ABSA 203: Intermediate Financial Accounting I

30

ABSA 203: Intermediate Financial Accounting I Tutorial Exercises Christos Minas PhD (Cand.), FAIA, MSc, BA

Transcript of ABSA 203: Intermediate Financial Accounting I

ABSA 203: Intermediate Financial Accounting I

Tutorial Exercises

Christos Minas PhD (Cand.), FAIA, MSc, BA

2

SUBJECT OUTLINE

Objectives of the subject The aim of the subject is to build on the knowledge gained in the previous introductory accounting courses. The major thrust of Intermediate Accounting I is the application of financial accounting principles in a corporate setting.

Content (Major units) 1. Issue of Shares and Debentures, Redemptions, Bonus issues, Forfeiture,

Reserves. 2. Reconstructions and reorganizations. 3. Income statement for publication and internal use. 4. Balance sheet for publication and internal use. 5. Stockholders equity and present value 6. Stockholders interest and Capital employed 7. Consolidated accounts. 8. Long-term assets and liabilities such as acquisition, disposal and depreciation of

fixed assets as well as amortization of intangible assets. 9. Reference is made on related SSAP's and the company’s acts

Bibliography Wood, F. Business Accounting Volume I and II, 11th Edition, Pitman Publishing 2009. J D Spiceland,J Sepe,L A Tomassini, Intermediate Accounting, 3/e, McGraw-Hill, 2004 Other texts may be used to supplement as an alternative to the above book. Additional titles of texts and specific readings will be given during lectures.

Assessment 1. Two test required, 40% of the final grade the first in the 4th week and the second in 8th week. 2. Final examination, 60% (end of semester).

3

Class Activity 1

Barry Limited issued 1 million Ordinary shares with a nominal value of £0.50 each. The market price was £0.85 per share. A total of 30 cents per share was paid on the application, 20 cents per share on the allotment, 20 cents per share for the first call and 15 cents per share for final calls. Applications were received for 1.3 million shares. The applications rejected were carried forward to the allotment account. One shareholder who applied for 15,000 shares failed to make the final call and another shareholder (with 20,000 shares) at the time of the first call paid both the first call and final call.

You are required to:

(a) Make the relevant journal entries.

(b) Make the relevant ledger entries.

Class Activity 2

Kyriakos Limited issued 3 million Ordinary shares with a nominal value of €1 each. The market price was €6.00 per share. A total of 50 cents per share was paid on the application, 350 cents per share on the allotment and 200 cents per share for first and final call. Applications were received for 5 million shares and any excess applications were refunded.

All funds for the issue were received in full except for those due on the first and final call in respect for 500,000 shares.

You are required to make the relevant ledger entries for the above.

Class Activity 3

AEK plc invited Subscriptions for an issue of 1,000,000 ordinary shares of £1 each at a premium of £0.10 per share payable:

£0.2 on Application 1 January 2006

£0.6 on Allotment (including the premium) 31 January 2006

£0.3 on First & Final Call 30 April 2006

Applications were received for 1,400,000 shares and the Directors disposed of the matter as follows:

To Applications for 800,000 Allotment in Full

To Applications for 400,000 One share for every two applied

To Applications for 200,000 None (Refund application money)

All cash was received on due dates except for the Call money on 50,000 shares which were forfeited on 1 May. On 15 May the shares were re-issued to Mr. Renos Kinigos as fully paid for £0.80 per share.

Required

(a) Make the necessary ledger entries, balancing the accounts at 31 May 2006.

4

(b) What is the minimum price that the above forfeited shares can be re-issued?

Class Activity 4

Explain the difference between a “bonus issue” and a “rights issue” and contrast

their accounting treatment.

Class Activity 5

Luke Moore Limited issued 2 million Ordinary shares with a nominal value of £0.50 each. The market price was £0.90 per share. A total of 35 cents per share was paid on the application, 25 cents per share on the allotment, 20 cents per share for the first call and 10 cents per share for final calls. Applications were received for 2.5 million shares. Excess application money were refunded.

You are required to make the relevant ledger entries.

5

Class Activity 6

The following trial balance was extracted from the books of Jubiler PLC on 31 December 2008:

Debit Credit

£ £

Ordinary Share Capital £0.50 each 75,000

8% Preference Share Capital £1 each 20,000

6% Debentures 20,000

Directors Remuneration 18,000

Audit fees 4,000

Goodwill 15,000

Carriage Inwards 1,300

Stock at 1 January 2008 30,000

Sales 250,500

Purchases 100,500

Debtors 11,600

Cash at Bank 25,500

Land 93,000

Buildings 70,000

Fixtures and Fittings 15,000

Trade Creditors 19,500

Interim ordinary dividend 3,750

Salaries and Wages 19,700

Rent and Rates 17,500

General Reserve 5.000

Retained Earnings at 1 January 2008 22,850

Provision for depreciation on Building 5,000

Provision for depreciation on Fixtures and Fittings 7,000

424,850 424,850

You are also given the following information at 31 December 2008:

• The stock at 31 December 2008 amounted to £35,000.

• Provide for £8,000 Corporation Tax for the year.

• Provide for the preference dividend for the year.

• Provide the final dividend £0.05 cent per ordinary share.

• The total interest due on Debentures is due.

• The Goodwill has been impaired by £9,000.

• The Salaries and Wages are accrued by £2000 and Director Remuneration is accrued by £3,000.

• Rent and Rates are prepaid by £900.

• Buildings are to be depreciated at 2% on cost and Fixtures and Fittings by 15% on the book value.

Prepare a Profit and Loss Account (Income Statement) for the year ended 31

December 2008 and a Balance Sheet at 31 December 2008.

6

Class Activity 7

The following trial balance was extracted from the books of Tommy PLC on 31 December 2007 after the preparation of the Trading Account:

Debit Credit

£ £

Ordinary Share Capital 70,000

8% Preference Share Capital 25,000

6% Debentures 20,000

Directors Remuneration 8,300

Audit fees 4,700

Goodwill 10,000

Gross Profit 58,400

Stock 30,300

Debtors 6,300

Cash at Bank 32,000

Land 36,000

Buildings 46,000

Fixtures and Fittings 4,000

Trade Creditors 15,800

Interim ordinary dividend 3,500

Salaries and Wages 16,200

Rent and Rates 3,100

General Expenses

Retained Earnings at 1 January 2005 11,200

200400 200,400

You are also given the following information at 31 December 2007:

• Provide for £4,300 Corporation Tax for the year.

• Provide £2,000 for the preference dividend for the year.

• The total interest due on Debentures of £1,200 is due.

• The Goodwill has been impaired by £4,300.

• A provision for bad debts of 1% of debtors is to be provided.

• The Salaries and Wages are accrued by £1900.

• Rates are prepaid by £420.

• Buildings are to be depreciated at 2% on the book value and Fixtures and Fittings by 15% on the book value.

You are required to:

a) Prepare a Profit and Loss Account for the year ended 31 December 2005.

b) Prepare a Balance Sheet as at 31 December 2005.

7

Class Activity 8

The Trial Balance of Finikoudes Plc at 31 December 2006 appeared as follows:

£ £

8% Preference share capital of £1 each, fully paid 40.000

Ordinary shares of £2 each, fully paid 100.000

Purchases 540.000

Retained profit 60.000

Freehold land at cost 270.000

Fixtures, at cost 40.000

Depreciation on fixtures 18.000

Directors Remuneration 15.000

Motor vehicles, cost 56.000

Depreciation on vehicles 28.000

Insurance 4.000

Stock at 1 January 2006 70.000

Debtors 64.000

Trade creditors 48.000

Sales 840.000

Bank 30.200

10% Debentures (redeemable 2007) 80.000

Debenture interest 5.000

Wages and salaries 68.000

Heat and light 8.400

Audit fees 12.800

Debenture discount 2.400

Motor expenses 4.000

Provision for bad debts 2.000

Bad debts 1.200

General Reserve 15.000

Goodwill 40.000

---------- ----------

1.231.000 1.231.000

====== ======

8

Notes:

1. Stock at 31 December 2006 was £90000

2. Depreciation for 2006 has yet to be provided on the following bases:

Fixtures 15% straight line method

Motor vehicles 20% Reducing balance method

3. Write off additional bad debts of £4.000 and adjust the provision for bad debts equal to 5% on the remaining debtors.

4. Insurance of £400 had been prepaid at the year end, and wages of £2.000 were accrued

5. The directors propose the final dividend on preference shares and 12% dividend on the ordinary shares.

6. Taxation of £9.500 is to be provided.

7. Transfer £9.000 to General Reserve and write off half the Goodwill.

REQUIRED

Prepare for Finikoudes Plc:

(a) A Trading, Profit & Loss Account for the year ended 31 December 2006.

(b) A Balance Sheet as at 31 December 2006.

(c) Who decides whether a dividend must be proposed and the amount of the dividend to be proposed.

9

Class Activity 9

The following is an extract from the trial balance of Angel Limited a limited liability company at 30 June 2005:

$000

Plant and Equipment - cost 60000

Equipment – accumulated depreciation at 1 July 2004

12000

Stock at 1 July 2004 9200

Dividend Receivable 14000

Motor Vehicles - cost 25000

Motor Vehicles– accumulated depreciation at 1 July 2004

10000

Sales Revenue 65000

Purchases 25500

Distribution costs 8000

Administrative expenses 10000

Factory closure costs 6000

Provision for bad debts at 1 July 2004 1250

Bad debts written off 900

8% Debentures 20000

Interest paid on loan notes 800

Retained profit at 1 July 2004 33000

Suspense account 330

Debtors 25000

Notes: 1. The closing stock at 30 June 2005 was $12,800,000. 2. Bad debts written off and the movement on the provision for bad debts are to be

included in distribution costs. The provision for bad debts at 30 June 2005 amounted to 6% of Debtors,

3. The balance on the suspense account is the proceeds on the sales of motor vehicles, entered to the suspense account pending the correct treatment in the records. The motor vehicles had originally cost $500,000 and had a written down value at 1 July 2004 of $400,000. It is the company’s policy to provide a full year’s depreciation in the year of purchases and none in the year of sale.

4. Depreciation is to be provided for on the basis of cost as follows:

• Equipment – 10% on cost

• Motor Vehicles – 20% on cost 5. Prepayments and accruals were:

Accruals Prepayments

$000 $000

Administrative expenses 50 70

Distribution costs 160 130

6. The estimated income tax expense for the year is $2,000,000. There was an

overprovision of corporation tax of $10,000 for the year ended 30 June 2004.

10

You are required to: Prepare Angel Limited’s Profit and Loss Account (Income Statement) for the

year ended 30 June 2005.

Class Activity 10

The following trial balance was extracted from the books of Thelma Tsoura PLC on 31 December 2008:

Debit Credit

£ £

Ordinary Share Capital 75,000

8% Preference Share Capital 20,000

6% Debentures 20,000

Directors Remuneration 18,000

Audit fees 4,000

Goodwill 15,000

Carriage Inwards 1,300

Stock at 1 January 2008 30,000

Sales 155,500

Purchases 100,500

Debtors 11,600

Cash at Bank 25,500

Land 33,000

Buildings 30,000

Fixtures and Fittings 15,000

Trade Creditors 31,500

Interim ordinary dividend 3,750

Salaries and Wages 19,700

Rent and Rates 12,300

General Expenses 5,200

Retained Earnings at 1 January 2008 22,850

324,850 324,850

You are also given the following information at 31 December 2008:

• The stock at 31 December 2006 amounted to £35,000.

• Provide for £8,000 Corporation Tax for the year.

• Provide for the preference dividend for the year.

• The total interest due on Debentures is due.

• The Goodwill has been impaired by £9,000.

• The Salaries and Wages are accrued by £1600 and Director Remuneration is accrued by £3,000.

• Rent and Rates are prepaid by £900.

• Buildings are to be depreciated at 5% on the book value and Fixtures and Fittings by 15% on cost.

You are required to prepare a Profit and Loss Account (Income Statement) for

the year ended 31 December 2008 and a Balance Sheet as at 31 December 2008.

11

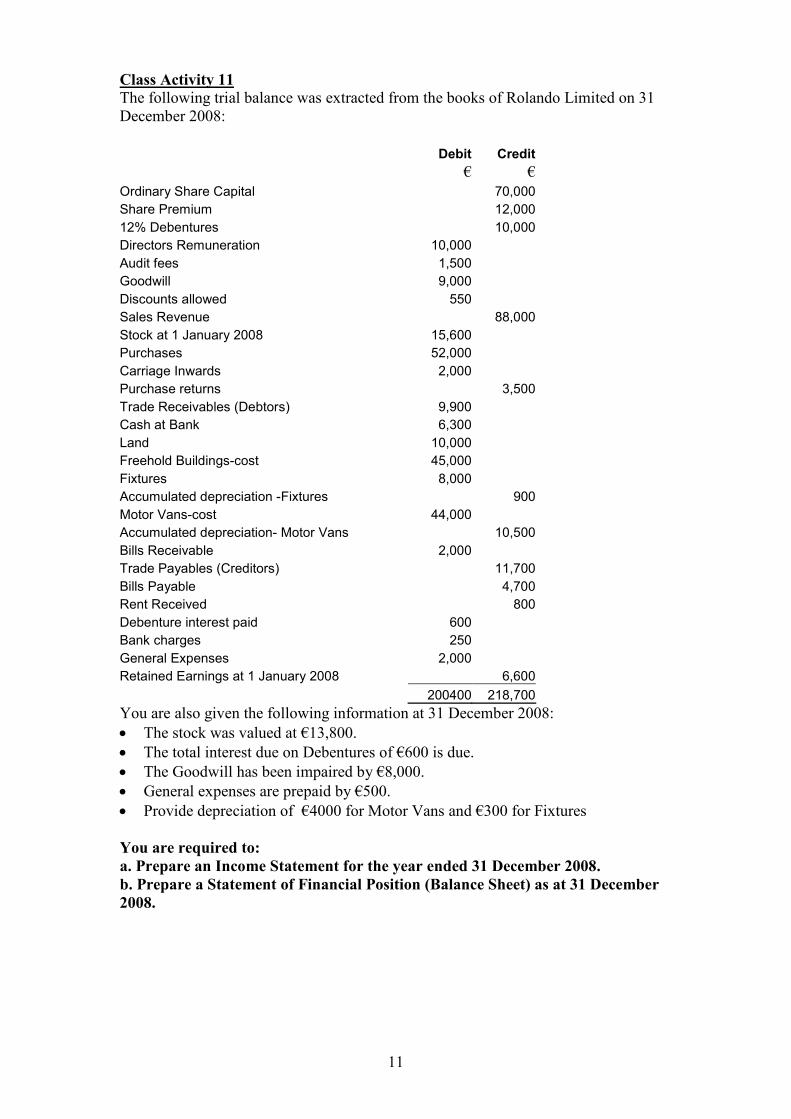

Class Activity 11

The following trial balance was extracted from the books of Rolando Limited on 31 December 2008:

Debit Credit

€ €

Ordinary Share Capital 70,000

Share Premium 12,000

12% Debentures 10,000

Directors Remuneration 10,000

Audit fees 1,500

Goodwill 9,000

Discounts allowed 550

Sales Revenue 88,000

Stock at 1 January 2008 15,600

Purchases 52,000

Carriage Inwards 2,000

Purchase returns 3,500

Trade Receivables (Debtors) 9,900

Cash at Bank 6,300

Land 10,000

Freehold Buildings-cost 45,000

Fixtures 8,000

Accumulated depreciation -Fixtures 900

Motor Vans-cost 44,000

Accumulated depreciation- Motor Vans 10,500

Bills Receivable 2,000

Trade Payables (Creditors) 11,700

Bills Payable 4,700

Rent Received 800

Debenture interest paid 600

Bank charges 250

General Expenses 2,000

Retained Earnings at 1 January 2008 6,600

200400 218,700

You are also given the following information at 31 December 2008:

• The stock was valued at €13,800.

• The total interest due on Debentures of €600 is due.

• The Goodwill has been impaired by €8,000.

• General expenses are prepaid by €500.

• Provide depreciation of €4000 for Motor Vans and €300 for Fixtures

You are required to:

a. Prepare an Income Statement for the year ended 31 December 2008.

b. Prepare a Statement of Financial Position (Balance Sheet) as at 31 December

2008.

12

Class Activity 12

The following trial balance was extracted from the ledger accounts of Angel plc at 30 September, 2007:

Debit Credit

£ £ Share capital (£1 ordinary shares fully paid) 400,000 Share premium 100,000 Debentures – interest 12% p.a. issued 2004 200,000 Fixed Assets at cost

Freehold premises 935,000 Machinery and equipment 160,000 Motor vehicles 125,000

Provision for depreciation at 1 October, 2006 Freehold premises 130,000 Machinery and equipment 40,000 Motor vehicles 62,500

Sales & Purchases 458,200 1,791,600 Discounts Allowed/Received 14,200 9,800 Opening Stock 113,400 Debtors and Creditors 154,100 231,400 Provision for doubtful debts at 1 October, 2006 5,700 Bad debts 6,900 Wages and salaries 238,400 Administrative expenses 332,800 Auditors fees 39,600 Debenture interest 12,000 Directors Remuneration 40,000 Retained profits at 1 October, 2006 115,200 Goodwill at cost 230,000 Bank balance 226,600

3,086,200 3,086,200

Additional information relevant to the year ended 30 September, 2007 is as follows:

1. Stock held at 30 September, 2004 is £121,300.

2. Provision for doubtful debts to be increased to £9,500.

3. Machinery and equipment and motor vehicles are to be depreciated at 25%

per annum on cost. A further £10,000 is to be written off the freehold premises.

4. Corporation tax on the profits of the year is to be provided for at £235,000.

5. The cost of goodwill is to be amortised over 20 years.

6. A dividend is proposed at the rate of 10p per share.

7. Wages and administrative expenses accruals amount to £1,500 and £900

respectively.

13

8. The debenture interest in the trial balance is the amount paid during the year. The terms of the debenture state that interest is to be paid half-yearly in arrears.

Required

(a)Prepare for Angel plc a Trading, Profit and Loss Account for the year ended 30 September, 2007 together with a Balance Sheet as at that date.

(b) Prepare the accounts for proposed dividend and corporation tax.

14

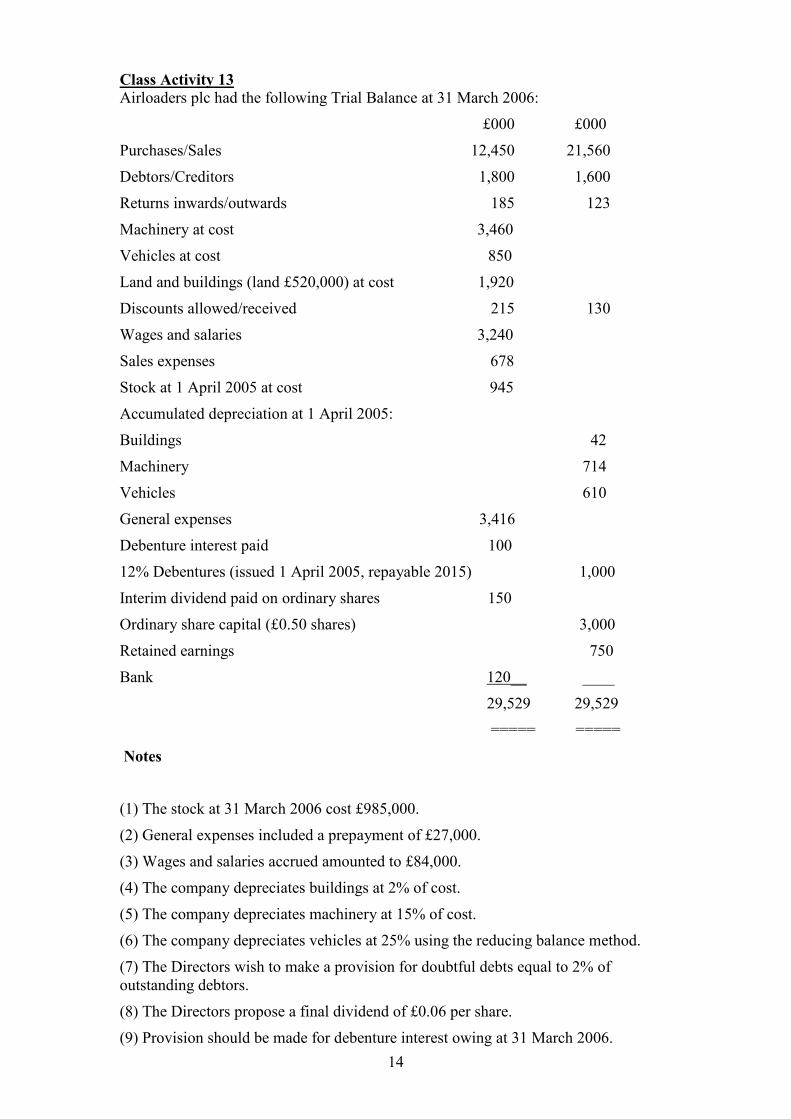

Class Activity 13

Airloaders plc had the following Trial Balance at 31 March 2006:

£000 £000

Purchases/Sales 12,450 21,560

Debtors/Creditors 1,800 1,600

Returns inwards/outwards 185 123

Machinery at cost 3,460

Vehicles at cost 850

Land and buildings (land £520,000) at cost 1,920

Discounts allowed/received 215 130

Wages and salaries 3,240

Sales expenses 678

Stock at 1 April 2005 at cost 945

Accumulated depreciation at 1 April 2005:

Buildings 42

Machinery 714

Vehicles 610

General expenses 3,416

Debenture interest paid 100

12% Debentures (issued 1 April 2005, repayable 2015) 1,000

Interim dividend paid on ordinary shares 150

Ordinary share capital (£0.50 shares) 3,000

Retained earnings 750

Bank 120__ ____

29,529 29,529

===== =====

Notes

(1) The stock at 31 March 2006 cost £985,000.

(2) General expenses included a prepayment of £27,000.

(3) Wages and salaries accrued amounted to £84,000.

(4) The company depreciates buildings at 2% of cost.

(5) The company depreciates machinery at 15% of cost.

(6) The company depreciates vehicles at 25% using the reducing balance method.

(7) The Directors wish to make a provision for doubtful debts equal to 2% of outstanding debtors.

(8) The Directors propose a final dividend of £0.06 per share.

(9) Provision should be made for debenture interest owing at 31 March 2006.

15

(10) Provision for Corporation tax £15,000 should be made.

REQUIRED

Prepare for Airloaders plc:

(a) A Trading, Profit & Loss Account for the year ended 31 March 2006.

(b) A Balance Sheet as at 31 March 2006.

Class Activity 14

The following is the Balance Sheet of Evdokia PLC at 31 December 2007:

Non-current (Fixed) Assets 235,000

Current Assets (except cash) 193,000

Cash and bank 82,000

TOTAL ASSETS 510,000

Ordinary share capital of £1 each 200,000

8% Preference Shares of £1 each 60,000

Share Premium 55,000

Profit and Loss Reserve 85,000

7% Debentures 46,000

Current Liabilities 64,000

TOTAL EQUITY AND LIABILITIES 510,000

On the same day the company resolved to redeem 25,000 Preference Shares at £1.30 each. In order to provide fund for the redemption, the company issued 25,000 ordinary shares at £1.80. The preference shares had been issued at a premium of 30%.

You are required to:

a) Make the journal entries, including those relating to cash.

b) Draw up the Balance Sheet after the redemption.

c) Explain the difference between ordinary and preference shares.

16

Class Activity 15

The following is extracts of the Statement of financial position (Balance Sheet) of Demetris Limited on 31 December 2007:

Ordinary share capital of €1 each 300,000

8% Preference Shares of €1 each 50,000

Share Premium 265,000

Profit and Loss Reserve 235,000

During 2008 the following transactions were carried out that affected the capital structure of the company:

1. On 1 February 2008 the company carried out a 2 for 3 bonus issue for its ordinary shares. The bonus issue was made from the share premium account.

2. On 1 August 2008 the company carried out a 1 for 5 rights issue for its ordinary shares at a market price of €2.90 per share.

3. On 1 August 2008 the company redeemed 30,000 preference shares at a redemption price of €1.20 per share. The preference shares were originally issued at an issue price of €1.20 per share.

4. The retained earnings for the year ended 31 December 2008 amounted to €77,400.

You are required to carry out the double entries for the above and to show

Statement of financial position (Balance Sheet) extracts of the capital

structure at 31 December 2008 (18 marks).

Class Activity 16

Gardening Supplies plc has an authorised capital consisting of 5,000,000 ordinary shares of £0.25 each and 500,000 8% preference shares of £1 each. The balances

on its capital and loan accounts at 31 March 2005 were as follows:

£000

2,000,000 ordinary shares of £0.25 each 500

300,000 8% preference shares of £1 each 300

Share premium 128

Revaluation reserve 150

Retained earnings 170

10% debenture loan repayable 2015 250

On 1 April 2005 the directors decided:

(1) to make a capitalisation issue of 4 ordinary shares for every 5ordinary shares in issue, making maximum use of the non-distributable reserves;

(2) to make a rights issue at £0.30 per share of all the remaining un-issued ordinary shares;

(3) to issue a further 100,000 preference shares at a premium of £0.10;

(4) to redeem the debenture loan early at a premium of 2 per cent;

(5) to buy machinery at a cost of £500,000.

17

Required

(a) Prepare journal entries (without narratives) to record the above

transactions.

(b) Calculate the total on the reserves of Gardening Supplies plc after the

above transactions have been carried out.

(C) Calculate the effect on the company’s bank balance of the above

transactions.

(d) Give one reason why Gardening Supplies plc might replace a debenture

loan with share capital.

Class Activity 17

The following is the Balance Sheet of Zenovia PLC at 31 December 2007:

Non-current (Fixed) Assets 335,000

Current Assets (except cash) 293,000

Cash and bank 182,000

TOTAL ASSETS 810,000

Ordinary share capital of £1 each 300,000

8% Preference Shares of £1 each 160,000

Share Premium 85,000

Profit and Loss Reserve 135,000

7% Debentures 66,000

Current Liabilities 64,000

TOTAL EQUITY AND LIABILITIES 810,000

On the same day the company resolved to redeem 50,000 Preference Shares at £1.30 each. In order to provide fund for the redemption, the company issued 50,000 ordinary shares at £1.80. The preference shares had been issued at a premium of 30%.

You are required to:

d) Make the journal entries, including those relating to cash.

e) Draw up the Balance Sheet after the redemption.

f) Explain the difference between the revaluation reserve and profit and loss

reserve.

18

Class Activity 18

At 1 January 2003, Martin O’Neil Limited acquired 60% of Randy Lerner Limited when the Retained Earnings Reserves of the later were $60,000. The Balance Sheets of both companies at 31 December 2006 were as follows:

Martin O’Neil Randy Lerner

$000s $000s

Property, Plant and Equipment

784 548

Cost of Investment in Randy Lerner

356 0

Stocks 120 43

Debtors 86 26

Cash at Bank and in Hand 34 11

Total assets 1380

628

Ordinary shares 740 400

Retained Earnings Reserve 422 130

Trade Creditors 131 63

8%Debentures 30 12

Bank Overdraft 57 23

Total Equity and

Liabilities

1380

628

You are required to prepare the Consolidated Balance Sheet as at 31 December

2006.

19

Class Activity 19

At 1 January 2006, MUFC Limited acquired 70% of BCFC Limited when the reserves of the later were $45,000. The Balance Sheets of both companies at 31 December 2007 were as follows:

MUFC BCFC

$000s $000s

Land and Buildings 250 140

Cost of Investment in Steven Stride

155 0

Stocks 85 45

Debtors 55 25

Cash at Bank 35 40

Total assets 580

250

Share Capital 200 60

Reserves 235 95

Trade Creditors 75 58

Long Term Loans 70 37

Total Equity and

Liabilities

580

250

You are required to prepare the Consolidated Balance Sheet as at 31 December

2007.

Class Activity 20

At 1 January 2004, Doug Ellis Limited acquired 100% of Steven Stride Limited when the reserves of the later were $40,000. The Balance Sheets of both companies at 31 December 2004 were as follows:

Doug Ellis Steven Stride

$000s $000s

Land and Buildings 180 140

Cost of Investment in Steven Stride

150 0

Stocks 80 45

Debtors 50 25

Cash at Bank 30 40

Total assets 490

250

Share Capital 180 100

Reserves 220 90

Trade Creditors 60 30

Long Term Loans 30 30

Total Equity and

Liabilities

490

250

20

You are required to prepare the Consolidated Balance Sheet as at 31 December

2004.

Class Activity 21

At 1 January 2004, Bobby Charlton Limited acquired 60% of Pele Limited when the Retained Earnings Reserves of the later were €50,000. The Balance Sheets of both companies at 31 December 2008 were as follows:

Bobby Charlton Pele

€000s €000s

Property, Plant and Equipment

654 468

Investment in Pele Limited 461 0

Inventories (Stocks) 135 73

Receivables (Debtors) 193 56

Cash at Bank and in Hand 37 41

Total assets 1480

638

Ordinary shares 600 200

Retained Earnings Reserve 462 230

Trade Payables (Creditors) 181 93

8%Debentures 190 72

Bank Overdraft 47 43

Total Equity and Liabilities 1480

628

You are required to prepare the Consolidated Balance Sheet as at 31 December

2008.

Class Activity 22

The directors of Milner Limited are reviewing the company’s draft financial statements for the year ended 31 March 2005. The following matters are under discussion:

a) At 1 April 2004 the company’s Land and Buildings were valued at a cost of $3 million and the Provision for Depreciation at that date amounted to $300,000. The revaluation that was carried by an independent surveyor showed a value of $4.5 million. The directors intend to include this valuation in its accounts.

b) The company incurred research cost of $50,000 for the year ended 31 March 2005. It also developed a new product whose development costs amounted to $100,000. However the directors are uncertain whether the product would be a commercial success.

c) At 31 March 2005, the company had Investments with a carrying value of $900,000 that is available for immediate sale. It is considered probable by the directors that the Investments would be sold. If the investments have a fair value of $450,000 and any expected selling costs would amount to 1% of the selling price.

21

You are required to advise the directors on the correct accounting treatment of

the matters applying the relevant accounting standard that justifies your answer.

Show your calculations where necessary.

Class Activity 23

The directors of Agbonalor Limited are reviewing the company’s draft financial statements for the year ended 31 August 2006. The following matters are under discussion:

d) At 1 March 2006 the company bought Land and Buildings at a cost of $800,000. Included in this figure is Land worth $100,000. It is estimated that the buildings have a useful life of 50 years.

e) The company incurred research cost of $90,000 for the year ended 31 August 2006. It also developed a new product whose development costs amounted to $160,000. The new product is to be sold from 1 February 2007. The directors are confident that the product will be a commercial success.

f) At 31 August 2006, the company had Investments with a carrying value of $700,000 that is available for immediate sale. It is considered probable by the directors that the Investments would be sold. If the investments have a fair value of $950,000 and any expected selling costs would amount to 1% of the selling price.

g) On 1 September 2005 the company sold a Motor Van for $8,000. The original cost of the van was $15,000 and the Accumulated Depreciation on this Van at 31 August 2005 was $6,000.

h) Included in the balances of 1 September 2005 are Computer Equipment that has a cost of $10,000 and Accumulated Depreciation of $2,000. The company has decided to revise the remaining life on this equipment (as from 1 September 2005) to 2 years.

You are required to advise the directors on the correct accounting treatment of

the matters applying the relevant accounting standard that justifies your answer.

Show your calculations where necessary.

22

SUBJECT: ABSA 203 – INTERMEDIATE FINANCIAL

ACCOUNTING I

DATE: TIME: 2 ½ HOURS

INSTRUCTIONS TO CANDIDATES

This paper consists of TWO SECTIONS: SECTION A and

SECTION B. SECTION A is compulsory and from SECTION B you

are required to answer any 2 from 3 questions.

SECTION A: COMPULSORY

QUESTION 1

The following trial balance was extracted from the books of Rolando Limited on 31 December 2008:

Debit Credit

€ €

Ordinary Share Capital 70,000

Share Premium 12,000

12% Debentures 10,000

Directors Remuneration 10,000

Audit fees 1,500

Goodwill 9,000

Discounts allowed 550

Sales Revenue 88,000

Stock at 1 January 2008 15,600

Purchases 52,000

Carriage Inwards 2,000

Purchase returns 3,500

Trade Receivables (Debtors) 9,900

Cash at Bank 6,300

Land 10,000

Freehold Buildings-cost 45,000

Fixtures 8,000

Accumulated depreciation -Fixtures 900

Motor Vans-cost 44,000

Accumulated depreciation- Motor Vans 10,500

Bills Receivable 2,000

Trade Payables (Creditors) 11,700

Bills Payable 4,700

Rent Received 800

Debenture interest paid 600

Bank charges 250

General Expenses 2,000

Retained Earnings at 1 January 2008 6,600

200400 218,700

You are also given the following information at 31 December 2008:

• The stock was valued at €13,800.

• The total interest due on Debentures of €600 is due.

• The Goodwill has been impaired by €8,000.

• General expenses are prepaid by €500.

• Provide depreciation of €4000 for Motor Vans and €300 for Fixtures

23

You are required to:

c) Prepare an Income Stastement for the year ended 31 December 2008 (25

marks).

d) Prepare a Statement of Financial Position (Balance Sheet) as at 31 December

2008 (25 marks).

SECTION B: ANSWER ANY TWO QUESTIONS

QUESTION 2

a) Kyriakos Limited issued 3 million Ordinary shares with a nominal value of €1 each. The market price was €6.00 per share. A total of 50 cents per share was paid on the application, 350 cents per share on the allotment and 200 cents per share for first and final call. Applications were received for 5 million shares and any excess applications were refunded.

All funds for the issue were received in full except for those due on the first and final call in respect for 500,000 shares.

You are required to make the relevant ledger entries for the above (17 marks).

b) Explain the recognition criteria for intangible assets. Explain the

accounting treatmen concerning research and development expenditure

(8 marks).

QUESTION 3

a) The following is extracts of the Statement of financial position (Balance Sheet) of Demetris Limited on 31 December 2007:

Ordinary share capital of €1 each 300,000

8% Preference Shares of €1 each 50,000

Share Premium 265,000

Profit and Loss Reserve 235,000

During 2008 the following transactions were carried out that affected the capital structure of the company:

5. On 1 February 2008 the company carried out a 2 for 3 bonus issue for its ordinary shares. The bonus issue was made from the share premium account.

6. On 1 August 2008 the company carried out a 1 for 5 rights issue for its ordinary shares at a market price of €2.90 per share.

7. On 1 August 2008 the company redeemed 30,000 preference shares at a redemption price of €1.20 per share. The preference shares were originally issued at an issue price of €1.20 per share.

8. The retained earnings for the year ended 31 December 2008 amounted to €77,400.

You are required to carry out the double entries for the above and to show

Statement of financial position (Balance Sheet) extracts of the capital

structure at 31 December 2008 (18 marks).

b) Explain why companies may decide to purchase their own shares (7

marks).

24

QUESTION 4

a) At 1 January 2004, Bobby Charlton Limited acquired 60% of Pele Limited when the Retained Earnings Reserves of the later were €50,000. The Balance Sheets of both companies at 31 December 2008 were as follows:

Bobby Charlton Pele

€000s €000s

Property, Plant and Equipment

654 468

Investment in Pele Limited 461 0

Inventories (Stocks) 135 73

Receivables (Debtors) 193 56

Cash at Bank and in Hand 37 41

Total assets 1480

638

Ordinary shares 600 200

Retained Earnings Reserve 462 230

Trade Payables (Creditors) 181 93

8%Debentures 190 72

Bank Overdraft 47 43

Total Equity and Liabilities 1480

628

You are required to prepare the Consolidated Balance Sheet as at 31 December

2008 (18 marks).

b) Compare and contrast he accounts of sole traders as opposed to limited

companies (7 marks).

25

SUBJECT: ABSA 203 – INTERMEDIATE FINANCIAL

ACCOUNTING I

DATE: TIME: 2 ½ HOURS

INSTRUCTIONS TO CANDIDATES

This paper consists of TWO SECTIONS: SECTION A and

SECTION B. SECTION A is compulsory and from SECTION B you

are required to answer any 2 from 3 questions.

SECTION A: COMPULSORY QUESTION 1

The following trial balance was extracted from the books of Tommy PLC on 31 December 2007 after the preparation of the Trading Account:

Debit Credit

£ £

Ordinary Share Capital 70,000

8% Preference Share Capital 25,000

6% Debentures 20,000

Directors Remuneration 8,300

Audit fees 4,700

Goodwill 10,000

Gross Profit 58,400

Stock 30,300

Debtors 6,300

Cash at Bank 32,000

Land 36,000

Buildings 46,000

Fixtures and Fittings 4,000

Trade Creditors 15,800

Interim ordinary dividend 3,500

Salaries and Wages 16,200

Rent and Rates 3,100

General Expenses

Retained Earnings at 1 January 2005 11,200

200400 200,400

You are also given the following information at 31 December 2007:

• Provide for £4,300 Corporation Tax for the year.

• Provide £2,000 for the preference dividend for the year.

• The total interest due on Debentures of £1,200 is due.

• The Goodwill has been impaired by £4,300.

• A provision for bad debts of 1% of debtors is to be provided.

• The Salaries and Wages are accrued by £1900.

• Rates are prepaid by £420.

• Buildings are to be depreciated at 2% on the book value and Fixtures and Fittings by 15% on the book value.

26

You are required to:

e) Prepare a Profit and Loss Account for the year ended 31 December 2005 (25

marks).

f) Prepare a Balance Sheet as at 31 December 2005 (25 marks).

SECTION B: ANSWER ANY TWO QUESTIONS

QUESTION 2

a) At 1 January 2006, MUFC Limited acquired 70% of BCFC Limited when the reserves of the later were $45,000. The Balance Sheets of both companies at 31 December 2007 were as follows:

MUFC BCFC

$000s $000s

Land and Buildings 250 140

Cost of Investment in Steven Stride

155 0

Stocks 85 45

Debtors 55 25

Cash at Bank 35 40

Total assets 580

250

Share Capital 200 60

Reserves 235 95

Trade Creditors 75 58

Long Term Loans 70 37

Total Equity and

Liabilities

580

250

You are required to prepare the Consolidated Balance Sheet as at 31 December

2007 (18 marks).

b) “Bonus issues do not involve cash whereas rights issues do.” Discuss this

statement and reach a conclusion (7 marks).

QUESTION 3

The following is the Balance Sheet of Evdokia PLC at 31 December 2007:

Non-current (Fixed) Assets 235,000

Current Assets (except cash) 193,000

Cash and bank 82,000

TOTAL ASSETS 510,000

Ordinary share capital of £1 each 200,000

8% Preference Shares of £1 each 60,000

Share Premium 55,000

Profit and Loss Reserve 85,000

7% Debentures 46,000

Current Liabilities 64,000

27

TOTAL EQUITY AND LIABILITIES 510,000

On the same day the company resolved to redeem 25,000 Preference Shares at £1.30 each. In order to provide fund for the redemption, the company issued 25,000 ordinary shares at £1.80. The preference shares had been issued at a premium of 30%.

You are required to:

g) Make the journal entries, including those relating to cash (8 marks).

h) Draw up the Balance Sheet after the redemption (10 marks).

i) Explain the difference between ordinary and preference shares (7 marks).

QUESTION 4 c) Kyriakos Limited issued 2.5 million Ordinary shares with a nominal value of

£0.50 each. The market price was £1.20 per share. A total of 75 cents per share was paid on the application, 25 cents per share on the allotment, 15 cents per share for the first call and 5 cents per share for final calls. Applications were received for 3.5 million shares and any excess applications were refunded.

You are required to make the relevant ledger entries for the above (15 marks).

b) Explain what is meant by the term “depreciation”. Explain the different ways

in which Property, Plant and Equipment may be measured (10 marks).

28

SUBJECT: ABSA 234 PART (A) – FINANCIAL ACCOUNTING

DATE: TIME: 2 ½ HOURS

INSTRUCTIONS TO CANDIDATES

This paper consists of TWO SECTIONS: SECTION A and

SECTION B. SECTION A is compulsory and from SECTION B you

are required to answer any 2 from 3 questions.

SECTION A: COMPULSORY QUESTION 1

The following trial balance was extracted from the books of Tommy PLC on 31 December 2007 after the preparation of the Trading Account:

Debit Credit

£ £

Ordinary Share Capital 70,000

8% Preference Share Capital 25,000

6% Debentures 20,000

Directors Remuneration 8,300

Audit fees 4,700

Goodwill 10,000

Gross Profit 58,400

Stock 30,300

Debtors 6,300

Cash at Bank 32,000

Land 36,000

Buildings 46,000

Fixtures and Fittings 4,000

Trade Creditors 15,800

Interim ordinary dividend 3,500

Salaries and Wages 16,200

Rent and Rates 3,100

General Expenses

Retained Earnings at 1 January 2005 11,200

200400 200,400

You are also given the following information at 31 December 2007:

• Provide for £4,300 Corporation Tax for the year.

• Provide £2,000 for the preference dividend for the year.

• The total interest due on Debentures of £1,200 is due.

• The Goodwill has been impaired by £4,300.

• A provision for bad debts of 1% of debtors is to be provided.

• The Salaries and Wages are accrued by £1900.

• Rates are prepaid by £420.

• Buildings are to be depreciated at 2% on the book value and Fixtures and Fittings by 15% on the book value.

29

You are required to:

a) Prepare a Profit and Loss Account for the year ended 31

December 2005 (25 marks).

b) Prepare a Balance Sheet as at 31 December 2005 (25 marks).

SECTION B: ANSWER ANY TWO QUESTIONS

QUESTION 2

a) At 1 January 2006, MUFC Limited acquired 70% of BCFC Limited when the reserves of the later were $45,000. The Balance Sheets of both companies at 31 December 2007 were as follows:

MUFC BCFC

$000s $000s

Land and Buildings 250 140

Cost of Investment in Steven Stride

155 0

Stocks 85 45

Debtors 55 25

Cash at Bank 35 40

Total assets 580

250

Share Capital 200 60

Reserves 235 95

Trade Creditors 75 58

Long Term Loans 70 37

Total Equity and

Liabilities

580

250

You are required to prepare the Consolidated Balance Sheet as at 31 December

2007 (18 marks).

b) “Bonus issues do not involve cash whereas rights issues do.” Discuss this

statement and reach a conclusion (7 marks).

QUESTION 3

The following is the Balance Sheet of Evdokia PLC at 31 December 2007:

Non-current (Fixed) Assets 235,000

Current Assets (except cash) 193,000

Cash and bank 82,000

TOTAL ASSETS 510,000

Ordinary share capital of £1 each 200,000

8% Preference Shares of £1 each 60,000

Share Premium 55,000

Profit and Loss Reserve 85,000

7% Debentures 46,000

Current Liabilities 64,000

30

TOTAL EQUITY AND LIABILITIES 510,000

On the same day the company resolved to redeem 25,000 Preference Shares at £1.30 each. In order to provide fund for the redemption, the company issued 25,000 ordinary shares at £1.80. The preference shares had been issued at a premium of 30%.

You are required to:

a) Make the journal entries, including those relating to cash (8 marks).

b) Draw up the Balance Sheet after the redemption (10 marks).

c) Explain the difference between ordinary and preference shares (7 marks).

QUESTION 4 a) Kyriakos Limited issued 2.5 million Ordinary shares with a nominal value of £0.50 each. The market price was £1.20 per share. A total of 75 cents per share was paid on the application, 25 cents per share on the allotment, 15 cents per share for the first call and 5 cents per share for final calls. Applications were received for 3.5 million shares and any excess applications were refunded.

You are required to make the relevant ledger entries for the above (15 marks).

b) Explain what is meant by the term “depreciation”. Explain the different ways

in which Property, Plant and Equipment may be measured (10 marks).