A3 Medicare Tax and NIIT - mntaxclass.commntaxclass.com/files/A3_Medicare_Tax_and_NIIT.pdf ·...

104

mntaxclass.com 1 Post-2012 Net Investment Income Tax Chapter 3 2

Transcript of A3 Medicare Tax and NIIT - mntaxclass.commntaxclass.com/files/A3_Medicare_Tax_and_NIIT.pdf ·...

mntaxclass.com

1

Post-2012 Net Investment Income

Tax

Chapter 3

2

3.8% “Net Investment

Income”Tax

New IRS Form 89603

New Code §1411

4

5

Final Regulation Preamble

§1411 ‐‐

Imposition

of tax

Reg. § 1.1411‐0: Table of contents of provisions

applicable to section 1411.

Reg. §1.1411‐1: General rules.

Reg. §1.1411‐2: Application to individuals.

Reg. §1.1411‐3: Application to estates and trusts.

Reg. §1.1411‐4: Definition of net investment income.

Reg. §1.1411‐5: Trades or businesses to which tax applies.

Reg. §1.1411‐6: Income on investment of working capital

subject to tax.

Reg. §1.1411‐7 [Reserved. Exception for dispositions of

interests in partnerships and S corporations.]

Reg. § 1.1411‐8: Exception for distributions from qualified

plans.

Reg. §1.1411‐9: Exception for self‐employment income.Reg. §1.1411‐10: Controlled foreign corporations and passive foreign

investment companies.

Update

Investment Income (before deductions)

CategoryOne

Gross Income – Interest, Dividends, Annuities, Royalties, and Rents that are:

• Nonbusiness (investment)• Passive business income• Trading business income

CategoryTwo

Other Gross Income that is:• Passive business income or• Trading business income

Category Three

Net Gain from the disposition of property that:

• Nonbusiness (invest. or personal)• Passive business• Trading business

6

Investment Income (before deductions)

CategoryOne

Gross Income – Interest, Dividends, Annuities, Royalties, and Rents that are:

• Nonbusiness (investment)• Passive business income• Trading business income

CategoryTwo

Other Gross Income that is:• Passive business income or• Trading business income

Category Three

Net Gain from the disposition of property that:

• Nonbusiness (invest. or personal)• Passive business• Trading business

7

Investment Income (before deductions)

CategoryOne

Gross Income – Interest, Dividends, Annuities, Royalties, and Rents that are:

• Nonbusiness (investment)• Passive business income• Trading business income

CategoryTwo

Other Gross Income that is:• Passive business income or• Trading business income

Category Three

Net Gain from the disposition of property that:

• Nonbusiness (invest. or personal)• Passive business• Trading business

8

Tax Calculation

9

3.8% of lesser of:• NII

• MAGI > threshold

10

MAGI > threshold• $250,000 for MFJ• $125,000 for MFS• $200,000 for all others

Same for a short year but not if a change in annual accounting period.

11

MAGI

AGI + 911 Exclusion as adjusted.

+ Possible adjustment for PFICs or CFCs.

12

• $200,000 for Single

X wages = $350,000NII = $10,000

MAGI = $360,000- 200,000$160,000

13

• $200,000 for Single

X wages = $350,000NII = $10,000

MAGI = $360,000- 200,000$160,000

$10,000 x 3.8% = $380

14

• $200,000 for Single

X wages = $350,000NII = $10,000

MAGI = $360,000- 200,000$160,000

$10,000 x 3.8% = $380$150,000 x .9% = $1,350

15

Example 2

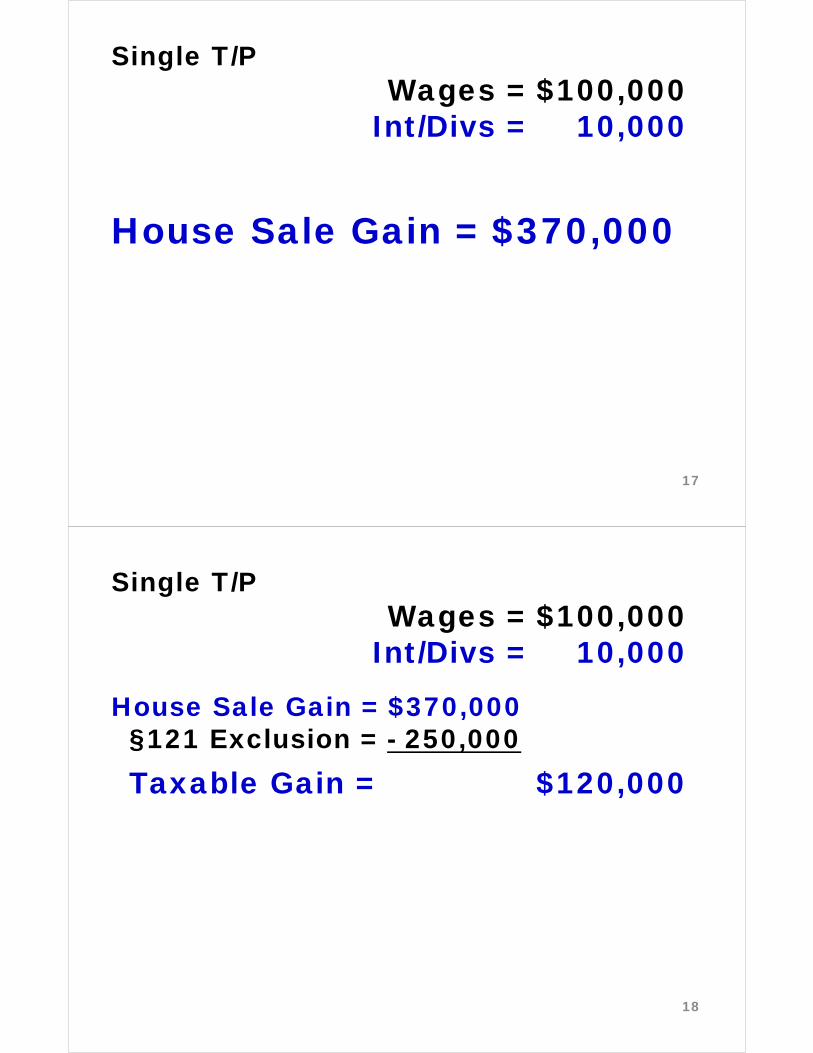

Single T/PWages = $100,000

Int/Divs = 10,000

16

Single T/PWages = $100,000

Int/Divs = 10,000

House Sale Gain = $370,000

17

Single T/PWages = $100,000

Int/Divs = 10,000

House Sale Gain = $370,000§121 Exclusion = - 250,000Taxable Gain = $120,000

18

Single T/PWages = $100,000

Int/Divs (Cat. 1 NII) = 10,000

House Sale Gain = $370,000§121 Exclusion = - 250,000

Taxable Gain (Cat. 3 NII): 120,000MAGI = $230,000

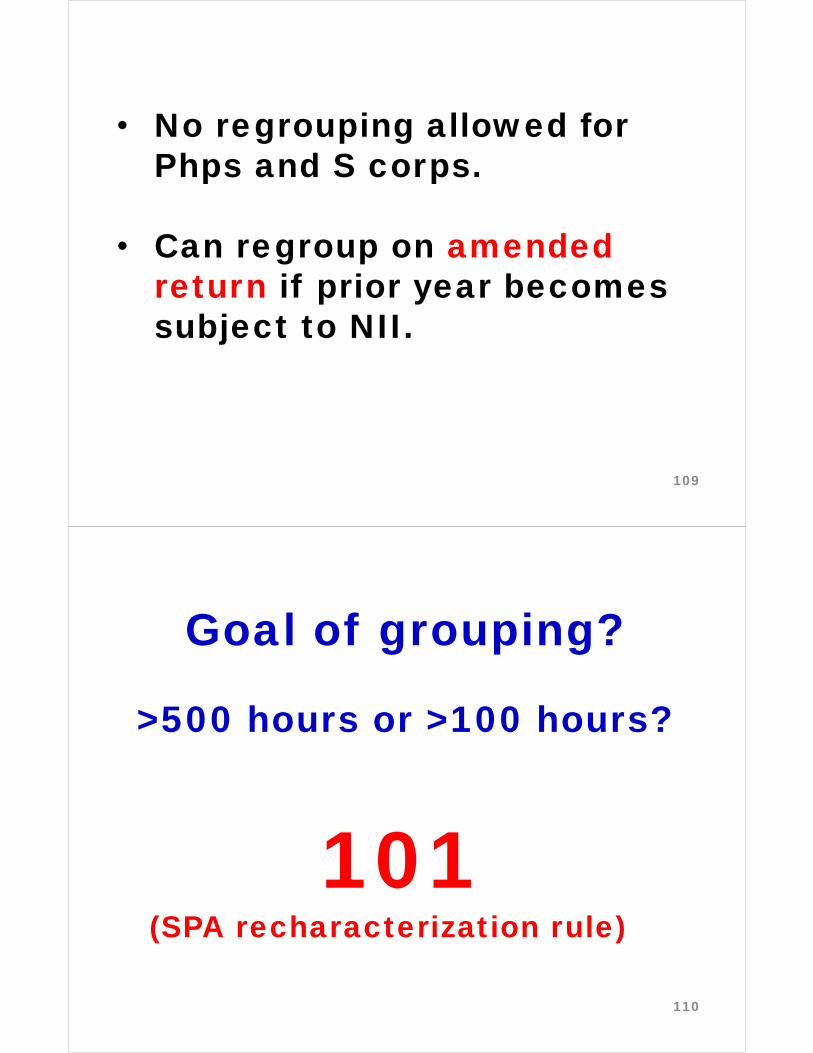

- 200,000Taxable NII = $30,000

NIIT = $1,140 (3.8% x $30,000)19

2013 Top rates “Net Investment Income”:

LTCG: 23.8% (20 + 3.8)Dividends: 23.8%NII: 43.4% (39.6 + 3.8)

20

Wages $230,000Interest $20,000AGI $250,000Married under age 652 Children age 15Standard Deduction

Regular Tax $49,682AMT $921Total Tax $50,603Tax Bracket 28%

21

Add $10,000

of Wages

22

Wages $240,000Interest $20,000AGI $260,000

Regular Tax $52,939AMT $1,164NIIT 380Total Tax $54,483 vs. $50,603 Tax Bracket 33%

23

Tax Increase = $3,880

Marginal Rate on $10,000 = 38.8% (35% AMT + 3.8% NIIT) 24

Investment Income Does NOT Include

• Items excluded from gross income- e.g., muni bond interest, excluded principal residence gain

• Distributions from retirement plans

25

Retirement Plan Dist.• A qualified pension, stock bonus, or

profit-sharing plan (401(a))• A qualified annuity plan (403(a)) • A tax-sheltered annuity (403(b))• An individual retirement account

(IRA) (408)• A Roth IRA (408A)• A deferred compensation plan of a

State and local government or a tax-exempt organization (457(b))

26

Investment Income Does NOT Include

Income subject to SE Tax

27

Not NII

28

• Wages• Schedule C Income• Schedule F Income• Alimony• Social Security Benefits• Unemployment Comp• Alaska Permanent Fund Dividends

Nonresident aliens are not subject

to the Net Investment

Income Tax.

29

IRS DraftForm8960

(Elections)

30

31

Draft

1

1 Election to treat NRA as resident of the U.S. for joint return purposes.

Final regs. add sec. 6013(h) election for married dual status NRA in year of first becoming U.S. resident.

32

2

2 Irrevocable Election for CFCs and PFICs with QEF election.

The -10(g) election conforms NII with Chapter 1 for CFCs (sec. 951) and PFICs (sec. 1293) 33

Reg. 1.1411-10(g) ElectionFinal Regs.

• An entity-by-entity election.

• Can be made on amended return if S of L open.

• Partnerships and S corps can make the election.

34

Final and Proposed RegulationsPublished

November 26, 2013

35

Major Benefits in Final Regs.• Safe harbors for when rental

real estate is a trade or business.

• Allow <$3,000> net capital loss within limits.

• Allow NOL deductions within limits.

36

• Traders mark-to-market losses are allowed.

• Freed-up passive losses can offset NII

• More generous method of calculating “properly allocable deductions” particularly for itemized deductions.

37

• Simplified methods for sales of Php Interests and S corps. (prop. regs.)

• Clarifications such as the treatment of tax credits, trust and estate income, CRTs, etc.

38

• Must apply final regs. in TYBA 2013

• May apply final or proposed regs. to TYBB 1/1/2014(including 2012 Prop. regs.)

39

The statute applies to tax years beginning

after12/31/2012

40

Category One Investment Income

41

Investment Income (before deductions)

CategoryOne

Gross Income – Interest, Dividends, Annuities, Royalties, and Rents that are:

• Nonbusiness (investment)• Passive business income• Trading business income

CategoryTwo

Other Gross Income that is:• Passive business income or• Trading business income

Category Three

Net Gain from the disposition of property that:

• Nonbusiness (invest. or personal)• Passive business• Trading business

42

CategoryOne

Gross Income – Interest, Dividends, Annuities, Royalties, and Rents that are:

• Nonbusiness (invest.)• Passive business inc.• Trading business inc.

What escapes category one?Nonpassive business income except for trading income.

43

IRS DraftForm8960

(Category One)

44

Draft

45

Category One NII

46

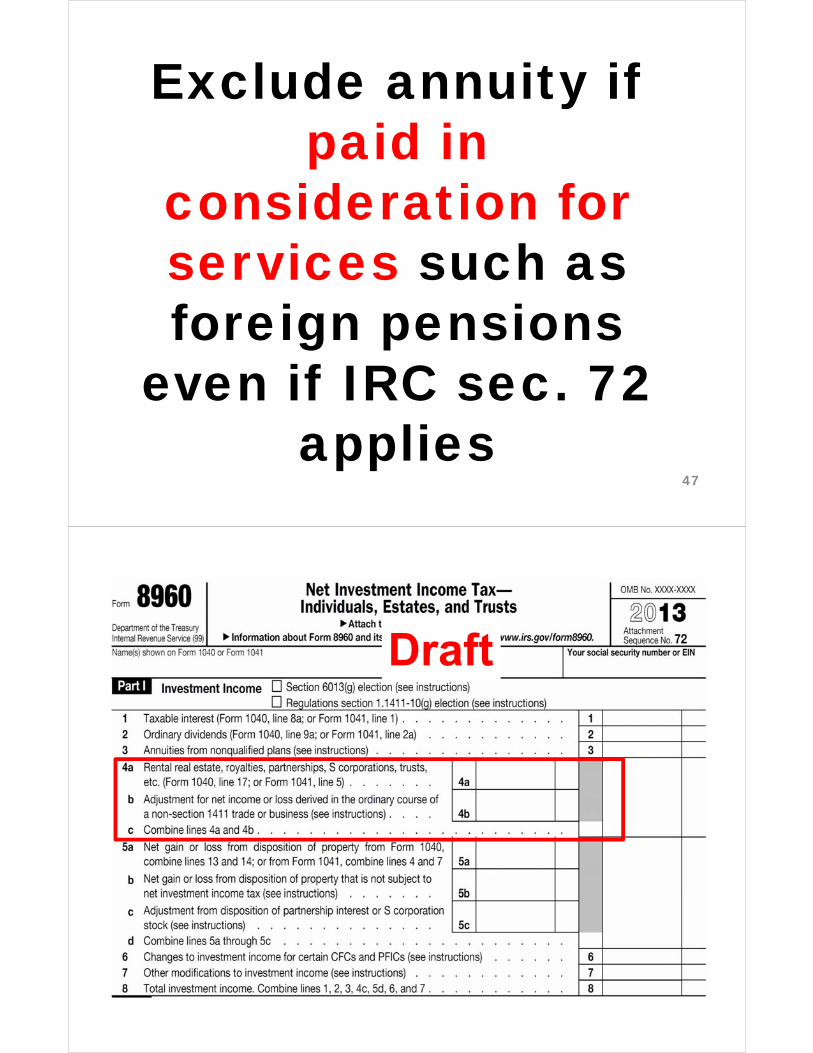

Annuity, Endowment or Life Insurance

Contract

47

Exclude annuity if paid in

consideration for services such as foreign pensions

even if IRC sec. 72 applies

48

Draft

49

Draft Form 8960

50

Draft 2013 Form 1040

Schedule E Income

51

Draft Form 8960

Interest Income NII Exclusions

1) Nonpassive money lending business interest income.

52

2) Self-charged interest• Interest income on loan

to passthrough entity in which the lender materially participates.

(Reg. 1.1411-5(g)(5))

53

• Example: L, a 40% S shareholder, loans $100,000 to S Corporation in which L materially participates.

54

• Exclusion limited to lender’s share of the nonpassive interest deduction.

• No relief if SE tax (HI tax) is reduced.Ex: General Ptr loans..

55

Rental Income in Category One

• Passive trade or business rental income

• Investment rental income—even if nonpassive.

56

Rental Real Estate NII Exclusions

Potenial Nonpassive T or B rental income:• Real Estate Professionals• Self-Rentals• Vacation Rentals

57

When is rental real estate a

trade or business?

58

59

“Commentators cited cases such as [Fackler, Hazard, Lagreide] for the proposition that the activities of a single property can rise to the level of a trade or business.”

60

“The Treasury Department and the IRS agree with commentators that, in certain circumstances, the rental of a single property may require regular and continuous involvement such that the rental activity is a trade or business within the meaning of section 162.”

61

Rental shouldissue1099’s

if T or B treatment

sought

But the rental real estate trade or business must be nonpassive to

escape 141162

63

Safe Harbor For Real Estate Professionals

(REPs)(Reg. sec. 1.1411-4(g)(7))

64

Real Estate Prof. (REP)Per 469(c)(7)

(1) > 50% of personal services are a real property trade or business (RPTB) in which you materially participate

(2) Over 750 hours of services in an RPTB in which you materially participate

65

RPTB sec. 469(c)(7)

• Real property development• Redevelopment • Construction• Reconstruction• Acquisition • Conversion

66

• Rental• Operation• Management• Leasing• Brokerage

67

Final Reg. Relief: The rental is a deemed trade or business if the REP materially participates in the rental real estate for over 500 hours.

Reg. 1.469-9(g) aggregation election may be crucial, and will pull in

investment rentals and LP interests

68

Over 500 hours for five of prior ten years in the rental is also a deemed trade or business for a REP.

Includes pre-2013 years

69

Rev Proc 2011-34contains simplified relief

for late aggregation elections

by real estate professionals.

(Reg. sec. 1.469-9(g) election)

70

Safe harbor also applies to sale gain

71

Failure to meet the >500 hour safe harbor

does not preventtrade or business

treatment for nonpassive rental

real estate of a REPReg. 1.469-9(g) aggregation election remains useful, but avoid net leases

Relief for Self-Rentals

(Reg. sec. 1.1411-4(g)(6))

72

73

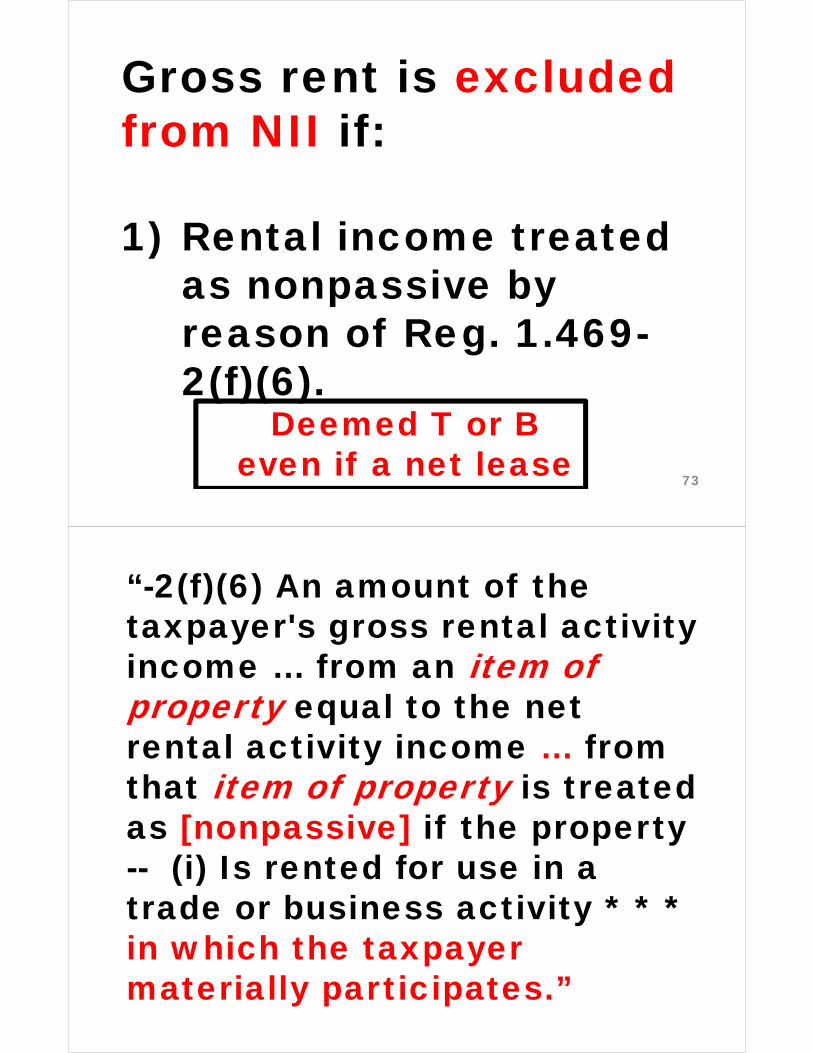

Gross rent is excluded from NII if:

1) Rental income treated as nonpassive by reason of Reg. 1.469-2(f)(6).

Deemed T or B even if a net lease

“-2(f)(6) An amount of the taxpayer's gross rental activity income … from an item of property equal to the net rental activity income … from that item of property is treated as [nonpassive] if the property -- (i) Is rented for use in a trade or business activity * * * in which the taxpayer materially participates.”

SCORP

CPADebbie

100%

ProfitableNonpassive Gross

income

RENT

MateriallyParticipates

Business

Example 15 Pg. 3-30 but opposite

answer

NoGrouping

Escapes NII 75

SCORP

CPADebbie

100%

ProfitableNonpassive Gross

income

RENT

MateriallyParticipates

Business

Debbie is 10% S shareholder

Escapes NII 76

10%

CPADebbie

100%

ProfitableNonpassive Gross

income

RENT

MateriallyParticipates

Business

Debbie is Partner

Escapes NII 77

10%

Php

CCORP

CPADebbie

100%

ProfitableNonpassive Gross

income

RENT

MateriallyParticipates

Business

Debbie is a C corpShareholder

Escapes NII 78

10%

79

2) Rental income alternatively escapes NII as a result of Reg. 1.469-4(d)(1) grouping of the rental with a nonrental T or B activity

SCORP

CPADebbie

100%

ProfitableNonpassive

Activity

RENT

MateriallyParticipates

Business

GROUPAS

ONEBUSINESSACTIVITY

Escapes NII80

SCORP

CPADebbie

100%

LossesNonpassive

Losses

RENT

MateriallyParticipates

Business

GROUPAS

ONEBUSINESSACTIVITY

81

82

The self-rental relief also applies to sale gain

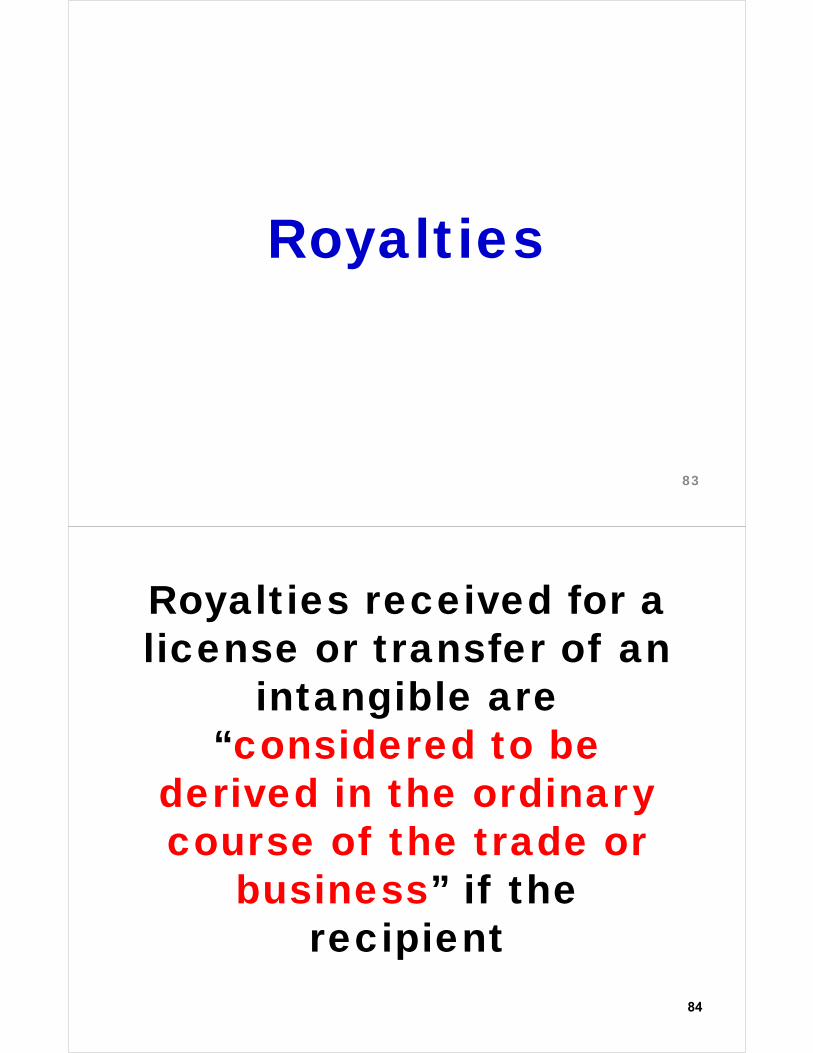

Royalties

83

Royalties received for a license or transfer of an

intangible are “considered to be

derived in the ordinary course of the trade or

business” if the recipient

84

1) Created such property; or

2) Performed substantial services or incurred substantial costs with respect to the development or marketing of such property.

Temp. reg. sec. 1.469-2T(c)(3)(iii)(B)101 hours 85

Category Two Investment Income

86

Investment Income (before deductions)

CategoryOne

Gross Income – Interest, Dividends, Annuities, Royalties, and Rents that are:

• Nonbusiness (investment)• Passive business income• Trading business income

CategoryTwo

Other Gross Income that is:• Passive business income or• Trading business income

Category Three

Net Gain from the disposition of property that is:

• Nonbusiness (invest. or personal)• Passive business• Trading business

87

CategoryTwo

Other Gross Income that is:• Passive business income

or• Trading business income

What escapes category two?Nonpassive business income (except for trading income), and investment income.

88

Examples

89

In Category Two: Passivelimited partner LP’s income from a trucking business.

Excluded from NII: Nonpassive limited partner LP’s income from trucking business.

IRS DraftForm8960

(Category Two)

90

91

Draft

92

Draft Form 8960

93

Draft 2013 Form 1040

Schedule E Income

94

Draft Form 8960

95

Final 2013 K-1

96

Final 2013 K-1 Box 20

Y Net Investment Income

No K-1 Instructions Yet

97

98

Line 4b Adjustment:

Business income of general partners whether passive or nonpassive (SE Income)

99

GP, K-1, Line 1 business incomeof $100,000 (SE Income)

100

$100,000

- $100,000Investment Income $0

$100,000 Passive Bus. Inc. -- LP <100,000> Nonpassive Bus. Loss -- GP

101

+$100,000

$0

Investment Income = $100,000

Line 4b Adjustment:

Business income of limited partners who materially participate

102

Limited PhpXYZ Trucking

Business

GP X

1%1,000 Hrs.General Partner

Focus on Limited Partner (LP) Y

SE Income

LPY

99%LimitedPartner

Zero Hours

No SE Income

103

No NII-SE & Nonpassive

NII-Passive

What if:Limited Partner Y also

owns a controlling interest in a grocery store

partnership that Y participates in for 1000

hours 104

In prior years, Y did not bother to group the XYZ LP interest, because it was profitable.

105

Consider one-shot

regrouping election

3-34106

Limited PhpXYZ Trucking

Business

GP X

1%1,000 Hrs.

Y With Grouping

LPY

99%Zero Hours

No SE Inc.

No NII--Nonpassive

107

Regrouping in Final Regs.• Rejected fresh-start for

everyone.

• Can regroup in first post-2012 year in which NII applies –follow Rev. Proc. 2010-13 procedure.

108

• No regrouping allowed for Phps and S corps.

• Can regroup on amended return if prior year becomes subject to NII.

109

Goal of grouping?

>500 hours or >100 hours?

110

101(SPA recharacterization rule)

• Written statement attached to original return.

• The names, addresses, and EINs, if applicable, for the business activities or rental activities being grouped

111

Rev. Proc. 2010-13 Grouping Requirements

• A declaration that the grouped activities constitute an appropriate economic unit

112

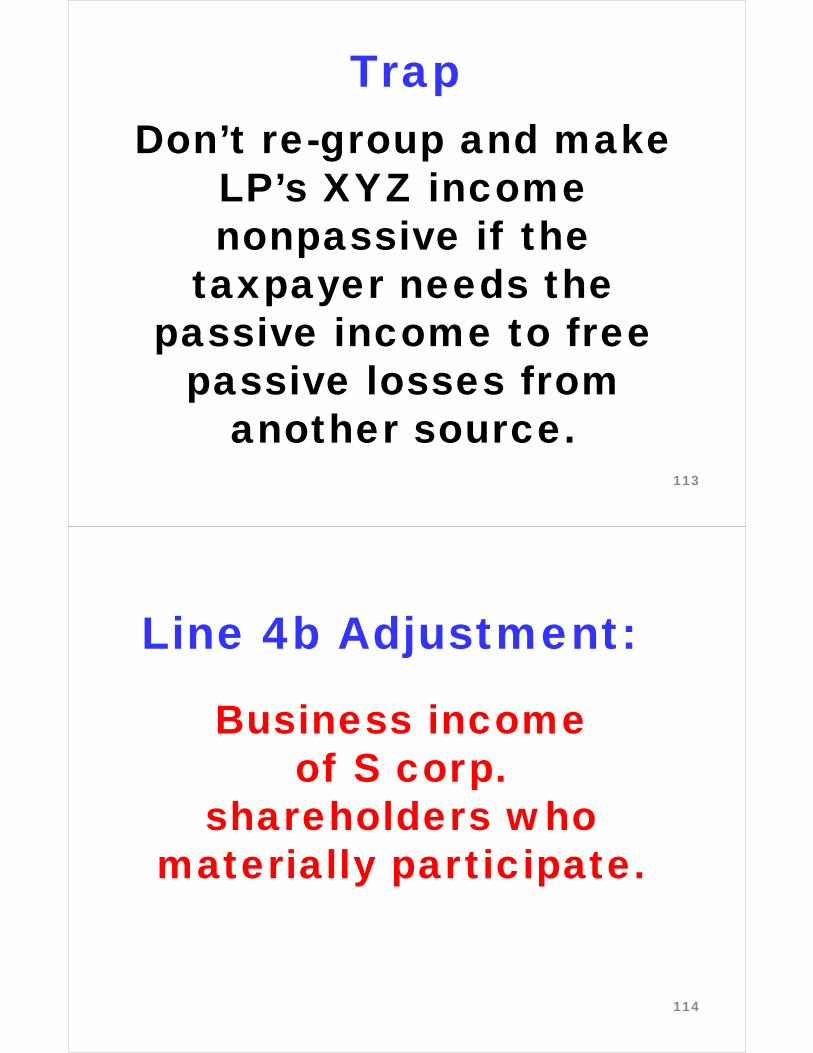

Don’t re-group and make LP’s XYZ income nonpassive if the

taxpayer needs the passive income to free

passive losses from another source.

113

Trap

Business income of S corp.

shareholders who materially participate.

Line 4b Adjustment:

114

Z

0 Hrs

X

1,000 hrs

No SE Income No SE Income

S CorporationTrucking Business

Profitable

NII -- passiveNot NII -- nonpassive

115

Category ThreeInvestment Income

116

Investment Income (before deductions)

CategoryOne

Gross Income – Interest, Dividends, Annuities, Royalties, and Rents that is:

• Nonbusiness (investment)• Passive business income• Trading business income

CategoryTwo

Other Gross Income that is:• Passive business income or• Trading business income

Category Three

Net Gain from the disposition of property that is:

• Nonbusiness (invest. or personal)• Passive business• Trading business

117

Category Three

Net Gain from the disposition of property thatis:

• Nonbusiness (invest. or personal)

• Passive business• Trading business

What escapes category three?

Nonpassive business gain except for trading assets.

118

IRS DraftForm8960

(Category Three)

119

120

Draft

121

122

Draft 2013 Form 1040

Examples of Category Three NII

123

• Gains from the sale of stocks, bonds, and mutual funds.

• Capital gain distributions from mutual funds.

• Gains from sale of principal residence in excess of exclusion

124

• Gain from the sale of investment land.

• Gains from the sale of passive trade or business rental real estate.

• Gains from investment rental real estate, even if nonpassive.

125

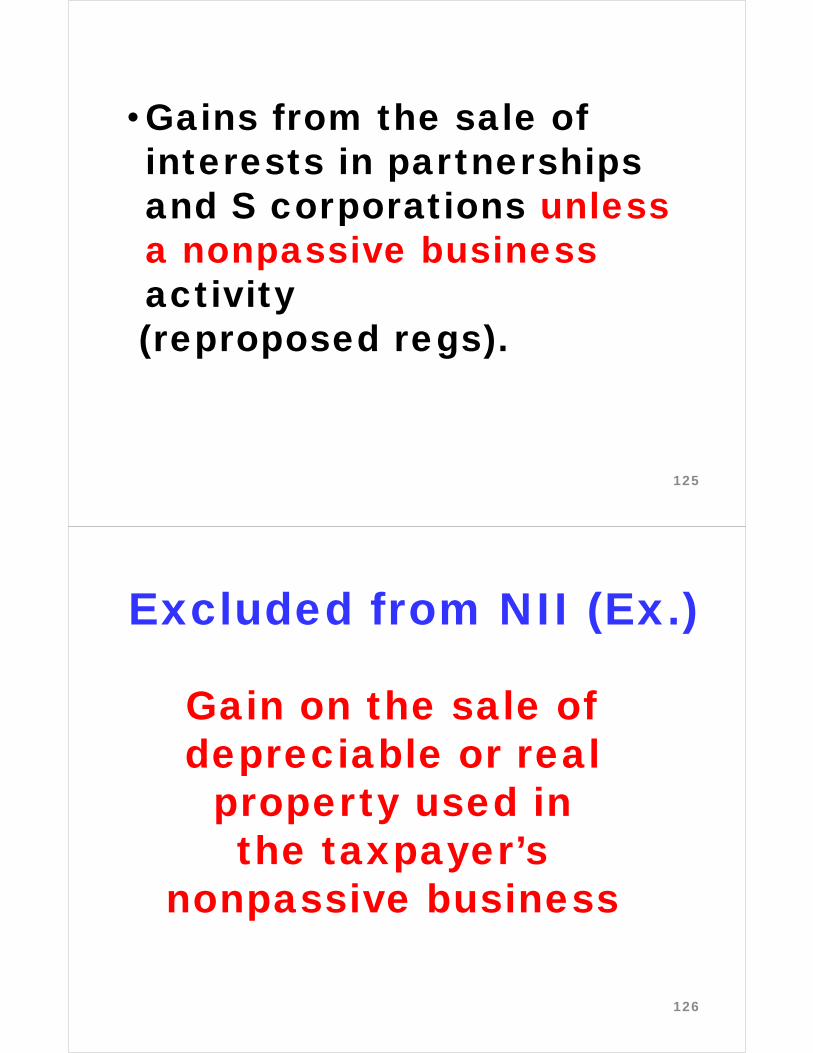

• Gains from the sale of interests in partnerships and S corporations unless a nonpassive business activity(reproposed regs).

Excluded from NII (Ex.)

Gain on the sale of depreciable or real

property used inthe taxpayer’s

nonpassive business

126

Installment Sales

127

Character of gain is determined

in the year of sale

128

For example, for an installment sale of

investment land pre-2013, recognized gains in post-2012 years are category three gain.

Reg. 1.1411-4(d)(4)(i)(C) Example 2

129

What if a pre-2013 installment sale of a

nonpassivebusiness use asset?

NOT NII in post-2012

Years

130

Ex: AD Auto Dealership Partnership General Partner A is a 40% partner who materially participates in the AD business.

D, 60% partner, does not materially participate in the AD business.

131

In 2012, dealership sells on the installment method, a dealership facility, and realizes a gain of $3.5 million.

Partners allocable Share:2012 Gain Rec.

2013 Gain Rec.

NIIIn 2013?

Ptr A $90,000 $90,000

Ptr D $135,000 $135,000

132

In 2012, dealership sells on the installment method, a dealership facility, and realizes a gain of $3.5 million.

Partners allocable Share:2012 Gain Rec.

2013 Gain Rec.

NIIIn 2013?

Ptr A $90,000 $90,000 NO

Ptr D $135,000 $135,000 YES

133

Same facts but assume that A died January 1, 2013 and A’s estate recognizes $135,000 of the installment gain as IRD.

The IRD retains its character as nonpassive business gain so no NII to the estate on the gain.

134

Same relief for a 2011 installment sale of rental

real estate by a real estate professional who

materially participated in the

pre-2013 trade or business rental.

135

Rev Proc 2011-34contains simplified relief

for late aggregation elections

by real estate professionals.

(Reg. sec. 1.469-9(g) election)

Whatabout

netlosses?

136

Final Regs treat IRC sec. 165 net losses

as“properly allocable

deductions” rather than category

three losses137

Thus a net <$3,000> capital loss may be

allowed as a “properly allocable deduction” against investment income.

138

Capital loss carryovers, within limits, can reduce subsequent year

category three gain.

139

A pre-2013 capital loss carryover can offset post-2012 Cap Gain. See Reg.

1.1411-4(d)(3)(ii) Example 3

140

Example

In 2013 Abby:

(1) Sells Apple stock for STCG of $19,000

(2) Sells Nonpassive Php. interest for LTCL <$19,000>

141

Draft 2013 Form 1040

0

Form 1040 Schedule D:

Stock STCG $19,000 (NII)

Php LTCL <$19,000> (Not in NII)

IRC Chapter 1

142

143

$0

+19,000Stock Gain $19,000

Adjustment

None of the <$19,000> nonpassivebusiness loss is allowed for NIIT purposes.

Draft Form 8960

1

1

144

Prop. Reg. 1.1411-4(d)(B) Example

A, single Year 1:(1) sells stock for STCG of $4,000

(2) Sells Nonpassive Php. interest for LTCL <$19,000> Not allowed for NIIT

145

Draft 2013 Form 1040

<$3,000>

Form 1040 Schedule D:

Stock STCG $4,000 NII

Php Sale Loss <$19,000> Not NII

LTCL Carryforward of <$12,000>

IRC Chapter 1

146

147

<$3,000>

+7,000Stock Gain $4,000

Adjustment

None of the <$19,000> nonpassivebusiness loss is allowed for NIIT purposes.

Draft Form 8960

1

1

148

Prop. Reg. 1.1411-4(d)(B) Example

A, Year 2:

Year 1 carryforward net capital loss of <$12,000> of which <$3,000> is allowed for Chapter 1 purposes

149

Draft 2013 Form 1040

<$3,000>

Form 1040 Schedule D:

LTCL <$12,000>

LTCL Carryforward of <$9,000>

IRC Chapter 1

150

151

<$3,000>

+3,000$0

Adjustment

None of the Year 1 <$12,000> remaining nonpassive business loss is allowed for NIIT purposes.

Draft Form 8960

1

1

152

Prop. Reg. 1.1411-4(d)(B) Example

A, Year 3:(1) $5,000 short-term capital gain

on nonpassive business asset

(2) <$1,000> STCL on stock sale

(3) <$9,000> LTCL carryforwardfrom Year 2.

153

Draft 2013 Form 1040<$3,000>

Form 1040 Schedule D:

STCG $5,000 (not in NII)

STCL Stock Sale <$1,000> (in NII)

LTCL Carryforward <$9,000> (not in NII)

LTCL Carryforward of <$2,000>

IRC Chapter 1

154

155

<$3,000>

+$2,000$<$1,000>

Adjustment

• <$1,000> stock sale loss is allowed as a deduction for NIIT purposes.

• $5,000 gain is not in NII

• <$9,000> remaining nonpassive business loss does not reduce NII

Draft Form 8960

1

1

156

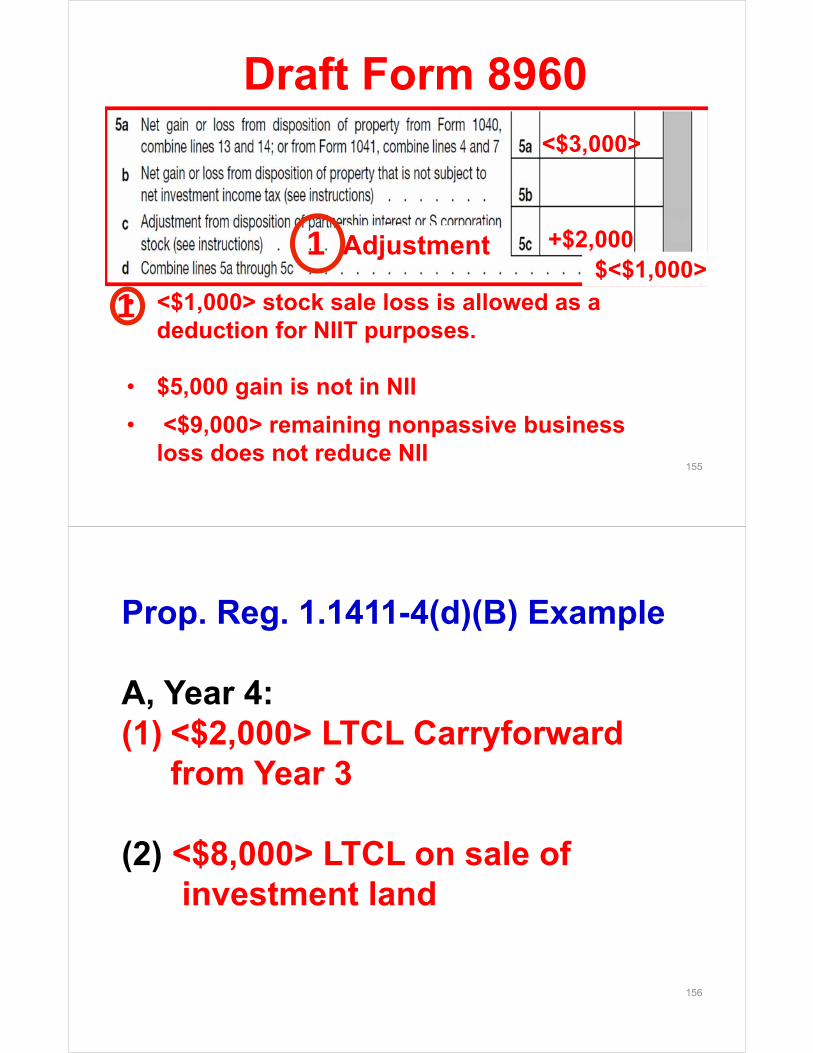

Prop. Reg. 1.1411-4(d)(B) Example

A, Year 4:(1) <$2,000> LTCL Carryforward

from Year 3

(2) <$8,000> LTCL on sale of investment land

157

Draft 2013 Form 1040<$3,000>

Form 1040 Schedule D:

LTCL Land Sale <$8,000> (in NII)

LTCL Carryforward <$2,000> (not in NII)

LTCL Carryforward of <$7,000>

IRC Chapter 1

158

159

<$3,000>

+0$<$3,000>

Adjustment

• <$8,000> land sale loss is in NII so <$3,000> of the land sale loss is allowed in Year 4 as a properly allocable deduction.

• <$4,000> remaining net nonpassive business loss ($9,000 - $5,000) not in NII

Draft Form 8960

1

1

160

Prop. Reg. 1.1411-4(d)(B) Example

A, Year 5:(1) <$7,000> LTCL Carryforward

Nothing Else

161

Draft 2013 Form 1040<$3,000>

Form 1040 Schedule D:

LTCL Carryforward <$7,000> ($5,000 in NII)($2,000 not in NII)

LTCL Carryforward of <$4,000>

IRC Chapter 1

162

163

<$3,000>

+0$<$3,000>

Adjustment

• <$3,000> of the <$5,000> remaining land sale loss is allowed first

• <$5,000> remaining loss on land sale in NII• <$2,000> remaining loss not in NII

Draft Form 8960

1

1

164

Prop. Reg. 1.1411-4(d)(B) Example

A, Year 6:(1) <$4,000> LTCL Carryforward

Nothing Else

165

Draft 2013 Form 1040<$3,000>

Form 1040 Schedule D:

LTCL Carryforward <$4,000> ($2,000 in NII)($2,000 not in NII)

LTCL Carryforward of <$1,000>

IRC Chapter 1

166

167

<$3,000>

+1,000$<$2,000>

Adjustment

• <$2,000> land sale loss is allowed first

Draft Form 8960

1

1

168

Prop. Reg. 1.1411-4(d)(B) Example

A, Year 7:(1) <$1,000> LTCL Carryforward

Nothing Else

169

Draft 2013 Form 1040<$1,000>

Form 1040 Schedule D:

LTCL Carryforward <$1,000> (not in NII)

IRC Chapter 1

170

171

<$1,000>

+1,000$<$0>

Adjustment

• <$1,000> loss is not in NII so no deduction.

Draft Form 8960

1

1

172

Generally, the final regs. assign all financial trading

gains and losses to category three

173

A “section 475 trader’s” net loss in category three can

offset income in Category One or

Two.

Former Passive Activity

Deductions(IRC sec. 469(f)(1))

174

175

Former passive activity deductions

that reduce TI reduce NII

(Reg. sec. 1.1411-4(g)(8))

176

• Wages $205,000• $7,000 S corp income—Alice

materially participates in 2013.• <$10,000> prior year

suspended passive loss from S Corp. when Alice did not materially participate.

• $500 Interest Income (S corpworking capital)

• $1,000 Passive Rental Income

Reg. Ex.: Alice’s Income in 2013

177

IRC sec. 469(f)(1):

The <$10,000> suspended passive loss reduces:

(1) S corp income of 7,000(2) Passive Rentals of $1,000

The <$2,000> balance is a suspended PAL

178

Alice’s NII: $500

$500 Interest Income

$1,000 Rental Income<$1,000> S Corp 469(f)(1)(C) loss

Freed-Up Passive Losses on Disposition(IRC sec. 469(g))

179

180

Losses allowed by IRC sec. 469(g) are either considered

as part of:category three net gain

or as “properly allocable

deductions”

(Reg. sec. 1.1411-4(g)(9); no examples)

181

• Interest $1,000,000

• $100,000 Gain on complete disposition of passive rental real estate.

• <$300,000> Previously suspended PALs on the rental real estate.

• $800,000 AGI

Example : Alice’s Income in 2013

182

• <$100,000> of the supendedPALs offset category three disposition gain.

• <$200,000> are properly allocable deductions that reduce the $1,000,000 interest income to $800,000.

Alice’s NII $800,000:

183

• Interest $500,000• Wages $500,000

• $100,000 Gain on complete disposition of passive rental real estate.

• <$300,000> Previously suspended PALs on the rental real estate.

• $800,000 AGI

Example : Same facts but:

184

• The entire <$200,000> of properly allocable deductions apparently reduce the $500,000 interest income (not the wages)

• The regs. do not provide an example.

Alice’s NII$300,000 if:

NOLs

185

186

NOL in loss year attributed to NII items

and deductions can generate an NII NOL

See Reg. 1.1411-4(h)Examples (1) and (2)

Trader with Large NOL

NOL Deduction

Whatabout

Credits?

187

• IRC Subtitle A tax credits reduce NIIT

• Tax credits limited to Chapter 1 tax are not allowed against the NIIT such as:• The foreign tax credit• The general business credit

Reg. Sec. 1.1411-1(e)

• Normally, no treaty relief; but a foreign tax deduction could reduce NII 188

“Net Investment Income”

“Investment Income”

minusProperly Allocable

Deductions

189

IRS DraftForm8960

(Itemized Deductions)

190

191

192

3-38

Reg. sec. 1.1411-4(f)(7)(iv) Example

193

$75,000

Misc. I.D.2% cut +

Sec. 68 cut

Sec. 68 cut only

2% of AGI Misc. I.D. floor is $40,000

• $30,000 Job related Expenses• $10,000 Investment Expenses

Overall 3% cut is $54,000

• $54,000 of $100,000 of State income tax not allocable to NII

194

Draft

$400,000

$400,000195

196

$75,000

$20,000

$60,000

$155,000

$155,000

197

198

$2,000,000$200,000

$1,800,000 $245,000

NIIT: 3.8% x 245,000 = $9,310

199

NII: $400,000 - $155,000 = $245,000

Draft Form 1040 Page 2

$9,310X

200

201

The deduction for unrecovered annuity basis

on the decedent’s final return (IRC sec. 72(b)(3))

is a properly allocable deduction.

Reg. sec. 1.1411-4(f)(3)(iv)

202

The final regulations provide special rules for deductions

in respect of a decedent (IRC sec. 691(b) as well as

the IRC sec. 691(c) deduction for estate tax on

IRD.

Treatment of Recoveries of

Amounts Previously Deducted.

Reg. sec. 1.1411-4(g)(2)203

204

Recoveries of previous year NII

deductions included in NII in the year of

recovery--no problem

Recovery of bad debt on back rent

205

If recoveries are NOT in NII, then the refund of NII deductions in later years cause a reduction in the properly allocable deductions in the year of the recovery.

206

• In Year 1, D, an individual, allocated $15,000 of taxes out of a total of $75,000 to NII (20%).

• D received no Chapter 1 tax benefit due to AMT.

• But the $15,000 reduced D’s NII.

Reg. Example (2)

207

• In Year 3, D received a refund of $5,000 of state income tax.

• Excluded for Chapter 1 purposes by IRC sec. 111.

• D reduces D’s Year 3 properly allocable deductions by $1,000 ($5,000 x ($15,000/$75,000)).

208

• In Year 3, D allocated $30,000 of state income taxes out of a total of $90,000 to NII (1/3)

• D's allocation of 33 1/3% of taxes in Year 3 to NII is irrelevant to the calculation.