A Refresher Course on Current Financial Reporting...

93

A Refresher Course on Current Financial Reporting Standards 2013 (Day 5) 1 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. HKAS 12 Income Taxes

Transcript of A Refresher Course on Current Financial Reporting...

A Refresher Course on Current Financial Reporting Standards 2013 (Day 5)

1

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

HKAS 12 Income Taxes

COOPERATION REQUESTED

Please make sure that your

mobile phones and pagers

have been switched off or turned to the

vibration mode

2

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

The Hong Kong Institute of Certified Public Accountants and

the speakers DO NOT accept any responsibility or

liability, and DISCLAIM all responsibilities and liabilities, in

respect of the contents of this workshop and any

consequences that may arise from any person acting or

refraining from action as a result of any materials in this

course. Any reliance on the materials in this workshop is

solely at the user’s risk.

DISCLAIMER

3 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

HKAS 12

Income Taxes

4 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Agenda

Part 1 - HKAS 12 Income Taxes

Part 2 - Amendments to HKAS 12 Income Taxes

5 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Part 1

HKAS 12 Income Taxes

6 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Introduction

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 7

Income

taxes

Deferred

taxes

Current

taxes

Current

Tax

Liabilities

Current

Tax

Assets

Deferred

Tax

Liabilities

Deferred

Tax

Assets

Tax expense (tax income)

is the aggregate amount included in the determination of profit or loss for

the period in respect of current tax and deferred tax.

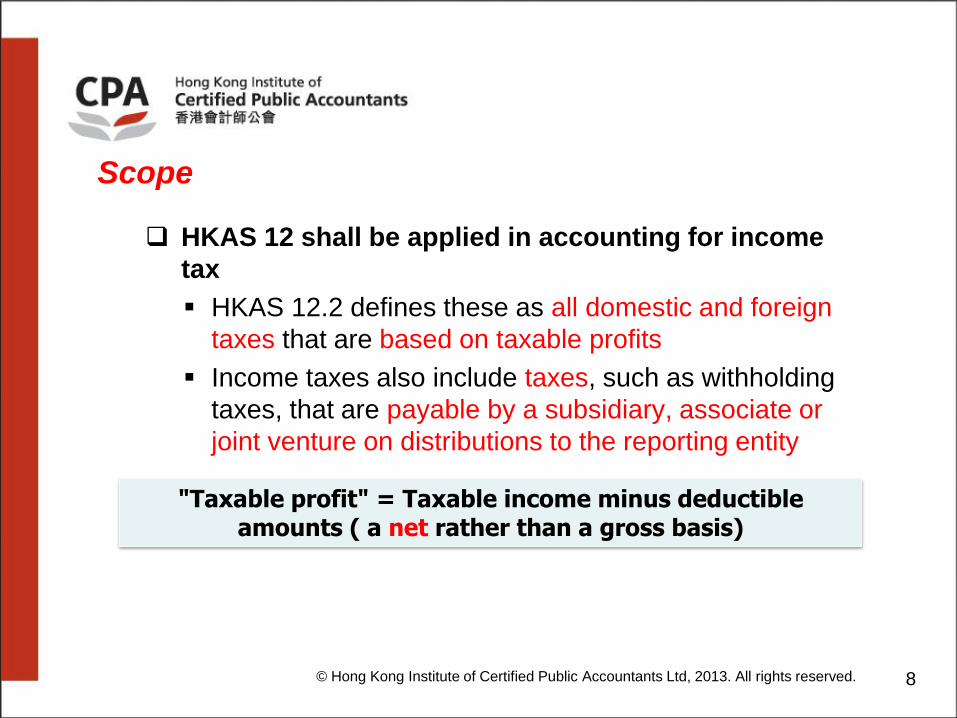

Scope

HKAS 12 shall be applied in accounting for income

tax

HKAS 12.2 defines these as all domestic and foreign

taxes that are based on taxable profits

Income taxes also include taxes, such as withholding

taxes, that are payable by a subsidiary, associate or

joint venture on distributions to the reporting entity

"Taxable profit" = Taxable income minus deductible

amounts ( a net rather than a gross basis)

8 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Scoped Out

Such taxes should be presented based on its nature, either as finance cost (e.g. interest) or operating expense (e.g.

penalty)

Sales taxes – Transactional taxes based

on sales value

Interest and penalties assessed on under-

payment or late payment of income tax

Tonnage tax paid on basis of tonnage

transported, tonnage capacity or a notional

profit

Scoped out from HKAS 12

Scoped out from HKAS 12

Scoped out from HKAS 12

9 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Current tax

10 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Definitions

Current tax:

Current tax is defined as the amount of income taxes

payable (recoverable) in respect of the taxable profit

(tax loss) for a period [HKAS 12.5]

It is the tax that the entity expects to pay (recover) in

respect of the financial period

Taxable profit (tax loss)

Taxable profit (tax loss) is defined as the profit (loss) for

a period, determined in accordance with the rules

established by the taxation authorities, upon which

income taxes are payable (recoverable) [HKAS 12.5]

11 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Current Tax – Recognition

Basic requirements: [HKAS 12.12-13]

Current tax for current and prior periods shall, to the

extent unpaid, be recognised as a liability

If the amount already paid in respect of current and prior

periods exceeds the amount due for those periods, the

excess shall be recognised as an asset

The benefit relating to a tax loss that can be carried back

to recover current tax of a previous period shall be

recognised as an asset

12 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Current Tax – Recognition (cont'd)

Generally, current tax is recognised in profit or loss

Exceptions: [HKAS 12.58]

• where the current tax arises as a result of a

transaction or event which is recognised, in the same

or a different period, outside profit or loss, either in

other comprehensive income or directly in equity or

• where the current tax arises from a business

combination

13 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Current Tax – Measurement

Current tax liabilities (assets) for the current and prior

periods shall be measured at the amount expected to be

paid to (recovered from) the taxation authorities, using the

tax rates (and tax laws) that have been enacted or

substantively enacted by the end of the reporting

period

14 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

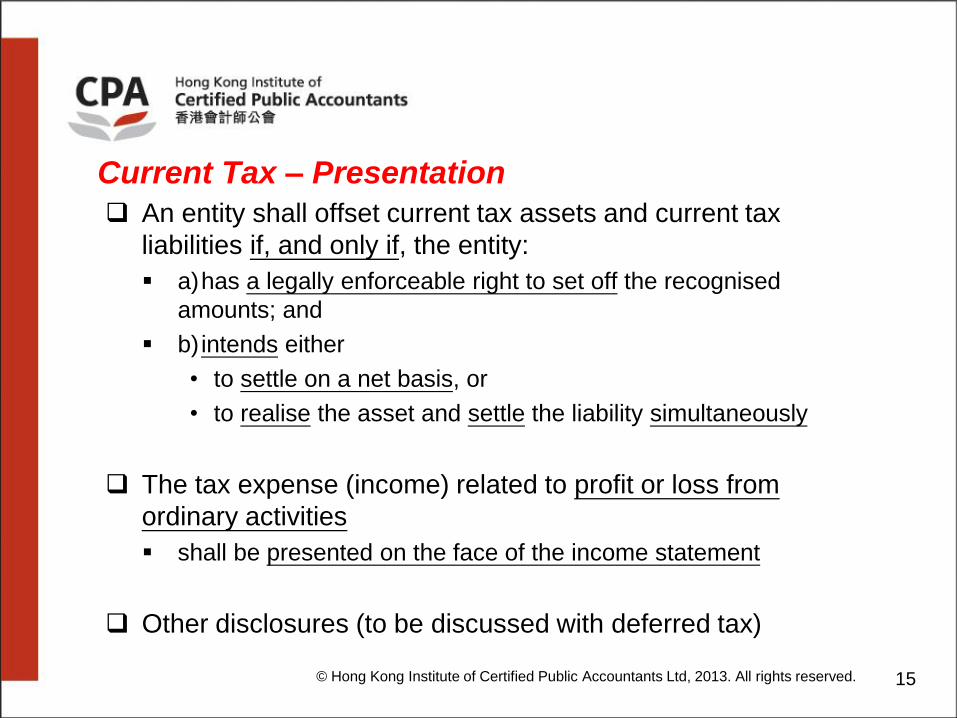

Current Tax – Presentation

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 15

An entity shall offset current tax assets and current tax

liabilities if, and only if, the entity:

a) has a legally enforceable right to set off the recognised

amounts; and

b) intends either

• to settle on a net basis, or

• to realise the asset and settle the liability simultaneously

The tax expense (income) related to profit or loss from

ordinary activities

shall be presented on the face of the income statement

Other disclosures (to be discussed with deferred tax)

Deferred tax

16 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Deferred Tax – Overview

HKAS 12 Income Taxes adopts:

Balance sheet liabiity method

• largely focuses on the statement of financial position by

recognising the tax effects of temporary differences between

the carrying amount of an asset or a liability and its tax base

Full provision approach

• recognised all differences, except for some limited cases

17 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Deferred Tax - Definitions

Deferred tax liabilities:

Deferred tax liabilities are defined as the amounts of

income taxes payable in future periods in respect of

taxable temporary differences [HKAS 12.5]

Deferred tax assets:

• Deferred tax assets are defined as the amounts of

income taxes recoverable in future periods in respect of :

[HKAS 12.5]

Deductible temporary differences;

the carryforward of unused tax losses; and

the carryforward of unused tax credits

18 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Principal steps in arriving at deferred tax assets/liabilities

Step 1: Calculate the tax base of each asset and liability in the statement of financial position

Step 2: Calculate the temporary difference (if any) for each of the above items

Step 3: Identify those temporary differences that will give rise to deferred tax assets or liabilities taking into account the recognition criteria and initial exemption laid down in the Standard

Step 4: Calculate the deferred tax attributable to those temporary differences by multiplying each temporary difference by the tax rate that is expected to apply when the temporary difference reverses based on enacted or substantively enacted tax rates

Step 5: Recognise the movement between the deferred tax balances in the opening and closing statements of financial position in profit or loss, in other comprehensive income, in equity, or as part of the initial accounting for a business combination

19 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 1: Deferred tax – Tax bases

The tax base of an asset or liability is the amount attributed

to that asset or liability for tax purposes

The amount of the tax base can vary according to the

manner in which the entity expects to recover the asset, or

settle the liability

e.g. properties held for use

e.g. properties held for sale

20 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 2: Deferred tax - temporary differences

Temporary difference is the difference between the carrying

amount of an asset or liability in the statement of financial

position and its tax base

When the recovery of an asset (non-taxable assets) or settlement

of a liability (non-deductible liabilities) has no tax consequences,

the tax base is equal to the carrying amount (i.e., temporary

difference is nil)

Two types of temporary differences:

taxable temporary difference

deductible temporary difference

21 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Temporary difference

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 22

Examples of circumstances resulting in taxable temporary differences:

Depreciation of an asset is accelerated for tax purposes

Interest revenue is received in arrears and is included in accounting profit

on a time apportionment basis but is included in taxable profit on a cash

basis

Development costs have been capitalised and will be amortised to the

income statement but were deducted in determining taxable profit in the

period in which they were incurred

Prepaid expenses have already been deducted on a cash basis in

determining the taxable profit of the current or previous periods

Financial assets or investment property are carried at fair value which

exceeds cost but no equivalent adjustment is made for tax purposes

An entity revalues property, plant and equipment (under HKAS 16) but no

equivalent adjustment is made for tax purposes

23

Examples of circumstances resulting in deductible temporary differences:

Accumulated depreciation of an asset in the financial statements is greater

than the cumulative depreciation allowed up to the balance sheet date

for tax purposes

The net realisable value of an item of inventory, or the recoverable amount

of an item of property, plant or equipment, is less than the previous carrying

amount and an entity therefore reduces the carrying amount of the asset, but

that reduction is ignored for tax purposes until the asset is sold

Research costs are recognised as an expense in determining accounting

profit but are not permitted as a deduction in determining taxable

profit until a later period

Income is deferred in the balance sheet but has already been included in

taxable profit in current or prior periods

Financial assets or investment property are carried at fair value which is

less than cost, but no equivalent adjustment is made for tax purposes

Temporary difference (cont’d)

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

24

Examples: Temporary difference

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Property held for

use

Revalued

property held

for use

Bad debt

expense

Deferred

revenue

Carrying

amount

500 1000 450

(gross amt of

500, less

allowance for bad

debt of 50)

800

(deferred

revenue received

in advance)

Tax base 300

(Tax written down

value)

300

(Tax written

value)

500

(allowance only

deductible upon

write-off)

0

(taxable on a

cash receipt

basis)

Temporary

difference/

deductible

temporary

difference

200

700

(50)

(800)

Step 3: Deferred tax – Temporary difference that

gives rise to deferred assets and liabilities

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 25

All

recognised?

Taxable

temporary

difference

Deductible

temporary

difference

Unused tax

losses or credits

Deferred tax

liability

Deferred tax

asset

• Balance sheet liability

method - full provision

approach

General rule: Recognise all

unless specific exceptions

apply (to be discussed later)

Taxable/deductible temporary differences

Carrying amount – tax base

Type of temporary difference

Gives rise to…

Asset Positive Taxable Deferred tax liability

Asset Negative Deductible Deferred tax asset

Liability Positive Deductible Deferred tax asset

Liability Negative Taxable Deferred tax liability

26 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 4: Deferred tax – Measurement

Computation of deferred tax assets and liabilities

To calculate the amount of a deferred tax asset or liability, HKAS 12 contains the following formula:

A deferred tax asset can also arise from tax losses that have been carried forward. These deferred tax assets are calculated as follows:

Deferred tax liabilities or assets

Taxable or deductible temporary difference

Tax rate = ×

Deferred tax asset Unused tax losses and /

or tax credit Tax rate = ×

27 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 4: Deferred tax – Measurement (cont'd)

Applicable tax rates and laws

Deferred assets and liabilities shall be measured:

• at the tax rates that are expected to apply to the period

when the temporary difference reverses

• based on tax rates and tax laws enacted or

substantively enacted at the end of the reporting period

28 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Example:

• A PRC joint venture is entitled to tax concessions during its

initial years of operation

• The standard income tax rate is 30%. However, the joint

venture is fully exempted from PRC income tax for 2 years

starting from its first profit-making year, followed by a 50%

reduction in the PRC income tax rate for the next 3 years

• The joint venture has an item of equipment that cost RMB

12,000, which is depreciated over 6 years for accounting

purposes and 3 years for PRC income tax purposes, using the

straight-line method. The first year that the joint venture has

taxable profit is 2011

Step 4: Deferred tax – Measurement (cont'd)

29 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

• The temporary differences arising as a result of the accelerated tax depreciation

will reverse during years 2014, 2015 and 2016 as follows:

Carrying

amount

Tax base Temporary

difference

Reversal of

temporary

difference

Tax rate Deferred tax

liability

RMB RMB RMB RMB RMB

2011 10,000 8,000 2,000 N/A 0% 300 (2,000x15%)

2012 8,000 4,000 4,000 N/A 0% 600 (4,000x15%)

2013 6,000 0 6,000 N/A 15% 1,200 (4,000x15%)

+(2,000x30%)

2014 4,000 0 4,000 2,000 15% 900 (2,000x15%)

+(2,000x30%)

2015 2,000 0 2,000 2,000 15% 600 (2,000x30%)

2016 0 0 - 2,000 30% -

The above table illustrates that, where tax rates vary, it is necessary to estimate the tax rate that willl apply

when the temporary difference reverses. In the example, it is predictable that the temporary difference

arising in 2011 will reverse in 2014 and, therefore, the appropriate tax rate for deferred tax purposes is 15%

rather than 0%. Similarly, the temporary differences arising in 2012 and 2013 will reverse in 2015 and 2016,

and tax rates of 15% and 30% should therefore be applied for the temporary differences arising in 2012 and

2013 respectively.

Step 4: Deferred tax – Measurement (cont'd)

30 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 4: Deferred tax – Measurement (cont'd)

Progressive or graduated tax rates

• When different tax rates apply to different levels of taxable

income, deferred tax assets and liabilities are measured

using the average rates that are expected to apply to the

taxable profit (tax loss) of the periods in which the

temporary differences are expected to reverse

[HKAS 12.49]

31 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 4: Deferred tax – Measurement (cont'd)

Substantively enacted tax rates

Current and deferred tax assets and liabilities are usually

measured using the tax rates and tax laws that have been

enacted. However, in some jurisdictions, announcements

of tax rates and tax laws by the government have the

substantive effect of actual enactment, which may follow

the announcement by a period of several months. In these

circumstances, tax assets and liabilities are measured

using the announced tax rate and tax laws

[HKAS 12.48]

32 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 4: Deferred tax – Measurement (cont'd)

Changes in tax rates after the reporting period

Where there is a change in tax rates or laws after the

reporting period, no adjustment is made to the carrying

amounts of deferred tax assets and liabilities

However, where the effect of the change is such that "non-

disclosure could influence the economic decisions of users

taken on basis of the financial statements", disclosure will

be required in accordance with HKAS 10 Event after the

Reporting Period [HKAS 10.21]

33 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 4: Deferred tax – Measurement (cont'd)

Discounting

HKAS 12 explicitly prohibits the use of discounting for the

measurement of deferred tax assets and liabilities

[HKAS 12.53]

34 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Step 4: Deferred tax – Measurement (cont'd)

The measurement of deferred tax liabilities and deferred tax

assets shall reflect the tax consequences that would follow

from the manner in which the entity expects, at the end of the

reporting period, to recover or settle the carrying amount of

its assets and liabilities

[HKAS 12.51]

35 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Examples:

36 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

An item of PPE has a carrying

amount of 100 and a tax base of 60

• Tax rate of 20%

would apply if

the asset were

sold

• Tax rate of 30%

would apply to

other income

• The entity recognises a

deferred tax liability of 8 (40 at

20%) if it expects to sell the

item without further use or

• a deferred tax liability of 12 (40

at 30%) if it expects to retain

the item and recover its

carrying amount through use

Examples:

37 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

• An item of PPE with a

cost of 100 and a

carrying amount of 80

is revalued to 150

• No equivalent

adjustment is made

for tax purposes

• Cumulative

depreciation for tax

purposes is 30 and tax

rate is 30%

• If the item is sold for

more than cost, the

cumulative tax

depreciation of 30 will

be included in taxable

income, but sale

proceeds in excess of

cost will not be

taxable

• Tax base =

70

• Taxable

temporary

difference

= 80

• if the entity expects to recover the carrying

amount by using the item, it must generate

taxable income of 150, but will only be able to

deduct depreciation of 70

• On this basis, there is a deferred tax liability

of 24 (80 at 30%)

• If the entity expects to recover the carrying

amount by selling the item immediately for

proceeds of 150, the deferred tax liability is:

Taxable

temporary

difference

Tax rate Deferred tax

liability

Cumulative

tax

depreciation

30 30% 9

Proceeds in

excess of cost

50 nil -

Total 80 9

Step 5: Deferred tax - Recognition of movement

Deferred tax should be recognised as income or an expense and included in the net profit or loss for the period, except to the extent that the movement in deferred tax: [HKAS 12.58, 61A & 66]

Relates to an item recognised in other comprehensive income,

deferred tax also recognised in other comprehensive income

Relates to an item recognised in equity, deferred tax also recognised in equity

Arises in relation to a business combination, adjusts goodwill

.

38 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Example: Deferred tax liability arising on the revaluation of a

property

B Limited revalues a property from a carrying amount of $100,000 to $150,000. The tax

base of the asset is $100,000. The carrying amount of the property is expected to be

recovered through use. The applicable tax is 30%.

A taxable temporary difference of $50,000 ($150,000-$100,000) arises on revaluation ,

giving rise to a deferred tax liability of $15,000 ($50,000 x 30%). The following entries

record the revaluation and the deferred tax liability:

DR CR

$ $

Property, plant and equipment 50,000

Property revaluation reserve 50,000

Property revaluation reserve 15,000

Deferred tax liability 15,000

39 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Example : Deferred tax liability arising on the revaluation of a

property (Cont'd)

In subsequent periods, the property will be depreciated for both accounting

and tax purposes, changing the temporary difference. Any movements in the

deferred tax liability are recognised in the income statement. For instance, if

the carrying amount of the property at the end of the next reporting period is

$120,000 and tax base is $90,000, there is a taxable temporary difference of

$30,000 and a deferred tax liability of 9,000 ($30,000x30%). This movement

for the year is recorded as follows:

DR CR

$ $

Deferred tax liability ($15,000 -$9,000) 6,000

Deferred tax (I/S) 6,000

40 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Presentation

Classification:

Tax assets and liabilities may not be combined with other

assets and liabilities, but must be shown separately on the

statement of financial position

Deferred tax assets and liabilities must be presented

separately from current tax assets and liabilities; and

Deferred tax assets and liabilities must be classified as

non-current

41 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Offset of current tax

An entity should offset current tax assets and current tax liabilities if, and only if, the entity: [HKAS 12.71] • has a legally enforceable right to set off tax assets/tax liabilities;

and

• intends either to settle tax assets/liabilities on a net basis, or to realise the asset and settle the liability simultaneously

An entity normally has a legally enforceable right to set off current tax assets against current tax liabilities when they relate to taxes levied by the same taxation authority, and that authority permits the entity to make or receive a single net payment [HKAS 12.72]

Presentation (cont'd)

42 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Offset of current tax (cont'd)

Where a company is preparing consolidated financial statements, current tax assets and liabilities arising from different group companies should not be offset unless:

[HKAS 12.73]

• the companies concerned have a legally enforceable right to make or

receive a single net payment; and

• the companies intend to make or receive such a net payment or to recover the asset and settle the liability simultaneously

Presentation (cont'd)

43 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Offset of deferred tax assets and liabilities

An entity should offset deferred tax assets and deferred tax liabilities if, and only if: [HKAS 12.74]

• the entity has a legally enforceable right to set off current tax assets against current tax liabilities; and

• the deferred tax assets and the deferred tax liabilities relate to income taxes levied by the same taxation authority on either:

the same taxable entity; or

different taxable entities which intend either to settle current tax liabilities and assets on a net basis, or to realise the assets and settle the liabilities simultaneously, in each future period in which significant amounts of deferred tax liabilities or assets are expected to be settled or recovered

Presentation (cont'd)

44 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Disclosure

HKAS 12 has extensive disclosure

requirements on income tax

Statement of comprehensive income

Major components of the tax charge or credit in the

statement of comprehensive income are required to be

separately identified, including:

• Current tax expense or income;

• Adjustments to current tax of prior periods

• Deferred tax expense (income) relating to: • Origination and reversing of temporary differences

• Changes in tax rates or new taxes

45 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Disclosure

Reconciliation of tax charge or credit to accounting profit:

HKAS 12 requires the presentation of an explanation of the

relationship between the tax expense (income) and accounting

profit in either or both of the following forms:

• A numerical reconciliation between tax expense (income) and the product of

accounting profit multiplied by the applicable tax rates disclosing also the

basis on which the applicable tax rates are computed; or

• A numerical reconciliation between the average effective tax rate (being the

tax expense (income) divided by the accounting profit) and the applicable tax

rate, disclosing also the basis on which the applicable tax rate is computed

An explanation is required of changes in the applicable tax

rates compared to the previous accounting period

46 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Disclosure: Reconciliation of tax charge (i) Reconciliation in absolute terms 20X1 20X0

$'000 $'000

Accounting profit 8,740 8,775

Tax at the applicable rate of 35% (20X0:40%) 3,059 3,510

Tax effect of expenses that are not deductible in determining

taxable profit

122

480

Reduction in opening deferred tax liability resulting from

reduction in tax rate

(1,127)

-

Tax expense 2,054 3,990

(ii) Reconciliation in percentage terms 20X1 20X0

% %

Applicable tax rate 35.0 40.0

Tax effect of expenses that are not deductible in determining

taxable profit

1.4 5.5

Effect on opening deferred tax liability of reduction in tax rate (12.9) -

Average effective tax rate (tax expense divided by profit before

tax

23.5

45.5

47 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Disclosure – Deferred tax

For each type of temporary difference, unused tax loss and tax

credit:

• Amount of the deferred tax assets and liabilities recognised

• Amount of deferred tax income or expense recognised in profit

or loss

The amount and expiry date of temporary differences, unused tax

losses and tax credits; and

The amount of temporary differences associated with investments in

subsidiaries, branches and associate and interests in joint ventures,

for which deferred tax liabilities have not been recognised.

48 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

and many others……(please refer to the

standard itself for a comprehensive

list)

Deferred tax – Recognition exceptions

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 49

All

recognised?

Taxable

temporary

difference

Deductible

temporary

difference

Unused tax

losses or credits

Deferred tax

liability

Deferred tax

asset

• Balance sheet liability

method - full provision

approach

General rule: Recognise all

unless specific exceptions

apply (to be discussed later)

Deferred tax – Recognition exceptions

Initial recognition of an asset or liability which affects neither

accounting profit or loss nor taxable profit or loss, other than from a

business combination

Initial recognition of goodwill

An investment in a subsidiary, branch, associates or joint ventures,

if the parent, investor or venturer is able to control the timing of the

reversal of the temporary difference; and it is probable that the

temporary difference will not reverse in the foreseeable future

Deferred tax assets recognised only to the extent that recoverability

is probable

50 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition exception – Initial recognition of an asset

or liability

Temporary differences are not permitted to be

recognised where the difference arises in respect of the

initial recognition of an asset or liability in a transaction

that:

is not a business combination; and

at the time of the transaction, affects neither accounting profit

(loss) nor taxable profit (tax loss)

51 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition exception – Initial recognition of an asset

or liability

HKAS 12 requires the recognition of deferred tax on

temporary differences arising on the initial recognition of an

asset or liability when:

a transaction affects the income statement (e.g. anticipation of income receivable (asset), or accrual of costs payable (liability); or

a transaction affects taxable income (e.g. expenditure on assets such as computer equipment allowed for tax purposes when paid (asset), or deferral of income recognition in respect of funds that are taxable when received (liability); or

a business combination

52 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Does the temporary difference arise on the initial recognition of an asset or a liability?

Was the asset or liability acquired in a business combination?

Did the transaction giving rise to the asset or liability affect either the accounting result or the taxable profit (loss) at the time of the transaction?

Do not recognise deferred tax impact

Recognise deferred tax

impact (subject to

other exceptions)

Yes

Yes

Yes

No

No

No

53

Recognition exception – Initial recognition of an asset

or liability

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Company A purchases an asset for $100,000. Only $60,000 is qualifying expenditure for tax

purposes. The carrying amount of the asset will be recovered through use in taxable manufacturing

operations. The asset is depreciated on a straight-line basis at 25% for both tax and accounting

purposes.

No deferred tax is ever recognised in respect of the original temporary

difference

Example 1: Deferred tax liability arising on the recognition of an

asset – asset depreciated at the same rate for tax and accounting

purposes

Carrying amount Tax base Temporary

difference

Unrecognised

difference

Deferred tax

Year $ $ $ $ $

20X0 100,000 60,000 40,000 40,000 -

20X1 75,000 45,000 30,000 30,000 -

20X2 50,000 30,000 20,000 20,000 -

20X3 25,000 15,000 10,000 10,000 -

20X4 0 0 - - -

54 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Facts same example 1, but the asset is depreciated at 25% for accounting purposes and

33 1/3% for tax purposes. The tax rate is 17.5%.

* Being the initial temporary difference of 40,000 of which initial recognition exception applied

Example 2: Deferred tax liability arising on the recognition of an

asset – different depreciation rates for tax and accounting purposes

Carrying

amount

Tax base Temporary

difference

Un-

recognised

temporary

difference

Recognised

temporary

difference

Deferred

tax

liability

Year $ $ $ $ $ $

A B A-B=C D* C-D=E E x17.5%

20X0 100,000 60,000 40,000 40,000 - -

20X1 75,000 40,000 35,000 30,000 5,000 875

20X2 50,000 20,000 30,000 20,000 10,000 1,750

20X3 25,000 0 25,000 10,000 15,000 2,625

20X4 0 0 - - - -

55 © Hong Kong Institute of Certified Public

Accountants Ltd, 2013. All rights reserved.

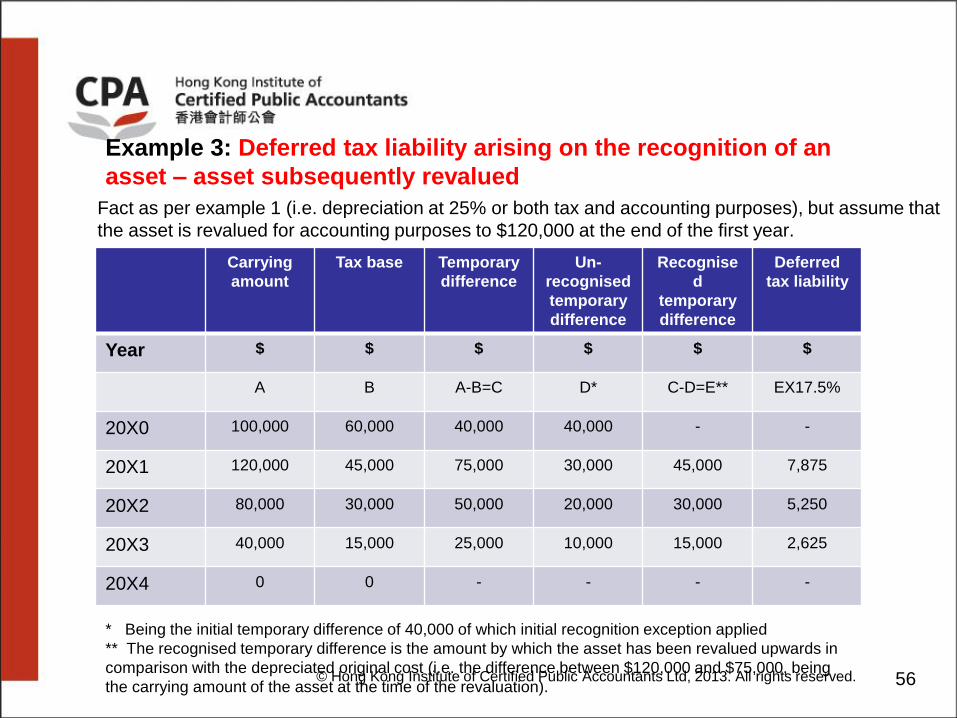

Fact as per example 1 (i.e. depreciation at 25% or both tax and accounting purposes), but assume that

the asset is revalued for accounting purposes to $120,000 at the end of the first year.

Example 3: Deferred tax liability arising on the recognition of an

asset – asset subsequently revalued

Carrying

amount

Tax base Temporary

difference

Un-

recognised

temporary

difference

Recognise

d

temporary

difference

Deferred

tax liability

Year $ $ $ $ $ $

A B A-B=C D* C-D=E** EX17.5%

20X0 100,000 60,000 40,000 40,000 - -

20X1 120,000 45,000 75,000 30,000 45,000 7,875

20X2 80,000 30,000 50,000 20,000 30,000 5,250

20X3 40,000 15,000 25,000 10,000 15,000 2,625

20X4 0 0 - - - -

* Being the initial temporary difference of 40,000 of which initial recognition exception applied

** The recognised temporary difference is the amount by which the asset has been revalued upwards in

comparison with the depreciated original cost (i.e. the difference between $120,000 and $75,000, being

the carrying amount of the asset at the time of the revaluation). 56 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

HKAS 12 prohibits the recognition of a temporary difference

in respect of goodwill at initial recognition

Non-deductible goodwill – no deferred tax impact

57 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition exception – Initial recognition of goodwill

Example – Goodwill Exemption

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 58

Deferred tax implications for the CEF Group of companies

• CEF Ltd acquired DEF Ltd on 1 January 2012 for $6 million when the fair value

of the net assets was $4 million, and the tax written down value of the net

assets was $3 million.

• According to the local tax laws for CEF Ltd, impairment of goodwill is not tax

deductible.

Answers

The CEF group Carrying Tax

amount base

Goodwill $2 million -

Net assets $4 million $3 million

Temporary

differences

$2 million

$1 million

Deferred

tax

liability?

• Provision is made for the temporary differences of net assets

• But NO provision is made for the temporary difference of goodwill

• As an entity shall not recognise a deferred tax liability arising from

initial recognition of goodwill.

Taxable temporary differences associated with investments in

subsidiaries, branches and associates and interests in joint

ventures required to be recognised as deferred tax liability, except

for taxable temporary differences where: [HKAS 12.39]

The investor is able to control the timing of the reversal; and

It is probable that the difference will not reverse in the

foreseeable future

Temporary difference may arise if:

Gain from sale investment is taxable

Dividends received from investment is taxable

No temporary difference where recovery has no tax impact

59 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition exception – Investments in

subsidiaries/associates/joint ventures

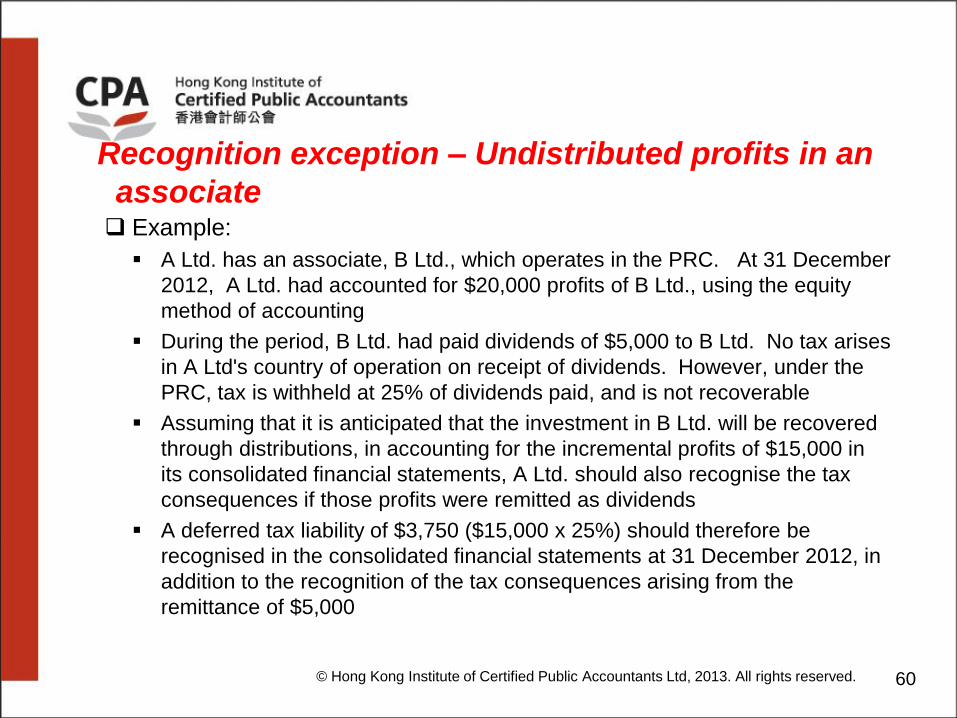

Example:

A Ltd. has an associate, B Ltd., which operates in the PRC. At 31 December

2012, A Ltd. had accounted for $20,000 profits of B Ltd., using the equity

method of accounting

During the period, B Ltd. had paid dividends of $5,000 to B Ltd. No tax arises

in A Ltd's country of operation on receipt of dividends. However, under the

PRC, tax is withheld at 25% of dividends paid, and is not recoverable

Assuming that it is anticipated that the investment in B Ltd. will be recovered

through distributions, in accounting for the incremental profits of $15,000 in

its consolidated financial statements, A Ltd. should also recognise the tax

consequences if those profits were remitted as dividends

A deferred tax liability of $3,750 ($15,000 x 25%) should therefore be

recognised in the consolidated financial statements at 31 December 2012, in

addition to the recognition of the tax consequences arising from the

remittance of $5,000

60 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition exception – Undistributed profits in an

associate

Entity A has a subsidiary with a carrying amount of $2M and a tax

base of $1.8M. Entiy A controls the distribution of dividends by the

subsidiary

Entity A does not have any need for the subsidiary to make a

distribution and has active plans for the undistributed profits to be

reinvested for expansion

61 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition exception – Undistributed profits in a

subsidiary

Entity A can control the timing of the reversal and the temporary difference is

not expected to reverse in the foreseeable future

Entity A cannot recognise a deferred tax liability on the temporary difference

of $200K

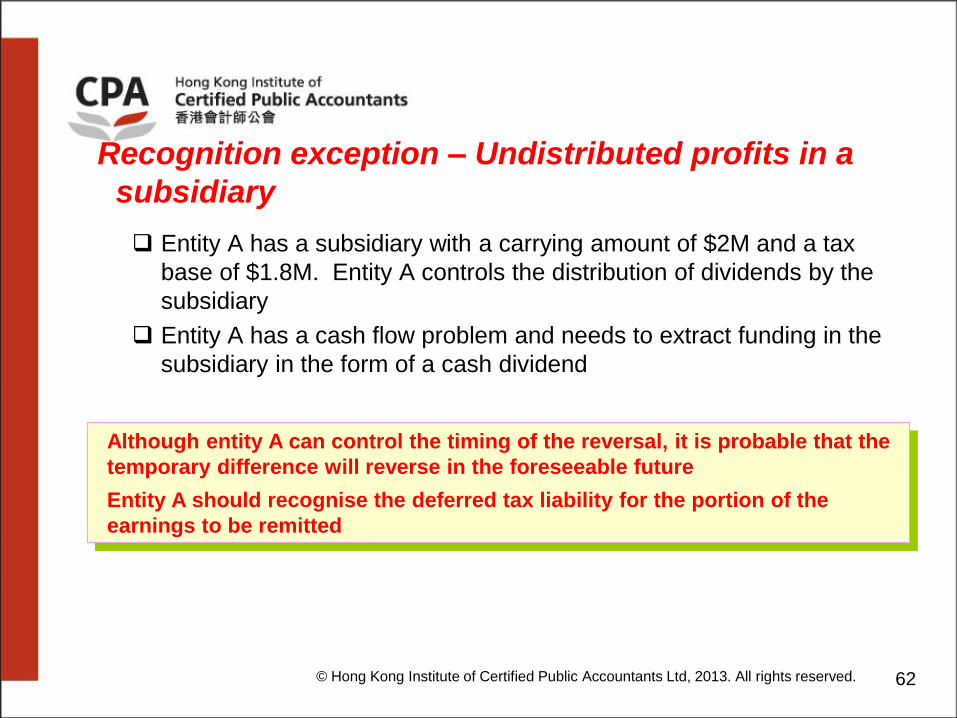

Entity A has a subsidiary with a carrying amount of $2M and a tax

base of $1.8M. Entity A controls the distribution of dividends by the

subsidiary

Entity A has a cash flow problem and needs to extract funding in the

subsidiary in the form of a cash dividend

62 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition exception – Undistributed profits in a

subsidiary

Although entity A can control the timing of the reversal, it is probable that the

temporary difference will reverse in the foreseeable future

Entity A should recognise the deferred tax liability for the portion of the

earnings to be remitted

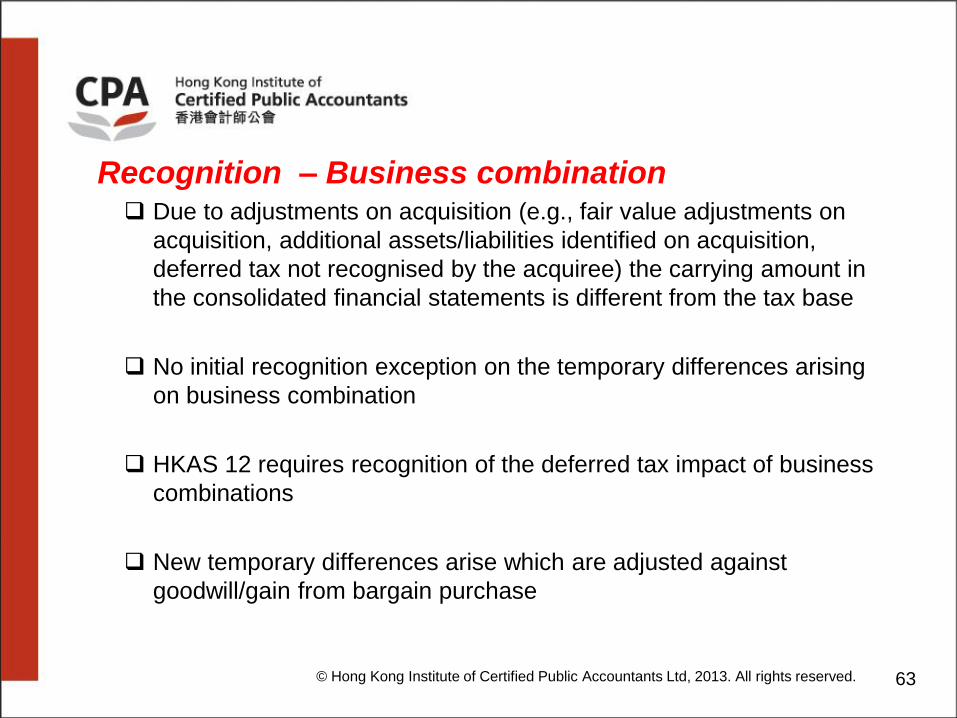

Due to adjustments on acquisition (e.g., fair value adjustments on

acquisition, additional assets/liabilities identified on acquisition,

deferred tax not recognised by the acquiree) the carrying amount in

the consolidated financial statements is different from the tax base

No initial recognition exception on the temporary differences arising

on business combination

HKAS 12 requires recognition of the deferred tax impact of business

combinations

New temporary differences arise which are adjusted against

goodwill/gain from bargain purchase

63 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition – Business combination

Background

On 1 January 2012, entity H acquired 100% of entity S for $3,500

At the date of acquisition, entity S had net assets at carrying amount of $2,500 (including $140 recognised deferred tax liability)

Fair value of owner-occupied property is revalued upward by$400

An intangible asset is recognised at its fair value of $200

A provision for an onerous lease contract of $300 is recognised

Applicable tax rate is 20%

64 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Example – Business combination

Net assets at carrying amount 2,500

Fair value adjustment of property

Fair value of intangible assets

Provision for onerous contract

400

200

(300)

Deferred tax on:

- fair value adjustment of property (20% X 400)

- fair value of intangible assets (20% X 200)

- provision for onerous contract (20% X 300)

(80)

(40)

60

Fair value of net assets acquired 2,740

Goodwill 760

Consideration paid 3,500

65 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Example – Business combination

Fact pattern:

Entity H sold inventory costing $100 to its overseas subsidiary, entity

S, for $160

Entity H’s tax rate: 30%

Entity S’s tax rate: 25%

The inventory remains on hand at year-end and unrealised profit of $60

to be eliminated on consolidation

No change in tax base

What is the deferred tax balance?

Example: Elimination of unrealised profits on consolidation

66 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Analysis:

Entity H:

• recognises a current tax liability of $18 ($60 profit at 30%)

• does not recognise any deferred tax balances, no future tax consequences

from entity H’s point of view

Entity S

• entitled to a future deduction for $160 paid for the inventory

• tax base for the inventory is $160

• In entity S’s individual financial statements, the tax base is equal to the

carrying amount, and no temporary difference arises

Example: Elimination of unrealised profits on consolidation

(cont'd)

67 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Analysis:

Consolidated F/S of entity H

• the carrying amount of the inventory is reduced from $160 to $100 on

consolidation

• A $60 deductible temporary difference arises, representing the difference

between the carrying amount ($100) and the tax base ($160)

• A deferred tax asset is calculated by multiplying the temporary difference of

$60 by 25%, as the deduction is available to entity S at that rate when the

unrealised profit is realised outside the group on sale of the inventory by S

Limited

The deferred tax asset arising of $15 is recognised on consolidation

Example: Elimination of unrealised profits on consolidation

(cont'd)

68 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 69

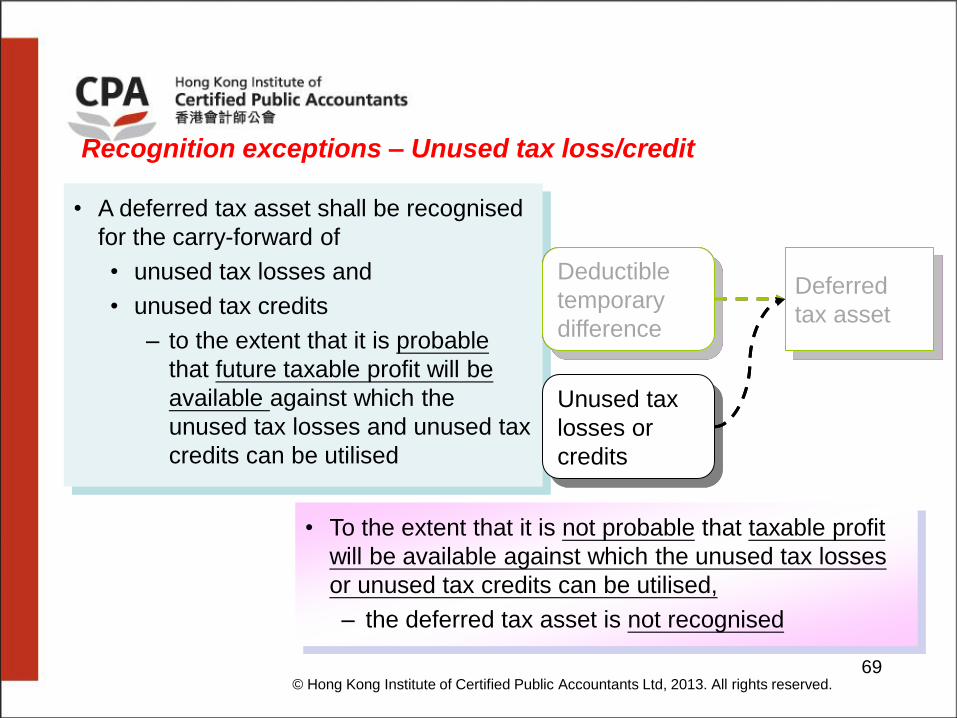

• A deferred tax asset shall be recognised

for the carry-forward of

• unused tax losses and

• unused tax credits

– to the extent that it is probable

that future taxable profit will be

available against which the

unused tax losses and unused tax

credits can be utilised

• To the extent that it is not probable that taxable profit

will be available against which the unused tax losses

or unused tax credits can be utilised,

– the deferred tax asset is not recognised

Deductible

temporary

difference

Unused tax

losses or

credits

Deferred

tax asset

Deductible

temporary

difference

Deferred

tax asset

Recognition exceptions – Unused tax loss/credit

Availability of future profits

A deferred tax asset represents a future tax deduction

It is valuable only if the entity will have future taxable profits against which the deduction can be offset

Important question to answer is when can it be

considered probable that an entity will have sufficient

taxable profits available in the future to enable the

deferred tax asset to be recovered ?

70 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Recognition exceptions – Unused tax loss/credit (cont'd)

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 71

Examples criteria in assessing available taxable profit:

a) whether there are sufficient taxable temporary differences

(deferred tax liabilities) relating to the same taxation authority

and the same taxable entity

b) whether it is probable that the entity will have sufficient taxable

profits before the unused tax losses or unused tax credits

expire; and

c) whether tax planning opportunities are available

Recognition exceptions – Unused tax loss/credit

Recognition – Unrecognised deferred tax assets

© Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved. 72

Periodic Re-assessment

At each balance sheet date,

– an entity re-assesses unrecognised deferred

tax assets

The entity recognises a previously unrecognised

deferred tax asset

– to the extent that it has become probable that

future taxable profit will allow the deferred tax

asset to be recovered

Recognition exceptions – Unused tax loss/credit

Amendments to HKAS 12

Income Taxes

73 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Amendment to HKAS 12 – Deferred tax of

investment properties

General principle: Measurement of deferred tax assets or

liabilities which reflect the tax consequences that would follow

the manner in which management expects to recover or settle

the carrying amount of the entity's assets or liabilities

Management may expect to recover the investment property by

using it, by selling it, or by a combination of use and sale

Such expectation can affect the measurement of deferred taxes

when different tax rates or tax bases apply to the profits generated

from using and selling the investment property

74 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Highlights of amendments to HKAS 12

HKAS 12 has been updated to include:

• A rebuttable presumption that deferred tax on investment property

measured using the fair value model in HKAS 40 should be determined

on the basis that its carrying amount will be recovered through sale;

and

• A requirement that deferred tax on non-depreciable assets, measured

using the revaluation model in HKAS 16, should always be measured on

a sale basis

75 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Impact

Who will be affected ?

For entities holding investment property measured at fair value in

territories where

a) the capital gains tax rate is different from the income tax

rate, and/or;

b) the tax base from sale is different from tax base from use

Example :

For investment properties in Hong Kong, movement in the fair

value will not be tax-affected as there is no capital gains tax in

Hong Kong. Deferred tax liabilities will be reduced significantly

76 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Further considerations

The presumption can be rebutted…

if the investment property is depreciable and is held within a

business model whose objective is to consume

substantially all of the economic benefits embodied in the

investment property over time, rather than through sale

this is not a policy choice

it also applies when a deferred tax arises from measuring

investment property in a business combination if the entity

will use the fair value model for subsequent measurement

77 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Further considerations (cont.)

For entities subject to Hong Kong tax, recovery of

investment property through sale does not necessarily

mean that the deferred tax liability on fair value gains is nil

Need to consider the possible claw back of previously

granted tax allowances in respect of the property

If the IRD considers the investment property is held for

trading purposes (i.e., disposal would not be deemed

to be a capital transaction), the zero rate applicable to

capital gains will not apply

78 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Further considerations (cont.)

Impact on deferred tax assets

Applying the presumption does not change the

principles to be adopted when recognising and

measuring deferred tax assets

The amendment is likely to reduce significantly deferred

tax liabilities

The entity might need to reconsider the recoverability

of the entity's deferred tax assets due to the changes in

the nature and amount of deferred tax liabilities

79 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Illustrations

Example 1

On 1 Jan 2010, entity B purchased an investment property for $100K

The investment property does not have a freehold land component and is

measured at fair value subsequently

At 31 Dec 2012, the fair value of the investment property is $120K

Tax depreciation of 4% of the cost per annum is claimed for investment

properties

. Income tax rate is 30%

The cumulative tax depreciation claimed previously will be included in the

taxable income if the investment property is sold for more than the tax

written-down value

Sale proceeds in excess of the cost are not taxed

The tax written down value is $88K at 31 Dec 2012

80 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

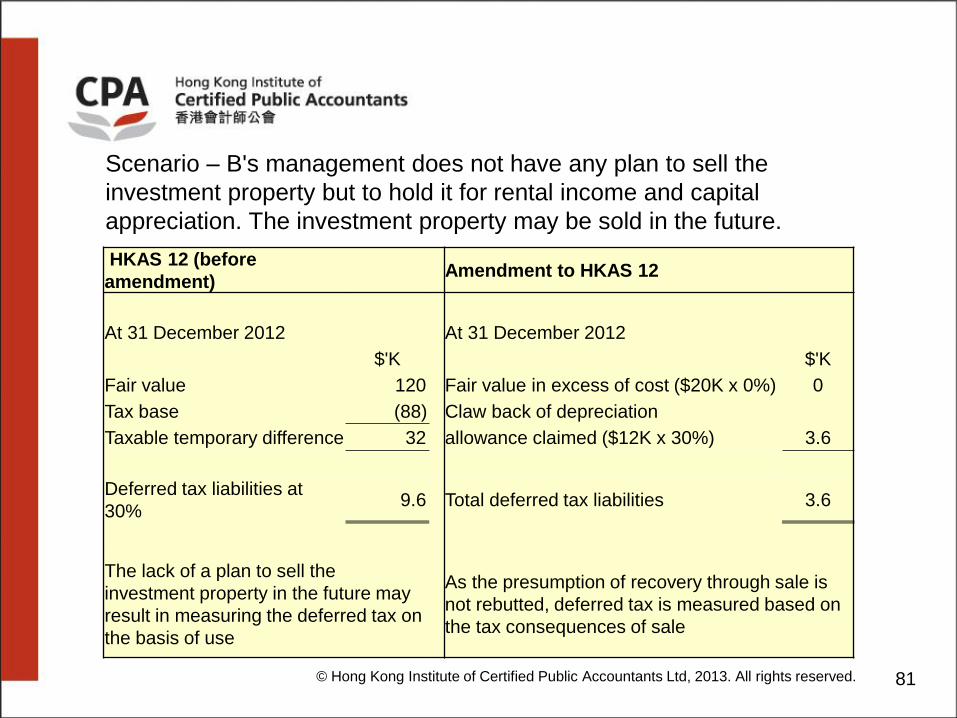

Scenario – B's management does not have any plan to sell the

investment property but to hold it for rental income and capital

appreciation. The investment property may be sold in the future.

HKAS 12 (before

amendment) Amendment to HKAS 12

At 31 December 2012 At 31 December 2012

$'K $'K

Fair value 120 Fair value in excess of cost ($20K x 0%) 0

Tax base (88) Claw back of depreciation

Taxable temporary difference 32 allowance claimed ($12K x 30%) 3.6

Deferred tax liabilities at

30% 9.6 Total deferred tax liabilities 3.6

The lack of a plan to sell the

investment property in the future may

result in measuring the deferred tax on

the basis of use

As the presumption of recovery through sale is

not rebutted, deferred tax is measured based on

the tax consequences of sale

81 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Illustrations Example 2

Background

An entity holds an investment property with the following details:

Cumulative

Cost Fair value tax depreciation

Land (unlimited useful life) 40 60 N/A

Buildings 60 90 30

Total 100 150

tax rate

If sales > cost 20%

Claw back of tax

depreciation

claimed if sales > cost 30%

82 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Illustrations

Example 2 – if the presumption is NOT rebutted…

Taxable temporary Deferred tax

difference Tax rate liabilities

Claw back of depreciation

allowance claimed 30 30% 9

Fair value in excess of

cost 50 20% 10

(150-100)

80 19

83 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Illustrations

Example 2 – if the presumption is rebutted…

Taxable

temporary Deferred tax

difference Tax rate liabilities

Buildings

Fair value in excess of

tax base (90 -30) 60 30% 18

Land (with unlimited useful life)

Fair value in excess of tax base

(60-40) 20 20% 4

80 22

84 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

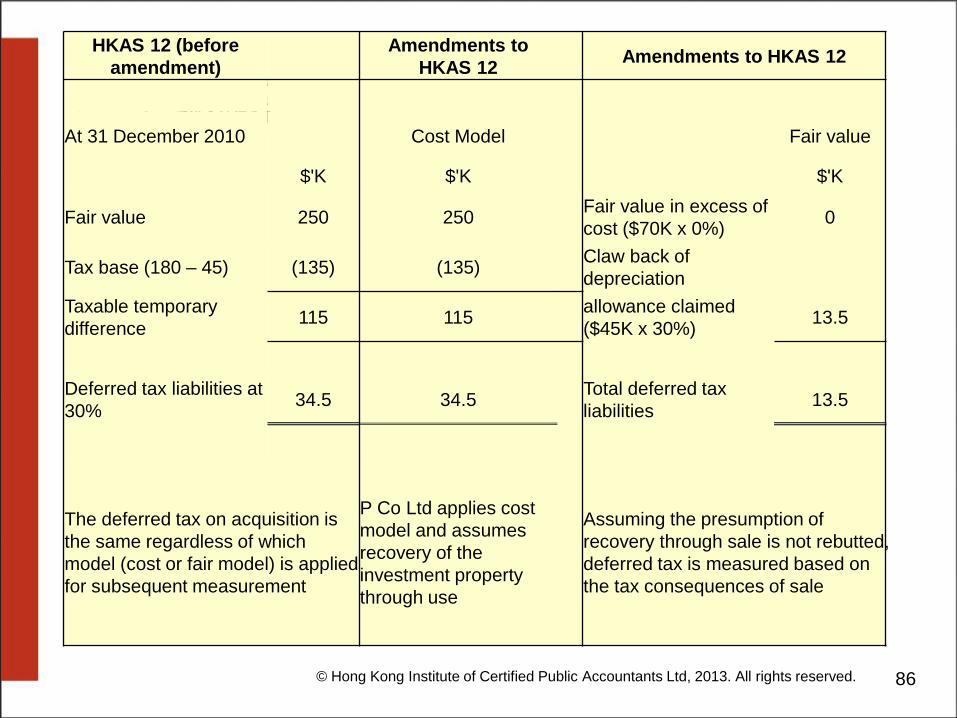

Illustrations Example 3

Entity P acquired the entire shares of entity S for $500K on 31 Dec 2010

The identifiable assets acquired included an investment property of fair value

$250K and other net assets (excluding deferred tax on property) with a fair

value of $100K

Entity S purchased the investment property for $180K. The cumulative tax

depreciation at 31 Dec 2010 is $45K

Income tax rate is 30%

The cumulative tax depreciation claimed previously will be included in the

taxable income if the investment property is sold for more than the tax

written-down value

Sale proceeds in excess of the cost are not taxed

85 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

HKAS 12 (before

amendment)

Amendments to

HKAS 12 Amendments to HKAS 12

At 31 December 2010 Cost Model Fair value

$'K $'K $'K

Fair value 250 250 Fair value in excess of

cost ($70K x 0%) 0

Tax base (180 – 45) (135) (135) Claw back of

depreciation

Taxable temporary

difference 115 115

allowance claimed

($45K x 30%) 13.5

Deferred tax liabilities at

30% 34.5 34.5

Total deferred tax

liabilities 13.5

The deferred tax on acquisition is

the same regardless of which

model (cost or fair model) is applied

for subsequent measurement

P Co Ltd applies cost

model and assumes

recovery of the

investment property

through use

Assuming the presumption of

recovery through sale is not rebutted,

deferred tax is measured based on

the tax consequences of sale

86 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

HKAS 12

(before

amendment)

Amendments to HKAS 12

Cost model Fair value

model

$'K $'K $'K

Purchase consideration 500 500 500

Fair value of investment property (250) (250) (250)

Fair value of other identifiable net assets (100) (100) (100)

Deferred tax liability on the investment

property 34.5 34.5 13.5

Goodwill 184.5 184.5 163.5

The choice of the accounting polices for subsequent measurement

of investment properties acquired in a business combination might

affect the goodwill

87 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Effective date

An entity shall apply these amendments for annual periods

beginning on or after 1 January 2012

The amendments do not contain any transitional provisions,

which means that they need to be applied retrospectively in

accordance with HKAS 8, except if retrospective application

is impracticable

88 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Disclosures

Disclose the impact of retrospective application, including:

Nature and description

Impact in current and prior periods presented for each line

item affected

Impact on earnings per share (basic and diluted) (HKAS

8.28)

Disclose judgments made by management that have had the most

significant effect on the financial statements (HKAS 1.122)

HKAS 8

89 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Disclosure (cont.)

Present a statement of financial position as at the beginning of the

earliest comparative period for a change in accounting policy

adopted retrospectively or retrospective restatements /

reclassifications (HKAS 1.10(f))

e.g., if the amendments are adopted early for a December year

end entity. Present a statement of financial position as at

31 December 2012 31 December 2011 1 January 2010

90 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Disclosure (cont.)

(for a listed entity) Adjust the 5 year financial summary included

in the annual report presented under para 19 of Appendix 16 /

GEM 18.33.

When an entity has not applied the amendments (because they

have been issued but are not yet effective), disclose:

This fact

Known or reasonably estimable information relevant to

assessing the possible impact in the period of initial

application (HKAS 8.30)

91 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Disclosure (cont.)

• When it is impracticable to adjust comparative information,

disclosure such circumstances and a description of how and

from when the change in accounting policy has been applied

(HKAS 8.28(h))

92 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.

Thank you for your

attention

93 © Hong Kong Institute of Certified Public Accountants Ltd, 2013. All rights reserved.