A08-Marginal & Absorption Overview eng -final · Teacher reviews the definition of fixed and...

62

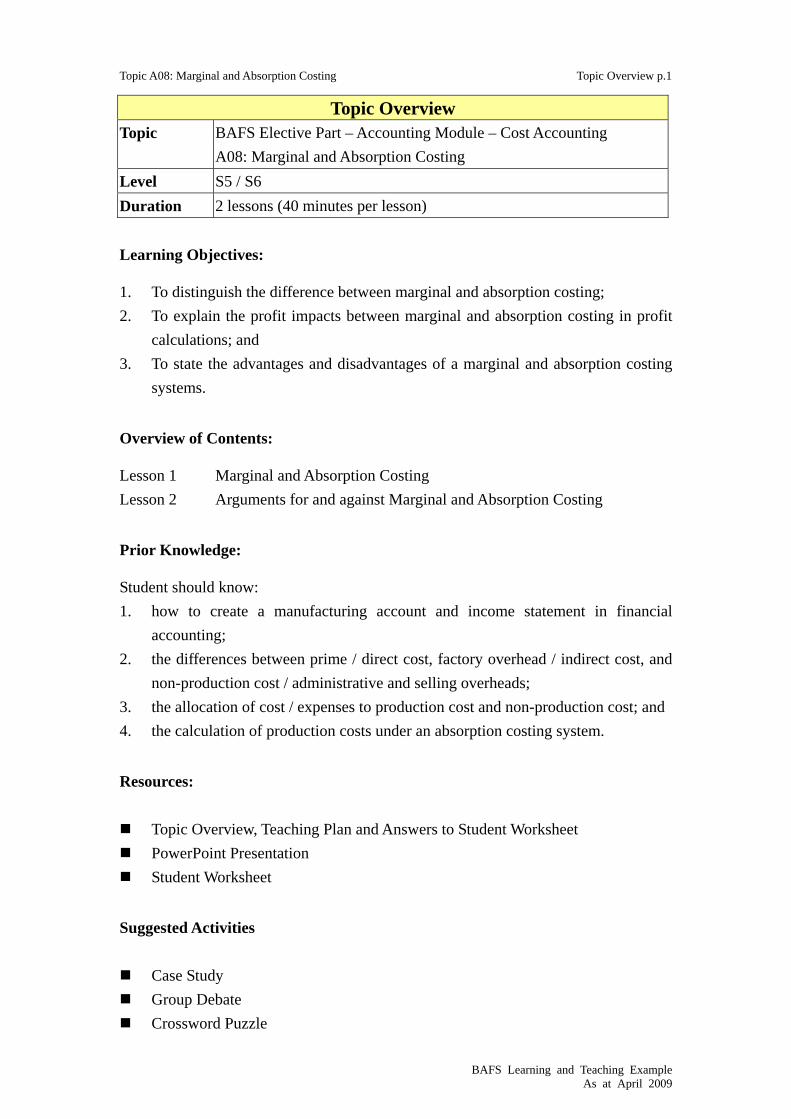

Topic A08: Marginal and Absorption Costing Topic Overview p.1 BAFS Learning and Teaching Example As at April 2009 Learning Objectives: 1. To distinguish the difference between marginal and absorption costing; 2. To explain the profit impacts between marginal and absorption costing in profit calculations; and 3. To state the advantages and disadvantages of a marginal and absorption costing systems. Overview of Contents: Lesson 1 Marginal and Absorption Costing Lesson 2 Arguments for and against Marginal and Absorption Costing Prior Knowledge: Student should know: 1. how to create a manufacturing account and income statement in financial accounting; 2. the differences between prime / direct cost, factory overhead / indirect cost, and non-production cost / administrative and selling overheads; 3. the allocation of cost / expenses to production cost and non-production cost; and 4. the calculation of production costs under an absorption costing system. Resources: Topic Overview, Teaching Plan and Answers to Student Worksheet PowerPoint Presentation Student Worksheet Suggested Activities Case Study Group Debate Crossword Puzzle Topic Overview Topic BAFS Elective Part – Accounting Module – Cost Accounting A08: Marginal and Absorption Costing Level S5 / S6 Duration 2 lessons (40 minutes per lesson)

Transcript of A08-Marginal & Absorption Overview eng -final · Teacher reviews the definition of fixed and...

Topic A08: Marginal and Absorption Costing Topic Overview p.1

BAFS Learning and Teaching Example As at April 2009

Learning Objectives: 1. To distinguish the difference between marginal and absorption costing; 2. To explain the profit impacts between marginal and absorption costing in profit

calculations; and 3. To state the advantages and disadvantages of a marginal and absorption costing

systems. Overview of Contents: Lesson 1 Marginal and Absorption Costing Lesson 2 Arguments for and against Marginal and Absorption Costing Prior Knowledge: Student should know: 1. how to create a manufacturing account and income statement in financial

accounting; 2. the differences between prime / direct cost, factory overhead / indirect cost, and

non-production cost / administrative and selling overheads; 3. the allocation of cost / expenses to production cost and non-production cost; and 4. the calculation of production costs under an absorption costing system. Resources:

Topic Overview, Teaching Plan and Answers to Student Worksheet PowerPoint Presentation Student Worksheet

Suggested Activities

Case Study Group Debate Crossword Puzzle

Topic Overview Topic BAFS Elective Part – Accounting Module – Cost Accounting

A08: Marginal and Absorption Costing Level S5 / S6 Duration 2 lessons (40 minutes per lesson)

Topic A08: Marginal and Absorption Costing Topic Overview p.2

BAFS Learning and Teaching Example As at April 2009

Lesson 1

Theme Marginal and Absorption Costing Duration 40 minutes

Expected Learning Outcomes: Upon completion of this lesson, students will be able to: 1. Define marginal and absorption costing; 2. Distinguish differences between marginal and absorption costing; 3. Prepare profit statements based on a marginal costing and an absorption costing

system; and 4. Explain the difference in profits between marginal and absorption costing profit

calculations.

Teaching Sequence and Time Allocation:

Activities Reference Time

AllocationPart I: Introduction

Teacher reviews the definition of fixed and variable costs and asks students to give examples in relation to their family’s monthly expenses.

Activity 1 – Case Study Teacher asks students to identify fixed and variable

costs, production and non-production costs in a manufacturing account and income statement of Pattie Company and calculate the unit product costs for the month of June Year 8 (Task 1 and 2).

Teacher informs students of two main accounting streams: financial accounting and cost accounting. Financial accounting is concerned with the provision of information to external parties. Cost accounting is concerned with the provision of information to internal parties. A number of costing systems are being applied by organisations

PPT#1-19

Student Worksheet

pp.1-7

15 minutes

Topic A08: Marginal and Absorption Costing Topic Overview p.3

BAFS Learning and Teaching Example As at April 2009

to provide relevant information to help managers make better decisions.

Teacher uses flowchart to introduce the term ‘absorption costing system’ and its mechanism.

Teacher tells students the relationship between the fixed cost and variable cost with absorption and marginal costing systems.

Teacher uses flowchart to show the framework of marginal costing system.

Teacher asks students to prepare the income statement for Pattie Company, using marginal costing method (Task 3)

Teacher asks students to determine the major effectif marginal costing is used and explains the meaning of contribution.

Part II: Content

Activity 2 – Case Study Students form groups of four or five, read the case

concerning of a cyber-firm and complete the tasks. Teacher invites students to present their answers. Teacher checks answers and draws conclusion for

each task.

PPT #20-32

Student Worksheet

pp.8-16

22 minutes

Part III: Conclusion Teacher concludes lesson by highlighting the

differences between marginal and absorption costing. Teacher asks students to consider the advantages and

disadvantages for marginal and absorption costing for the upcoming lesson.

PPT #33-35 3 minutes

Topic A08: Marginal and Absorption Costing Topic Overview p.4

BAFS Learning and Teaching Example As at April 2009

Lesson 2

Theme Arguments for and against Marginal and Absorption Costing Duration 40 minutes Expected Learning Outcomes: Upon completion of this lesson, students will be able to: 1. Explain the advantages and disadvantages of marginal costing; 2. Explain the advantages and disadvantages of absorption costing; and 3. Explain circumstances when suitable to use marginal or absorption costing. Teaching Sequence and Time Allocation:

Activities Reference Time

AllocationPart I: Introduction

Teacher starts the lesson by introducing the problem faced by Alice, the Managing Director of Bullet Manufacturing Company and asks students to set up a debate on the adoption of a marginal costing system in the company.

PPT #36 4 minutes

Part II: Content

Activity 3 – Preparation for the debate Students are divided into two groups; one is the

affirmative side and the other is the negative side. Students are required to discuss within their groups

and to develop arguments. Each group nominates one representative to take

part in the debate.

PPT #37

Student Worksheet pp.17-19

15 minutes

Activity 3 – Debate Each representative has 4 minutes to present their

group’s views and arguments. Teacher decides winner, concludes the debate and

introduces suitable circumstances for using marginal and absorption costing.

PPT #38-45 12 minutes

Topic A08: Marginal and Absorption Costing Topic Overview p.5

BAFS Learning and Teaching Example As at April 2009

Part III: Conclusion

Teacher concludes session by highlighting the advantages of marginal and absorption costing and asks students to choose the preferred costing methods under different circumstances.

Teacher asks students to complete the crossword puzzle at home to check their understanding on the concepts of marginal and absorption costing. The answers will be distributed during next lesson.

PPT #46 – 48

Student Worksheets

pp.20-22

9 minutes

Topic A08: Marginal and Absorption Costing Topic Overview p.6

BAFS Learning and Teaching Example As at April 2009

Task 1: Cost Classification

Fixed Cost Variable Cost Production Cost Non-Production Cost

Direct Materials Direct Materials

Direct Wages Direct Wages

Direct Expenses Direct Expenses

Factory Manager Salary Factory Manager Salary

Factory Management Fee

Factory Management

Fee

Factory Rent and Rates Factory Rent and Rates

Factory Fire Insurance Factory Fire Insurance

Factory Labour

Insurance Factory Labour

Insurance

Provision for Depreciation –

Machinery

Provision for Depreciation –

Machinery

Bank Loan Interest Bank Loan Interest

Provision for Depreciation – Office

Equipment

Provision for Depreciation –

Office Equipment

Cleaning Expenses Cleaning Expenses

Salesman’s Salaries Salesman’s Salaries

Carriage Outwards

Carriage Outwards

Advertising Advertising

Sales Commission Sales Commission

Office Rent and Rates Office Rent and

Rates

Answer to Activity 1

Topic A08: Marginal and Absorption Costing Topic Overview p.7

BAFS Learning and Teaching Example As at April 2009

Task 2: Cost Computation Total Production Cost: $76,200 Unit Produced: 2,540 Unit Product Cost = Total Production Cost ÷ Unit Produced = $76,200 ÷ 2,540 units = $30

Task 3: Income Statement (a)Unit Selling Price = Sales Revenue ÷ No of units sold

= $191,475 ÷ (57 + 2,540 – 44)

= $191,475 ÷ 2,553

= $75 Variable Production Cost = $(30,600 + 20,800 + 5,000 + 1,800)

= $58,200

Closing Stock Value (44 units) = $58,200 ÷ 2,540 x 44 = $1,008 Variable Non-production Cost = $(195 + 445)

= $640

Fixed Production Cost = $(9,000 + 500 + 7,000 + 600 + 900)

= $18,000

Fixed Non-production Cost = $(750 + 250 + 159 + 12,643 + 190 + 7,905)

= $21,897

Topic A08: Marginal and Absorption Costing Topic Overview p.8

BAFS Learning and Teaching Example As at April 2009

Income Statement for the month ending 30 June Year 8 (Marginal Costing)

HK$ HK$ Sales 191,475 Less: Variable Production Cost of Goods Sold Finished Goods Opening Stock 1,254 Add: Variable Production Cost 58,200 59,454 Less: Finished Goods Closing Stock 1,008 58,446 133,029

Less: Variable non-production cost 640 Contribution 132,389 Less: Fixed cost Production 18,000 Non-production 21,897 39,897 Net profit 92,492

(b)

Major Effect: Profit calculated under Marginal Costing is higher than that of Absorption Costing. Reason: The closing inventory value calculated under the Absorption Costing method is higher than Marginal Costing, as fixed production costs are treated as product and costs will be carried forward to the next accounting period if unsold. Therefore, a decrease in the stock levels mean a larger portion of the fixed costs will be charged to the current accounting period under Absorption Costing and the profit calculated will be lower than that of Marginal Costing.

Topic A08: Marginal and Absorption Costing Topic Overview p.9

BAFS Learning and Teaching Example As at April 2009

Task 1: Cost Classification Examples of fixed cost:

Cost of setting up business on Yahoo Small Business Platform Monthly service fee paid to Yahoo Hire charges for heat transfer machines Packaging tools and materials

Examples of variable cost:

T-shirt purchase cost Transaction fee paid to Yahoo Delivery charges

Task 2: Cost Estimation

Cost Items HK$

Monthly service fee paid to Yahoo Range from HK$160 to HK$320, depends on plans selected

Hire charges for heat transfer machines (Assuming 2 machines will be hired)

Machines with more functions are higher, normally below HK$1,000 each

T-shirt purchase cost Range from a few dollars to hundreds, depends on quality and quantity selected

Transfer paper for laser printer Around HK$6 each

Packaging tools and materials Range from few dollars to hundreds, depends on materials and packaging

Printing charges (e.g. cartridge) Range from a few dollars to hundreds, depends on cartridge and number of colours

Transaction fee paid to Yahoo Range from 1% - 2% of the monthly revenue, depends on the plan selected

Delivery charges Range from a few dollars to hundreds, depends on location and delivery point

Answer to Activity 2

Topic A08: Marginal and Absorption Costing Topic Overview p.10

BAFS Learning and Teaching Example As at April 2009

Task 3: Cost Computation (a)

Cost Classification under Cost Items Details

Fixed or Variable

Production or Non-production

Service fee paid to Yahoo $400/month Fixed Cost Non-production Cost

Hire charges for 2 heat transfer machines

$1,500/ month

Fixed Cost Production Cost

T-shirt purchase cost $15/piece

Variable Cost

Production Cost

Transfer paper $4/sheet

Variable Cost

Production Cost

Printing charges $3/sheet

Variable Cost

Production Cost

Packaging tools & materials $2,000/ month

Fixed Cost Production Cost

Stationery expenses $300/month Fixed Cost Non-production Cost Advertising fee (a fixed amount charged by an advertising firm)

$1,000/month Fixed Cost Non-Production Cost

Transaction fee charged by Yahoo

1.5% on sales Variable Cost

Non-Production Cost

Delivery charges 1% on sales Variable Cost

Non-Production Cost

(b)

Under Marginal Costing: T-shirt purchases cost $15 Transfer paper $ 4 Printing charges $ 3 Unit product cost $22

Under Absorption Costing: T-shirt purchases $15 Transfer paper $ 4 Printing charges $ 3 Production overhead* $ 7 Unit product cost $29

*($1,500 + $2,000) ÷ 500 = $7

Topic A08: Marginal and Absorption Costing Topic Overview p.11

BAFS Learning and Teaching Example As at April 2009

Task 4: Profit Computation (a) Absorption Costing

1st month 2nd month 3rd month Total HK$ HK$ HK$ HK$ Sales 21,750.00 17,400.00 23,925.00 63,075.00 Less: Production cost of sales

Opening stock - - 2,900.00 - Production cost 14,500.00 14,500.00 14,500.00 43,500.00 Closing stock - (2,900.00) (1,450.00) (1,450.00) 14,500.00 11,600.00 15,950.00 42,050.00

Gross profit 7,250.00 5,800.00 7,975.00 21,025.00 Less: Non-production cost Fixed 1,700.00 1,700.00 1,700.00 5,100.00 Variable 543.75 435.00 598.13 1,576.88 Net profit 5,006.25 3,665.00 5676.87 14,348.12

(b) Marginal Costing

1st month 2nd month 3rd month Total HK$ HK$ HK$ HK$ Sales 21,750.00 17,400.00 23,925.00 63,075.00 Less: Variable production

cost of sales

Opening stock - - 2,200.00 - Variable production cost 11,000.00 11,000.00 11,000.00 33,000.00 Closing stock - (2,200.00) (1,100.00) (1,100.00) 11,000.00 8,800.00 12,100.00 31,900.00 Variable non-production

cost 543.75 435.00 598.13 1,576.88

11,543.75 9,235.00 12,698.13 33,476.88 Contribution 10,206.25 8,165.00 11,226.87 29,598.12 Less: Fixed cost Production 3,500.00 3,500.00 3,500.00 10,500.00 Non-production 1,700.00 1,700.00 1,700.00 5,100.00 Net profit 5,006.25 2,965.00 6,026.87 13,998.12

Topic A08: Marginal and Absorption Costing Topic Overview p.12

BAFS Learning and Teaching Example As at April 2009

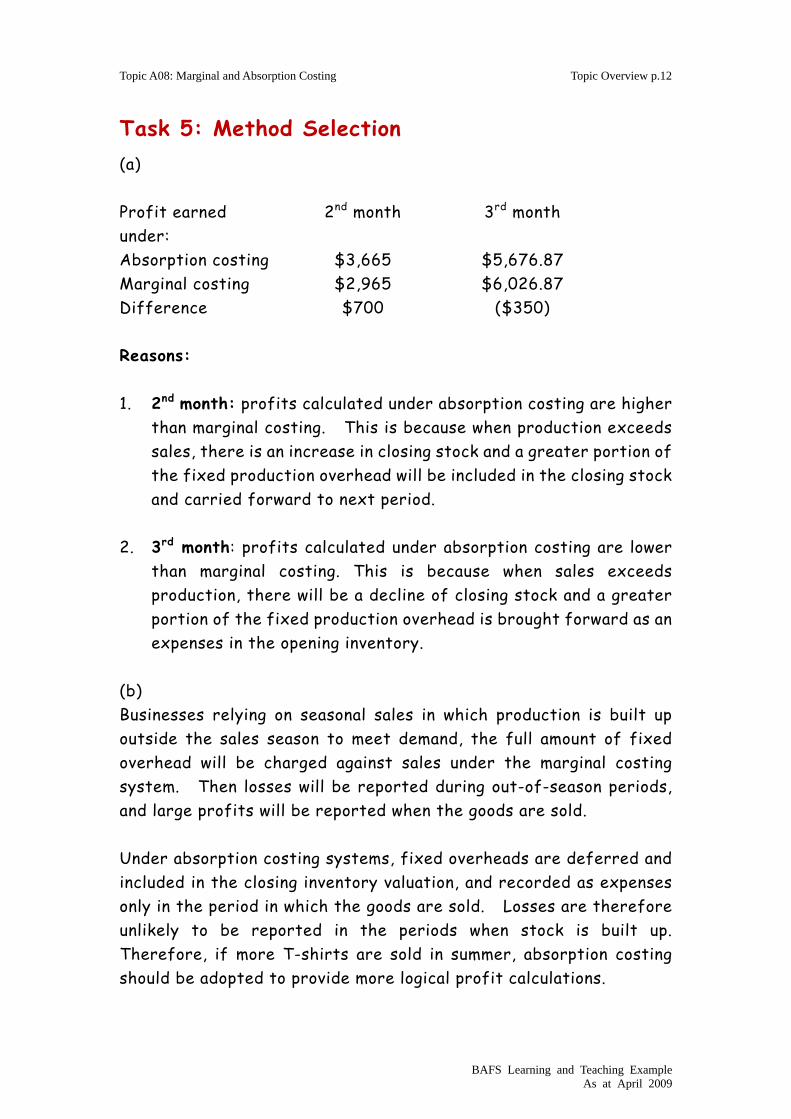

Task 5: Method Selection (a) Profit earned under:

2nd month 3rd month

Absorption costing $3,665 $5,676.87 Marginal costing $2,965 $6,026.87 Difference $700 ($350) Reasons: 1. 2nd month: profits calculated under absorption costing are higher

than marginal costing. This is because when production exceeds sales, there is an increase in closing stock and a greater portion of the fixed production overhead will be included in the closing stock and carried forward to next period.

2. 3rd month: profits calculated under absorption costing are lower

than marginal costing. This is because when sales exceeds production, there will be a decline of closing stock and a greater portion of the fixed production overhead is brought forward as an expenses in the opening inventory.

(b) Businesses relying on seasonal sales in which production is built up outside the sales season to meet demand, the full amount of fixed overhead will be charged against sales under the marginal costing system. Then losses will be reported during out-of-season periods, and large profits will be reported when the goods are sold. Under absorption costing systems, fixed overheads are deferred and included in the closing inventory valuation, and recorded as expenses only in the period in which the goods are sold. Losses are therefore unlikely to be reported in the periods when stock is built up. Therefore, if more T-shirts are sold in summer, absorption costing should be adopted to provide more logical profit calculations.

Topic A08: Marginal and Absorption Costing Topic Overview p.13

BAFS Learning and Teaching Example As at April 2009

Arguments for the proposition (hints: students are required to emphasise the advantages of Marginal Costing and disadvantages of Absorption Costing) Advantages of Marginal Costing

Easy to understand – avoids arbitrary allocation of fixed overheads. Fixed overhead is excluded from inventory costs – avoids the varying

charges per unit and hence distortion in stock valuations. Fixed overheads are NOT carried forward in stock valuations – avoids the

effect of changes in closing inventory level on profits. Contribution and profits are directly driven by sales – shows clearly the

effect of sales on cash flows and relationships between cost, price and volume.

Focuses on controllable business aspects – facilities execution of cost controls.

Disadvantages of Absorption Costing

More complicated – have to make arbitrary assumptions on apportionment of fixed overheads.

Fixed overheads are charged to production – unit inventory costs may vary according to production.

Part of the current year’s fixed overhead is carried forward in closing stock to the following year – management may manipulate profits by building up inventories and hence deferring the fixed overheads to the following years.

Profit is not a direct function of sales. There’s a possibility that profit may drop even though sales are up.

Relationships between cost, price and volume are ignored since the focus is on total cost.

Answer to Activity 3

Topic A08: Marginal and Absorption Costing Topic Overview p.14

BAFS Learning and Teaching Example As at April 2009

Arguments against the proposition (hints: students are required to emphasise the advantages of Absorption Costing and disadvantages of Marginal Costing) Advantages of Absorption Costing

Fixed costs are absorbed in inventory – ensures all fixed costs will be recovered and met in the long run.

Recognition of the importance of fixed overheads in production – finished goods and work in progress stock will not be understated, giving a true and fair view of the firm’s financial affairs.

Compliance with Accounting Standards – is useful for external reporting. All costs are variable in the long run – recognises all “long run variable”

costs. Less profit fluctuations when production remains constant but sales

fluctuate. Disadvantages of Marginal Costing

It ignores that fixed costs must be recovered in the long run, so if selling price is based only on marginal costs, it’s possible that a positive contribution might NOT be sufficient to cover all fixed costs in the long run.

Finished goods and work in progress stock will be understated. Exclusion of fixed costs from stock valuations does not conform to

acceptable accounting practices. It fails to recognise that all costs are variable in the long run. For firms that have a seasonal sales pattern, profits tend to fluctuate

greatly. Losses are reported during the slack season while huge profits are reported during the peak session.

It’s not easy to establish the variability of costs, as variable costs are rarely completely variable and fixed cost are rarely completely fixed.

Topic A08: Marginal and Absorption Costing Topic Overview p.15

BAFS Learning and Teaching Example As at April 2009

Marginal Costing Absorption Costing

Short run decision-making

Long run decision-making

When sales is subject to high seasonal fluctuations

Comparison of performance of different departments/product lines

External reporting

Summary for lesson 2

Topic A08: Marginal and Absorption Costing Topic Overview p.16

BAFS Learning and Teaching Example As at April 2009

3V 1A R I A B L E 4C O N T R I B U T I O N 8C

S O

O 7C N

1M A R G I N A 5L T

2P P S O R 3F

6G R E A T E R H W 6S O I

O I 7E Q U A L 4O X

D O R M P E

U 5U N D E R 2O V E R H E A D

C N

T I

8P R O D U C T I O N

G

Answer to Activity 4

1

BAFS Elective PartAccounting Module –

Cost Accounting

Topic A08: Marginal and Absorption Costing

Technology Education SectionCurriculum Development Institute

Education Bureau, HKSARGApril 2009

IntroductionThis session aims to help students distinguish between marginal and absorption costing and their impact on profit calculations. Students will build a solid understanding through active participation in debate and case study.

DurationTwo 40-minute lessons

ContentsLesson 1 – Marginal and Absorption CostingLesson 2 – Arguments for and against Marginal and Absorption Costing

2

2Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Fixed Costs

Lesson 1

Teacher starts the lesson by introducing the definition of fixed cost.Definition of fixed cost: A cost which is incurred for a period, and which, within certain output and turnover limits, tends to be unaffected by fluctuations in the level of activity. (CIMA Official Terminology)

Teacher provides examples of fixed costs. They include• Business registration fee• Factory/office rent• Factory/office rates• Factory/office management fee• Supervisors’/executives’ salaries• Depreciation of factory building/equipment/machinery• Fire insurance of factory building/equipment/machinery

3

3Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Examples of fixed cost in relation to your family’s monthly expenses

Teacher asks students to give examples of fixed costs in relation to their family’s monthly expenses.

Examples are:1. Monthly rent2. Rates3. Property insurance4. Life insurance5. Management fee6. School fee7. Monthly wages to maid8. Residential telephone service fee (i.e. fixed line)

4

4Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Variable Costs

Total Variable Cost($)

Output (units)

Teacher introduces the definition of variable costs.

Definition of variable costs: A cost which tends to vary with the level of activity. (CIMA Official Terminology)

Teacher provides examples of variable cost. They include:• Direct materials• Piecework labour wages• Royalty payments• Power cost• Sales commission• Delivery charges• Motor vehicle running expenses

5

5Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Examples of variable cost in relation to your family’s monthly expenses

Teacher asks students to give examples of variable costs in relation to their family’s monthly expenses.

Examples are:1. Traveling expenses2. Food3. Electricity charges4. Gas fee5. Clothing6. Entertainment expenses7. Water charges8. Motor vehicle running expenses

6

6Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

AActivity 1ctivity 1::

Pattie Pattie CompanyCompany

(Refer to Student Worksheet Page 1 to 3)

Teacher asks students to read the case and pay special attention on the questions raised by the owner, Pattie.

7Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Pattie Company

Manufacturing AccountIncome Statement

The manufacturing account and income statement of the Pattie Company are given for information.

8Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Pattie Company

Except direct, indirect cost, what are fixed and variable cost?

Are there any other ways to calculate the production cost?

Highlights of the case:- The owner, Pattie, has heard about fixed and variable costs from her

friends and wants to know their meanings.- Pattie asks the accountant to propose an alternative method to calculate

the production costs and the unit product costs

9

9Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 1 - Cost Classification

Identify the fixed, variable, production and non-production cost from the Pattie Company’s Manufacturing Account and Income Statement for the month ended 30 June Year 8.

Fixed Cost Variable Cost ProductionCost

Non-Production Cost

e.g. Direct Materials

e.g. Direct Materials

Teacher asks students to identify the fixed, variable, production and non-production costs from the financial statements. Direct materials are used as an example to guide students fill in the table.

Teacher may prompt students to pay attention on the following two questions in doing the classification:

- Will the costs/expenses be affected when activity levels fluctuate within certain output and turnover limits? (If yes, it is a variable cost. If no, it is a fixed cost.)

- Are the costs/expenses involved in the manufacturing process of the product? (If yes, it is a production cost. If no, it is a non-production cost.)

10

10Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Fixed Cost Variable Cost Production Cost Non-Production Cost

Direct Materials Direct Materials

Direct Wages Direct Wages

Direct Expenses Direct Expenses

Factory Manager Salary Factory Manager Salary

Factory Management Fee Factory Management Fee

Factory Rent and Rates Factory Rent and Rates

Factory Fire Insurance Factory Fire Insurance

Factory LabourInsurance Factory Labour Insurance

Provision for Depreciation –Machinery Provision for Depreciation –Machinery

Bank Loan Interest Bank Loan Interest

Provision for Depreciation –Office Equipment Provision for Depreciation –Office Equipment

Cleaning Expenses Cleaning Expenses

Salesman’s Salaries Salesman’s Salaries

Carriage Outwards Carriage Outwards

Advertising Advertising

Sales Commission Sales Commission

Office Rent and Rates Office Rent and Rates

Task 1 - Cost Classification (cont’d)

Teacher invites students to give the answers before showing the table. Teacher then checks the answer with students.

11

11Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Assuming 2,540 units of goods were produced by Pattie Company for the month of June Year 8, the production cost for each unit would be:

Task 2 - Cost Computation

Total Production Cost:

Unit Produced:

Unit Product Cost = Total Production Cost ÷ Unit Produced

=

=

Teacher asks students to compute the unit product for the month of June Year 8.

Total Production Cost refers to the “production cost of goods completed”computed in the Manufacturing Account.

12

12Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Total Production Cost: $76,200

Unit Produced: 2,540

Unit Product Cost = Total Production Cost ÷ Unit Produced

= $76,200 ÷ 2,540 units

= $30

Task 2 - Cost Computation(cont’d)

Teacher checks the answer with students.

Teacher explains there are two main streams in accounting: financial accounting and cost accounting.

Financial accounting is concerned with the provision of information to external parties, such as potential investors, creditors and government. Financial accounting statements must be prepared in compliance with the legal requirements and generally accepted accounting principles.

Cost accounting is concerned with the provision of information to internal parties within the organisation, such as managers, to help them make better decisions and improve the efficiency and effectiveness of operations. Unlike financial accounting, there are no statutory requirements for cost accountants to produce nor follow externally imposed rules. The preparation of a cost accounting reports are optional and the information should only be produced if the benefit obtained from the information provided exceeds the cost of collecting it.

A number of costing systems are being applied by an organisation to provide relevant information to help managers make better decisions. The costing system used in task 2 for calculating the unit product cost is known as absorption costing.

13

13Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Absorption Costing

Cost

Work in progress stock

Production overheads Non-production overheads

Overheads(Indirect materials, indirect labour and indirect expenses)

Direct costs(Direct materials, direct labour and direct expenses)

Finished goods stock Profit and loss account

Teacher explains the flowchart with students and shows them how cost is charged under absorption costing.

Costs build-up under absorption costing:Costs incurred by an enterprise can be classified into direct costs and indirect costs/overheads. Direct costs are those costs which can be directly identified with a product or service, such as direct materials, direct labour and direct expenses. Indirect costs/overheads are those costs which cannot be identified specifically and exclusively with a product or service. Indirect costs/overheads can be further classified as productionoverheads and non-production overheads. Overheads which occur in production, such as factory rent and rates are called productionoverheads. Those overheads, other than production overheads, such as office rent and rates, are referred as non-production overheads.All production costs (direct/prime costs and production overheads) are considered as product costs and are included in the (finished goods and work in progress) stock valuation. Non-production overheads are excluded from the stock valuation. They are charged directly to the profit and loss account. The unsold stock will therefore contain a share of the production overheads incurred in the period.

14

14Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Cost Relationships

Teacher introduces another costing system: marginal costing.

Teacher tells students the relationship between the fixed costs and variable costs within the two costing systems.

Absorption costing is an accounting system in which all production costs (i.e. both fixed and variable) are charged to cost units.

Marginal costing is an accounting system in which only variable production costs are charged to cost units and the rest of the costs are written off in the period incurred.

15

15Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Marginal Costing

Cost

Finished goods stockWork in progress stock

Fixed production overheads

Production overheads Non-production overheads

Profit and loss account

Overheads(Indirect materials, indirect labour and indirect expenses)

Direct costs*(Direct materials, direct labour and direct expenses)

Variable production overheads

* Direct costs behave as variable costs

Teacher explains the flowchart and shows how costs are charged under the marginal costing system.

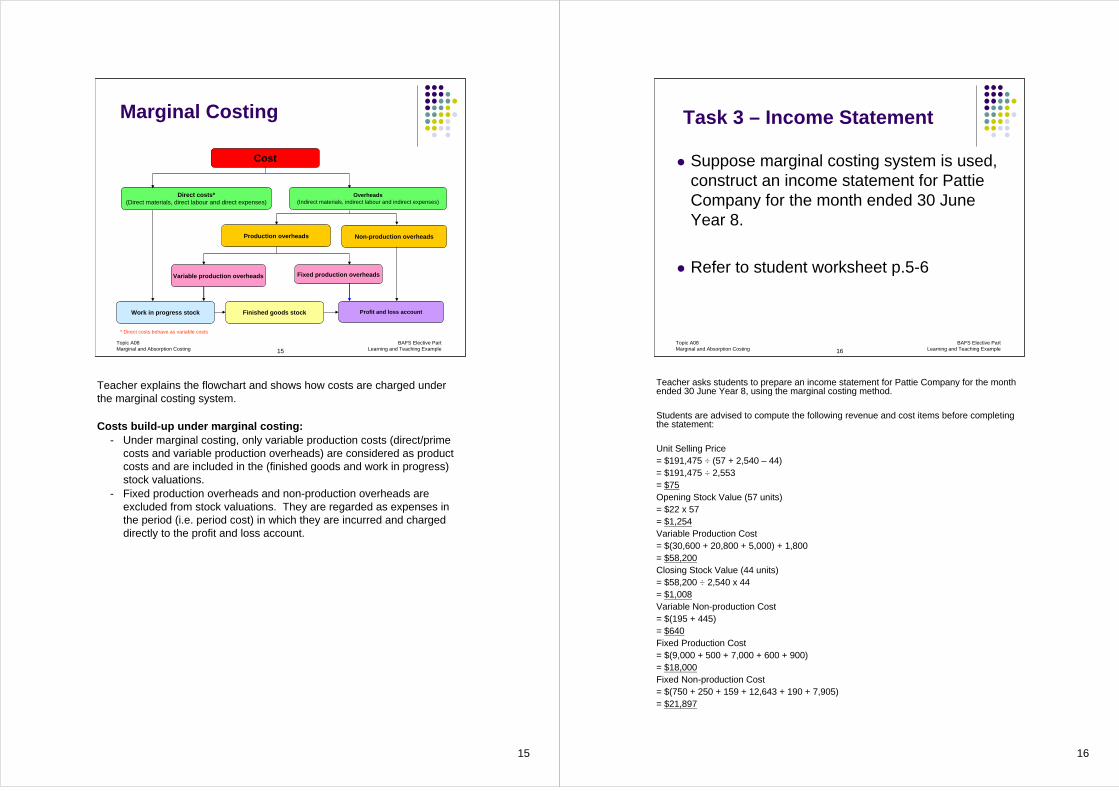

Costs build-up under marginal costing:- Under marginal costing, only variable production costs (direct/prime

costs and variable production overheads) are considered as product costs and are included in the (finished goods and work in progress) stock valuations.

- Fixed production overheads and non-production overheads are excluded from stock valuations. They are regarded as expenses in the period (i.e. period cost) in which they are incurred and charged directly to the profit and loss account.

16Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 3 – Income Statement

Suppose marginal costing system is used, construct an income statement for Pattie Company for the month ended 30 June Year 8.

Refer to student worksheet p.5-6

Teacher asks students to prepare an income statement for Pattie Company for the month ended 30 June Year 8, using the marginal costing method.

Students are advised to compute the following revenue and cost items before completing the statement:

Unit Selling Price = $191,475 ÷ (57 + 2,540 – 44)= $191,475 ÷ 2,553= $75Opening Stock Value (57 units)= $22 x 57= $1,254Variable Production Cost = $(30,600 + 20,800 + 5,000) + 1,800= $58,200Closing Stock Value (44 units)= $58,200 ÷ 2,540 x 44= $1,008Variable Non-production Cost= $(195 + 445)= $640Fixed Production Cost= $(9,000 + 500 + 7,000 + 600 + 900)= $18,000Fixed Non-production Cost= $(750 + 250 + 159 + 12,643 + 190 + 7,905)= $21,897

16

17Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 3 – Income Statement (cont’d)

Income Statement for the month ended 30 June Year 8

HK$ HK$ Sales 191,475Less: Variable Production Cost of Goods Sold Finished Goods Opening Stock 1,254Add: Variable Production Cost 58,200

59,454Less: Finished Goods Closing Stock 1,008 58,446

133,029Less: Variable non-production cost 640Contribution 132,389Less: Fixed costProduction 18,000Non-production 21,897 39,897Net profit 92,492

Teacher checks the answer with students and explains the meaning ofwhat contribution is.

Contribution is the difference between sales and all variable costs (both production and non-production), from which fixed costs are deducted to show net profit/loss. In general, if:total contribution > fixed cost profittotal contribution < fixed cost loss

17

18Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 3 – Income Statement (cont’d)

State the major effect of using marginal costing in preparing the Income Statement of Pattie Company and explain why this happened.

Teacher asks students to compare the income statement prepared in part (a) with that prepared under absorption costing and read the hints provided. Students are required to state the major effect of using marginal costing and explain why this happened.

Inventory valuation

The value of the closing inventory calculated under absorption costing would be higher than that of marginal costing as fixed production costs are treated as product cost and can be carried forward to the next period. For marginal costing, it only includes variable production cost and the fixed non-production costs are written off in the period incurred.

Income determination

If opening stock is less than closing stock, there will be an increase in closing stock. The profit calculated under absorption costing will be higher as a larger portion of the fixed production overhead will be carried forward to next accounting period. The profit calculated under marginal costing will be lower as all fixed production costs incurred will not be carried forward and are charged directly to the current profit.

Opposite result will be obtained if there is a decrease in closing stock.

18

19Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 3 – Income Statement (cont’d)

Absorption Costing Marginal Costing

Differences in the 2 costing systems

(a) Fixed production costs are treated as product cost.

(b) If closing stock , part of the fixed production cost is carried forward to the next accounting period.

(a) Fixed production costs are treated as period cost.

(b) If closing stock , no fixed production cost is carried forward because all fixed production costs are written off in the period incurred.

Impact on

Inventory valuation

Higher closing stock value(reason (a) above)

Lower closing stock value(reason (a) above)

Income determination

Higher profit(reason (b) above)

Lower profit(reason (b) above)

Answers to task 3 (b)

20

20Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Activity 2: Case Study

Form groups of four to five

Read the case carefully, discuss and complete Task 1 of Activity 2

Teacher asks students to form groups of four or five. Students must read the case on setting up a cyber-firm to sell their own custom designed heat-transfer print T-shirt on Yahoo and complete task 1.

21

21Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 1 - Cost Classification

List the fixed and variable costs that would incur in setting up a cyber-firm selling your own designed heat-transfer print T-shirt on the Internet.

Teacher asks students to list the fixed and variable costs that would incur in setting up a cyber-firm selling their own custom designed heat-transfer print T-shirt on internet and invites volunteers to share their suggestions with the class.

22

22Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 1 - Cost Classification (cont’d)

Examples of fixed cost• Cost of setting up a business on Yahoo

Small Business Platform• Monthly service fee paid to Yahoo• Hire charges for heat transfer machines• Packaging tools and materials

Examples of Variable cost• T-shirt purchase cost• Transaction fee paid to Yahoo• Delivery charges

Teacher concludes students’ suggestions and gives some examples for the fixed and variable costs that would be incurred setting up a cyber-firm.

23

23Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 2 - Cost EstimationEstimate the monthly running cost of the business :

Cost Items: HK$

Monthly service fee paid to Yahoo

Hire charges for heat transfer machines (Assuming 2 machines will be hired)

T-shirt purchase cost

Transfer paper for laser printer

Packaging tools and materials

Printing charges (e.g. cartridge)

Others:

Teacher asks students to complete Task 2 and invites volunteers to share their answers with the class. Here are some suggestions:

• Monthly service fee paid to Yahoo: express plan US$19.95 (~HK$160); starter plan US$39.95 (~HK$320); standard plan US$99.95 (~HK$780)

• Hire charges for heat transfer machines: below HK$1,000 each• T-shirt purchase cost: depends on the quality and quantity, it may range from a few dollars

to hundreds.• Transfer paper for laser printer: around HK$6 each• Packaging tools and materials: depends on the materials and types of packaging• Printing charges: cartridge - HK$100-HK$200 per color, each cartridge can produce 40 -

50 A4 size copies.• Others: Transaction fee paid to Yahoo – 2.0% for express plan; 1.5% for starter plan; 1.0%

for standard plan. Delivery charges – depends on the type of delivery mail or DHL. Teacher may, at his/her own discretion, arouse students’ interest/attention on some cost items by asking the following questions:

• How many service plans are provided by Yahoo? (Three service plans are provided –express plan, starter plan and standard plan. Fees will be higher if more services are provided)What is the size of a heat transfer machine? (The sizes are varied. Some of them may be as small as a printer.)Will there be a need of leasing a flat to place the heat transfer machines? (If only 1 or 2 heat transfer machines are leased, there is no need to rent extra areas for storage. Students should be able to store them at home.)Where will they buy the T-shirt? (They can purchase directly from the T-shirt manufacturer.)What is their target purchase price for the T-shirt? (Higher quality – Higher price; Lower quality – Lower price; Larger quantity – Lower price; Smaller quantity – Higher price. The price may be lower if they purchase from the manufacturer in China. However, it may incur higher transportation cost.Who are their target customers, local or overseas? (The delivery and packaging charges will be higher if they need to send the T-shirt to overseas customers.)

24

24Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 3 (a) - Cost Computation cont’dComplete the following table based on the characteristics of different cost items:

Cost Items Details Cost Classification underFixed or Variable

Production or Non-production

Service fee paid to Yahoo $400/month Fixed Cost Non-production cost

Hire charges for 2 heat transfer machines

$1,500/ month

T-shirt purchase cost $15/pieceTransfer paper $4/sheetPrinting charges $3/sheetPackaging tools & materials $2,000/ monthStationery expenses $300/monthAdvertising fee (a fixed amount charged by an advertising firm)

$1,000/month

Transaction fee charged by Yahoo 1.5% on sales

Delivery charges 1% on sales

Teacher asks student to complete Task 3(a).

Students are required to look at each cost item, then classify it into either:(a) Fixed or variable cost; and(b) Production or non-production overheads.

25

25Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 3 (a) - Cost Computation (cont’d)

Suggested Answer:

Cost Items Details Cost Classification under(Marginal Costing)Fixed or Variable

(Absorption Costing)Production or Non-

production

Service fee paid to Yahoo $400/month Fixed Cost Non-production Cost

Hire charges for 2 heat transfer

machines

$1,500/ month Fixed Cost Production Cost

T-shirt purchase cost $15/piece Variable Cost Production Cost

Transfer paper $4/sheet Variable Cost Production Cost

Printing charges $3/sheet Variable Cost Production Cost

Packaging tools & materials $2,000/ month Fixed Cost Production Cost

Stationery expenses $300/month Fixed Cost Non-production CostAdvertising fee (a fixed amount

charged by an advertising firm)

$1,000/month Fixed Cost Non-Production Cost

Transaction fee charged by Yahoo 1.5% on sales Variable Cost Non-Production Cost

Delivery charges 1% on sales Variable Cost Non-Production Cost

Teacher invites students to give their answers before checking the answers with them.

Teacher then checks students’ understanding of the difference between the two costing methods by asking:

• Under what costing method is cost separated into fixed and variable? (answer: marginal costing)

• Under what costing method is cost separated into production and non-production? (answer: absorption costing)

26

26Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 3 (b) - Cost Computation

Assuming 500 units of T-shirt will be produced per month and production overhead will be absorbed on unit basis, compute the production cost for each unit based on the data in 3(a), using

(i) Marginal Costing

(ii) Absorption Costing

Teacher asks students to compute the unit product cost for each T-shirt, using marginal costing and absorption costing methods.Teacher may, at own discretion, use the following questions to guide students to complete the calculations:For marginal costing

Do we have to include fixed production cost in the computation of unit product cost? (No. They are treated as period cost and charged directly to the profit and loss account.)Do we need to include all variable cost in the computation of unit product cost? (No. Only variable production costs e.g. direct materials, direct labor and variable production overhead are included in stock valuation. Variable non-production overheads, such as delivery charges and sales commission are not considered as product cost but they must be used in calculation of contribution.)

For absorption costing

Should all cost items be included in the computation of unit product cost? (No. Only production costs that are identified with goods produced for resale are required to be included.)Do we have to separate the production cost into fixed and variable elements for the computation? (In general, it is not required. Costs are only required to be classified into production and non-production under absorption costing. However, for better presentation, students may classify them into variable production cost and fixed production cost.)How to treat a cost which is for both factory use and office use? (Apportionment must be made.)How to determine the basis for apportionment (It depends on the cost driver and there is opportunity for arbitrary assumption.)

27

27Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 3 (b) - Cost Computation (cont’d)

Suggested Answers:

Under Marginal Costing:T-shirt purchase cost $15Transfer paper $ 4Printing charges $ 3Unit product cost $22

Under Absorption Costing:T-shirt purchase cost $15Transfer paper $ 4Printing charges $ 3Production overhead* $ 7Unit product cost $29

*($1,500+$2,000) ÷500=$7

Teacher checks answers with students.

The major difference between the 2 costing methods is the treatment of fixed production overheads of $7*.

Under marginal costing, only variable production costs (i.e. T-shirt purchase cost, transfer paper cost and printing charges) are considered as product cost. Non-production variable cost (i.e. transaction fees charged by Yahoo and delivery charges) and all fixed costs (i.e. service fee paid to Yahoo, hire charges for 2 heat transfer machines, packaging materials & tools, stationery expenses andadvertising fee) are excluded from the computation.

Under absorption costing, all production costs related to the product produced are required to be included in the stock valuation (i.e. T-shirt purchase cost, transfer paper cost, printing charges, hire charges of 2 heat transfer machines and packaging tools and materials). Non-production cost (i.e. service fee paid to Yahoo, stationery expenses, advertising fee, transaction fee charged by Yahoo and delivery charges) are treated as period costs and excluded from the computation.

* Referring to slide 13, fixed production overheads consist of hire charges of $1,500 and packaging tools and materials costs of $2,000. The total amount of $3,500 fixed production overheads are to be absorbed by the 500 T-shirts produced (i.e.$7 per unit).

28

28Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 4 - Profit Computation

Based on the forecasted sales and the data in Task 3(a), construct a profit statement for the first three months of operation using:(a) Absorption Costing (using a mark up of 50%)(b) Marginal Costing (using the same selling price as

calculated under absorption costing)

Teacher asks students to prepare profit statements for the first three months of operation using marginal costing and absorption costing methods.

29

29Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 4 - Profit Computation (cont’d)

4(a) Suggested Answer (Absorption Costing):

Teacher checks the answer with students.Workings:

Selling price (50% mark up) = $29 x (1+50%) = $43.5Sales :

1st month $43.5 x 500 units = $21,7502nd month $43.5 x 400 units = $17,4003rd month $43.5 x 550 units = $23,925

Opening stock1st month nil2nd month nil3rd month $29 x 100 units = $2,900

Production costs for 1st/2nd/3rd month: $29 x 500 units = $14,500

Closing stock1st month nil2nd month $29 x 100 units = $2,9003rd month $29 x 50 units = $1,450

Fixed non-production cost: $400 (service fee to Yahoo) + $300 (stationery) + $1,000 (advertising)Variable non-production cost: (1.5% transaction fee + 1% delivery charge) x Sales

1st month 2.5% x $21,750 = $543.752nd month 2.5% x $17,400 = $4353rd month 2.5% x $23,925 = $598.13

30

30Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 4 - Profit Computation (cont’d)4(b) Suggested Answer (Marginal Costing):

Teacher checks the answers with students. Workings:

Sales: (using same selling price as calculated under absorption Costing )1st month $43.5 x 500 units = $21,750 2nd month $43.5 x 400 units = $17,4003rd month $43.5 x 550 units = $23,925

Opening stock1st month nil2nd month nil3rd month $22 x 100 units = $2,200

Variable Production costs for 1st/2nd/3rd month: $22 x 500 units = $11,000

Closing stock1st month nil2nd month $22 x 100 units = $2,200

3rd month $22 x 50 units = $1,100

Variable non-production cost: (1.5% transaction fee + 1% delivery charge) x Sales

1st month 2.5% x $21,750 = $543.752nd month 2.5% x $17,400 = $4353rd month 2.5% x $23,925 = $598.13

Fixed production cost: $1,500 (hire charges) + $2,000 (packaging)

Fixed non-production cost : $400 (service fee to Yahoo) + $300 (stationery) + $1,000 (advertising)

31

31Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 5 (a) - Method Selection

Based on the profit statements prepared in Task 4, suggest two reasons for the difference in net profits for the 2nd and 3rd month of sales.

Profit earned

Absorption costing 2nd month $3,665 3rd month $5,676.87Marginal costing 2nd month $2,965 3rd month $6,026.87Difference 700 ($350)

Reasons:

1. In 2nd month, the profit calculated under absorption costing is higher than that of marginal costing. It is because when production exceeds sales, there will be an increase in closing stock and a greater portion of the fixed production overhead will be included in the closing stock and carried forward to next period.

2. In 3rd month, the profit calculated under absorption costing is lower than that of marginal costing. It is because when sales exceedsproduction, there will be a decline of closing stock and a greater portion of the fixed production overhead is brought forward as an expenses in the opening inventory.

32

32Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Task 5 (b) – Method Selection

As more T-shirts will be sold in summer, which costing method should be adopted?

Teacher invites volunteers to give their opinions on this question.

In a business that relies on seasonal sales and in which production is built up outside the sales season to meet demand, the full amount of fixed overhead incurred will be charged against sales under marginal costing system. If so, losses will be reported during out-of-season period, and large profit will be reported in the periods when the goods are sold. By contrast, in an absorption costing system, fixed overheads will be deferred and included in the closing inventory valuation, and will be recorded as an expense only in the period in which the goods are sold. Losses are therefore unlikely to be reported in the periods when stocks are being built up. Therefore, if more T-shirt will be sold in summer, absorption costing should be adopted to provide more logical profit calculation.

33

33Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Summary for lesson 1

Major Differences in the 2 costing methods:

Marginal Costing Absorption Costing

1. Cost classification Fixed vs. variable Production vs. non-production

2. Inventory valuation Variable production Full production costs costs only (Variable + Fixed)

3. Treatment of “fixed” Period expenses Product costproduction costs (charged to P/L a/c) (absorbed into units produced)

4. Profit & sales Profit is a function of Profit is a function of relationship sales sales and production

Teacher concludes the lesson and highlights the difference between marginal and absorption costing.

Rational behind marginal costing – Fixed costs relate to a period of time and are the same irrespective of sales and production. They should be charged directly to the P/L account as period expenses. On the other hand, variable costs are the marginal costs incurred in production and stock is therefore to be valued at VARIABLE production costs only.

Rational behind absorption costing – All costs incurred in the production of a product are required to be allocated/absorbed into the product. Stock is therefore to be valued at FULL production costs.

34

34Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Summary for lesson 1

Major DifferencesMajor Differences in the 2 costing methods:in the 2 costing methods:

5. Effect of changes in period-end closing stock level on profit:

(a) When closing inventory increases Marginal < Absorption(i.e. Production > Sales) costing profit costing profit

(b) When closing inventory decreases Marginal > Absorption(i.e. Production < Sales) costing profit costing profit

(c) When closing inventory is unchanged Marginal = Absorption(i.e. Production = Sales) costing profit costing profit

Teacher concludes the lesson and highlights the difference between marginal and absorption costing.

Teacher may ask the following questions to test students’ understanding:

Q1: Why does profit calculated under marginal costing greater than absorption costing when closing stock increases?

(Answer: It is because under absorption costing, a portion of the fixed production overhead will be included in the closing stock and carried forward to the following period. But under marginal costing, the total amount of fixed production overhead is charged to the profit and loss account in the period it incurs)

Q2: Why does profit calculated under marginal costing less than absorption costing when closing stock drops?

(Answer: It is because under absorption costing, a greater portion of the fixed production overhead will be written off when the goods are sold.)

Q3: In the long run, which costing method will generate a higher profit?(Answer: Both methods will give the same profit because the total costs will be the same in the long run)

35

35Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Preparation for next lesson

Marginal CostingMarginal Costing Absorption CostingAbsorption Costing

Advantages

& Disadvantages

Teacher asks students to think over the advantages and disadvantages of marginal costing and absorption costing for next lesson.

End of Lesson 1.

36

36Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

A Case study:A Case study:

Bullet Manufacturing Bullet Manufacturing

CompanyCompany

(Refer to Student Worksheet p.10)

Lesson 2

Teacher introduces the case to students and states the problem faced by the Managing Director, Alice, of Bullet Manufacturing Company.

- Bullet has been using absorption costing for internal reporting purpose.

- In the month of July, production of Bullet exceeded sales and the profit statement showed a decline in profit margins despite a 20% sales increase.

- The accounting manager was asked by the marketing manager to explain this contradictory result.

- The issue of using marginal costing was brought up and Alice wasdeciding whether to switch to marginal costing for internal reporting purpose.

37

37Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Activity 3: Debate

“ Bullet Manufacturing Company should use marginal costing instead of

absorption costing in preparing the company’s accounting reports”

Teacher divides students into 2 groups and sets up a topic for debate: “Bullet Manufacturing Company should use marginal costing instead of absorption costing in preparing the company’s accounting reports”

• Divide students into two groups. Assign one group as the affirmative side and the other group as the opposition side.

• Remind students to read the case on Student Worksheet page 17.

• Give students 15 minutes to discuss and formulate their arguments. (Teacher may guide students through their discussion by asking the following questions. Answers can be found on slide 42-45)

Which costing method is easier to use and understand?Which method better suits the need of management for cost control and internal performance evaluation?Which method is required by current accounting standard for external reporting?What are the pros and cons of including fixed overheads in stockvaluation?How would the changes of inventory level affect profits under each method?In case of highly fluctuating levels of production, which costing method will give a more realistic set of cost data?Which costing method will give a more accurate picture of how a firm’s cash flows are affected by changes in sales volume?Which costing method will show a clearer relationship between cost, price and volume?

38

38Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Each group nominates onerepresentative to present their views and arguments.

Use marginal costing as ….

Use absorption costing as ….

Each group will name one representative who will be allowed 4 minutes to present the group’s views and arguments.

After the presentation, teacher goes through the advantages and disadvantages of each method, draws conclusion and decides the winner based on students’ arguments and performance.

39

39Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

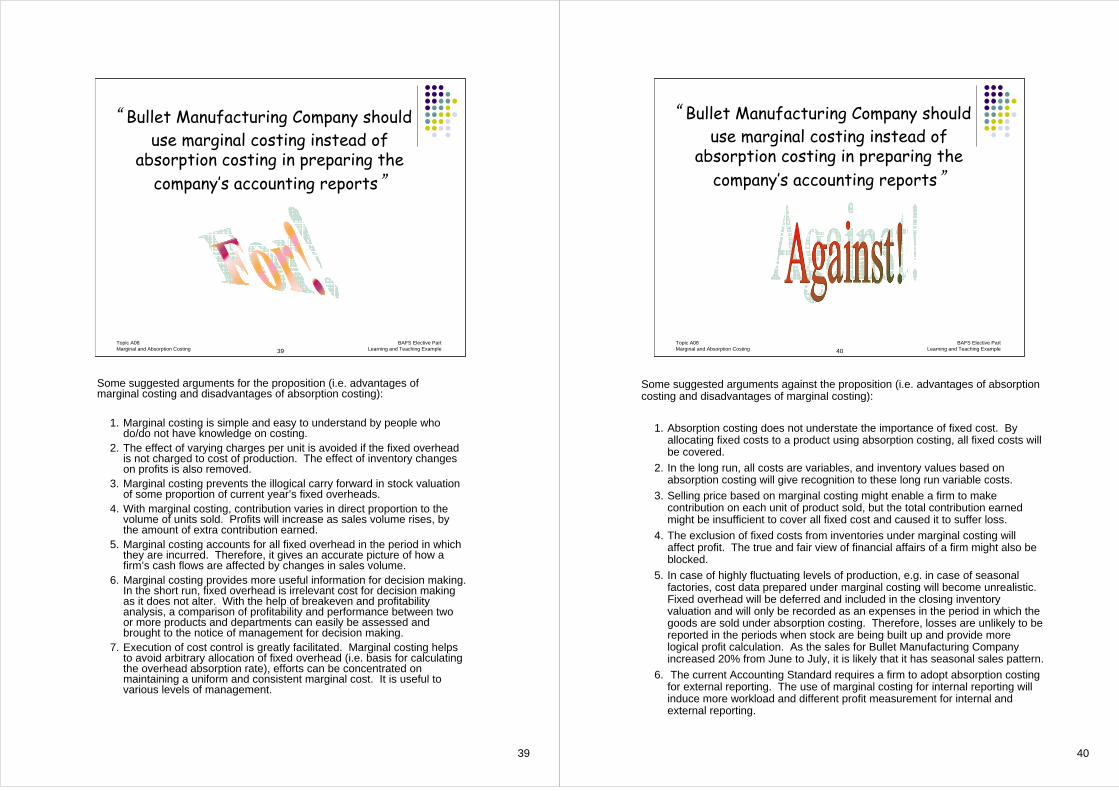

“ Bullet Manufacturing Company should use marginal costing instead of

absorption costing in preparing the company’s accounting reports”

Some suggested arguments for the proposition (i.e. advantages of marginal costing and disadvantages of absorption costing):

1. Marginal costing is simple and easy to understand by people who do/do not have knowledge on costing.

2. The effect of varying charges per unit is avoided if the fixed overhead is not charged to cost of production. The effect of inventory changes on profits is also removed.

3. Marginal costing prevents the illogical carry forward in stock valuation of some proportion of current year’s fixed overheads.

4. With marginal costing, contribution varies in direct proportion to the volume of units sold. Profits will increase as sales volume rises, by the amount of extra contribution earned.

5. Marginal costing accounts for all fixed overhead in the period in which they are incurred. Therefore, it gives an accurate picture of how a firm’s cash flows are affected by changes in sales volume.

6. Marginal costing provides more useful information for decision making. In the short run, fixed overhead is irrelevant cost for decision making as it does not alter. With the help of breakeven and profitability analysis, a comparison of profitability and performance between two or more products and departments can easily be assessed and brought to the notice of management for decision making.

7. Execution of cost control is greatly facilitated. Marginal costing helps to avoid arbitrary allocation of fixed overhead (i.e. basis for calculating the overhead absorption rate), efforts can be concentrated on maintaining a uniform and consistent marginal cost. It is useful to various levels of management.

40

40Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

“ Bullet Manufacturing Company should use marginal costing instead of

absorption costing in preparing the company’s accounting reports”

Some suggested arguments against the proposition (i.e. advantages of absorption costing and disadvantages of marginal costing):

1. Absorption costing does not understate the importance of fixed cost. By allocating fixed costs to a product using absorption costing, all fixed costs will be covered.

2. In the long run, all costs are variables, and inventory values based on absorption costing will give recognition to these long run variable costs.

3. Selling price based on marginal costing might enable a firm to make contribution on each unit of product sold, but the total contribution earned might be insufficient to cover all fixed cost and caused it to suffer loss.

4. The exclusion of fixed costs from inventories under marginal costing will affect profit. The true and fair view of financial affairs of a firm might also be blocked.

5. In case of highly fluctuating levels of production, e.g. in case of seasonal factories, cost data prepared under marginal costing will become unrealistic.Fixed overhead will be deferred and included in the closing inventory valuation and will only be recorded as an expenses in the period in which the goods are sold under absorption costing. Therefore, losses are unlikely to be reported in the periods when stock are being built up and provide more logical profit calculation. As the sales for Bullet Manufacturing Company increased 20% from June to July, it is likely that it has seasonal sales pattern.

6. The current Accounting Standard requires a firm to adopt absorption costing for external reporting. The use of marginal costing for internal reporting will induce more workload and different profit measurement for internal and external reporting.

41

41Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Conclusion

Teacher concludes the debate by setting the scene:

- Management normally requires accounting reports, especially profit statements, for each major product group or segment of the business for evaluating the performance of divisional managers. In general, the identification of variable costs and contribution will facilitate management’s decision making (e.g. budget decision) and enable management to easily see how contribution will be affected by changes in sales volume.

- On the other hand, absorption costing is useful of setting selling prices as full production is covered.

42

42Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Advantages of Marginal Costing

Easy to understand Fixed overheads are excluded from inventory costs Fixed overheads are NOT carried forward in stock valuation Contribution and profits is directly driven by salesFocus on the controllable aspect of a business

Teacher concludes the lesson by highlighting the advantages of marginal costing.

Marginal costing can:

- avoid arbitrary allocation of fixed overheads.- avoid the varying charges per unit and hence distortion in stock

valuation.- avoid the effect of changes in closing inventory level on profits.- show clearly the effect of sales on cash flows and the relationship

between cost, price and volume.- facilitate the execution of cost control.

43

43Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Disadvantages of Marginal Costing

Marginal costing ignores that fixed costs must be recovered over the long runFinished goods and work in progress stock will be understatedIt fails to recognise that all costs are variable over the long runFirms with seasonal sales patterns, profits will fluctuate greatlyNot easy to establish the cost variabilities

Teacher concludes the lesson by highlighting the disadvantages of marginal costing.

In marginal costing,

- selling price is based only on marginal cost, it’s possible that a positive contribution earned might NOT be sufficient to cover all fixed costs in the long run.

- the practice of exclusion of fixed cost from inventory valuation does not conform to acceptable accounting practice.

- losses will be reported during the slack season while huge profits will be reported in the peak season. This problem is avoided if absorption costing is used because fixed overheads will be deferred in the closing inventories and will only be expensed in the period they are sold.

- variable costs are rarely completely variable and fixed costs are rarely completely fixed.

44

44Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Advantages of Absorption Costing

Fixed costs are absorbed in inventoryRecognition of the importance of fixed overheads in productionCompliance with Accounting StandardsAll costs are variable over the long run Less fluctuation in profits

Teacher concludes the lesson by highlighting the advantages of absorption costing.

Using absorption costing:

- can ensure all fixed costs will be recovered and met in the long run.- will not understate the finished goods and work in progress stock

value and helps to give a true and fair view of the financial affairs of a firm.

- can comply with the external reporting requirement recommended by the Accounting Standards.

- can recognise all “long run variable” costs. - there will be less fluctuation in profit when production remains

constant but sales fluctuate.

45

45Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Disadvantages of Absorption Costing

More complicated Fixed overheads are charged to production Part of the current year’s fixed overheads are carried forward in closing stock to the following year Profit is not a direct function of salesRelationships between cost, price and volume is ignored

Teacher concludes the lesson by highlighting the disadvantages of absorption costing .

In absorption costing,

- one has to make arbitrary assumptions on apportionment of fixed overheads (based on overhead absorption rate).

- the unit inventory costs may vary according to production.- management may manipulate profits by building up inventories and

hence deferring the fixed overheads to the following years.- there’s possibility that profit may drop even though sales goes up. - the relationships between cost, price and volume is ignored since the

focus is on total cost.

46

46Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Summary for lesson 2

Both marginal and absorption costing systems have their own advantages and limitations.

Therefore, management must decide which method provides more meaningful information to meet planning, control and decision making needs.

Teacher concludes the lesson and highlights the main uses of marginal and absorption costing.

47

47Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

Summary for lesson 2Which costing system would you choose?

Marginal Costing

Absorption Costing

Short run decision-making

Long run decision-making

When sales is subject to high seasonal fluctuationsComparison of performance of different departments/product linesExternal reporting

Teacher concludes the lesson by inviting students to choose the preferred costing method under different circumstances, students can also mark the answer in student worksheet p.20.

• Short-run decision making – fixed overheads are irrelevant for decision making in the short run as it does not change. Marginal costing is preferred.

• Long-run decision making – all costs are variable and relevant in the long run; and fixed costs must be met. Absorption costing is preferred.

• When sales is subject to high seasonal fluctuations – during the out-season periods when production are greater than sales and inventories are built up, huge losses will be reported under marginal costing because the full amount of fixed overheads incurred in production will be expensed in that period.

• On the contrary, during high seasons when sales are greater than production, huge profits will be reported under marginal costing because the amount of fixed overheads written off to the profit and loss account remain the same.

• Comparison of performance of different departments and product line – marginal costing provides information on contribution which enables management to easily get a clear picture of performance.

• External reporting – the inclusion of fixed costs in inventories will give a true and fair view and is required by accounting standards. Absorption costing is to be used.

Teacher asks students to complete the crossword puzzle (Activity 4, Student Worksheet page 20-21) at home so as to check their understanding on the concepts of marginal and absorption costing. The answers will be distributed in next lesson.

48Topic A08Marginal and Absorption Costing

BAFS Elective PartLearning and Teaching Example

The End

End of Lesson 2.

Topic A08: Marginal and Absorption Costing Student Worksheet p.1

BAFS Learning and Teaching Example As at April 2009

BAFS Elective Part – Accounting Module – Cost Accounting Topic A08: Marginal and Absorption Costing

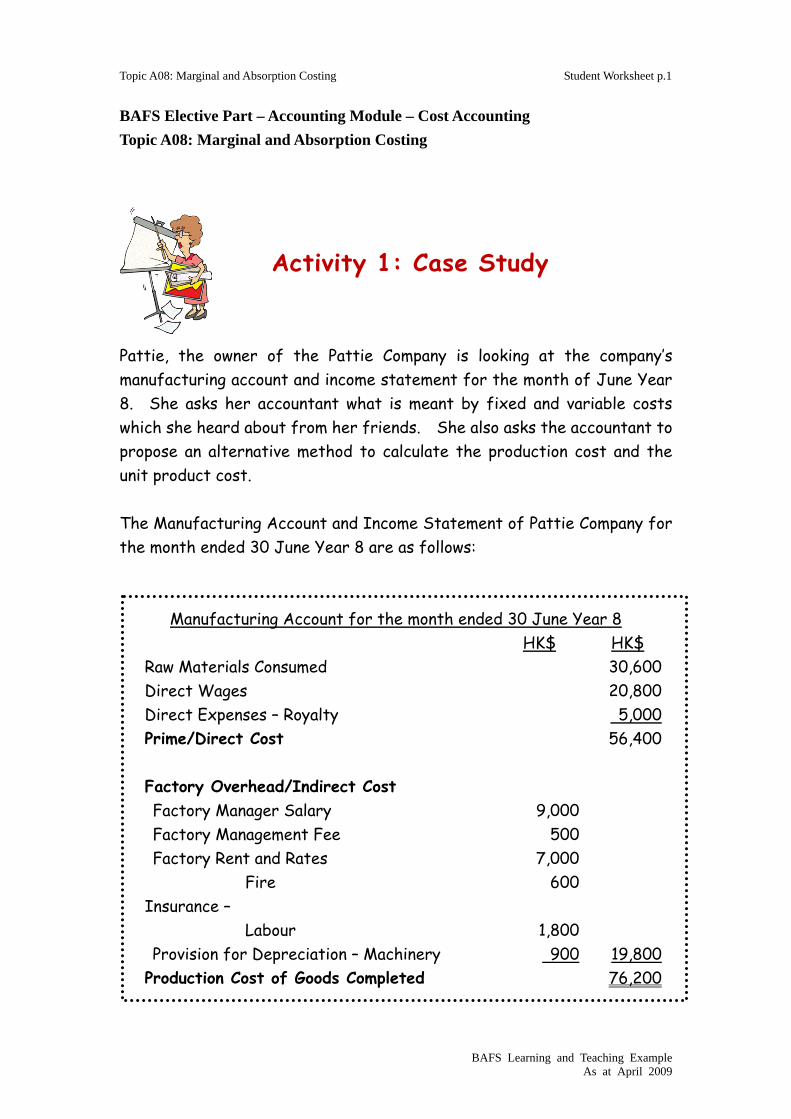

Pattie, the owner of the Pattie Company is looking at the company’s manufacturing account and income statement for the month of June Year 8. She asks her accountant what is meant by fixed and variable costs which she heard about from her friends. She also asks the accountant to propose an alternative method to calculate the production cost and the unit product cost. The Manufacturing Account and Income Statement of Pattie Company for the month ended 30 June Year 8 are as follows:

Manufacturing Account for the month ended 30 June Year 8 HK$ HK$ Raw Materials Consumed 30,600 Direct Wages 20,800 Direct Expenses – Royalty 5,000 Prime/Direct Cost 56,400 Factory Overhead/Indirect Cost Factory Manager Salary 9,000 Factory Management Fee 500 Factory Rent and Rates 7,000 Insurance –

Fire 600

Labour 1,800 Provision for Depreciation – Machinery 900 19,800 Production Cost of Goods Completed 76,200

Activity 1: Case Study

Topic A08: Marginal and Absorption Costing Student Worksheet p.2

BAFS Learning and Teaching Example As at April 2009

Income Statement for the month ended 30 June Year 8 HK$ HK$

Sales 191,475 Less: Production Cost of Goods Sold Finished Goods Opening Stock (57

units) 1,710

Add: Production Cost of Goods Completed

76,200

77,910 Less: Finished Goods Closing Stock (44

units) 1,320 76,590

Gross Profit 114,885 Less: Expenses Bank Loan Interest 750 Provision for Depreciation: Office Equipment 250 Cleaning Expenses 159 Salesmen’s Salaries 12,643 Carriage Outwards 195 Advertising 190 Sales Commission 445 Office Rent and Rates 7,905 22,537 Net Profit 92,348

Topic A08: Marginal and Absorption Costing Student Worksheet p.3

BAFS Learning and Teaching Example As at April 2009

You, as the accountant of the Pattie Company, decide to use the company’s spending to explain to Pattie about the characteristics of fixed and variable costs. To facilitate the calculation of unit product cost, you also try to allocate the cost/expenses to production cost and non-production cost. Identify the fixed, variable, production and non-production costs from the Pattie Company’s Manufacturing Account and Income Statement for the month ended 30 Year 8. The first example is given for reference.

Fixed Cost Variable Cost Production Cost Non-Production Cost

Direct Materials Direct Materials

Task 1: Cost Classification

Topic A08: Marginal and Absorption Costing Student Worksheet p.4

BAFS Learning and Teaching Example As at April 2009

Assuming 2,540 units of goods were produced by the Pattie Company for the month of June Year 8, the production cost for each unit would be:

Task 2: Cost Computation

Total Production Cost: Unit Produced: Unit Product Cost = Total Production Cost ÷ Unit Produced = =

Topic A08: Marginal and Absorption Costing Student Worksheet p.5

BAFS Learning and Teaching Example As at April 2009

You decide to recast the March Income Statement using Marginal Costing and present it to Pattie to show the major effects when this method is used. (a) Suppose Marginal Costing system is used. Construct an Income

Statement for the Pattie Company for the month ended 30 June Year 8. (Assuming variable production cost for opening stock is $22/unit and the company uses First In-First Out method for stock valuation.)

Unit Selling Price = Sales Revenue ÷ No of units sold =

=

Opening Stock Value (57 units) = = Variable Production Cost =

= Closing Stock Value (44 units) = = Variable Non-production Cost =

= Fixed Production Cost =

= Fixed Non-production Cost =

=

Task 3: Income Statement

Topic A08: Marginal and Absorption Costing Student Worksheet p.6

BAFS Learning and Teaching Example As at April 2009

Income Statement for the month ended 30 June Year 8

HK$ HK$ Sales Less: Variable Production Cost of Goods Sold Finished Goods Opening Stock Add: Variable Production Cost Less: Finished Goods Closing Stock

Less: Variable non-production cost Contribution Less: Fixed cost Production Non-production Net profit

(b) Compare the Income Statement prepared in part (a) with that

prepared under Absorption Costing. State the major effects of using Marginal Costing and explain why this happened. Hints: Differences of Absorption Costing and Marginal Costing and their impacts on inventory valuation and profit determination.

Absorption Costing Marginal Costing

Differences in the 2 costing systems

(a) How are fixed production costs treated?

(b) If closing stock , what will happen to part of the fixed production cost?

(a) How are fixed production costs treated?

(b) If closing stock , what will happen to the fixed production cost?

Inventory valuation

Higher / Lower closing stock value (reason (a) above)

Higher / Lower closing stock value

(reason (a) above) Impact on

Income determination

Higher / Lower profit (reason (b) above)

Higher / Lower profit (reason (b) above)

Topic A08: Marginal and Absorption Costing Student Worksheet p.7

BAFS Learning and Teaching Example As at April 2009

Major Effects: Reasons:

Topic A08: Marginal and Absorption Costing Student Worksheet p.8

BAFS Learning and Teaching Example As at April 2009

Form a group of four or five. Read the following case carefully and complete the tasks. It’s the end of May and summer vacation is near. To gain practical experience and make some pocket money, you and your classmates come up with an idea to set up a cyber-firm to sell custom designed heat-transfer print T-shirts on Yahoo. Today, you and your classmates hold an informal meeting at the school canteen to discuss and to work out a business plan.

Activity 2: Case Study

Topic A08: Marginal and Absorption Costing Student Worksheet p.9

BAFS Learning and Teaching Example As at April 2009

After conducting market research and lengthy discussions, your group comes to the consensus that the project is a feasible and could be a go-ahead. List the fixed and variable costs incurred in setting up a cyber-firm selling your own custom designed heat-transfer print T-shirts on the Internet:

Task 1: Cost Classification

Fixed Costs:

Variable Costs:

Topic A08: Marginal and Absorption Costing Student Worksheet p.10

BAFS Learning and Teaching Example As at April 2009

One of your classmates has the computer, laser printer and essential software to custom design and print images. However, you are required to forecast the monthly business operating costs for further discussion on required initial capital. Estimate the monthly running cost of the business (assuming 500 T-shirt will be produced per month) and complete the following table:

Task 2: Cost Estimation

Cost Items: HK$

Monthly service fee paid to Yahoo Hire charges for heat transfer machines (Assuming 2 machines will be hired)

T-shirt purchase cost Transfer paper for laser printer Packaging tools and materials Printing charges (e.g. cartridge) Others:

Topic A08: Marginal and Absorption Costing Student Worksheet p.11

BAFS Learning and Teaching Example As at April 2009

A list of costs related to the operating the business is created up after the discussions. Your group would like to use cost-plus pricing to establish the selling price. As you have learnt marginal and absorption costing in your previous studies, you decide to apply your knowledge to compute the unit cost. (a) Classify the following cost items according to the characteristics of

Marginal and Absorption costing systems and complete the table:

Cost Classification under Cost Items Details Fixed or Variable

Production or Non-production

Service fee paid to Yahoo

$400/month Fixed Cost

Non-production cost

Hire charges for 2 heat transfer machines

$1,500/ month

T-shirt purchase cost $15/piece

Transfer paper $4/sheet

Printing charges $3/sheet

Packaging tools & materials

$2,000/ month

Stationery expenses

$300/month

Advertising fee (a fixed amount charged by an advertising firm)

$1,000/ month

Transaction fee charged by Yahoo

1.5% on sales

Delivery charges 1% on sales

Task 3: Cost Computation

Topic A08: Marginal and Absorption Costing Student Worksheet p.12

BAFS Learning and Teaching Example As at April 2009