About the Tech Bubble in the Late 1990s Facts...

26

Some Facts About the Tech Bubble in the Late 1990s (Some of the Slides from a Recent NBER Discussion ) Pietro Veronesi Graduate School of Business, University of Chicago CEPR, NBER NBER – April 2006

Transcript of About the Tech Bubble in the Late 1990s Facts...

Some Facts About the Tech Bubble in the Late 1990s

(Some of the Slides from a Recent NBER Discussion )

Pietro Veronesi

Graduate School of Business,

University of Chicago

CEPR, NBER

NBER – April 2006

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 1

Some Facts About the Nasdaq “Bubble”

A. What “went up” at the end of the 1990s?

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 1

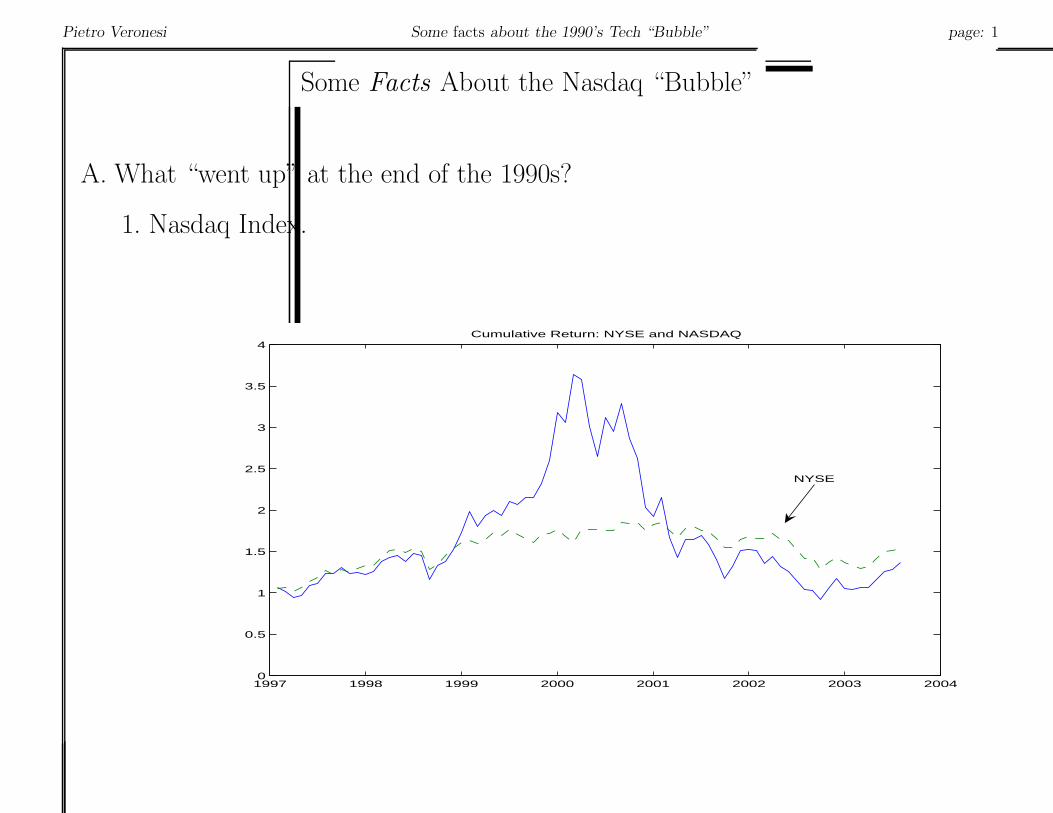

Some Facts About the Nasdaq “Bubble”

A. What “went up” at the end of the 1990s?

1. Nasdaq Index.

1997 1998 1999 2000 2001 2002 2003 20040

0.5

1

1.5

2

2.5

3

3.5

4Cumulative Return: NYSE and NASDAQ

NYSE

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 2

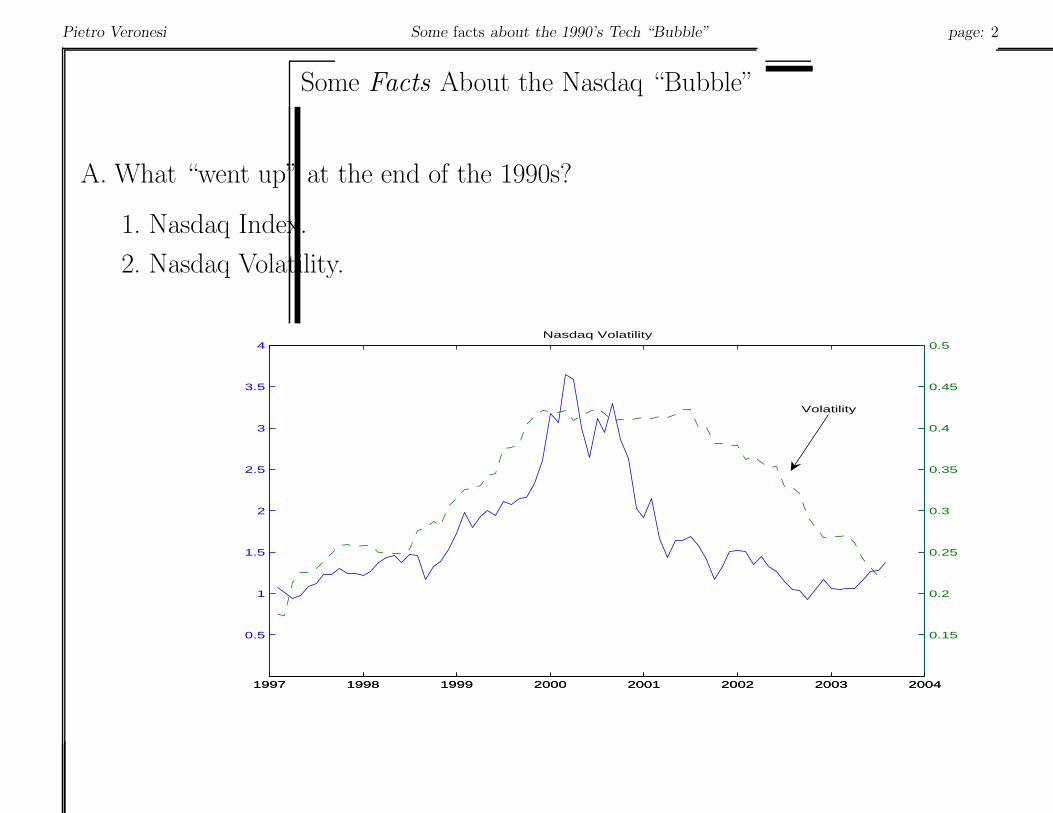

Some Facts About the Nasdaq “Bubble”

A. What “went up” at the end of the 1990s?

1. Nasdaq Index.

2. Nasdaq Volatility.

1997 1998 1999 2000 2001 2002 2003 2004

0.5

1

1.5

2

2.5

3

3.5

4Nasdaq Volatility

1997 1998 1999 2000 2001 2002 2003 2004

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Volatility

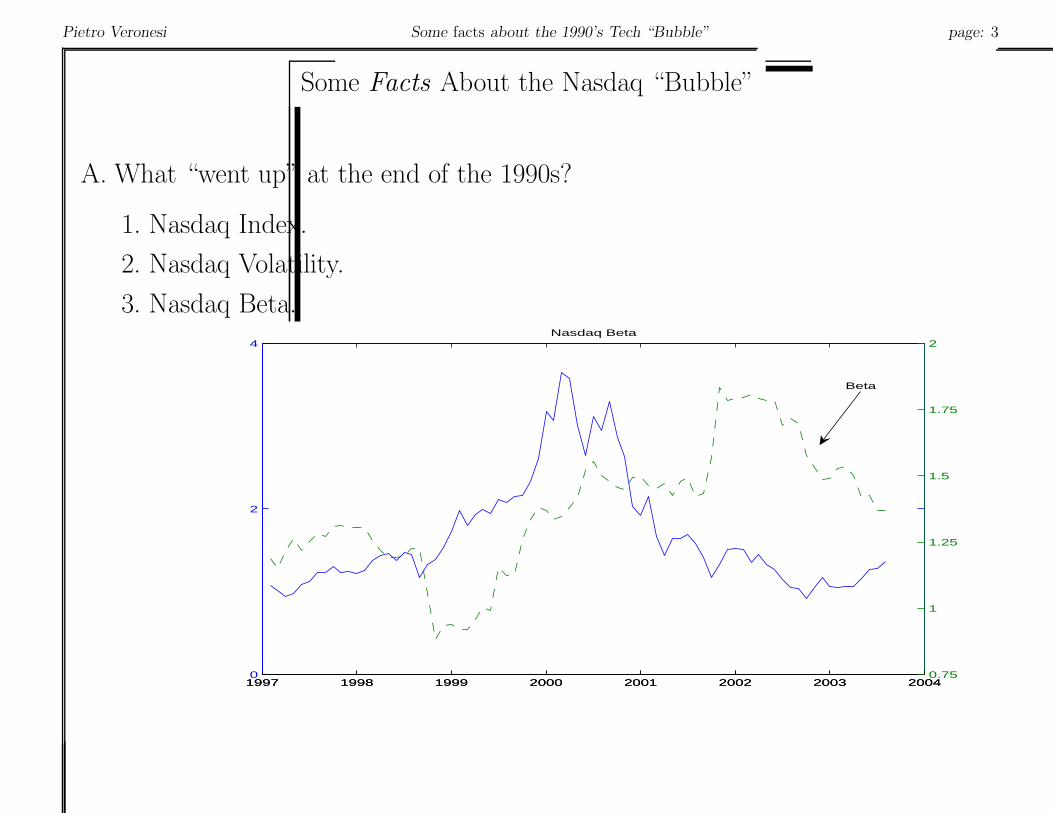

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 3

Some Facts About the Nasdaq “Bubble”

A. What “went up” at the end of the 1990s?

1. Nasdaq Index.

2. Nasdaq Volatility.

3. Nasdaq Beta.

1997 1998 1999 2000 2001 2002 2003 20040

2

4Nasdaq Beta

1997 1998 1999 2000 2001 2002 2003 20040.75

1

1.25

1.5

1.75

2

Beta

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 4

The Less Famous NYSE High Tech “Bubble”

B. Whatever happened to Nasdaq also happened to NYSE High-Tech Stocks.

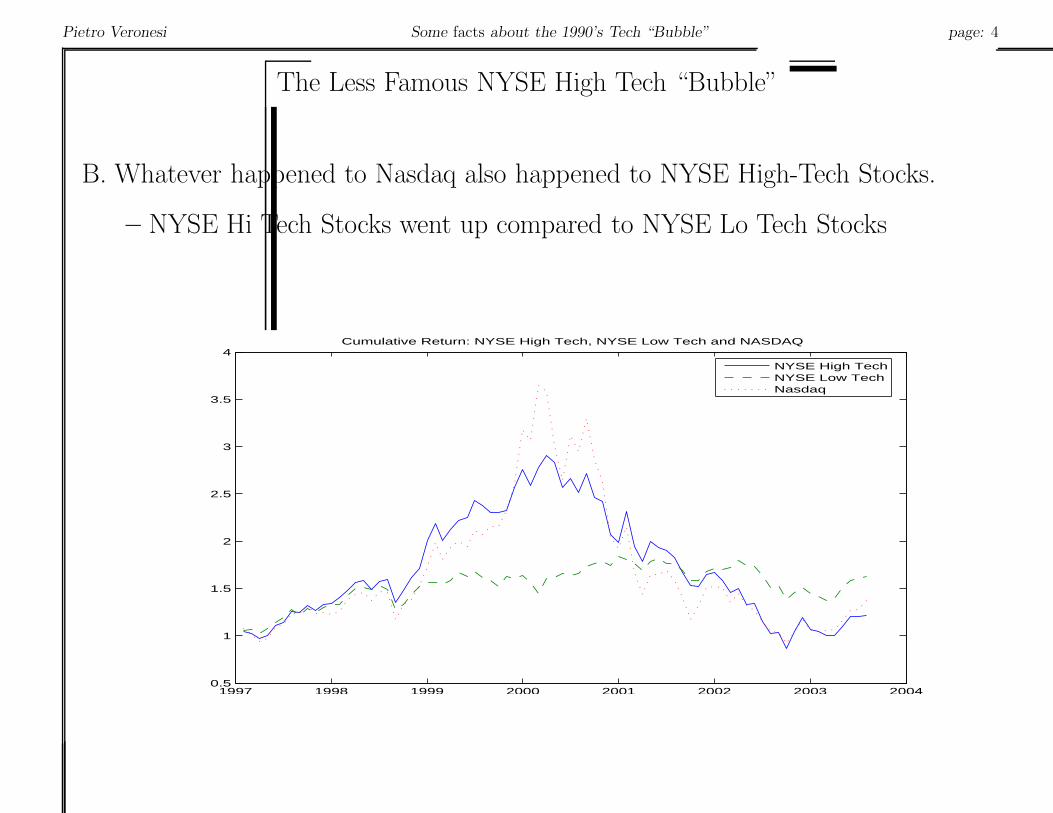

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 4

The Less Famous NYSE High Tech “Bubble”

B. Whatever happened to Nasdaq also happened to NYSE High-Tech Stocks.

– NYSE Hi Tech Stocks went up compared to NYSE Lo Tech Stocks

1997 1998 1999 2000 2001 2002 2003 20040.5

1

1.5

2

2.5

3

3.5

4Cumulative Return: NYSE High Tech, NYSE Low Tech and NASDAQ

NYSE High TechNYSE Low TechNasdaq

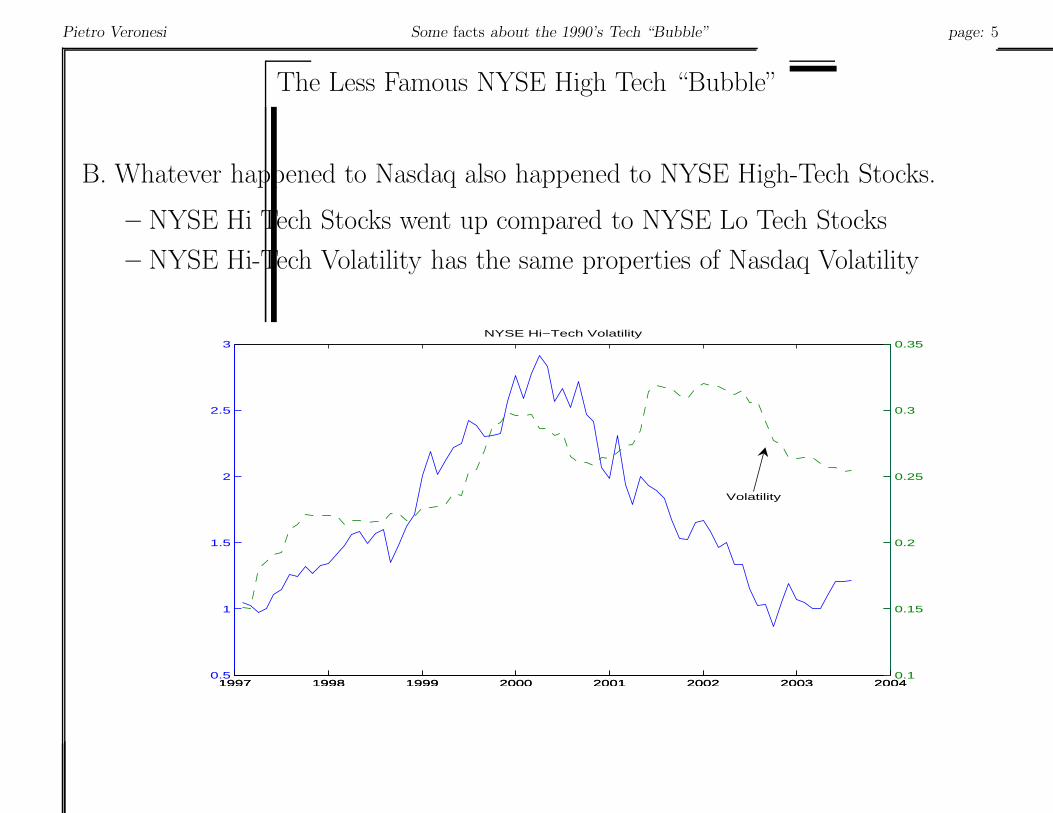

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 5

The Less Famous NYSE High Tech “Bubble”

B. Whatever happened to Nasdaq also happened to NYSE High-Tech Stocks.

– NYSE Hi Tech Stocks went up compared to NYSE Lo Tech Stocks

– NYSE Hi-Tech Volatility has the same properties of Nasdaq Volatility

1997 1998 1999 2000 2001 2002 2003 20040.5

1

1.5

2

2.5

3NYSE Hi−Tech Volatility

1997 1998 1999 2000 2001 2002 2003 20040.1

0.15

0.2

0.25

0.3

0.35

Volatility

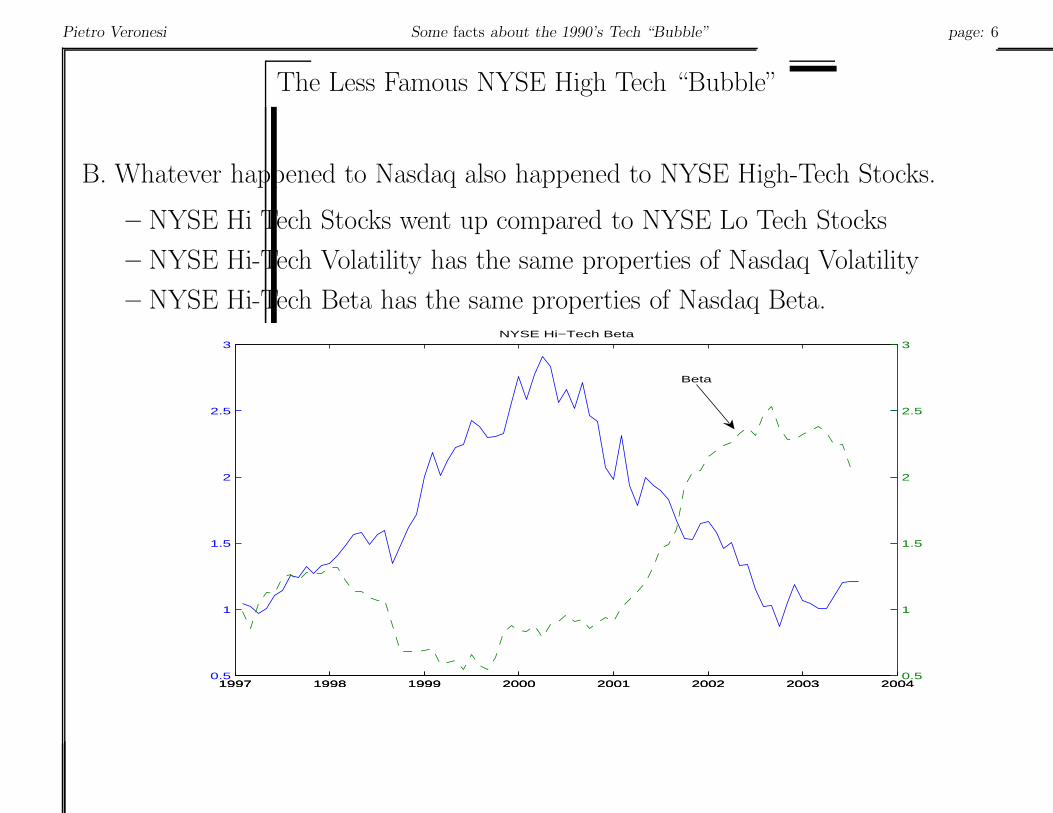

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 6

The Less Famous NYSE High Tech “Bubble”

B. Whatever happened to Nasdaq also happened to NYSE High-Tech Stocks.

– NYSE Hi Tech Stocks went up compared to NYSE Lo Tech Stocks

– NYSE Hi-Tech Volatility has the same properties of Nasdaq Volatility

– NYSE Hi-Tech Beta has the same properties of Nasdaq Beta.

1997 1998 1999 2000 2001 2002 2003 20040.5

1

1.5

2

2.5

3NYSE Hi−Tech Beta

1997 1998 1999 2000 2001 2002 2003 20040.5

1

1.5

2

2.5

3

Beta

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 7

Trading Volume in Tech Stocks

C. Is it really true that trading volume in tech stocks went up in the late 1990s?

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 7

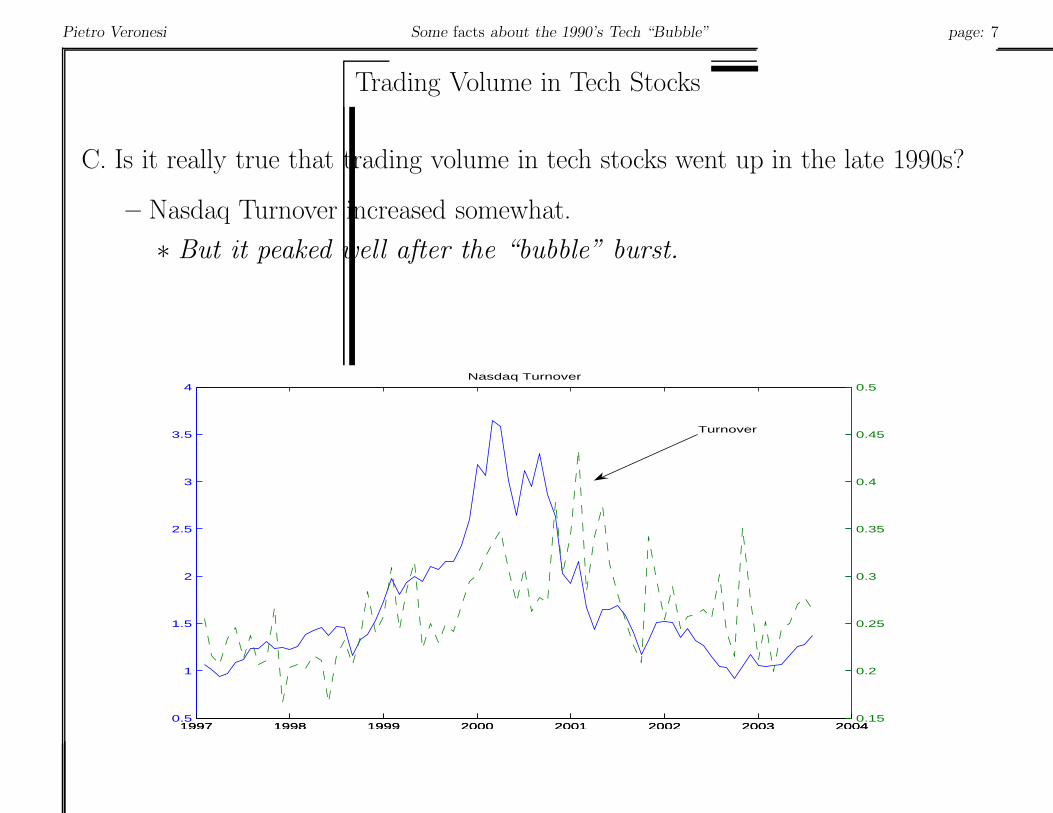

Trading Volume in Tech Stocks

C. Is it really true that trading volume in tech stocks went up in the late 1990s?

– Nasdaq Turnover increased somewhat.

∗ But it peaked well after the “bubble” burst.

1997 1998 1999 2000 2001 2002 2003 20040.5

1

1.5

2

2.5

3

3.5

4Nasdaq Turnover

1997 1998 1999 2000 2001 2002 2003 20040.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Turnover

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 8

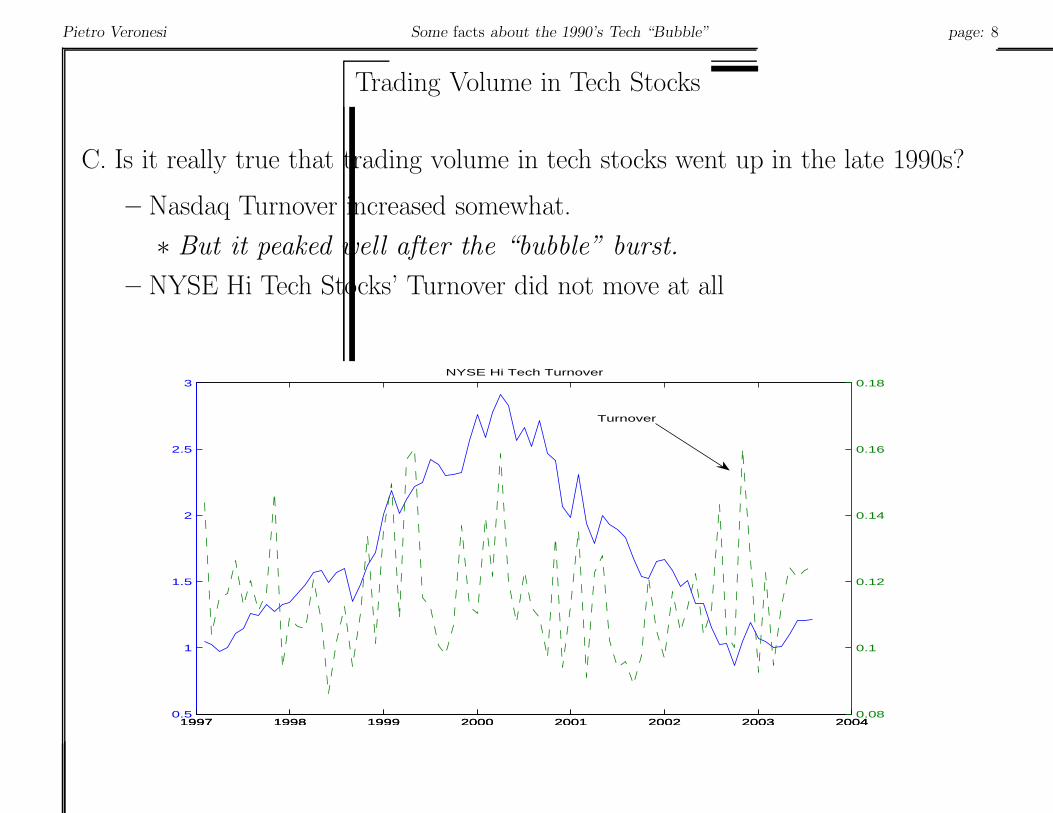

Trading Volume in Tech Stocks

C. Is it really true that trading volume in tech stocks went up in the late 1990s?

– Nasdaq Turnover increased somewhat.

∗ But it peaked well after the “bubble” burst.

– NYSE Hi Tech Stocks’ Turnover did not move at all

1997 1998 1999 2000 2001 2002 2003 20040.5

1

1.5

2

2.5

3NYSE Hi Tech Turnover

1997 1998 1999 2000 2001 2002 2003 20040.08

0.1

0.12

0.14

0.16

0.18

Turnover

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 9

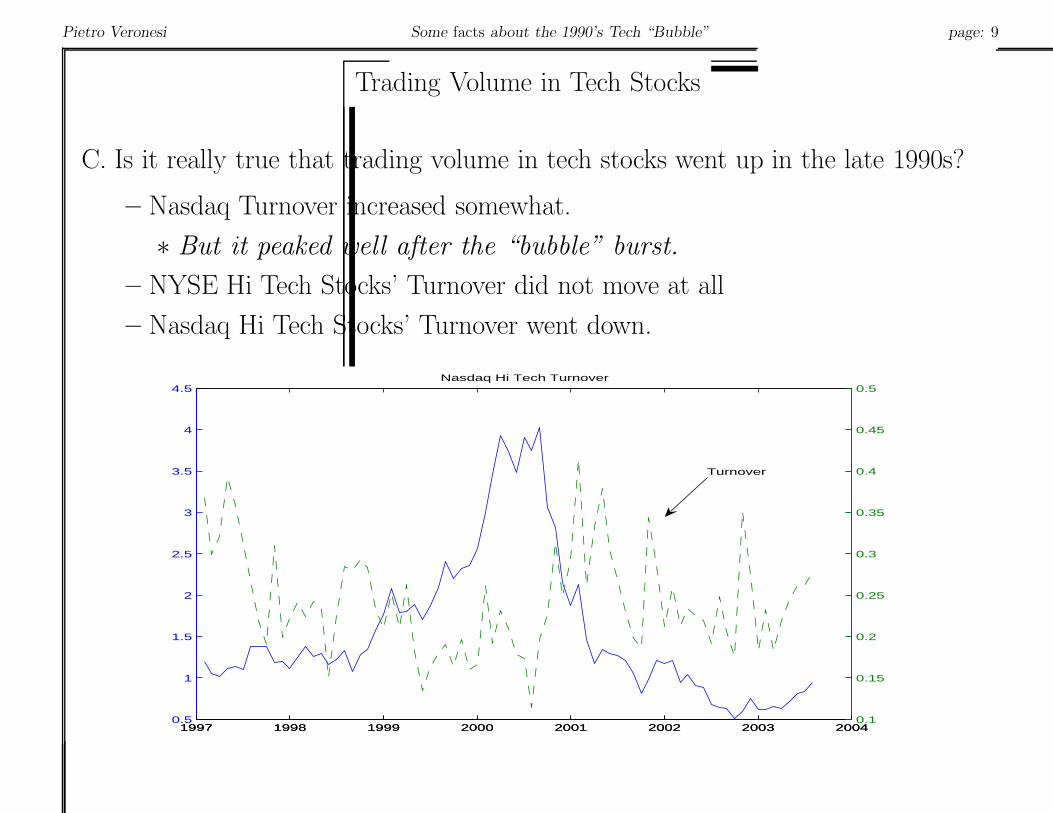

Trading Volume in Tech Stocks

C. Is it really true that trading volume in tech stocks went up in the late 1990s?

– Nasdaq Turnover increased somewhat.

∗ But it peaked well after the “bubble” burst.

– NYSE Hi Tech Stocks’ Turnover did not move at all

– Nasdaq Hi Tech Stocks’ Turnover went down.

1997 1998 1999 2000 2001 2002 2003 20040.5

1

1.5

2

2.5

3

3.5

4

4.5Nasdaq Hi Tech Turnover

1997 1998 1999 2000 2001 2002 2003 20040.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Turnover

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 10

Why Did the “Bubble” Burst?

D. There is little doubt of what caused tech stock prices to drop in 2000.

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 10

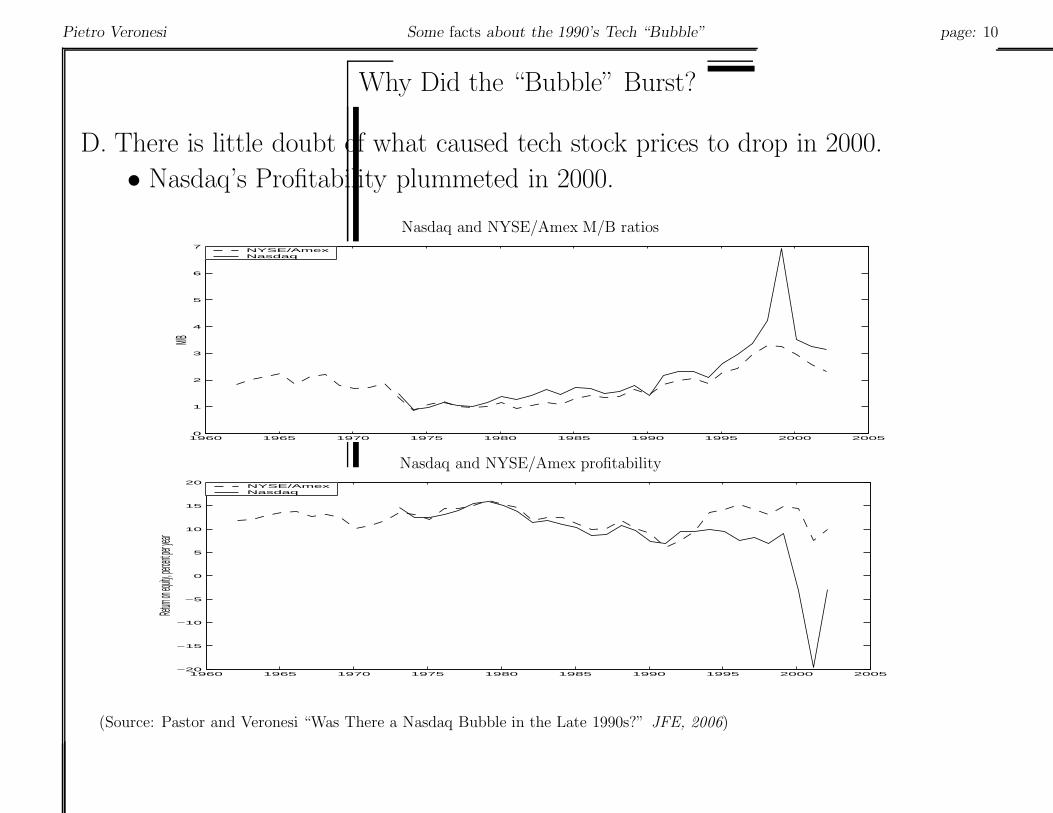

Why Did the “Bubble” Burst?

D. There is little doubt of what caused tech stock prices to drop in 2000.

• Nasdaq’s Profitability plummeted in 2000.

Nasdaq and NYSE/Amex M/B ratios

1960 1965 1970 1975 1980 1985 1990 1995 2000 20050

1

2

3

4

5

6

7

M/B

NYSE/AmexNasdaq

Nasdaq and NYSE/Amex profitability

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005−20

−15

−10

−5

0

5

10

15

20

Return o

n equity,

percent

per yea

r

NYSE/AmexNasdaq

(Source: Pastor and Veronesi “Was There a Nasdaq Bubble in the Late 1990s?” JFE, 2006)

fpverone

Line

fpverone

Line

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 11

Was it a Bubble?

• It is possible that prices exceeded fundamentals in the late 1990s for tech stocks.

• However, an explanation based on short sales constraints may find it hard toexplain why exactly the same pattern of return, volatility and “risk” occurredin NYSE Hi Tech stocks.

– Short sales constraints are much less binding for NYSE stocks.

• Short sales constraints though may have played a role in Nasdaq

– The “bubble” was stronger in Nasdaq

– Trading seemed more active in Nasdaq during the “bubble” period (but itpeaked later).

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 12

Was it a Bubble?

• Uncertainty about long term growth and low risk aversion may also have playedan important role.

(see Pastor and Veronesi “Was there a Nasdaq bubble in the late 1990s?”, 2006, JFE)

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 12

Was it a Bubble?

• Uncertainty about long term growth and low risk aversion may also have playedan important role.

(see Pastor and Veronesi “Was there a Nasdaq bubble in the late 1990s?”, 2006, JFE)

– This story explains all of the facts discussed earlier.

1. High uncertainty about long term growth + low risk aversion imply (very)high prices.

2. High uncertainty implies a high return volatility and a high beta.

3. High uncertainty implies a strong reaction of prices to bad news in prof-itability (and hence price drop)

4. High uncertainty + differences of opinion implies a high trading volume.

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 12

Was it a Bubble?

• Uncertainty about long term growth and low risk aversion may also have playedan important role.

(see Pastor and Veronesi “Was there a Nasdaq bubble in the late 1990s?”, 2006, JFE)

– This story explains all of the facts discussed earlier.

1. High uncertainty about long term growth + low risk aversion imply (very)high prices.

2. High uncertainty implies a high return volatility and a high beta.

3. High uncertainty implies a strong reaction of prices to bad news in prof-itability (and hence price drop)

4. High uncertainty + differences of opinion implies a high trading volume.

– Moreover, it explains other facts about the late 1990s

1. High uncertainty increases option value of new ventures and thus increaseincentive to go public

=⇒ IPO wave of tech stocks at the end of the 1990s

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 13

Was it a Bubble?

• Uncertainty and learning also imply one additional reason why prices shoulddecline during a technological revolution.

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 13

Was it a Bubble?

• Uncertainty and learning also imply one additional reason why prices shoulddecline during a technological revolution.

– Technological Revolutions imply an Increase in Risk

(See Pastor and Veronesi, “Technological Revolutions and Stock Prices,” NBER WP 2005)

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 13

Was it a Bubble?

• Uncertainty and learning also imply one additional reason why prices shoulddecline during a technological revolution.

– Technological Revolutions imply an Increase in Risk

(See Pastor and Veronesi, “Technological Revolutions and Stock Prices,” NBER WP 2005)

• Why?

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 13

Was it a Bubble?

• Uncertainty and learning also imply one additional reason why prices shoulddecline during a technological revolution.

– Technological Revolutions imply an Increase in Risk

(See Pastor and Veronesi, “Technological Revolutions and Stock Prices,” NBER WP 2005)

• Why?

– Productivity of new technologies is uncertain

∗ =⇒ High volatility

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 13

Was it a Bubble?

• Uncertainty and learning also imply one additional reason why prices shoulddecline during a technological revolution.

– Technological Revolutions imply an Increase in Risk

(See Pastor and Veronesi, “Technological Revolutions and Stock Prices,” NBER WP 2005)

• Why?

– Productivity of new technologies is uncertain

∗ =⇒ High volatility

– Initially, this uncertainty is mainly idiosyncratic as new technologies aredeveloped on a small case

∗ =⇒ prices up (e.g. PV 2003)

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 13

Was it a Bubble?

• Uncertainty and learning also imply one additional reason why prices shoulddecline during a technological revolution.

– Technological Revolutions imply an Increase in Risk

(See Pastor and Veronesi, “Technological Revolutions and Stock Prices,” NBER WP 2005)

• Why?

– Productivity of new technologies is uncertain

∗ =⇒ High volatility

– Initially, this uncertainty is mainly idiosyncratic as new technologies aredeveloped on a small case

∗ =⇒ prices up (e.g. PV 2003)

– If technology was eventually adopted (as in a Tech Revolution), the uncer-tainty gradually changes from idiosyncratic to systematic.

∗ =⇒ discount rate up and prices down.

Pietro Veronesi Some facts about the 1990’s Tech “Bubble” page: 13

Was it a Bubble?

• Uncertainty and learning also imply one additional reason why prices shoulddecline during a technological revolution.

– Technological Revolutions imply an Increase in Risk

(See Pastor and Veronesi, “Technological Revolutions and Stock Prices,” NBER WP 2005)

• Why?

– Productivity of new technologies is uncertain

∗ =⇒ High volatility

– Initially, this uncertainty is mainly idiosyncratic as new technologies aredeveloped on a small case

∗ =⇒ prices up (e.g. PV 2003)

– If technology was eventually adopted (as in a Tech Revolution), the uncer-tainty gradually changes from idiosyncratic to systematic.

∗ =⇒ discount rate up and prices down.

– This model implies all of the stylized facts discussed earlier.