000 ton)

350

850

1,350

1,850

2,350

2,850

3,350

3,850

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Import parity Export parity Yellow YM1

0

500

1000

1500

2000

2500

3000

3500

4000

89/90 92/93 95/96 98/99 01/02 04/05 07/08

Source: CBOT, SAGIS, SAFEX, BTT, Own calculations

Absa AgriBusiness

SA White maize price trends

SA White maize prices (R/ton) Ending stocks for white maize ('000 ton)

200

700

1,200

1,700

2,200

2,700

3,200

3,700

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Import Parity Export Parity Domestic

0

500

1000

1500

2000

2500

3000

3500

90/91 93/94 96/97 99/00 02/03 05/06 08/09

Source: SAGIS, SAFX, Own calculations

Absa AgriBusiness

World sunflower price trends

World sunflower supply, consumption and price trends International Sunflower price trends (US$/ton)

0

5000

10000

15000

20000

25000

30000

35000

1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

0

100

200

300

400

500

600

700

Consumption ProductionStocks Price

(US $/t)('000 ton)

240

340

440

540

640

740

840

940

1040

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Source: FAO, USDA Economic Research Services

Absa AgriBusiness

South African sunflower price trends

Relationship between sunflower supply, demand And price for South Africa

Sunflower Seed Prices (R/ton SAFEX)

0

200

400

600

800

1000

1200

1400

79/80 83/84 87/88 91/92 95/96 00/01 '04/05 '08/09

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000Consumption ProductionStocks Price

(R/ton)('000 ton)

Safex

1,150.00

1,650.00

2,150.00

2,650.00

3,150.00

3,650.00

4,150.00

4,650.00

5,150.00

Source: SAGIS, SA Weather Bureau, SAFEX, Own calculations

Absa AgriBusiness

South African sunflower price trends

SA sunflower prices (R/ton) SA sunflower ending stocks ('000 ton)

900

1900

2900

3900

4900

5900

6900

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Sun Import parity Sun domestic

0

50

100

150

200

250

300

350

400

450

500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Source: USDA Agricultural Market Services, SAGIS, Own calculations

Absa AgriBusiness

Soyabean world trends

World soybean supply, consumption and price trends International soybean price trends (US$/ton)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1985 1988 1991 1994 1997 2000 2003 2006 2009

0

50

100

150

200

250

300

350

400

450Consumption Production

Stocks Price(US $/t)('000 ton)

100

200

300

400

500

600

700

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

10

20

30

40

50

60

70Sojabeans Cakemeel

Oil Oil US c/lb)US $/ton)

Source: FAO, USDA Economic Research Services

Absa AgriBusiness

SA Soyabean trends

Relationship between soybean supply, demand And price for South Africa

Soybean Future Prices (R/ton)

0

100

200

300

400

500

600

700

1982 1987 1992 1997 2002 2007

0

500

1000

1500

2000

2500

3000

3500

4000

4500Consumption ProductionImports StocksPrice

(R/ton)('000 ton)

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Derived importparity SAFEX

Absa AgriBusiness

World wheat trends

World wheat price and stock trends International wheat price trends (US$/ton)

0

200,000

400,000

600,000

800,000

1,000,000

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

0

50

100

150

200

250

300

Consumption Production

Stocks Price

(US $/t)('000 ton)

120

160

200

240

280

320

360

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Soft red Hard red

FAO, USDA - Economic Research Services, USDA - Agricultural Marketing Services

Absa AgriBusiness

SA wheat trends

Relationship between supply, demand and price for South Africa

SAFEX Futures Price Trends

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

200

700

1200

1700

2200

2700

3200

3700Consumption Production ImportsStocks Price

(R/ton)('000 ton)

1200

1700

2200

2700

3200

3700

4200

4700

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

SAFEX

Source: SAGIS, SA Weather Bureau

Absa AgriBusiness

SA Wheat price trends

SA Wheat prices (R/ton) Ending stocks for wheat ('000 ton)

400

900

1,400

1,900

2,400

2,900

3,400

3,900

4,400

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

Import parity Export parity Domestic

0

200

400

600

800

1000

1200

1990 1994 1998 2002 2006

Source: CBOT, SAGIS, SAFX, BTT, Own calculations

Absa AgriBusiness

Agricultural outlook - Content

• General market trends

• Field crops– Maize, Wheat, Sunflower, Soya

• Fibre – Cotton, Wool, Mohair

• Livestock– Poultry, Pork, Beef, Mutton, Dairy Ostrich

• Vegetables– Tomato, Potato, Cabbage, Carrots

Absa AgriBusiness

World fibre production trends

World Fibre Production Trends ('000 ton) Cotton / Synthetic Fibre Price Ratio

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

1980 1984 1988 1992 1996 2000 2004 2008

Cotton Wool Rayon Polyester Silk Flax Hemp

0.45

0.55

0.65

0.75

0.85

0.95

1.05

1.15

1.25

1.35

1982 1986 1990 1994 1998 2002 2006

Cotton/Raylon Cotton/Polyester

Figure 1. World Fibre Production and Cotton/Synthetic Fibre Price Ratio Source: USDA Economic Research Service & FAO.

Absa AgriBusiness

World cotton trends

Relation Between World Cotton Ending Stocks and Price

World Cotton Ending Stocks Trends ('000 ton)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

0

10

20

30

40

50

60

70

80

90

100

Ending stock US Mill price(FOB) US Farm price

('000 ton) (US c/lb)

0

2,000

4,000

6,000

8,000

10,000

12,000

1992 1995 1998 2001 2004 2007

China India USA Brazil

Pakistan Australia Argentina Uzbekista

Turkey RSA Other

Figure 4. Relation Between World Cotton Ending Stock and Price and World Ending Stock Trends: Source: USDA Economic Research Services, FAO, ABARE.

Absa AgriBusiness

SA cotton price trends

South African Cotton Production and Price Trends SA Cotton Ending Stocks ('000 ton)

0

10

20

30

40

50

60

70

80

90

100

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 20090

2000

4000

6000

8000

10000

12000

14000

16000

SA Production ImportsProducer price Derived lint price

('000 ton) (R/ton)

0

5

10

15

20

25

1991 1993 1995 1997 1999 2001 2003 2005 2007

Figure 5. South African Production Trends and Cotton Ending Stocks. Source: National Department of Agriculture, Cotton SA, Own calculations.

Absa AgriBusiness

Australian clean wool prices World clean wool stocks (‘000 ton)

0

10

20

30

40

50

60

70

19701973197619791982198519881991199419972000200320062009

South Africa Australia AUS $/kg Australia R/kg

900,000

1,300,000

1,700,000

2,100,000

2,500,000

2,900,000

1990 1994 1998 2002 2006

Production Stocks

Consumption

Source: Economic Research Services, US Department of Agriculture

Absa AgriBusiness

SA Wool price trends

Expected clean wool equivalent production and price trends for South African (SA c/kg)

0

20,000

40,000

60,000

80,000

100,000

120,000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 20080

10

20

30

40

50

60

70Production (ton) Price (R/kg)

1,700.00

2,700.00

3,700.00

4,700.00

5,700.00

6,700.00

7,700.00

Nov-02 Nov-04 Nov-06 Nov-08 Nov-10

Australian South Africa

Source: National department of Agriculture, Cape wools, Wesfarmers Landmark, AWEX, Own calculations

Absa AgriBusiness

World mohair production trends

World mohair production trends ('000 ton)

South African Goat herd (millions)

0

5

10

15

20

25

30

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

S A USA Turkey ArgentinaLesotho Australia New Zealand

0

0.5

1

1.5

2

2.5

3

1990 1995 2000 2005

Angora All goats

Sources Mohair South Africa, Cape Mohair and Wool, Owen calculations.

Absa AgriBusiness

Mohair price trends

Domestic and world mohair price trends Contribution to price

0

20

40

60

80

100

120

140

160

180

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

S A (R/kg) Kid (R/kg) USA (US c/kg)

Kids37%

Strong Adults13%

Fine Adults22%

Lox13%

Young Goats15%

2008 production season Sources Mohair South Africa, USDA Economic Research Services, Owen calculations.

Absa AgriBusiness

Agricultural outlook - Content

• General market trends

• Field crops– Maize, Wheat, Sunflower, Soya

• Fibre – Cotton, Wool, Mohair

• Livestock– Poultry, Pork, Beef, Mutton, Dairy Ostrich

• Vegetables– Tomato, Potato, Cabbage, Carrots

Absa AgriBusiness

Poultry production trends

Domestic production trends for poultry (ton) Poultry imports and exports

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

Production Imports

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

1982 1986 1990 1994 1998 2002 2006

Imports Exports

Source: USDA Agricultural market service (AMS), SAMIC, Abstracts of Agricultural Statistics, Own calculations

Absa AgriBusiness

Poultry Price trends

Domestic broiler price trends (c/kg) Relation between poultry and maize prices

300

500

700

900

1100

1300

1500

1700

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Whole IFQ Import parity

4

6

8

10

12

14

16

18

20

22

Apr-00 Apr-02 Apr-04 Apr-06 Apr-08 Apr-10

200

400

600

800

1000

1200

1400

1600

Poulrty / maize ratio Frozen whole birdBreakeven Ratio (c/kg)

Source: USDA Agricultural market service (AMS), SAMIC, Abstracts of Agricultural Statistics, SAFEX, Own calculations

Absa AgriBusiness

Pork price tends

Relationship between pork consumer prices and producer prices (c/kg)

Pork to maize price ratios

400

600

800

1000

1200

1400

1600

1800

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Contract porker Contract Baconer

3

5

7

9

11

13

15

17

19

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09

0

200

400

600

800

1000

1200

1400

1600

1800

Pork/maize ratioBreak-evenBaconer price

Ratio Price(c/kg)

Sources: SAGIS, SAVPO, SAMIC, Own Calculations

Absa AgriBusiness

SA Beef Herd Numbers

South African beef herd trends

0

100

200

300

400

500

600

700

800

900

1000

1966 1971 1976 1981 1986 1991 1996 2001 2006

Rai

n(m

m)

6

7

8

9

10

11

12

13

14

15

Her

d (m

illio

ns)

Rain 3 yr Avg Beef herd

1

3

5

7

9

11

13

15

1966 1976 1986 1996 2006

Her

d (m

illio

ns)

54%

56%

58%

60%

62%

64%

66%

68%

70%

72%

Percentage fem

ales

Beef herd Percentage females

Source: Department of Agriculture, Weather Bureau, Own calculations

Absa AgriBusiness

SA Beef prices

South African Beef Price trends and the relation between Maize and Weaner Calf Prices

500

1000

1500

2000

2500

3000

3500

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Class A Class B Class CContract A2/A3 Consumer

0

250

500

750

1000

1250

1500

1750

2000

2250

2500

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

8

10

12

14

16

18

20

22

24

26

28

Beef / Maize Contract A2Weaner calf B/E Contract

(c/kg) (Ratio)

Source: SAMIC, Stock Owners, Noord Kaap Lewendehawe, selected feedlots, Own calculations

Absa AgriBusiness

Mutton Price trends

Domestic mutton prices (c/kg) Relation between mutton and maize prices

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

J an-00

J an-01

J an-02

J an-03

J an-04

J an-05

J an-06

J an-07

J an-08

J an-09

J an-10

SA C lass A SA C lass CContract C lass A Consumer

200

700

1,200

1,700

2,200

2,700

3,200

3,700

4,200

Apr-00

Apr-01

Apr-02

Apr-03

Apr-04

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

0

10

20

30

40

50

60

Meat / maize ratio Contract LambFeeder lamb Class A * 0.5Breakeven ratio

Price (c/kg) Price ratio

Source: SAMIC, SAFEX, and own calculations.

Absa AgriBusiness

SA Producer milk price trends

Producer milk price trends (c/l) Milk to maize price ratio

60

110

160

210

260

310

360

410

Jul-95 Jul-97 Jul-99 Jul-01 Jul-03 Jul-05 Jul-07 Jul-09

0

0.5

1

1.5

2

2.5

3

3.5

Jan-00 Jan-03 Jan-06 Jan-09

0

50

100

150

200

250

300

350

400

RatioBreakeven

Producer milk price

Ratio c/l

Sources: Milk producers Association (MPO), SAFEX and Own calculations

Absa AgriBusiness

Estimated ostrich slaughtering in South Africa South African ostrich production and usage trends (ton)

050,000

100,000150,000200,000

250,000300,000

350,000400,000

1987 1991 1995 1999 2003 2007

0

2

4

6

8

10

12

14

Slaughtering Slaughtering per breeding bird

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

1985 1989 1993 1997 2001 2005 2009

Domestic consumption Exports

Absa AgriBusiness

Gross producer income trends for South Africa (R/bird) Ostrich Price trends

0

100000000

200000000

300000000

400000000

500000000

600000000

700000000

1985 1990 1995 2000 2005 2010

Meat Skin Feather

0

20

40

60

80

100

120

140

160

180

200

1985 1990 1995 2000 2005 20100

200

400

600

800

1000

1200

1400

Meat (R/kg) Feather (R/kg)

Skin (R/skin)

Source: NOKSA, KKK, Camdebo, Agrimark trends, Own calculations

Absa AgriBusiness

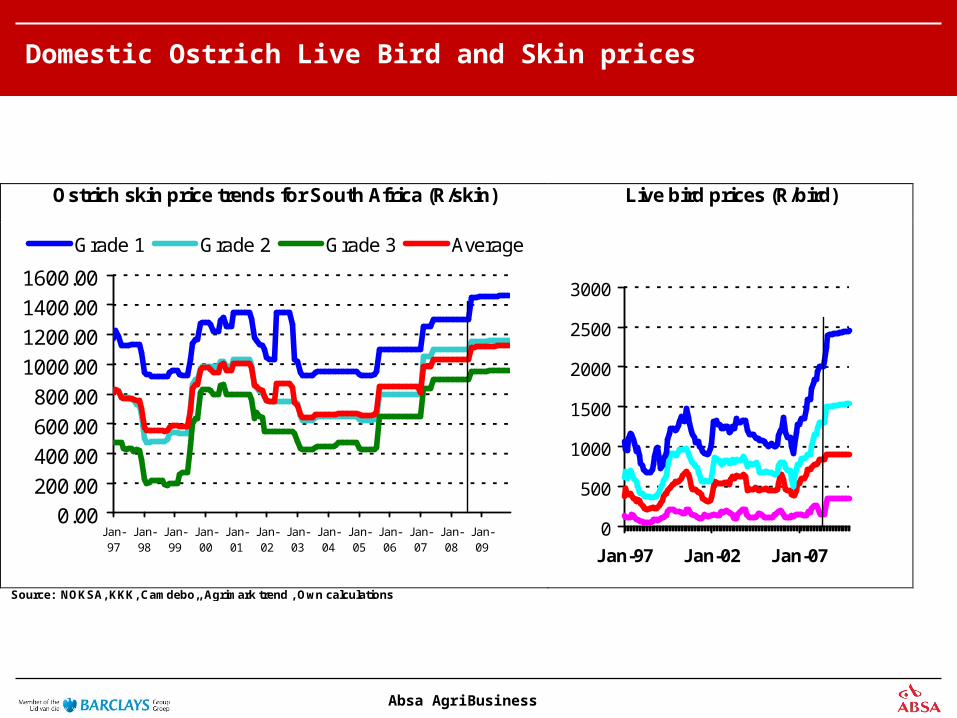

Domestic Ostrich Live Bird and Skin prices

Ostrich skin price trends for South Africa (R/skin) Live bird prices (R/bird)

0.00200.00

400.00

600.00

800.00

1000.00

1200.001400.00

1600.00

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Grade 1 Grade 2 Grade 3 Average

0

500

1000

1500

2000

2500

3000

Jan-97 Jan-02 Jan-07

Source: NOKSA, KKK, Camdebo,, Agrimark trend , Own calculations

Absa AgriBusiness

Agricultural outlook - Content

• General market trends

• Field crops– Maize, Wheat, Sunflower, Soya

• Fibre – Cotton, Wool, Mohair

• Livestock– Poultry, Pork, Beef, Mutton, Dairy Ostrich

• Vegetables– Tomato, Potato, Cabbage, Carrots

Absa AgriBusiness

Cabbage market trends

Real adjusted Cabbage market trends (Price = R/ton, Volume = ton)

-

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

7,000.00

8,000.00

9,000.00

10,000.00

3 yr AVG Vol 2008 Vol 3 yr AVG Price 2008 Price

Absa AgriBusiness

Carrot market trends

Real adjusted Carrots market trends (Price = R/ton, Volume = ton)

-

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

7,000.00

8,000.00

9,000.00

10,000.00

3 yr AVG Vol 2008 Vol 3 yr AVG Price 2008 Price

Absa AgriBusiness

Onion market trends

Real adjusted Onions market trends (Price = R/ton, Volume = ton)

-

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

Series2 Series4 Series1 Series3

Absa AgriBusiness

Real adjusted Potatoes market trends (Price = R/ton, Volume = ton)

-

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08

-

10,000.00

20,000.00

30,000.00

40,000.00

50,000.00

60,000.00

70,000.00

80,000.00

Series2 Series4 Series1 Series3

Absa AgriBusiness

Summery – every thing is market driven

Absa AgriBusiness

Thank you for the opportunity to share some ideas

Contact details

E JanovskyTel (011) 350 6102

Email [email protected]

Disclaimer: Although everything has been done to ensure the accuracy of the information, the Bank takes no responsibility for actions or losses that might occur due to the usage of this information.