A Presentation for IPTA: Chemical Tanker Market · PDF fileA Presentation for IPTA: Chemical...

30

A Presentation By A Presentation for IPTA: Chemical Tanker Market Analysis London, 12-13 March, 2013

Transcript of A Presentation for IPTA: Chemical Tanker Market · PDF fileA Presentation for IPTA: Chemical...

A Presentation

By

A Presentation for IPTA:

Chemical Tanker Market Analysis

London, 12-13 March, 2013

2

GLOBAL SHIPBROKING

MARKET RESEARCH

CONSULTANCY

INTEGRATED LOGISTICS SOLUTIONS

GENERAL AGENCY

Services :

Vision :

s & peri

Our vision is to offer unbounded thought and analysis to create safe, reliable and cost effective

bulk shipping and logistics solutions, putting us at the forefront of the industry's best practice.

Presence :

3

Contents

CONTENTS

Part 1. GDP Growth / Product Flows / Fleet Growth

Part 2. Freight Trends

Part 3. Industry Issues: - Impact of 18-22,999 Dwt (SS)

- Why Fewer Segregations

- Charter Party Terms

4

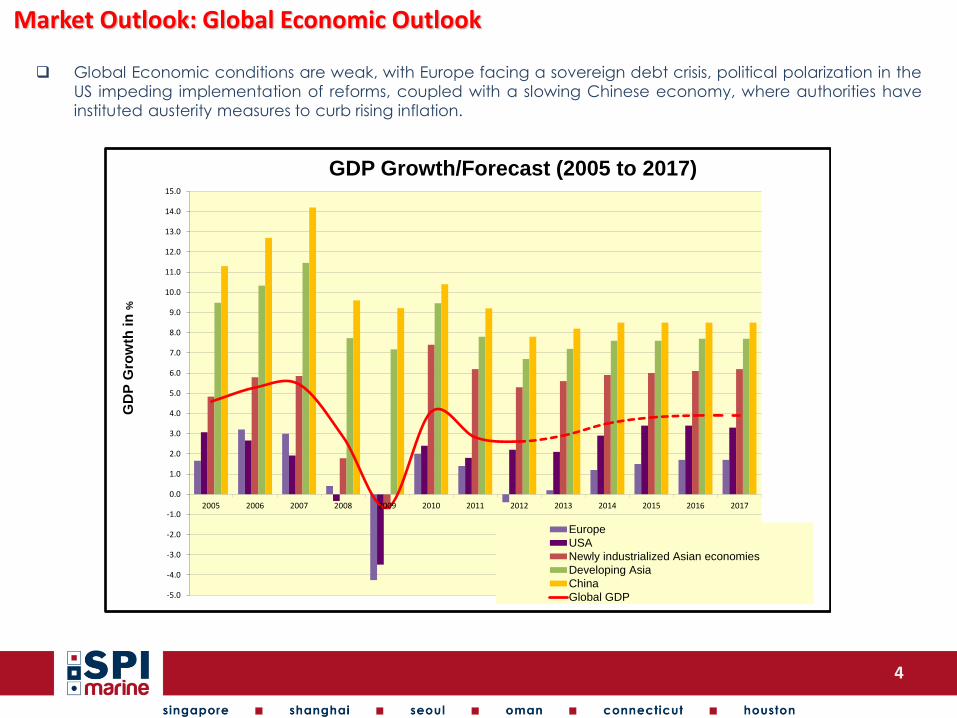

Market Outlook: Global Economic Outlook

Global Economic conditions are weak, with Europe facing a sovereign debt crisis, political polarization in the

US impeding implementation of reforms, coupled with a slowing Chinese economy, where authorities have

instituted austerity measures to curb rising inflation.

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

GDP Growth/Forecast (2005 to 2017)

Europe

USA

Newly industrialized Asian economies

Developing Asia

China

Global GDP

GD

P G

row

th in

%

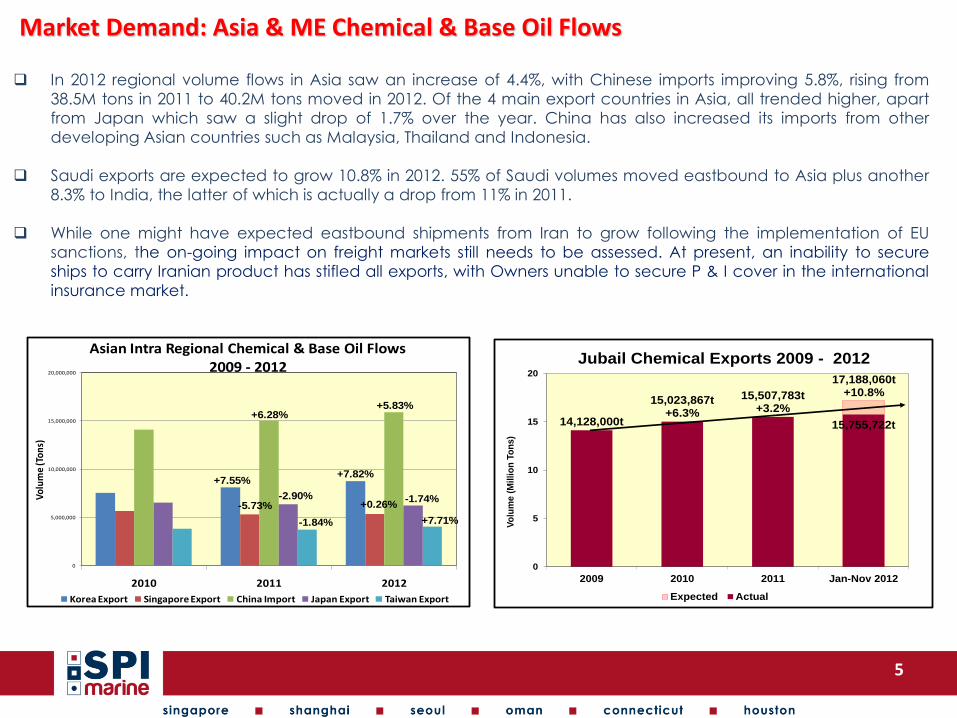

Market Demand: Asia & ME Chemical & Base Oil Flows

In 2012 regional volume flows in Asia saw an increase of 4.4%, with Chinese imports improving 5.8%, rising from

38.5M tons in 2011 to 40.2M tons moved in 2012. Of the 4 main export countries in Asia, all trended higher, apart

from Japan which saw a slight drop of 1.7% over the year. China has also increased its imports from other

developing Asian countries such as Malaysia, Thailand and Indonesia.

Saudi exports are expected to grow 10.8% in 2012. 55% of Saudi volumes moved eastbound to Asia plus another

8.3% to India, the latter of which is actually a drop from 11% in 2011.

While one might have expected eastbound shipments from Iran to grow following the implementation of EU

sanctions, the on-going impact on freight markets still needs to be assessed. At present, an inability to secure

ships to carry Iranian product has stifled all exports, with Owners unable to secure P & I cover in the international

insurance market.

0

5,000,000

10,000,000

15,000,000

20,000,000

2010 2011 2012

Vo

lum

e (T

on

s)

Asian Intra Regional Chemical & Base Oil Flows 2009 - 2012

Korea Export Singapore Export China Import Japan Export Taiwan Export

+7.55%

-5.73%

+6.28%

-2.90%

-1.84%

+7.82%

+0.26%

+5.83%

-1.74%

+7.71%

14,128,000t

15,023,867t+6.3%

15,507,783t+3.2%

15,755,722t

0

5

10

15

20

2009 2010 2011 Jan-Nov 2012

Vo

lum

e (

Mil

lio

n T

on

s)

Jubail Chemical Exports 2009 - 2012

Expected Actual

17,188,060t+10.8%

5

6

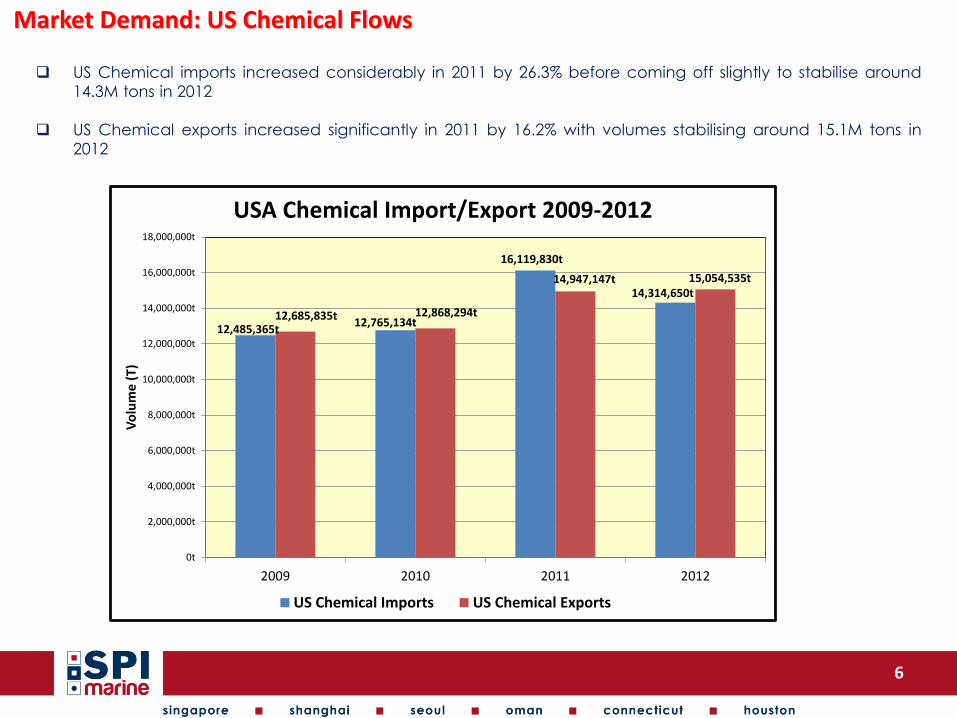

Market Demand: US Chemical Flows

US Chemical imports increased considerably in 2011 by 26.3% before coming off slightly to stabilise around

14.3M tons in 2012

US Chemical exports increased significantly in 2011 by 16.2% with volumes stabilising around 15.1M tons in

2012

12,485,365t12,765,134t

16,119,830t

14,314,650t

12,685,835t 12,868,294t

14,947,147t 15,054,535t

0t

2,000,000t

4,000,000t

6,000,000t

8,000,000t

10,000,000t

12,000,000t

14,000,000t

16,000,000t

18,000,000t

2009 2010 2011 2012

Vo

lum

e (

T)

USA Chemical Import/Export 2009-2012

US Chemical Imports US Chemical Exports

7

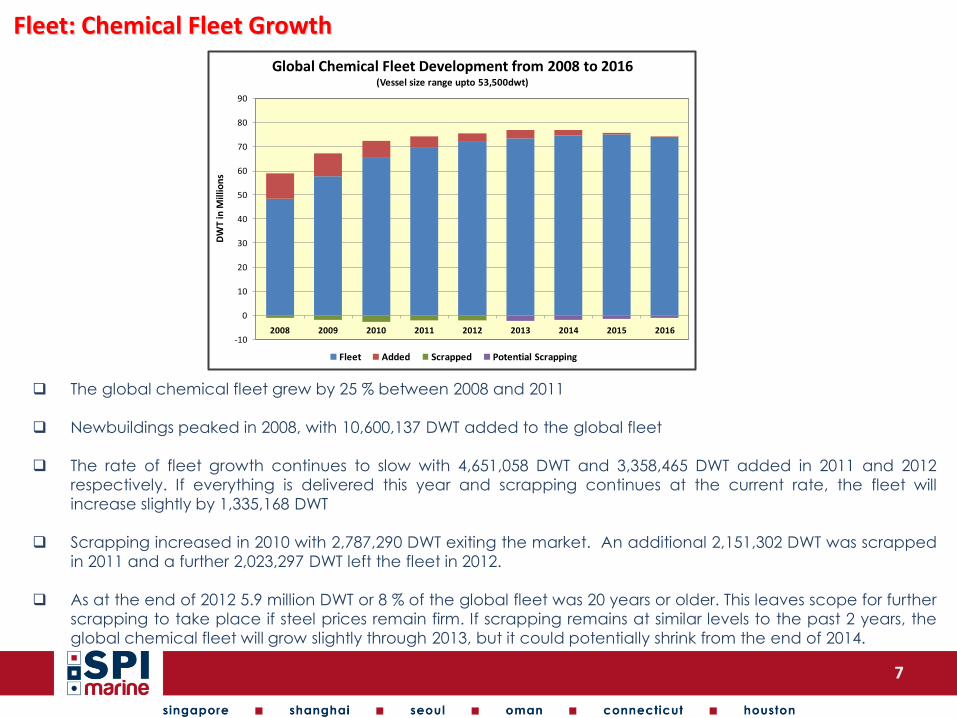

Fleet: Chemical Fleet Growth

The global chemical fleet grew by 25 % between 2008 and 2011

Newbuildings peaked in 2008, with 10,600,137 DWT added to the global fleet

The rate of fleet growth continues to slow with 4,651,058 DWT and 3,358,465 DWT added in 2011 and 2012

respectively. If everything is delivered this year and scrapping continues at the current rate, the fleet will

increase slightly by 1,335,168 DWT

Scrapping increased in 2010 with 2,787,290 DWT exiting the market. An additional 2,151,302 DWT was scrapped

in 2011 and a further 2,023,297 DWT left the fleet in 2012.

As at the end of 2012 5.9 million DWT or 8 % of the global fleet was 20 years or older. This leaves scope for further

scrapping to take place if steel prices remain firm. If scrapping remains at similar levels to the past 2 years, the

global chemical fleet will grow slightly through 2013, but it could potentially shrink from the end of 2014.

-10

0

10

20

30

40

50

60

70

80

90

2008 2009 2010 2011 2012 2013 2014 2015 2016

DW

T in

Mill

ion

s

Global Chemical Fleet Development from 2008 to 2016(Vessel size range upto 53,500dwt)

Fleet Added Scrapped Potential Scrapping

8

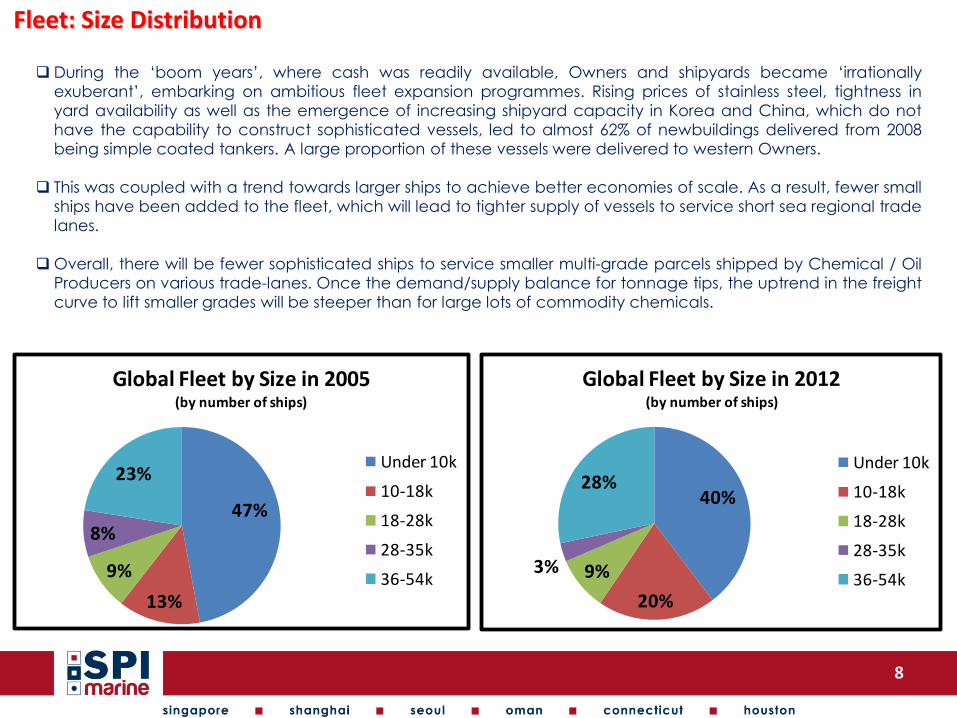

Fleet: Size Distribution

During the ‘boom years’, where cash was readily available, Owners and shipyards became ‘irrationally

exuberant’, embarking on ambitious fleet expansion programmes. Rising prices of stainless steel, tightness in

yard availability as well as the emergence of increasing shipyard capacity in Korea and China, which do not

have the capability to construct sophisticated vessels, led to almost 62% of newbuildings delivered from 2008

being simple coated tankers. A large proportion of these vessels were delivered to western Owners.

This was coupled with a trend towards larger ships to achieve better economies of scale. As a result, fewer small

ships have been added to the fleet, which will lead to tighter supply of vessels to service short sea regional trade

lanes.

Overall, there will be fewer sophisticated ships to service smaller multi-grade parcels shipped by Chemical / Oil

Producers on various trade-lanes. Once the demand/supply balance for tonnage tips, the uptrend in the freight

curve to lift smaller grades will be steeper than for large lots of commodity chemicals.

47%

13%

9%

8%

23%

Global Fleet by Size in 2005(by number of ships)

Under 10k

10-18k

18-28k

28-35k

36-54k

40%

20%

9%3%

28%

Global Fleet by Size in 2012 (by number of ships)

Under 10k

10-18k

18-28k

28-35k

36-54k

9

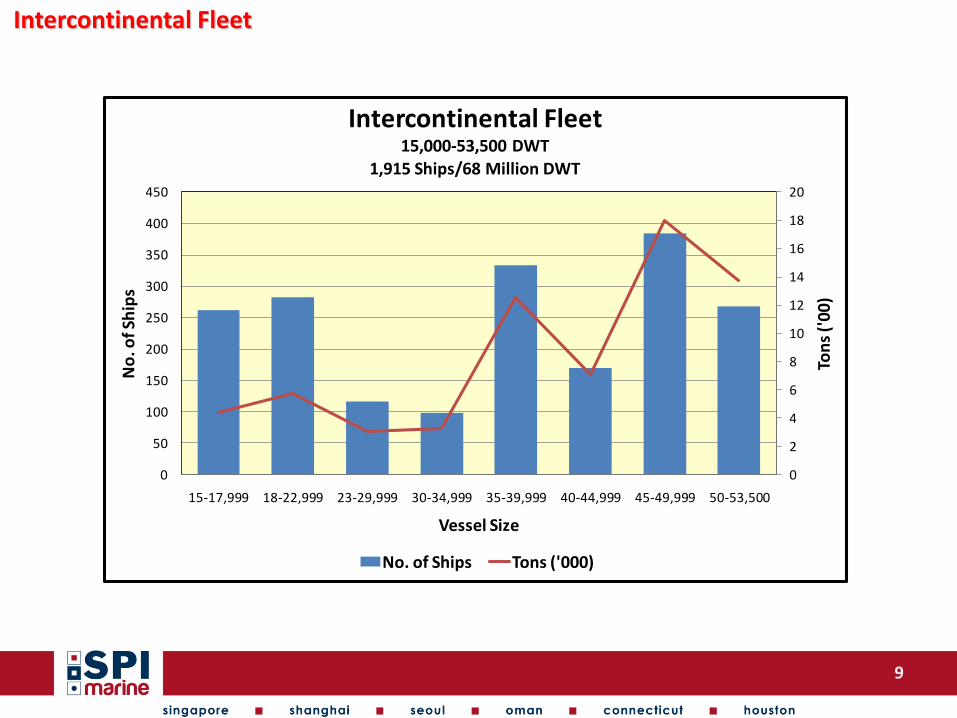

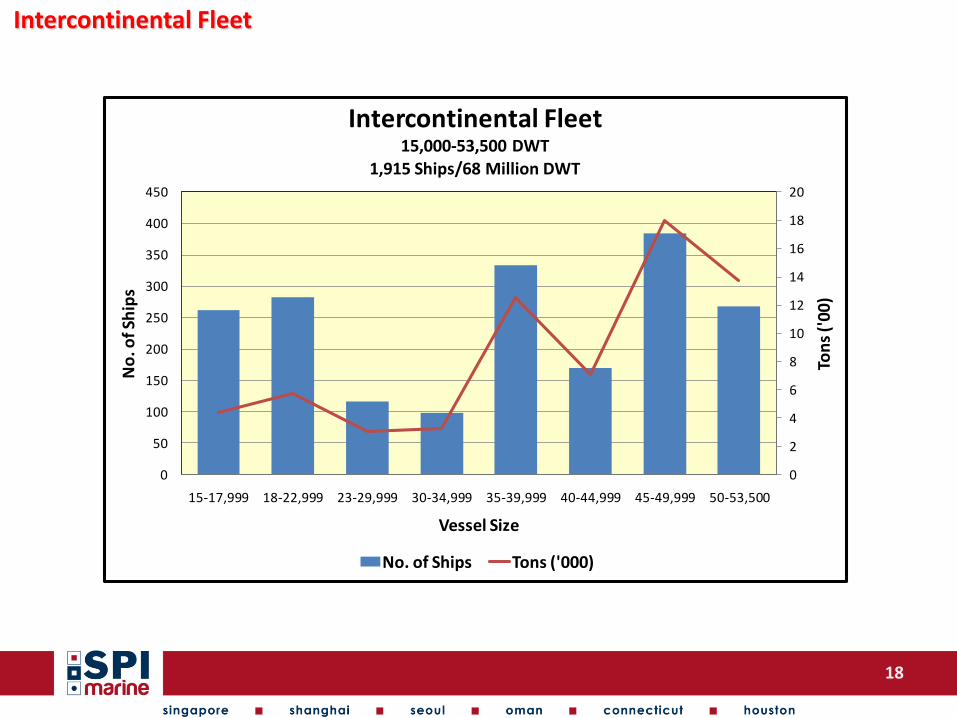

Intercontinental Fleet

0

2

4

6

8

10

12

14

16

18

20

0

50

100

150

200

250

300

350

400

450

15-17,999 18-22,999 23-29,999 30-34,999 35-39,999 40-44,999 45-49,999 50-53,500

Ton

s ('

00

)

No

. of S

hip

s

Vessel Size

Intercontinental Fleet 15,000-53,500 DWT

1,915 Ships/68 Million DWT

No. of Ships Tons ('000)

10

Freight Trends: Asian Trade Routes

$30.50

$32.00

$20.00

$22.00

$24.00

$26.00

$28.00

$30.00

$32.00

$34.00

Jan. 2012 Mar. 2012 May. 2012 Jul. 2012 Sep. 2012 Nov. 2012

Fre

igh

t R

ate

s U

S$

/T

Intra SE Asia Freight Trend

3,000t Singapore to Merak 3,000t Singapore to BKK

Jan. 2013 vs Dec. 2012 + 3.31%Jan. 2013 vs Jan. 2012 + 22.45%

$47.50

$53.50

$30.00

$34.00

$38.00

$42.00

$46.00

$50.00

$54.00

$58.00

Jan. 2012 Mar. 2012 May. 2012 Jul. 2012 Sep. 2012 Nov. 2012 Jan. 2013

Fre

igh

t R

ate

s U

S$

/T

SE Asia Northbound Freight Trend

3,000t Singapore to Kaohsiung 3,000t Singapore to M. China

Jan. 2013 vs Dec. 2012 + 2.03%Jan. 2013 vs Jan. 2012 + 16.08%

$50.50

$39.00

$41.00

$43.00

$45.00

$47.00

$49.00

$51.00

$53.00

Jan. 2012

Feb. 2012

Mar. 2012

Apr. 2012

May. 2012

Jun. 2012

Jul. 2012

Aug. 2012

Sep. 2012

Oct. 2012

Nov. 2012

Dec. 2012

Jan. 2013

Fre

igh

t R

ate

s U

S$

/T

Singapore to WC India Freight Trend

5,000t Singapore to Bombay

Jan. 2013 vs Dec. 2012 + 0%Jan. 2013 vs Jan. 2012 + 13.0%

$52.00

$78.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

$100.00

$110.00

Jan. 2012 Mar. 2012 May. 2012 Jul. 2012 Sep. 2012 Nov. 2012 Jan. 2013

Fre

igh

t R

ate

s U

S$

/T

Middle East Eastbound and Westbound Freight Trend

10,000t AG to M. China 10,000t AG to NW Europe

Westbound:Jan. 2013 vs Dec. 2012 + 0%Jan. 2013 vs Jan. 2012 + 2.0%

Eastbound:Jan. 2013 vs Dec. 2012 + 0%Jan. 2013 vs Jan. 2012 + 5.0%

11

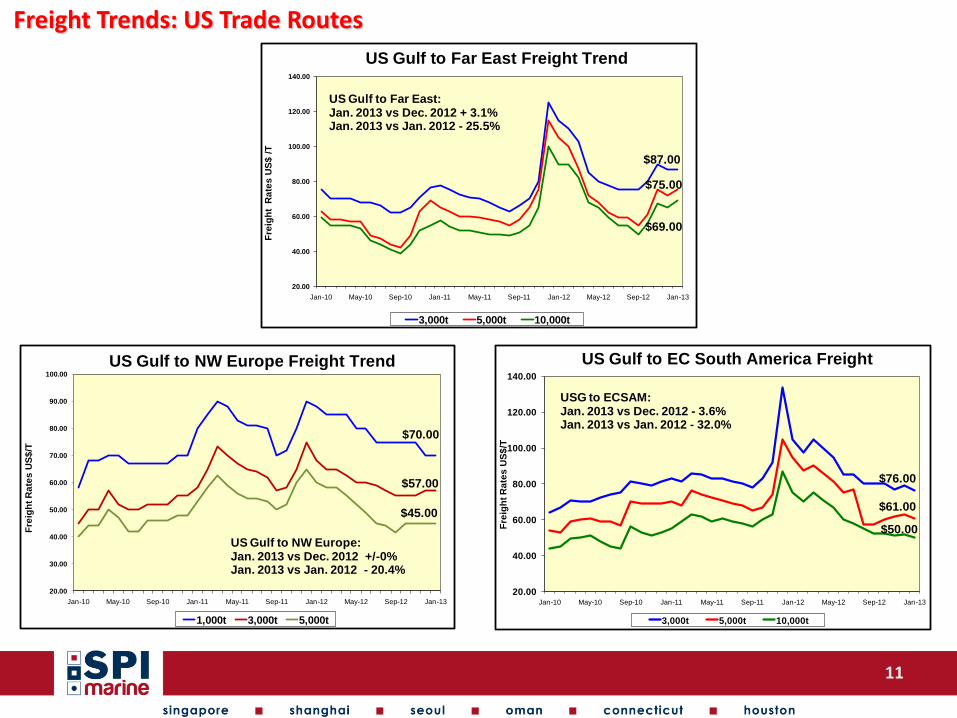

Freight Trends: US Trade Routes

$87.00

$75.00

$69.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13

Fre

igh

t R

ate

s U

S$

/T

3,000t 5,000t 10,000t

US Gulf to Far East Freight Trend

US Gulf to Far East:Jan. 2013 vs Dec. 2012 + 3.1%Jan. 2013 vs Jan. 2012 - 25.5%

$76.00

$61.00

$50.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13

Fre

igh

t R

ate

s U

S$

/T

3,000t 5,000t 10,000t

US Gulf to EC South America Freight

USG to ECSAM:Jan. 2013 vs Dec. 2012 - 3.6%Jan. 2013 vs Jan. 2012 - 32.0%

$70.00

$57.00

$45.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13

Fre

igh

t R

ate

s U

S$

/T

1,000t 3,000t 5,000t

US Gulf to NW Europe Freight Trend

US Gulf to NW Europe:Jan. 2013 vs Dec. 2012 +/-0%Jan. 2013 vs Jan. 2012 - 20.4%

12

Freight Market Outlook: Demand versus Supply Downward Market Pressure:

The global economy remains weak and analysts project the world is unlikely to return to the rate of economic

activity seen before the financial crisis until 2014 or possibly later.

China has overtaken Japan as the second largest economy in the world. However, China put in place

measures to avoid overheating at the beginning of the year (although we do expect to see stimulus to the

Chinese economy in 2013). According to the International Monetary Fund, Developing Asia is forecast to

grow by 6.7% in 2012, down from 8.2% last year, not least because of falling demand from key export markets,

such as the US and Europe.

Upward Market Pressure:

Global demand for petrochemicals continues to grow, especially in emerging markets, which are advancing

at a faster pace than other regions. Globally, demand for chemical shipping is expected to increase by 5% in

2012 and 5.7% in 2013, compared to a fleet growth of 2.3% and 2% in these two years.

China’s chemical demand is expected to increase annually by 1.5 times China’s GDP growth. Based on

current GDP expectations, demand is likely to increase by around 12% in 2013, drawing ships from the Intra SE

Asia trade.

During the last peak cycle, cheap debt and plentiful bank liquidity led to an order-book for chemical tankers

stretching into 2012. However, almost no newbuilding activity has taken place in the past 3 years. As Owners

and ship finance players contend with over-priced assets ordered during the last peak cycle, we are unlikely

to see a pick-up in newbuilding activity in the near term, despite significantly reduced values.

As a result, the Asian Fleet Growth could shrink from 2012, while global fleet growth will likely shrink only from

2013.

Operating costs remain at historically high levels, leading to a strong inducement for Owners to aggressively

seek freight improvements.

13

Freight Market Outlook: Demand versus Supply

Conclusion:

While rates are likely to remain subdued during the 1H of 2013, despite an uncertain demand outlook, we

expect freight rates will continue to recover into 2013, as the number of newbuilding deliveries dwindle, while

scrapping picks up.

Despite slowing GDP growth in Asia overall, we have continued to see volumes growing year-on-year, which

has allowed the market to absorb the glut of newbuildings that entered the market over the past 3 years,

with little negative impact on freight rates.

While freight rates have remained subdued over the seasonally slower summer months of 2012, despite an

uncertain demand outlook, we expect Asian freight rates to continue to show a steady recovery from the

end of 2012 and into 2013.

As the number of newbuilding deliveries dwindle, while scrapping picks up, the freight market is expected to

emerge from the down-cycle that started in 2008.

Once the demand/supply balance for chemical tankers tips and the global economy recovers, we are likely

to see freight rates increase strongly as current time-charter equivalent returns remain well below levels

needed for investments made during the peak years to become profitable. Due to relatively fewer

smaller/sophisticated ships, the trend is likely to be steeper for short sea shipments and for shipments of smaller

grades or products with special handling requirements.

The coming 12 months will remain very challenging for Owners, who will have to rely on the support of banks

to survive and, given recent examples (Dorval, BLTC and EOS), it is reasonable to assume that some may not.

14

Freight Market Outlook: Swing Factors

Potential Swing factors, could pull the market in different directions:

Demand

Threat of a double dip or further economic decline in Europe and the US due to high debt, unemployment and reduced consumption in the developed world.

High oil and commodity prices could harm a sustainable economic recovery

War/unrest in the Middle East ‘Arab Spring’ or Natural disasters like Japan’s Earthquake

Slowing growth and weakness in the Chinese banking system, as propagated by the ‘Chinese Bears’

Supply

Rebalancing of tonnage: If freight demand in Asia picks up, while markets in other regions remain dull, tonnage may be drawn to the region.

15

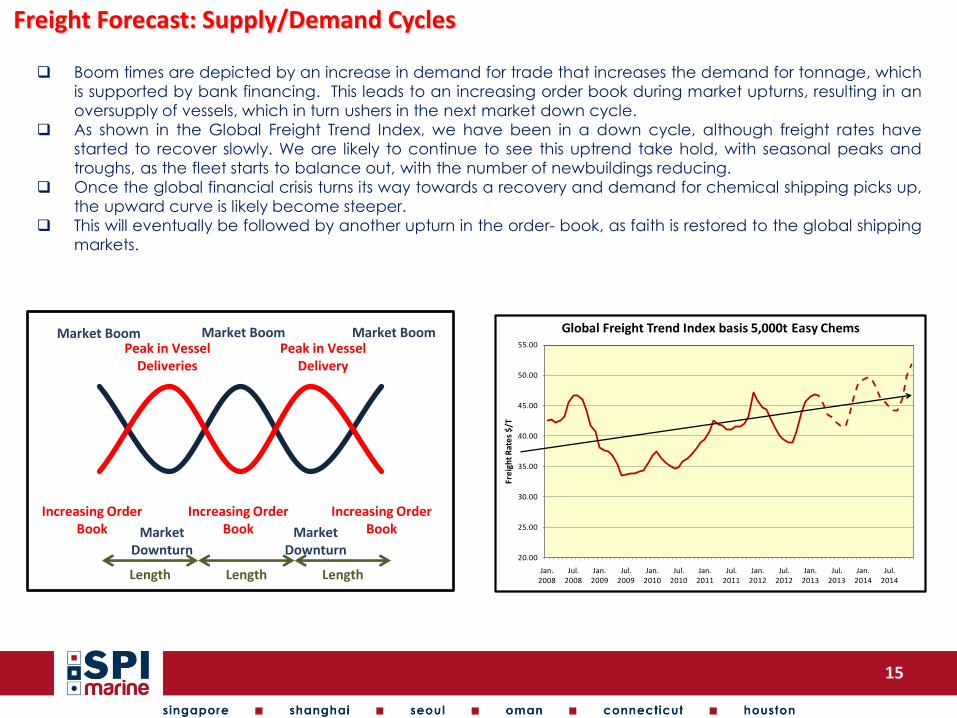

Freight Forecast: Supply/Demand Cycles

Boom times are depicted by an increase in demand for trade that increases the demand for tonnage, which

is supported by bank financing. This leads to an increasing order book during market upturns, resulting in an

oversupply of vessels, which in turn ushers in the next market down cycle.

As shown in the Global Freight Trend Index, we have been in a down cycle, although freight rates have

started to recover slowly. We are likely to continue to see this uptrend take hold, with seasonal peaks and

troughs, as the fleet starts to balance out, with the number of newbuildings reducing.

Once the global financial crisis turns its way towards a recovery and demand for chemical shipping picks up,

the upward curve is likely become steeper.

This will eventually be followed by another upturn in the order- book, as faith is restored to the global shipping

markets.

Increasing Order Book Market

Downturn

Increasing Order Book

Increasing Order Book Market

Downturn

Peak in Vessel Deliveries

Peak in Vessel Delivery

Market Boom Market Boom Market Boom

Length Length Length

20.00

25.00

30.00

35.00

40.00

45.00

50.00

55.00

Jan. 2008

Jul. 2008

Jan. 2009

Jul. 2009

Jan. 2010

Jul. 2010

Jan. 2011

Jul. 2011

Jan. 2012

Jul. 2012

Jan. 2013

Jul. 2013

Jan. 2014

Jul. 2014

Fre

igh

t R

ate

s $

/T

Global Freight Trend Index basis 5,000t Easy Chems

16

Freight Market Outlook: Time Charter Rates

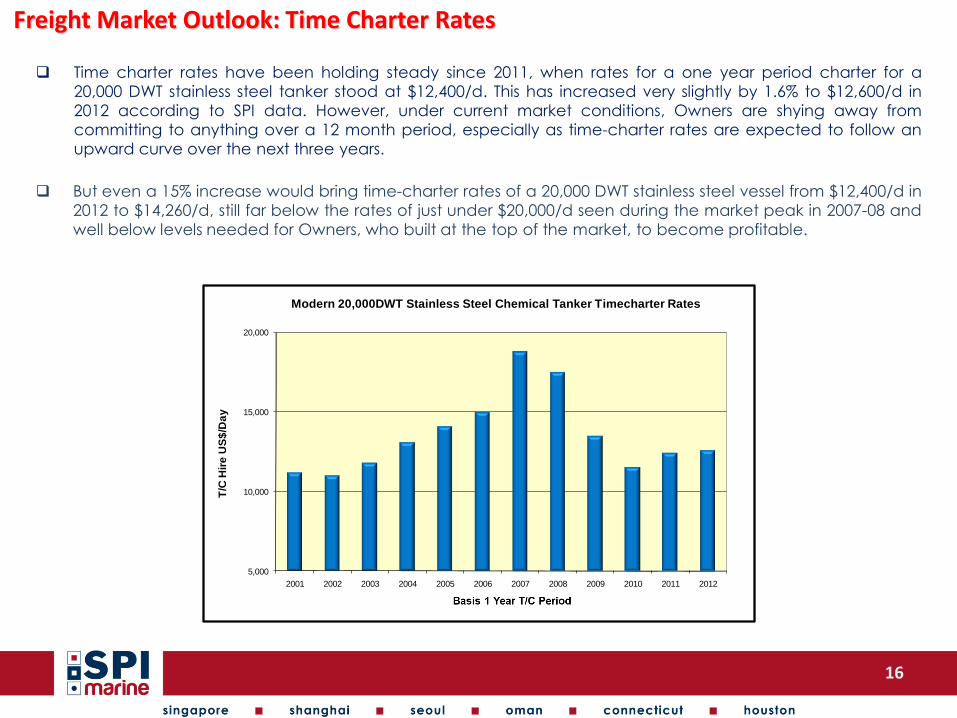

Time charter rates have been holding steady since 2011, when rates for a one year period charter for a

20,000 DWT stainless steel tanker stood at $12,400/d. This has increased very slightly by 1.6% to $12,600/d in

2012 according to SPI data. However, under current market conditions, Owners are shying away from

committing to anything over a 12 month period, especially as time-charter rates are expected to follow an

upward curve over the next three years.

But even a 15% increase would bring time-charter rates of a 20,000 DWT stainless steel vessel from $12,400/d in

2012 to $14,260/d, still far below the rates of just under $20,000/d seen during the market peak in 2007-08 and

well below levels needed for Owners, who built at the top of the market, to become profitable.

5,000

10,000

15,000

20,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

T/C

Hir

e U

S$

/Da

y

Modern 20,000DWT Stainless Steel Chemical Tanker Timecharter Rates

17

Freight Market Outlook: Chemical Tanker Operating Costs

While the supply of tankers has outstripped demand for freight in recent years, high bunker prices have helped

to keep freight rates propped up.

Bunkers, which trend crude prices, remain at historical highs however from last summer bunkers came off quite

dramatically allowing Owners room for negotiation, but they have since picked up, although they have not

returned to the highs seen at the beginning of last year.

With freight earned in US Dollars, weakness of the US Dollar versus other currencies has further squeezed ship

owner margins.

OPEX costs for chemical tankers rose by over 21.8% from 2008 to 2012 and remain high.

Continued high fuel costs – 2013 average costs expected to be higher than 2012

Dry dock costs up 61.2%

Crewing up 20.5%

P and I premiums up 15%

Increases in port costs and canal dues

When the supply/demand balance shifts in favour of Owner/Operator we will likely see an aggressive surge to

move freight rates up.

18

Intercontinental Fleet

0

2

4

6

8

10

12

14

16

18

20

0

50

100

150

200

250

300

350

400

450

15-17,999 18-22,999 23-29,999 30-34,999 35-39,999 40-44,999 45-49,999 50-53,500

Ton

s ('

00

)

No

. of S

hip

s

Vessel Size

Intercontinental Fleet 15,000-53,500 DWT

1,915 Ships/68 Million DWT

No. of Ships Tons ('000)

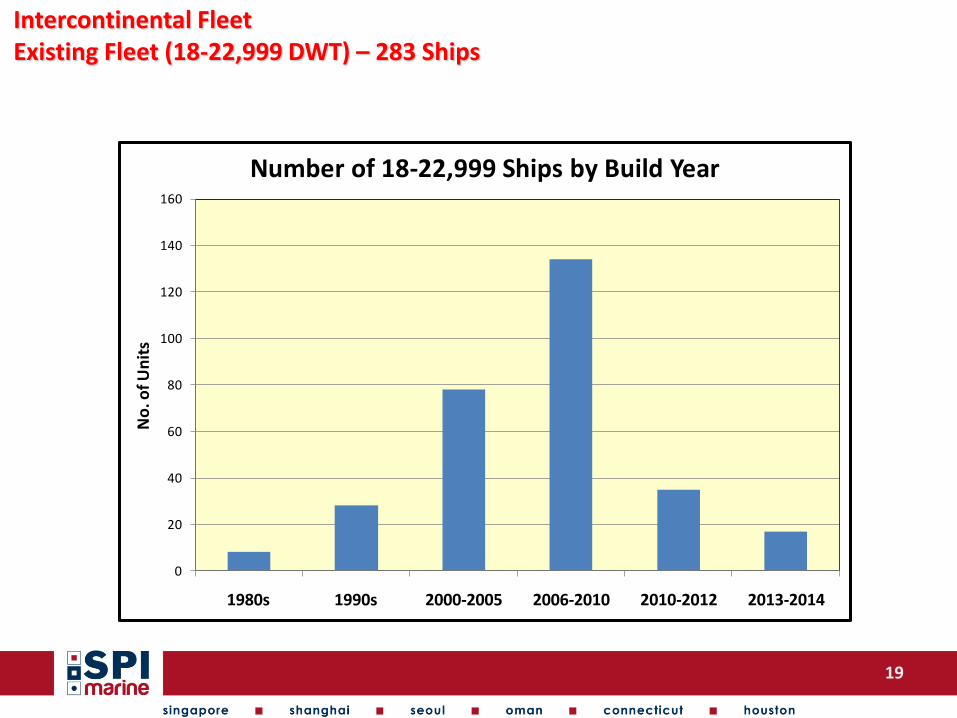

Intercontinental Fleet Existing Fleet (18-22,999 DWT) – 283 Ships

0

20

40

60

80

100

120

140

160

1980s 1990s 2000-2005 2006-2010 2010-2012 2013-2014

No

. of U

nit

s

Number of 18-22,999 Ships by Build Year

19

Intercontinental Fleet Existing Fleet (18-22,999 DWT) – 283 Ships

• 86% of existing ships in this size range built between 2000-2012

• 70% Stainless Steel – 30% Coated

• 55 ships in this size range were built 1980s through to 1990s. Assuming this size ship was a optimum size for trading and allowing for a generous growth of 7.5% in the number of ships built each year from 2000 through 2012 the fleet should have grown to about 141 ships

• With 283 existing units, this suggests considerable speculative building on the part of shipyards supported by Financial Institutions and Owners

• 204 units (72%) are 19-19,999 DWT

What was the love affair with this size of ship?

20

Intercontinental Fleet Existing Fleet (18-22,999 DWT) – 283 Ships

• Asian yards (particularly Japanese) accounted for approx. 76% of all ships built in this size range. Many of the Japanese yards were stretched to their limits with this size.

• Inert gas requirements by Solas/IMO (1986) could be avoided if ship was less than 20,000 DWT. However the cost savings in construction and operational costs alone could not have driven demand for this size.

• A number of respectable Owner / Operators have found trades where this size ship with stainless steel cargo tanks fit well. However, the ship is considered by many to be too large for many regional trades and too small for most intercontinental trades.

• Too many Owner/Operators are trading spot/prompt and given the flexibility of these ships have moved in and out of both regional and intercontinental trades seeking employment. The over capacity of these types of ships have contributed towards softening of spot freight rates which are highly influential on contract renewals.

21

Intercontinental Fleet Existing Fleet (18-22,999 DWT) – 283 Ships

0

10

20

30

40

50

60

70

80

90

Nordic/ Siva/

Womar

Allied/ Fairfield Chemical

Odfjell MTMM Tokyo Marine

Hansa BLT Chembulk

MISC NAVIG8 Stolt Zodiac

No

. of

Ship

s

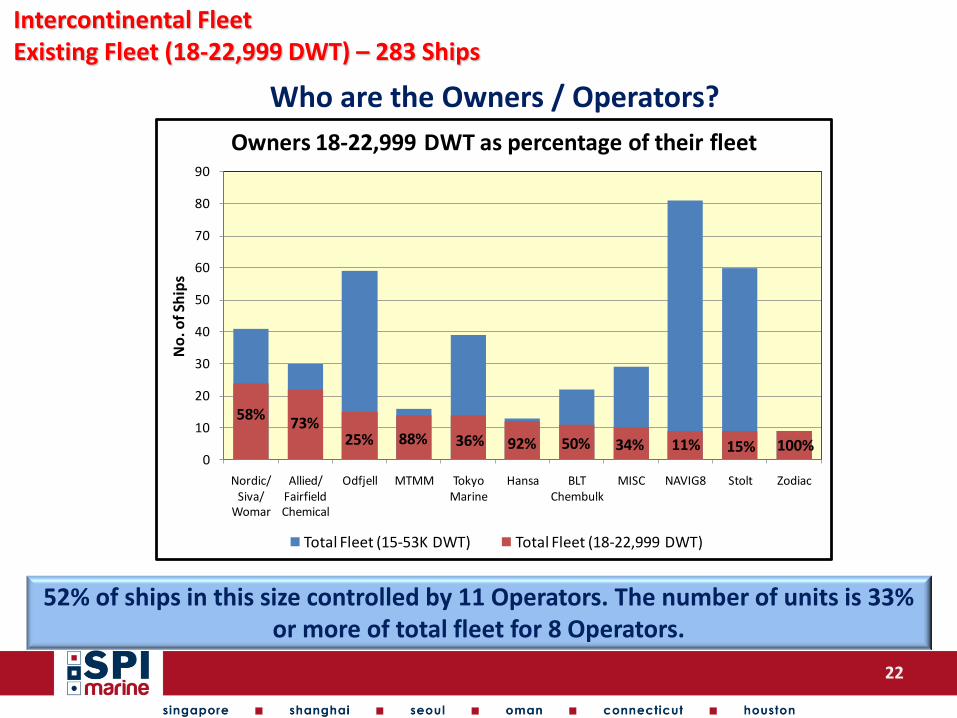

Owners 18-22,999 DWT as percentage of their fleet

Total Fleet (15-53K DWT) Total Fleet (18-22,999 DWT)

58%73%

25% 88% 36% 92% 50% 34% 11% 15% 100%

Who are the Owners / Operators?

52% of ships in this size controlled by 11 Operators. The number of units is 33% or more of total fleet for 8 Operators.

22

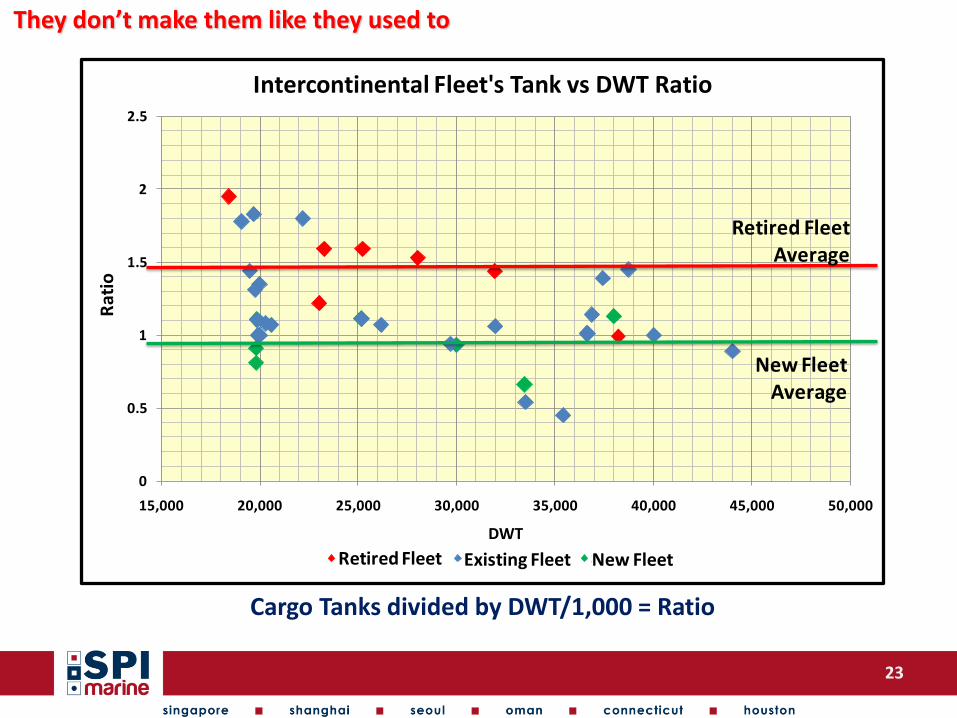

23

They don’t make them like they used to

Cargo Tanks divided by DWT/1,000 = Ratio

0

0.5

1

1.5

2

2.5

15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

Rat

io

DWT

Intercontinental Fleet's Tank vs DWT Ratio

18,421 19,087 25,147Retired Fleet Existing Fleet New Fleet

New Fleet Average

Retired Fleet Average

24

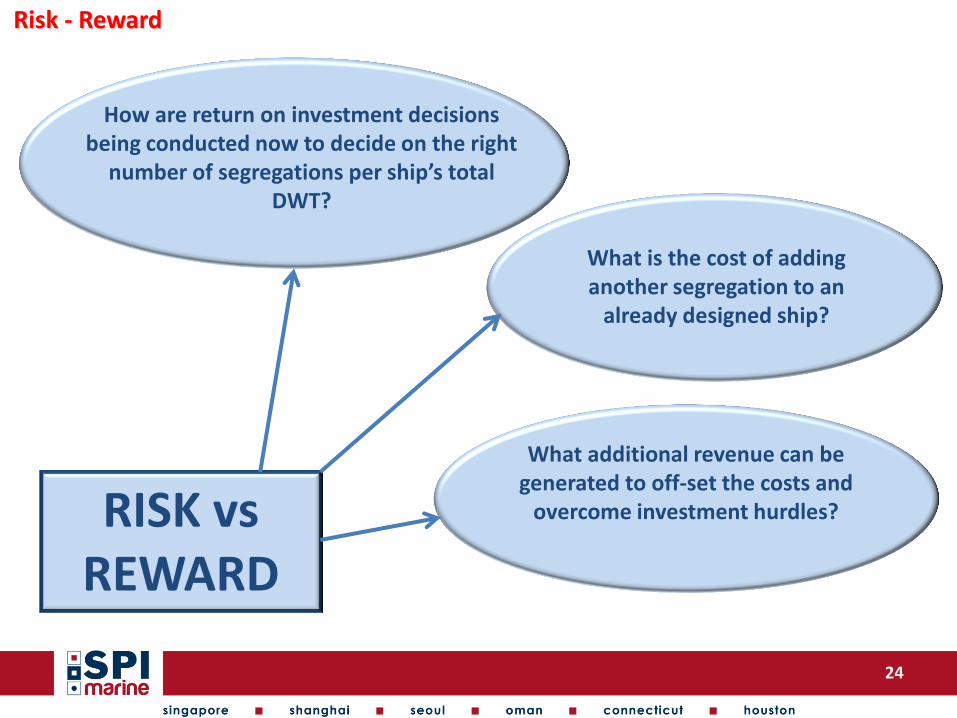

Risk - Reward

RISK vs REWARD

How are return on investment decisions being conducted now to decide on the right

number of segregations per ship’s total DWT?

What is the cost of adding another segregation to an

already designed ship?

What additional revenue can be generated to off-set the costs and

overcome investment hurdles?

25

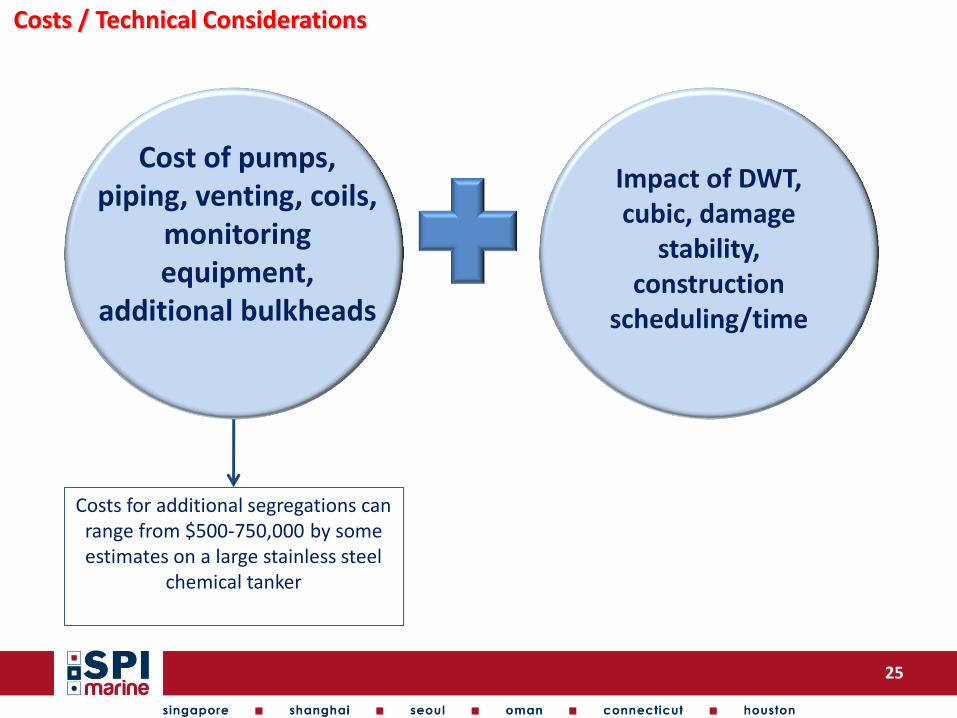

Costs / Technical Considerations

Costs for additional segregations can range from $500-750,000 by some estimates on a large stainless steel

chemical tanker

Cost of pumps, piping, venting, coils,

monitoring equipment,

additional bulkheads

Impact of DWT, cubic, damage

stability, construction

scheduling/time

26

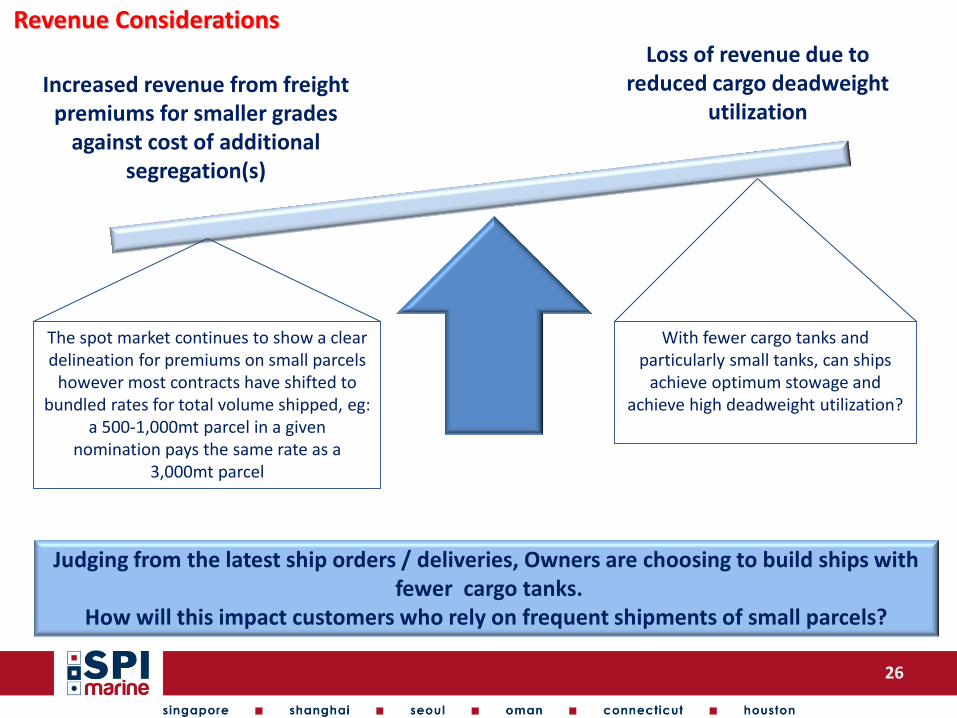

Revenue Considerations

Increased revenue from freight premiums for smaller grades

against cost of additional segregation(s)

The spot market continues to show a clear delineation for premiums on small parcels

however most contracts have shifted to bundled rates for total volume shipped, eg:

a 500-1,000mt parcel in a given nomination pays the same rate as a

3,000mt parcel

Loss of revenue due to reduced cargo deadweight

utilization

With fewer cargo tanks and particularly small tanks, can ships

achieve optimum stowage and achieve high deadweight utilization?

Judging from the latest ship orders / deliveries, Owners are choosing to build ships with fewer cargo tanks.

How will this impact customers who rely on frequent shipments of small parcels?

27

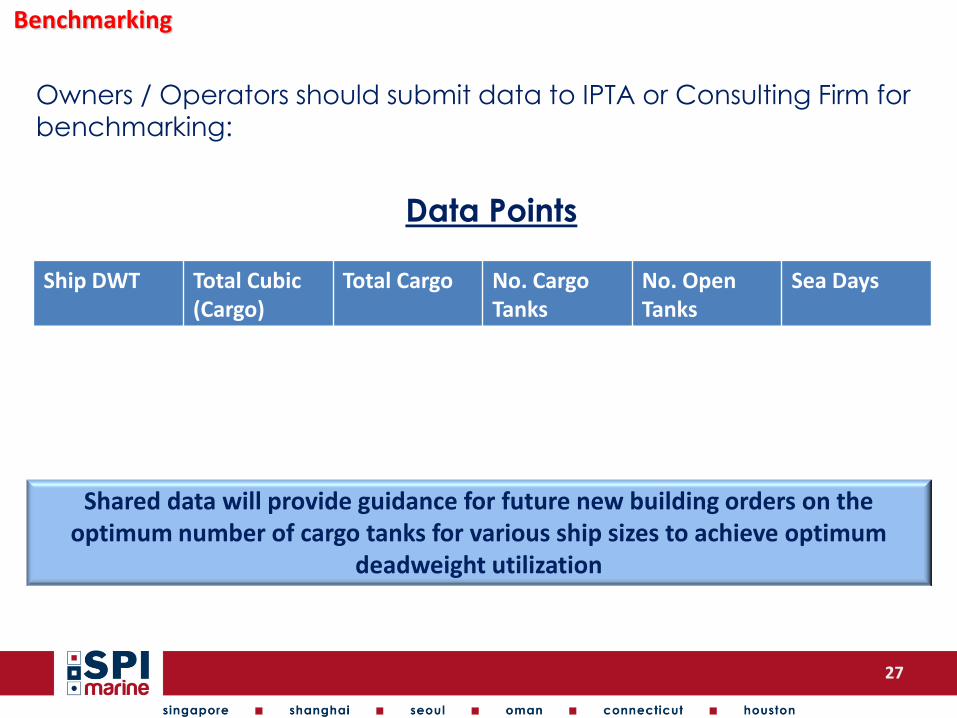

Benchmarking

Owners / Operators should submit data to IPTA or Consulting Firm for

benchmarking:

Data Points

Ship DWT Total Cubic (Cargo)

Total Cargo No. Cargo Tanks

No. Open Tanks

Sea Days

Shared data will provide guidance for future new building orders on the optimum number of cargo tanks for various ship sizes to achieve optimum

deadweight utilization

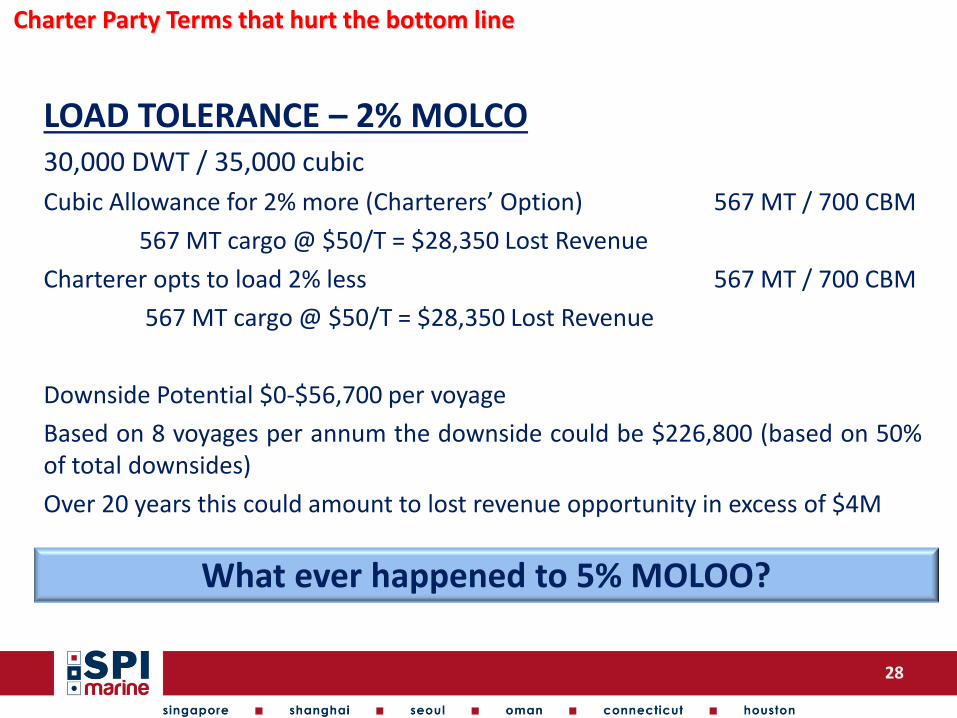

Charter Party Terms that hurt the bottom line

LOAD TOLERANCE – 2% MOLCO 30,000 DWT / 35,000 cubic

Cubic Allowance for 2% more (Charterers’ Option) 567 MT / 700 CBM

567 MT cargo @ $50/T = $28,350 Lost Revenue

Charterer opts to load 2% less 567 MT / 700 CBM

567 MT cargo @ $50/T = $28,350 Lost Revenue

Downside Potential $0-$56,700 per voyage

Based on 8 voyages per annum the downside could be $226,800 (based on 50% of total downsides)

Over 20 years this could amount to lost revenue opportunity in excess of $4M

What ever happened to 5% MOLOO?

28

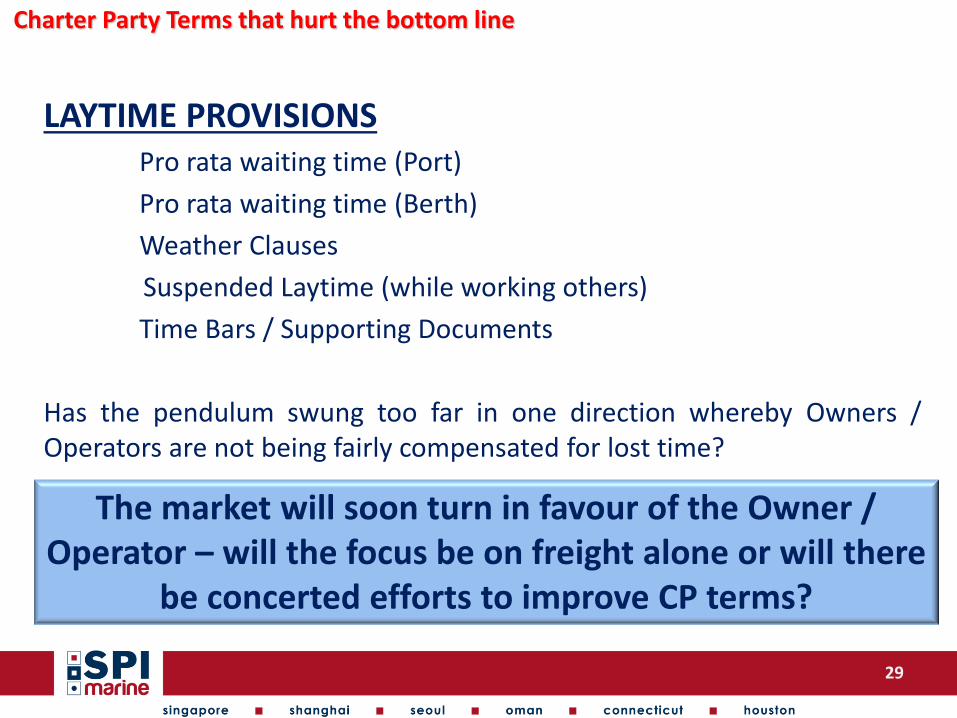

Charter Party Terms that hurt the bottom line

LAYTIME PROVISIONS Pro rata waiting time (Port)

Pro rata waiting time (Berth)

Weather Clauses

Suspended Laytime (while working others)

Time Bars / Supporting Documents

Has the pendulum swung too far in one direction whereby Owners / Operators are not being fairly compensated for lost time?

The market will soon turn in favour of the Owner / Operator – will the focus be on freight alone or will there

be concerted efforts to improve CP terms?

29

30

Contact Details

www.spimarineasia.com www.spimarineusa.com

SPI Marine (Asia) Pte. Ltd.

72-a Peck Seah St

Singapore 079329

Tel: +65 6226 6612

Email: [email protected]

SPI Marine Consulting (Shanghai) Co.Ltd.

Room 1302, Sino Life Tower,

707 Zhangyang Road,

Shanghai 200120

Tel: +86 21 5130 7380

Fax: +86 21 5130 7390

Email: [email protected]

SPI Marine (Korea) Ltd

Korea Office, 604-2 Daewoo Building

167 Naesu-Dong, Jongno-Gu

Seoul, Korea (110-719)

Tel: +82 2 723 6612

Fax: +82 2 723 6663

Email: [email protected]

SPI Marine (Oman) Ptv.

Oman Representative Office

P O Box 474, Falaj al Qabail

PC 322, Sohar, Sultanate of Oman

Tel: +968 9237 8900

Email: [email protected]

SPI Marine (USA), Inc.

Norwalk Cove Marina

50A Calf Pasture Beach Road

Norwalk, CT 06855

Tel: +1 203 642 0100

Email: [email protected]

SPI Marine (Houston), Inc.

1900 West Loop South

Houston, TX 77027

Tel: +1 713 843 7760

E-mail: [email protected]

Contact :