ABN 51 116 399 430 For personal use only · 2009. 2. 24. · Goodman Fielder Limited Analyst...

43

Goodman Fielder Limited ABN 51 116 399 430 75 Talavera Road Macquarie Park, NSW, 2113 Phone: 02 8874 6000 Fax: 02 8874 6099 www.goodmanfielder.com.au The registered office of Goodman Fielder Limited and its Australian subsidiaries is 75 Talavera Road, Macquarie Park, NSW, 2113 25 February 2009 Announcements Officer Listed Company Relations Company Announcements Office New Zealand Exchange Limited ASX Limited Level 2, NZX Centre Exchange Centre 11 Cable Street 20 Bridge Street WELLINGTON SYDNEY NSW 2000 NEW ZEALAND Goodman Fielder Limited Analyst Briefing – Results for the period ended 31 December 2008 I attach a copy of the Analyst Briefing to be presented today in connection with the financial results of Goodman Fielder Limited for the half year ended 31 December 2008. The Analyst Briefing will be posted to Goodman Fielder’s website once released to the market. Yours sincerely, JONATHON WEST Company Secretary For personal use only

Transcript of ABN 51 116 399 430 For personal use only · 2009. 2. 24. · Goodman Fielder Limited Analyst...

Goodman Fielder Limited ABN 51 116 399 430

75 Talavera Road

Macquarie Park, NSW, 2113

Phone: 02 8874 6000

Fax: 02 8874 6099

www.goodmanfielder.com.au

The registered office of Goodman Fielder Limited and its Australian subsidiaries is 75 Talavera Road, Macquarie Park, NSW, 2113

25 February 2009 Announcements Officer Listed Company Relations Company Announcements Office New Zealand Exchange Limited ASX Limited Level 2, NZX Centre Exchange Centre 11 Cable Street 20 Bridge Street WELLINGTON SYDNEY NSW 2000 NEW ZEALAND

Goodman Fielder Limited Analyst Briefing – Results for the period ended 31 December 2008

I attach a copy of the Analyst Briefing to be presented today in connection with the financial results of Goodman Fielder Limited for the half year ended 31 December 2008. The Analyst Briefing will be posted to Goodman Fielder’s website once released to the market. Yours sincerely,

JONATHON WEST Company Secretary

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 1

Right

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 2

Right

AgendaAgenda

1. Group Highlights

2. Divisional Review

3. Financial Results

4. Outlook

3

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 3

Right

Group HighlightsGroup Highlights

5

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 4

Right

Group HighlightsGroup Highlights

• Strong revenue growth

• Commodity volatility impacts earnings– $120m cost increase

• Changing consumer buying patterns– PLG migration

• Reported earnings– Timing on NZ brand sale (H1→H2)

– Includes $6.6m restructuring costs

7

8

Group Financial SummaryGroup Financial Summary

8

A$m HY F’09 HY F’08 Change

Revenue 1,477.6 1,316.8 12.2%

EBITDA 175.9 189.7 -7.3%

Reported NPAT 73.9 94.6 -21.9%

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 5

Right

Group HighlightsGroup Highlights

• Strong Cash Flows

• Prudent Balance Sheet management

• Dividend Payout Ratio of 80%

9

10

Group Financial SummaryGroup Financial Summary

10

A$m HY F’09 HY F’08 Change

Free Cash Flow 164.6 168.3 -2.2%

Operating Cash Flow 87.7 95.3 -8.0%

Cash Realisation 115% 99% 16%

Net Debt 1,103.1 1,060.0 -4.1%

Dividend (cps) 4.5 6.0 -25%For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 6

Right

Group HighlightsGroup Highlights

Accelerated product innovation program

• Successful Lawson’s launch

• Helga’s Seed Sensations

• Frozen par-bake developments

• Dairy renovation complete

• Building new product development facility(Aug 2009 completion)

11

12

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 7

Right

Group HighlightsGroup Highlights

Efficiency drive well advanced

• Erskine Park completion 2009

• Stage 1 Mascot closure Dec 2008

• China commercial production Nov 2008

• Announced development of new Brisbane bakery

• On track to reduce workforce by 5% during F’09

13

Photo ofErskine Park

New Erskine Park FacilityNew Erskine Park Facility

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 8

Right

Group HighlightsGroup Highlights

• Good progress in the development of a scale Asia-Pacificbusiness

– Strong revenue growth (+36.8%)

– Established local manufacturing capability

– New category development leveraging expertise inDairy / Milling / Fats & Oils

– Strong management team

15

16

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 9

Right

Group HighlightsGroup Highlights

• Good progress in the development of a scale Asia-Pacificbusiness

– Strong revenue growth (+36.8%)

– Established local manufacturing capability

– New category development leveraging expertise inDairy / Milling / Fats & Oils

– Strong management team

• Commodities retreating from historic highs

– Goodman Fielder well positioned

17

Group HighlightsGroup Highlights

185YR Average July 2008 Feb 2009 Jun 2009 (Forecast)

254

428

298

0

100

200

300

400

500

Wheat

36

56

48

40

0

10

20

30

40

50

60

Dairy (Milk)

1084

1680

1310

0

500

1000

1500

2000

Canola

Market PricesA$/mt cpl A$/mt

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 10

Right

Group HighlightsGroup Highlights

• Good progress in the development of a scale Asia-Pacificbusiness

– Strong revenue growth (+36.8%)

– Established local manufacturing capability

– New category development leveraging expertise inDairy / Milling / Fats & Oils

– Strong management team

• Commodities retreating from historic highs

– Goodman Fielder well positioned

• Successfully refinanced $770m debt over the last 12 months

19

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 11

Right

Divisional ReviewDivisional Review

21

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 12

Right

GF Fresh BakingGF Fresh Baking –– Key Take OutsKey Take Outs

• Earnings impacted by– Slowing economy (PLG growth)

– High wheat costs

– Weaker (NZ) currency

• Improved Q2 following successful NPD initiatives– Lawson’s

– La Famiglia

• Continued strong management of working capital

23

24

GF Fresh BakingGF Fresh Baking

24

A$m HY F’09 HY F’08 Change

Revenue 493.3 499.4 -1.2%

EBITDA 57.5 75.6 -23.9%

EBITDA Margin (%) 11.7% 15.1% -3.4%

Working Capital -3.9 16.2 124.1%

Free Cash Flow 43.2 69.2 -37.6%

Capex 13.0 9.7 -34.0%For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 13

Right

GF Fresh BakingGF Fresh Baking –– Key Take OutsKey Take Outs

• Outstanding progress in our manufacturing performance– Cost / Quality / Service

– 6 Sigma program

• Manufacturing consolidation– New Brisbane Bakery

• Logistics restructure to be completed (Q3)

25

26

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 14

Right

GF Fresh BakingGF Fresh Baking –– Key Take OutsKey Take Outs

• Continuing to build our frozen par-bake capability

• Improved commodity outlook to underpin margindevelopment

• PLG contract negotiations in progress

27

28

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 15

Right

GF CommercialGF Commercial –– Key Take OutsKey Take Outs

• A difficult trading environment; Viz– Extreme commodity volatility

– Softening customer demand (weaker economy)

– Competitive discounting to move inventory

– Existing conditions set to continue through F’09

29

30

GF CommercialGF Commercial

30

A$m HY F’09 HY F’08 Change

Revenue 286.7 251.3 14.1%

EBITDA 32.2 29.5 9.2%

EBITDA Margin (%) 11.2% 11.7% -0.5%

Working Capital 96.2 82.6 -16.5%

Free Cash Flow 9.4 6.5 44.6%

Capex 6.0 5.8 -3.4%For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 16

Right

GF CommercialGF Commercial –– Key Take OutsKey Take Outs

• Portfolio development– Leveraging expertise in Milling / Fats & Oils technology /

Bakery solutions

• Channel development– Food Service / Industrial / QSR

• Operational improvements well progressed– Murarrie / Footscray capital programs

– Mascot closure 2009

– China in-country production commenced (Nov)

– Management talent 31

32

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 17

Right

GF CommercialGF Commercial –– Key Take OutsKey Take Outs

• Paradigm shift in commodity markets– Catalyst for further industry consolidation

33

34

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 18

Right

GF Home IngredientsGF Home Ingredients –– Key Take OutsKey Take Outs

• Strong revenue growth– Paradise acquisition

– Solid market shares

• Spreads growth constrained by new line commissioning

• Earnings solid despite commodity cost increases

35

36

GF Home IngredientsGF Home Ingredients

36

A$m HY F’09 HY F’08 Change

Revenue 266.7 197.8 34.8%

EBITDA 49.7 46.9 6%

EBITDA Margin (%) 18.6% 23.7% -5.1%

Working Capital 44.0 35.7 -23.2%

Free Cash Flow 60.7 55.9 8.6%

Capex 8.1 - -For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 19

Right

GF Home IngredientsGF Home Ingredients –– Key Take OutsKey Take Outs

• Robust category growth despite a softening economy

37

GF Home IngredientsGF Home Ingredients

11.8

8.0

19.0

1.4

10.0

6.9 6.3

11.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Spreads D&M FrozenPastry

Cooking Oil Flour Cake Mix Dips Biscuits

%C

hg

Category

NationalDollars (000s) Growth % YA

Qtr to 4/1/09

38* Aztec Data to 4/1/09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 20

Right

GF Home IngredientsGF Home Ingredients –– Key Take OutsKey Take Outs

• Robust category growth despite a softening economy

• Successful NPD program

39

40

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 21

Right

GF Home IngredientsGF Home Ingredients –– Key Take OutsKey Take Outs

• Robust category growth despite a softening economy

• Successful NPD program

• Significant improvement in operational capability– Carole Park (Biscuits)

– Salisbury (Dips)

• Erskine Park liquid grocery facility well advanced

41

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 22

Right

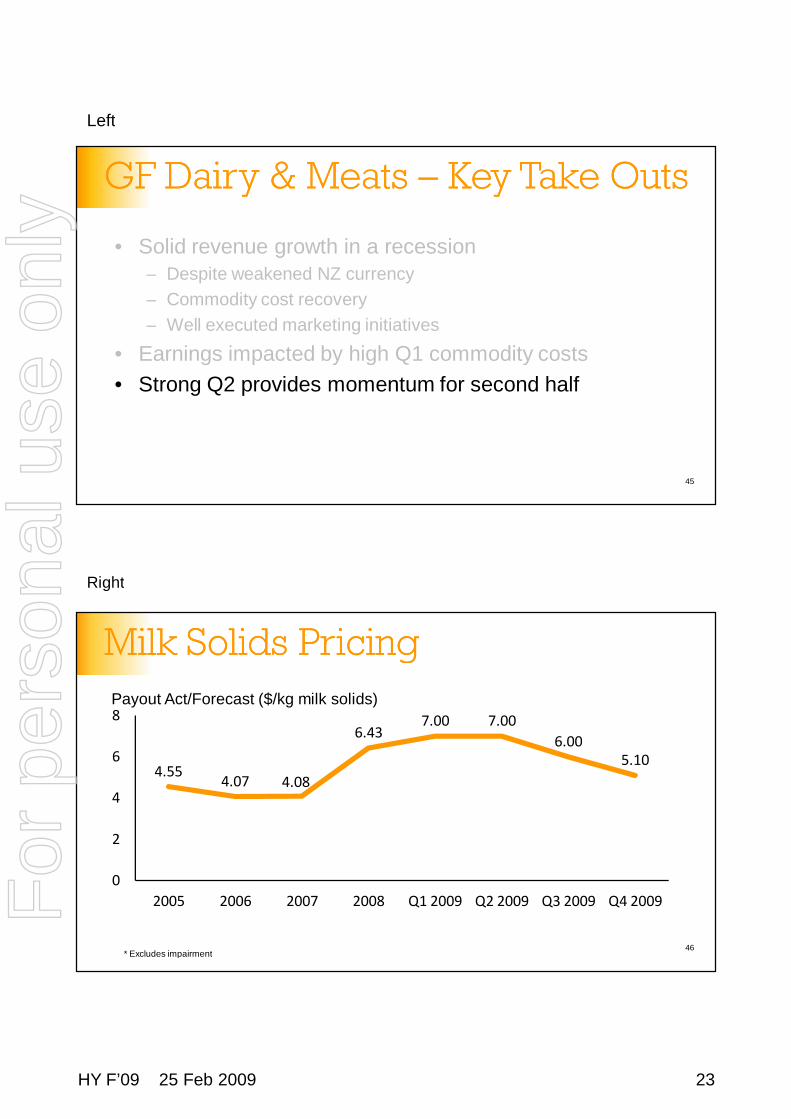

GF Dairy & MeatsGF Dairy & Meats –– Key Take OutsKey Take Outs

• Solid revenue growth in a recession– Despite weakened NZ currency

– Commodity cost recovery

– Well executed marketing initiatives

• Earnings impacted by high Q1 commodity costs

43

44

GF Dairy & MeatsGF Dairy & Meats

44

A$m HY F’09 HY F’08 Change

Revenue 243.1 231.0 5.2%

EBITDA 18.2 26.0 -30.0%

EBITDA Margin (%) 7.5% 11.3% -3.8%

Working Capital 10.7 60.2 82.2%

Free Cash Flow 25.2 20.0 26%

Capex 2.9 7.7 62.3%For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 23

Right

GF Dairy & MeatsGF Dairy & Meats –– Key Take OutsKey Take Outs

• Solid revenue growth in a recession– Despite weakened NZ currency

– Commodity cost recovery

– Well executed marketing initiatives

• Earnings impacted by high Q1 commodity costs

• Strong Q2 provides momentum for second half

45

Milk Solids PricingMilk Solids Pricing

46

4.554.07 4.08

6.437.00 7.00

6.005.10

0

2

4

6

8

2005 2006 2007 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009

* Excludes impairment

Payout Act/Forecast ($/kg milk solids)

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 24

Right

GF Dairy & MeatsGF Dairy & Meats –– Key Take OutsKey Take Outs

• Marketing programs building for the future– Beverages

• Impulse

– Yogurts / desserts

– Specialty cheese• Blue / brie

47

48

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 25

Right

GF Dairy & MeatsGF Dairy & Meats –– Key Take OutsKey Take Outs

• Marketing programs building for the future– Meats / Smallgoods

• Kiwi

49

50

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 26

Right

GF Dairy & MeatsGF Dairy & Meats –– Key Take OutsKey Take Outs

Manufacturing optimisation

• Longburn

– Major capital works completed

– Improved labour efficiency

– Yield focus

• Christchurch

– Low cost UHT production

– Reviewing capacity expansion

• Puhoi

– Significant yield / efficiency improvements51

52

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 27

Right

GF Asia PacificGF Asia Pacific –– Key Take OutsKey Take Outs

• Strong revenue growth– Price recovery against commodity cost increases

– Solid Pacific volumes

• Earnings performance underpinned by Pacificmarketing initiatives

53

54

GF Asia PacificGF Asia Pacific

54

A$m HY F’09 HY F’08 Change

Revenue 187.8 137.3 36.8%

EBITDA 23.8 17.9 33%

EBITDA Margin (%) 12.7% 13.0% -0.3%

Working Capital 58.8 37.5 -56.8%

Free Cash Flow 26.1 16.7 56.3%

Capex 1.4 0.8 -75%For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 28

Right

GF Asia PacificGF Asia Pacific –– Key Take OutsKey Take Outs

• Future growth underpinned by– Category expansion (Dairy / Bakery / Snacks)

– Improved commodity cost outlook

– Strong management team

55

56

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 29

Right

2009 Strategy Focus2009 Strategy Focus

• Cash generation

• Preserve our strong Balance Sheet

• Strategic review underway

57

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 30

Right

Financial ResultsFinancial Results

59

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 31

Right

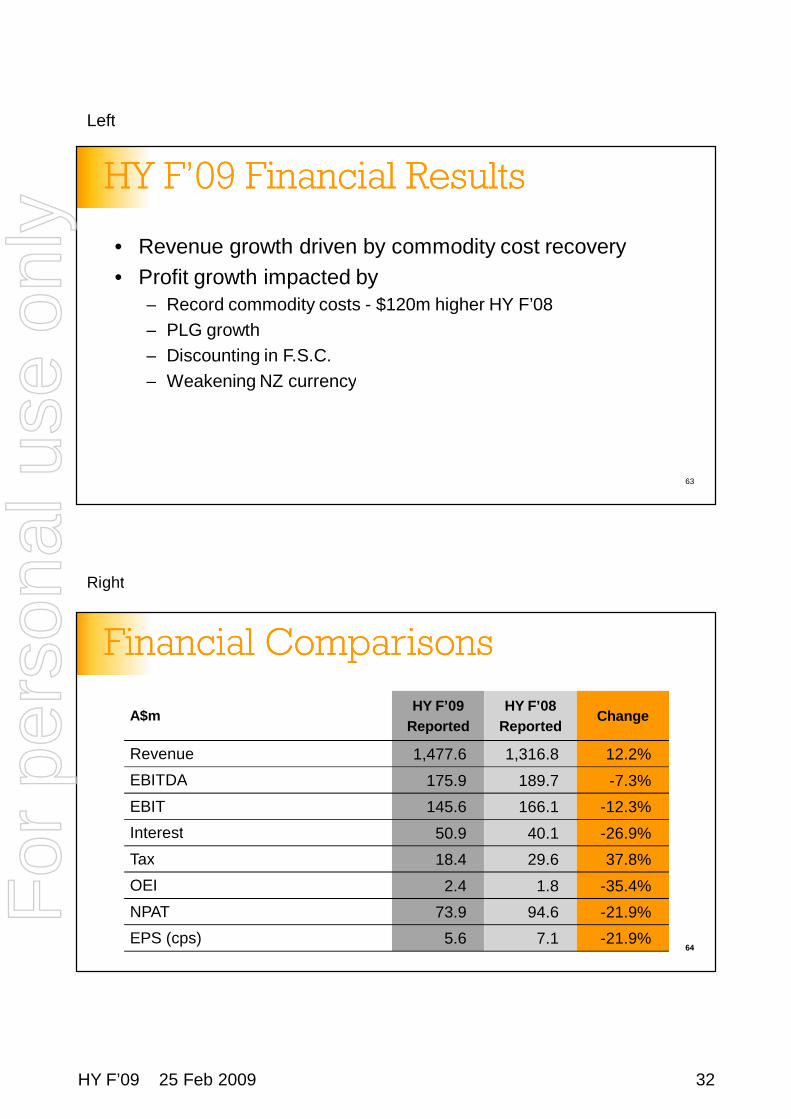

HY F’09 Financial ResultsHY F’09 Financial Results

• EBITDA includes restructure costs $6.6m

• Interest reflects impact of commodity costs peak

• Tax rate 19.4% incorporates significant ongoingR&D benefit

• Reported Net Profit @ 5% of sales at the top ofcommodity cycle

61

62

HY F’09 Financial ResultsHY F’09 Financial Results

62

A$mHY F’09

Reported% NSV

Revenue 1,477.6 100%

EBITDA 175.9 11.9%

EBIT 145.6 9.9%

Interest 50.9 3.4%

Tax 18.4 1.2%

OEI 2.4 0.2%

NPAT 73.9 5%

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 32

Right

HY F’09 Financial ResultsHY F’09 Financial Results

• Revenue growth driven by commodity cost recovery

• Profit growth impacted by– Record commodity costs - $120m higher HY F’08

– PLG growth

– Discounting in F.S.C.

– Weakening NZ currency

63

64

Financial ComparisonsFinancial Comparisons

64

A$mHY F’09

Reported

HY F’08

ReportedChange

Revenue 1,477.6 1,316.8 12.2%

EBITDA 175.9 189.7 -7.3%

EBIT 145.6 166.1 -12.3%

Interest 50.9 40.1 -26.9%

Tax 18.4 29.6 37.8%

OEI 2.4 1.8 -35.4%

NPAT 73.9 94.6 -21.9%

EPS (cps) 5.6 7.1 -21.9%

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 33

Right

Key Movements HY F’09 v HY F’08Key Movements HY F’09 v HY F’08

• COGS increases substantially recovered

• Maintaining brand investment

• Higher fuel costs only partially off-set by logistics re-orgs

• Fixed costs reduction reflecting lower employee numbers

65

Key Movements HY F’09 v HY F’08Key Movements HY F’09 v HY F’08

66

-15

1 3

161

-165

-1

-200

-150

-100

-50

0

50

100

150

200

Revenue COGS Selling &

Marketing

Warehousing

& Distribution

General &

Admin

Other

$m

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 34

Right

Balance SheetBalance Sheet

• Absolute focus on cash generation and debt minimisation

• Pleasing working capital result as inventory values peak

• Capital Expenditure staged to align with internal cashtargets

67

68

Balance SheetBalance Sheet

68

A$m Dec 08 June 08

Trade & Other Debtors 280.3 290.4

Inventory 236.2 201.0

Net PPE 545.9 527.8

Goodwill & Intangibles 1,956.5 1,885.1

Other 7.6 28.4

Trade & Other Creditors (406.0) (358.9)

Capital Employed 2,620.5 2,573.8

Net Debt (1,103.1) (1,043.4)

Net Tax Assets 100.6 69.2

Net Assets 1,618.0 1,599.6

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 35

Right

Cash FlowCash Flow

• Ongoing strong cash generation

• Efficient cash realisation*

HY F’09 115%

HY F’08 99%

FY F’08 105%

69

* Cash realisation ratio = [net cash inflow from operating activities] / [profit for the period]

Cash FlowCash Flow

70

145.6

87.7

45.6

31.3

20.9

30.3

9.6

0

20

40

60

80

100

120

140

160

180

200

Reported EBIT Dep'n andAmort'n

Changes inworking capital

Interest paid Tax paid Other Operating cashflow

A$m

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 36

Right

F’09 Key RatiosF’09 Key Ratios

• F’09 EBITDA margin reflects high commoditycosts partially off-set by tight expense control

• Dividend payout ratio maintained at 80%

71

72

F’09 Key RatiosF’09 Key Ratios

72

HY F’09 HY F’08

EBITDA Margin 11.9% 14.4%

Earnings per Share (c) 5.6 7.1

Dividends per Share (c) 4.5 6.0

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 37

Right

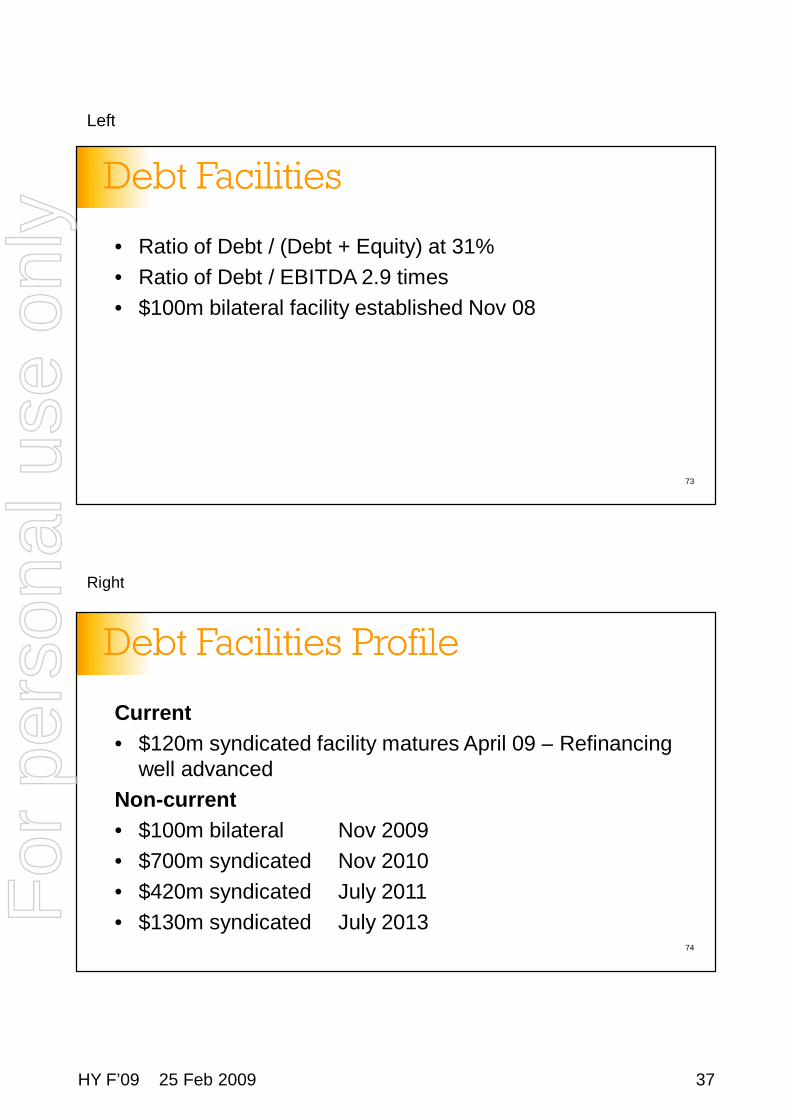

Debt FacilitiesDebt Facilities

• Ratio of Debt / (Debt + Equity) at 31%

• Ratio of Debt / EBITDA 2.9 times

• $100m bilateral facility established Nov 08

73

Debt Facilities ProfileDebt Facilities Profile

Current

• $120m syndicated facility matures April 09 – Refinancingwell advanced

Non-current

• $100m bilateral Nov 2009

• $700m syndicated Nov 2010

• $420m syndicated July 2011

• $130m syndicated July 201374

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 38

Right

DividendDividend

• DRP implemented F’09– 2.5% discount

– 50% underwritten

• Franking impacted by lower tax

• Payout ratio 80% of reported NPAT

• HY franking 31% & estimated FY 31%

75

76

DividendDividend

76

DPS Franking %

F’09 Interim 4.5¢ 31%

F’08 Interim 6.0¢ 30%

Full Year F’08 13.5¢ 36%

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 39

Right

OutlookOutlook

77

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 40

Right

F’09 OutlookF’09 Outlook

• F’09 NPAT guidance of $170m - $185m

• Reflects;– Weakening NZ currency

– Timing on commodity cycle

– Softer economic conditions

• EBITDA projected above prior year

• Continued strong cash flows

79

FullYear NPAT GuidanceFullYear NPAT Guidance

80

F'08 * F'09

* Excludes impairment

NPAT A$m197

185

170

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 41

Right

OutlookOutlook

• The company remains optimistic for F’10; viz:– Lower commodity costs (dairy/wheat/oils)

– Manufacturing cost improvements• Finalised plant closures

• New plants operational

• Operational disciplines

– Growth from innovation

– Strategic review recommendations

81

Building for the futurePresentation to Analysts - HY F’09

82

For

per

sona

l use

onl

y

Left

HY F’09 25 Feb 2009 42

Right

83

Building for the futurePresentation to Analysts - HY F’09

For

per

sona

l use

onl

y