A strong hold on your investments - HSBC€¦ · debt funds in a portfolio allows the investor to...

13

HSBC Mutual Fund presents HSBC MIP * HSBC Income Fund HSBC Gilt Fund HSBC Floating Rate Fund HSBC Cash Fund HSBC Liquid Plus Fund HSBC Fixed Term Series A strong hold on your investments HSBC Investments

Transcript of A strong hold on your investments - HSBC€¦ · debt funds in a portfolio allows the investor to...

HSBC Mutual Fundpresents

HSBC MIP*

HSBC Income Fund HSBC Gilt Fund

HSBC Floating Rate FundHSBC Cash Fund

HSBC Liquid Plus FundHSBC Fixed Term Series

A strong hold on yourinvestments

HSBC Investments

2

Risk/Return Tradeoff

Low Risk

Low Return

Debt Funds

Equity Funds

High Risk

High Return

Standard Deviation (or Risk)

Retu

rn

Why Debt Funds?

The world of investing can be a cold, chaotic, and confusing place. Markets can play havoc with your investments from time to time. It is therefore very critical to be disciplined with your investments so that the downside risk is controlled. This means adopting fundamental financial concepts diligently and consistently while making your investments.

Some of the most important of these are the concepts of Risk/ Return Tradeoff, Portfolio Diversification & Asset Allocation, and Tax Planning. These concepts explain the need to diversify investments across various asset classes to minimise risk and improve tax efficiency thereby highlighting the need for investments in Debt Funds.

There are several reasons why one should look at debt as an asset class to invest in. Some of the main reasons are:

Need to balance risk and return - The Risk/Return TradeoffNeed to diversify - Portfolio Diversification & Asset AllocationNeed for Tax Planning

The Risk/Return Tradeoff

Deciding what amount of risk you can take while remaining comfortable with your investments is very important. Low risks are generally associated with low potential returns. High risks are generally associated with high potential returns. The risk/return tradeoff is an effort to achieve a balance between the desire for the lowest possible risk and the highest possible return. This is demonstrated graphically in the chart below. A higher standard deviation means a higher risk and therefore a higher potential return.

Debt Funds from

HSBC Mutual Fund

3

Debt Funds typically lie towards the lower end of the risk/return chart. Debt as an asset class/investment category tends to provide lower returns at lower risk compared to equity as a category, which tends to provide higher returns at higher risk levels. Debt mutual funds, which invest in debt markets, therefore, in turn, tend to offer lower returns at relatively lower risk levels.

In case of Debt Funds the risks are two fold:Counter Party/Credit RiskInterest Rate Risk

The counter party/credit risk can be mitigated by investing in rated securities. At HSBC Investments, restrictions have been set to mitigate counter party risk. The Fund/Scheme shall not invest more than 10% of its NAV in unrated debt instruments issued by a single issuer and the total investment in such instruments shall not exceed 25% of the NAV of the Scheme. All such investments are made with the prior approval of the Board of Trustees and the Board of the AMC or a Committee constituted on its behalf.

Interest rate risk, however, is something that has more to do with the kind of fund it is and the tenor of the securities the fund holds. For example, the risks associated with an income fund would be greater than that of a liquid/cash fund since the income fund would typically hold securities of higher tenor/duration than those held by a liquid/cash fund. Duration Strategy (that allows for management of duration/tenor) is an integral part of the Fixed Income Investment process at HSBC Investments which allows us to manage Interest rate risk better.

HSBC Investments offers the following products under its debt fund umbrella:

HSBC MIP (Monthly income is not assured and is subject to distributable surplus)HSBC Income Fund (Investment Plan & Short Term Plan)HSBC Gilt Fund (Short Term Plan)HSBC Floating Rate Fund (Long Term Plan & Short Term Plan)HSBC Cash FundHSBC Liquid Plus FundHSBC Fixed Term Series (of various tenors)

Plotted on a risk (interest rate risk) and return chart, these funds stack up as follows:

HSBC Mutual Fund Schemes

Po

ten

tial

Inte

rest

Rat

e R

isk

Potential Return

Potential Risk involved indicates interest rate risk and is not an indicator of credit risk.HSBC Fixed Term Series is not plotted on the chart since it is available in varied tenors.

HSBC

Cash

Fund

HSBC

Liquid Plus

Fund

HSBC

Floating Rate

Fund – Short

Term Plan

HSBC

Floating Rate

Fund – Long

Term Plan

HSBC

Income

Fund – Short

Term Plan

HSBC Gilt

Fund – Short

Term Plan HSBC Income

Fund –

Investment

Plan

HSBC MIP

4

A brief description and note on the performance of each of these funds is provided in subsequent pages of this brochure.

Diversification & Asset AllocationDiversification is a risk-management technique that mixes a wide variety of investments within a portfolio in order to minimise the impact that any one security will have on the overall performance of the portfolio. Diversification essentially lowers the risk of your portfolio.

There are three main practices that can help you ensure the best diversification:

Spread your portfolio among multiple investment vehicles such as cash, stocks, bonds, mutual funds, and perhaps even some real estate.

Vary the risk in your investments. If you're investing in debt, you could consider both long-term and short-term debt. It would be wise to pick investments with varied risk levels.

Vary your securities by credit worthiness. This will minimise the impact of specific risks of certain counterparties.

Diversification is the most important component in helping you reach your long-term financial goals while minimising your risk. Out of the three points mentioned above, the first point on diversifying investments across equity, debt, real estate etc. is the most critical. This again highlights the need to invest in debt funds to control risk.

Asset allocation is an investment portfolio technique that aims to balance risk and create diversification by dividing assets among major categories such as bonds, stocks, real estate, and cash. Each asset class has different levels of return and risk, so each will behave differently over time. At the same time that one asset is increasing in value, another may be decreasing or not increasing as much.

The underlying principle of asset allocation is that the older a person gets, the lesser the risk he or she should face. After you retire you may have to depend on your savings as your only source of income. It follows that you should invest more conservatively at this time since capital preservation is crucial.

Therefore one must change asset allocation over time to move more towards safer asset classes (bonds, treasuries) as one gets older.

Certain broad asset allocation profiles are shown below. Debt mutual funds (which form a part of fixed income securities) play an important role in creating a suitable asset allocation profile. They enable the investor to control risk in his portfolio and add

stability to returns. Debt funds are essential for effective diversification of one's investments and should therefore form an integral part of the asset allocation strategy of every investor.

5

70 to 75%

Fixed Income

securities

15 to 20%

Equities

5 to 15%Cash and equivalents

Conservative Portfolio

Debt Funds fit in here

5 to 15%Cash and equivalents

50 to 55%

Equities

35 to 40%

Fixed Income

Securities

Moderately Aggressive Portfolio

Debt Funds fit in here

0 to 10%Cash and equivalents

90 to 100%

Equities

Aggressive Portfolio

Debt Funds fit in here

Profile 1: Conservative Portfolio Characteristics

1. Objective is to maintain real portfolio value i.e. protect against inflation2. Generate high current income and yield long-term capital growth through investment

in equities3. Medium term investment horizon (2-3 years)4. Low risk tolerance

Profile 2: Moderate Portfolio Characteristics

1. Primary objective is to look for capital growth through equity investments2. Secondary objective would be to provide stability in portfolio value by investing

35-40% in fixed income securities thereby limiting down-side risk (risk of capital erosion)

3. Investment horizon of 4 years or more4 Medium to high risk tolerance

Profile 3: Aggressive Portfolio Characteristics

1. Objective is to look for capital growth through equity investments2. Investment horizon of 4 years or more3. High risk tolerance

6

Need for Tax Planning

Be it individuals or corporates, debt funds provide a better investment option in terms of tax efficiency vis-à-vis other tax related debt instruments like deposits, bonds etc. This is explained in the table below:

Note: The above tax implications apply to an investor in the category of "individual" for the Finance Act, 2007.* Plus surcharge @ 10% and education cess of 3% (additional)** Plus surcharge @ 10% (where total income exceeds Rs 10 lacs) and education cess of 3% in all cases.

Evidently, Debt Mutual Funds form a better tax saving/planning tool.

To summarise, why should one invest in Debt Funds

Debt Funds offer investors all the benefits associated with Mutual Funds in general. Some of the benefits are transparency in operation, professional management, diversification, liquidity, convenience and low costs.

Debt Funds lie towards the lower end of the risk spectrum. They offer lower risk compared to equity as an asset class.

Debt Funds provide an alternative for diversification of one's portfolio. A healthy mix of debt funds in a portfolio allows the investor to control risk and add stability to returns.

Performance of Debt Funds is more predictable compared to equity as an asset class.

Debt Funds offer tax benefits.

Debt Mutal Fund

PPF

Bonds notified u/s 54 EC

6.5% Savings Bonds

KVP

BANK FD

NSC

Tax-free in the hands of the investor. Mutual Fund

has to pay Dividend Distribution Tax @

12.5%*.

Taxable as per relevant tax slab**

No limit Not Applicable10%** without Cost Inflation Index benefit or 20%** with Cost Inflation

Index benefit

15 yearsTax-free Not Applicable Not Applicable Rs 70,000

3 yearsTaxable as per relevant tax slab**

Taxable as per relevant tax slab**

20%** without Cost Inflation Index benefit

No limit

6 yearsNot Applicable No limitTaxable as per relevant tax slab**

Not Applicable

2.5 years. Pre-mature

withdrawal is subject to certain

conditions

No limitTaxable as per relevant tax slab**

Not Applicable Not Applicable

Variable (increases as interest rate increases)

No limitNot ApplicableNot ApplicableTaxable as per relevant tax slab**

6 years. Pre-mature withdrawal

is allowed only in exceptional

circumstances

Not Applicable No limitNot ApplicableTaxable as per relevant tax slab**

Dividend / InterestShort Term Capital

Gains (holding period < one year)

Long Term Capital Gains (holding period >= one

year)

Maximum amount that can be invested Lock-in period

7

Debt Funds from HSBC Investments

HSBC Investments in India currently offers the following debt funds:

HSBC MIP

An open-ended Fund. Monthly income is not assured and is subject to availability of distributable surplus. HMIP, launched in February 2004, seeks to generate reasonable returns through investments in debt and money market instruments with a small portion of the corpus invested in equities to seek capital appreciation. The Fund offers two Plans: Regular Plan and Savings Plan. The Regular Plan can have up to 15 per cent of the corpus invested in equities while the Savings Plan can have up to 25 per cent invested in equities.

Performance* of HSBC MIP - Regular Plan1

Performance* of HSBC MIP - Savings Plan1

1Past performance may or may not be sustained in the future.

HSBC MIP - Regular Plan Crisil MIP Blended Index

1 Year 2 Years Since Inception

2

4

6

8

12

14

HSBC MIP - Regular Plan

1010.12

9.66

13.1811.66

3 Years

9.31 9.498.24

7.59

0

HSBC MIP - Savings Plan Crisil MIP Blended Index

2 Years Since Inception

HSBC MIP - Savings Plan

13.44

9.6611.05

7.59

1 Year

17.52

11.66

3 Years

12.52

9.49

0

2

4

6

8

10

12

14

16

18

8

HSBC Income Fund - Investment Plan

It seeks to generate reasonable income whilst maintaining a prudent policy of capital conservation. It invests in bonds, debentures, short-term instruments like commercial papers, repos etc. The

ideal investment period for this fund would be around 1 year and above.

Performance* of HSBC Income Fund - Investment Plan - Regular2

HSBC Income Fund - Short Term Plan

It seeks to generate reasonable income whilst maintaining a prudent policy of capital conservation. It invests in bonds, debentures, short-term instruments like commercial papers, repos etc. The ideal

investment period for this fund would be around 3 - 6 months.

Performance* of HSBC Income Fund - Short Term Plan - Regular2

2Past performance may or may not be sustained in the future.

HSBC Income Fund -

Investment Plan - Regular

HIF - Investment Plan - Regular Crisil Composite Bond Fund Index

1 Year 2 Years 3 Years Since Inception

1

2

3

4

5

6

8

77.43

5.355.12

5.56

6.45

4.63

4.56

4.68

0

HSBC Income Fund -

Short Term Plan - Regular

HIF - Short Term Plan - Regular Crisil Short Term Bond Fund Index

1

2

3

4

5

6

7

Since Inception1 Year 2 Years 3 Years

6.826.03

5.67 5.60

7.38

5.985.50

5.11

0

9

HSBC Gilt Fund - Short Term Plan

HGF seeks to generate reasonable returns through investments in Government Securities (G-Secs) of various maturities.

Performance* of HSBC Gilt Fund - Short Term Plan3

3Past performance may or may not be sustained in the future.

HSBC Floating Rate Fund - Short Term Plan

HFRF, launched in November 2004, is an open-ended scheme that seeks to generate income commensurate with prudent risk from a portfolio comprising of floating rate debt instruments and fixed rate debt instruments swapped for floating rate returns. The scheme may also invest in fixed rate money market and debt instruments. The Fund has two Plans - Long Term and Short Term - and is suitable for investors with different investment horizons. The Short Term Plan is ideally

suited for an investment horizon of 1 - 3 months.

Performance* of HSBC Floating Rate Fund - Short Term Plan - Regular4

HSBC Floating Rate Fund - Long Term Plan

HFRF, is an open ended scheme that seeks to generate income commensurate with prudent risk from a portfolio comprising of floating rate debt instruments and fixed rate debt instruments swapped for floating rate returns. The scheme may also invest in fixed rate money market and debt instruments. The Fund has two Plans - Long Term and Short Term - and is suitable for inves-tors with different investment horizons. The Long Term Plan is ideally suited for an invest-

ment horizon of 6 - 12 months.

HSBC Gilt Fund - Short Term Plan I-Sec -Si-BEX

1 Year 3 Years

1

2

3

4

5

6

7

8

HSBC Gilt Fund - Short Term Plan

2 Years

4.624.10 3.99

7.96

6.84

5.90

Since Inception

3.39

5.61

0

Crisil Liquid Fund Index

1

2

3

4

5

6

7

9

HFRF - Short Term Plan - Regular

HSBC Floating Rate Fund - Short Term Plan - Regular

1 Month 3 Months 6 Months 1 Year 2 Years Since Inception

7.24 7.608.10

7.52

6.566.28

7.71

8.43

7.35

6.39 6.27 5.96

0

10

Performance* of HSBC Floating Rate Fund - Long Term Plan - Regular4

4Past performance may or may not be sustained in the future.

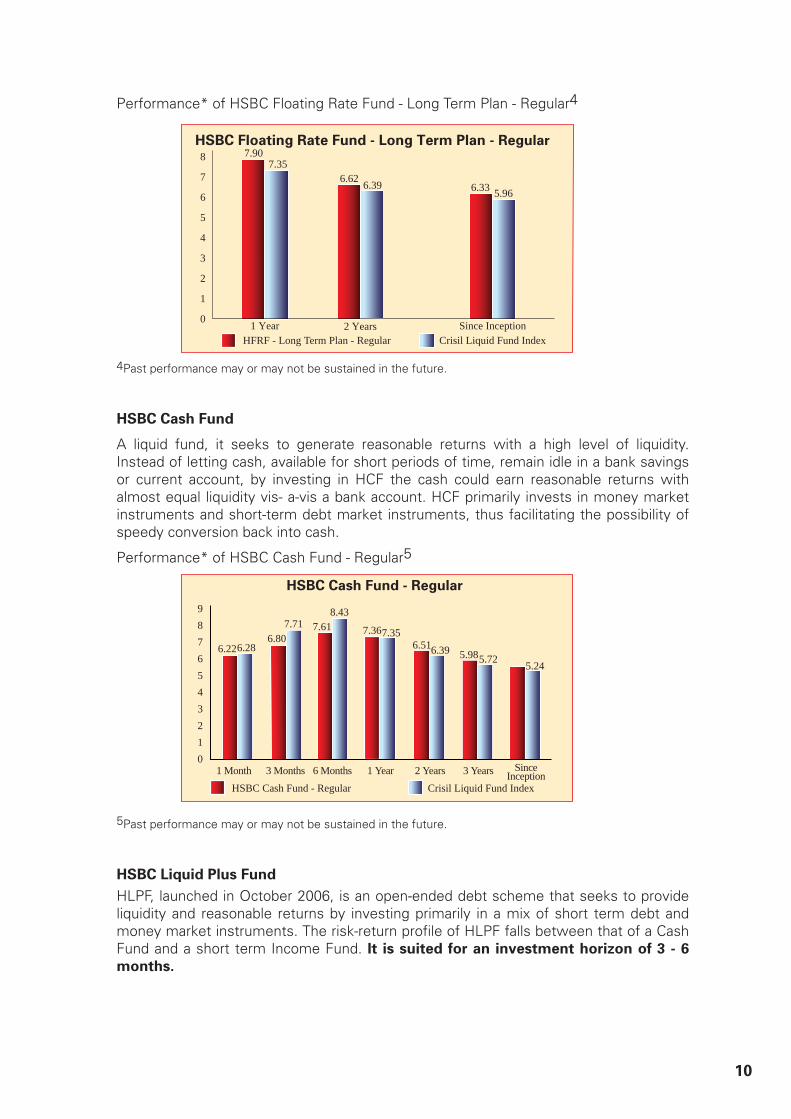

HSBC Cash Fund

A liquid fund, it seeks to generate reasonable returns with a high level of liquidity. Instead of letting cash, available for short periods of time, remain idle in a bank savings or current account, by investing in HCF the cash could earn reasonable returns with almost equal liquidity vis- a-vis a bank account. HCF primarily invests in money market instruments and short-term debt market instruments, thus facilitating the possibility of speedy conversion back into cash.

Performance* of HSBC Cash Fund - Regular5

5Past performance may or may not be sustained in the future.

HSBC Liquid Plus Fund

HLPF, launched in October 2006, is an open-ended debt scheme that seeks to provide liquidity and reasonable returns by investing primarily in a mix of short term debt and money market instruments. The risk-return profile of HLPF falls between that of a Cash Fund and a short term Income Fund. It is suited for an investment horizon of 3 - 6

months.

HFRF - Long Term Plan - Regular Crisil Liquid Fund IndexSince Inception

1

0

2

3

4

5

7

8

6

HSBC Floating Rate Fund - Long Term Plan - Regular

2 Years

6.626.336.39

1 Year

7.907.35

5.96

HSBC Cash Fund - Regular

HSBC Cash Fund - Regular Crisil Liquid Fund Index

1 Month 6 Months3 Months 1 Year 2 Years 3 Years Since Inception

1

0

2

3

4

5

6

8

9

76.22

6.807.61 7.36

6.515.98

6.28

7.718.43

7.35

6.395.72

5.24

11

Performance* of HSBC Liquid Plus Fund - Regular6

6Past performance may or may not be sustained in the future. *Returns less than or equal to 1 year are absolute. Returns greater than 1 year are compounded annualised. HFRF STP and HCF returns are annualised for all period. Returns are as on 31 July 2007 and based on Growth NAVs. Since inception returns are calculated on Rs 10 invested at inception. Inception date of the schemes: HMIP – 24 Feb 2004; HIF – 10 Dec 2002; HGF – 5 Dec 2003; HFRF – 16 Nov 2004; HCF – 10 Dec 2002; HLPF – 17 Oct 2006.

HSBC Fixed Term Series

HFTS is a close-ended scheme offering various plans with fixed maturity tenors that range from 3 months to 36 months. The investment objective of the Scheme is to seek generation of reasonable returns by investing in a portfolio of fixed income instruments normally maturing in line with the time profile (tenor) of the respective plan. HFTS will primarily invest in debt instruments (like bonds issued by, both, the government and corporates) and money market instruments (like treasury bills, certificates of deposit and commercial papers).

Why HSBC Investments?

HSBC Investments is the Investment Manager to HSBC Mutual Fund. Launched in November 2002 HSBC Mutual Fund held client assets of Rs 18,298.79 crores as on 31 July 2007.

HSBC Investments' success in India can be attributed to its following strengths:Reputation and financial strength with a global outlook

Founded in 1865, HSBC is one of the largest banking and financial services organisations in the world with banking and insurance businesses across five continents and over 139 years of experience. HSBC serves 125 million customers from more than 9,500 offices in 76 countries and territories. An established reputation for stability, integrity and sound financial management has made HSBC a household name worthy of trust.

Focused Investment Expertise

Investment professionals in each location are responsible for industry, sector and stock selection decisions. These experts are close to the market, speak the local language and have an intimate understanding of the local business environment, all of which gives HSBC a unique insight and access to investment opportunities to meet your needs.

Risk Controls to Enhance Safety of Investments

We champion global best practices in all aspects of our operations, including managing risk. We control operational and documentation risks, investment risks, reputational risks, credit risks and market risks across the business in an independent and holistic way for all our clients.

Client Service Commitment

We have dedicated call centres to attend to our customers' needs. Our client service com-

HSBC Liquid Plus Fund - Regular

HSBC Liquid Plus Fund - Regular Crisil Liquid Fund Index

Since Inception

1

0

2

3

4

5

6

7 6.516.07

12

mitment extends beyond the provision of accomplished investment management. It also embraces innovative product development, committed after-sales service and access to our first-hand expertise of markets.

Transparency

We promote transparency using technology and the full range of available media to achieve clear, open and appropriate communication with our clients.

Unique Investment Process

The Fixed Income investment process is a ‘Top Down - Bottom Up’ approach with a Top Down perspective being applied to Duration and Credit and a Bottom Up perspective being applied to Curve Positioning and Individual Security Selection.

Statutory Details and Risk Factors

Investors may obtain Offer Documents and Key Information Memorandums along with application forms from the office of HSBC Mutual Fund, 314 D. N. Road, Fort, Mumbai 400 001. Tel: 022-6666 8819. Statutory Details: HSBC Mutual Fund has been set up as a trust by HSBC Securities and Capital Markets (India) Private Limited (liability restricted to the corpus of Rs 1 lakh). The Sponsor / associates of the Sponsor/Asset Management Company (AMC) are not responsible or liable for any loss or shortfall resulting from the operation of the Schemes. The Trustees of HSBC Mutual Fund have appointed HSBC Asset Management (India) Private Limited as the Investment Manager. Risk Factors: All investments in mutual funds and securities are subject to market risks and the Net Asset Value (NAV) of the Scheme(s) may go up or down depending on the factors and forces affecting the securities markets. There can be no assurance that the objectives of the Scheme(s) will be achieved. Past performance of the Sponsor, AMC, Mutual Fund or any associates of the Sponsor/AMC does not indicate the future performance of the Scheme(s) of the Mutual Fund. HSBC Income Fund (HIF), HSBC Gilt Fund (HGF), HSBC Cash Fund (HCF), HSBC Liquid Plus Fund (HLPF), HSBC MIP (HMIP), HSBC Floating Rate Fund (HFRF) and HSBC Fixed Term Series (HFTS) are the names of the Schemes and do not in any manner indicate the quality of the Schemes or their future prospects or returns. Scheme Classification: HIF (an open-ended income Scheme) aims to provide reasonable income through a diversified portfolio of fixed income securities. The AMC’s view of interest rate trends and the nature of the Plans will be reflected in the type and maturities of securities in which the Short Term and Investment Plans are invested. HGF (an open-ended gilt Scheme) aims to generate reasonable returns through investments in Government Securities of various maturities. HCF (an open-ended liquid Scheme) aims to provide reasonable returns, commensurate with low risk while providing a high level of liquidity, through a portfolio of money market and debt securities. HLPF (an open-ended debt Scheme) seeks to provide liquidity and reasonable returns by investing primarily in a mix of short term debt and money market instruments. HMIP (an open-ended Fund with Regular & Savings Plans. Monthly income is not assured and is subject to availability of distributable surplus.) seeks to generate reasonable returns through investments in Debt and Money Market Instruments. The secondary objective of the Scheme is to invest in equity and equity related instruments to seek capital appreciation. HFRF (an open-ended income Scheme) seeks to generate a reasonable return with commensurate risk through investments in floating rate debt instruments and fixed rate debt instruments swapped for floating rate returns. The Scheme may also invest in fixed rate money market and debt instruments. HFTS (a close-ended Income Scheme) seeks to generate reasonable returns by investing in a portfolio of fixed income instruments normally maturing in line with the time profile of the respective Plan(s). Terms of Issue: Units of the Scheme(s) are being offered at NAV based prices, subject to the prevailing loads. The AMC calculates and publishes NAVs and offers for sale, redemption and switch outs, units of the Scheme(s) on all Business Days, at the Applicable NAV for all Schemes. However HFTS will not be open for ongoing subscriptions/switch ins. Load Structure (includes SIP/STP): HMIP – Entry – Nil. Exit - 0.5% for investments < Rs 10 lakhs, if redeemed/switched out* within 6 months from date of investment. For STP/SEP – Nil. In case of HIF-IP & HFRF-LTP - Entry - Nil. Exit - 0.5% for < Rs 10 lakhs in Regular Option, if redeemed/switched out* within 6 months from the date of investment. For STP/SEP – Nil. *No load in case of switches between equity Schemes of HSBC Mutual Fund. No load in case of HCF, HGF, HLPF, HIF-ST & HFRF-ST. Load in case of dividend reinvestments: Entry - 2.25% in case of Weekly Dividend sub-option under Institutional & Institutional Plus Option of HCF & HFRF-STP. Exit – Nil. No load in case of investments by Fund-of-Funds, FIIs & their sub-accounts. The entry / exit loads set forth above are subject to change at the discretion of the AMC and such changes shall be implemented prospectively. Please read the Offer Document for details and risk factors before investing.

For further information please consult your investment advisor or contact us at the numbers below.

HSBC Mutual Fund Investor Service Centres:

Write to us at [email protected] or visit www.hsbcinvestments.co.insms INVEST to 56767

Issued by HSBC Asset Management (India) Private Limited

• Ahmedabad : 098983 77319 / 21

• Andhra Pradesh : 098496 77319 / 21

• Bangalore : 080 4118 6519 / 21

• Bihar : 099313 97319 / 21

• Chandigarh : 0172 500 8119 / 21

• Chennai : 044 4200 8719 / 21

• Coimbatore : 098944 77319 / 21

• Delhi : 011 4149 0719 / 21

• Hyderabad : 040 6667 4719 / 21

• Indore : 098934 77319 / 21

• Jaipur : 099280 37319 / 21

• Karnataka : 099280 37319 / 21

• Kerala : 098954 77319 / 21

• Kochi : 098954 77319 / 21

• Kolkata : 033 2213 9919 / 21

• Lucknow : 099367 97319 / 21

• Maharashtra / Goa : 099600 77321

• MP / Chattisgarh : 098934 77319 / 21

• Mumbai : 022 6666 8819 / 21

• NCR : 099107 97319

• Pune : 020 2600 1119 / 21

• Punjab : 098769 37319 / 21

• UP : 099350 97321

• Vadodara : 098983 77319 / 21

Sep

tem

ber

II

2007