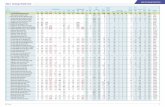

A New Milestone for Exchange Traded Funds...exchange traded funds (ETFs) have evolved from an early...

8

A New Milestone for Exchange Traded Funds

Transcript of A New Milestone for Exchange Traded Funds...exchange traded funds (ETFs) have evolved from an early...

A New Milestone for Exchange Traded Funds

Semi-transparent active exchange traded funds (ETFs) have evolved from an early concept 10 years ago to a pair of products now live in the market. Despite launching in the midst of COVID-19 market disruption, their trading experience so far has been highly encouraging.

1

Ever since the introduction of

the first US ETF in 1993, one of

the vehicle’s core attributes has

been full transparency into the

basket or portfolio holdings.

This requirement has kept most active equity

and many fixed-income strategies from the

marketplace, based on concerns that the

portfolios would be subject to front-running

or free-riding.

A major milestone for the industry occurred

on March 31, 2020, when American Century

Investments launched a pair of active ETFs

that were the first of their kind. Trading under

the ticker symbols FDG and FLV, these ETFs

leverage intellectual property developed by

Precidian Investments known as ActiveShares®.

This strategy enables an asset manager to

disclose its ETF holdings with the same

frequency as its mutual funds.

The key to the Precidian ActiveShares

structure is the creation of a new participant

in the ecosystem, the authorized participant

representative (APR). The APR(s) are hired

by the ETF sponsor and contracted by the

authorized participant (AP) to trade the basket

on its behalf. The only entities that could serve

in this capacity would be “agency-only” trading

firms. The ETF issuer would also hire a Verified

Indicative Intraday Value (VIIV) agent to stream

the value of the underlying holding every second

to the consolidated tape. With this information

and other publicly disclosed information such

as the prospectus, statement of additional

information (SAI) and Fund Fact Sheets, industry

participants would have the data needed to “make

markets,” as they do for daily disclosed ETFs.

State Street has been involved with the creators

and licensees of the ActiveShares structure for

several years, helping to conceptualize and develop

the operating model and workflows to service

the product. This has included engagement with

the Securities and Exchange Commission (SEC)

staff and commissioners to help educate them

on the structure and our automated servicing

capabilities. We were the first and only ETF service

provider asked to participate in the ActiveShares

ETF Working Group that ultimately designed the

operating model and shared those insights with

the broader ETF ecosystem.

We discussed with Frank Koudelka and

Jeff Sardinha, our ETF specialists and

Chris Scharver, responsible for the APR role

at State Street, to know how the launch went,

how the products are trading and what they

are hearing from the marketplace.

“ There are always lessons learned with every new innovation and launch.”

2

How did the launch go? What did you learn?

The successful seeding and listing of the

products occurred on March 31 and April 2.

The implementation was accomplished with

poise and confidence across all market

participants that had a hand in the initial

launch. The project planning began in earnest

prior to the Rule 19B-4 filing in June 2019.

This laid the groundwork for all parties to

confidently execute amidst the unprecedented

market volatility linked to COVID-19, as well as

the new operating complexities of alternative

working arrangements, school and business

closures, and social distancing. The initial

seed orders were placed, processed and

settled within the expected timeframes,

including the introduction of the new entrant

to the ecosystem, the APR. Since launch,

the funds have had regular primary market

activity and have introduced a second APR.

There are always lessons learned with every

new innovation and launch, and the American

Century Investments ActiveShares were no

different. Three particular themes stand out.

Planning

Take the time and effort to update your

project plans for the operational nuances of

the ActiveShares wrapper. Yes, this is an ETF

and functions as an ETF within an operational

ecosystem that exists today. But, there are

some operational differences that need to

be mapped out and understood by all parties.

The key is to educate, plan for and test

those nuances. State Street (as back-office

administrator, custodian and APR), American

Century and the rest of the support firms

(distributor, exchange, VIIV agent) for these

products set aside ample time for different

testing runs, including a full end-to-end model

office that took place over a period of several

months for baskets, trading, etc.

Overcommunication

The ActiveShares process flow required

the creation of a new role, APR, in the middle

of the primary market clearance. While this

change brings a new party to the table, it also

slightly changes the expectations of another

party already at the table, the AP. Thus, you will

want a single entity to coordinate communication

and instill the expectation of overcommunication

across the entire ecosystem. This helps to make

sure that members are not caught off guard or

assume this ETF works like others with similar

investment profiles, so they know exactly what is

expected throughout the lifecycle.

“ The key is to educate, plan for and test the operational nuances.”

3

Flexibility

Do not underestimate the work required to

establish the new APR role. State Street has

been involved in the ETF ecosystem, including

trading AP restricted names (assisted trading),

lending the ETFs and underlying portfolios

(securities lending) and exchanging currencies

(foreign exchange). Even with all of our experience

servicing ETFs, the APR role was new and

different. Although we have been involved

in the ActiveShares Operating Group for

several years, we assembled a strong project

management team when Precidian received

their SEC notice of approval in April 2019.

The working group included compliance, legal,

risk, operations, trading, technology, custody

servicing, etc., to ensure all parties had input

to make the role successful. Receiving the

fund’s confidential portfolio information is

a monumental undertaking not to be dealt

with lightly. To be successful, we knew we

needed to be flexible and understanding.

There would be unforeseen issues that may

require changes to workflow, systems

modeling and participants’ expectations.

How are the products trading?

Has there been activity since the launch?

The products have been trading efficiently,

with bid-ask spreads of approximately

20–25 bps. The first trading day was April 2

and we have consistently seen trading of 15,000

to 25,000 average daily volume. Assets grew

from US$8 million to over US$23 million during

the first month since launch.

What are you hearing from the marketplace?

This was one of the most-watched and

anticipated launches in the last several years.

Active managers have been looking for a way

to introduce their investment strategies to

the market using the ETF wrapper. State Street

has been conducting ongoing education sessions

with more than 50 of the top asset management

firms in the industry, who find the ETF structure

appealing based on its advantages of liquidity,

ease of trading, and cost and tax efficiency.

Many firms wanted to see how the first

products performed before making their

own leap into the market. American Century

launched in a volatile market, with large

swings in the Dow Jones, S&P and NASDAQ

averages and significant volume. The major

areas of industry interest — spreads, volume

and flows — have all seen positive trends so

far, which has renewed the interest of those

on the sidelines.

“ You will want to instill the expectation of overcommunication across the entire ecosystem.”

4

We are anticipating additional activity and

launches in the short- and medium-term.

It is important to note that the ActiveShares

structure was the first to gain approval and

adoption in the marketplace. There are two

licensees (Legg Mason and Gabelli) that have

received their exemptive relief approvals and

are in different phases of their Rule 19b-4,

prospectus, and registration filings. Other

firms have indicated that they will leverage

the ActiveShares structure and file soon.

What’s next?

We have several other clients that

are also developing active ETF capabilities.

While these firms may be in various stages

of development, there is a level of consistency

in the delivery model used to bring ETFs to

market. The planned approach is known as

the proxy basket structure, where market

makers use proxy baskets and other information

publicly disclosed to value ETFs and ensure

efficient trading. Authorized Participants (APs)

can create and redeem shares directly with

the issuer, just as they do for disclosed ETFs.

1. Fidelity is using proprietary intellectual

property that they will license to additional

asset managers. What is interesting about

the Fidelity approach is they are the only

licensor that has the perspective of both

an active manager and ETF issuer.

The Fidelity model will come with both

platform and distribution benefits.

2. Natixis has licensed its methodology from

the New York Stock Exchange. The firm will

tap into the investment expertise from affiliate

managers — Harris Associates, Loomis Sayles

and Vaughan Nelson, to launch both single and

multimanager ETFs.

3. T. Rowe Price has received approval for its

own structure. Other asset managers have

been engaged with T. Rowe Price to replicate

the methodology in its filing. T. Rowe Price

will not charge a license fee. Additionally,

T. Rowe Price is planning to provide other

services to assist active ETF providers.

Our ETF servicing team is targeting launches

for these and other clients interested in

disclosing a basket that is designed to replicate

the performance of the underlying portfolio, but

is not a pro rata slice of the fund. These vehicles

will leverage daily reporting supported by our

Performance and Investment Analytics team

to assist market makers in understanding how

the proxy basket performance compares to

the actual fund holdings.

5

“ While firms may be in various stages of product development, there is a level of consistency in the delivery model used to bring ETFs to market.”

6

This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on

State Street CorporationOne Lincoln Street, Boston, MA 02111

www.statestreet.com

as such. The whole or any part of this report may not be reproduced, copied or transmitted, or any of its contents disclosed to third parties without State Street’s express written consent.

©2020 State Street Corporation All Rights Reserved3092513.1.1.GBL.INSTExpiration date: 5/31/2021

For more information, please contact:

Frank Koudelka is responsible for

new product development strategy

and specialized ETF products.

Jeff Sardinha is a member of State Street’s

ETF Bridge team, working directly with

participants in the ETF ecosystem to

design and implement operating models

for ETFs and keep them current on market

developments. He had a direct role in

helping build the operational framework

for semi-transparent active ETFs.

Chris Scharver is a member of the

specialized trading team in State Street

Global Markets.

FRANK KOUDELKA

Senior Vice President

+1 617 662 4749

JEFF SARDINHA

Managing Director

+1 617 866 7283

CHRIS SCHARVER

Vice President

+1 617 664 8426