A Smiling Bear in the Equity Options Market and the Cross ... · A Smiling Bear in the Equity...

48

A Smiling Bear in the Equity Options Market and the Cross-section of Stock Returns Hye Hyun Park * , Baeho Kim † , and Hyeongsop Shim ‡ (This verstion: September 20, 2016) § ABSTRACT We propose a measure for the convexity of an option-implied volatility curve, IV convexity, as a forward-looking measure of risk-neutral tail-risk contribution to the perceived variance of underlying equity returns. Using equity options data for individual U.S.-listed stocks during 2000-2013, we find that the average realized return differential between the lowest and highest IV convexity quintile portfolios exceeds 1% per month, which is both economically and statistically significant on a risk-adjusted basis. Our empirical findings indicate the contribution of informed options trading to price discovery in terms of the realization of tail-risk aversion in the stock market. Keywords: Implied volatility; Convexity; Equity options; Stock returns; Predictability JEL Classification: G12; G13; G14 * Korea University Business School, Anam-dong, Sungbuk-Gu, Seoul 136-701, Republic of Korea, E- mail: [email protected]. † Corresponding Author. Korea University Business School, Anam-dong, Sungbuk-Gu, Seoul 136-701, Republic of Korea, Phone: +82-2-3290-2626, Fax: +82-2-922-7220, E-mail: [email protected]. ‡ Ulsan National Institute of Science and Technology, UNIST-gil 50, Technology Management Building 701-9, Ulsan, 689-798 Republic of Korea. E-mail: [email protected]. § This research was supported by the National Research Foundation of Korea Grant funded by the Korean Government (2015S1A5A8014515), for which the authors are indebted. The authors are grateful for helpful discussions and insightful comments to Kyounghun Bae, Ki Beom Binh, Bart Frijns, Paul Geertsema, Daejin Kim, Dongcheol Kim, James A. Park, Bumjean Sohn, Sun-Joong Yoon, and participants of the 28th Australasian Finance and Banking Conference, 2015 Derivative Markets Conference, the 11th conference of Asia-Pacific Association of Derivatives. All errors are the authors’ responsibility.

Transcript of A Smiling Bear in the Equity Options Market and the Cross ... · A Smiling Bear in the Equity...

A Smiling Bear in the Equity Options Market

and the Cross-section of Stock Returns

Hye Hyun Park∗, Baeho Kim†, and Hyeongsop Shim‡

(This verstion: September 20, 2016)§

ABSTRACT

We propose a measure for the convexity of an option-implied volatility curve,

IV convexity, as a forward-looking measure of risk-neutral tail-risk contribution to

the perceived variance of underlying equity returns. Using equity options data for

individual U.S.-listed stocks during 2000-2013, we find that the average realized

return differential between the lowest and highest IV convexity quintile portfolios

exceeds 1% per month, which is both economically and statistically significant on

a risk-adjusted basis. Our empirical findings indicate the contribution of informed

options trading to price discovery in terms of the realization of tail-risk aversion in

the stock market.

Keywords: Implied volatility; Convexity; Equity options; Stock returns; Predictability

JEL Classification: G12; G13; G14

∗Korea University Business School, Anam-dong, Sungbuk-Gu, Seoul 136-701, Republic of Korea, E-mail: [email protected].†Corresponding Author. Korea University Business School, Anam-dong, Sungbuk-Gu, Seoul 136-701,

Republic of Korea, Phone: +82-2-3290-2626, Fax: +82-2-922-7220, E-mail: [email protected].‡Ulsan National Institute of Science and Technology, UNIST-gil 50, Technology Management Building

701-9, Ulsan, 689-798 Republic of Korea. E-mail: [email protected].§This research was supported by the National Research Foundation of Korea Grant funded by

the Korean Government (2015S1A5A8014515), for which the authors are indebted. The authors aregrateful for helpful discussions and insightful comments to Kyounghun Bae, Ki Beom Binh, BartFrijns, Paul Geertsema, Daejin Kim, Dongcheol Kim, James A. Park, Bumjean Sohn, Sun-Joong Yoon,and participants of the 28th Australasian Finance and Banking Conference, 2015 Derivative MarketsConference, the 11th conference of Asia-Pacific Association of Derivatives. All errors are the authors’responsibility.

1. Introduction

The non-normality of stock returns has been well-documented in literature as a natural

extension of the traditional mean-variance approach to portfolio optimization.1 In general,

a rational investor’s utility is also a function of higher moments, as the investor tends to

have an aversion to negative skewness and high excess kurtosis of her asset return; see

Scott & Horvath (1980), Dittmar (2002), Guidolin & Timmermann (2008), and Kimball

(1990).2 While considerable research has subsequently examined whether the higher-

moment preference is indeed priced in the realized stock returns (e.g., Chung, Johnson &

Schill (2006); Dittmar (2002); Doan, Lin & Zurbruegg (2010); Harvey & Siddique (2000);

Kraus & Litzenberger (1976); and Smith (2007)), the higher-moment pricing effect is

embedded in equity option prices in a forward-looking manner. Specifically, the shape of

an option-implied volatility curve reveals the ex-ante higher-moment implications beyond

the standard mean-variance framework, as the curve expresses the degree of abnormality

in the option-implied distribution of the underlying stock return by inverting the standard

Black & Scholes (1973) option-pricing model.3

Although empirical research abounds in examining the risk-neutral skewness of

stock returns implied by equity option prices, the option-implied excess kurtosis has

received less attention.4 Our study attempts to fill this gap. Exploiting the fact that the

shape of an option-implied volatility curve contains information about ex-ante

higher-moment asset pricing implication, we propose a method to decompose the shape

of option-implied volatility curves into the slope and convexity components. Motivated

by stochastic volatility (SV) model and stochastic-volatility jump-diffusion (SVJ) model

specifications, we conjecture that slope and convexity of the option-implied volatility

curve contain distinct information about future stock return and convey the information

about risk-neutral skewness and the excess kurtosis of the underlying return

distributions, respectively. We confirm that the slope and convexity components (IV

slope and IV convexity hereafter) carry different information from extensive numerical

1The mean-variance approach is consistent with the maximization of expected utility if either (i)the investors’ utility functions are quadratic, or (ii) the assets’ returns are jointly normally distributed.However, a quadratic utility function may be unrealistic for practical purposes, as it exhibits increasingabsolute risk aversion, consistent with investors who reduce the dollar amount invested in risky assets astheir initial wealth increases; see Arrow (1971).

2Decreasing absolute prudence implies the kurtosis aversion according to Kimball (1990).3To better explain the positively-skewed and platokurtic preference of rational investors, prior studies

have attempted to relax the unrealistic normality assumption to capture the negatively-skewed and fat-tailed distribution of option-implied stock returns by extending the standard Black & Scholes (1973)model to stochastic volatility models and jump-diffusion models.

4There are some notable exceptions from this trend; refer to Bali, Hu & Murray (2015) and Chang,Christoffersen & Jacobs (2013) for example.

1

analyses and investigate whether the risk-neutral kurtosis, proxied by IV convexity,

predicts the cross-section of future stock returns, even after the option-implied skewness

effect is controlled.

Using equity options data for both individual U.S. listed stocks and the Standard

& Poor’s 500 (S&P500) index during 2000-2013, we study the ability of IV convexity

to predict the cross-section of future equity returns across quintile portfolios ranked by

the curvature of the option-implied volatility curve. We find a significantly negative

relationship between IV convexity and subsequent stock returns. The average return

differential between the lowest and highest IV convexity quintile portfolios exceeds 1%

per month, both economically and statistically significant on a risk-adjusted basis. The

results are robust across various definitions of the IV convexity measure. Both time series

and cross-sectional tests show that other well-known risk factors and firm characteristics

do not subsume the additional return on the zero-cost portfolio. Moreover, the predictive

power of our proposed IV convexity measure is significant for both the systematic and

idiosyncratic components of IV convexity, and the results are robust even after controlling

for the slope of the option-implied volatility curve and other known predictors based on

stock characteristics.

Where does the predictive power of IV convexity come from? Our finding is

consistent with earlier studies demonstrating the informational leading role of the

options market to the stock market. Extensive research demonstrates that equity option

markets provide informed traders with opportunities to capitalize on their information

advantage thanks to several advantages of option trading relative to stock trading.

Examples include (i) reduced trading costs (Cox & Rubinstein (1985)), (ii) the lack of

restrictions on short selling (Diamond & Verrecchia (1987)) and (iii) greater leverage

effect and built-in downside protection (Manaster & Rendleman (1982)). In this

context, Chakravarty, Gulen & Mayhew (2004) document that the option market’s

contribution to price discovery is approximately 17% on average.5 Although one may

think of the private information as being directional, information on uncertainty can

also motivate informed options trading; see Ni, Pan & Poteshman (2008) for instance.

Then, why is the relationship negative between IV convexity and the realized return of

underlying equity return in the subsequent month? We highlight that the shape of option-

implied volatility curves reveals the implication of risk-neutral higher order moments of

underlying return distributions. Given that excessive tail-risk is certainly unfavorable

to rational equity investors, the fat-tailed risk-neutral distribution incorporates ex-ante

5See also An, Ang, Bali & Cakici (2014), Chowdhry & Nanda (1991), Easley, O’Hara & Srinivas(1998), Bali & Hovakimian (2009), and Cremers & Weinbaum (2010) among others.

2

estimates of market risk premia regarding future rare events. In other words, a heavier tail

in the risk-neutral distribution is associated with a higher required return (or, equivalently,

a larger discount rate), and the informed option trading related to IV convexity predicts

a negative short-term return on the underlying stock returns as a result of price discovery

driven by an asymmetric information transmission from options traders to stock investors.

Simply put, our empirical findings indicate the contribution of informed options trading

to price discovery in terms of the realization of tail-risk aversion in the stock market. We

confirm that the predictive power of IV convexity becomes more pronounced for the firms

with stronger information asymmetry and more severe short-sale constraints, especially

during economic contraction period, and the cross-sectional predictability of IV convexity

disappears as the forecasting horizon increases.

Our study extends recent literature showing an increased interest in inter-market

inefficiency, leading to a proliferation of studies into the potential lead-lag relationship

between options and stock prices. For example, An et al. (2014) find stocks with large

innovations in at-the-money (ATM) call (put) implied volatility positively (negatively)

predict future stock returns. Xing, Zhang & Zhao (2010) propose an option-implied

volatility skew (henceforth IV smirk) measure showing its significant predictability for

the cross-section of future equity returns. Jin, Livnat & Zhang (2012) find that options

traders have superior abilities to process less anticipated information relative to equity

traders by analyzing the slope of option-implied volatility curves. Yan (2011) reports a

negative predictive relationship between the slope of the option implied volatility curve (as

a proxy of the average size of the jump in the stock price dynamics) and the future stock

return by taking the spread between the ATM call and put option-implied volatilities

(henceforth IV spread) as a measure of the slope of the implied volatility curve. Cremers

& Weinbaum (2010) argue that future stock returns can be predicted by the deviation

from the put-call parity in the equity option market, as stocks with relatively expensive

calls compared to otherwise identical puts earn approximately 50 basis points per week

more in profit than the stocks with relatively expensive puts.

This paper offers several contributions to the existing literature. First, this study

examines whether IV convexity exhibits significant predictive power for future stock

returns even after controlling for the effect of IV slope and other firm-specific

characteristics. Although recent evidence shows that the skewness component of the

risk-neutral distribution of underlying stock returns, our research is, to the best of our

knowledge, the first study that makes a sharp distinction between the 3rd and 4th

moments of equity returns implied by option prices. Specifically, we decompose the

information extracted from the shape of option-implied volatiltiy curve into separate IV

3

slope and IV convexity measures, and empirically verify that IV convexity significantly

predicts the cross section of future stock returns even after controlling for the IV slope

effect. Furthermore, IV spread measure proposed by Yan (2011) simply captures the

effect of the average jump size but not the effect of jump-size volatility in the SVJ

model framework. We extend those findings by examining how IV convexity explains

the cross-section of future stock returns to address the jump-size volatility effect.

Furthermore, this paper overcomes the potential caveat of ex-post information from past

realized returns in the previous studies on the effect of skewness (e.g., Kraus &

Litzenberger (1976); Lim (1989); Harvey & Siddique (2000)) by estimating an ex-ante

measures of skewness (IV slope) and excess kurtosis (IV convexity) from the

forward-looking option price data.6

This paper sheds new light on the relationship between the higher-moment

information from individual equity option prices and the cross-section of future stock

returns. Chang et al. (2013) investigate how market-implied skewness and kurtosis affect

the cross-section of stock returns by looking at the risk-neutral skewness and kurtosis

implied by index option prices based on the model framework proposed by Bakshi,

Kapadia & Madan (2003). However, their approach ignores the idiosyncratic

components of option-implied higher moments in stock returns.7 Our paper extends the

findings of Chang et al. (2013) by employing firm-level equity option price data, and

further decomposing IV convexity into systematic and idiosyncratic components to fully

identify the lead-lag relationship between IV convexity and the cross-section of future

stock returns.

2. Motivation

In this section, we demonstrate the asset pricing implications of our proposed IV

convexity measure. As known, an option-implied risk-neutral distribution of the

underlying stock return exhibits heavier tails than the normal distribution with the same

mean and standard deviation, in the presence of higher moments such as skewness and

excess kurtosis.8 Accordingly, information about these higher moments embedded in the

various shapes of implied volatility curves can be examined from various perspectives.

6The ex-post higher moments estimated from the realized stock returns can be biased unless the returndistribution is stationary and time-invariant; refer to Bali et al. (2015) and Chang et al. (2013).

7Yan (2011) finds that both the systematic and idiosyncratic components of IV spread are priced andthat the latter dominates the former in capturing the cross-sectional variation of future stock returns.

8Hereafter, we use kurtosis and excess kurtosis interchangeably, despite their conceptual differences.

4

Figure 1: Shape of the Implied Volatility Curves

This figure illustrates the effect of different values of skewness and excess kurtosis of underlying

asset returns on the shape of the implied volatility curve. The base parameter set is taken as (r,

σ, skewness, excess kurtosis)=(0.05, 0.3,−0.5, 1.0) where r is the risk-free rate and σ is standard

deviation, and (S0, T ) = (100, 0.5) as an illustrative example.

0.8 0.85 0.9 0.95 1 1.05 1.1 1.15 1.20.2

0.22

0.24

0.26

0.28

0.3

0.32

0.34

0.36

Moneyness (K/S)

Impl

ied

Vol

atili

ty

Skewness = −1.0Skewness = −0.75Skewness = −0.5Skewness = −0.25Skewness = 0.0

0.8 0.85 0.9 0.95 1 1.05 1.1 1.15 1.20.23

0.24

0.25

0.26

0.27

0.28

0.29

0.3

0.31

0.32

0.33

Moneyness (K/S)

Impl

ied

Vol

atili

ty

Kurtosis = 0.0Kurtosis = 0.5Kurtosis = 1.0Kurtosis = 1.5Kurtosis = 2.0

2.1. Risk-neutral Higher-order Moments

To explore the effects of risk-neutral skewness and excess kurtosis on option pricing, we

consider a geometric Levy process to model the risk-neutral dynamics of the underlying

stock price given by

St = S0eXt , (1)

where X is the return process whose increments are stationary and independent. In this

context, a natural characterization of a probability distribution is specifying its cumulants,

as we can readily expand the probability distribution function via the Gram-Charlier

expansion, a method to express a density probability distribution in terms of another

(typically Gaussian) probability distribution function using cumulant expansions.9 This

feature aids in understanding how the skewness and kurtosis of the underlying asset return

affect the shape of the option-implied volatility curves.10

Figure 1 illustrates the effect of different values of skewness and excess kurtosis on the

shape of an implied volatility curve. We can observe that a negatively skewed distribution,

ceteris paribus, leads to a steeper volatility smirk, whereas an increase in the excess

9The nth cumulant is defined as the nth coefficient of the Taylor expansion of the cumulant generatingfunction, the logarithm of the moment generating function. Intuitively, the first cumulant is the expectedvalue, and the nth cumulant corresponds to the nth central moment for n = 2 or n = 3. For n ≥ 4, thenth cumulant is the nth degree polynomial in the first n central moments.

10See Tanaka, Yamada & Watanabe (2010) for details of the application of Gram-Charlier expansionfor option pricing.

5

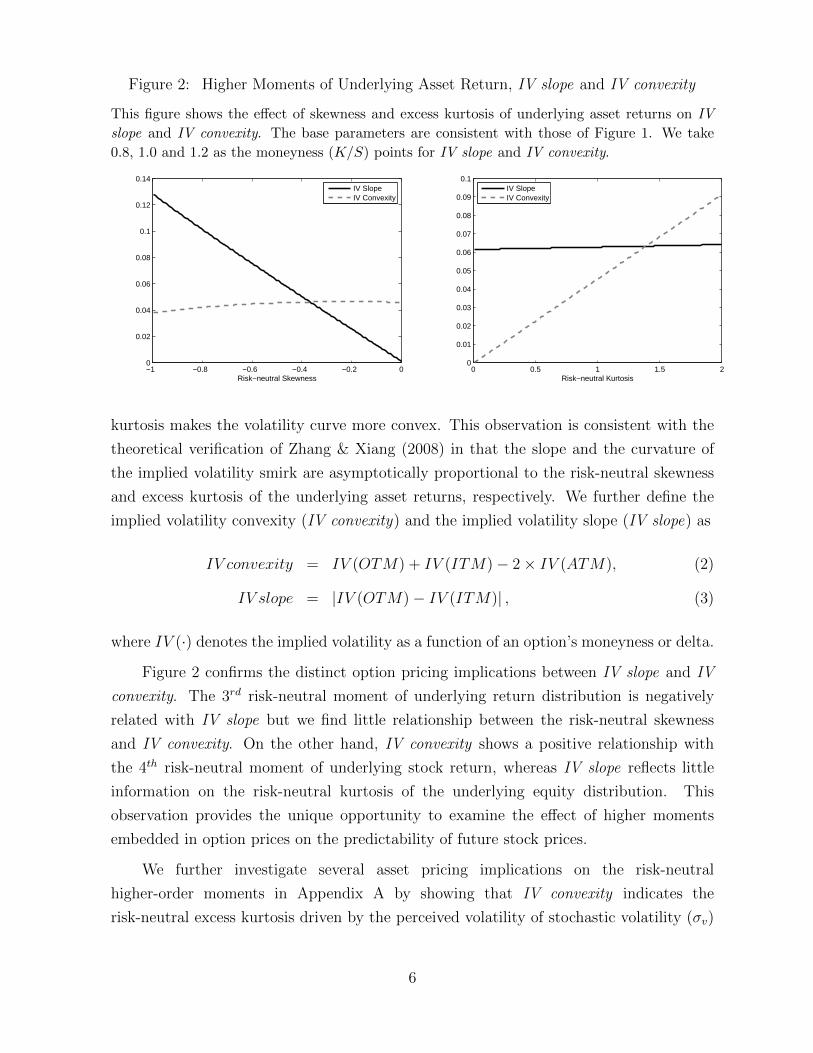

Figure 2: Higher Moments of Underlying Asset Return, IV slope and IV convexity

This figure shows the effect of skewness and excess kurtosis of underlying asset returns on IV

slope and IV convexity. The base parameters are consistent with those of Figure 1. We take

0.8, 1.0 and 1.2 as the moneyness (K/S) points for IV slope and IV convexity.

−1 −0.8 −0.6 −0.4 −0.2 00

0.02

0.04

0.06

0.08

0.1

0.12

0.14

Risk−neutral Skewness

IV SlopeIV Convexity

0 0.5 1 1.5 20

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.1

Risk−neutral Kurtosis

IV SlopeIV Convexity

kurtosis makes the volatility curve more convex. This observation is consistent with the

theoretical verification of Zhang & Xiang (2008) in that the slope and the curvature of

the implied volatility smirk are asymptotically proportional to the risk-neutral skewness

and excess kurtosis of the underlying asset returns, respectively. We further define the

implied volatility convexity (IV convexity) and the implied volatility slope (IV slope) as

IV convexity = IV (OTM) + IV (ITM)− 2× IV (ATM), (2)

IV slope = |IV (OTM)− IV (ITM)| , (3)

where IV (·) denotes the implied volatility as a function of an option’s moneyness or delta.

Figure 2 confirms the distinct option pricing implications between IV slope and IV

convexity. The 3rd risk-neutral moment of underlying return distribution is negatively

related with IV slope but we find little relationship between the risk-neutral skewness

and IV convexity. On the other hand, IV convexity shows a positive relationship with

the 4th risk-neutral moment of underlying stock return, whereas IV slope reflects little

information on the risk-neutral kurtosis of the underlying equity distribution. This

observation provides the unique opportunity to examine the effect of higher moments

embedded in option prices on the predictability of future stock prices.

We further investigate several asset pricing implications on the risk-neutral

higher-order moments in Appendix A by showing that IV convexity indicates the

risk-neutral excess kurtosis driven by the perceived volatility of stochastic volatility (σv)

6

and jump volatility (σJ) of underlying asset returns. The results confirm that IV

convexity is a forward-looking measure of excess tail-risk contribution to the perceived

variance of underlying equity returns under the risk-neutral measure.

2.2. Hypothesis Development

Having observed that the convexity of an option-implied volatility curve is a

forward-looking measure of the perceived likelihood of extreme movements in the

underlying equity price, we develop our empirical research question by examining how

IV convexity is related to the cross-section of future underlying stock returns. Notice

that the aforementioned theoretical analyses are based on the perfect information flow

between options and stock markets, where expected returns are irrelevant for option

pricing and equity investors express their tail-risk aversion simultaneously when equity

option investors generate leptokurtic implied distributions of future stock returns.

In reality, however, numerous empirical studies have identified that options market

would be an ideal venue for informed trading and options market could lead stock market

in the price discovery process, as informed traders have incentives to trade in options

markets to benefit from their informational advantage. Specifically, higher risk-neutral

excess kurtosis in the options market, ceteris paribus, can be an early warning signal of

the realized tail-risk aversion in the equity market, and vice versa. As such, we expect

that a persistent predictive capability of IV convexity for future stock returns with a

negative relationship would appear to link the risk-neutral excess kurtosis of the option-

implied stock returns to tail-risk aversion of stock investors with a significant time lag.

We summarize our research questions in the following testable main hypothesis:

• Main hypothesis: A slow and one-way information transmission from options to

stock markets enables informed options traders to capitalize on their private

information on the forthcoming of ex-post tail-risk perception in the stock market.

As a result, IV convexity would appear to link the excess kurtosis of the

risk-neutral stock returns to the realization of equity investors’ tail-risk aversion

associated with a higher tail-risk premium (or, equivalently, a larger discount rate)

with a significant time lag. This delayed price discovery mechanism will show a

persistent predictive capability of IV convexity for future stock returns with a

negative relationship.

The overall goal of our empirical analysis is to examine if the IV convexity measure

can show a significant cross-sectional predictive power for future equity returns. If we

7

observe negative relationship between IV convexity and future stock return with statistical

significance, it would empirically support the existing literature demonstrating the lead-

lag relationship between the options and stock markets in terms of the realization of

delayed tail-risk premium in the stock market.

3. Empirical Analysis

This section introduces our data set and methodology to estimate option-implied

convexity in a cross-sectional manner. We test whether IV convexity has strong

predictive power for future stock returns with statistical significance. Then, we compare

the impact of IV convexity with that of option-implied volatility slope on the future

underlying stock returns in the presence of various control variables.

3.1. Data and Sample

We obtain the U.S. equity and index option data from OptionMetrics on a daily basis

from January 2000 through December 2013. As the raw data include individual equity

options in the American style, OptionMetrics applies the binomial tree model of Cox,

Ross & Rubinstein (1979) to estimate the options-implied volatility curve to account for

the possibility of an early exercise with discrete dividend payments. Employing a kernel

smoothing technique, OptionMetrics offers an option-implied volatility surface across

different option deltas and time-to-maturities. Specifically, we obtain the fitted implied

volatilities on a grid of fixed time-to-maturities, (30 days, 60 days, 90 days, 180 days,

and 360 days) and option deltas (0.2, 0.25, . . . , 0.8 for call options and -0.8, -0.75, . . . ,

-0.2 for put options), respectively. Following An et al. (2014) and Yan (2011), we then

select the options with 30-day time-to-maturity at the end of each month to examine the

predictability of IV convexity for future stock returns.

[Table 1 about here.]

Table 1 shows the summary statistics of the fitted implied volatility and fixed deltas

of the individual equity options with one month (30 days) time-to-maturity chosen at the

end of each month. We can observe a positive convexity in the option-implied volatility

curve as a function of the option’s delta in that the implied volatilities from in-the-money

(ITM) options (calls for delta of 0.55 ∼ 0.80, puts for delta of −0.80 ∼ −0.55) options

and OTM (calls for delta of 0.20 ∼ 0.45, puts for delta of −0.45 ∼ −0.20) are greater on

8

average than those near the ATM options (calls for delta of 0.50, puts for delta of −0.50).

Panel B of Table1 reports the unique number of firms by industry each year. Each firm is

assigned into one of the Fama-French 12 industries (FF1-12) classification based on its SIC

code. There are 2,900 unique firms in 2000, rising to 4,159 in 2013. We obtain daily and

monthly individual common stock (shrcd in 10 or 11) returns from the Center for Research

in Security Prices (CRSP) for stocks traded on the NYSE (exchcd=1), Amex (exchcd=2),

and NASDAQ (exchcd=3). Stocks with a price less than three dollars per share are

excluded to weed out very small or illiquid stocks and the potential extreme skewness

effect (Loughran & Ritter (1996)). Accounting data is obtained from Compustat. We

obtain both daily and monthly data for each factor from Kenneth R. French’s website.11

3.2. Variables and portfolio formation

We adopt IV convexity as a risk-neutral proxy for the option-implied tail-risk perception

on the underlying stock returns over the life of option. Throughout this paper, we propose

our main measure of IV convexity defined as

IV convexity = IVput(−0.2) + IVput(−0.8)− 2× IVcall(0.5), (4)

where IVput(∆) and IVcall(∆) refer to the fitted put and call option-implied volatilities

with one month (30 days) to expiration, and ∆ is each options’ delta.12 Note that the

violation of put-call parity is commonly observed in practice, as the parity does not

account for potential market frictions and there is an early exercise possibility for deep

in-the-money American put options; e.g., Yan (2011) and Cremers & Weinbaum (2010)

find that the spread between put- and call-implied volatilities can predict the cross-section

of unerlying stock returns.

As shown in (4), IV convexity is defined as the sum of OTM and ITM put implied

volatilities less double the ATM call implied volatility.13 The rationale is that those who

have private information on the (forthcoming) widespread tail-risk aversion would buy a

cheap deep-OTM put option as a protection against the potential decrease in the stock

return for hedging purposes or buy a deep-ITM put option for taking its early exercise

premium as a leverage to grab a quick profit for speculative purposes to capitalize on

11http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.12Delta is commonly used as the industry practice of measuring moneyness, as an option’s delta is

sensitive to the option’s intrinsic value and time-value at the same time. Our results are robust acrossdifferent measures of moneyness, as we consider short-term maturity options in our analysis.

13See Section 3.4 for alternative measures of IV convexity.

9

private information.14 For the same reasoning, an informed investor who anticipate

heavier tail-risk aversion prevailing in the stock market would sell call options. We

subtract double the implied volatility of the ATM call option, which is generally the

most frequently traded option best reflecting market participants’ sentiment regarding

the firm’s future condition.

We also consider other measures related to the shape of option-implied volatility

curve. Specifically, option-implied volatility level and slope, denoted by IV level and IV

slope respectively, are defined as

IV level = 0.5× [IVput(−0.5) + IVcall(0.5)] , (5)

IV slope = IVput(−0.2)− IVput(−0.8), (6)

respectively. This decomposition enables us to investigate whether the IV slope and

IV convexity actually have distinct impacts on a cross-section of future stock returns,

thereby to check whether IV convexity carries extra predictability of future stock returns

controlling for return predictability of IV slope. Furthermore, we define IV spread as

IV spread = IVput(−0.5)− IVcall(0.5), (7)

which is proposed by Yan (2011), who argues that the IV spread mainly reflects the

contribution of 3rd moments of return distributions driven by the mean jump size in the

price dynamics. Next, motivated by Xing et al. (2010), we define IV smirk as the difference

between the implied volatility of the OTM put options and the ATM call options on the

same stock. If there are more than one record of OTM put or ATM call options for a

certain stock on the same day, we take the OTM put option with the moneyness (= K/S)

closest to 0.95 and the ATM call option with its moneyness (= K/S) closest to 1.15

14Although an ITM put option is costly, its demand can increase under strong short-sale constraints ofunderlying stocks with pessimistic tail-risk perception, as a severe short-selling constraint would make itmore expensive to capitalize on their negative private information in the equity market, where ITM putoptions would be rational alternatives. Recall that the delta of a deep-ITM American put option is closeto -1 owing to the possibility of early exercise.

15Xing et al. (2010) estimate IV smirk from the implied volatilities of options data, for which we applythe following filters to minimize the impact of recording errors. Following their methodology, we eliminatethe prices that violate no-arbitrage condition by using call data only when the call option prices fall insideof the interval (St −Dt,T −Ke−rt,T , S) and use put data only when the put option prices remain insideof the interval (Ke−rt,T − (St −Dt,T ), S), where S is the price of underlying stock, K is the strike priceof options, r is risk-free rate and D is the dollar dividend and T is the expiration time. We remove theoptions from the sample if their average of best bid price and best ask price is higher than $0.125, thebid price is equal to zero, or the ask price is lower than the bid price. We include the option contractwith positive open interest and non-missing volume data. The time-to-maturity of the options must bebetween 10-60 days and the implied volatility of the option should be between 3% and 200%.

10

Taking advantage of both equity options and index options data, we can disentangle

IV convexity into systematic and the idiosyncratic components. For this purpose, we run

the time series regression each month using the S&P500 index options with 30-day time-to

maturity as a benchmark for the market along with individual equity options at the end

of each month given by

IV convexityi,k = αi + βi × IV convexityS&P500,k + εi,k, (8)

where t − 30 ≤ k ≤ t − 1 on a daily basis. We define the fitted values and residual

terms as the systematic component of IV convexity (convexitysys) and the idiosyncratic

component of IV convexity (convexityidio), respectively.

[Table 2 about here.]

At the end of each month, we compute the cross-sectional IV level, IV slope, IV

convexity, IV smirk, and IV spread measures from 30-day time-to-maturity options. Panel

A of Table 2 shows the descriptive statistics for each implied volatility measure computed

at the end of each month using 30-day time-to-maturity options. As for the average values

for each of variable, IV level has 0.4739, IV slope for 0.0423, IV spread for 0.0090, IV

smirk for 0.0687, and IV convexity for 0.0952, respectively. The standard deviation of

IV convexity is 0.2774, and 0.1703 for convexitysys, 0.2235 for convexityidio, respectively.

Panel B of Table 2 reports the descriptive statistics of firm characteristics and asset pricing

factors.16

3.3. Predictive power of IV convexity

We now report our empirical results regarding the predictive power of IV convexity for

the cross-section of future underlying stock returns. When constructing a single sorted IV

convexity portfolio, we sort all stocks at the end of each month based on the IV convexity

and match with the subsequent monthly stock returns. The IV convexity portfolios are

rebalanced every month.

[Table 3 about here.]

Panel A of Table 3 reports the means and standard deviations of the five IV convexity

quintile portfolios and average monthly portfolio returns of both equal-weighted (EW) and

16See Appendix B for our variable definitions of firm characteristics (Size, BTM) and asset pricingfactors (Market β, MOM, REV, ILLIQ and Coskew).

11

value-weighted (VW) portfolios over the entire sample period. To examine the relationship

between IV convexity and future stock returns, we form five portfolios according to the

IV convexity value at the end of each month. Quintile 1 is composed of stocks with the

lowest IV convexity, while Quintile 5 is composed of stocks with the highest IV convexity.

These portfolios are rebalanced every month, and assumed to be held for the subsequent

one-month period. As shown, the average EW portfolio return monotonically decreases

from 0.0208 for the lowest quintile portfolio Q1 to 0.0074 for the highest quintile portfolio

Q5. The average monthly return of the arbitrage portfolio buying the lowest IV convexity

portfolio Q1 and selling highest IV convexity portfolio Q5 is significantly positive (0.0134

with t-statistics of 7.87). The average VW portfolio returns exhibit a similar decreasing

pattern from Q1 (0.0136) to Q5 (0.0023), and the return of zero-investment portfolio

(Q1-Q5) is significantly positive (0.0113 with t-statistics of 5.08).

Panel B and C of Table 3 show the average monthly returns of quintile portfolios

sorted by IV spread and IV smirk, respectively. The EW portfolios sorted by IV spread

show that their EW portfolio returns decrease monotonically from 0.0145 for quintile

portfolio Q1 to 0.0013 for quintile portfolio Q5, where the average return difference

between Q1 and Q5 amounts to 0.0131 with t-statistics of 7.31 and similar patterns are

observed with VW portfolios sorted by IV spread. These results certainly confirm the

empirical finding of Yan (2011) in that low IV spread stocks outperform high IV spread

stocks. In a similar vein, we find from Panel C that the average returns of quintile

portfolios sorted by IV smirk are decreasing in IV smirk, and the returns of

zero-investment portfolios (Q1-Q5) are all positive and statistically significant for both

the EW and VW portfolios, consistent with Xing, Zhang and Zhao (2010) in that there

exists a negative predictive relationship between IV smirk and future stock return.

Left panel of Figure 3 shows the monthly average IV convexity value for each quintile

portfolio, while Right panel plots the monthly average return of the arbitrage portfolio

formed by taking long position in the lowest quintile and short position in the highest

quintile portfolios (Q1-Q5). The time-varying average monthly returns of the long-short

portfolio are mostly positive, confirming the results reported in Table 3.

3.4. Alternative IV convexity measures

We next consider alternative measures of options-implied volatility convexity than ours

given by (4). We first explore various IV convexity measures by varying ITM and OTM

points of put options. Panel A of Table 4 reports descriptive statistics for average portfolio

returns based on the main IV convexity measure given by (4) estimated with various delta

12

Figure 3: Average IV convexity and Quintile Portfolio Returns

This figure shows the time-series behavior of the average IV convexity of the quintile portfolios

(Left panel) and the monthly average returns of the long-short portfolios Q1-Q5 (Right panel)

from Jan 2000 to Dec 2013 on a monthly basis.

Jan-00 01-Sep 03-May 05-Jan 06-Sep 08-May 10-Jan 11-Sep 13-May-0.5

0

0.5

1

1.5

Q1Q2Q3Q4Q5

Feb-00 01-Oct 03-Jun 05-Feb 06-Oct 08-Jun 10-Feb 11-Oct 13-Jun-0.05

0

0.05

0.1

0.15

Q1-Q5

points. The decreasing patterns in portfolio returns are still observed across different delta

points and arbitrage portfolio (Q1-Q5) returns are significantly positive for both the

equal-weighted and value-weighted portfolio returns. This result confirms the negative

relationship between IV convexity and future stock returns whatever delta points of put

options we use to compute convexity.

[Table 4 about here.]

Next, we construct various alternative measures of IV convexity, denoted by

IV convexity(·), between calls and puts given by

IV convexity(II) = IVput(−0.2) + IVput(−0.8)− 2× IVput(−0.5), (9)

IV convexity(III) = IVcall(0.2) + IVcall(0.8)− 2× IVcall(0.5), (10)

IV convexity(IV ) =IV convexity(II) + IV convexity(III)

2, (11)

IV convexity(V ) = IVput(−0.2) + IVcall(0.2)− 2× IVput(−0.5), (12)

IV convexity(V I) = IVput(−0.2) + IVcall(0.2)− 2× IVcall(0.5). (13)

As a benchmark, we first construct a put-based convexity measure, IV convexity(II), and

a call-based measure, IV convexity(III). Then, we define IV convexity(IV ) as the average

of IV convexity(II) and IV convexity(III) to incorporate comprehensive implied volatility

information from call and put options. Further, IV convexity(V ) and IV convexity(V I) are

13

constructed by the sum of OTM option-implied volatilities less the ATM option-implied

volatility. The rationale behind them is the fact that OTM put (call) options are generally

more liquid than the ITM call (put) options at the same strike prices.

We then construct a set of single-sorted quintile portfolios (from Q1 to Q5) by

sorting all stocks at the end of each month based on each of the alternative IV convexity

measures and match with the subsequent monthly stock returns. Quintile 1 is composed

of stocks with the lowest IV convexity(·) while Quintile 5 is composed of stocks with the

highest IV convexity(·). That is, at the end of each month, all firms are assigned to one

of five portfolio groups based on alternative options implied convexity. These portfolios

are equally weighted, rebalanced every month, and assumed to be held for the

subsequent one-month period. This process is repeated in every month. Panel B of

Table 4 reports the descriptive statistics of the average portfolio returns sorted by

alternative measures of IV convexity given by (4)-(13). Our empirical results show that

the alternative IV convexity measures generally produce a monotone decreasing pattern

of the average quintile portfolio returns, and the realized returns of the arbitrage

portfolio (Q1-Q5) across different definitions of IV convexity remain positive with

statistical significance.17 This result confirms our main hypotheses in that the negative

relationship between IV convexity and future stock returns are robust and consistent

across different definitions of IV convexity.

3.5. Controlling Firm-specific Factors

We investigate whether the positive arbitrage portfolio returns (Q1-Q5) are still significant

even after controlling for firm-specific equity risk factors. Accordingly, we test whether a

set of representative firm characteristics crowd out the negative relationship between IV

convexity and stock returns. To examine whether the relationship between IV convexity

and stock returns disappear after controlling for the firm characteristics, we double-sort

all stocks following Fama & French (1992). Specifically, all stocks are sorted into five

quintiles by ranking on standard equity risk factors and then sorting within each quintile

into five quintiles according to IV convexity.

[Table 5 about here.]

We first adopt the suggestion of Fama & French (1993) in that firm size,

book-to-market ratio, and Market β are regarded as the three main firm characteristic

17The mean arbitrage portfolio returns are significantly positive at 5% confidence level across differentmeasures of IV convexity except for the case of IV convexity(II) at 10% level of confidence.

14

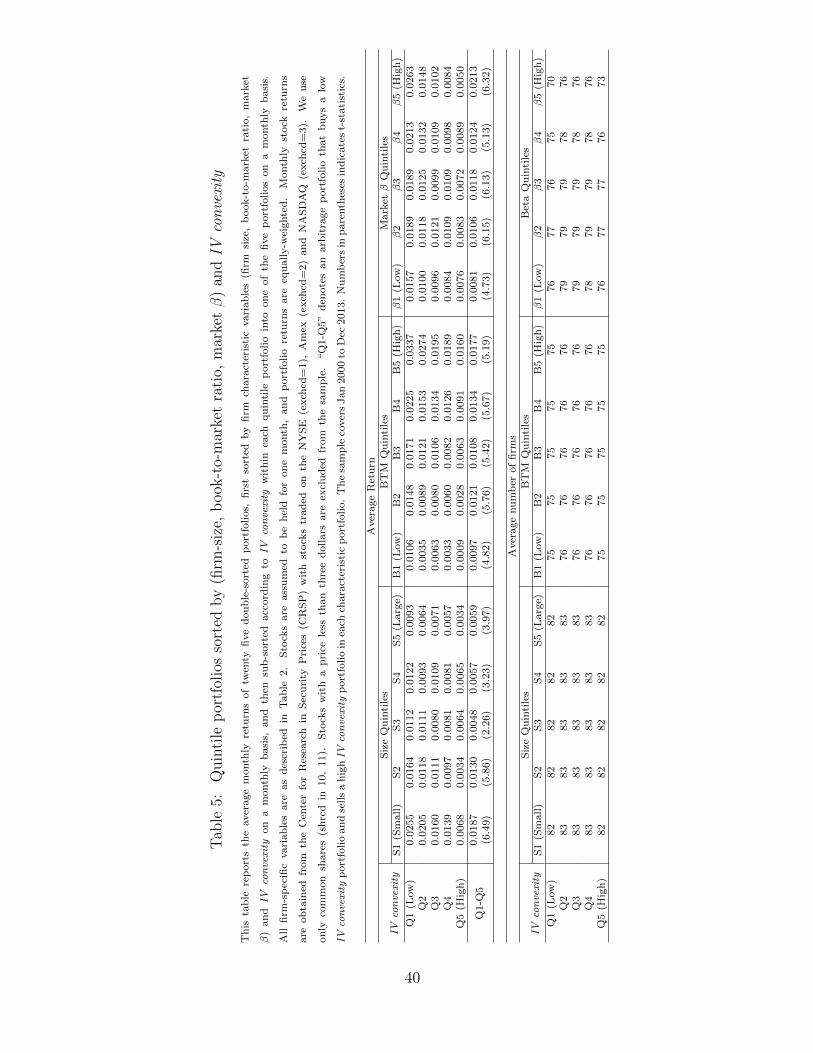

factors of stock returns. Table 5 reports the average monthly returns of the 25 (5 × 5)

portfolios sorted first by firm characteristic risks (firm size, book-to-market ratio, and

Market β) and then by IV convexity and average monthly returns of the long-short

arbitrage portfolios (Q1-Q5). We can observe that the average monthly portfolio returns

generally decline as the average firm-size increases. As shown in the results from

double-sorting using firm-size and IV convexity, we find that the returns of the IV

convexity quintile portfolios are still decreasing in IV convexity in most size quintiles,

and the return of all zero-investment portfolios (Q1-Q5) in size quintiles are all positive

and statistically significant. In particular, the positive difference in the smallest quintile

is the largest (0.0187) compared to the other size quintile portfolios.

The two-way cuts on book-to-market and IV convexity show that the higher book-

to-market portfolio gets more returns compared to the lower book-to-market portfolios

in each IV convexity quintile. The decreasing patterns in IV convexity portfolio returns

remain even after controlling the systematic compensation drawn from the book-to-market

factor. Note that the overall zero-cost portfolios formed by long Q1 and short Q5 are also

positive and statistically significant: 0.0097 (t-statistic of 4.82) for B1 (BTM quintile 1),

0.0121 (t-statistic of 5.76) for B2, 0.0108 (t-statistic of 5.42) for B3, 0.0134 (t-statistic of

5.67) for B4, and 0.0177 (t-statistic of 5.19) for B5.

When sorting the 25 portfolios first by Market β and then by IV convexity, the

negative relationship between IV convexity and stock return persists, implying that this

decreasing pattern cannot be explained by Market β. Note that the average monthly

portfolio returns generally increase as the average Market β rises.

We also consider the other four pricing factors of (i) the momentum effect documented

by Jegadeesh & Titman (1993), (ii) the short-term reversal suggested by Jegadeesh (1990)

and Lehmann (1990), (iii) the illiquidity proposed by Amihud (2002) and (iv) co-skewness

suggested by Harvey & Siddique (2000) to examine whether the decreasing pattern of

portfolio returns in IV convexity disappears when controlling these systematic risk factors.

Stocks are first sorted into five groups based on their momentum (or reversal, illiquidity,

co-skewness) measures and then sorted by IV convexity forming 25 (5 × 5) portfolios.

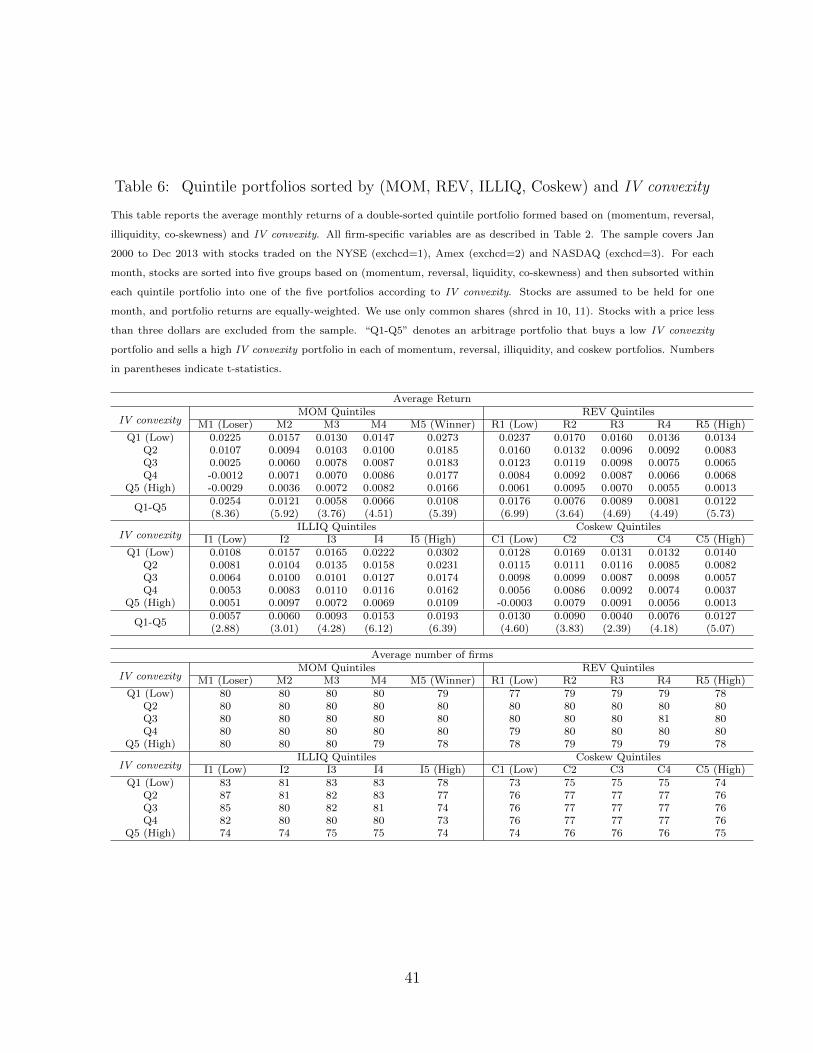

[Table 6 about here.]

Table 6 presents the returns of 25 portfolios sorted by each of four equity pricing

factors (momentum, reversal, illiquidity, co-skewness) and IV convexity. When we look

at the momentum patterns in the momentum-IV convexity portfolios, winner portfolios

consistently achieve more abnormal returns than loser portfolios except for the lowest

15

momentum-lowest IV convexity quintiles, which could be caused by using a different

sample datasets compared to that in Jegadeesh & Titman (1993). While Jegadeesh &

Titman (1993) use only stocks traded on the NYSE (exchcd=1) and Amex (exchcd=2),

we add stocks traded on the NASDAQ (exchcd=3). For the holding period strategies,

Jagadeesh and Titman (1993) adopt 3-, 6-, 9-, and 12-month holding periods, while this

study assumes that portfolios are held for one month.

Even after controlling momentum as a systematic risk, we observe that the portfolio

return differential between the lowest and highest IV convexity in each momentum

quintile remains significantly positive, indicating that IV convexity contains

economically meaningful information that cannot be explained by the momentum factor.

For the reversal-IV convexity double sorted portfolio case, there is a clear reversal

patterns in most cases when using a reversal strategy (i.e., the past winner earns higher

returns in the next month compared to past loser), though there are some distortions

in the lowest reversal-highest IV convexity quintiles. The Q1-Q5 strategy of buying and

selling stocks based on IV convexity in each reversal portfolio and holding them for one

month still earns significantly positive returns. This implies that the same results still

hold even after controlling for reversal effects.

We further incorporate the Amihud (2002) measure of illiquidity to address the role

of the liquidity premium in asset pricing. Amihud (2002) finds that the expected market

illiquidity has positive and highly significant effect on the expected stock returns, as

investors in the equity market require additional compensation for taking liquidity risk.

We examine whether the market illiquidity measure (ILLIQ) explains the higher return

on the lowest IV convexity stock portfolio (Q1) relative to the highest IV convexity

stock portfolio (Q5). The double-sorted quintile portfolios by ILLIQ andIV convexity

exhibit analogous patterns in that their average returns tend to decrease in IV

convexity. The zero-investment portfolios (Q1-Q5) based on the ILLIQ quintiles

demonstrate their significantly positive average returns across different ILLIQ quintiles.

This finding implies that a significantly negative IV convexity premium remains even

after we control for the illiquidity premium effect.

Next, we consider conditional skewness, as Harvey & Siddique (2000) find that

conditional skewness (Coskew) can explain the cross-sectional variation of expected

returns even after controlling factors based on size and book-to-market value. To

examine whether this Coskew factor captures the higher returns of the lowest IV

convexity stocks relative to the highest IV convexity stocks, we constructed 25 portfolios

sorted first by Coskew and then by IV convexity. For the Coskew-IV convexity double

16

sorted portfolios, there is a clear decreasing pattern in IV convexity within each Coskew

sorted quintile portfolio. The returns of zero-cost IV convexity portfolios (Q1-Q5)

within each Coskew quintile portfolio are all positive and statistically significant: 0.0130

(t-statistic of 4.60) for C1 (Coskew quintile 1), 0.0090 (t-statistic of 3.83) for C2, 0.0040

(t-statistic of 2.39) for C3, 0.0076 (t-statistic of 4.18) for C4, and 0.0127 (t-statistic of

5.07) for C5, respectively. A negative IV convexity premium remains significantly even

after we control for the Coskew premium effect. After all, we conclude that the negative

relationship between IV convexity and stock return consistently persists even after

controlling for various kinds of firm-specific risks identified in prior researches.

3.6. Correcting for implied-volatility skew

It is empirically important to figure out whether the implication of IV convexity is really

significant even after we correct for the skew of the implied-volatility curves. To answer

this question, we examine if the negative relationship between IV convexity and stock

returns persists after controlling for the effect of the option-implied volatility slope on

stock returns suggested by other researchers. For this purpose, we consider the following

three measures for the slope of the option-implied volatility curve: (i) IV slope, (ii) IV

spread, and (iii) IV smirk, where the last two measures are defined and estimated as in

Yan (2011) and Xing et al. (2010), respectively.

[Table 7 about here.]

Table 7 presents the average monthly returns of 25 portfolios sorted first by IV

slope, IV spread, andIV smirk and then sorted by IV convexity within each of IV slope,

IV spread, and IV smirk sorted quintile portfolios, respectively. The first five columns

show the results of our IV slope-IV convexity double sorted portfolio returns. We can

observe a decreasing pattern with respect to IV convexity in each IV slope quintile, and

the Q1-Q5 strategy based on IV convexity in each IV slope portfolio and holding them

for one month returns significantly positive profits across the different specifications. As

for IV spread, the IV convexity strategy that buys the lowest quintile portfolio and sells

the highest quintile portfolio within each IV spread portfolio yields significantly positive

returns in all cases, suggesting that IV spread does not capture the IV convexity effect.

It is also noteworthy that IV convexity arbitrage portfolios (Q1-Q5) from S1 to S5 IV

smirk portfolios produce significantly positive returns. This observation reveals that IV

smirk cannot fully capture the negative relationship between IV convexity and future

stock returns across different IV smirk quintile portfolios.

17

It might be the case that the predictive power of IV convexity is partially driven by

IV smirk and vice versa. To disentagle the problem, we decompose IV convexity into the

IV smirk part and the orthogonalized IV convexity part by regressing daily IV convexity

against IV smirk. Specifically, the orthogonalized implied volatility convexity, denoted by

orthogonalized IV convexity, is defined as the residual terms of the regression specification

given by

IV convexityi,k = αi + βi × IV smirki,k + εconvexityi,k , (14)

where t− 30 ≤ k ≤ t− 1 on a daily basis. In a similar vein, we define the orthogonalized

IV smirk as the residual terms of the regression specification given by

IV smirki,k = αi + βi × IV convexityi,k + εsmirki,k . (15)

We then sort all stocks at the end of each month based on the orthogonalized IV

convexity (εconvexity) and orthogonalized IV smirk (εsmirk), and match with the subsequent

monthly stock returns by rebalancing the 5 quintile (from the lowest Q1 to the highest Q5)

portfolios every month. As a result, we observe that the average portfolio return decreases

from Q1 (0.0090) to Q5 (0.0064), and the monthly return differential between Q1 and Q5

is 0.0025 with t-statistics of 2.74. This result indicates that the return predictability of IV

convexity cannot be fully explained by that of IV smirk. On the other hand, it is shown

that the predictive power of orthogonalized IV smirk is statistically insignificant, as the

difference between average return of Q1 (0.0085) and that of Q5 (0.0084) is less than

0.0001 with t-statistics of 0.030. That is, the return predictability of IV smirk disappears

if we correct for the effect of IV convexity.

All in all, these findings support the proposition that the negative relationship of

IV convexity to future stock returns still holds after considering the impact of IV slope,

IV spread, and IV smirk on stock returns. Our observation implies that the impact of

IV convexity on the distribution of stock returns does not fully come from IV slope, IV

spread, and IV smirk and that IV convexity is an important factor in determining the

fat-tailed distribution characteristics of future stock returns.

3.7. Systematic and Idiosyncratic Components of IV convexity

Total risk of stock returns can be decomposed into systematic and idiosyncratic

components. In theory, the systematic risk factor (Market β) should be priced in

equilibrium, while the idiosyncratic risk factor cannot capture the cross-sectional

18

variation of stock returns. However, the real-world investors cannot perfectly diversify

away the idiosyncratic risks, thereby it is often observed that idiosyncratic risk can also

play an important role in the cross-sectional variation of stock returns. In this context,

we decompose IV convexity into systematic and idiosyncratic components to further

investigate the source of negative relationship between IV convexity and the

cross-section of future stock returns. As our data set includes both equity options and

index options, we can effectively decompose IV convexity into the systematic and

idiosyncratic components by performing a simple regression analysis given by (8).

[Table 8 about here.]

Panel A of Table 8 provides the descriptive statistics for the average portfolio

returns sorted by systematic components and idiosyncratic components of IV convexity.

It shows that the average portfolio return monotonically decreases from Q1 to Q5 and

that the return differential between Q1 and Q5 is significantly positive. It is worth

noting that the negative pattern is robust even if we decompose IV convexity into the

systematic and idiosyncratic components. That is, convexitysys and convexityidio reveal

decreasing patterns in the portfolio returns as the IV convexity portfolio increases. The

difference between the lowest and the highest quintile portfolios sorted by convexitysys

and convexityidio are significantly positive with t-statistics of 6.56 and 5.72, respectively.

This implies that both components have predictive power for future portfolio returns

and are significantly priced.

Panel B of Table 8 reports the average monthly portfolio returns of the 25 quintile

portfolios formed by sorting stocks based on (convexitysys, convexityidio) first, and then

sub-sorted by IV convexity in each of convexitysys or convexityidio quintile. This will

allow us to figure out how the systematic or idiosyncratic components contribute to IV

convexity. In other words, if the decreasing patterns of returns in IV convexity portfolio

become less clearly observed under the control of (convexitysys, convexityidio), this can

be interpreted as a component of convexitysys or convexityidio and can mostly explain the

cross-sectional variation of return on IV convexity compared to the other component of

convexitysys or convexityidio .

As for the results from the sample sorted first by convexitysys and then by IV

convexity, the decreasing patterns generally persist for the convexitysys quintiles, though

there are some distortions in the 1st and 3rd convexitysys quintiles for the highest IV

convexity quintiles. Note that the arbitrage portfolio’s returns (Q1-Q5) in each

convexitysys quintile portfolio still remain large and statistically significant. As for the

19

convexityidio-IV convexity double sorted portfolios shown in the right-hand side of Table

8, the negative relationship between IV convexity and average portfolio return exists,

though the order of portfolio returns are not perfectly preserved in the 3rd and 5th

convexityidio quintiles. In addition, the long-short IV convexity portfolio returns in the

convexityidio quintile portfolio (Q1-Q5) are significantly positive with a t-statistic larger

than two. Thus, these results provide evidence that neither component can fully capture

and explain all cross-section variations of returns on IV convexity, but both components

(convexitysys and convexityidio) have decreasing patterns of portfolio returns, and are

needed to capture the cross-sectional variations of returns.

3.8. Short-selling Constraints and Information Asymmetry

We next look at the negative relationship between IV convexity and future stock returns

with respect to firm-level information asymmetry and short-selling constraints. We first

hypothesize that the decreasing pattern of the IV convexity portfolio returns becomes

more pronounced for the firms with more restrictive short-selling constraints. Secondly,

we infer that informed traders have more opportunities to get higher profit from the stocks

with more severe disparity of information possessed by informed traders. Subsequently,

the decreasing pattern of the IV convexity portfolio returns will become more pronounced

for the stocks with stronger information asymmetry.

In this context, we employ the measures of analyst coverage and analyst forecast

dispersion as proxies for information asymmetry along with the share of institutional

ownership as a proxy for the short-selling constraints. According to Diether, Malloy &

Scherbina (2002), analyst forecast dispersion is measured by the scaled standard

deviation of I/B/E/S analysts’ fiscal quarterly earnings per share forecasts. Stronger

information asymmetry is implied by less numbered analyst coverage and greater

analyst forecast dispersion. As the measure of short-sale constraint, following Campbell,

Hilscher & Szilagyi (2008) and Nagel (2005), we calculate the share of institutional

ownership by summing the stock holdings of all reporting institutions for each stock on

a quarterly basis. Nagel (2005) refers that short-sale constraints are most likely to bind

among the stocks with high individual (i.e., low institutional) ownership, so the stocks

with less institutional ownership suffer from more binding short-sale constraints.

[Table 9 about here.]

Table 9 reports the average monthly returns of double-sorted portfolios, first sorted

by the previous quarterly percentage of shares outstanding held by institutions obtained

20

from the Thomson Financial Institutional Holdings (13F) database, previous quarter’s

analyst coverage obtained from I/B/E/S, previous quarter’s analyst forecast dispersion

obtained from I/B/E/S, respectively and then sub-sorted according to IV convexity within

each quintile portfolio on a monthly basis. We observe that the decreasing pattern in the

average monthly portfolio returns appears to be more pronounced for the stocks with

institutional investors owning a small fraction of the firm’s share. Furthermore, we find

that the IV convexity zero-cost portfolio within lowest institutional ownership portfolio

earns greater positive return than that within the highest institutional ownership portfolio.

The IV convexity effect appears to be stronger when less sophisticated investors (i.e.,

more individual investors) own a large fraction of a firm’s shares. This result confirms

the hypothesis that the decreasing patterns of the IV convexity portfolio returns become

more pronounced for the stocks with stronger short-selling constraints.

The next five columns show how the degree of information asymmetry affects the

predictability of IV convexity. We find that the decreasing pattern of the IV convexity

quintile portfolio returns becomes stronger for in lower analyst coverage quintiles, albeit

some distortion in AC4 and AC5 quintiles. The last pair of columns show the results based

on the analyst forecast dispersion as a proxy for information asymmetry measure. We find

that the IV convexity effect becomes stronger for high analyst forecast dispersion firms,

and the returns of zero-investment IV convexity portfolios (Q1-Q5) within the lowest AD

quintile portfolio return is 0.0081, while that of the highest AD quintile portfolio return

amounts to 0.0162 on a monthly basis. These results imply that the stocks with strong

information asymmetry and with severe short-sale constraints induce the informed traders

mainly trade in the options market rather than in the stock market. This finding confirms

our Hypothesis in the sense that there is a slow one-way information transmission from

the options market to the stock market owing to the cross-market information asymmetry.

4. Robustness Checks

This section addresses additional aspects of IV convexity for robustness. We first explore

time-series analysis along with different forecasting horizons, and then conduct a Fama-

MacBeth regression analysis with various control variables. Subsequently, we perform a

sub-period analysis as a robustness check.

21

4.1. Time-series Analysis

To test whether the existing risk factor models can absorb the observed negative

relationship between IV convexity and future stock returns, we conduct a time-series

test based on CAPM and the Fama & French (1993) three factor model (FF3). The

Fama & French (1993) model has three factors: (i) Rm − Rf (the excess return on the

market), (ii) SMB (the difference in returns between small stocks and big stocks) and

(iii) HML (the difference in returns between high book-to-market stocks and low

book-to-market stocks). Along with the FF3 model, we also use an extended four-factor

model (FF4) of Carhart (1997) by including a momentum factor (UMD) suggested by

Jegadeesh & Titman (1993).

[Table 10 about here.]

Table 10 reports the coefficient estimates of CAPM, FF3, and FF4 time-series

regressions for monthly excess returns on five portfolios sorted by IV convexity and its

systematic and idiosyncratic components. The left-most six columns are the results

using a portfolio sorted by IV convexity. When running regressions using CAPM, FF3,

and FF4, we generally observe strictly positive intercepts, which are statistically

significant and the quintile portfolio returns show negative patterns when they are

formed by IV convexity. In addition, the differences in the intercept between the lowest

and highest IV convexity are 0.0132 (t-statistic of 7.72) for CAPM, 0.0134 (t-statistic of

7.75) for FF3, and 0.0136 (t-statistic of 7.61) for FF4. Adopting Gibbons, Ross &

Shanken (1989), we test the null hypothesis that all estimated intercepts are

simultaneously zero. We find that the null hypothesis is rejected with a p-value less than

0.001 in the CAPM, FF3, and FF4 model specifications. These results imply that the

widely-accepted existing factors (Rm −Rf , SMB, HML, UMD) cannot fully capture and

explain the negative portfolio return patterns sorted by IV convexity. Thus, we confirm

that IV convexity can capture the cross-sectional variations in equity returns not

explained by existing models such as CAPM, FF3, and FF4.

When we conduct time-series test using the portfolios sorted by decomposed

components of IV convexity into convexitysys and convexityidio, most of the estimated

intercepts are significantly positive in general. The joint test to examine whether the

model explains the average portfolio returns sorted by each component of IV convexity

show that the null hypothesis of zero intercepts from Q1 to Q5 is strongly rejected with

a p-value less than 0.001 in the CAPM, FF3, and FF4 for both systematic and

idiosyncratic components of IV convexlty. Therefore, regardless of whether IV convexity

22

Figure 4: Monthly returns formed by IV convexity with different forecasting horizons

This figure shows the monthly average returns and risk-adjusted returns (implied by Fama-

French 3 and 4 factor models) of the long-short IV convexity portfolios for various forecasting

horizons. “Q1-Q5” plots the average monthly returns of the long short IV convexity portfolio

during Jan 2000 to Dec 2013, whereas αFF3 and αFF4 plot the risk-adjusted (implied by Fama-

French 3 and 4 factor models) monthly returns of the long-short IV convexity portfolios for the

same period. The 95% and 99% confidence intervals are reported in each panel.

2 4 6 8 10 12−0.4

−0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6Q1−Q5

Mon

thly

Por

tfolio

Ret

urn

(in p

erce

nt)

2 4 6 8 10 12−0.4

−0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

αFF3

Forecasting Horizon (in months)

2 4 6 8 10 12−0.4

−0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

αFF4

99% Confidence Interval95% Confidence Interval

is invoked by the market (systematic) or by idiosyncratic risk, none of the components

can be explained by existing standard equity risk factors. These results provide strong

evidence supporting our Hypothesis.

We next examine how long IV convexity effect persists and whether this IV convexity

effect caused by slow information transmission between options market and stock market

disappears as the forecasting horizon increases by investigating the long-short arbitrage

strategy based on IV convexity portfolios. Figure 4 plots the average monthly returns and

the risk-adjusted returns implied by Fama-French 3 and 4 factor models of the long-short

IV convexity portfolios for various forecasting horizons along with their 95% and 99%

confidence intervals. We observe that the average monthly returns of Q1-Q5 portfolio

and the risk-adjusted returns implied by Fama-French 3 and 4 factor models (αFF3 and

αFF4) dramatically decrease (from 1.134 to 0.0031 for Q1-Q5, 0.018 to 0.0025 for αFF3, and

0.012 to 0.0026 for αFF4) during the first two months after the portfolio formation time.

Thereafter, the trading strategy based on IV convexity does not generate economically

meaningful profits. The wide confidence intervals indicate that there is quite little chance

to get positive profits based on the IV convexity information in a long run. Our finding

implies that the arbitrage profits based on the IV convexity information can be realized

in the first few months only, because the arbitrage opportunity from the inter-market

information asymmetry disappears as the forecasting horizon increases.

23

4.2. Fama-MacBeth Regression

The time-series test results indicate that the existing factor models may not be able to

perfectly capture the return predictability of IV convexity. To test if IV convexity can

predict stock returns, we conduct Fama & MacBeth (1973) cross-sectional regressions at

the firm level to investigate whether IV convexity has sufficient explanatory power beyond

others suggested in previous literature. Specifically, we consider Market β estimated by

Fama & French (1992), size (ln mv), book-to-market (btm), momentum (MOM), reversal

(REV), illiquidity (ILLIQ), option-implied volatility skew (IV slope), idiosyncratic risk

(idio risk), implied volatility level (IV level), systematic volatility (v2sys), and idiosyncratic

implied variance (v2idio) as common measures of risks that explain stock returns.18 We run

the monthly cross-sectional regression of individual stock returns of the subsequent month

on IV convexity and other control variables as above.

[Table 11 about here.]

Table 11 reports the averages of the monthly Fama & MacBeth (1973) cross-sectional

regression coefficient estimates for individual stock returns with Market β and other widely

accepted risk factors as a control variable along with the Newey & West (1987) adjusted t-

statistics for the time-series average of coefficients with a lag of 3. The column of Model 1

shows the results with Market β and other stock fundamentals including firm-size (ln mv)

and book-to-market ratio (btm) as control variables. We observe that the coefficient on

IV convexity is significantly negative, and this result confirms our previous finding in the

portfolio formation approach. When we include both IV convexity and IV slope, as shown

in Model 2, the coefficient on IV convexity is still significantly negative, indicating that

IV convexity has a strong explanatory power for stock returns that IV slope cannot fully

capture. The significantly negative coefficients on log(MV) confirm the existence of size

effects shown in earlier studies, whereas the coefficients on btm are significantly positive,

supporting the existence of a value premium.

Models 3 and 4 represent the result using Market β, ln mv, btm, MOM, REV,

ILLIQ, and idiosyncratic risk. These variables are widely accepted stock characteristics

that can capture the cross-sectional variation in stock returns. However, the result is

surprising in that the coefficients on Market β are insignificant, while ln mv and btm

18We do not include the co-skewness factor in the specification of Fama & MacBeth (1973) regression.Harvey & Siddique (2000) argue that co-skewness is related to the momentum effect, as the low momentumportfolio returns tend to have higher skewness than high momentum portfolio returns. Thus, we excludeco-skewness from the Fama-MacBeth regression specification to avoid the multi-collinearity problem withthe momentum factor.

24

have significantly negative and positive coefficients, respectively. The estimated

coefficients on MOM and ILLIQ lose their statistical significance, whereas REV has

significantly negative coefficients. Moreover, the estimated coefficients on idiosyncratic

risk (idio risk) suggested by Ang, Hodrick, Xing & Zhang (2006) are significantly

negative. In an ideal asset pricing model that fully captures the cross-sectional variation

in stock return, idiosyncratic risk should not be significantly priced. Fu (2009) finds a

significantly positive relationship between idiosyncratic risk and stock returns, and Bali

& Cakici (2008) show no significant negative relationship, but insignificant positive

relationships when they form equal-weighted portfolios. However, the statistical

significance of the estimated coefficients on the idiosyncratic risk in Model 3 to Model 4

imply that idiosyncratic risk is negatively priced in the presence of other control

variables. Note that IV convexity has a significantly negative coefficient in the presence

of other control variables including idiosyncratic risk in Model 3. We conjecture that IV

convexity explains the cross-sectional variation in returns that cannot be fully explained

by Market β, ln mv, btm, MOM, REV, ILLIQ or idiosyncratic risk. The statistical

significance of IV convexity remains, even after including IV slope in Model 4.

When alternative ex-ante volatility measures such as IV level, systematic volatility

(v2sys), and idiosyncratic implied variance (v2

idio), are included, as in Models 5-8, the sign

and significance for the IV convexity coefficients remain unchanged. This observation

confirms the negative relationship between IV convexity and future stock returns. All

in all, it can be inferred that there is no evidence that existing risk factors and firm

characteristics suggested by prior research can explain the negative return patterns in

IV convexity, and IV convexity captures the cross-sectional variations in the future stock

returns not explained by existing models.

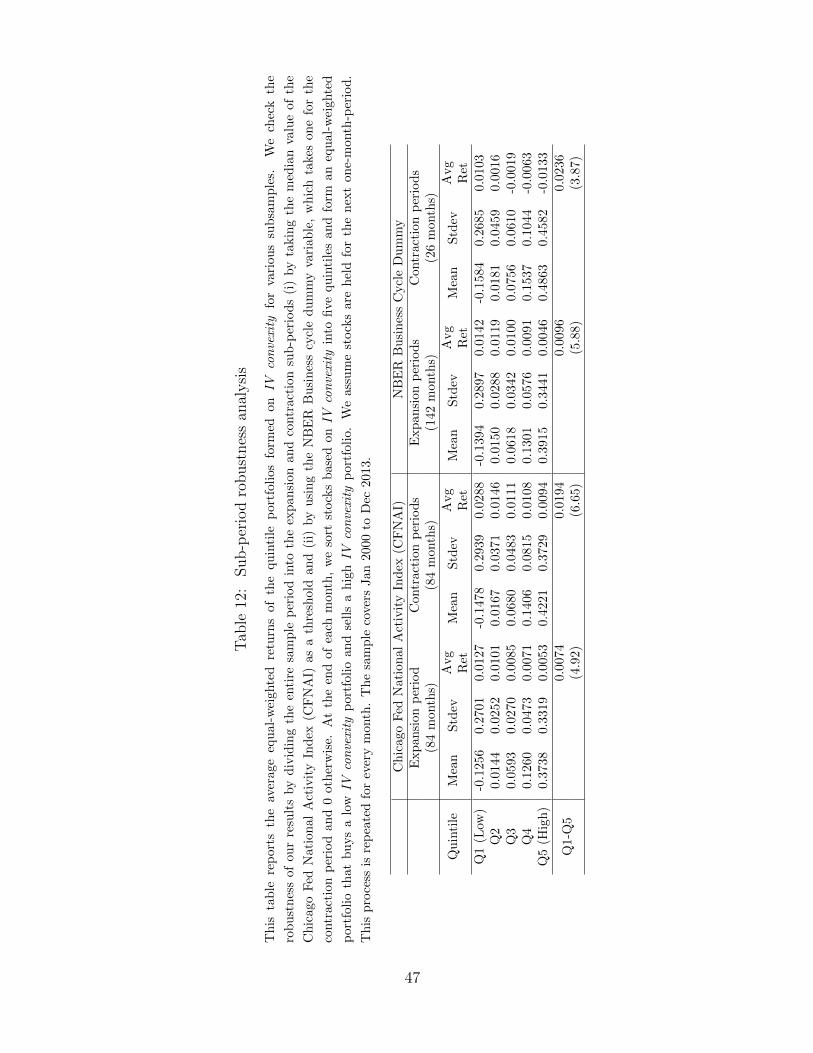

4.3. Sub-period Analysis

We further examine whether the predictive power of IV convexity depends on the state of

the economic condition. For this purpose, we classify states of the economy based on the

Chicago FED National Activity Index (CFNAI) and the National Bureau of Economic

Research (NBER) recession dummy variable.

[Table 12 about here.]

Table 12 shows the average monthly returns of the Q1-Q5 portfolios sorted by IV

convexity based on the CFIAN and the NBER recession dummy, respectively. In the left

25

panel, we divide the entire sample period into the expansion and contraction periods by

taking the median value of the CFNAI as the threshold level. As shown, the decreasing

patterns of the portfolio returns sorted by IV convexity are consistently observed in

both periods. Furthermore, we find that the Q1-Q5 zero-cost portfolio formed on IV

convexity earns significantly positive return in each sub-period. Interestingly, the values

of average portfolio returns of each quintile in the contraction period are higher than

those in the expansion period. The return of zero-investment IV convexity portfolios

(Q1-Q5) is 0.0074 with the t-statistics of 4.92 for the expansion period, whereas the

return becomes 0.0194 with the t-statistics of 6.65 for the contraction period. Overall,

the trading strategy based on IV convexity seemingly earns more pay-off in the

contraction period than in expansion period, as investors tend to overreact to bad news

and the inter-market information asymmetry exacerbates in the recession state.

In the right panel, we take the NBER business cycle dummy variable to classify

the entire period into the expansion and contraction periods. Specifically, the NBER

recession dummy variable takes the value of one if the U.S. economy is in recession as

determined by the NBER, and vice versa. It is notable that similar results are observed,

as both sub-periods show the decreasing patterns in IV convexity portfolios along with

strictly positive returns in zero-cost portfolios with statistical significance. The decreasing

patterns in the IV convexity portfolios are more pronounced in the contraction period than

those in expansion periods, and the magnitude of the zero-investment (Q1-Q5) portfolio

return in the contraction period is larger than that in the expansion period.

5. Conclusion

This study finds empirical evidence that IV convexity, our proposed measure for the

convexity of an option-implied volatility curve, has a negative predictive relationship

with the cross-section of future stock returns, even after controlling for the slope of an

option-implied volatility curve discussed in recent literature. We demonstrate that the

IV convexity measure, as a proxy of both the volatility of stochastic volatility and the

volatility of stock jump size, reflects informed options traders’ anticipation of the excess

tail-risk contribution to the perceived variance of the underlying equity returns.

Consistent with earlier studies, our empirical findings indicate that options traders

have an information advantage over stock traders in that informed traders anticipating

heavier tail risk proactively choose the options market to capitalize on their private

information. The average portfolio returns sorted by IV convexity monotonically

26

decrease from the lowest (Q1) to highest (Q5) IV convexity quintile portfolios on a

monthly basis, implying that the average monthly return on the arbitrage portfolio

buying Q1 and selling Q5 is significantly positive. This pattern persists after

decomposing IV convexity into systematic and idiosyncratic components. In addition,

the negative relationship between IV convexity and future stock returns is robust after