A View of Colombian and Regional DCMs · Peru BBB+ Stable Colombia BBB Negative Panama BBB Stable...

27

Alejandro Bertuol Managing Director, Latin America ASOBANCARIA Medellín, August 2019 A View of Colombian and Regional DCMs

Transcript of A View of Colombian and Regional DCMs · Peru BBB+ Stable Colombia BBB Negative Panama BBB Stable...

Alejandro Bertuol

Managing Director, Latin America

ASOBANCARIA

Medellín, August 2019

A View of Colombian and Regional DCMs

1

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

2011 2012 2013 2014 2015 2016 2017 2018 2019F 2020F

(Mark

et exchange r

ate

weig

hts

, %

)

Source: Fitch Ratings

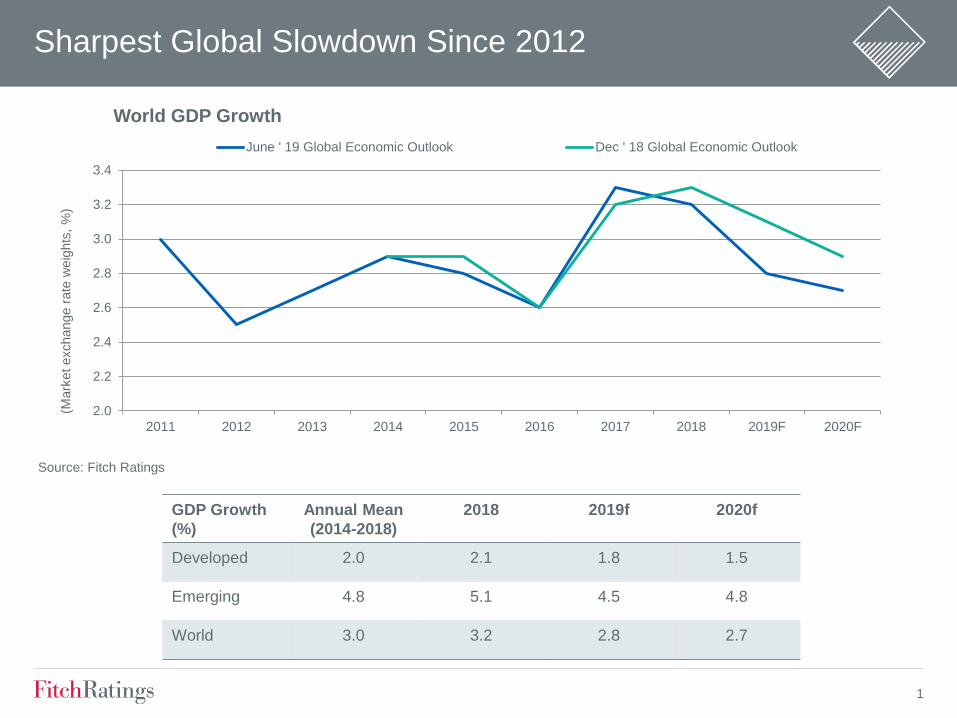

World GDP Growth

June ' 19 Global Economic Outlook Dec ' 18 Global Economic Outlook

Sharpest Global Slowdown Since 2012

GDP Growth

(%)

Annual Mean

(2014-2018)

2018 2019f 2020f

Developed 2.0 2.1 1.8 1.5

Emerging 4.8 5.1 4.5 4.8

World 3.0 3.2 2.8 2.7

2

World Growth in 2020 Revised Down in Fitch’s June GEO

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

Bra

zil

South

Afr

ica

Me

xic

o

South

Kore

a

Austr

alia

Ca

nad

a

Ru

ssia

India

(F

Y)

Germ

any

EM

Fra

nce

Indon

esia

Ita

ly

Tu

rkey

World

Japa

n

Un

ite

d S

tate

s

DM

Ch

ina

Spain

Sw

itzerl

and

Un

ite

d K

ing

dom

Euro

zone

Pola

nd

(Revis

ions s

ince M

ar

'19 G

EO

, p.p

.)

2019 2020

Source: Fitch Ratings

Revisions to Fitch GDP Growth Forecasts

3

LatAm Growth Underperforming EMs, World and US

-2

-1

0

1

2

3

4

5

6

7

8

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

(% GDP)

Largest Economies Dragging Down Regional Growth

Emerging Markets LatAm excl. Ven

Latam ex big 3, ex Ven Big 3

Source: Fitch Ratings

-2

-1

0

1

2

3

4

5

6

7

8

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

(% GDP)

Region Growing Below World and US since 2013

USA LatAm excl. Ven World

4

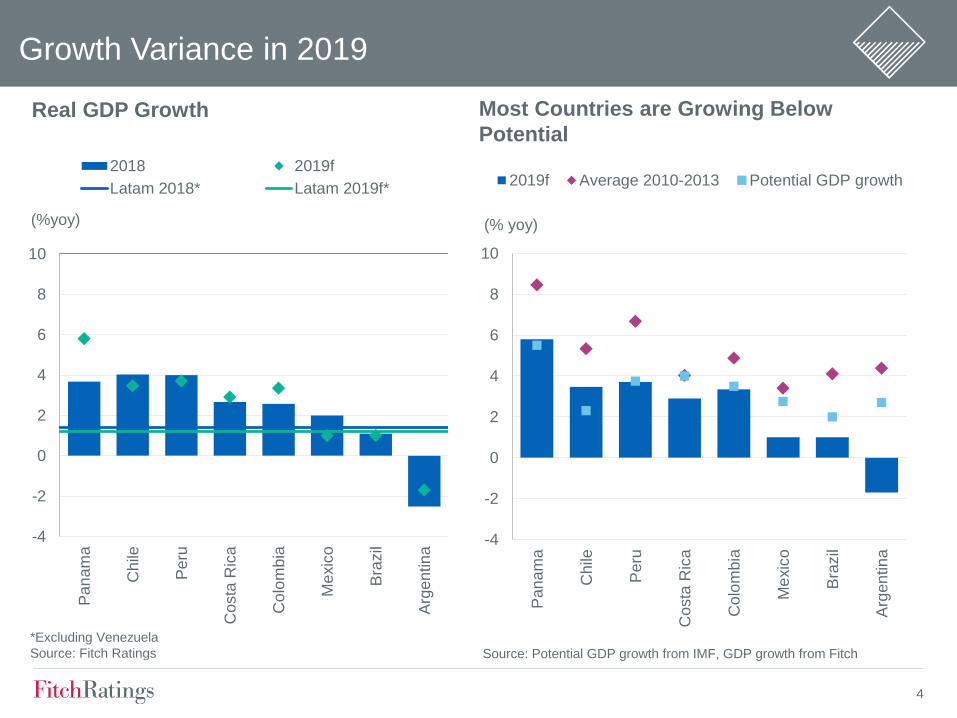

Growth Variance in 2019

-4

-2

0

2

4

6

8

10

Pan

am

a

Chile

Peru

Costa

Ric

a

Colo

mb

ia

Me

xic

o

Bra

zil

Arg

en

tin

a

(%yoy)

Real GDP Growth

2018 2019f

Latam 2018* Latam 2019f*

*Excluding Venezuela

Source: Fitch Ratings

-4

-2

0

2

4

6

8

10

Pan

am

a

Ch

ile

Peru

Costa

Ric

a

Co

lom

bia

Me

xic

o

Bra

zil

Arg

en

tin

a

(% yoy)

2019f Average 2010-2013 Potential GDP growth

Source: Potential GDP growth from IMF, GDP growth from Fitch

Most Countries are Growing Below

Potential

5

Lagging Consolidation Amid Rising Debt Burden

-12

-10

-8

-6

-4

-2

0

2

4

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9f

202

0f

(%GDP)

Argentina Brazil ColombiaChile Mexico Peru

Source: Fitch Ratings

Gradual Reduction in Fiscal Deficits General Government Balance

0

10

20

30

40

50

60

70

80

90

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9f

202

0f

(%GDP)

Argentina Brazil Chile

Colombia Mexico Peru

Source: Fitch Ratings

... And Debt Keeps Growing in Many

6

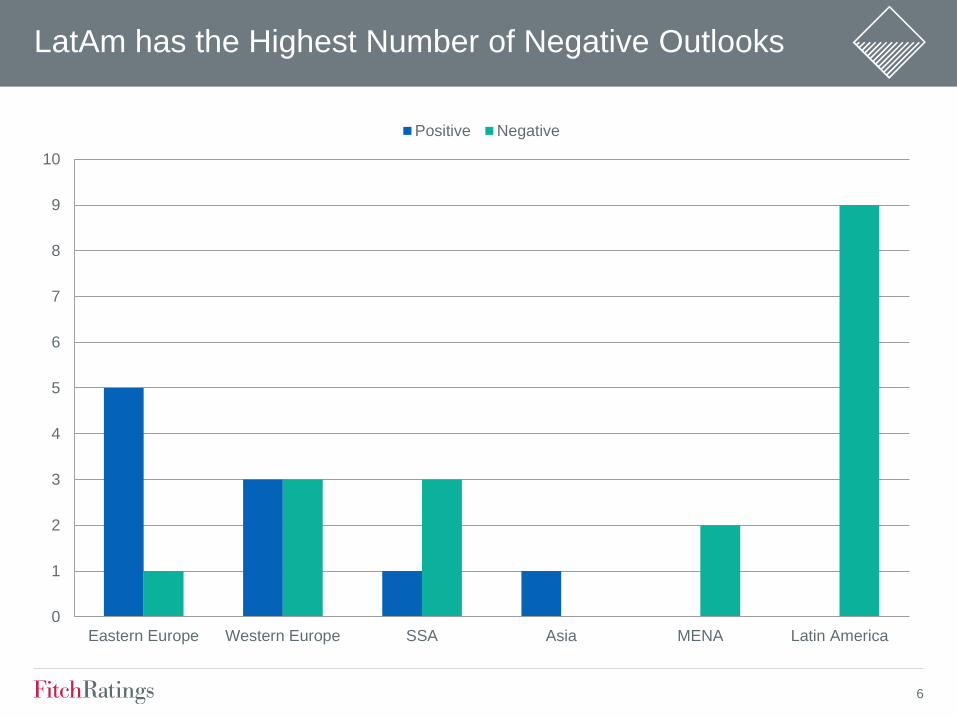

LatAm has the Highest Number of Negative Outlooks

0

1

2

3

4

5

6

7

8

9

10

Eastern Europe Western Europe SSA Asia MENA Latin America

Positive Negative

7

Ratings and Recent Actions

Sovereign LTFC Outlook

Chile A Stable

Mexico BBB Stable

Peru BBB+ Stable

Colombia BBB Negative

Panama BBB Stable

Aruba BBB- Negative

Uruguay BBB- Negative

Paraguay BB+ Stable

Guatemala BB Negative

Bolivia BB- Negative

Brazil BB- Stable

Dom. Republic BB- Stable

Costa Rica B+ Negative

Jamaica B+ Stable

Argentina CCC --

Nicaragua B- Negative

Ecuador B- Negative

El Salvador B- Stable

Suriname B- Stable

Negative Rating Pressures

8 of the 19 sovereigns on Negative Outlook

Lukewarm and uneven growth, persistent fiscal

challenges, political risks, and difficult market

access for some

Negative Actions in 2018-19

Mexico downgraded to BBB from BBB+ (2019)

Ecuador Outlook to Negative from Stable (2019)

Costa Rica to ‘B+’ from ‘BB, ’ Neg. Outlook (2019)

Bolivia Outlook to Negative from Stable (2019)

Colombia Outlook to Negative from Stable (2019)

Guatemala Outlook to Negative from Stable (2019)

Nicaragua to ‘B-’ from ‘B’, Negative Outlook (2018)

Argentina Outlook to Negative from Stable (2018)

Brazil to ‘BB-’ from ‘BB’, Stable Outlook (2018)

Positive Actions in 2018-19

Jamaica to ‘B+’ from ‘B’, Stable Outlook (2019)

Paraguay to ‘BB+’ from ‘BB’, Stable Outlook (2018)

Suriname Outlook to Stable from Negative (2018)

8

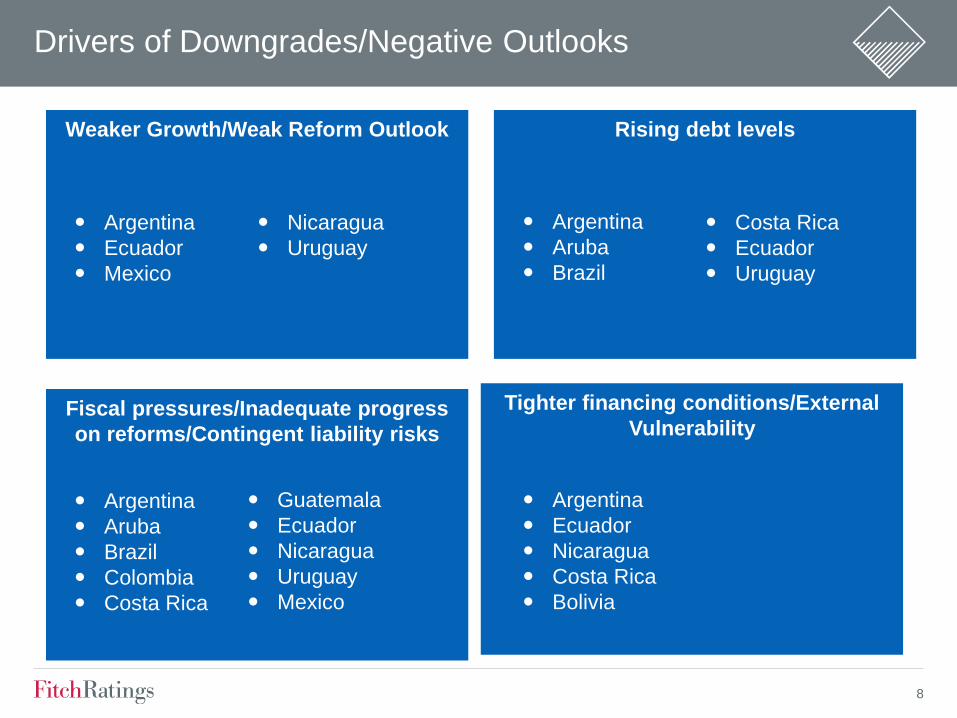

Drivers of Downgrades/Negative Outlooks

Weaker Growth/Weak Reform Outlook Rising debt levels

Fiscal pressures/Inadequate progress

on reforms/Contingent liability risks

Tighter financing conditions/External

Vulnerability

Argentina

Aruba

Brazil

Colombia

Costa Rica

Argentina

Ecuador

Nicaragua

Costa Rica

Bolivia

Argentina

Ecuador

Mexico

Argentina

Aruba

Brazil

Costa Rica

Ecuador

Uruguay

Guatemala

Ecuador

Nicaragua

Uruguay

Mexico

Nicaragua

Uruguay

9

Political Risks Vary Across Countries

Political violence / Deep Political

Divisions

Managing Macro & Fiscal Policy

Adjustment

Governability Risk / Political

Polarization or Congressional

Fragmentation

Uncertainty from new administrations

Brazil

Costa Rica

El Salvador

Brazil

Mexico

Nicaragua

Venezuela

Argentina

Brazil

Colombia

Costa Rica

Ecuador

Uruguay

Guatemala

Peru

10

Colombia Rating Overview

Outlook revised to negative in May 2019,

affirmed at ‘BBB’, to reflect risks to fiscal

consolidation and the trajectory of

government debt, the weakening of fiscal

policy credibility, and increasing risk from

external balances.

Increased difficulty in meeting fiscal

targets from 2020 onwards as a result of

cuts in corporate tax rates passed in the

2018 Financing Law.

Current account deficit widened to 3.8%

of GDP in 2018 and forecast to widen

further to 4.2% of GDP in 2019.

Fitch forecasts growth acceleration in

2019 to 3.3% driven by supportive

consumption and higher investment.

Key Indicators 2018 2019f 2020f

Real GDP growth (%) 2.6 3.3 3.5

Inflation (%) 3.2 3.2 3.1

Central government balance (% of GDP) (3.1) (2.7) (2.3)

General government debt (% of GDP)* 42.3 43.6 43.7

Current account balance (% of GDP) (3.8) (4.2) (4.0)

International reserves, incl. gold (USDbn) 47.9 52.6 57.6

Net external debt (% of CXR) 51.1 51.6 51.7 Source: Fitch Ratings

*General government includes central government, provincial, regional and local

governments, social security funds and extra-budgetary funds.

1995 1998 2001 2004 2007 2010 2013 2016 2019

Rating History

Source: Fitch Ratings

Source: Fitch Ratings

BB+

BB

BBB+

BBB

BBB-

BB-

11

Colombia (BBB/Negative)

SRM output Qualitative overlay FC IDR

BBB-

Factor Notch adjustment

BBB

Macro

Long track record of prudent and consistent

macroeconomic policies.

+1

Public finances 0

External finances 0

Structural features 0

Total +1

Negative Sensitivities

× Failure to implement credible structural

measures to put government debt on a stable

or downward trajectory.

× Sustained deterioration in external imbalances

that leads to a continued rise in the external

debt burden and weak external liquidity

indicators.

× Growth underperformance relative to the ‘BBB’

median that detracts from per-capita income

convergence with similarly rated sovereigns.

Positive Sensitivities

Fiscal consolidation through credible and

predictable policies consistent with an improved

trajectory for public debt dynamics.

Reduced external imbalances that improve

external debt and liquidity ratios.

Higher growth that reduces income gap with

higher-rated sovereigns.

12

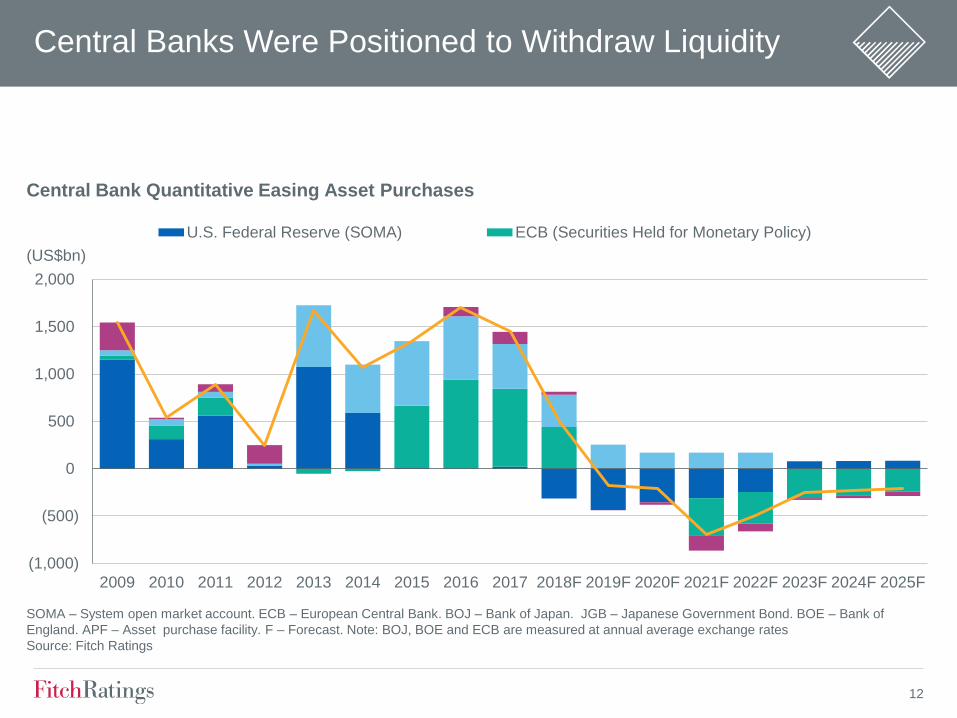

Central Banks Were Positioned to Withdraw Liquidity

(1,000)

(500)

0

500

1,000

1,500

2,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F 2022F 2023F 2024F 2025F

U.S. Federal Reserve (SOMA) ECB (Securities Held for Monetary Policy)

SOMA – System open market account. ECB – European Central Bank. BOJ – Bank of Japan. JGB – Japanese Government Bond. BOE – Bank of

England. APF – Asset purchase facility. F – Forecast. Note: BOJ, BOE and ECB are measured at annual average exchange rates

Source: Fitch Ratings

Central Bank Quantitative Easing Asset Purchases

(US$bn)

13

40

42

44

46

48

50

52

54

56

-5

0

5

10

15

20

2011 2012 2013 2014 2015 2016 2017 2018 2019

Balance>50 = easing (% Y/Y)

Source: Fitch Ratings, IIF, BIS, Haver Analytics

EM Bank Lending Standards and Dollar Lending

USD Credit to Emerging Markets

EM Bank Lending Conditions Survey (RHS)

Tightening in EM Credit Conditions

14

Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

-20

-15

-10

-5

0

5

10

15

20

25

30

35

Source: Fitch Ratings, IIF

USD bn

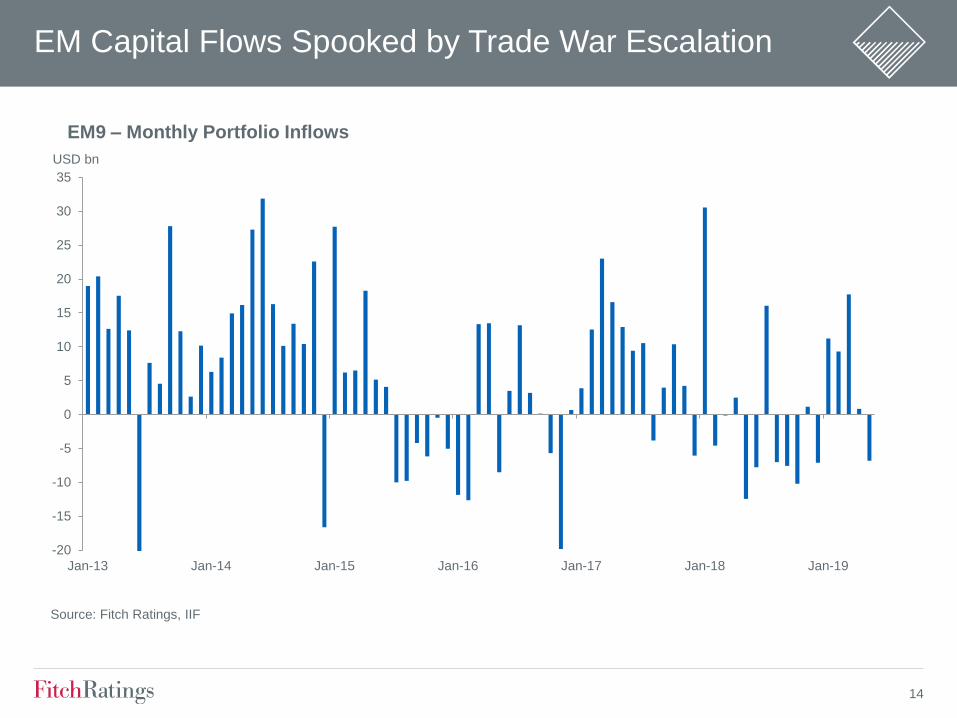

EM9 – Monthly Portfolio Inflows

EM Capital Flows Spooked by Trade War Escalation

15

-500

0

500

1000

1500

2000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 F 2020 F

(USD bn)

Source: Fitch Ratings, ECB, Fed, BOJ, BOE, Haver Analytics

Central Bank QE Purchases in USD Equivalent Terms

BOJ (JGB's) ECB (Sec. Held for Monetary Policy) Fed (SOMA) BOE (APF & TFS) USD Total

Back to Global Quantitative Easing in 2020

16

0

50

100

150

World Arg Bra Chile Col Peru Mex

2012

2018

Regional DCMs

Market Cap of Listed Domestic Companies (%GDP) Stocks Traded, Turnover Ratio Domestic Shares (%)

0

50

100

150

World Arg Bra Chile Col Peru Mex

0

50

100

150

World Arg Bra Chile Col Peru Mex

Stocks Traded, Total Value (% GDP)

0

100

200

300

400

Arg Bra Chile Col Peru Mex

Listed Domestic Companies, Total

Source: World Federation of Exchanges; The World Bank

17

Colombian DCM Indicators

Fixed Domestic Income Issuance (COP, BN) Domestic Corp Fixed Income Issuance (COP, MM)

Bid-to-Cover, Domestic Corporate Issuance Corp Spreads Over CPI (2018)

Source: BVC, Fitch Ratings, Fitch Solutions; as of July 30, 2019

0

5

10

15

2013 2014 2015 2016 2017 2018 2019

Non-FI

FI

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2013 2014 2015 2016 2017 2018 2019

AA(col) AAA(col)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2013 2014 2015 2016 2017 2018 2019

(X)

AA(col) AAA(col)

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0 5 10 15 20 25 30

Term (years)

AAA(col) AA(col)

18

Colombia - Manageable Maturity Horizon (Corp)

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

10,0

11,0

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 Thereafter

(COP Tril.)

Source: Superintendencia Financiera.

Vencimientos Bonos Locales — Portafolio Fitch

0

500

1.000

1.500

2.000

2.500

3.000

3.500

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028Thereafter

(USD Mil.)

Source: Fitch Ratings, Fitch Solutions.

Vencimientos Cross-Border Maturities — Portfolio Fitch

Estable 81%

Negativo15%

Positivo4%

Source: Fitch Ratings, Fitch Solutions.

Perspectiva de Calificaciones Nacionales(Mayo, 2019)

19

• Regional growth prospects, external environment

and pressured sovereign profiles suggest volatility

• National scale issuance rating concentration

• Broaden access to local, regional and global

DCMs

• TIG

• Transition to risk based supervision and

management

• Innovation and disruption

DCM Challenges & Opportunities

20

0

10

20

30

40

50

60

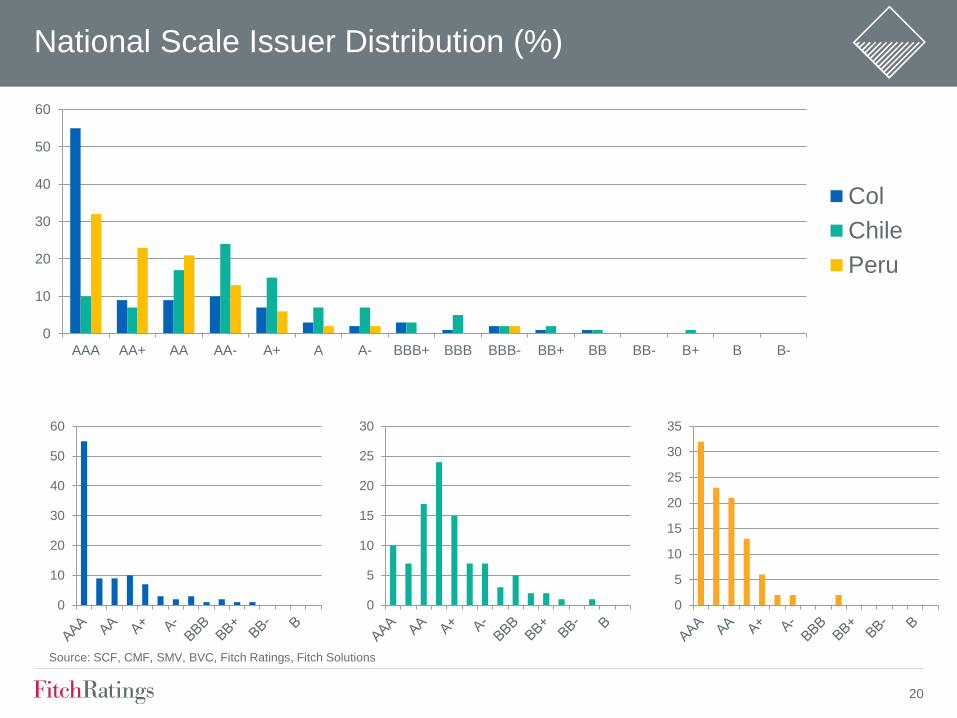

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ BB BB- B+ B B-

Col

Chile

Peru

National Scale Issuer Distribution (%)

0

5

10

15

20

25

30

0

5

10

15

20

25

30

35

0

10

20

30

40

50

60

Source: SCF, CMF, SMV, BVC, Fitch Ratings, Fitch Solutions

21

• Regional growth prospects, external environment

and pressured sovereign profiles suggest volatility

• National scale issuance rating concentration

• Broaden access to local, regional and global

DCMs

• TIG

• Transition to risk based supervision and

management

• Innovation and disruption

DCM Challenges & Opportunities

22

MISIÓN DEL MERCADO DE CAPITALES 2019

Arreglo Institucional

Regulación e Incentivos

Productos

Ámbito Internacional

Estructura del Mercado

Manejo de Activos Públicos

Promoción y Educación

Ámbito Tributario

Source: Minhacienda

23

Financial Integration: Pacific Alliance

Portfolio Investments (Dom vs PA, US$ MM, 2016) Does your organization see potential to increase its

investments or business volumes in the AP? (%)

Principal Factor Inhibiting FI in the PA (%) Non-national Investor Tax in PA Countries via MILA

Source: Centro UC CLAPES ; OEAP, December 2018

Origin

Colombia Chile Mexico Peru

Colombia 45,850 1,347 142 1,504

Chile 163 106,433 41 1,516

Mexico 267 3,987 139,288 718

Peru 325 1,437 10 25,530

0 20 40 60 80

No opinion

No

Yes

0 10 20 30 40 50

Tax

Foreign Exchange

Regulatory

Inversionista no

nacional que

invierte en:

Dividendos Ganacia de Capital

Colombia Cuatro regimenes

tibutarios

Tres regimenes

tributarios

Chile Dos regimenes

tributarios

Dos regimenes

tributarios

Mexico Régimen único Tres regimenes

tributarios

Perú Régimen único

(con variaciones en el

tiempo)

Dos regimenes

tributarios

24

• Regional growth prospects, external environment

and pressured sovereign profiles suggest volatility

• National scale issuance rating concentration

• Broaden access to local, regional and global

DCMs

• TIG

• Transition to risk based supervision and

management

• Innovation and disruption

DCM Challenges & Opportunities

25

Fitch Ratings’ credit ratings rely on factual information received from issuers and other sources.

Fitch Ratings cannot ensure that all such information will be accurate and complete. Further, ratings are inherently forward-

looking, embody assumptions and predictions that by their nature cannot be verified as facts, and can be affected by future

events or conditions that were not anticipated at the time a rating was issued or affirmed.

The information in this presentation is provided “as is” without any representation or warranty. A Fitch Ratings credit rating is

an opinion as to the creditworthiness of a security and does not address the risk of loss due to risks other than credit risk,

unless such risk is specifically mentioned. A Fitch Ratings report is not a substitute for information provided to investors by the

issuer and its agents in connection with a sale of securities.

Ratings may be changed or withdrawn at any time for any reason in the sole discretion of Fitch Ratings. The agency does not

provide investment advice of any sort. Ratings are not a recommendation to buy, sell, or hold any security.

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE

LIMITATIONS AND DISCLAIMERS AND THE TERMS OF USE OF SUCH RATINGS AT WWW.FITCHRATINGS.COM.

@fitchratings

fitchratings.com

New York London 33 Whitehall Street

New York, NY 10004

30 North Colonnade

Canary Wharf

London, E14 5GN

![QBE at a glance UK · QBE Insurance Group Limited A– [negative] A– [negative] bbb [negative] QBE Insurance (Europe) Limited A– [negative] a [negative] QBE Re (Europe) Limited](https://static.fdocuments.in/doc/165x107/5fa8e28b58047158406a3b4f/qbe-at-a-glance-uk-qbe-insurance-group-limited-aa-negative-aa-negative-bbb.jpg)