AAII Orange County Chapter · Multi-Asset Class Global Equities Return Period Annual Return Annual...

33

Osborne Partners Capital Management, LLC AAII Orange County Chapter February 22, 2020

Transcript of AAII Orange County Chapter · Multi-Asset Class Global Equities Return Period Annual Return Annual...

Osborne Partners Capital Management, LLC

AAII Orange County Chapter

February 22, 2020

Osborne Partners Capital Management, LLC

2

Justin McNichols, CFA – Chief Investment Officer • Chief Investment Officer and Principal for OPCM with over 25 years of experience. • Previously, the head of equity research at Wells Fargo Asset Management. • Additionally at Wells, managed over $1 billion in separate account and mutual fund assets. • A CFA Charterholder and a member of the CFA Society San Francisco and CFA Institute. • Earned a Bachelor of Arts degree in Economics in three years and a M.B.A. in Finance from the

University of California at Irvine.

3

• The 2020s – The Great Normalization

• Introduction to Osborne Partners

Agenda

The Last 20 Years of Bubbles and

What It Means for the Future

Justin W. McNichols, CFA – Chief Investment Officer

4

Two Decades of Asset Bubbles, Easy Money,

and Severe Bull and Bear Markets

5

2000 Starts With a Generational Internet Bubble

That Causes a Major Recession

6

The Internet Bubble Causes a Major Recession,

Prompting The Federal Reserve To Enact Easy Monetary Policy

7

Easy Money Causes Bubble #2 –

A Housing Bubble That Pops in 2005

8

Continued Easy Money Causes Bubble #3 –

Credit That Pops In 2007

9

Global Easy Money Creates Bubble #4 –

Natural Resources Which Pops In 2008

10

Easy Money Result –

An Unprecedented Triple Bubble Implosion

11

Four Types of Recessions

12

Earnings Recession: 1990, 2001, 2015 • Recession caused by any number of short-term factors

• Corporate earnings slightly negative for at least two quarters

• Economy Bottoms less than 1-2 years after peaking

• Equities usually fall by less than 20%

Economic Recession: Today? • Recession caused by Economic Old Age

• Corporate Earnings are negative for at least two quarters

• Economy Bottoms 1-2 Years After Peaking

• Equities fall around 20-30%

Federal Reserve Recession: 1969-1970, 1980-1982 • Recession caused by the Federal Reserve Raising Interest Rates too quickly or for too long

• Corporate earnings usually fall for more than two quarters

• Equities can fall more than 30%

Credit Recession: 2007-2009 • Major recession caused by a lengthy period of easy money, spike in consumer and

corporate debt levels

• Corporate earnings can fall for years

• Economy bottoms years later and the economic rebound is long and tepid

• Equities can fall more than 40%

What Happened Coming Out of the

2007-2009 Major Credit Recession

13

1) The U.S. quickly reduces interest rates to a 0% Fed Funds.

2) The U.S. exits the global recession first before most of the rest of the

world.

Results in three major factors:

1) The U.S. dollar starts a decade long rise of 40% versus other currencies.

• Result: U.S. equities outperform Foreign equities.

• Result: Natural Resources that are priced in U.S. dollars face multi-

year headwind.

2) Economic growth is slow for many years:

• Result: Any company with higher earnings growth is consistently bid

higher – Amazon, Netflix, cloud software, tech in general.

3) Persistent Record Low Interest Rates:

• Result: Income investors bid up “bond proxies” like utilities,

consumer staples, and REITs to levels rarely seen

Valuations Spike and Risk Spikes!

Valuations For High Growth Companies = High Risk

14

Valuations for Bond Proxies = High Risk

15

Result Twenty Years Later – Slow Build Up of Extremes

16

• Abnormal Returns for all asset classes

• Strong returns concentrated in one asset class and only a few sectors

• Recency bias causes herd mentality and overvaluation continues

An investor cannot invest directly in an index. Please see the end of this presentation for more information regarding this table. The Alternatives asset class is since 1987.

Last 10 Years Since 1977 Return

Annual Return Annual Return Difference

------------- ------------- -------------

Domestic Equities 13.6 11.4 2.2

Foreign Equities 5.0 9.6 (4.6)

Natural Resources (4.7) 5.9 (10.6)

Real Estate 8.9 10.7 (1.8)

Alternatives 4.5 6.9 (2.4)

Fixed Income 3.1 6.9 (3.8)

Equal Weighted 5.3 9.6 (4.3)

Osborne Partners Capital Management, LLC.PERFORMANCE COMPARISON TABLE

Asset Class Return Divergence From The Long-Term Average

12/31/2019

Our Present Environment – Five Extremes

Extreme #1 = U.S. Equities versus Foreign Equities

17

Our Present Environment – Five Extremes

Extreme #2 = U.S. Growth Equities versus Value Equities

18

Our Present Environment – Five Extremes

Extreme #3 = U.S. Dollar Versus Foreign Equities and Natural Resources

19

Our Present Environment – Five Extremes

Extreme #4 = Hedging No Longer Useful

20

Our Present Environment – Five Extremes

Extreme #5 = Interest Rates

21

What To Expect From The 2020s

“The Great Normalization”

22

1) The U.S. dollar appreciation slows or ceases:

• Demand increases for previously underperforming, but improving

currencies and economies

• Foreign Equities and Natural Resources headwinds are reduced.

2) Countries outside the U.S. begin to post earnings growth at or above the U.S.

• 2020 estimated EPS growth for U.S. is similar to the rest of the world.

3) Extreme valuation differential reverses

• U.S. trades at a 30% premium to ROW

• U.S. trades at a 40% premium to Emerging Markets

• U.S. trades at a 30% premium to Germany

• U.S. trades at a 25% premium to Japan and Brazil

• U.S. trades at the same valuation as India

4) Natural Resources: Improved supply, rebounding demand, no USD headwind.

What To Expect From The 2020s

“The Great Normalization”

U.S. Dollar Appreciation Slows

23

What Happens To Foreign Equities if the U.S. dollar appreciation slows or ceases?

What To Expect From The 2020s

“The Great Normalization”

Foreign Equities Begin To Outperform U.S. – Earnings Growth and Valuation

24

2020 Estimated Earnings Growth = U.S. 8-10%, Rest Of The World 8-10%

2020 P/E Premium U.S. versus ROW = 32% (One of the highest in decades)

What To Expect From The 2020s

“The Great Normalization”

Value Outperforms Growth – Investors Overweight Growth

25

Growth equities are trading at a 20-year valuation high of nearly 25x earnings

Growth equities trade at a 60% premium to value equities as value earnings are bottoming:

What To Expect From The 2020s

“The Great Normalization”

Natural Resources in the 2020s

26

Natural Resources versus the U.S. Dollar:

What To Expect From The 2020s

“The Great Normalization”

Natural Resources in the 2020s

27

Natural Resources Example Inventory Levels:

Source: The International Coffee Organization

What To Expect From The 2020s

“The Great Normalization”

Fixed Income in the 2020s

28

The Consensus Is Interest Rates Are Staying At Record Lows Or Headed Lower.

Over the Past 30 Yrs, the Average Inflation Rate Is 2.4% and the Average Fed Funds Rate Is 3.0%.

If Inflation Is at the 30 Year Average Today, Why Is the Fed Funds 1.50-1.75%?

Do Interest Rates Belong at These Levels?

What To Expect From The 2020s

“The Great Normalization”

How To Invest?

1) Avoid overweighting U.S. Equities, along with HiGroHiVal and Bond Proxies:

29

What To Expect From The 2020s

“The Great Normalization”

How To Invest?

30

2) Use a Multi-Asset Class Discipline. Delivers Equity-like Returns with Less Risk

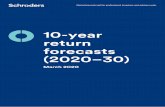

Simple Equal Weighted Multi-Asset Class Portfolio:

Returns Achieved With Long-Term Standard Deviation (Risk) of 10.7%.

The Long-Term Standard Deviation of Global Equities is 19.0%

The Multi-Asset Class level of risk is 44% less than a portfolio of 100% global stocks.

Multi-Asset C lass Global Equities Return

Period Annual Return Annual Return Capture

------------- ------------- ------------- -------------

3 Year 7.2 12.5 58%

5 Year 4.5 8.6 52%

7 Year 4.8 10.1 47%

10 Year 5.3 9.3 57%

20 Year 5.9 5.1 116%

43 Year 9.6 10.6 90%

Multi-Asset Class Return Capture Versus Global Equit ies

12/31/2019

Please see the presentation disclosures for more information regarding this table.

31

Osborne Partners provides sophisticated investment management with

active financial planning for wealthy individuals, families, and institutions.

The OPCM Difference

• History – Over 82 years. One of the oldest firms in the U.S.

• Discipline – Customized, actively managed multi-asset class, using individual

securities

• Team – CFA® Charterholders and CFP ® Practitioners on the team

• Service – Long term annual client retention routinely 99%

• Performance – A history of outperformance with low downside capture

CFA Institute does not endorse, promote or warrant the accuracy or quality of Osborne Partners Capital Management LLC. CFA® and Chartered Financial Analyst® are registered

trademarks owned by CFA Institute.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™ and federally registered CFP (with flame design) in the U.S.,

which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Presentation Disclosures Osborne Partners Capital Management, LLC (OPCM) is registered with the Securities and Exchange Commission as a Registered Investment

Adviser (RIA). Registration is not meant to denote any form of recommendation or endorsement by the SEC or state securities regulators.

This presentation is offered for informational purposes only by OPCM and should not be considered investment advice. The opinions expressed

herein are strictly those of Osborne Partners Capital Management, LLC.

Past performance is not indicative of future results. Inherent in any investment is the possibility of loss. None of the data presented herein

constitutes a recommendation or solicitation to invest in any particular investment strategy and should not be relied upon in making an

investment decision. Each investor should select asset classes for investment based on his/her own goals, time horizon and risk tolerance.

OPCM does not provide tax or legal advice. This presentation should not be considered a comprehensive review or analysis of the topics

discussed today. These materials are not a substitute for consulting with your legal and/or financial professional(s) in a one-on-one context

whereby all the facts of your situation can be considered in their entirety.

Despite efforts to be accurate and current, this presentation may contain out-of-date information. Additionally, OPCM will not be under an

obligation to advise you of any subsequent changes.

Information provided during this presentation is provided “as is” without warranty of any kind, either express or implied, including, without

limitation, warranties and merchantability, fitness for a particular purpose, or non-infringement. OPCM assumes no liability or responsibility for

any errors or omissions in the content of the presentation.

CFA Institute does not endorse, promote or warrant the accuracy or quality of Osborne Partners Capital Management, LLC. CFA® and Chartered

Financial Analyst® are registered trademarks owned by CFA Institute.

In the Performance Comparison Table on slides 16 and 30, the following benchmarks are used to represent each asset class: Fixed Income –

Barclays US Aggregate Bond Index (1977-1999), Barclays US Govt/Credit Interm Bond Index (2000-2019); Domestic Equities – S&P 500; Foreign

Equities – MSCI EAFE (1977-2000), MSCI World ACWI ex US (2001-2019); Natural Resources – GSCI (1977-1991), Bloomberg Commodity

(1992-2019); Real Estate – NAREIT (1977-2004), NAREIT Global (2005-2019); Alter-natives – Hennessee Market Hedge Fund Index (1987-

1999), HFRI Fund Weighted Index (2000-2007), HFRI Asset Weighted Index (2008-2019). The Equal Weighted Portfolio represents a hypothetical

portfolio equally weighted in each asset class of the corresponding benchmark. The Global Equities return on slide 30 is the average weight of

the S&P500 and the MSCI World ACWI ex. US.

33