A robust and sustainableA robust and sustainable business model

21

A robust and sustainable A robust and sustainable business model 13 December 2013 Rodney Alfvén Head of Investor Relations Rodney Alfvén, Head of Investor Relations

Transcript of A robust and sustainableA robust and sustainable business model

A robust and sustainableA robust and sustainable business model13 December 2013Rodney Alfvén Head of Investor RelationsRodney Alfvén, Head of Investor Relations

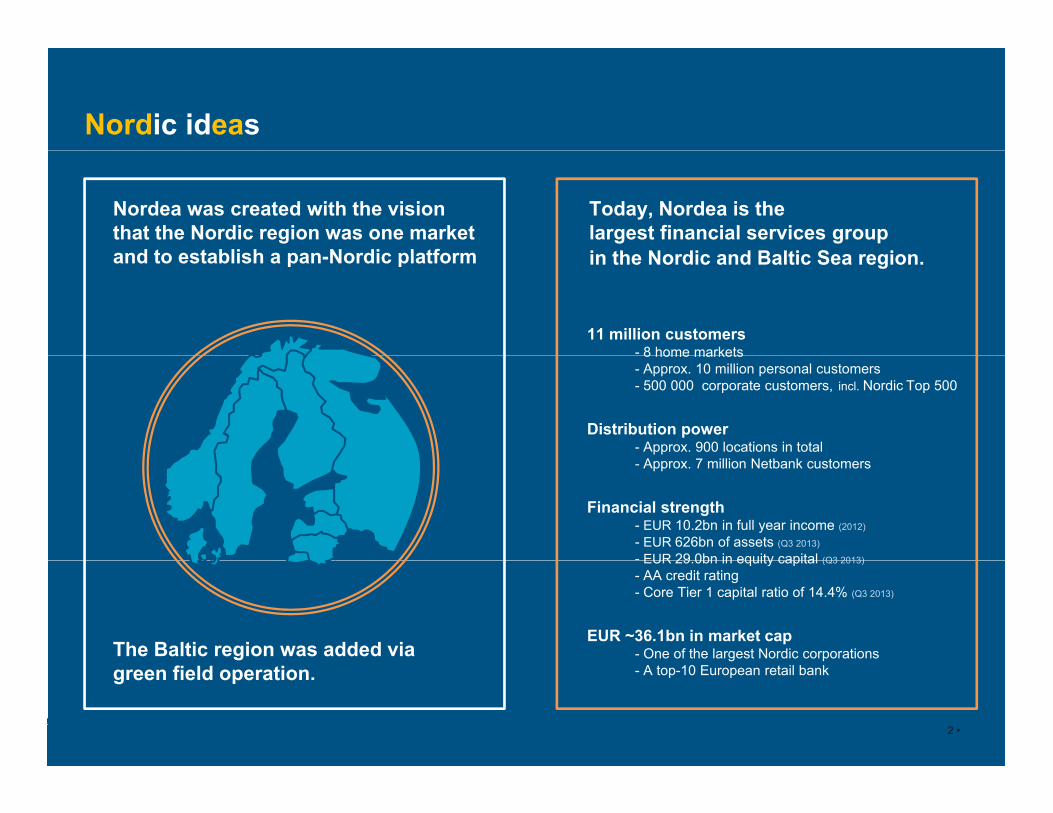

Nordic ideas

Nordea was created with the vision that the Nordic region was one market and to establish a pan Nordic platform

Today, Nordea is the largest financial services group i th N di d B lti S i

11 million customers- 8 home markets

and to establish a pan-Nordic platform in the Nordic and Baltic Sea region.

8 home markets- Approx. 10 million personal customers- 500 000 corporate customers, incl. Nordic Top 500

Distribution power- Approx. 900 locations in total- Approx. 7 million Netbank customers

Financial strength- EUR 10.2bn in full year income (2012)

- EUR 626bn of assets (Q3 2013)

- EUR 29 0bn in equity capital (Q3 2013)EUR 29.0bn in equity capital (Q3 2013)

- AA credit rating- Core Tier 1 capital ratio of 14.4% (Q3 2013)

EUR ~36.1bn in market cap- One of the largest Nordic corporationsThe Baltic region was added via - A top-10 European retail bankgreen field operation.

2 •

Nordea is the most diversified Nordic bank…

Russia 1%

Largest market contributionTotal loans to public by geography, %Geographic exposure vs. Nordic peers¹, %

~70% ~70%

~80%

~90%

Norway 17%

Baltics 2%Russia 1%

29%

~60%71% Finland 29%

Denmark 25%29%

Sweden26%

25%

Nordea Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

Total: EUR 343bn

1 Comparison based on reported geographical breakdown of loans to the public; latest available financials.

3 •

…with lower earnings volatility and stable ROE over the cycle

61

147Net income volatility vs. Nordic peers1, %

11 13 2454 61

Nordea Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

18 021.5

19.118.1

Stable ROE over the cycle Not a single quarter below

8%. Every year above 11%

ROE development 2007-20132, %

18.0 18.115.816.215.014.413.9

12.011.78.1

11.39.5

12.212.812.011.58.5

12.311.912.510.3

12.311.111.510.8

2008 2009 2010 2011 20122007

CT1 = ~13%CT1 = ~6%

2013

1 Annual net income volatility over last 5 years.2 ROE adjusted for restructuring costs 2011.

4 •

Boring is beautifulBoring is beautiful

One offering to all our stakeholders

Massive regulatory

Regulationg y

agenda with many and interlinked metrics

A clear value proposition to all

CustomersInvestorsInvestor support a

prerequisite for proposition to all our customers

prerequisite for contributing to

society

Bank sector contributing to

Society

gsociety

6 •

A clear value proposition to our customersCustomers

Continuous inflow of Gold and Private Banking customers Clear value proposition to relationship customers

Customer’s benefits

2.931

3.0513.112

3.168Trust bank’s

ability…

…holistic advice in best

interest…

…one provider of all

services…

…stability; a bank for

sunny and rainy days

2.423

2.568

2.697

Know the customer

Advise the customer

Service the customer

Commit to the

customer

Focus on the id tif

…service all financial l lt d

customer

Q3/07 Q3/08 Q3/09 Q3/10 Q3/11 Q3/12 Q3/13

Number of Gold and Private Banking customers, m

Focus on the right

customers/ projects…

…identify efficient

solutions…

financial needs/

benefit from diversification

…

…loyalty and higher

profitability

Bank’s benefits

7 •

Superior Corporate and institutions franchiseCustomers

100% Only bank with a substantial lead bank footprint in all Nordea

Nordea top ranked for relationship and quality Multi-local presence

70%

80%

90%

ship

s

y pmarkets

Deep and intimate local presence

Interaction on all levels with many touch points

Nordea

Peer 2Peer 1

40%

50%

60%

porta

nt re

latio

n Interaction on all levels with many touch-points

Coordination of effort in customer teams

Proactivity on all levels

Peer 2

Peer 3

Peer 4

P 5

0%

10%

20%

30%Imp Peer 5

0%(40) (20) 0 20 40 60 80 100

Greenwich Quality Index Large Corporates -Difference from average1

8 1 The Greenwich Quality Index reflects a normalised composition of all quantitative scores.

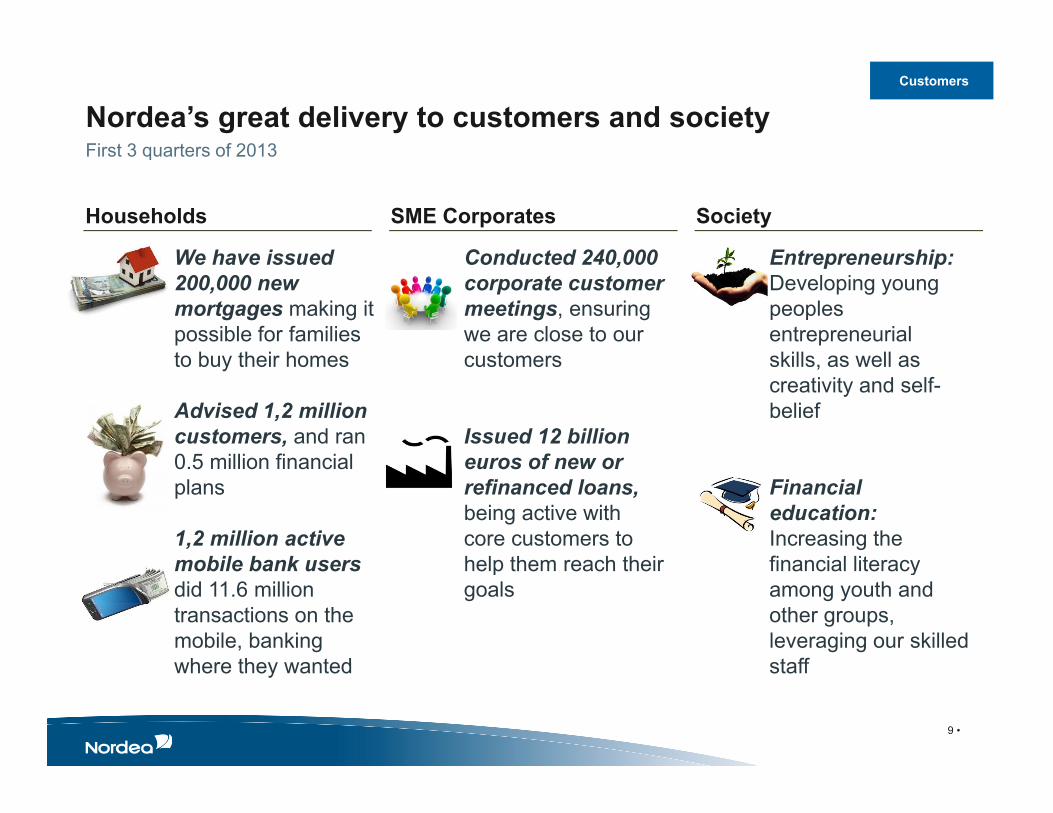

Nordea’s great delivery to customers and societyFirst 3 quarters of 2013

Customers

W h i d

Households

C d t d 240 000

SME Corporates

E t hi

Society

First 3 quarters of 2013

We have issued 200,000 new mortgages making it possible for families t b th i h

Conducted 240,000 corporate customer meetings, ensuring we are close to our

t

Entrepreneurship: Developing young peoples entrepreneurial kill llto buy their homes

Advised 1,2 million customers, and ran 0 5 million financial

customers

Issued 12 billion euros of new or

skills, as well as creativity and self-belief

0.5 million financial plans

1,2 million active mobile bank users

euros of new or refinanced loans, being active with core customers to help them reach their

Financial education: Increasing the financial literacymobile bank users

did 11.6 million transactions on the mobile, banking where they wanted

help them reach their goals

financial literacy among youth and other groups, leveraging our skilled staff

9 •

where they wanted staff

Swedish bank sector contributing to societySociety

Share oftotal corporate tax

Directemployment

DirectContribution to GDP **** p

11%11%p y

85 00085 000 144 144 bnbn ** %%

10 • • Year 2010 ** Incl insurance companies• ** SEK

Source: Bankföreningen

Increased costs of risk… Investors

Beta

Source: UBS 11 •

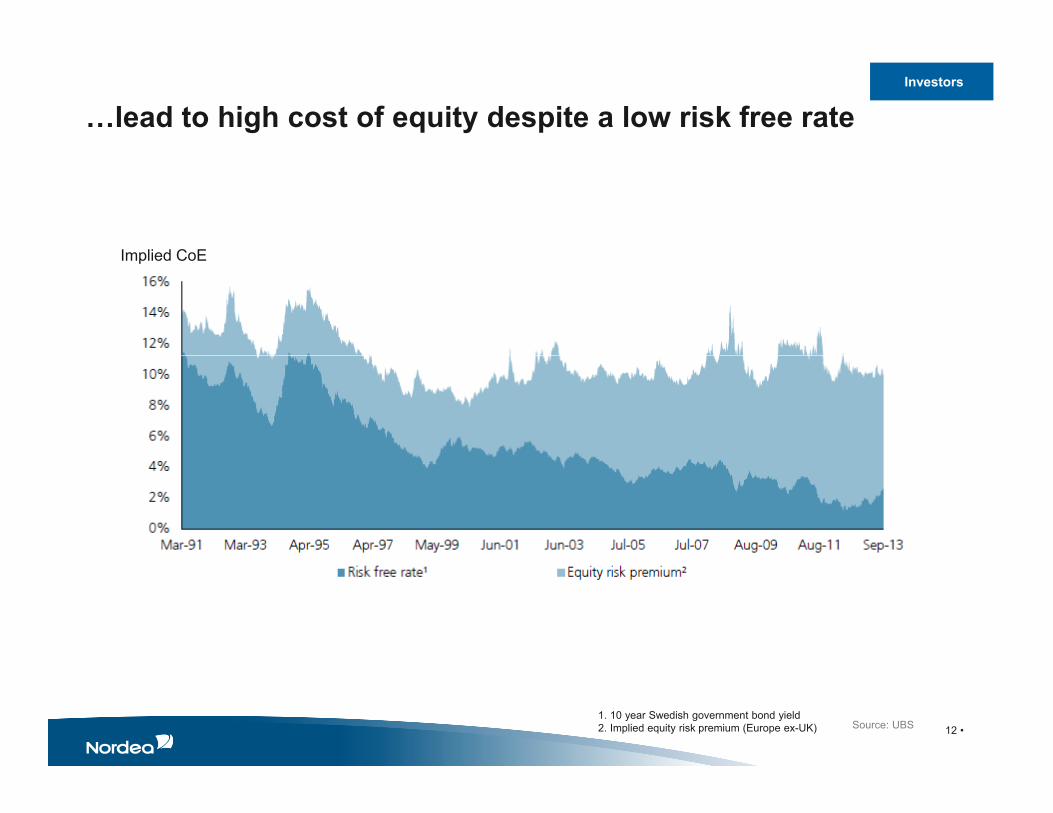

…lead to high cost of equity despite a low risk free rateInvestors

Implied CoEImplied CoE

12 • Source: UBS 1. 10 year Swedish government bond yield2. Implied equity risk premium (Europe ex-UK)

A sound valuation of equity gives positive effect on funding costs and customer offerings

Investors

1.8

2.0

Swedbank

SHB

1.4

1.6

alue

Nordea

SEB

DNB

KBC

1.0

1.2

e to

book

va Nordea DNB

Danske Erste

BBVA

Santander

0.6

0.8Pric

e

BNP

Barclays

Deutsche

Erste

SG

RBS Intesa

U iC dit

0.2

0.4

0 20 40 60 80 100 120 140 160 180 200

CACommerz

UniCredit

13 •

0 20 40 60 80 100 120 140 160 180 200

5 year CDS spread

Efficiency amongst the best in the worldInvestors

Cost / income ratio vs Cost to avg assets

Source: Citi 14 •

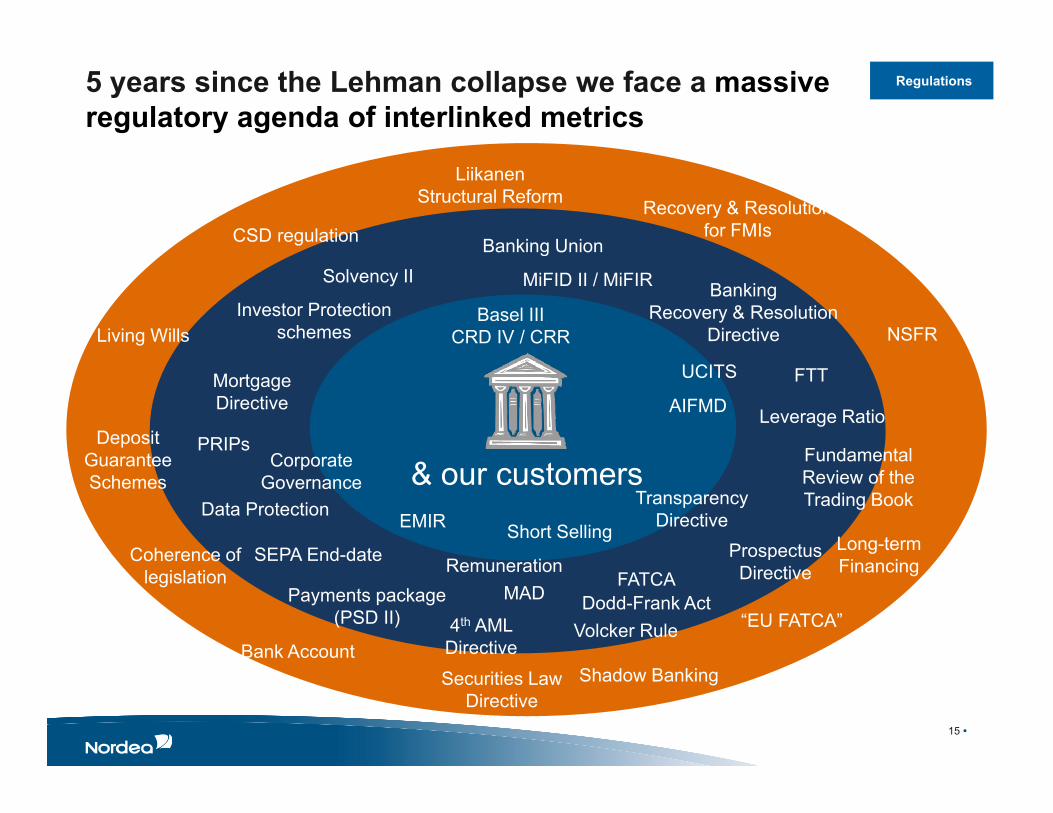

5 years since the Lehman collapse we face a massive regulatory agenda of interlinked metrics

Regulations

Recovery & Resolution for FMIs

LiikanenStructural Reform

CSD regulation Banking Union

Investor Protection schemesLiving Wills

g

MiFID II / MiFIR

Basel IIICRD IV / CRR

BankingRecovery & Resolution

Directive NSFR

Solvency II

PRIPs Deposit Guarantee

Mortgage Directive

FTT

Leverage RatioAIFMD

UCITS

FundamentalCorporate

Long-term Fi i

Data Protection

Guarantee Schemes

Prospectus Coherence of

& our customers

SEPA End-date

EMIR Short Selling

Fundamental Review of the Trading BookTransparency

Directive

CorporateGovernance

R ti

Dodd-Frank Act

FinancingPayments package

(PSD II)Volcker Rule

FATCA Directive Coherence of

legislation

“EU FATCA”4th AML Directive Bank Account

MAD

SEPA End date Remuneration

Securities Law Directive

Shadow Banking

15 •

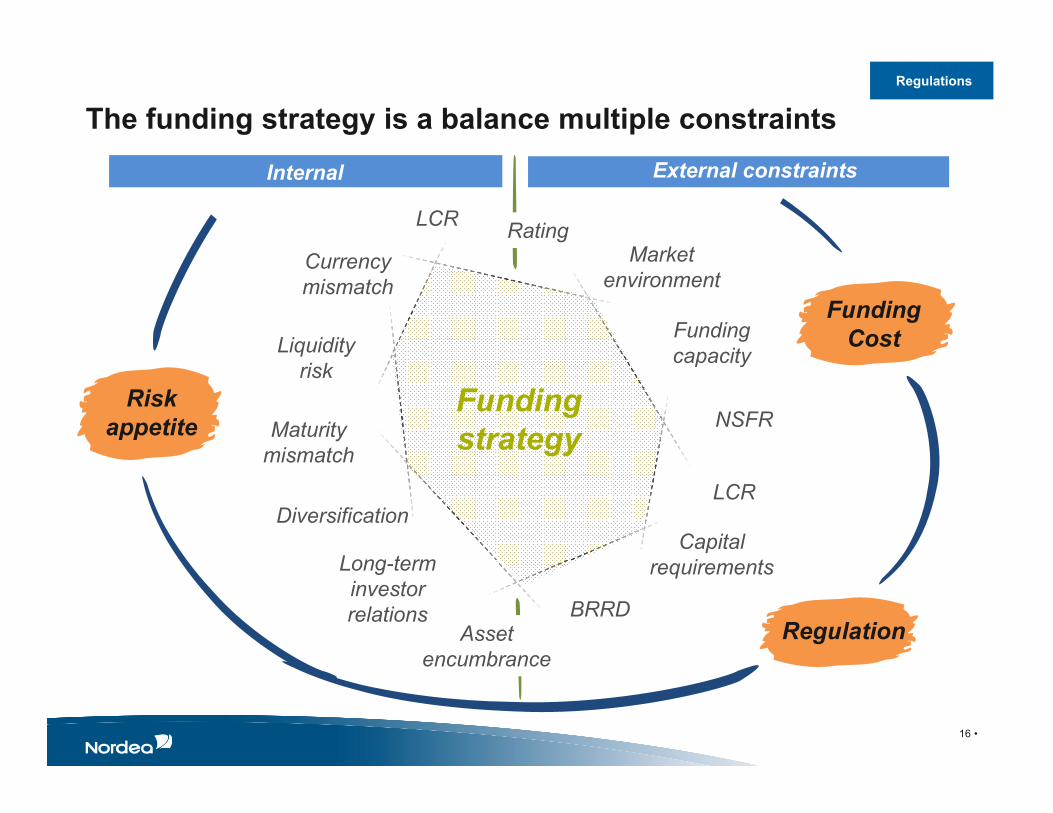

The funding strategy is a balance multiple constraintsRegulations

MarketRatingLCR

Internal constraints

External constraints

Market environment

Funding capacity

Currency mismatch

Liquidity Funding

Cost

Risk appetite

capacity

Maturity mismatch

q yrisk

Funding strategy

NSFR

LCR

Capital i t

mismatch

Long term

Diversification

requirements

Asset encumbrance

BRRDRegulation

Long-term investor relations

16 •

encumbrance

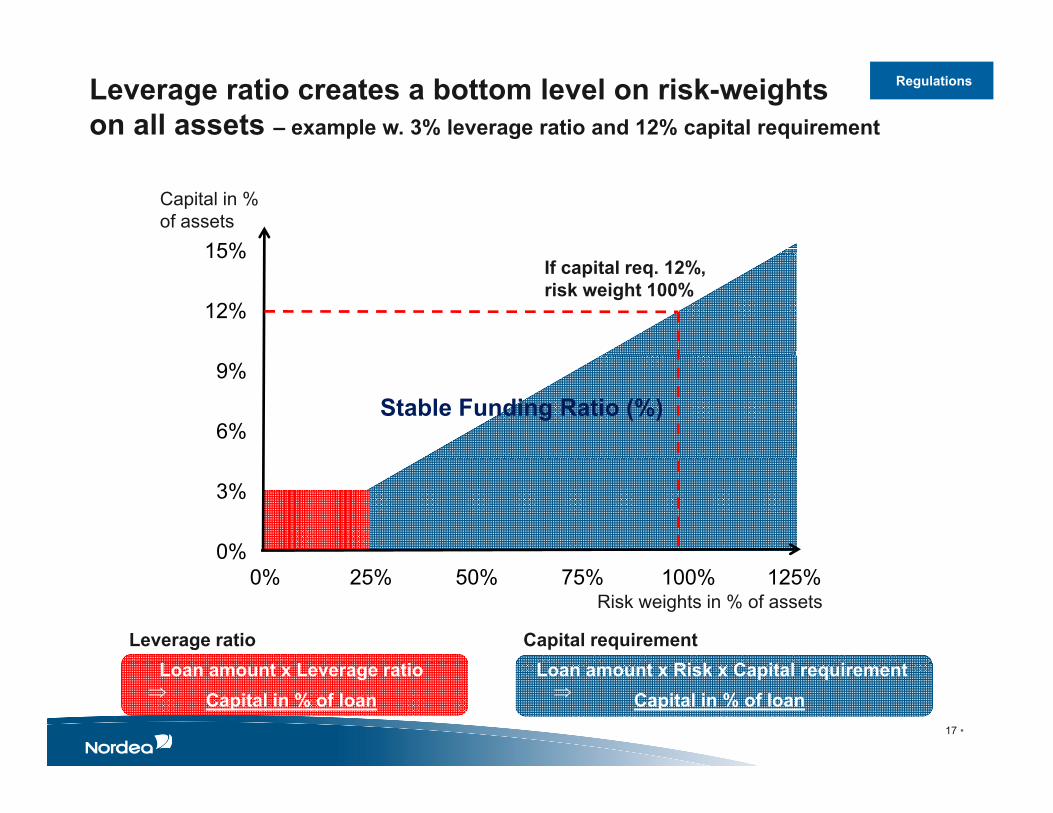

Leverage ratio creates a bottom level on risk-weights on all assets – example w. 3% leverage ratio and 12% capital requirement

Regulations

15%

Capital in % of assets

12%

15%If capital req. 12%,risk weight 100%

6%

9%

Stable Funding Ratio (%)

0%

3%

L Ri k C i l i

0% 25% 50% 75% 100% 125%

L L i

Risk weights in % of assets

Leverage ratio Capital requirementLoan amount x Risk x Capital requirement

Capital in % of loanLoan amount x Leverage ratio

Capital in % of loan

17 •

The Nordic-Baltic regions reliance on wholesale fundingRegulations

• Advance saving markets and good knowledge on the customer side

• High savings ratios – but not in deposits

• Reformed pension systems - less deposits

• But stable and reliable funding through covered bonds instead of deposits –• Liquid markets • Functioned well during the financial crisisFunctioned well during the financial crisis• Domestic markets in Denmark, Finland, Norway and Sweden

18 •

Regulations

Structural liquidity- Stable funding ratio by S&P 12

4

122

119

119

113

113

111

109

107

105

105

101

101

101

99 99 99 98 98 97 96 96 95 95 94 94 93 93 92 92 92 91 91 90 90 89 8 8 6 6 6

100

120

140

9 9 9 8 88 88 86 86 86 84 84 82 79 78 75

70 69

40

60

80

28

0

20

40

/A-1

+/A

-1+

e/A

-1e/

A-1

/A-1

+/A

-1+

e/A

-1e/

A-2

e/A

-2e/

A-1

e/A

-2e/

A-1

ive/

Be/

A-1

e/A

-1e/

A-1

e/A

-1e/

A-2

/A-1

+e/

A-1

e/A

-1N

eg/B

ble/

Be/

A-3

e/A

-2e/

A-1

e/A

-1e/

A-2

e/A

-1e/

A-2

Neg

/Be/

A-2

A-1

+e/

A-1

ive/

B

e/A

-3

e/A

-1

e/A

-1

Neg

/B

e/A

-1

e/A

-1

ive/

B

e/A

-3

ive/

B

/A-1

+

e/A

-2

ive/

B

e/A

-1

ive/

C

e/A

-2

anC

har,

AA

-/Neg

ativ

e/ol

ding

s, A

A-/N

egat

ive/

Ers

te, A

/Neg

ativ

eU

BS

, A/S

tabl

e

oper

ativ

e, A

A-/S

tabl

e/ZK

B, A

AA

/Neg

ativ

e/

RZB

, A/N

egat

ive

mer

zban

k, A

-/Neg

ativ

e

KB

C, A

-/Pos

itive

RB

S, A

/Neg

ativ

e

utsc

he, B

BB

+/N

egat

ive

Nat

ionw

ide,

A/N

egat

ive

AIB

, BB

/Neg

atD

NB

, A+/

Sta

ble

Lloy

ds, A

/Neg

ativ

eB

arcl

ays,

A/S

tabl

e

AB

N A

mro

, A/S

tabl

ent

ande

r, B

BB

/Neg

ativ

e

Rab

oban

k, A

A-/S

tabl

e/IN

G, A

+/N

egat

ive

Sw

edba

nk, A

+/S

tabl

eC

aixa

, BB

-/Wat

ch N

BO

I, B

B+/

Sta

bU

nion

e, B

BB

-/Neg

ativ

e

oban

ca, B

BB

/Neg

ativ

eC

redi

t Sui

sse,

A/S

tabl

e

SE

B, A

+/N

egat

ive

niC

redi

t, B

BB

/Neg

ativ

e

Cre

dit M

utue

l, A

/Sta

ble

Inte

sa, B

BB

/Neg

ativ

e

BC

P, B

/Wat

ch N

Dan

ske,

A-/S

tabl

e

orde

a, A

A-/N

egat

ive/

AS

ocG

en, A

/Neg

ativ

e

Pop

olar

e, B

B/N

egat

BB

VA

, BB

B-/N

egat

ive

BN

P, A

+/N

egat

ive

BP

CE

, A/N

egat

ive

o S

anto

, BB

-/Wat

ch N

DB

, A/S

tabl

e

dit A

gric

ole,

A/N

egat

ive

Sab

adel

l, B

B/N

egat

Cai

xa, B

BB

-/Neg

ativ

e

Ban

kia,

BB

-/Neg

at

bank

en, A

A-/N

egat

ive/

Bel

fius,

A-/N

egat

ive

BP

E, B

B-/N

egat

Nyk

redi

t, A

+/N

egat

ive

NB

G, C

CC

/Neg

ati

Dex

ia, B

BB

/Sta

ble

Sta

HS

BC

Ho

Coo

Com

m

Nor

ddeu N

San R U

Med

io C Un C No

Esp

irito

Cre

d

Han

dels

b

-Source: Standard & Poor’s based on YE 2012-Highlighting in; Green = Above Average; Orange = Average; Red = Below Average

19 •

The value of a common Nordic-Baltic approachRegulations

• The Nordic-Baltic region – One market!

• Good cooperation with the various authorities in the region

• But cooperation and harmonization could be improved – would be beneficial for growth and further developments in the Nordic-Baltic region

• We have well developed and advanced banking markets in the Nordic-Baltic region – in some areas a coordinated approach with the authorities to support the distinctiveness of the Nordic-Baltic region would be welcomed

20 •

A robust and sustainableA robust and sustainable business model13 December 2013Rodney Alfvén Head of Investor RelationsRodney Alfvén, Head of Investor Relations

![Robust Model Predictive Control - Carnegie Mellon …cepac.cheme.cmu.edu/.../Ronust_Control_Classnotes.pdf1 Robust Model Predictive Control Formulations of robust control [1] The robust](https://static.fdocuments.in/doc/165x107/5aab45707f8b9a2b4c8bd345/robust-model-predictive-control-carnegie-mellon-cepacchemecmueduronustcontrol.jpg)