A — Personal taxation - Department of the...

146

Page 1 A — Personal taxation A1. PERSONAL INCOME TAX ....................................................................................... 3 A fair personal income tax system...............................................................................................4 A simple and transparent system ................................................................................................5 A system designed to reduce disincentives to work and save ....................................................7 A1–1 The structure of personal income tax ........................................................................................11 Personal income tax rates .........................................................................................................13 Taxing people as individuals .....................................................................................................23 The taxation of transfer payments .............................................................................................26 Tax offsets .................................................................................................................................29 A1–2 Income from work and deductions.............................................................................................37 Employee income ......................................................................................................................38 Income from self-employment ...................................................................................................50 Deductions .................................................................................................................................53 A1–3 Taxation of income from savings ...............................................................................................62 A consistent treatment of savings..............................................................................................62 Simplifying the taxation of capital gains.....................................................................................78 Taxing savings on an individual basis .......................................................................................83 Annex A1: Concessional offsets in detail ...............................................................................................86 A2. RETIREMENT INCOMES ....................................................................................... 95 A2–1 The strategic report into the retirement income system ............................................................95 A2–2 Taxing retirement incomes ........................................................................................................96 The equity, complexity and adequacy impacts of the current tax arrangements ......................98 A new arrangement for taxing superannuation contributions ................................................. 100 The taxation of earnings ......................................................................................................... 106 Effect of recommendations on retirement incomes ................................................................ 108 Effect of recommendations on overall saving......................................................................... 113 Other tax-related issues.......................................................................................................... 115 A2–3 Responding to increasing life expectancies ........................................................................... 117 Responding to higher life expectancies .................................................................................. 118 Role of longevity insurance products...................................................................................... 121 A2–4 Improving people’s awareness of the retirement income system .......................................... 128 A2–5 Other retirement income issues.............................................................................................. 130 Superannuation funds and infrastructure ............................................................................... 130 Superannuation guarantee for contractors ............................................................................. 130 Preservation ages for mandatory retirement occupations ...................................................... 131 Annex A2: Assumptions used in this section....................................................................................... 133 A3. WEALTH TRANSFER TAXES............................................................................... 137 A3–1 How a tax on bequests measures up ..................................................................................... 137 Efficiency ................................................................................................................................ 138 Equity ................................................................................................................................. 140 Simplicity................................................................................................................................. 141 Sustainability........................................................................................................................... 142 A3–2 The current system has some impact on bequests ................................................................ 143 A3–3 Parameters for a possible tax on bequests ............................................................................ 144 A tax on the whole estate or on individual inheritances? ....................................................... 144 The breadth of the base ......................................................................................................... 145 Setting sensible rates ............................................................................................................. 145 Other design issues ................................................................................................................ 146

-

Upload

nguyentruc -

Category

Documents

-

view

223 -

download

2

Transcript of A — Personal taxation - Department of the...

Page 1

A — Personal taxation

A1. PERSONAL INCOME TAX .......................................................................................3 A fair personal income tax system...............................................................................................4 A simple and transparent system ................................................................................................5 A system designed to reduce disincentives to work and save ....................................................7

A1–1 The structure of personal income tax ........................................................................................11 Personal income tax rates .........................................................................................................13 Taxing people as individuals .....................................................................................................23 The taxation of transfer payments .............................................................................................26 Tax offsets .................................................................................................................................29

A1–2 Income from work and deductions.............................................................................................37 Employee income ......................................................................................................................38 Income from self-employment ...................................................................................................50 Deductions.................................................................................................................................53

A1–3 Taxation of income from savings...............................................................................................62 A consistent treatment of savings..............................................................................................62 Simplifying the taxation of capital gains.....................................................................................78 Taxing savings on an individual basis .......................................................................................83

Annex A1: Concessional offsets in detail ...............................................................................................86

A2. RETIREMENT INCOMES.......................................................................................95 A2–1 The strategic report into the retirement income system ............................................................95 A2–2 Taxing retirement incomes ........................................................................................................96

The equity, complexity and adequacy impacts of the current tax arrangements ......................98 A new arrangement for taxing superannuation contributions................................................. 100 The taxation of earnings ......................................................................................................... 106 Effect of recommendations on retirement incomes ................................................................ 108 Effect of recommendations on overall saving......................................................................... 113 Other tax-related issues.......................................................................................................... 115

A2–3 Responding to increasing life expectancies ........................................................................... 117 Responding to higher life expectancies.................................................................................. 118 Role of longevity insurance products...................................................................................... 121

A2–4 Improving people’s awareness of the retirement income system .......................................... 128 A2–5 Other retirement income issues.............................................................................................. 130

Superannuation funds and infrastructure ............................................................................... 130 Superannuation guarantee for contractors............................................................................. 130 Preservation ages for mandatory retirement occupations...................................................... 131

Annex A2: Assumptions used in this section....................................................................................... 133

A3. WEALTH TRANSFER TAXES...............................................................................137 A3–1 How a tax on bequests measures up ..................................................................................... 137

Efficiency ................................................................................................................................ 138 Equity ................................................................................................................................. 140 Simplicity ................................................................................................................................. 141 Sustainability........................................................................................................................... 142

A3–2 The current system has some impact on bequests................................................................ 143 A3–3 Parameters for a possible tax on bequests ............................................................................ 144

A tax on the whole estate or on individual inheritances? ....................................................... 144 The breadth of the base ......................................................................................................... 145 Setting sensible rates ............................................................................................................. 145 Other design issues................................................................................................................ 146

Page 3

A1. Personal income tax

Personal income tax is Australia’s single biggest source of taxation revenue, raising 37 per cent of total tax revenue. It should raise revenue simply and transparently from a relatively efficient tax base, while maintaining incentives to work and save. Personal income tax also plays a central role in achieving a progressive tax system by raising proportionally more revenue from those who have a greater capacity to pay.

Most adult Australians are affected by the personal income tax system every year, with around 12 million people filing tax returns annually.

As a proportion of GDP, revenue from personal income tax has fallen over the past two decades, with a series of tax cuts a major contributor in the last decade. In the future, demographic change will impact on growth in personal income tax revenue because a greater proportion of the population will be in retirement. If rising debt and reductions in government services are to be avoided, action will be needed to increase the amount of revenue raised from this or other tax bases.

The share of personal income tax in Australia, at 37 per cent of total tax revenue, is high compared to the OECD average of 25 per cent. Much of this difference is explained by the fact that Australia does not levy additional social security taxes in the way that most other OECD countries do (with benefits based on a person’s previous earnings), at an average rate of 25 per cent of total tax revenue. Instead, Australia funds social security payments from general government revenues, and has a compulsory superannuation guarantee (that is, excluded from the calculation). Taking this into account, Australia’s total taxation on personal income is among the lowest in the OECD, at 41 per cent compared to an OECD average of 51 per cent.1

The tax system has a close relationship with the transfer payment system, given the large number of people who are in both systems at any given time. The two systems have different objectives, with the tax system focused on capacity to pay and the transfer system on need. The Review has considered in some depth the extent to which key structural elements of the two systems might be aligned, such as the definition of income and the unit and period of assessment. It has concluded that full integration of the two systems is neither achievable nor desirable because of the differences in their purposes, although policy in the two systems should always be developed jointly and service delivery should be coordinated.

Fairness should continue to be a key principle in the design of the personal income tax system. For the community to be willing to comply with the tax law, people need to be confident that their liability is assessed fairly and reflects their ability to pay. There is strong and widespread support for the proposition that proportionally more revenue should be raised from those with a greater ability to pay. While there are many ways to reach such outcomes, it is important they be achieved in as simple and transparent a way as possible. In

1 Total taxation on personal income includes personal income tax, social security tax and payroll tax. It does not include Australia’s compulsory superannuation guarantee, as this is not currently classified as a tax.

Australia's future tax system — Report to the Treasurer

Page 4

addition, a personal income tax system to suit an ageing population needs to be structured to reduce disincentives to work for the smaller proportion of the population who are of working age and to increase incentives for people to save and invest for their future.

Principles

The personal income tax system should raise revenue fairly — in terms of both the income on which tax is levied (the tax base) and the rates that apply — and contribute to achieving the government’s redistribution goals.

Revenue-raising through the personal income tax system should operate as simply and transparently as possible.

Revenue-raising through the personal income tax system should avoid discouraging work and saving as far as possible.

A fair personal income tax system

The fairness of personal income tax is fundamental as an expression of societal values and is a prerequisite for people to be committed to the system and prepared to meet their obligations. There are two core elements to a fair system — a progressive tax rate structure and an appropriate definition of income.

The current personal income tax system seeks to aggregate income from both work and savings to form a single measure of taxable income. In practice the major part of household savings, including owner-occupied housing and superannuation, is exempt or effectively exempt. In designing the personal income tax system, labour income and the income from savings should be considered as separate though interconnected elements.

Income from work is currently taxed in different ways, depending on the nature of the worker’s employment or their remuneration. While most people with work income have either salary and wage income or business income, which are taxed similarly, many people take some of their remuneration in the form of superannuation or fringe benefits, both of which have completely separate taxation arrangements. Some people’s income from work is entirely exempt from tax. The costs associated with earning income are also treated inconsistently. A tax system for the future would tax wages and fringe benefits in a similar way, and also tax compulsory superannuation contributions with reference to a progressive personal income tax rates scale.

Income from savings, other than lifetime savings, is also taxed in a wide variety of ways. Varying arrangements apply to interest-bearing deposits, income from domestic shares, income from foreign shares, and rents from residential properties. A tax system for the future would tax these different forms of investment as consistently as possible, and also take account of the way inflation affects the effective tax rate on savings. It could do so by providing a common discount for a range of savings income or by applying a flat rate of tax to that income. Long-term, lifetime savings in the form of superannuation and owner-occupied housing should continue to be effectively exempt from income tax.

Personal income tax is calculated by applying a marginal rates scale to a person’s combined income from work and savings. The progressive personal income tax rates scale is a strength

A1 — Personal income tax

Page 5

of the system that should be retained. At present, the great majority of tax revenue comes from higher income earners. In 2007–08, the 16 per cent of taxpayers on more than $75,000 accounted for 55 per cent of personal income tax revenue, with almost half of that coming from the three per cent of taxpayers with taxable income over $150,000.

A progressive system can be achieved in various ways. At present, Australia has a relatively low tax-free threshold and four marginal rates above it, along with a large number of tax offsets that alter the marginal rates for people in particular situations. The direction of change has been towards fewer marginal tax rates, from as many as six or seven during much of the 1980s and early 1990s. An alternative way of delivering a progressive personal income tax rates scale would be through a much higher tax-free threshold and a flat or rising rate scale. This would make the system easier to understand by removing the need for a number of tax offsets. By taking more income support recipients out of the tax system, it could also reduce the number of people who have to deal with both systems at the same time.

Chart A1–1 shows such a tax scale, with progressivity delivered through a large tax-free threshold and a constant marginal tax rate of 35 per cent for most taxpayers.

Chart A1–1: Indicative personal income tax rates scale A simple scale with a high tax-free threshold

0

5

10

15

20

25

30

35

40

45

50

0 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 180,000 200,000Taxable income ($pa)

0

5

10

15

20

25

30

35

40

45

50

Marginal tax rates

Average tax rates

Tax rate (%) Tax rate (%)

Source: Treasury estimates.

A simple and transparent system Many people find the personal income tax system complex, not only because of the rates scale and the lack of a coherent definition of taxable income, but also because they must deal with a large set of complex deduction rules, numerous tax offsets and different forms of exempt income.

A consequence of this is that the system is not transparent to taxpayers. It can be difficult for taxpayers to have a sense of their taxable income because of the complex rules associated with deductions, which are claimed by 80 per cent of personal income taxfilers. A common response to this and other forms of complexity in the tax system is to seek advice from a tax agent. Around three quarters of taxfilers seek such assistance. Nonetheless, in 2007–08, 86 per cent either claimed no deductions at all or only claimed work-related expenses, gifts

Australia's future tax system — Report to the Treasurer

Page 6

and the costs of managing tax affairs. This suggests that the system is too complex and the compliance burden too high.

Australia’s use of tax agents is high by international standards; only Italy’s is higher. By contrast, the Nordic countries, which have pre-filling arrangements for tax returns, have very low levels of tax agent use (see Chart A1–2). To simplify people’s interactions with the tax system and facilitate much greater levels of pre-filling of tax returns, an automatic standard deduction should be introduced. However, to ensure that individuals with more complex affairs or high expenses are not disadvantaged, taxpayers would still have the option of substantiating a claim for all eligible expenses.

Chart A1–2: Percentage of taxfilers using a tax agent, 2005

0102030405060708090

100

Slo

vak

Rep

ublic

Por

tuga

l

Cze

ch R

epub

lic

Luxe

mbo

urg

Nor

way

Den

mar

k

Sw

eden

Spa

in

Sw

itzer

land

Net

herla

nds

New

Zea

land

Icel

and

Can

ada

Kor

ea

Pol

and

Uni

ted

Kin

gdom

Uni

ted

Sta

tes

Turk

ey

Aus

tria

Irela

nd

Aus

tralia

Italy

0102030405060708090100

Taxfilers (%) Taxfilers (%)

Source: OECD (2005). A more transparent system would improve people’s ability to understand their tax rate and to predict the impact of changes in their work or savings arrangements. A key way of achieving this would be to incorporate some offsets into the personal income tax rates scale, and to limit non-structural offsets to situations where they meet an ongoing need that cannot be met in a more targeted way. The transparency of the system would also be improved by a more complete separation of the tax system from the transfer system. This could be achieved by setting the tax-free threshold at a much higher level for all taxpayers.

Longer term reforms should be made with a view to creating a simpler and more transparent system. Policy changes should support simplification by facilitating fully automated preparation of tax returns. Using information that is reported by a third party such as an employer or financial institution is an important part of this, rather than relying on information that has to be collected by the taxpayer over the course of the tax year. People of retirement age could be given the option of submitting their details on a single form with their partner, thus reducing the compliance burden where they own assets jointly. While it would be more complex, joint assessment could be considered for couples of late retirement age. Policy changes should also support transparency so that people can understand the incentives they face to work and save, and are better able to predict the impact of a change to their work or personal circumstances.

A1 — Personal income tax

Page 7

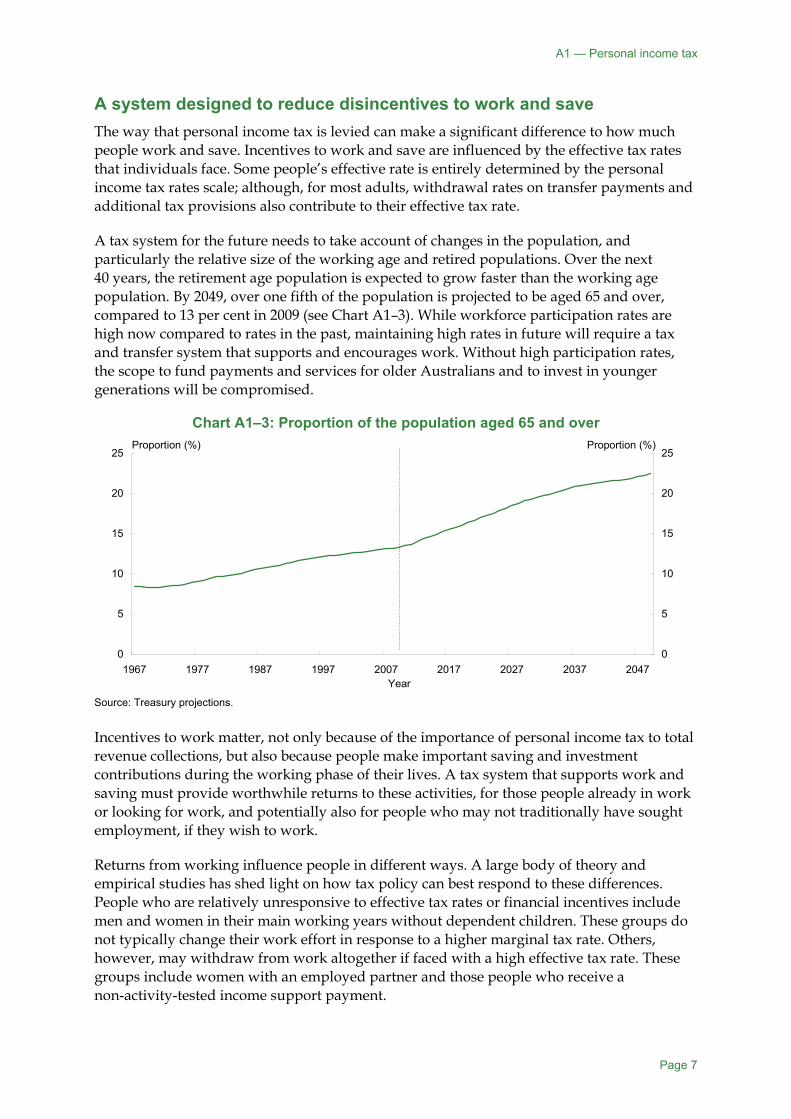

A system designed to reduce disincentives to work and save The way that personal income tax is levied can make a significant difference to how much people work and save. Incentives to work and save are influenced by the effective tax rates that individuals face. Some people’s effective rate is entirely determined by the personal income tax rates scale; although, for most adults, withdrawal rates on transfer payments and additional tax provisions also contribute to their effective tax rate.

A tax system for the future needs to take account of changes in the population, and particularly the relative size of the working age and retired populations. Over the next 40 years, the retirement age population is expected to grow faster than the working age population. By 2049, over one fifth of the population is projected to be aged 65 and over, compared to 13 per cent in 2009 (see Chart A1–3). While workforce participation rates are high now compared to rates in the past, maintaining high rates in future will require a tax and transfer system that supports and encourages work. Without high participation rates, the scope to fund payments and services for older Australians and to invest in younger generations will be compromised.

Chart A1–3: Proportion of the population aged 65 and over

0

5

10

15

20

25

1967 1977 1987 1997 2007 2017 2027 2037 20470

5

10

15

20

25

Year

Proportion (%) Proportion (%)

Source: Treasury projections. Incentives to work matter, not only because of the importance of personal income tax to total revenue collections, but also because people make important saving and investment contributions during the working phase of their lives. A tax system that supports work and saving must provide worthwhile returns to these activities, for those people already in work or looking for work, and potentially also for people who may not traditionally have sought employment, if they wish to work.

Returns from working influence people in different ways. A large body of theory and empirical studies has shed light on how tax policy can best respond to these differences. People who are relatively unresponsive to effective tax rates or financial incentives include men and women in their main working years without dependent children. These groups do not typically change their work effort in response to a higher marginal tax rate. Others, however, may withdraw from work altogether if faced with a high effective tax rate. These groups include women with an employed partner and those people who receive a non-activity-tested income support payment.

Australia's future tax system — Report to the Treasurer

Page 8

The capacity of the tax system to respond to these different behaviours is limited, but it does affect incentives for people who do not receive transfer payments and it interacts with transfer payments for people who may do some work now or in the future. At present, the tax system adapts to accommodate the transfer system, by removing maximum-rate full-year income support recipients from the requirement to pay tax. It does this by providing tax offsets for income support recipients with little or no private income. A more transparent system would reverse this arrangement, with the same tax rules applying to everyone and the transfer system adapting to the tax rules. This could be achieved by exempting income support and other transfer payments from tax entirely. In addition, withdrawal rates on payments could be reduced once an individual’s income was high enough to produce a tax liability, to cap the overall effective marginal tax rate. The benefit of these changes would be more transparent effective tax rates.

While the proportion of Australians who participate in the workforce is high by international standards (76 per cent of the working age population compared to an OECD average of 71 per cent), this is partly due to Australia having the highest labour participation rate for students in the OECD. After making adjustments to account for measurement differences, the Productivity Commission found that the participation rate of Australian men aged 25 to 54 is below the OECD average. Australian women in the same age group have participation rates above the OECD average, but still curtail their engagement in the workforce during the typical child-bearing years more than is the case in New Zealand, the United Kingdom and the United States (Chart A1–4).

Chart A1–4: Female participation rates, by age, 2008

30

40

50

60

70

80

90

100

15 to 19 20 to 24 25 to 29 30 to 34 35 to 39 40 to 44 45 to 49 50 to 54 55 to 59

Age group

30

40

50

60

70

80

90

100

Canada Australia New ZealandSweden United Kingdom United States

Participation rate (%) Participation rate (%)

Source: OECD(2008b). Lower participation rates for women of child-bearing age are also reflected in employment rates. The employment rate for women with a youngest child aged between three and five years is below the average for all OECD countries that collect this data, and is 25 percentage points below the Swedish rate (ABS 2007a).

This suggests that women of child bearing age constitute one of the key groups with greater potential for paid employment. Many of these women are caring for children, and prefer to take a period out of employment while they do so. Many seek employment, but do not

A1 — Personal income tax

Page 9

always have access to satisfactory child care. The longer the period out of the workforce, the greater the risk of skills atrophying and poorer employment opportunities later on. While there are many factors at play, financial incentives cannot be ignored. One of the most effective ways to improve financial incentives for people with dependent children is to set effective tax rates that support part-time work and recognise that carers in couple families are likely to have lower earnings than their partner. Taxing people as individuals is important in terms of financial incentives, because it applies a different tax rate to each partner in a couple rather than both people facing a pooled tax rate.

For non-lifetime savings, the current tax system’s inconsistent treatment of different types of saving not only affects the level of savings but can also affect how households allocate their savings between different assets or savings vehicles. A future tax system would reduce these biases by taxing different types of saving more consistently.

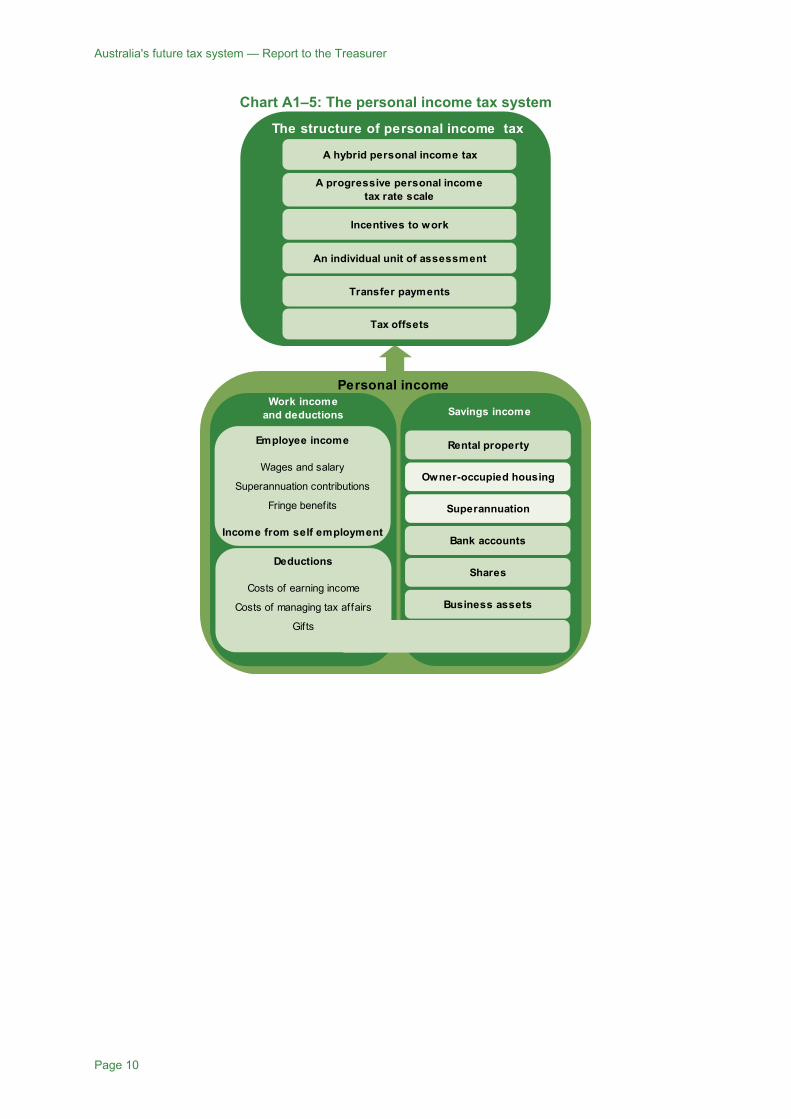

The remainder of this section discusses core elements of the personal income tax system (see Chart A1–5) in more detail:

• A1–1 The structure of personal income tax — tax rates, particularly in terms of progressivity in the tax system and incentives to work and save.

• A1–2 Income from work and deductions.

• A1–3 Taxation of income from savings — other than superannuation (see Section A2 Retirement incomes).

Australia's future tax system — Report to the Treasurer

Page 10

Chart A1–5: The personal income tax system

A hybrid personal income tax

The structure of personal income tax

A progressive personal incometax rate scale

Incentives to work

Transfer payments

Tax offsets

An individual unit of assessment

Work incomeand deductions

Employee income

Wages and salary.

Superannuation contributions.

Fringe benefits

Income from self employment

Deductions

Costs of earning income.

Costs of managing tax affairs.

Gifts

Savings income

Owner-occupied housing

Personal income

Rental property

Bank accounts

Superannuation

Business assets

Shares

A1 — Personal income tax

Page 11

A1–1 The structure of personal income tax

Key points

The personal income tax system should continue to be progressive, but it should operate in a simpler and more transparent way. The centrepiece of the system should be a high tax-free threshold with a constant marginal rate for most people.

The personal income tax system should support workforce participation by limiting high effective tax rates, especially for those people who are likely to be most responsive to financial incentives to work.

The primary unit in the personal tax system should continue to be the individual, and subsidies for dependants through the tax system should be restricted.

Income support and supplementary payments should be exempt to simplify tax and transfer interactions.

Where possible, tax offsets that are structural in nature should be incorporated into the personal income tax rates scale, along with the Medicare levy. Tax offsets that provide a concession for a particular group should be removed or delivered as a direct payment or service.

The taxation of personal income is the most important means of raising revenue in developed countries. However, personal income taxes discourage workforce participation and savings, both of which are important for economic growth.

The main purpose of the personal income tax system is to allow governments to raise revenue to pay for public goods (like education, health care and law enforcement), and to provide income support for those less able or available to support themselves. Underpinning the design of the income tax system is the desire to provide a balance between ensuring that those people with more capacity to pay contribute more (vertical equity) and that those with a similar capacity to pay bear the same burden (horizontal equity).

The practice of taxing those with greater capacity to pay reflects the view that an extra dollar of income is generally of more value for a person with a lower income than for a person with a higher income. That is, people on lower incomes benefit more from a lower average tax rate than people on higher incomes lose from paying a higher average tax rate.

An individual’s capacity to pay is difficult to define. In the absence of existing wealth, there is an argument for redistributive tax policy to be based on an individual’s potential earnings capacity. However, as information on potential earnings capacity is not readily available, observable proxies are required.

Actual labour income is often used as a proxy for potential earnings capacity. But wage and income differentials may reflect a number of other factors, including choices about how much to work or study. Taxing wages or income therefore biases decisions to undertake paid work and may also affect decisions about undertaking education and training. Savings income is also relevant to a person’s capacity to pay, particularly for pre-existing savings or

Australia's future tax system — Report to the Treasurer

Page 12

taxes on economic rent. But taxing the normal return to saving is likely to bias savings, labour supply (for those that save part of their wages) and consumption decisions.

As income taxes can lead to a decline in overall economic output, there can be a trade-off between equity and efficiency when designing the personal income tax system.

A hybrid personal income tax base

Australia’s personal income tax system should continue to represent a hybrid personal income tax — with income from long-term, lifetime, savings taxed at a lower rate than other income or exempt from income tax. In particular, the main forms of lifetime savings for most Australians, superannuation and owner-occupied housing, should continue to be taxed at a lower rate or exempt from income tax — consistent with an expenditure tax benchmark that exempts the returns to saving (see Section A2–2). Comprehensive income taxation, under which all savings income is taxed in the same way as labour income, is not an appropriate policy goal or benchmark.

The essential reason for exempting lifetime savings or taxing them at a lower rate is that income taxation creates a bias against savings. The income taxation of savings therefore discriminates against taxpayers who save. They pay a higher lifetime tax bill than people with similar earnings who choose to save less. As savings can be thought of as deferred consumption, the longer the person saves and reinvests, the greater the implicit tax on future consumption (see Chart A1–6). For a person who works today and saves, taxing savings also reduces the benefit from working.

Chart A1–6: Tax wedge on future consumption

0

500

1,000

1,500

0 5 10 15 20 25 30 35 40 45

Years consumption is deferred

0

500

1,000

1,500

Before tax After tax

Tax wedge ($) Tax wedge ($)

Tax on future consumption

Source: Treasury estimates. Assumptions: Pre-tax interest rate of 6 per cent per annum and a tax rate of 30 per cent. The increasing implicit tax on future consumption provides an argument to tax longer-term lifetime savings at a lower rate. An individual can undertake lifetime saving through a variety of savings vehicles, but there are asset types that are more conducive or related to lifetime savings: namely superannuation and owner-occupied housing. It is possible to convert savings in these assets into present consumption by borrowing against them, directly or in effect. Further, the family home yields a stream of income (imputed rent) that is also a

A1 — Personal income tax

Page 13

form of current consumption. While these features could diminish their status as lifetime savings vehicles, in practice these assets will in net terms remain major forms of lifetime savings for most Australians, and provide for a major part of their retirement income.

An exemption from income tax or applying relatively low rates of tax to superannuation and owner-occupied housing is common practice around the world and has been a longstanding feature of the Australian tax system. The family home has not been subject to income tax in Australia since the earlier part of last century. Imputed rental income and capital gains from owner-occupied housing are generally exempt in the OECD countries, with a few exceptions.

While owner-occupied housing represents more than lifetime or retirement savings, other factors support its continued exemption. Given there is little community acceptance for applying income tax to the family home, any attempt to subject it to taxation is unlikely to be sustainable. Australia’s current approach avoids the worst of the biases found in some other countries, where limited taxation of income or gains combined with full tax deductibility of mortgage expenses encourages people to over-invest in housing and take on too much household debt.

Retirement savings are also generally lightly taxed around the world. Many OECD countries tax retirement benefits at a person’s marginal tax rate, and exempt contributions and earnings. In Australia, retirement savings are also taxed lightly but in a different manner — as both contributions and earnings are taxed at low rates while superannuation benefits are generally tax-exempt when paid after the age of 60.

Principles

Superannuation and owner-occupied housing should continue to be taxed at relatively low rates or be exempt from income tax, consistent with an expenditure tax benchmark.

Other savings income should continue to be subject to income tax.

Personal income tax rates

Options for achieving a progressive personal income tax rates scale

A progressive income tax is characterised by average rates that rise with income, in line with the idea that reductions in income caused by taxation reduce the wellbeing of low-income earners more than high-income earners. This means that higher-income people bear a greater than proportional share of the tax burden.

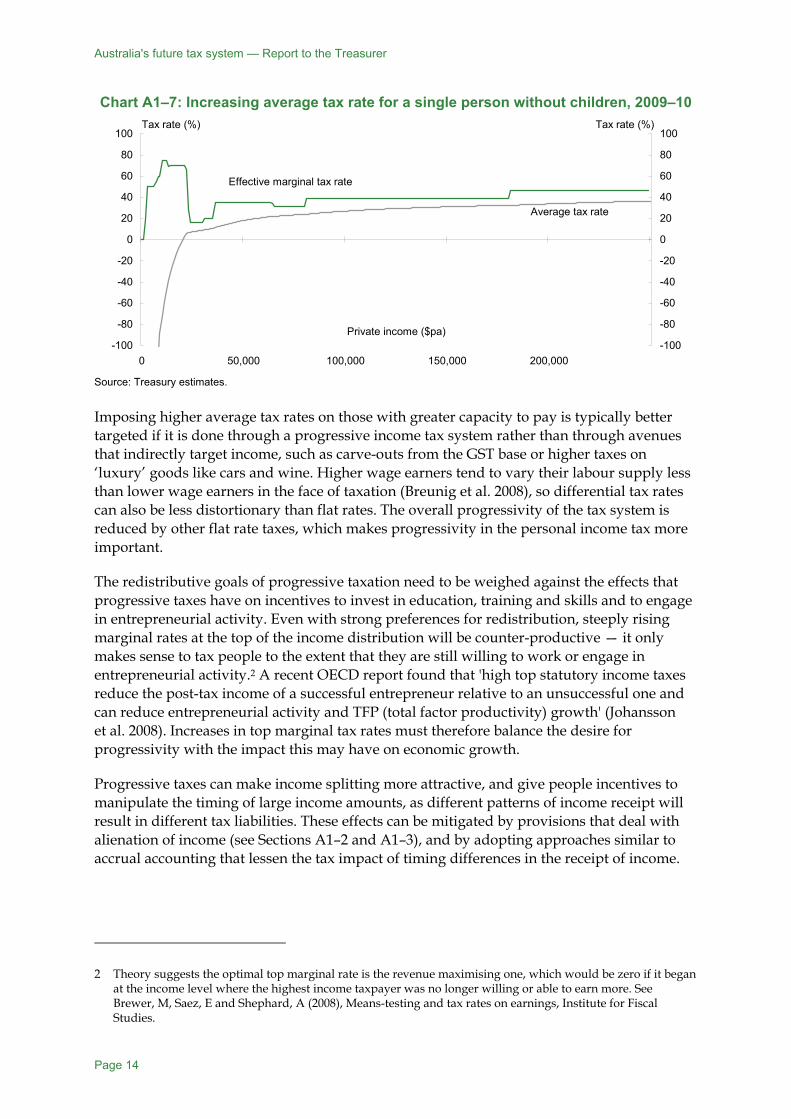

Progressivity can be achieved either through a flat tax rate with a tax-free threshold, a rising personal income tax rates scale, or a combination of both. Progressivity does not necessarily require increasing effective marginal tax rates, as illustrated in Chart A1–7.

Australia's future tax system — Report to the Treasurer

Page 14

Chart A1–7: Increasing average tax rate for a single person without children, 2009–10

-100

-80

-60

-40

-20

0

20

40

60

80

100

0 50,000 100,000 150,000 200,000

Private income ($pa)-100

-80

-60

-40

-20

0

20

40

60

80

100

Effective marginal tax rate

Average tax rate

Tax rate (%) Tax rate (%)

Source: Treasury estimates. Imposing higher average tax rates on those with greater capacity to pay is typically better targeted if it is done through a progressive income tax system rather than through avenues that indirectly target income, such as carve-outs from the GST base or higher taxes on ‘luxury’ goods like cars and wine. Higher wage earners tend to vary their labour supply less than lower wage earners in the face of taxation (Breunig et al. 2008), so differential tax rates can also be less distortionary than flat rates. The overall progressivity of the tax system is reduced by other flat rate taxes, which makes progressivity in the personal income tax more important.

The redistributive goals of progressive taxation need to be weighed against the effects that progressive taxes have on incentives to invest in education, training and skills and to engage in entrepreneurial activity. Even with strong preferences for redistribution, steeply rising marginal rates at the top of the income distribution will be counter-productive — it only makes sense to tax people to the extent that they are still willing to work or engage in entrepreneurial activity.2 A recent OECD report found that 'high top statutory income taxes reduce the post-tax income of a successful entrepreneur relative to an unsuccessful one and can reduce entrepreneurial activity and TFP (total factor productivity) growth' (Johansson et al. 2008). Increases in top marginal tax rates must therefore balance the desire for progressivity with the impact this may have on economic growth.

Progressive taxes can make income splitting more attractive, and give people incentives to manipulate the timing of large income amounts, as different patterns of income receipt will result in different tax liabilities. These effects can be mitigated by provisions that deal with alienation of income (see Sections A1–2 and A1–3), and by adopting approaches similar to accrual accounting that lessen the tax impact of timing differences in the receipt of income.

2 Theory suggests the optimal top marginal rate is the revenue maximising one, which would be zero if it began at the income level where the highest income taxpayer was no longer willing or able to earn more. See Brewer, M, Saez, E and Shephard, A (2008), Means-testing and tax rates on earnings, Institute for Fiscal Studies.

A1 — Personal income tax

Page 15

Principle

Personal income tax should be progressive, both through its own rates scale and also in combination with transfer payments.

Australia’s progressive personal income tax system

The progressivity of a tax system can be assessed in various ways. A relatively straightforward approach is to compare the marginal and average tax rates inherent in the personal income tax rates scale at a particular point in the income distribution. The OECD commonly makes such an assessment at different points, illustrating how point measures of progressivity are sensitive to where they are evaluated.3 For example, for a single person in 2008, the Australian tax system was the 7th most progressive in the OECD if they were earning 67 per cent of the average wage, 20th most progressive at 100 per cent, and 11th most progressive at 167 per cent. Using this same measure, since 2000 the tax system has become slightly more progressive at 67 per cent of the average wage, and slightly less progressive at 100 per cent and 167 per cent.

Complementary measures enable progressivity to be evaluated across the whole system, not only at specific income levels. As well as hypothetical calculations, actual outcomes can be assessed using empirical data.

Administrative data show that the tax-free threshold and rising marginal rates of the existing personal income tax system deliver progressive outcomes in Australia. Chart A1–8 compares how taxable income and tax paid are spread across the population, after ranking everyone according to their taxable income.4 Taxable income is unequally distributed across the population, with the top 20 per cent of taxfilers receiving 49 per cent of all taxable income. However, the income tax burden is even more concentrated, with the top 20 per cent of taxfilers paying 67 per cent of all personal income tax. Similarly, the bottom 20 per cent of taxfilers receive 3 per cent of all taxable income, but pay only 0.1 per cent of all personal income tax. This means that post-tax outcomes are more evenly distributed than pre-tax outcomes.

3 The measure is calculated as (1 — marginal tax rate)/(1 — average tax rate), and is reported in the annual OECD publication Taxing Wages. A variant of this was used in Arnold (2008).

4 People with negative or zero taxable income have been excluded.

Australia's future tax system — Report to the Treasurer

Page 16

Chart A1–8: Distribution of taxable income and tax paid, 2007–08

0

10

20

30

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

Cumulative percentage of taxfilers, by increasing taxable income (%)

0

10

20

30

40

50

60

70

80

90

100

Taxable income

Tax paid

Cumulative percent Cumulative percent

Excludes people with negative or zero taxable income. Source: Australian government administrative data. However, the progressivity of personal income tax also depends on how comprehensively income is assessed. The provision of tax offsets, concessions and exemptions affects the personal income tax rates scale that different individuals face, and hence changes the progressivity of the system. The more exemptions in the tax base, the weaker is taxable income as a guide to a person’s actual income. Compromises to the tax base include income received in forms that are taxed more lightly; for example, from salary sacrificing into superannuation and from splitting income with others to avoid higher tax rates.

Alongside the tax system, transfer payments are another key mechanism for delivering progressivity. In contrast to many other countries, which have social insurance systems that pay benefits based on a person’s previous earnings, Australia has a targeted transfer system focused on poverty alleviation. This delivers strongly progressive outcomes — Chart A1–9 compares the share of transfers paid to the richest half of the population in the OECD countries in 2005.

Chart A1–9: Share of transfers paid to the richest half of the population, 2005

0

10

20

30

40

50

60

70

80

Aus

tralia

New

Zea

land

Den

mar

kU

nite

d K

ingd

omIre

land

Finl

and

Net

herla

nds

Nor

way

Cze

ch R

epub

licS

wed

enC

anad

aS

witz

erla

ndB

elgi

umU

nite

d S

tate

sIc

elan

dS

lova

k R

epub

licK

orea

Hun

gary

Japa

nG

erm

any

Spa

inLu

xem

bour

gG

reec

eFr

ance

Italy

Aus

tria

Pol

and

Por

tuga

lM

exic

oTu

rkey

0

10

20

30

40

50

60

70

80

OECD average

Per cent Per cent

Source: Whiteford 2009.

A1 — Personal income tax

Page 17

Finding

Overall, Australia has a progressive personal income tax system. The personal income tax and transfer system taken together is among the most progressive in the OECD.

Setting tax rates to support workforce participation

Rates of tax are one of the key factors in determining incentives to work and save. For many taxpayers, tax rates are a more visible part of the tax system than other key design elements, such as the way that income is defined for tax purposes.

As a matter of principle, taxes should interfere as little as possible with work incentives, as this leaves society as well off as possible. In practice, people can avoid taxes by earning less, and this is more costly to society than if the person was willing to work more and pay more tax. For example, a taxpayer can decide to work fewer hours than they otherwise might, or a person who receives income support can elect not to work at all to prevent withdrawal of their payment. People may respond to taxes in ways other than simply adjusting their hours of work. They may alter their education or entrepreneurial plans, or the form in which they receive income.

A large body of literature has explored how best to set tax rates to meet a government’s needs for revenue while minimising the disincentive effects of taxes and taking account of societal preferences for redistribution; for example, Diamond (1998), Saez (2001), Moffitt (2008), Brewer, Saez and Shephard (2008). One of the key findings is that it can be more efficient to impose higher tax rates where fewer people are subject to them, such as at very low and very high incomes. Another insight from this literature is that it can be more efficient to impose higher rates on people whose behaviour is relatively unresponsive to tax rates, such as prime-aged men and women who are not caring for dependent children.

People respond to tax and to financial incentives delivered through both the tax and the transfer systems. For people who are able and expected to work full time, the progression from unemployment to self-support through work can involve a high effective tax rate. Relatively high effective tax rates on low earnings, such as earnings from part-time work, can encourage people to choose full time work to get a lower overall rate and a higher disposable income. By contrast, people who have limited capacity or limited availability for work may only ever seek part-time work. This could be due to caring responsibilities, disability or impairment, or age. People with such restrictions who work part-time may respond to a high effective tax rate by withdrawing from work altogether. A more efficient arrangement in those circumstances is to impose a lower effective tax rate on modest earnings. This could be delivered through the tax rate only, the income support withdrawal rate only, or a combination of the two. Greater certainty and transparency result from varying only the withdrawal rates rather than using the tax system as well.

If more people currently outside the workforce worked part or full time, this could help meet the challenges of an ageing population. This would be likely to require more employment services and other support, alongside financial incentives, for people who are sick or disabled, their carers, aged people and those who are engaged in home duties or the care of children (Abhayaratna et al. 2006).

Australia's future tax system — Report to the Treasurer

Page 18

Arrangements to support the employment of people who are sick or disabled are discussed in Section F The transfer system. The workforce participation of those who are engaged in home duties and the care of children is also discussed in that section. A key element of the personal income tax system that supports workforce participation is the unit of assessment.

Tax rates and withdrawal rates can have the same economic effect

In considering the incentive effects of the system, it is important to consider the combined impact of the personal tax system and the withdrawal rates applying to means tested benefits. This is because withdrawal rates can have the same economic impact as tax rates — the effect on a person’s disposable income is the same whether part of a payment is withdrawn or an additional amount of tax is collected. For example, the pension assets test acts like a tax on savings, and can affect savings decisions in the same way.

While in general tax rates and withdrawal rates should have the same impact on decisions, the impact is not identical where they use different income bases. In addition, timing differences can also alter the effective tax rate at a point in time by comparison with the final effective tax rate after a tax assessment. The practice of taxing and making payments to people at the same time (‘churn’) can be criticised on the grounds of administrative cost, but has the advantage of allowing governments to target taxes and transfers with much greater precision than would be possible if it simply reduced tax liabilities. Taxing and making payments at the same time allows the tax and transfer systems to reflect work responsiveness, the presence of children, and other characteristics.

The impact of taxes and withdrawal rates may also differ because an individual may react differently to having their earned income taxed compared to having a transfer payment reduced, even though the effect on their net disposable income is the same.

These different characteristics of tax and withdrawal rates, and of the tax and transfer systems, suggest that decisions about imposing tax rates through the tax and transfer systems should consider the relative strengths of the two systems.

Principles

The tax system should limit the extent to which people face high effective tax rates, particularly for those who are most likely to reduce their work effort as a result.

Effective tax rates should be tailored to individual circumstances to support workforce participation for those who are able to work and choose to do so. Tailoring should be achieved through adjusting withdrawal rates on transfer payments rather than through tax mechanisms.

Supporting work in an ageing population

Levying taxes efficiently is likely to become increasingly important as the population ages and there are fewer working people as a proportion of the population. Over the next four decades, the retirement age population is expected to grow faster than the working age population. By 2049, over one fifth of the population is projected to be aged 65 or more, compared to around 13 per cent in 2009. As Chart A1–10 illustrates, a corresponding reduction is expected in the relative size of the working age population, and this suggests that economic growth will slow.

A1 — Personal income tax

Page 19

Chart A1–10: Historic and projected labour force participation rates

50

55

60

65

70

75

80

1978-79 1989-90 2000-01 2011-12 2022-23 2033-34 2044-4550

55

60

65

70

75

80

People aged 15 and over People aged 15-64

Participation rate (%) Participation rate (%)

Year

Source: Treasury projections. Australia’s current workforce participation rates are high compared to those in the past, at 65.4 per cent in 2008 compared to 60.8 per cent in 1979 (ABS 2009f). Maintaining high levels in the future will require a tax and transfer system that supports work. The Council of Australian Governments (COAG) made the following comment on this issue:

… with an ageing population, there will be relatively fewer Australians of working age. To avoid putting too great a burden on those already in work, more Australians need to realise their potential by entering or rejoining the workforce (COAG 2006).

Key groups where Australian participation rates are relatively low compared to other OECD countries include prime aged men, women of child-bearing age, and older men and women.5 This suggests that incentives for existing workers to remain in work are critical. In addition, increases in participation by those not currently working should be supported and encouraged, whether they are not currently working because of illness or disability, caring responsibilities, age, home duties or the care of children.

High effective tax rates reduce incentives to work and save

The personal income tax rates scale is often the most visible component of the effective tax rates that people face. However, other parts of the tax system can raise effective tax rates above the marginal rates in the tax scale. The Medicare levy collects 1.5 per cent of income, and is phased in at a 10 per cent rate over an income range that is not announced until the end of the tax year. Means tested offsets, such as the senior Australians tax offset and the low income tax offset, also increase effective tax rates when they are being withdrawn.

Average tax rates in Australia are in the bottom third of the OECD for single people at 67 per cent of the average wage and at 100 per cent, and are still below the OECD average at 167 per cent. The top marginal rate is in the bottom half of those in OECD countries, and the

5 In 2005, Australia was ranked 25th for prime aged men (aged 25 to 54 years), 23rd for women of child-bearing age (aged 25 to 44 years), and 13th and for older men and women (aged 55 to 64 years).

Australia's future tax system — Report to the Treasurer

Page 20

corresponding threshold is set slightly above the OECD average in terms of multiples of average earnings (OECD 2009d).6

Other elements of the tax system can result in very high effective tax rates at particular points (such as thresholds for HELP repayments and the Medicare levy surcharge). Crossing these thresholds results in a higher rate of tax being levied on every dollar of income, not only on income over the threshold. This means that people’s disposable income can fall even though their private income has increased. Work by Chapman and Leigh identified a statistically significant degree of ‘bunching’ of incomes slightly below the HECS thresholds, suggesting that these very high effective tax rates do have an impact on behaviour (Chapman & Leigh 2006).

The transfer system overlays additional financial incentives on the tax system, because payment withdrawal rates interact with taxes. Recent studies of effective marginal tax rates (EMTRs) in Australia suggest that around 90 per cent of working age Australians face EMTRs below 40 per cent (Harding et al. 2006; Kalb 2007). (EMTRs measure the proportion of an extra dollar of income that is lost due to taxes and transfer withdrawals.) Due to the widening of eligibility for means tested family assistance, the proportion of working age Australians facing EMTRs over 50 per cent increased between 1996–97 and 2006–07, from 4.8 per cent to 7.1 per cent. However, the proportion facing EMTRs over 80 per cent declined over this period.

EMTRs do not give a complete picture of the incentive effects of the tax and transfer systems. It is difficult to fully capture these incentives, which may also be affected by factors such as child care costs, public housing rent-setting, and child support liabilities or receipts. More broadly, consumption and payroll taxes also affect the returns to work, and even corporate income taxes may be borne at least in part by workers (see Section B1 Company and other investment taxes).

In certain situations, EMTRs may not be an appropriate measure of the returns to work. For example, a person out of work may be less influenced by the effective tax rate on a small increase in earnings than by the effective tax rate when they move from not working to working — a much larger increase in private income. Effective tax rates on these larger increases in private income are often called participation tax rates (PTRs).

Research looking at the labour market transitions of Australian families over time found that PTRs have a moderate negative effect on the probability that women will enter employment, and a very large negative effect on the probability that an unemployed person will find work (Dockery et al. 2007). This may be a particular concern for jobless couple families with children, who can face high PTRs when one member takes up work. Among couple families with children under 15 where the woman is not working, around 19 per cent of the men are also out of work (ABS 2009g). This is in sharp contrast to males in couples generally, who have markedly higher rates of employment.

6 Average rates include employee social security contributions.

A1 — Personal income tax

Page 21

Chart A1–11: Participation tax rates

0

10

20

30

40

50

60

70

0 30,000 60,000 90,000 120,000 150,000 180,000 210,000 240,000

Private income ($pa)

0

10

20

30

40

50

60

70

One earner couple, two children

Single person

Participation tax rate (%) Participation tax rate (%)

Source: Treasury estimates. Chart A1–11 shows that, for an adult in a jobless couple family with two children, more than 58 per cent of their pay will be lost to tax and payment withdrawal if one member takes a job at the minimum wage. However, these high tax rates allow tax rates to be lower elsewhere in the system, which means that the overall effect on incentives is unclear.

To gain a clearer picture of the incentive effects of the tax and transfer systems, measures of effective tax rates need to be combined with empirical research on the responsiveness of the people who face them. The Australian Fair Pay Commission recently commissioned research into how much certain groups know about the impacts of the tax and transfer systems, and their motivation to work. This work established that people have limited theoretical understanding of how transfers are affected by changes in income, but also that once people are in receipt of a transfer payment, they may protect their entitlements by avoiding work that would move them off benefits.

Dandie and Mercante (2007) reviewed the literature on the responsiveness of various Australian groups, and found that partnered men, single men and single women without children are generally less responsive to changes in wages than partnered women. Lone parents tend to be more responsive than partnered women. Responsiveness varies according to factors such as level of education (higher responsiveness for those with lower education levels), whether the individual works part-time or full-time (higher responsiveness for part-time workers), and income level (generally higher responsiveness for those with lower incomes).

Finding

Effective tax rates can be high for some people, including for those likely to reduce their level of work as a result.

Australia's future tax system — Report to the Treasurer

Page 22

Reform directions — improve simplicity and incentives with a high tax-free threshold and a constant marginal rate for most people

Recommendation 2:

Progressivity in the tax and transfer systems should be delivered through the personal income tax rates scale and transfer payments. A high tax-free threshold with a constant marginal rate for most people should be introduced to provide greater transparency and simplicity.

The personal income tax rates scale is a key contributor to progressivity in the tax and transfer systems.

A new personal income tax rates scale would have a high tax-free threshold and a constant marginal rate for most people. This could take the form of a constant rate of tax for most taxpayers, with a higher rate for those on very high incomes. An indicative approach to implementing the personal income tax rates scale for Australian residents is shown in Table A1–1. The indicative scales shown in the table result in lower personal taxes for people with low incomes, and give rise to broadly comparable average tax rates for those with taxable incomes up to $100,000.

Table A1–1: Indicative personal income tax rates scale Taxable income ($) Rate (%)

0 – 25,000 0 25,001 – 180,000 35

180,001 + 45

This approach sets the tax-free threshold at $25,000, where income support recipients would either have exhausted their payments or have substantial private income. This would mean that more than 1.2 million additional people would no longer pay tax — over 10 per cent of current taxpayers. Many of these would not have to file a tax return (although some would continue to do so to claim withheld amounts or imputation credits). Setting the tax-free threshold at this level would remove the need for the low income tax offset and limit the need for the senior Australians tax offset.

Above the tax-free threshold, a constant rate of 35 per cent would apply for most taxpayers. In the example provided in Table A1–1, over 97 per cent of people over the tax-free threshold would be subject to the 35 per cent rate of tax. A constant rate of tax of this kind has the advantage of transparency for most working people. Combined with a tax exemption for transfer payments, it would be much easier for people to understand their marginal rate of tax.

A higher rate of tax could be applied to those on around three times average wages — $180,000 in this example. A top marginal rate that began at this multiple of average wages would be slightly above the OECD average, although internationally there is a high degree of variation in the level at which top marginal rates apply. For example, in the United States, the top marginal rate applies from nine times average wages, while in the United Kingdom it is 1.2 times average wages. Countries with top personal marginal tax rates that apply from around three times average wages include Canada, France, Italy and Korea.

A1 — Personal income tax

Page 23

This indicative personal income tax rates scale broadly reflects the aspirational tax cuts proposed by the Government for introduction in 2013–14. Introducing a rates scale of this kind would have a number of advantages. It would provide a higher level of transparency to individual taxpayers, as the great majority would have a single marginal rate. It would also improve the relationship between the tax and transfer systems: allied with a tax exemption for transfer payments, more people would be in only one system at any given time.

A tax scale of this kind could be implemented gradually, taking into account existing settings on marginal tax rates, offsets and the definition of income.

Incentives to work

A personal income tax system that provides more support to workforce participation should be delivered in a transparent way.

Currently, most taxpayers have more tax withheld throughout the year than is necessary, because part of the effective tax-free threshold is given through the low income tax offset (LITO) and is only available after the taxpayer files their tax return. By incorporating LITO into the explicit tax scale, people would receive better financial returns to work throughout the year, strengthening participation incentives.

As well as incorporating the existing LITO into the tax scale, a substantial increase in the tax-free threshold would increase the attractiveness of work to low-income earners (including secondary earners), who are typically more responsive to effective tax rates.

Reconfiguring the dependency offsets would better target support to those unable or not expected to work, which would improve participation incentives for those secondary earners not in these categories.

These changes build upon those proposed for the transfer system. Together, these reforms would better support employment and position Australia to meet the coming demographic challenges.

Taxing people as individuals In designing a personal tax system based on anything other than a strictly flat rate of tax, a fundamental choice has to be made about the unit of assessment — that is, whether people are taxed as individuals or as part of a couple or family. This choice involves judgments about how people in couples operate in society compared to single people and about the needs of other family members, particularly children.

The key consideration in determining the unit of assessment is how it gives effect to contemporary social norms about individuals and couples. The judgment implied in the choice of unit is whether horizontal equity is concerned with treating individuals or couples in like circumstances alike. It has particular practical implications for workforce participation.

Specifically, the unit of assessment determines the marginal tax rate that each person in a couple faces. There are advantages in having each partner face different marginal tax rates, according to their earnings and other characteristics. For example, in a couple where one partner is the primary earner and the other earns less, perhaps working part-time and caring

Australia's future tax system — Report to the Treasurer

Page 24

for children, imposing the same marginal tax rate on both may cause the secondary earner to reduce their work effort. By contrast, a lower marginal rate for that person may encourage and support work.

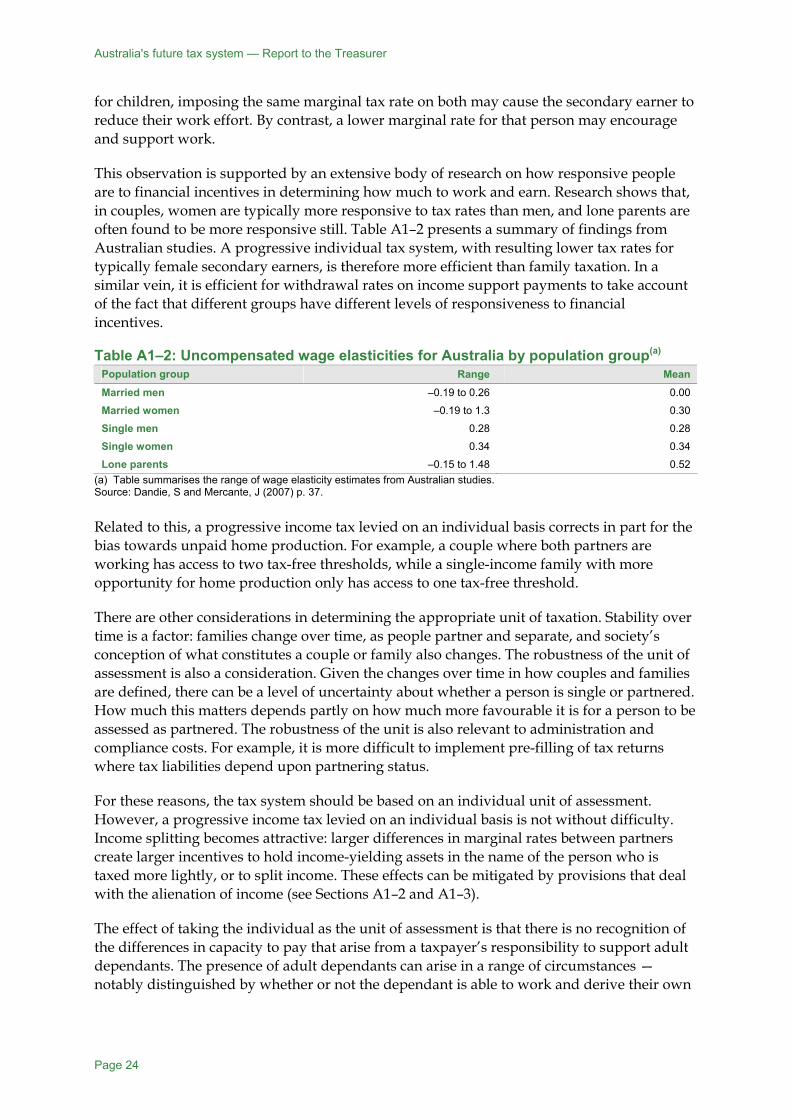

This observation is supported by an extensive body of research on how responsive people are to financial incentives in determining how much to work and earn. Research shows that, in couples, women are typically more responsive to tax rates than men, and lone parents are often found to be more responsive still. Table A1–2 presents a summary of findings from Australian studies. A progressive individual tax system, with resulting lower tax rates for typically female secondary earners, is therefore more efficient than family taxation. In a similar vein, it is efficient for withdrawal rates on income support payments to take account of the fact that different groups have different levels of responsiveness to financial incentives.

Table A1–2: Uncompensated wage elasticities for Australia by population group(a) Population group Range Mean Married men –0.19 to 0.26 0.00

Married women –0.19 to 1.3 0.30

Single men 0.28 0.28

Single women 0.34 0.34

Lone parents –0.15 to 1.48 0.52 (a) Table summarises the range of wage elasticity estimates from Australian studies. Source: Dandie, S and Mercante, J (2007) p. 37. Related to this, a progressive income tax levied on an individual basis corrects in part for the bias towards unpaid home production. For example, a couple where both partners are working has access to two tax-free thresholds, while a single-income family with more opportunity for home production only has access to one tax-free threshold.

There are other considerations in determining the appropriate unit of taxation. Stability over time is a factor: families change over time, as people partner and separate, and society’s conception of what constitutes a couple or family also changes. The robustness of the unit of assessment is also a consideration. Given the changes over time in how couples and families are defined, there can be a level of uncertainty about whether a person is single or partnered. How much this matters depends partly on how much more favourable it is for a person to be assessed as partnered. The robustness of the unit is also relevant to administration and compliance costs. For example, it is more difficult to implement pre-filling of tax returns where tax liabilities depend upon partnering status.

For these reasons, the tax system should be based on an individual unit of assessment. However, a progressive income tax levied on an individual basis is not without difficulty. Income splitting becomes attractive: larger differences in marginal rates between partners create larger incentives to hold income-yielding assets in the name of the person who is taxed more lightly, or to split income. These effects can be mitigated by provisions that deal with the alienation of income (see Sections A1–2 and A1–3).

The effect of taking the individual as the unit of assessment is that there is no recognition of the differences in capacity to pay that arise from a taxpayer’s responsibility to support adult dependants. The presence of adult dependants can arise in a range of circumstances — notably distinguished by whether or not the dependant is able to work and derive their own

A1 — Personal income tax

Page 25

income. These considerations are generally best addressed through the transfer system, while some horizontal equity benefits can be provided by dependant offsets.

Principle

The personal income tax system should generally tax people as individuals.

Retain the individual as the primary unit of assessment

The Australian tax system has always been based on individual assessment. This is one of the most important ways in which the personal tax system supports participation, by allowing different marginal tax rates to apply to each person in a couple. However, the system does include some elements that take account of the presence of a partner or children, and their circumstances.

Dependency offsets are examples of tax provisions that take account of partner or family circumstances. The senior Australians tax offset allows any unused value to be claimed by a person’s partner, if they have one. The Medicare levy low income phase-in arrangements take account of family size and structure. The Medicare levy surcharge’s thresholds are based on family size and structure. The spouse superannuation contributions tax offset is available for contributions on behalf of a spouse, while the medical expenses tax offset allows claims for family members as well as for the taxpayer themselves. These provisions are discussed in more detail in Annex A1.

These provisions depart from the principle that tax should be levied on each individual separately. They are a source of complexity in the system, often because the tax system does not routinely collect spouse information — a factor that can make compliance activity difficult. These provisions also tend not to provide responsive assistance in those cases where they are intended to support the costs of living. In many cases, more targeted support is available through the transfer system or other spending programs. They can also have a negative impact on participation incentives, where they affect dependants who could otherwise work.

There could be a case for optional couple assessment for people of retirement age or of late retirement age, on the grounds that these people are not expected to work and the great majority do not. Joint assessment would provide the same benefits to couples who have not shared their assets equally or where one member receives a superannuation pension from a defined benefit scheme, as for couples who have split their assets equally. Such a proposal would, however, introduce significant complexity into the tax system, by requiring the Australian Taxation Office (ATO) to assess relationships and changes in relationship status, as is currently required in the transfer system. While it is more complex, where participation incentives are not important, relaxation of the individual unit of assessment can assist other policy objectives.

Australia's future tax system — Report to the Treasurer

Page 26

Findings

The current tax system is generally based on taxing people as individuals. However, some provisions take account of couple or family circumstances.

Individual assessment supports workforce participation by secondary earners, by allowing different effective tax rates for each person in a couple.

Where participation incentives are not important, relaxation of the individual unit of assessment can assist other policy objectives.

Recommendation 3: The primary unit in the personal tax system should continue to be the individual, and subsidies for dependants through the tax system should be restricted (see Recommendation 6a). However, there could be a case for optional couple assessment for people of late retirement age.

The taxation of transfer payments Many Australians receive transfer payments, often at the same time as they pay tax. Income support and supplementary payments replace or supplement wages and salary for their recipients.

Commonwealth transfer payments are cash payments provided by the Australian government to individuals and families, including Age pensioners, veterans, people with a disability, carers, unemployed people, and people affected by natural disaster. Transfers play a vital role in the government’s redistributive policies and take a variety of forms, from income support and supplementary payments to cash payments for families with children.

Reflecting their poverty alleviation objectives and redistributive goals, cash transfers are typically targeted at low-income individuals and are designed to help recipients pay for daily living expenses and otherwise support themselves. Income support payments in particular assist poor households or those likely to fall into poverty without the transfer.

The rate of income support includes the base payment and any supplementary payments, such as Rent Assistance, Telephone Allowance and Pharmaceutical Allowance. These components should be treated on a consistent basis for tax purposes. The same treatment should also apply to government scholarships.

Family assistance has some different characteristics. It is not wage-like in its nature, as it is paid in addition to wages or income support for costs associated with children. Its tax status need not be the same as the tax status of income support.

Transfer payments have a mix of tax treatments