Member State Competitiveness, performance and policies: reinforcing competitiveness

McKinsey Global Institute

A sector view on competitiveness

Dr. Jan Mischke

October 23, 2013

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

OECDWorkshop “Understanding productivity growth”

McKinsey & Company | 1

Contents

▪ The (non-) importance of sector mix

▪ A sector view on competitiveness

McKinsey & Company | 2

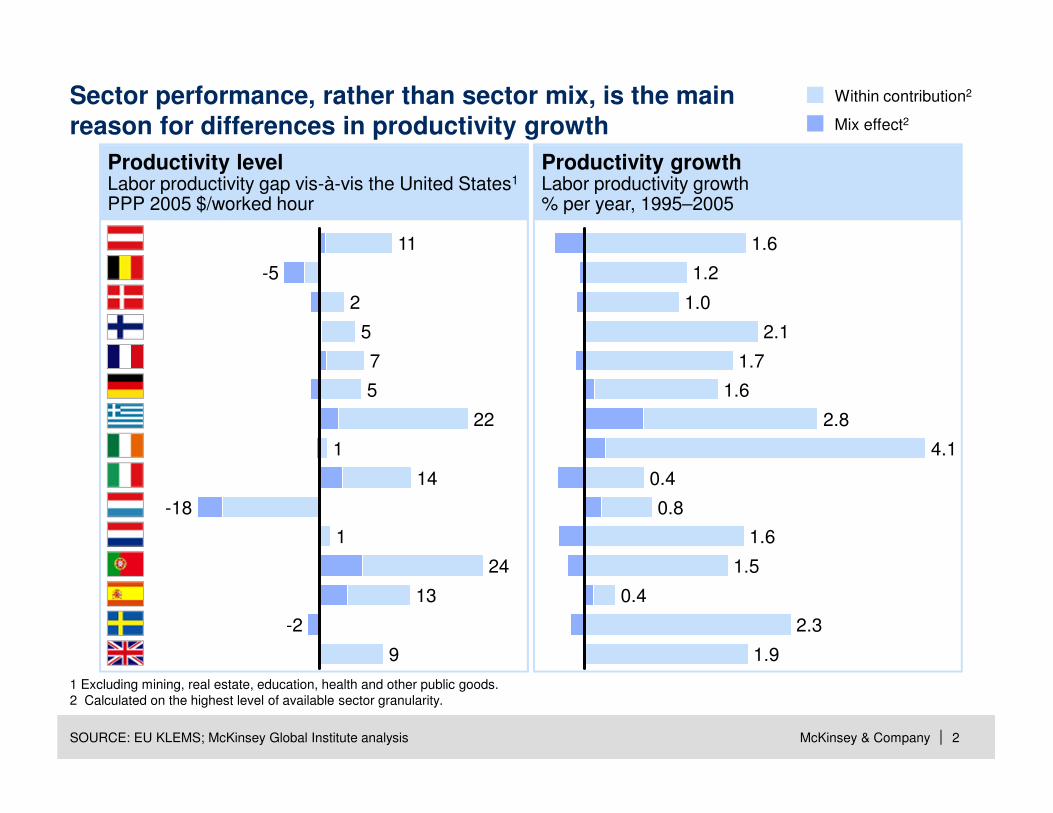

Sector performance, rather than sector mix, is the main reason for differences in productivity growth

Productivity growthLabor productivity growth% per year, 1995–2005

Productivity levelLabor productivity gap vis-à-vis the United States1

PPP 2005 $/worked hour

SOURCE: EU KLEMS; McKinsey Global Institute analysis

1.6

1.9

2.3

0.4

1.5

1.6

0.8

0.4

4.1

2.8

1.6

1.7

2.1

1.0

1.2

1 Excluding mining, real estate, education, health and other public goods.2 Calculated on the highest level of available sector granularity.

Mix effect2

Within contribution2

9

-2

13

24

1

-18

14

1

22

5

7

5

2

-5

11

McKinsey & Company | 4

Contents

▪ The (non-) importance of sector mix

▪ A sector view on competitiveness

– Manufacturing

– Tradable services

– Domestic services

– Public sector

McKinsey & Company | 5

0

5

10

15

20

25

30

35

40

Manufacturing employment% of total employment

10,000 20,0000 30,000 40,000

GDP per capita2012 PPP-adjusted EKS dollars

50,000

Manufacturing employment is not a meaningful indicator for competitiveness, as it follows an inverted-U pattern

Germany

United States

SwedenTaiwan

United KingdomMexico

India South Korea

Japan

SOURCE: Total Economy Database, The Conference Board

McKinsey & Company | 6

8

10

12

14

16

18

20

22

24

UK

Sweden

Germany

France

200720051995 2000

USA

Among advanced economies, Germany and Sweden maintained a comparatively high share of manufacturing

SOURCE: OECD; Eurostat (for Latvia and Lithuania); McKinsey Global Institute analysis

Manufacturing share of GDP%

McKinsey & Company | 7

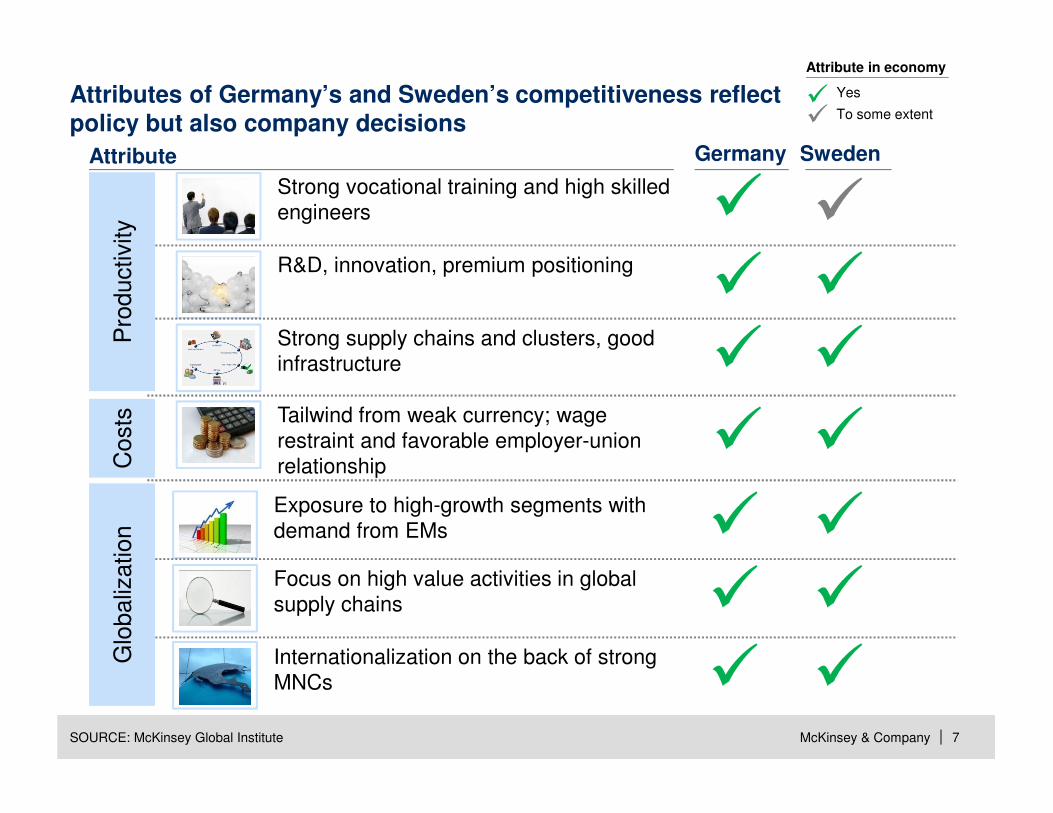

Attributes of Germany’s and Sweden’s competitiveness reflectpolicy but also company decisions

SOURCE: McKinsey Global Institute

Tailwind from weak currency; wage restraint and favorable employer-union relationship

Focus on high value activities in global supply chains

Internationalization on the back of strong MNCs

Strong vocational training and high skilled engineers

R&D, innovation, premium positioning

Exposure to high-growth segments with demand from EMs

Attribute SwedenGermany

Attribute in economy

Yes

To some extent

Strong supply chains and clusters, good infrastructure

Pro

ductivity

Costs

Glo

baliz

ation

McKinsey & Company | 8

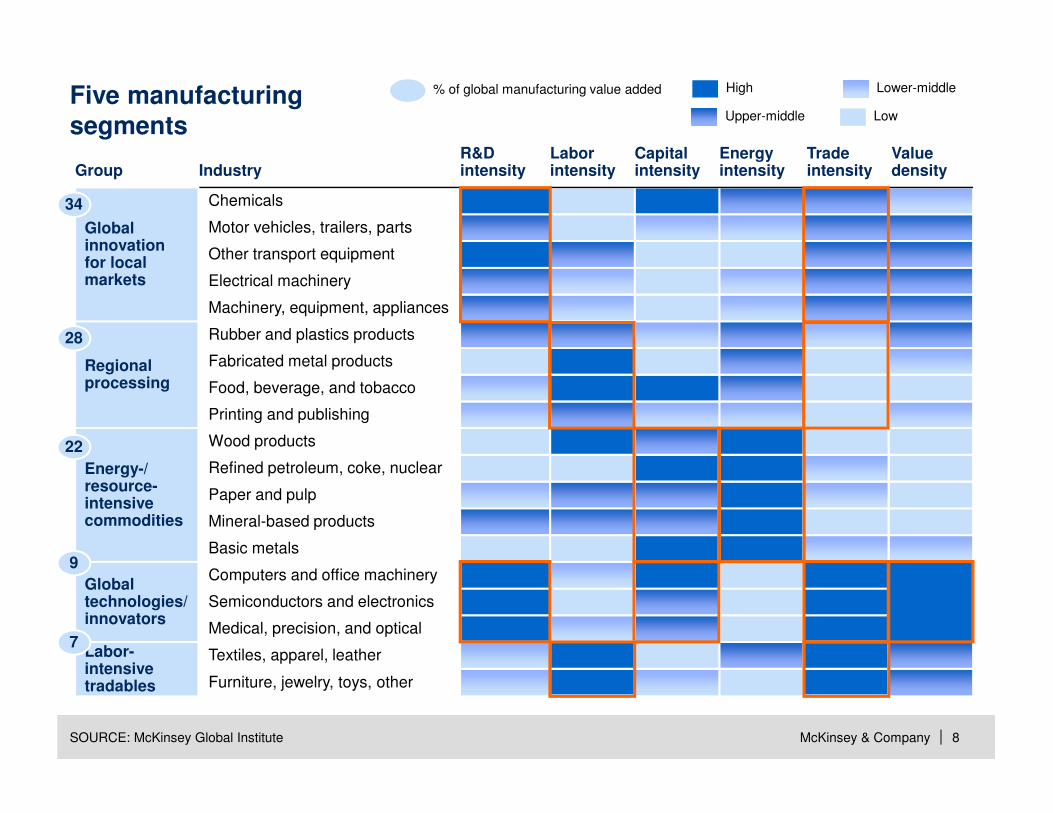

Furniture, jewelry, toys, other

Textiles, apparel, leather

Medical, precision, and optical

Semiconductors and electronics

Computers and office machinery

Basic metals

Mineral-based products

Paper and pulp

Refined petroleum, coke, nuclear

Wood products

Printing and publishing

Food, beverage, and tobacco

Fabricated metal products

Rubber and plastics products

Machinery, equipment, appliances

Electrical machinery

Other transport equipment

Motor vehicles, trailers, parts

Chemicals

Five manufacturingsegments

High

Upper-middle

Lower-middle

Low

% of global manufacturing value added

GroupValue density

Trade intensity

Energy intensity

Capital intensity

Labor intensity

R&D intensityIndustry

Labor-intensive tradables

Global technologies/ innovators

Energy-/ resource-intensive commodities

Regional processing

Global innovation for local markets

7

9

22

28

34

SOURCE: McKinsey Global Institute

McKinsey & Company | 9

Different trade regional patterns exemplified by Southern European strength in labor-intensive tradables vs. Continental European strength in Global innovation for local markets

Global technologies/innovators

-3

Energy- and resource-intensive commodities

22

Regional processing -4

Global innovationfor local markets

15

Labor-intensivetradables

-1

Net exports, 2011EUR billion

Nordics1 Southern2 Continental3 UK & Ireland 12 NMS4

5

22

-13

-10

-9

-36

-2

28

59

280

3

-4

-5

-5

19

-24

-20

30

-8

-34

SOURCE: Eurostat

1 Sweden, Finland, Denmark; 2 Greece, Spain, Italy, Portugal, 3 Germany, Austria, Luxemburg, Belgium, France, Netherlands; 4 Poland, Czech Republic, Cyprus, Latvia, Lithuania, Slovenia, Slovakia, Estonia,

Hungary, Malta, Bulgaria, Romania

McKinsey & Company | 10

Contents

▪ The (non-) importance of sector mix

▪ A sector view on competitiveness

– Manufacturing

– Tradable services

– Domestic services

– Public sector

McKinsey & Company | 11

Mature economies run large and increasing trade surpluses in business and financial services

SOURCE: OECD; McKinsey Global Institute analysis

-0.15

-0.10

-0.05

0

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Other services

Travel

Transportation

Royalties and license fees1

Business services

Financial services

2008042000971994

1 Significantly influenced by tax optimization strategies.

% of GDP; nominal

Service net exports of mature economies

McKinsey & Company | 12

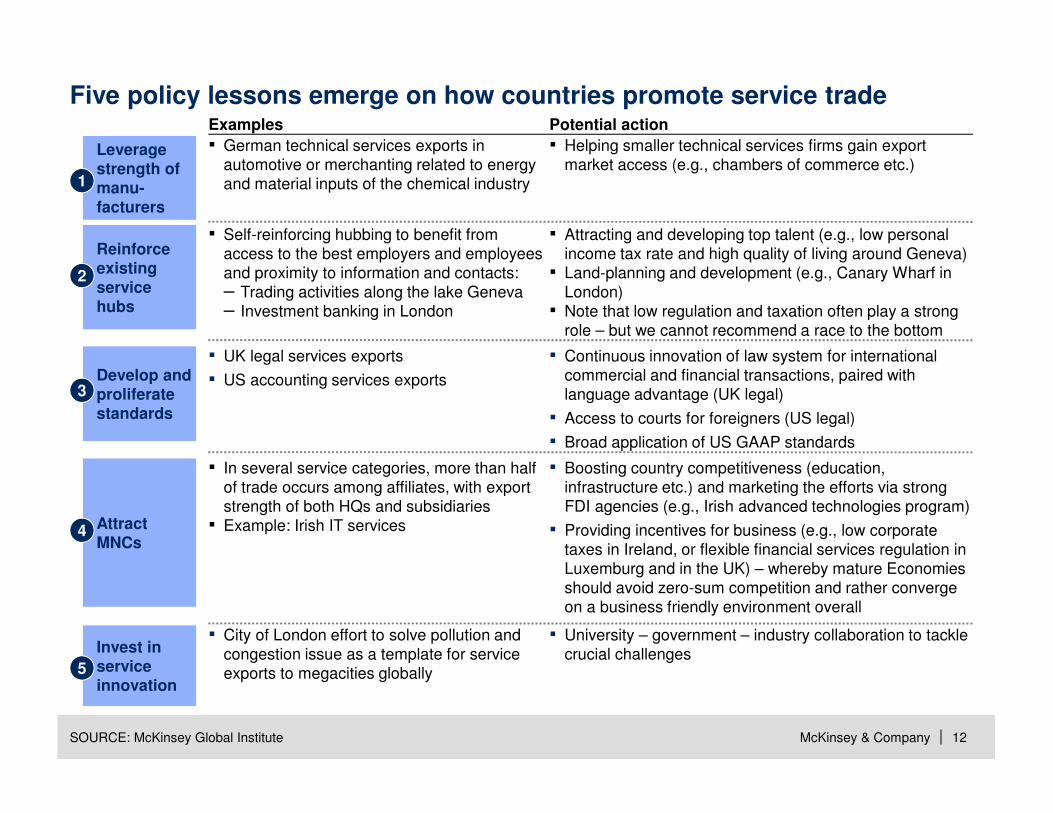

Five policy lessons emerge on how countries promote service trade

▪ German technical services exports in automotive or merchanting related to energy and material inputs of the chemical industry

▪ Self-reinforcing hubbing to benefit from access to the best employers and employees and proximity to information and contacts:– Trading activities along the lake Geneva– Investment banking in London

Leverage strength of manu-facturers

1

Reinforce existing service hubs

2

Examples

▪ City of London effort to solve pollution and congestion issue as a template for service exports to megacities globally

Invest in service innovation

5

▪ UK legal services exports

▪ US accounting services exportsDevelop and proliferate standards

3

▪ In several service categories, more than half of trade occurs among affiliates, with export strength of both HQs and subsidiaries

▪ Example: Irish IT servicesAttract MNCs

4

▪ Helping smaller technical services firms gain export market access (e.g., chambers of commerce etc.)

▪ Attracting and developing top talent (e.g., low personal income tax rate and high quality of living around Geneva)

▪ Land-planning and development (e.g., Canary Wharf in London)

▪ Note that low regulation and taxation often play a strong role – but we cannot recommend a race to the bottom

Potential action

▪ University – government – industry collaboration to tackle crucial challenges

▪ Continuous innovation of law system for international commercial and financial transactions, paired with language advantage (UK legal)

▪ Access to courts for foreigners (US legal)

▪ Broad application of US GAAP standards

▪ Boosting country competitiveness (education, infrastructure etc.) and marketing the efforts via strong FDI agencies (e.g., Irish advanced technologies program)

▪ Providing incentives for business (e.g., low corporate taxes in Ireland, or flexible financial services regulation in Luxemburg and in the UK) – whereby mature Economies should avoid zero-sum competition and rather converge on a business friendly environment overall

SOURCE: McKinsey Global Institute

McKinsey & Company | 13

Contents

▪ The (non-) importance of sector mix

▪ A sector view on competitiveness

– Manufacturing

– Tradable services

– Domestic services

– Public sector

McKinsey & Company | 14SOURCE: McKinsey Global Institute

EXAMPLES

Key barriers for productivity, innovation and growthSector

▪ Product market regulation like restrictions on assortment, opening hours

▪ Advertising restrictions and price fixes for pharmacies

▪ Land market regulation

▪ Labour regulation

Retail

▪ Setup of (public) (pre-)procurement hindering innovation

▪ Informalities and fragmentation

▪ Lack of standardization and pre-fabrication

Construction

▪ Price fixes for lawyers, accountants, notariesProfessional services

▪ Postal services monopolies or dominant incumbents

▪ Passenger rail monopolies or dominant incumbentsNetwork industries

Competitiveness and productivity of domestic service sectors often constrained by regulatory barriers

McKinsey & Company | 15

Key changes Impact

Sweden achieved high productivity growth in retail after comprehensive reforms

Factors explaining productivity development

Eased zoning laws

▪ Influence of municipalities on store type decisions was reduced

Shiftingindustrystructure

▪ Growth of large-scale store formats and shopping centers, triggered by zoning changes

▪ Trend to integrated chains like IKEA or H&M, creating scale advantages in purchasing, supply chain, store management, and marketing

▪ Growth of private label products has increased margins as retailers capture larger part of the value chain

Increasedcompetition

▪ Continued growth of ‘category killers’ (specialized chains) who put scale pressures on existing stores

▪ Increased share of highly productive formats, e.g., discounters

▪ New market entrants, e.g., discounters▪ New channels like internet shopping

Advanced IT usage

▪ Use of ICT has significantly improved supply chain and allowed for improved assortment and inventory management

5

2

3

SwedenEUUS

SOURCE: EU KLEMS, McKinsey Global Institute; team analysis

Productivity levelIndex: 100 = US 2005

Productivity growthCAGR 1995-2005 (%)

RETAIL EXAMPLE

75 114100

McKinsey & Company | 16

Contents

▪ The (non-) importance of sector mix

▪ A sector view on competitiveness

– Manufacturing

– Tradable services

– Domestic services

– Public sector

McKinsey & Company | 17

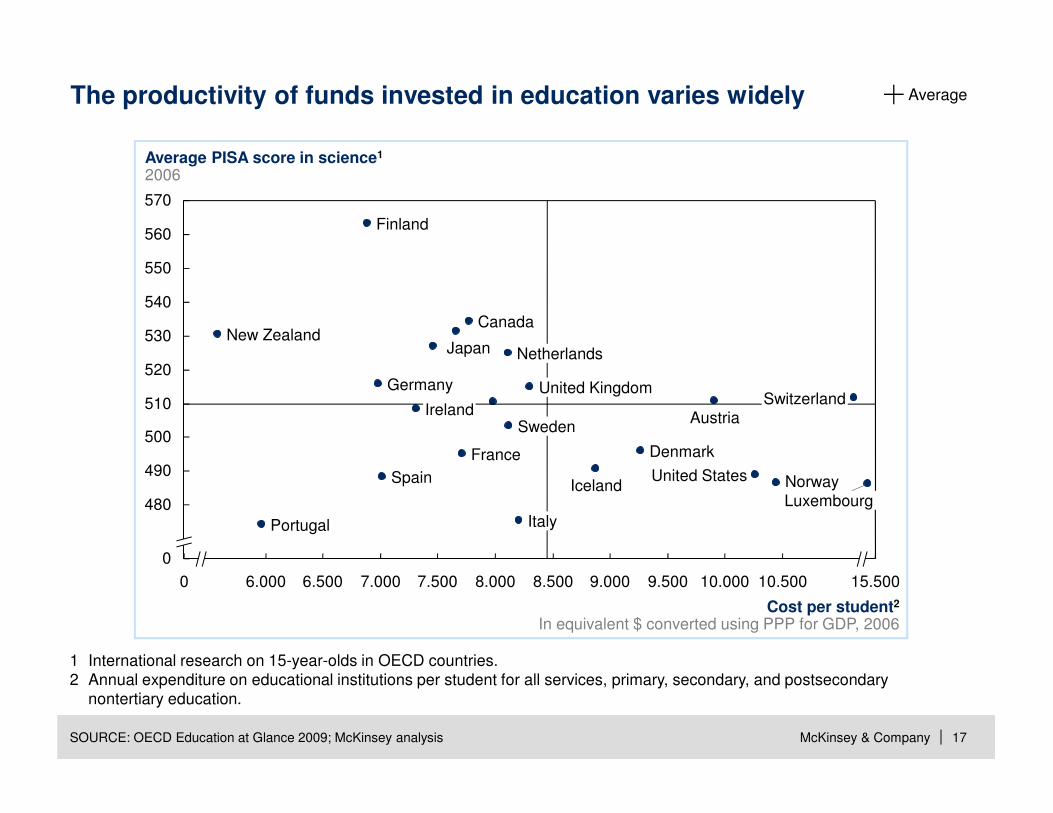

The productivity of funds invested in education varies widely

510

500

490

Average PISA score in science1

2006

0

Cost per student2

In equivalent $ converted using PPP for GDP, 2006

15.50010.50010.0009.500

570

560

550

480

540

530

9.0008.5008.0007.5007.0006.5006.0000

United States

United KingdomSwitzerland

Sweden

Spain

Portugal

Norway

New ZealandNetherlands

Luxembourg

Japan

Italy

Ireland

Iceland

Germany

France

520

Finland

Denmark

Canada

Austria

1 International research on 15-year-olds in OECD countries.2 Annual expenditure on educational institutions per student for all services, primary, secondary, and postsecondary

nontertiary education.

Average

SOURCE: OECD Education at Glance 2009; McKinsey analysis

McKinsey & Company | 18

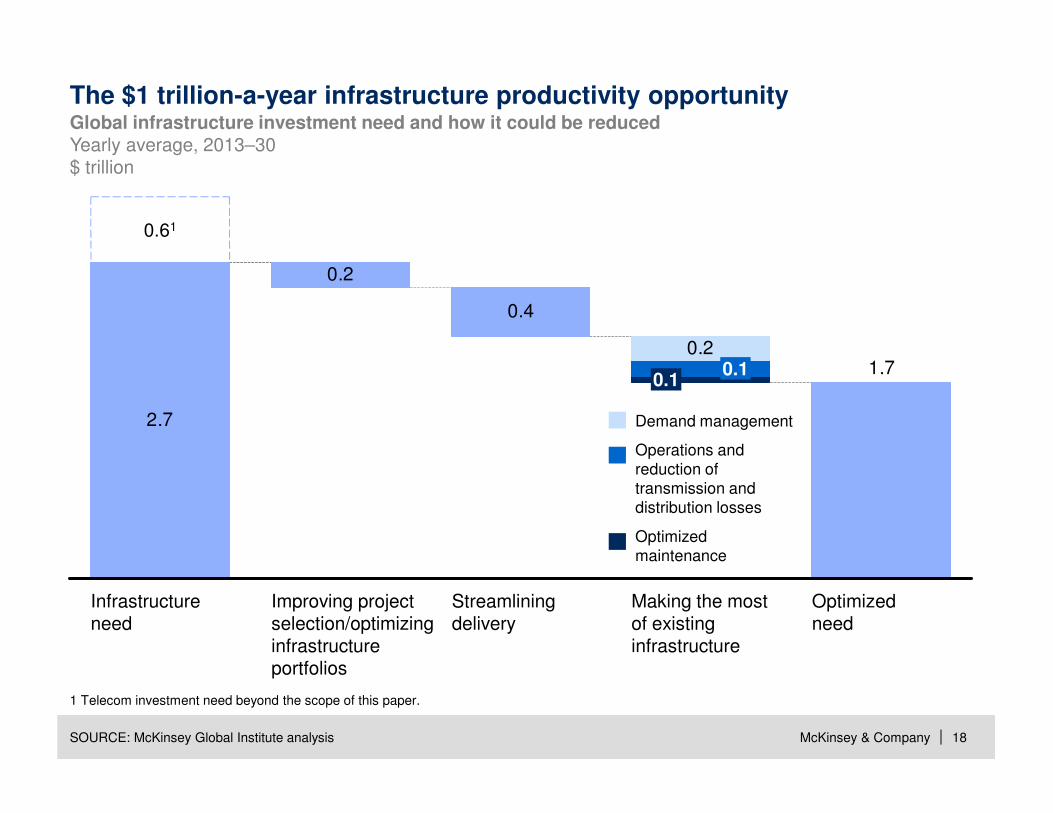

2.7

0.2

0.4

1.70.2

Optimizedneed

Making the most of existing infrastructure

0.10.1

Streamliningdelivery

Improving project selection/optimizing infrastructure portfolios

Infrastructureneed

0.61

Global infrastructure investment need and how it could be reducedYearly average, 2013–30$ trillion

The $1 trillion-a-year infrastructure productivity opportunity

SOURCE: McKinsey Global Institute analysis

1 Telecom investment need beyond the scope of this paper.

Demand management

Operations and reduction of transmission and distribution losses

Optimized maintenance