A Process for the Portfolio Management

10

mis e the por tfol io’ s func tional and fina ncial value to the business. Keywor ds : po rt foli o ma nagement , corpor at e real estate ma nagement , process, property management INTRODUCTION A cor porate rea l est ate (CRE) por tfolio can be viewed from three perspectives: — as a financial asset (or liability) of the corporation; — as a real estate market asset (or liability); and — as an operational asset that is a factor of production. A significant number of corporations deal with each of these perspectives separately and ra re ly se ek to ma na ge al l of th em to ge th er for th e gr eater good of the organisation. There is a similar tendency to manage as sets on a ‘one-o ff ’ basis, us ua ll y to fac ilitate ope rations or undertake trans- ac tion s. Once the as se t ba se reac he s a cert ain cr it ical mass , however, this in- cremental approach fails to maximise the portf olio’s funct iona l and fina ncial value to the company. (The point at which this criticality occurs will vary by organisation, Barry Var coe is responsi bl e for st rategi c development wi thin Jo hnson Co nt ro ls, Inc. Integ rated Faci lity Mana gemen t. This include s research & development, and leadership of the Int ernati ona l Per for man ce Man age ment Uni t, whi ch col lat es and ana lys es worki ng env iro n- ment quality , performance and technical knowledge. The unit was awarded the IDRC Best Practices Award in the Decision Suppor t category in 1997. Barry lives in England and is a Fellow of both the Roy al Ins tit utio n of Chartered Sur vey ors and the British Institute of Facilities Manage- ment. He has many years’ experience in building eco nomics , real est ate and faci lit ies man age- ment. A BSTRACT The paper ident i fies the nee d for a port fol io ap pr oa ch to the manage ment of re al estate assets, and se ts out it s key co mpone nts as a ‘macr o’ level proce ss. Portf olio manageme nt is positioned within an overall model of the corp orate real es tate function, fr om which a de finition is develo pe d. The main ge neric components of real estate portfolio management are described, and the most significant findings from a survey of current practices among a group of corporate organisations are presented. The paper conc lud es that in overall te rms a more robust approach to the portfolio manage- ment of real estate assets is required to maxi- A proces s for the portfolio management of real estate assets Barry Varcoe Received (in revised form): 24th December, 1999 Mr Barry Varcoe, Director of Strategic Development, Johnson Controls, Inc., 2 The Briars, Waterberry Drive, Waterlooville, Hants PO7 7YH, UK; Fax: 02392 230501; e-mail: Barry.J.V [email protected] Journal of Corporate Real Estate Volume 2 Number 2 Page 113 Journal of Corporate Real Estate Vol. 2 No. 2, 2000, pp. 113–122. Henry Stewart Publications, 1463-001X

-

Upload

brainy12345 -

Category

Documents

-

view

213 -

download

0

Transcript of A Process for the Portfolio Management

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 1/10

mise the portfolio’s functional and financial

value to the business.

Keywords: portfolio management,

corporate real estate management,

process, property management

INTRODUCTION

A corporate real estate (CRE) portfolio

can be viewed from three perspectives:

— as a financial asset (or liability) of the

corporation; — as a real estate market asset (or

liability); and

— as an operational asset that is a factor of

production.

A significant number of corporations deal

with each of these perspectives separately

and rarely seek to manage all of them

together for the greater good of the

organisation.

There is a similar tendency to manage

assets on a ‘one-off’ basis, usually to

facilitate operations or undertake trans-

actions. Once the asset base reaches a

certain critical mass, however, this in-

cremental approach fails to maximise the

portfolio’s functional and financial value

to the company. (The point at which this

criticality occurs will vary by organisation,

Barry Varcoe is responsible for strategic

development within Johnson Controls, Inc.

Integrated Facility Management. This includes

research & development, and leadership of the

International Performance Management Unit,

which collates and analyses working environ-

ment quality, performance and technical

knowledge. The unit was awarded the IDRC

Best Practices Award in the Decision Support

category in 1997.

Barry lives in England and is a Fellow of both

the Royal Institution of Chartered Surveyors

and the British Institute of Facilities Manage-

ment. He has many years’ experience in buildingeconomics, real estate and facilities manage-

ment.

A BSTRACT

The paper identifies the need for a portfolio

approach to the management of real estate

assets, and sets out its key components as a

‘macro’ level process. Portfolio management is

positioned within an overall model of the

corporate real estate function, from which a

definition is developed. The main generic

components of real estate portfolio management

are described, and the most significant findings

from a survey of current practices among a

group of corporate organisations are presented.

The paper concludes that in overall terms a

more robust approach to the portfolio manage-

ment of real estate assets is required to maxi-

A process for the portfolio management

of real estate assets

Barry Varcoe

Received (in revised form): 24th December, 1999

Mr Barry Varcoe, Director of Strategic Development, Johnson Controls, Inc., 2 TheBriars, Waterberry Drive, Waterlooville, Hants PO7 7YH, UK;Fax: 02392 230501; e-mail: [email protected]

Journal of Corporate Real Estate Volume 2 Num

Pag

Journal of Corporate Real Estat

Vol. 2 No. 2, 2000, pp. 113–12

Henry Stewart Publications,

1463-001X

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 2/10

depending upon the resource and skill

levels available within the CRE team;

the scale, number, geographic spread and

diversity of the properties; and the overall

size of the portfolio.) Little has been doneto adapt portfolio-wide concepts to cor-

porate real estate because it is expensive

and time-consuming for any one or-

ganisation to do so. The subject is broad,

the analysis involved can become com-

plex, and if it is not done in an or-

derly and modular way it can be dif ficult

to develop and update. It is surpris-

ing that a ‘systems’ answer has not yet

been created, but perhaps the projected

size and specialist nature of the potential

market for such products and serviceshave tended to discourage those vendors

who consider it before they even start.

In response to this need a group

of leading corporate real estate or-

ganisations, service providers, industry

specialists and university researchers in the

USA formed the Corporate Real Estate

Portfolio Alliance.1 The goal of the

Alliance was jointly to develop a portfolio

management approach that links a cor-

poration’s real estate portfolio to its overallstrategy and financial performance. Com-

mencing in September 1998, the research

focused on a number of areas, including

finance and analysis, process and tech-

nology, performance measurement, and

strategy and occupancy needs. The work,

which was completed at the end of April

1999, was considered by the participants

to have achieved significant advances in

several of these areas.

This paper focuses on the findings of

the research with respect to the process of

portfolio management. It identifies the

need for a more robust approach to the

portfolio management of corporate real

estate, clarifies its scope and its place

within the overall real estate function, and

then proposes an overall process for its

main components and activities.

THE NEED FOR A PORTFOLIO

APPROACH

Since 1993 the changing opinions of

leading real estate practitioners have been

collated and documented by the An-nual Survey of Corporate Real Estate

Practices.2 The work has established

many strong trends regarding key issues

and practices. One of these relates to

the importance placed upon portfolio

management as a discipline. The survey,

which is completed using a self-adminis-

tered questionnaire, in one section asks

respondents to indicate (using a 1 – 5 scale

measuring least important to most impor-

tant) the knowledge and skills crucial to

corporate real estate management in thefuture, from a list of 34 options. Over the

entire seven-year period the perception

that real estate portfolio management

is one of the most crucial areas of

knowledge and skill for corporate real

estate management in the future has not

changed (Figure 1).

Portfolio management has consistently

been one of the top three learning issues.

Furthermore, when the other two subjects

— strategic planning and a closer un-derstanding of the organisation’s business

— are considered, it can be seen that

they too are closely aligned to portfolio

management. The fact that these issues

have remained so important to learn about

in the future for seven years suggests that the

corporate real estate profession has not

made many advances in developing under-

standing in these areas. The comparative

scarcity of literature on the subject and the

infrequency of its discussion at the leading

industry conventions and seminars tend to

confirm this observation.

THE OVERALL CRE FUNCTION AND

PORTFOLIO MANAGEMENT

DEFINITION

In-depth analysis of CRE within the

A process for the portfolio management of real estate assets

Page 114

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 3/10

the Alliance for some of these activities are

set out in Table 1.

Once this asset perspective has been put

in place, going one step further provides

an aggregation for the overall portfolio,

which seeks to provide organisational

benefits above those achieved from the

management of assets individually. It is at

this strategic level that CRE is also bestplaced to look beyond its own activities

and consider their purpose — how best to

support the business of the corporation.

It also provides the logical interface

with other components of the corpora-

tion’s infrastructure, such as technology,

human resources and finance, an approach

being championed by the IDRC through

their Corporate Infrastructure Resource

management (CIR ) initiative.

This logical hierarchy of relationships

can be represented graphically, as shown

in Figure 2. In considering this structure

it is important to recognise that, although

it is based on the observation of current

practice, no one organisation is likely to

be performing all aspects in a robust way.

It therefore needs to be considered as a

model to be aspired to in the future,

Alliance member organisations enabled a

clear picture of corporate real estate, and of

the scope of portfolio management within

it, to emerge. Looked at logically, at its most

strategic CRE has a responsibility to its

organisation’s business to provide it with

effective, ef ficient and economic working

environments and other strategic real

properties. At its most tactical CRE has aresponsibility to deliver and operate those

working environments and other assets.

Somewhere in between those extremes lie

a myriad of functional activities, including

facility management, project management,

design and occupancy planning, property

management and property transactions.

There is also a need, however, to aggregate

the combined effect of those functional

activities into an overall asset-by-asset

perspective. This enables effective manage-

ment of the overall working environment

provided and its economic consequences,

and should allow management to achieve

significant organisational benefits above

those derived from the individual func-

tional activities (which, left to their own

devices, tend to be management and

information ‘silos’). The definitions used by

Figure 1 Annual

Survey of CRE

Practices

V

Pag

Organisations business

Portfolio management

Strategic planning

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 4/10

rather than the current state of the best

exemplars. (It should also be noted that

the model does not necessarily attempt to

represent how a CRE organisation should

be operationally structured.)This approach to understanding the

place and role of portfolio management

enabled a definition to be established.

After several iterations influenced by the

ongoing research activities, the following

established itself for the purposes of the

Alliance:

‘Corporate Real Estate Portfolio

Management: managing real properties

as a group in order to achieve greater

corporate benefits from them as

productive working environment as-

sets, financial assets and strategic assets,

above the benefits derived from

managing them individually.’

The most significant component of this

definition is arguably the last phrase —

requiring the portfolio management func-

tion to build on the other components of

CRE to deliver enhanced value to the

corporation.

PORTFOLIO MANAGEMENT

COMPONENTS

The interrogation and documentation of

the existing CRE practices within the

member organisations allowed the Al-

liance research team to identify the main

components and characteristics embraced

by portfolio management. These are rep-

resented graphically in Figure 3, which

identifies four logical phases:

— Inputs — which identify the ‘amount’

of the real estate portfolio (existing and

projected);

— Analysis — which considers the op-

tions available in providing it;

— Outcomes — which determine the

most beneficial options and establish

succinct ‘deliverables’;

A process for the portfolio management of real estate assets

Page 116

Table 1: Alliance definitions of CRE activities

Component De finition

Service delivery management The management and administration of resources engaged in thedelivery of specified service(s).

Facility management The practice of coordinating the physical workplace with the people

and work of the organisation. It integrates the principles of business

administration, architecture and the behavioural and engineering

sciences.

Functionality Being suitable for a particular use or function.3 (Note: in using this

definition it was recognised that functionality had application to all

aspects of CRE, but when analysing the key relationships its role in

linking use, design and asset management was seen to be the most

significant.)

Property management The management and administration of individual legal interests in

property(s), both from an occupier and landlord perspective.

Asset management The management of individual building assets to maintain their

ongoing operational and financial value.

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 5/10

new knowledge to enable and further

CRE and portfolio management ob-

jectives (ie how to do things better);

— Policy/guidelines/standards — the

rules by which the portfolio manage-

ment and overall real estate function

will operate;

— Financial analysis — analysing all

financial impacts the portfolio can

potentially have on the organisation;

— Risk analysis — assessing the risk ex-

posures and risk attitudes so that the

portfolio that is best for the organisa-

tion in overall terms is pursued;

— Comparisons, modelling and scenario

planning — bringing together all of

the informational components to un-

— Management — which makes sure that

the ‘deliverables’ are achieved in the

most effective and ef ficient manner.

Within each of the phases there are

several individual components, the main

purposes of which are as follows:

— (Long-term) demand forecasting —

identifying the needs of the occupying

organisation;

— Portfolio inventory — a register of all

of the buildings within the portfolio,

together with key information regard-

ing their size, legal status and use (i.e.

what is currently available);

— Research — the structured pursuit of

Figure 2 A model

of corporate real

estate

V

Pag

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 6/10

derstand better the gaps between whatis or can be available and what is or

may be required, and how best to

proceed to close those real or potential

gaps;

— Improvement initiatives — the iden-

tification and planning of pan-

portfolio initiatives of improvement,

not related to specific assets;

— Change planning — the identifica-

tion and planning of necessary changes

within the portfolio with respect to

individual or groups (or all) of assets;

— Budgetary management — financial

planning which shows in detail how

much money is available, how it is

to be spent and for what purpose

(derived from improvement initiatives

and change planning) within a certain

prescribed time-frame;

— Performance measures — the expres-sion of goals or achievements using

numbers, to motivate behaviour lead-

ing to improvement;

— Chargeback/allocations — the prac-

tice of charging users of the

portfolio’s working environments for

the resources that they consume.

CURRENT PRACTICE

The identification of the major individual

components of portfolio management

provided a basis for a more objective

assessment of current practice. Each was

expanded into a list of characteristics or

practices, which were compiled into a

questionnaire format. Each member CRE

organisation then completed the question-

naire to indicate the degree of sophistica-

Figure 3 Portfolio

management:

phases and

components

A process for the portfolio management of real estate assets

Page 118

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 7/10

— Capital returns analysis

— Exit strategies

— Improvement initiatives

The deficiencies in these areas were

mostly associated with the complete

absence of the activity, or its practice only

in isolated cases using ad hoc and

incomplete models. This is perhaps not

surprising, as the list contains most, if not

all, of the components that represent thegreatest complexity from a specialisation

and modelling point of view. Most are a

response to the more complex world of

business: an attempt to gain an im-

proved insight into the ‘futures’ that may

transpire, and the decisions that provide

the best outcomes and flexibility across

the most likely of them. They therefore

take time and knowledge to accomplish

properly, especially the first time they are

attempted. In today’s time and resource

compressed world there is therefore a

constant temptation to miss such activities

out, even if they offer significant potential

benefits, and instead to carry on existing

practices that arguably amount to no

more than educated guesses based on one

‘future’ extrapolated from the past.

In addition to the components of

tion and use each component had within

their normal activities. They identified for

each characteristic:

— whether it was carried out or not; and,

if ‘ yes’,

— whether it was a formal process or an

ad hoc action; and

— whether it was deployed across the

entire portfolio, to selected groups

within the portfolio (eg individualbusiness groups, regions or countries)

or just to individual buildings.

The survey clearly identified the com-

ponents of portfolio management that

were the strongest and the most mature

and also (perhaps more significantly) those

that were weakest and most in need of

improvement. At the overall phase level,

‘inputs’ and ‘management’ were much

stronger and more robust than ‘outcomes’

and ‘analysis’, the latter being the weakest

by a significant margin. This can be seen

from the following list of the weakest

individual components:

— Comparisons, modelling and scenario

planning

— Risk analysis

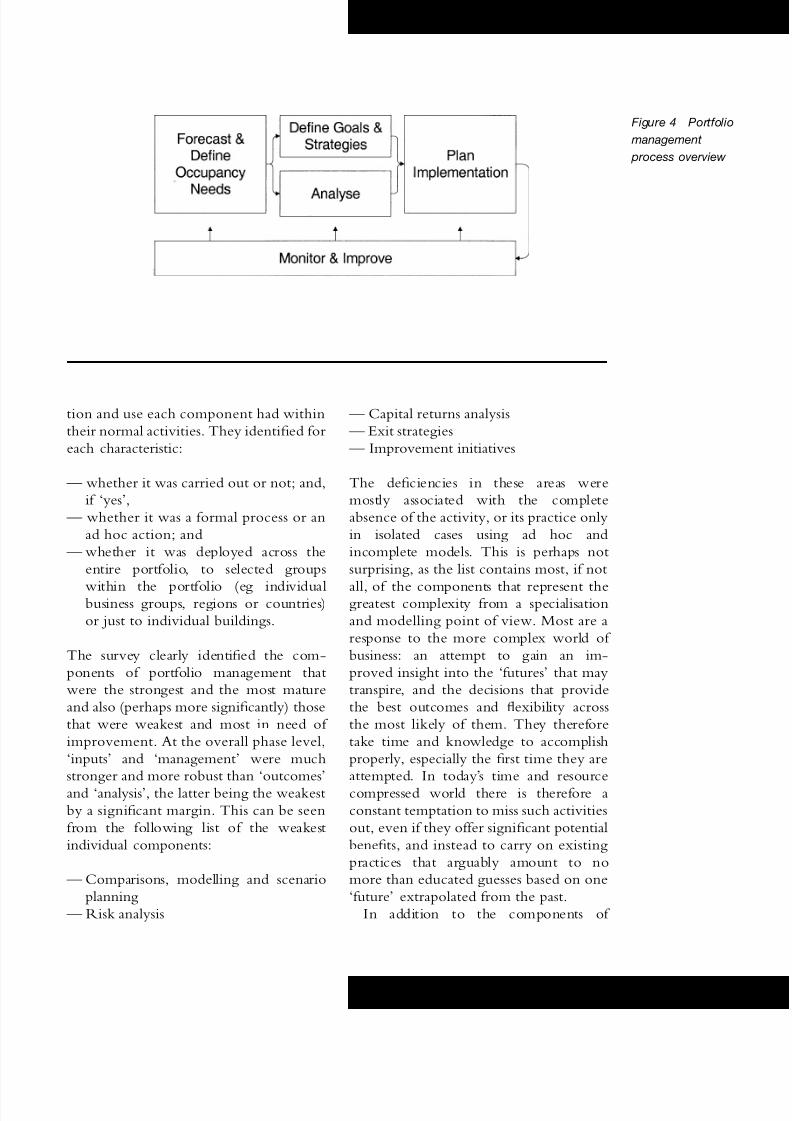

Figure 4 Portfolio

management

process overview

V

Pag

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 8/10

portfolio management, the survey also

collected similar information about other

aspects of CRE that have an important

interface with portfolio management.

Unsurprisingly all of the more tactical

individual management functions, such as

facility and property management, were

identified as being mature, but among

these asset management was compara-

tively weak, which is significant given its

important role as a ‘feeder ’ of information

to portfolio management. The ‘silo’ effect

of the individual management functions

was clearly influential in preventing the

complete and holistic management of

assets.

A PORTFOLIO MANAGEMENT

PROCESS

Given the scope, complexity and

variability of the portfolio management

function within CRE (let alone the

similar characteristics of corporations

overall), it is probable that there is no one

overall process that can be consistently

applied. There is nevertheless a value in

attempting to understand more about the

logical relationships involved, and to see

how the functional components pre-

viously identified can be combined into

practical activities.

The research proceeded to focus on this

issue, commencing with a strategic view

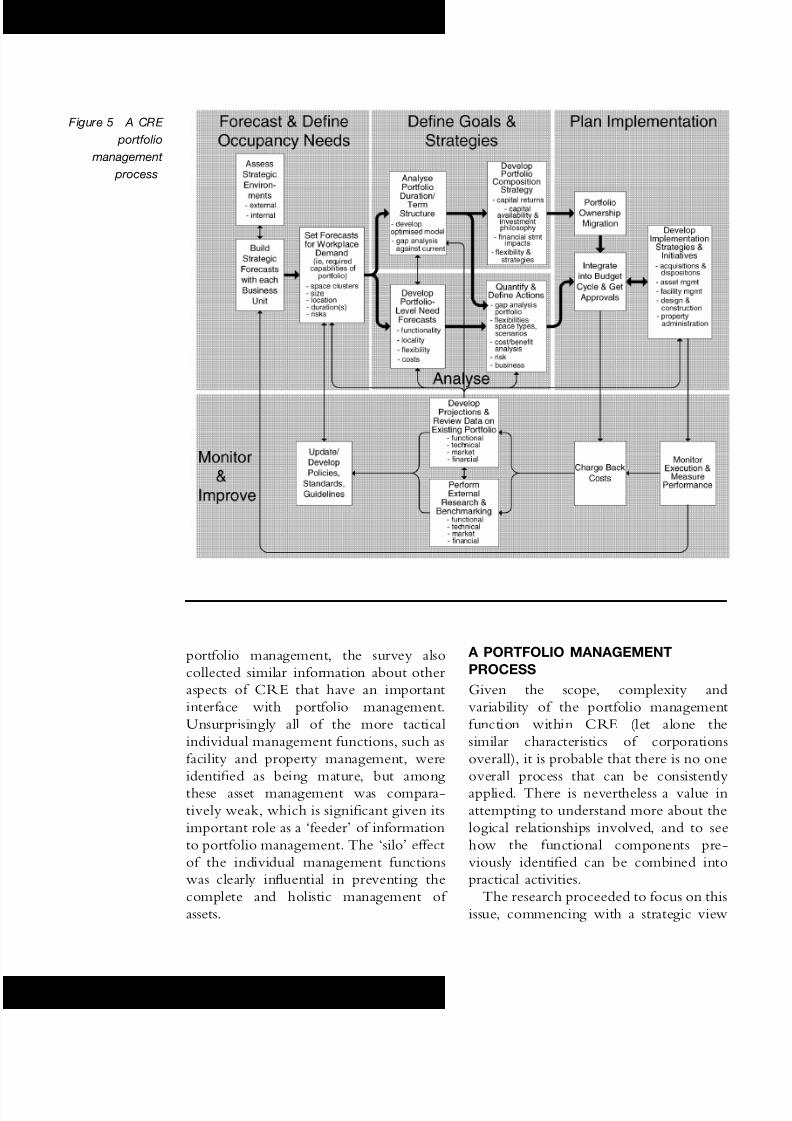

Figure 5 A CRE

portfolio

management

process

A process for the portfolio management of real estate assets

Page 120

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 9/10

entails and how all of its potential com-

ponents and activities can interrelate. At

least from that basis the inevitable short-

cuts and compromises are taken from a

position of comparative knowledge.Other parts of the Alliance research

began to demonstrate the significant

operational and financial benefits that

portfolio management can deliver to

CRE teams and their organisations. By

considering the definition and process

ideas introduced by the CRE Portfolio

Alliance, as outlined in this paper, it is

hoped that more professionals in CRE

will be able to start closing the gap

between potential and performance, and

as a result will thereby be able to deliver enhanced value to their organisations

from this vital facet of real estate.

REFERENCES

(1) The Corporate Real Estate Portfolio

Alliance is a consortium of 11 corporate

real estate organisations, and researchers

with various areas of expertise from

universities, industry groups and

corporate real estate service providers.

The member organisations comprise

BellSouth Telecommunications, Inc.,

Boeing Realty Corporation, Fidelity

Investments, Florida Power & Light,

Microsoft Corporation, Pacific Gas &

Electric Co., State Farm Insurance Co.,

Sun Microsystems Inc., US General

Services Administration, US West, Inc.,

Washington Mutual, Inc. The researcher

members comprise Tom Bomba, Andrew

Light and Sven Pole of The McMahan

Group; Wade Fransson of CB Richard

Ellis; Barry Varcoe of Johnson Controls,Inc.; Kevin Deeble of TriNet Corporate

Realty Trust; Gerald Davis and Francoise

Szigeti of International Centre for

Facilities; Dr Joseph Gyourko and Dr

Yongheng Deng of Zell/Lurie Real

Estate Centre at Wharton; Dr Martha A.

O’Mara of Harvard Graduate School of

Design; and John McMahan of UC

of the problem. This resulted in the

expansion of the four component phases

into five main process phases, with the

reshaping and expansion of the two in-

itial ‘analysis’ and ‘outcomes’ phases intothree. These are shown in Figure 4. The

portfolio needs are forecast and defined,

overall goals and strategies are defined, the

options are analysed and understood, the

best option(s) are selected and planned

for implementation, and the whole is

monitored from a performance perspec-

tive to stimulate improvement and check

progress. Another difference at this level

is the lack of any management of the

actual delivery, this being the role of the

various functional activities.With this overall structure in place,

the original portfolio management com-

ponents were then combined into logical

groups of activity and their interrelation-

ships were identified. This resulted in a

more detailed ‘macro’ level process for

portfolio management, which is shown in

Figure 5. With this established, the chal-

lenge for the corporate members of the

Alliance has been to compare its com-

ponents, activities and relationships withthe analysis of their own current perfor-

mance, and from that to identify the

most significant and high-risk deficiencies.

With the capability gaps thus prioritised,

resources can then be planned to rectify

them, either internally or through third

parties.

CONCLUSION

It is unlikely that any one CRE team,

when undertaking its portfolio manage-

ment responsibilities, will follow such a

process as that introduced here from start

to finish. Almost inevitably events will

overtake action and compromises will be

made and short-cuts will be taken. It is

important to understand, however, what

the function of portfolio management

V

Pag

8/12/2019 A Process for the Portfolio Management

http://slidepdf.com/reader/full/a-process-for-the-portfolio-management 10/10

Berkeley Fisher Center for Real Estate.

(2) Annual Survey of Corporate Real Estate

Practices, University of Reading and

Johnson Controls, Inc.

(3) ASTM Standards on Whole Building

Functionality and Serviceability, ASTM

(1996).

Barry Varcoe, Johnson Controls, Inc. and

CRE Portfolio Alliance 1999.

A process for the portfolio management of real estate assets