ABHASH RANJAN

36

By Abhash Ranjan

Transcript of ABHASH RANJAN

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 1/36

By

Abhash Ranjan

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 2/36

PRESENTATION AGENDA

•ABOUT USHA MARTIN

•PRESENCE

•BUSINESS SEGMENT

•DESIGN OF STUDY

•INVENTORY MANAGEMENT

•ABC ANALYSIS

•INTERPRETATION

•CONCLUSION•SUGGESTION

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 3/36

ABOUT USHA MARTIN

USHA MARTIN is a unique Rs. 3,600-crore global 17 companies

engaged in mining, manufacture, distribution and service centres

related to the steel industry across 4 continents, 14 countries and

24 global locations. From coal-iron ore mining, captive utility and

auxiliary facilities at one end, to the manufacture of specialitysteel, wires, wire ropes, and other value-added products and end-

use application solutions at the other. UML is also engaged in the

economic empowerment of communities.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 4/36

VISION OF USHA MARTIN

To retain market leadership in India and be globally

competitive through customer orientation, excellence in

quality, innovation and technology.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 5/36

HISTORY OF USHA MARTIN

1960:The Company was incorporated as Usha Martin Black (Wire

Ropes) Limited having its wire rope plant at Ranchi. The name

was changed to Usha Martin Black Ltd. in 1979 and further

changed to Usha Martin Industries Ltd.(UMIL) in 1983.

1965:

UMIL promoted Usha Ismal Ltd. (UIL) in collaboration with

CCL Systems Ltd of UK for the manufacture of fittings and

accessories, equipment for pre-stressed concrete system, wire

ropes and wire ropes splicing equipment at Ranchi. UIL merged

with UMIL in 1990 and became a division of the company

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 6/36

1971:

UMIL promoted Usha Alloy Steels Limited (UASL) forthe manufacture of billets at Jamshedpur. UASL merged

with UMIL in 1988.

1975:

UASL acquired an ongoing rolling mill at Agra.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 7/36

WIRE AND WIRE ROPE DIVISION

The Usha Martin Ltd. is produce 100,000 MT / annum

manufacturing facilities at Ranchi (Eastern India) is amongst the

top four wire rope producers in the world. Since its inception, the

division has continuously developed and expanded its range of product offerings and is considered a pioneer in certain classes of

products in India. Steel wire ropes manufactured by the division

find wide applications in oil exploration, mining, elevators,

Crane, fishing, construction, load transportation and general

engineering sectors.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 8/36

MACHINERY DIVISION This is located at Bangalore was set up in 1974 to

manufacture Wire Drawing and allied machines. Over the

years, the division has added a wide range of Wire, Wire

Rope and Cable machinery to its product range and is now

the leader in this field in India. The division started with

technical collaboration with M/s Marshall Richards Barcro of UK and subsequently has collaborated with internationally

reputed firms like De-Angeli Industries SPA, Italy,

Stolberger Maschinenfabrik, Germany, Hi-Draw Machinery

Ltd, UK and Redaelli Techna Meccanica, Italy. A faciltity in

ranchi has also been created for manufacturing machines

required for Wire Drawing and Stranding Applications.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 9/36

PRESENCE

•Headquartered in Kolkata, India;

•

Iron ore mine (Barajamda) and captive coal mines (Daltonganj) in thestate of Jharkhand, India;

•Steel manufacturing facilities located in Jamshedpur and Agra;

•Wire and wire rope manufacturing facilities located in Ranchi

(Jharkhand) and Hoshiarpur (Punjab) in India, Bangkok (Thailand),

Dubai (the UAE) and Nottinghamshire (the UK);

•High – value wire and conveyor cord manufacturing facilities at Ranchi;

•Machinery manufacturing and engineering application centers in

Ranchi and Bangalore;

•Manufacturing units for bright bars in Ranchi and Sriperumbudur(Tamil Nadu); Rigging shops in the Netherlands and the UK.

•Telecommunication cables manufacture at Silvassa (India).

•Wide global network of marketing and distribution warehouses in

Singapore,

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 10/36

CORPORATE SOCIAL RESPONSIBILITY

Usha Martin has strongly believed in its social responsibility being animportant part of business philosophy. The company has promoted

Krishi Gram Vikas Kendra (KGVK), as its’ social arms to take

appropriate initiative in various areas which affect health, social life

and economic well being of people for a period of over 35 years.Presently, KGVK reaches out to about one lack household of tribal

people and weaker sections of society in over 700 villages across 6

districts in the State of Jharkhand.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 11/36

USHA MARTIN AN INTEGRATED COMPANY:

Usha Martin is integrated from iron ore and coal mines at one end

to wire ropes at the other, connected through intermediate captive

power generation and the manufacture of steel and wires.

This is one of the most extensively integrated business modelswithin the wire ropes industry the world over. With new cost

optimisation projects being implemented by the beginning of

2012-13, the deeper integration will strengthen the Company’s

cost – advantage and reduce its already low dependence on external

raw material sources. Moreover, the Company will be better

equipped to manage industry cycles effectively.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 12/36

PRODUCTS:

The Company’s product basket comprises wires, strands,

wire ropes, cords, slings, wire rods, straight bars,

construction and structural steel, bright bars, conveyor

cords, specialty wires and telecommunication cables.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 13/36

WORLD’S LARGEST ARCH BRIDGE IN DUBAI

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 14/36

INCHEON BRIDGE NEW SONGDO CITY, KOREA

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 15/36

HOWRAH BRIDGE

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 16/36

SOURCE OF THE RAW MATERIAL

Steel Wire Rod (90% to 96%) : UASD, Jamshedpur

Steel Wire Rod (4% to 10%) : Other Sources (Imported or Local)

Fiber Core : M/S Chhota Nagapur WireRope, Ranchi.

Other Raw Material

Zinc : M/S Hindustan Zinc

Lead, Jute & Lubricants : Imported or Local

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 17/36

BOARD OF DIRECTORS:

•The Board of Directors of the Company comprises of

One Non-Executive Chairman

•Seven Independent Non-Executive Directors,

•

One Non-Executive Director and•Four Executive Directors.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 18/36

BUSINESS SEGMENT:

•STEEL AND MINING BUSINESS

•WIRE ROPES AND SPECIALITY PRODUCTS BUSINESS

•CABLE BUSINESS

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 19/36

MAJOR OVERSEAS UNITS:

•Usha Martin Singapore Pte Limited [UMSPL]

•Usha Martin Americas Inc. [UMAI]

•Brunton Wolf Wire Ropes FZCo [BWWR]

•Usha Siam Steel Industries Public Company Limited[USSIL]

•Usha Martin International Limited [UMIL]

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 20/36

INVENTORY MANAGEMENT AN

INTRODUCTION :

Inventory management is an important part of theworking capital management of any organisation.

Practical decisions have to be made as to how inventory

is going to be managed

– Which management system should be used, howmuch inventory should be kept and so on.

DESIGN OF STUDY

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 21/36

TYPES OF INVENTORY MANAGEMENT

SYSTEMS

•(JIT)

•(EOQ)

•(SS)

•

(LIFO) AND (FIFO)

•ABC METHOD

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 22/36

THE REASONS FOR INVENTORY

CONTROL

• Helps balance the stock as to value, size, color, style,

and price line in proportion to demand or sales trends.

• Help plan the winners as well as move slow sellers.

• Helps secure the best rate of stock turnover for each

item.

• Helps reduce expenses and markdowns.

• Helps maintain a business reputation for always

having new, fresh merchandise in wanted sizes and

colors.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 23/36

TYPE OF INVENTORIES

•Raw materials Inventory

•Work-in-Process Inventory

•Finished Goods Inventory

•

Stores and Spares

RawMaterials

Work inProgress

FinishedGoods

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 24/36

Usha Martin Limited has classified its inventories into 3

categories namely,

(1) Stores and Spare

(2) Production and

(3) Packing

INVENTORY MANAGEMENT AT USHA MARTIN LTD.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 25/36

GRAPHICAL REPRESENTATION OF ABC

METHOD

The items of all inventories are arranged in descending

order according to their book value. Then the

summation of consecutive items from the top is donewhich adds up to 70% of total inventory costs.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 26/36

USHA MARTIN USES ABC ANALYSIS SYSTEM FOR

INVENTORY MANAGEMENT:

ABC Analysis is generated according to the book value of the items

stores is custodian every items. Breakup of ABC: - A=70%, B=20%,

C=10%

Category A - Items whose book value constitutes up to 70% of the total

value of the material.

Category B- 20%.

Category C- Remaining 10%.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 27/36

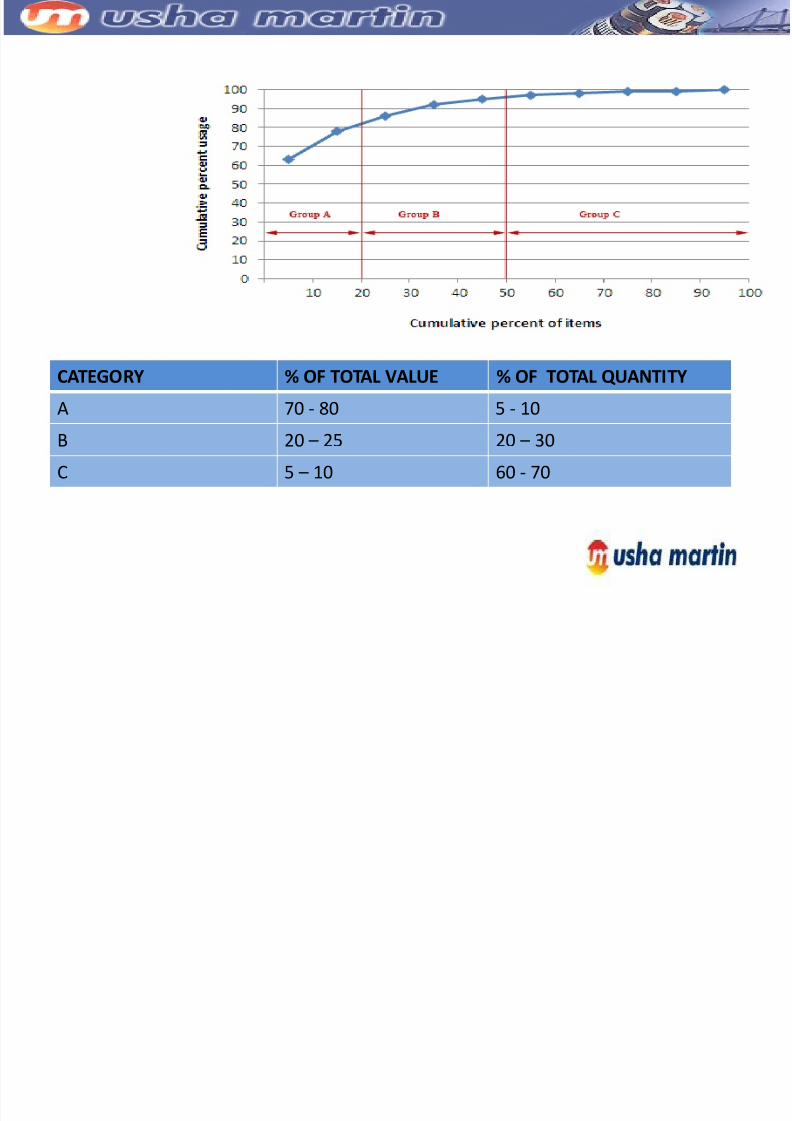

CATEGORY % OF TOTAL VALUE % OF TOTAL QUANTITY

A 70 - 80 5 - 10

B 20 – 25 20 – 30

C 5 – 10 60 - 70

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 28/36

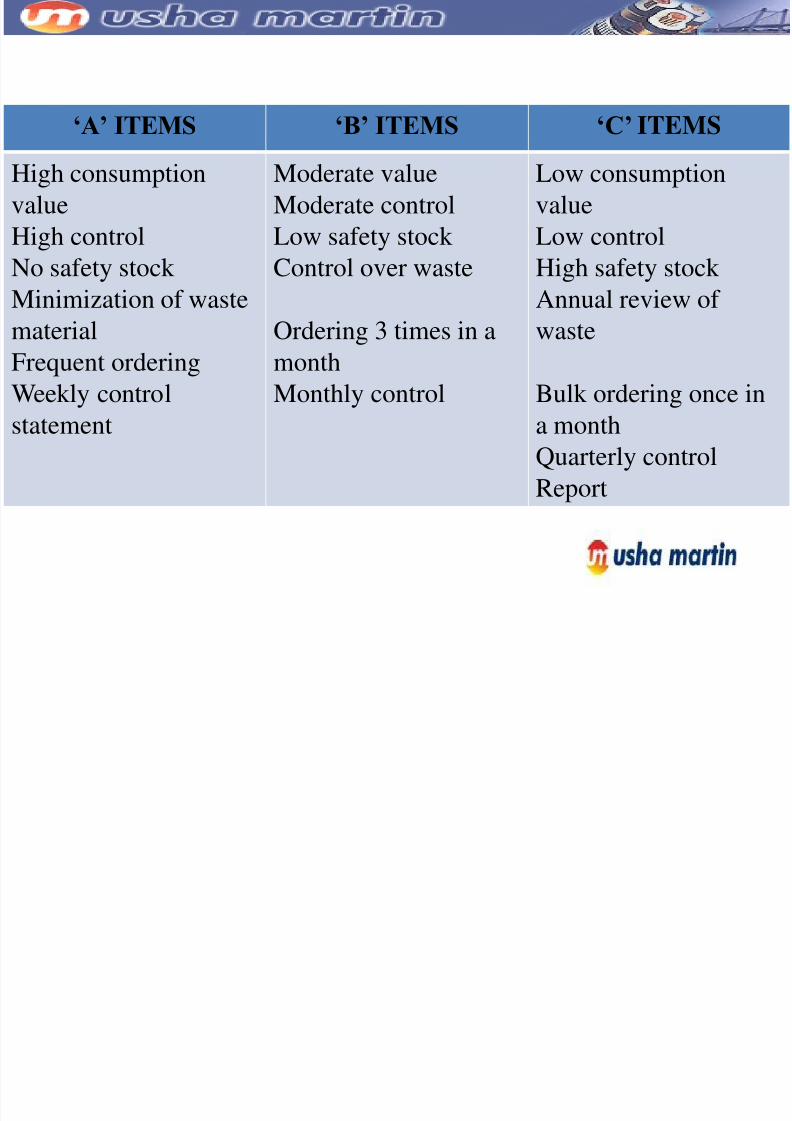

‘A’ ITEMS ‘B’ ITEMS ‘C’ ITEMS

High consumption

value

High control

No safety stock Minimization of waste

material

Frequent ordering

Weekly control

statement

Moderate value

Moderate control

Low safety stock

Control over waste

Ordering 3 times in a

month

Monthly control

Low consumption

value

Low control

High safety stock Annual review of

waste

Bulk ordering once in

a monthQuarterly control

Report

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 29/36

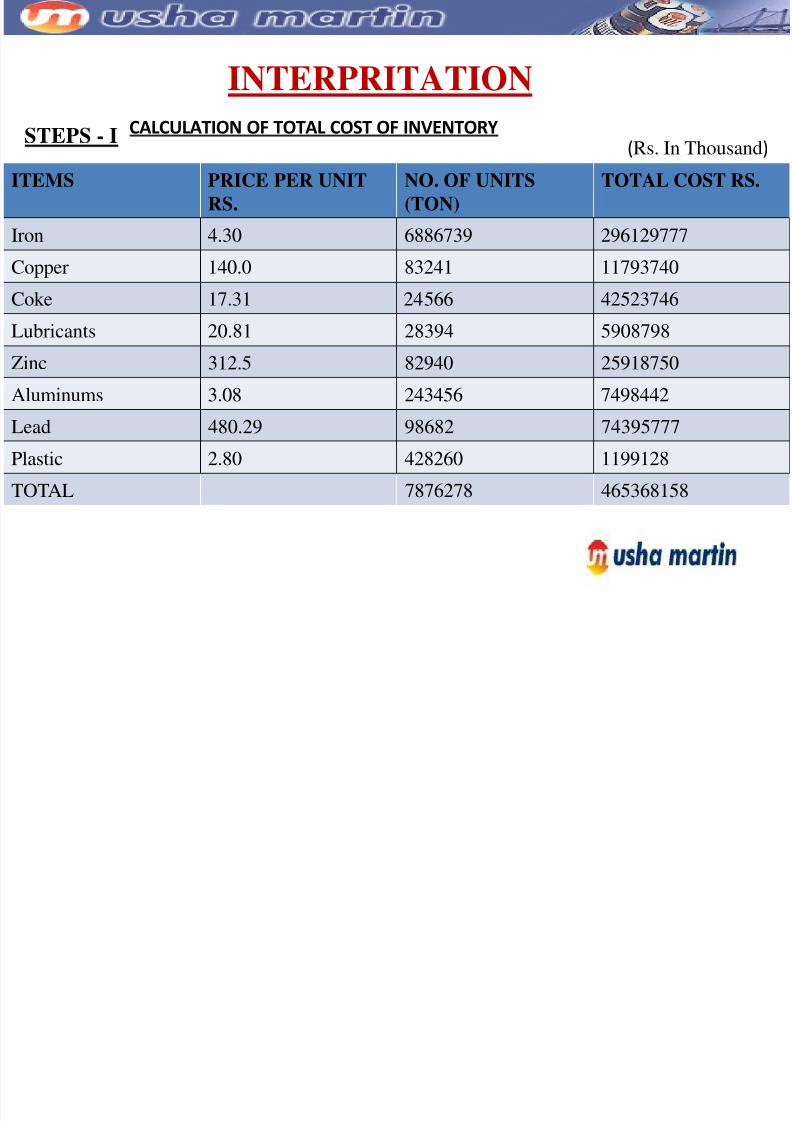

ITEMS PRICE PER UNIT

RS.

NO. OF UNITS

(TON)

TOTAL COST RS.

Iron 4.30 6886739 296129777

Copper 140.0 83241 11793740

Coke 17.31 24566 42523746

Lubricants 20.81 28394 5908798

Zinc 312.5 82940 25918750

Aluminums 3.08 243456 7498442

Lead 480.29 98682 74395777

Plastic 2.80 428260 1199128

TOTAL 7876278 465368158

(Rs. In Thousand)

INTERPRITATION

STEPS - ICALCULATION OF TOTAL COST OF INVENTORY

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 30/36

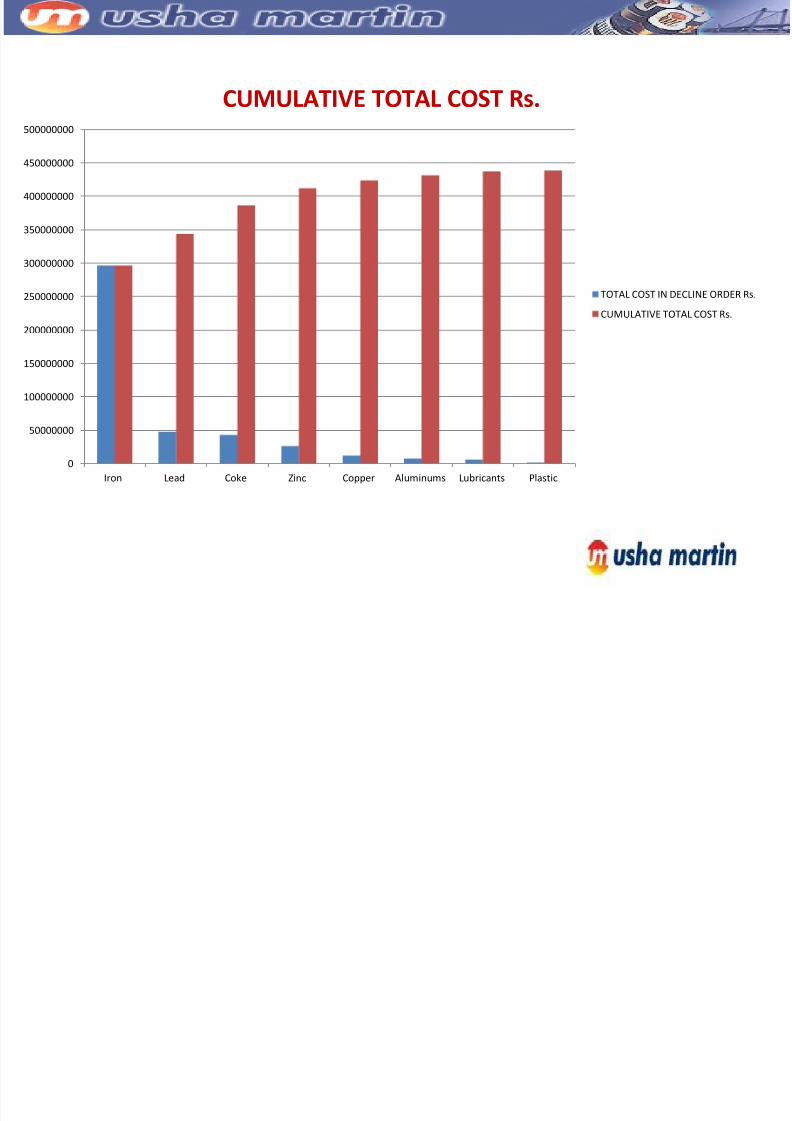

ITEMS TOTAL COST IN

DECLINE ORDER

Rs.

CUMULATIVE

TOTAL COST Rs.

Iron 296129777 296129777Lead 47395777 343525554

Coke 42523746 386049300

Zinc 25918750 411968050

Copper 11793740 423761790Aluminums 7498442 431260232

Lubricants 5908798 437169030

Plastic 1199128 438368158

STEPS - II

CALCULATION OF CUMULATIVE COST

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 31/36

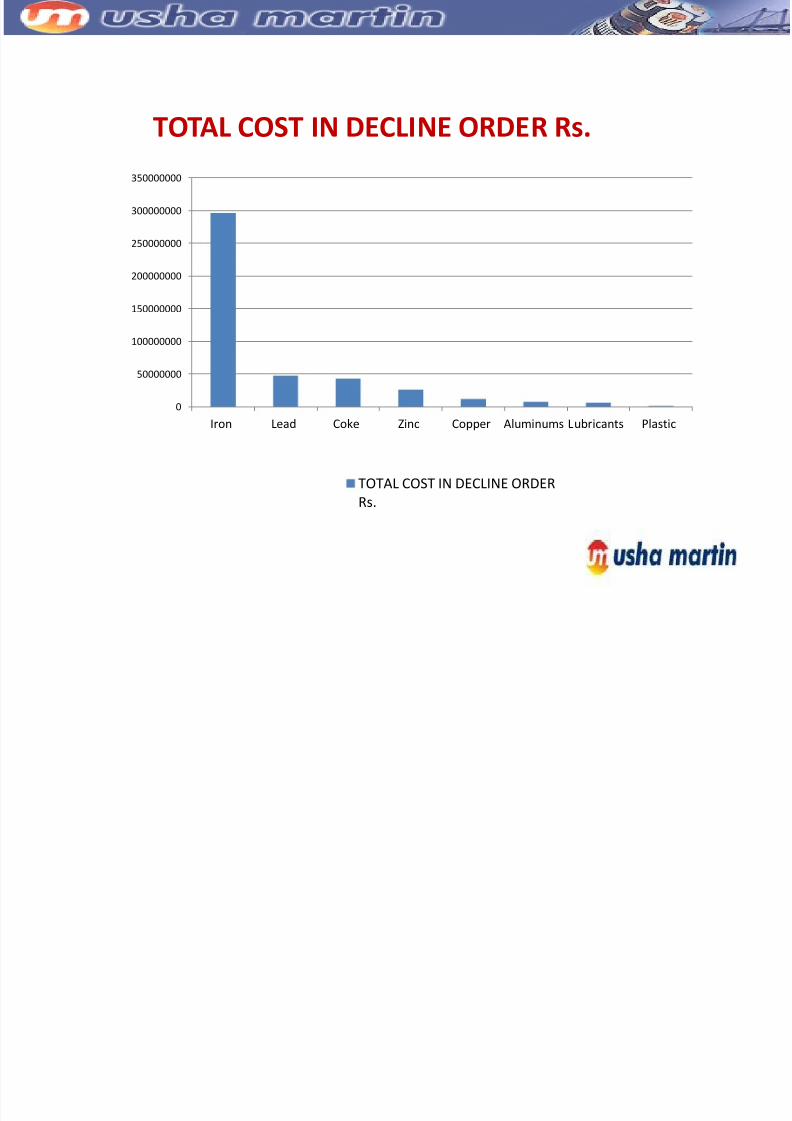

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

Iron Lead Coke Zinc Copper Aluminums Lubricants Plastic

TOTAL COST IN DECLINE ORDER Rs.

TOTAL COST IN DECLINE ORDER

Rs.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 32/36

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

400000000

450000000

500000000

Iron Lead Coke Zinc Copper Aluminums Lubricants Plastic

TOTAL COST IN DECLINE ORDER Rs.

CUMULATIVE TOTAL COST Rs.

CUMULATIVE TOTAL COST Rs.

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 33/36

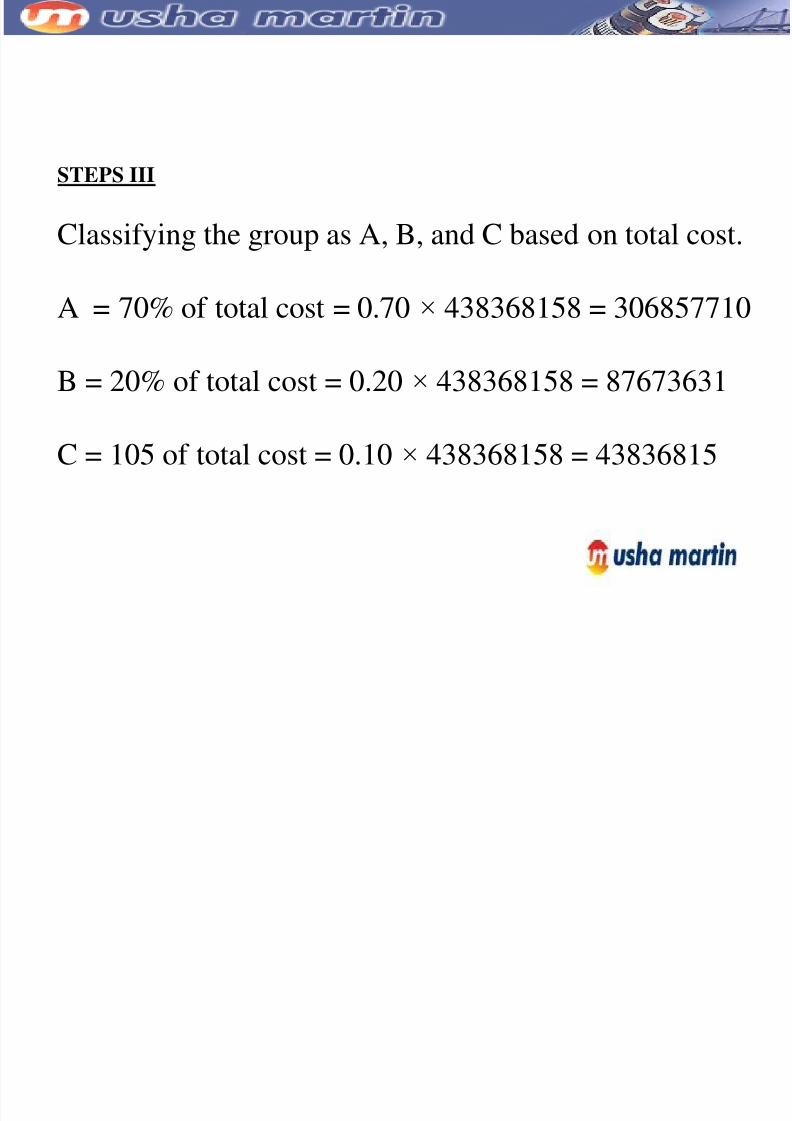

Classifying the group as A, B, and C based on total cost.

A = 70% of total cost = 0.70 × 438368158 = 306857710

B = 20% of total cost = 0.20 × 438368158 = 87673631

C = 105 of total cost = 0.10 × 438368158 = 43836815

STEPS III

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 34/36

UML has achieved phenomenal success with proper

utilization of Inventory Management. Inventory managementis so critical for planning or forecasting for the future needs

and for developing strategic plans to handle the market

situations. It needs a top down approach to structure an

effective way of tackling inventory managing problems.

If UML is to achieve incremental growth and maximize its

market capitalization, it has to give more emphasis on

effective inventory control and use available resources

optimally. UML has to keep itself abreast of new trends in

inventory management and lean manufacturing such as JIT.

CONCLUSION

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 35/36

•I suggested for ABC analysis and ABC analysis gives

more appropriate results and conclusion.

•I suggested little changes in the inventory managementsystems.

SUGGESTION

8/3/2019 ABHASH RANJAN

http://slidepdf.com/reader/full/abhash-ranjan 36/36