A021 - Information Champions - A People - Services and Productization Approach

29

Dec 2010 Information Champions: The People, Product & Services Framework Creating Information Leadership in the Banking Industry Bernard Sia ([email protected])

-

Upload

catatoniaunlimited -

Category

Documents

-

view

221 -

download

0

Transcript of A021 - Information Champions - A People - Services and Productization Approach

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 1/29

Dec 2010

Information Champions: The

People, Product & Services

Framework

Creating Information Leadership in the Banking

Industry

Bernard Sia ([email protected])

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 2/29

Page 2

EXECUTIVE SUMMARY

Information tends to take a lif e of its own with the prolif eration of disparate vertical, niche based and point

information solutions introduced throughout the lif e time of the business. Instead of managing the complexity,

organizations allowed the complexity to bury nuggets of intelligence where the effort to identify the proverbial

needle becomes more expensive than the negative results of making off the cuff decisions backed only by hunches.

Management consultants have attempted to provide horizontal based best practices and process abstractions that

unfortunately, have not been able to relate to the business and thus turn academic; resulting in artifacts resting

atop dust ridden shelves.

The solution lies in orientating the business decision making through business seeing glasses versus technological

myopia. In summary, the ability to truly demarcate and identify the value chain of the organization to uncover

essential business advantage.

The objective of this document is to produce a banking picture of how decision making should be supported and

enhanced by information. We aim to produce an actionable model that can be adopted immediately provided that

there are leaders who know where the organization should be and acts on meeting these goals.

THE PROBLEM STATEMENTS

MATRIX MADNESS, KINDA LIKE HELIUM

As Helium can exist as a superf luid at 2.17 degrees Kelvin (-271 Celcius) where liquid viscosity disappears,

exhibiting zero friction and thermal conductivity skyrockets; the same principles apply to organizational

accountability that lacks a central figure head. The situation requires tremendous energy to bring the excited

state of hot and gassy molecules to exhibit superf luidity; as an analogy, the performance levels required from a

performing organization. Thus having multiple organizational units accountable for similar sets of information will

only lead to conf lict and situational deadlocks and misalignment. Throw in a matrix reporting structure and

madness ensues.

BUSINESSES AND PEOPLE ARE NOT STATIC: DYNAMISM REQ UIRED

Various researchers have shown how conf licts, disasters and issues lead to unfreezing moments (Bruland, 1982), (Carley and Harrald ,1997), (Dutton, 1986); which unfortunately, is a sad but a very real phenomenon of managing

a virtual concept that exists only in the mind the business organization.Only through conf lict can we see that the

mirage of stability is not real, organizations require continuous change and fresh inputs.

An organization is not in the logo, in its walls, or departmental units; the organization is f luid and the virtual nature

means that the CEO must heard mists to coalesce into some semblance of transitionary reality. In line with that

spirit, any form of structural rigidity is also an illusion of control as it will only lead to myopism in both vision and

restrict the dynamism required to perform.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 3/29

Page 3

This problem is ref lected above, where a superuser group in B) is typically created to off load information

processing from actual customer fronting business people. Although still kept within the business structure, the

model is static. Superusers slowly but surely devolve into IT-speak; losing the business knowledge edge that the

team initially had. Instead of forcing down and evolving information needs, Superusers begin to def end the

inefficiencies and issues of IT. The biggest symptom of this happening is with organizations where the Superusers

are equated to the system, for example, Superuser A is in charge of the CRM system or Data Warehouse.

When the structure stagnates, f urther symptoms appear; for e.g. data inaccuracies, inability to identify information

needs and improvement pro jects which are summarily rejected by management because the team has lost the

business-speak required to quantifying and justify the improvements.

IN ORDER TO BUILD THE FUTURE, WE NEED TO BE COGNIZANT OF HISTORY

Alas, to address how strategically a virtual concept like business can be directed, the business needs to know

where it stands today and where it needs to be tomorrow; in relation to its competitors, itself , its customers and

stakeholder expectations.

The information management unit of the organization needs to build upon lessons learned much like how software

evolves from one f eature set to the next. Take the iPhone for example, and how Apple has continuously in jected

incremental improvements into a single branded product. An organization that does not have a productization

mindset will suff er the curse of repeating history. So we beg the question of whether a company has a soul, can it

ref lect and improve or choose to live only by the moment? And to answer the rhetoric, the soul is within the

product and services that the organization provides, the ability to evolve and improve upon the product f eature

set consciously and with deliberate intent.

So information evolution and the intelligence to make decisions from collective corporate information and

evolving these requirements as the company grows is a f undamental f eature of productizing information.

An organization without an information soul will be perpetually damned.

Figure 1 - Typical Static people configuration for Business/Application Services

Direction of Services offered

Business

A) Customer

Fronting

Business Users

B) Superusers

manages the

business

application

C) Information

Technology

supporting the

system

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 4/29

Page 4

SOLUTION SUMMARY INFORMATION AS A DYNAMIC SERVICE PRODUCT

In summary, we need to transition the existing environment where businesses own and inf luence information

technology adoption to a clean separation between business and IT per the figure below:

Figure 2 - Information as a Service

I n f o

r m a t i o

n R

e q u e

s t s

The vision is a service and f unction oriented approach where Information Owners displaces Information

Systems Owners. The definition, evolution and lif ecycle of usef ulness of the information will f undamentally be an

information governance activity that resides within the business.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 5/29

Page 5

Figure 3 A Balanced State of Existence sans Intermediaries (e.g.-> Info System owners)

Business

IT

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 6/29

Page 6

SOLUTION CA SE STUDY: THE BANKING INDUSTRY

In identifying information needs for the banking industry we must begin with identifying how value traverses

through the banking business. For purpose of simplicity we will only cover 4 aspects of banking, namely Retail,

Wholesale, Investment and Insurance. We will also perform a high level abstraction of how banking f unctions as a

financial intermediary between business to business, customer to business and customer to customer;

f undamentally, the lubricant that facilitates economic transaction and vis-à-vis national growth.

An important paradigm for the reader to adopt is that this is seen from a 3rd

party external view of the bank and

should not be conf used with how the bank examines itself internally. After which we will then analyze

informational needs required to both monitor and control the processes for performance. Secondly, we will

disregard whether the services are delineated by Islamic or conventional banking.

The figure below attempts to capture the essence of banking (from a customer standpoint) and we will then

explain how the services are consumed. Note that we will cover how the banks work with regulators subsequently.

In summary, economic activities are circular in nature, much like night and day; people buy and sell goods, and

buying can be f uelled by financing attained through loans, or should the consumer be a corporate entity, avenues

to attain f unds through listing appear. Banks facilitate this by providing credit and payments infrastructure,investment banking underwriting services, enabling even more buying and selling, thus perpetuating the cycle.

In short, banks should continuously ask the question, What business are they in?; what is the bigger picture? Are

banks in the loans or banking business?

Or are banks really in the business of business?

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 7/29

Figure 4 Abstraction of Major Banking Services

Note: Trustees, Will writing, estate management, venture capitalism are ignored for simplicity, and wealth management services are also left out on

simplified, and claims process are also hidden and abstracted as part of facilitating a payment transaction. There are also more complex activities in

exposure through securitization and structured products that we will not cover.

Business Activity

Flow of Transaction

Banking Services

Other Banking Services(e.g. Leveraging)

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 8/29

Page 8

Key

Activities

Description

1

At the end of the day, people and businesses need to pay for consumption.

2

Customers conduct investing activities through shares, bonds, options etc.

Customers also require financial protection through insurance products

Corporate customers conduct larger payments

Corporate customers also require a means to track payments that they receive, also to manage their trade re

A corporate customer may also acquire another corporate entity, and this transaction may require f unding a

Customers also require more f unding for business growth through private debt securities and/or equities

Ultimately, all the activities above will result in money changing hands.

A Simpl if ied View of the Banking Value Chain

Now we shift the paradigm inwards, where the ma jor activities above can be explained through the following value chains.

Ma jor Value Chain Description Ma jor

Business

Line

Input Output Value Added Objective

To marry retail/corporate

customers deposits with financing

needs of both other retail and

corporate customers (This can be

viewed in reverse from a financing

standpoint)

Retail

Banking and

Whole Sale

Banking

Deposits/

Savings

Financing and

credit

y The ability to widen the gap betwe

and the profits of providing credit.

y The ability the lower the cost of pr

y The ability to provide competitive

competitors)

To provide a bundled corporate

banking services that can

expediently assist and reinforce

the monetary transactions of

businesses

Whole Sale

Banking

Deposits,

Payments,

Receivables

Financial

Advice,

Product

bundles

y The ability to provide an end to en

package that is facilitative to busin

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 9/29

Page 9

To marry retail and corporate

investors with organizations seek

financing through private debt

placements or securities or

convertibles

Investment

Banking

Investments Underwriting

Services

y The ability to create a brand (prof e

expediency)

y The ability to understand the busin

to potential customers.

y The ability to perform all of the ab

To provide advisory and

consultancy services on corporatemergers and takeovers

Investment

Banking

Corporate

information

Advisory

Services

y The ability to value a takeover/me

y The ability to structure a leverage

raising activity required, suited to t

well as its day to day business ope

To provide a payments and

remittance infrastructure

Retail/Corpo

rate Banking

Entity,

Location,

Monetary

Amount

Successf ul

Transf er

y To provide the most competitive ra

convenient experience for this serv

To provide financial protection to

customers

Insurance Risk

Aggregate

Coverage y To provide the most competitively

the customer while lowering the c

expedient and pleasant experience

Internal Paradigm: The

Value Chain

External Paradigm:

Business Services

External Paradigm: How a bank aff ects and

profit from surrounding

micro/macroeconomic forces

Figure 5 - Two viewpoints that needs to be factored to perform strategic and operational analysis

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 10/29

Page 10

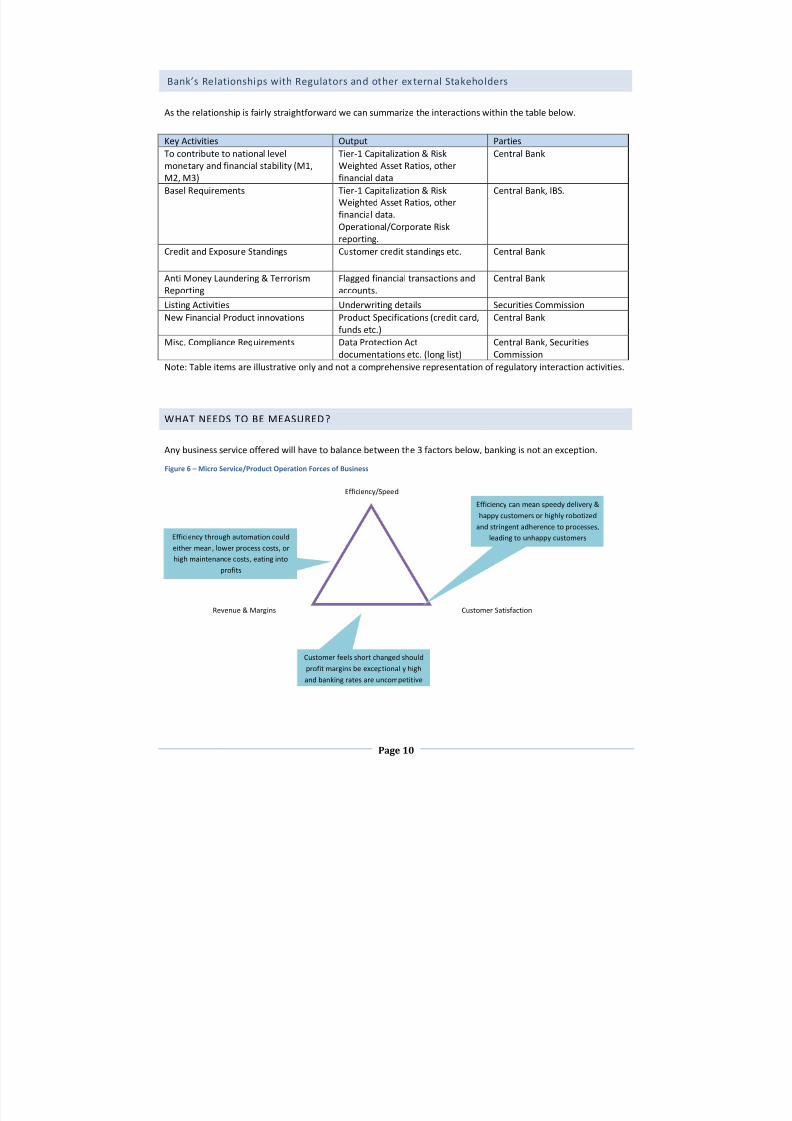

Banks Relationships with Regulators and other ex ternal Stakeho lders

As the relationship is fairly straightforward we can summarize the interactions within the table below.

Key Activities Output Parties

To contribute to national levelmonetary and financial stability (M1,

M2, M3)

Tier-1 Capitalization & Risk Weighted Asset Ratios, other

financial data

Central Bank

Basel Requirements Tier-1 Capitalization & Risk

Weighted Asset Ratios, other

financial data.

Operational/Corporate Risk

reporting.

Central Bank, IBS.

Credit and Exposure Standings Customer credit standings etc. Central Bank

Anti Money Laundering & Terrorism

Reporting

Flagged financial transactions and

accounts.

Central Bank

Listing Activities Underwriting details Securities Commission New Financial Product innovations Product Specifications (credit card,

f unds etc.)

Central Bank

Misc. Compliance Requirements Data Protection Act

documentations etc. (long list)

Central Bank, Securities

Commission

Note: Table items are illustrative only and not a comprehensive representation of regulatory interaction activities.

WHAT NEEDS TO BE MEASURED?

Any business service off ered will have to balance between the 3 factors below, banking is not an exception.

Efficiency/Speed

Revenue & Margins Customer Satisfaction

Efficiency can mean speedy delivery &

happy customers or highly robotized

and stringent adherence to processes,

leading to unhappy customers

Customer f eels short changed should

profit margins be exceptionally high

and banking rates are uncompetitive

Efficiency through automation could

either mean, lower process costs, or

high maintenance costs, eating into

profits

Figure 6 Micro Service/Product Operation Forces of Business

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 11/29

Page 11

In order to make sustainable decisions that maintains this precarious balance; succinct and accurate information

about the business performance is required. Hence we ask the reader the following questions, and it must be

answered through the following order of prioritization:-

a) Do you know the decisions that need to be made?b) Do you know how frequently these decisions are made?

c) Do you know the information that is required to support the decision?

d) Do you trust the information provided?

e) Do you have the information?

If the answer for the first question is not available, we should not proceed with any strategic uses of information

and work on operational needs only (keep the lights on activities). Any attempt at strategic uses will only lead to

wastef ul IT centric implementations with little value as the organization lacks the strategic maturity and will to

profit from the information. Interpreted diff erently, the business has no soul; it f unctions like a machine.

Another key takeaway is organizations that spend an inordinate amount of time gathering thousands of fields without knowing why the business makes the decisions that they do. Organizations that begin their information

management journey from the bottom up will be lost in the diarrhoea of data.

Lastly, the act of measuring and extracting information can also lead to behaviours that sacrifices one area for

the other. For example, most KPI systems fail to address corporate performance holistically, information are

typically massaged to look good and the KPI becomes an end in itself. Finally, the company falls into the trap of

reporting a KPI that has no correlation with actual business performance.

A good information management system and process are able to attain the required information for decision

making without in jection of decision making bias as well as disrupt the natural ecosystem of the business f low.

BREAK ING DOWN THE CASE: AN END TO END VALUE CHAIN ANALYSIS

For the example below we will break down the first value chain, bridging of depositors which has money with

creditors that require money into its individual processes.

Ma jor Value Chain

Description

Ma jor Business

Line

Input Output Value Added Objective

To marry retail/corporate

customers deposits with

financing needs of both

other retail and corporate

customers (This can be

viewed in reverse from a

financing standpoint)

Retail Banking and

Whole Sale

Banking

Deposits/

Savings

Financing

and

credit

y The ability to widen the gap between the cost of maintaining

deposits, and the profits of providing credit.

y The ability the lower the cost of providing these services

y The ability to provide competitive financing (compared to

competitors)

Although as explained above, that business activities looped back into it self , the internal intermediary processes

can be strung out and analyzed f urther.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 12/29

Page 12

Figure 7 - From Deposits to Loans

We are thus able to perform several key decisions to improve business performance; the triple forces described

previously apply as yardsticks. Ma jor processes within the value chain are in orange and secondary activities

spawned from the ma jor processes are in yellow. The subsections below describe potential information reporting

aggregation.

PRODUCT ADOPTION PERFORMANCE

We can boil down production adoption performance into several areas, for example:-

a) Conversion rate of new product marketing activities

b) Performance of current product, i.e. large number of NPLs is a symptom (which can be caused by systemic

economic factors or overzealous sales) and having 10 million depositors is not indicative of a performing

bank should the average deposit size be 1 dollar.

c) Ability to ascertain the elasticity of investing on one or more of the 2 factors (customer & efficiency), and

how it impacts the banks bottom line.

Key decisions that can be made are:-

a) New product innovation in deposit and savings to increase f unds f lowing into the banks coff ers.

b) Investments that need to be made into marketing activities and the potential returns that it will provide.

c) Defining what is competitive in terms of services and f ees when compared to other banks and deciding

on a targeted marketing approach to corner the market for a particular product.

d) Accepting and rejecting operational improvement pro jects

e) How banking products should be branded and evolve from one f unction set to another.

f) Decommissioning or collapsing non-performing products.

g) Ad justing product parameters to increase profits through pricing

CUSTOMER EXPER IENCE

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 13/29

Page 13

Without delving into the details, a holistic 360 view of banking customers will uncover f urther opportunities for the

banks to purvey their products. A key point here is that customer experience is highly correlated with product

performance (i.e. the overall service package experience). Secondly, customer analysis should ultimately focus on

customer buying behavior to capitalize on providing more services to facilitate the activity. The psychological

analysis and understanding allows the bank to compel customers to put money in the bank, be it for investment

purposes or for pure savings.

Lastly, the bank needs to understand the economic value chain of business to ensure that although money passes

from one customer to another; physically, money stays within the bank. It is not who the customers are, but who

the customer buys from and all the way up and around the economic chain.

FINANC IAL PERFORMANCE

Financial performance typically occurs at the end of the business transaction, in particular the example below. We

say so because only upon the first payment of a loan product can the bank earn revenues through interests. Should

we be examining a payment infrastructure value chain, revenues are recouped immediately through f ees charged

from each transaction.

In practice, financial performance will be taking revenue as well as cost information across all activities of the bank;

making it one of the most complex areas of information management. Ideally the financial system is a component

of an integrated ERP system consisting of human resources, procurement, and budgeting as well as materials

management.

Key decisions that need to be made are:-

a) Investment Appraisals

Should the company be spending money on a particular pro ject proposal or spend it elsewhere? Is there a

standard formula and calculation used that is understood by everyone in the organization, NPV, IRR and

Cost of capital, Discount rate used, does in factor in taxation, inf lation...?

b) Budget Performance

Should there be corrective actions made to reinforce budget utilization or should the money be

reinvested into treasury/trading activities?

c) Financial Performance

Which area of business provides the biggest revenue to the bank, and are there growth potential? Can the

bank invest more to extend its market penetration? How much should it spend (goes back to investment

appraisal)?

d) Cost Management , Treasury Performance etc the list goes on.

RISK AND EXPOSURE

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 14/29

Page 14

In order for the bank to ascertain the limit of how far it can extend itself financially through business financing,

information from the following processes is required. Looked at diff erently, a bank who is truly in control of their

risk and exposure information is able to tether at the brink of oblivion knowing confidently where the tipping point

is - a definitive competitive advantage.

Figure 8 - Information Set required to ascertain level of Financial Risk

REGULATORY REPOR TING

Regulatory reporting should be in principle, the easiest to define as the parameters are determined for the banks

by regulators. If the bank is able to perform the 4 diff erent information gathering and decision making above

efficiently and accurately, regulatory reporting is simply an easy extension.

IS IT REALLY THAT SIMPLE?

Naturally the answer is no; specifically because customers interface with the bank through various means:

If we just examine the first portion of the activity, we can already see the need for a physical presence, through a

retail branch and others specified in the figure. For each of the touch points, the bank needs to monitor service

level availability and performance. As we break down each interaction steps even f urther, the permutation for

measurements multiplies and leads to information noise. Management needs to filter out what is of value and

separate the chaff from the wheat.

We will see later how this is handled as operational needs in the organization structure section.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 15/29

Page 15

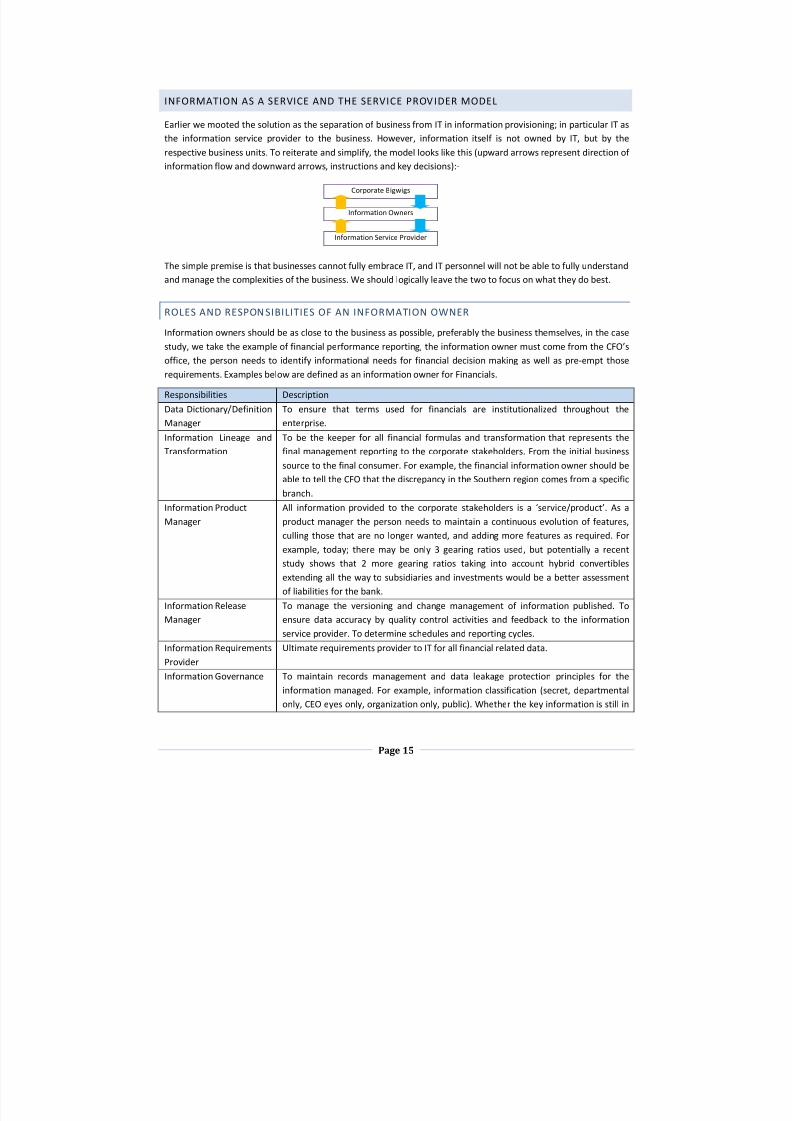

INFORMATION AS A SERVICE AND THE SERV ICE PROV IDER MODEL

Earlier we mooted the solution as the separation of business from IT in information provisioning; in particular IT as

the information service provider to the business. However, information itself is not owned by IT, but by the

respective business units. To reiterate and simplify, the model looks like this (upward arrows represent direction of information f low and downward arrows, instructions and key decisions):-

The simple premise is that businesses cannot f ully embrace IT, and IT personnel will not be able to f ully understand

and manage the complexities of the business. We should logically leave the two to focus on what they do best.

ROLES AND RESPON SIBILITIES OF AN INFORMATION OWNER

Information owners should be as close to the business as possible, pref erably the business themselves, in the case

study, we take the example of financial performance reporting, the information owner must come from the CFOs

office, the person needs to identify informational needs for financial decision making as well as pre-empt those

requirements. Examples below are defined as an information owner for Financials.

Responsibilities Description

Data Dictionary/Definition

Manager

To ensure that terms used for financials are institutionalized throughout the

enterprise.

Information Lineage and

Transformation

To be the keeper for all financial formulas and transformation that represents the

final management reporting to the corporate stakeholders. From the initial business source to the final consumer. For example, the financial information owner should be

able to tell the CFO that the discrepancy in the Southern region comes from a specific

branch.

Information Product

Manager

All information provided to the corporate stakeholders is a service/product. As a

product manager the person needs to maintain a continuous evolution of f eatures,

culling those that are no longer wanted, and adding more f eatures as required. For

example, today; there may be only 3 gearing ratios used, but potentially a recent

study shows that 2 more gearing ratios taking into account hybrid convertibles

extending all the way to subsidiaries and investments would be a better assessment

of liabilities for the bank.

Information ReleaseManager

To manage the versioning and change management of information published. To ensure data accuracy by quality control activities and f eedback to the information

service provider. To determine schedules and reporting cycles.

Information Requirements

Provider

Ultimate requirements provider to IT for all financial related data.

Information Governance To maintain records management and data leakage protection principles for the

information managed. For example, information classification (secret, departmental

only, CEO eyes only, organization only, public). Whether the key information is still in

Corporate Bigwigs

Information Owners

Information Service Provider

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 16/29

Page 16

draft stage or approved for publication. To aggregate disparate information sources

and govern the permutations of financial related information. To ensure non-

repudiation of critical corporate records and ageing e.g. archiving and disposal.

Information Area Subject

Matter expect

In this area, the person should be a Finance subject matter expert, i.e. Management

accounting, financial accounting, cost control etc. and should continuously be abreast

of the latest trend in the subject area and how it impacts the business. Regulatory requirement expertise will also be required

Key message: The information owner role cannot be static, and should be rotated on a semi-regular basis with

frontline financial personnel.

For example, on a yearly rotational basis the Head of Management Accounting & Budgeting could be the

Information Owner, subsequently the Head of Treasury etc. The idea is to attain a holistic and continuous

enrichment of reporting attributes and quality that is a close as possible to business activities. Another key

takeaway is somewhat achieving a Dewey like classification construct of aggregating information subjects together; in this case, financial information.

ROLES AND RESPON SIBILITIES OF AN INFORMATION SERVICE PRO VIDER

The information service provide is ultimately IT, and quaintly so seeing that the I stands for Information.

Responsibilities Description

Data Model

Manager/Designer

To ensure the data models used are continuously improved and kept abreast with

business f unctions. Tuned for performance and culled for lack of use.

Information Lineage and

Transformation

To be the keeper for all data mapping between source systems, datawarehouse and

business intelligence tools used to generate the reports. The ability to perform bi-

directional traceability of data stored in systems used.

Technology Product

Manager

Again, using the Financial example, the Technology Product Manager will evolve the

technology capabilities off ered through various dimensions. For example, for version

2.0 the system will now cater for both Islamic and Conventional financial reporting,

For version 3.0 it will be able to keep geographical information for each transaction

and now can be viewed over a mobile phone. These capability roadmap will be

managed by the respective product managers of both the Information Owner and

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 17/29

Page 17

Information Service Provider.

IT Planning & Operations In a nutshell, all requirements for Availability Management, Service Level

Management, Incident and Problem Management as well as the continuous

operational improvements of the technology platform used. Including Vendor

Management, Platform choice, including planning

etc. Release Manager To manage the versioning and control of the technology upgrades.

Platform Subject Matter

expect

Should IT consciously adopt a technology platform for financial information services,

the individual should be a subject matter expert for the technology used, for

illustrative example; Oracle FI or SAP FI and is able to map the next evolution and

upgrades that is required to meet the demands of the business

Similar activities for both these roles are:-

1) Change Management, all relevant training and documentation

2) Knowledge Management, continuous upkeep of the capabilities and lessons learned from being an Information Service Provider as well as an Information owner.

KEY TAKEAWAYS

1) There will no longer be an overarching information governance unit for the whole bank as the f unction is

embedded to the ma jor f unctional units.

2) Ownership of information will be a pillared aggregation of key business f unctions. For example, all

financial reporting will be focused on finance, all retail banking performance reporting will be owned by

the retail heads office and so forth.

3) Information Owners are Business Subject Matter experts.

4) A business subject matter expert need not be a process expert. A business expert is concerned with

revenues, competitive strategies, and customer satisfaction. A business subject matter expert should

ideally either hold revenue and/or operating accountability. This will ensure that only reports that are

most relevant to business decision making will be produced.

5) Information Owner role should not be a static department with a single permanent head, the head of

department should ideally f unction on a rotation basis. This ensures that the information owner is

constantly abreast with changing business needs. The longer the information owner is detached from day

to day running of the business, efficiency levels are expected to reduce.

6) The information service provider must work with the information owner to map out the next generation

capability set and business value to attain management support.

7) Finally, the service provider model means that all IT investments in providing and availing the information

to the required owners at the required service level will be done on a pay as you use cost shared model.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 18/29

Page 18

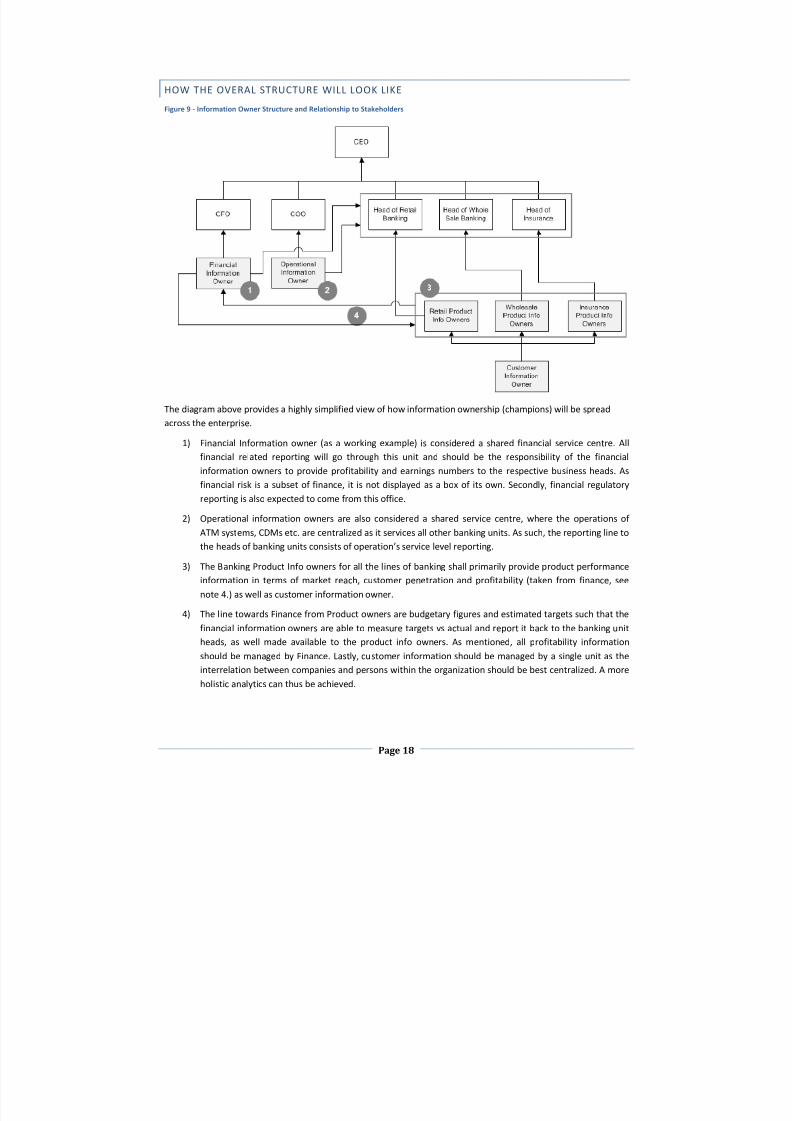

HOW THE OVERAL STRUCTURE W ILL LOOK LIKE

Figure 9 - Information Owner Structure and Relationship to Stakeholders

The diagram above provides a highly simplified view of how information ownership (champions) will be spread

across the enterprise.

1) Financial Information owner (as a working example) is considered a shared financial service centre. All

financial related reporting will go through this unit and should be the responsibility of the financial

information owners to provide profitability and earnings numbers to the respective business heads. As

financial risk is a subset of finance, it is not displayed as a box of its own. Secondly, financial regulatory

reporting is also expected to come from this office.

2) Operational information owners are also considered a shared service centre, where the operations of

ATM systems, CDMs etc. are centralized as it services all other banking units. As such, the reporting line to

the heads of banking units consists of operations service level reporting.

3) The Banking Product Info owners for all the lines of banking shall primarily provide product performance

information in terms of market reach, customer penetration and profitability (taken from finance, see

note 4.) as well as customer information owner.

4) The line towards Finance from Product owners are budgetary figures and estimated targets such that the

financial information owners are able to measure targets vs actual and report it back to the banking unit

heads, as well made available to the product info owners. As mentioned, all profitability information

should be managed by Finance. Lastly, customer information should be managed by a single unit as the

interrelation between companies and persons within the organization should be best centralized. A more

holistic analytics can thus be achieved.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 19/29

Page 19

Finally, the reader may ask, what about the information service provider? Simply, ISPs = IT; and the user should

already know that organizational structure best practices for IT is strewn in COBIT, ITIL and various other

frameworks, such; we will end our discussion on IT on that note.

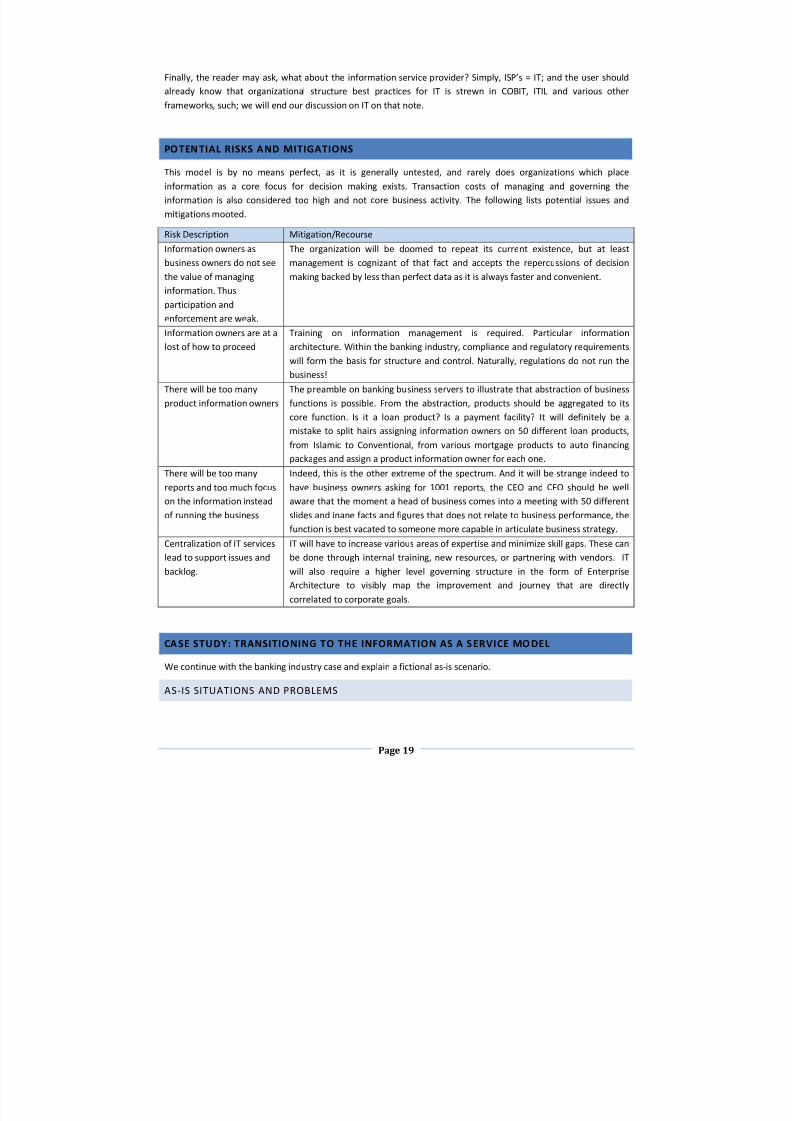

POTENTIAL RISKS AND MITIGATIONS

This model is by no means perf ect, as it is generally untested, and rarely does organizations which place

information as a core focus for decision making exists. Transaction costs of managing and governing the

information is also considered too high and not core business activity. The following lists potential issues and

mitigations mooted.

Risk Description Mitigation/Recourse

Information owners as

business owners do not see

the value of managing

information. Thus

participation and

enforcement are weak.

The organization will be doomed to repeat its current existence, but at least

management is cognizant of that fact and accepts the repercussions of decision

making backed by less than perf ect data as it is always faster and convenient.

Information owners are at a

lost of how to proceed

Training on information management is required. Particular information

architecture. Within the banking industry, compliance and regulatory requirements

will form the basis for structure and control. Naturally, regulations do not run the

business!

There will be too many

product information owners

The preamble on banking business servers to illustrate that abstraction of business

f unctions is possible. From the abstraction, products should be aggregated to its

core f unction. Is it a loan product? Is a payment facility? It will definitely be a

mistake to split hairs assigning information owners on 50 diff erent loan products,

from Islamic to Conventional, from various mortgage products to auto financing

packages and assign a product information owner for each one.

There will be too many

reports and too much focus

on the information instead

of running the business

Indeed, this is the other extreme of the spectrum. And it will be strange indeed to

have business owners asking for 1001 reports, the CEO and CFO should be well

aware that the moment a head of business comes into a meeting with 50 diff erent

slides and inane facts and figures that does not relate to business performance, the

f unction is best vacated to someone more capable in articulate business strategy.

Centralization of IT services

lead to support issues and

backlog.

IT will have to increase various areas of expertise and minimize skill gaps. These can

be done through internal training, new resources, or partnering with vendors. IT

will also require a higher level governing structure in the form of Enterprise

Architecture to visibly map the improvement and journey that are directly

correlated to corporate goals.

CA SE STUDY: TRANSITIONING TO THE INFORMATION AS A SERVICE MO DEL

We continue with the banking industry case and explain a fictional as-is scenario.

AS-IS SITUATIONS AND PROBLEMS

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 20/29

Page 20

THE ACTORS

A fictional bank contains the following departments, its daily tasks and challenges are explained.

Unit Name Roles and Achievements Challenges

Data Governance,

sits under the COO

Oversees primarily the administration

and upkeep of the Customer Master Data Management system. The team

has done an exemplar task in

maintaining consistency of Customer

Information throughout the group, but

unfortunately the sphere of inf luence

oddly stops with retail banking.

The team wishes to extend its sphere of governing

information throughout the enterprise which unfortunately, has been cornered by other units

like Enterprise InformationManagement and

Management Information System.

Enterprise

Information

Management

under Finance

Oversees the enterprise data

warehouse that is an extension of a

Financial application. Prepares

financial reporting to the CFO and

anyone else which requires financialreports

The team has total control over access of financial

information and guards all enhancements to the

system. However, issues vary between slow

system performance to inaccuracies that requires

time for revalidation. Working with IT and the MISteam to trace the problematic record or process

failures.

Management

Information

System

Department also

reporting to CFO

A program specifically created to

upgrade the business intelligence

capabilities of the bank and better

f lexibility for knowledge workers to

manage their own reporting and data

representation

Naturally being a tangent activity and somewhat

seen as IT driven, the team is fraught with

challenges in displaying that the investment has

value. The team is also receiving backlash due to

broken reports, as another pro ject which replaces

the existing Financial Accounting System (a source

system) to a new platform.

Unfortunately, the rewiring of BI reports that

dependent on the source system was not done

cleanly enough to stop the broken reports from

reaching management.

Other Banking

Units Financial

Management

structure

Fundamentally responsible for

performance reporting, market

strategy and aggregated sales

reporting up to the business unit

bosses.

Main gripes include existing reporting systems not

tailored to the respective business unit needs.

Essentially the practice is first come first serve,

where the first business unit who invests on the

said infrastructure & solution will hold a virtual

monopoly and usage. Forcing the business units to

establish their own system.

Information

Technology

The team thats responsible for the

overall operations of the IT systems as

well as configuration of the data

warehouse and BI systems.

The team is forced to capitulate whenever a new

vendor successf ully enamours the users and

introduces a new reporting tool. Platform

rationalization is only marginally successf ul and

remains a challenge due to these factors.

Secondly, rationalization exercises are not seen as

value adding to the business as it is IT focused

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 21/29

Page 21

instead of business focus. But little do business

know that these point solutions are escalating IT

support and maintenance costs.

The challenges and symptoms are all by products of:-

a) Having the user own a system/solution instead of IT. To some extent, f unding the IT improvements. This

leads to mine vs your system among the diff erent business units.

b) Allowing various units to handle essentially the same role, e.g. Data Governance roles clashes with other

Information units within Finance.

c) Inability to deliberately execute the technology investment plan from an IT standpoint as technology

selection is user driven instead of IT, leading to ad-hoc point solutions that cannot be reused or extended.

Vendor platforms, diversity and complexity skyrockets.

KEY OBJECTIVES & PROJECT TEAM STRUCTURE

Our objective is to establish a business focus information management framework where businesses drive

information needs while IT manages the technology landscape behind it. We also need to eliminate structural

issues that lead to the symptoms above.

PROJECT APPROACH & STRATEGY

In order to meet the final goal of information ownership by ma jor business f unctions, we have to start somewhere.

The strategy is to gain the most value and set the tone as well as foundation for subsequent implementation, i.e.

financial reporting and subsequently move on to other ma jor business units that can be abstracted and realigned.

For example, customer information management should be a shared service across the enterprise instead of

belonging to retail or wholesale banking separately.

1) Setting the Technical Foundation

Because of the disparate point solutions and multiple ownership of systems; head office needs to set the

example by f unding an appropriate end to end solution that can be shared across the bank. In this case a

standard solution for ETL, Data Warehousing and Business Intelligence.

If existing investment reusability is possible and the existing platforms can be expanded for this purpose;

all the better. Moving forward from there the implementation steps are similar to generic green-field

enterprise information reporting and data warehousing implementations but with a brown field inf luence

in impact analysis.

a. Establish a map and portfolio of all source systems in the bank and key data sources.

b. Establish a standard integration/extraction process

c. Establish a data model that can be expanded cleanly and quickly.

d. Establish a reporting subscription and publication model.

e. Establish a demand management process to address new information needs from other units

across the bank.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 22/29

Page 22

f. Establish a modelling process to be able to quickly simulate how information can be rapidly

provided to the business.

g. Establish a governance process to ensure that data dictionaries and definitions are steadily

institutionalized.

h. Establish a rapid testing process that can weed out data inaccuracies and ensure quality.

i. Establish a training program to ensure technical personnel are continuously abreast with the

technology used.

j. Remove/Consolidate reports that are underutilized.

2) Setting the Business Foundation

a. Establish a key product champion in finance that can steer and direct this engagement and

ensure compliance by other units.

b. Manage expectations of the key pro ject stakeholders that clear leadership is required.

c. Form the business team that will drive the change throughout the financial reporting structure.

This will be the core change management and training team.

d. Prioritize value statements, quantify those statements and ensure corporate sponsorship that

these values can be translated when the information is available. Also explain how.

e. Ramp up the breadth of financial management skills required to manage the transition as an

financial information owner.

PROJECT TEAM STRUCTURE

To reiterate the message of the framework, the structure is fragmented into ma jor business units and considering

the crux of banking lies with finance, the first information owner should be the CFOs office and a bank is too

highly regulated, and too visible to not have a performing financial reporting and analytics team.

We also assume that this structure will form the basis for all financial reporting and dashboards to the respective

heads of business unit and eventually the CFO. Its simply unacceptable to allow the head of Retail Banking to

receive a report thats totally diff erent from the CFOs numbers.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 23/29

Page 23

Note: PMO and procurement roles are hidden to not clutter the discussion.

Business Roles

Role Name Responsibilities

CFO (Program Sponsor) To provide steering, direction and decision tie breaking/resolution

Head of Retail Banking To provide steering, direction and ensure that Retail Banking financial reporting

interests are ref lected accurately.

Head of Wholesale

Banking

To provide steering, direction and ensure that Wholesale Banking financial reporting

interests are ref lected accurately.

Wholesale Banking

Financial Lead + Change

To ensure that requirements of Wholesale Banking financial reporting are captured

and provided to the IT/Business Analysis.

To provide f eedback, participate and coordinate the necessary change management

activities within Wholesale Banking come deployment of the new reporting

standards.

Retail Banking Financial

Lead + Change

To ensure that requirements of Retail Banking financial reporting are captured and

provided to the IT/Business Analysis.

To clearly articulate and envision business value and key decisions that will be made

from each information set.

To provide f eedback, participate and coordinate the necessary change management

activities within Retail Banking come deployment of the new reporting standards.

Financial Business

Architect (SME)

The primary business domain expertise on financial reporting, ensuring compliance to

regulatory reporting, ensuring standards in reporting, and requirements are gathered

accurately and ref lective of the needs of the business. To provide financial reporting

methodologies and best practices. To design a reporting structure that is easily

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 24/29

Page 24

understood and f lexible and to ensure that the terminologies are institutionalized

throughout the enterprise.

Requirements Lead To capture and document business requirements as well as necessary screen shot to

ensure accuracy and context of the requirements are not lost. The document shall be

clearly understood by the business. Able to handle workshops and manage conf licts

of interests during those sessions, able to keep the sessions moving. Business Pro ject Manager To ensure the coordination and alignment of the respective business units. To ensure

that the pro ject charter, scope, plan and deliverables are endorsed as well as adhered

to by the business participants. To collectively manage pro ject issues, risk and scope

change management with the IT pro ject manager. To provide pro ject

communications to relevant steering & stakeholders. To lead procurement activities.

To lead procurement activities and negotiations. To perform vendor management

during implementation.

Technical Roles

Role Name Responsibilities

IT Pro ject Manager To ensure the coordination and alignment of the respective business units. To ensurethat the pro ject charter, scope, plan and deliverables are endorsed as well as adhered

to by the technical participants. To collectively manage pro ject issues, risk and scope

change management with the Business pro ject manager. To provide pro ject

communications to relevant steering & stakeholders. To lead procurement activities

and negotiations. To perform vendor management during implementation.

IT Business Analyst To work with the Finance Business Architect (SME) in translating business

requirements into specifications that can be worked on by the DW & BI leads. To

work together with Finance Business Architect (SME) in clearly defining business

requirements.

Testing/Release Lead To ensure that the solution provided are tested for accuracy, stability, consistency,

availability & performance and to manage the bug tracking and closure exercise

during UAT and pre-live tests. To also perform release management of fixes post live

until handover is over.

IT Change

Management/Deployment

To ensure successf ul training of both the business users in acclimatizing to the new

reporting standards.

Solution Lead To ensure that the overall platform design and standards comply with the roadmap

and direction of Enterprise Architecture, and to cohesively glue the implementation

of the pro ject; covering aspects of ETL/DW/ BI Reports and the Infrastructure.

To work with ETL/DW/BI/Technical lead to define a logical roadmap of subsequent

evolution.

ETL&DW Lead (Note that

for complex tasks, this

role could be split into

two)

To design the reporting screens and prepare specifications of how the ETL processes

will be presented.

To design the data models required for the Datawarehouse.

To be an SME on the ETL and Datawarehouse tool.

BI/Reporting Lead To design the reporting screens and prepare specifications of how the BI report will

be presented.

To design the reports based on the technical constraints of the BI Tools.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 25/29

Page 25

To be an SME on the BI reporting tools capabilities

Technical Infrastructure

Lead

To lead and manage technical vendors engaged in preparing the necessary

infrastructure (servers, software, networks and security) required for the new system

to run.

SI Applications Vendor To perform configurations based on the specifications provided by the BI/Reporting

Lead and ETL/DW Lead SI Technical Vendor To perform the delivery, installation, configuration and testing preparation on the

infrastructure components specified by the technical leads.

WHAT HAPPENS TO THE ACTORS

1) IT will be part of the technical team in white.

2) Enterprise Information Management unit should technically be able to f unction as the Financial Business

Architect, provided that they have the relevant skill set and still tightly engaged as an operating area of

finance, e.g. Management Account, AR/PR, Treasury etc. If that skill set is lost, then they would be best

merged into the IT team as Business Analysts.

3) The MIS team can be absorbed into the technical and/or business implementation team as Testers,

Business Analysts and Change Management due to their exposure to the technology product.

4) The existing Data Governance unit will be merged into IT as experts in data quality and institutionalization

of data dictionaries for IT. They will be the SME to spread the gospel of data governance and records

management principles to the business as well. The team will lead respective Information Owner

Governance personnel to ensure cross pollination and institutionalization of governance principles.

TRANS ITION ING THE BUSINESS STRUCTURE POST LIVE

Once the pro ject has completed, the Financial Business Architect will need to be maintained for a short period of

time and f unction as the Information Owner. The person however, will plan to handover his reign to a specific

head of business in Finance during the end of their tenure. Ideally to ensure that the financial reporting standards

are continuously improved upon and tuned to capture the key decision needs of the other financial units. For

example, Treasury in Finance is f undamentally diff erent from the team managing Procurement or Accounting.

As the Head of unit also has a day job, there will be a need to create a more permanent Financial Information

Governance Team. This team will build upon the standards already defined during the implementation and ensure

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 26/29

Page 26

that the dictionary of terms used, traceability of information sources and conf lict resolution and troubleshooting of

discrepancies are done together with the IT people. They are also the requirements personnel to specify new

business specifications to IT.

Financial Info Release Management should assist the Financial Owner in planning out new sub pro jects and

improvement with the IT team; they will coordinate with the rest of finance in deploying these new f eatures and

work with IT in coordinate releases and managing the release process. For example, roll out, training. These two

boxes will f undamentally collapse the roles and responsibilities mentioned in Roles and Responsibilities on an

Information Owner. For example the Financial information Product Management role is a combination of both

these boxes.

HOW IS IT DEPARTMENT S STRUCTURE?

Fundamentally unchanged, but the operating paradigm needs to. Instead of being a cost centre it will be a profit

centre, with reasonable margins that is sufficient to be reinvested back to the overall IT system improvements. To

avoid conf licts of interest, the IT personnels KPI CANNOT be judged from margins made but through the overall

accuracy, performance and stability of the system. This will avoid overzealous IT managers from pegging margins

generated to their bonuses.

The service provider model will also reduce the need to depend on business for upgrades and improvements and

all f unding decisions will be a CFO decision. It also decouples the inf luence of business in determining for IT the

technology they would pref er to use.

The bank will transf er all asset ownership to IT, whereupon a cost plus allocation model will charge back the cost of

maintaining existing systems including a margin that is sufficient enough to snowball into f unds that can be

invested back into system improvements.

The calculation of the said margin and cost allocation model is beyond the scope of this model and needs to be

revisited separately. However, it is crucial for this to happen to break the cycle of me vs. Your system that is

prevalent amongst multi subsidiary and large corporations.

The key question here is whether the IT organization has the maturity and exposure to be managed as a profit

centre.

SUMMARY AND CONCLUSION

We began the journey with 3 problem statements, having multiple organizations managing overlapping set of data

but owning various systems; the static nature of organizational departments, particularly information

management; and the organizations lacks an information soul, the non-existence abstraction and productization of

information to be consumed by various areas of banking; resulting in leadership gaps and users who are unable to

drive requirements and improvements.

So we laid out the solution that began with leadership, the embracing business f unctions as the ultimate owners of

information and not the system. An idea that is largely inf luenced by Enterprise Architecture principles of starting

with the strategic intents, business aspirations and needs before we can even provide IT solutions to meet these

goals.

To end, we reemphasize that the info-owner role is not an ivory tower position and perpetual, the information

owner needs to be rotated through the particular business line that owns the subject area. Lastly, theres a need to

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 27/29

Page 27

decouple business from IT and for IT to f unction as an information solution provider to business. Let IT chart its

own destiny, and in order to do that, a mechanism that drives improvements through a self sustaining charge back

cost plus model is required.

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 28/29

8/8/2019 A021 - Information Champions - A People - Services and Productization Approach

http://slidepdf.com/reader/full/a021-information-champions-a-people-services-and-productization-approach 29/29

AP PENDIX - SOURCES

Bruland, Tine. Industrial conf lict as a source of technical innovation: three cases. Economy and Society 112 (May

1982): pp. 91-121.

Carley, Kathleen M., and John R. Harrald. Organizational Learning under Fire: Theory and Practice. American

Behavioral Scientist 40, no. 3 (1997): pp. 310-332.

Dutton, Jane, E. The Processing of Crisis and None Crisis Strategic Issue. Journal of Management Studies 23, no. 5

(1986): pp. 501-517.