A N EW A PPROACH T O E DF V ALIDATION ISDA 2000 2 VALIDATION BACKGROUND What is meant by Validation?...

25

A NEW APPROACH TO EDF VALIDATION ISDA 2000

-

Upload

phoebe-flowers -

Category

Documents

-

view

217 -

download

3

Transcript of A N EW A PPROACH T O E DF V ALIDATION ISDA 2000 2 VALIDATION BACKGROUND What is meant by Validation?...

A NEW APPROACH TO

EDF VALIDATION

ISDA 2000

2

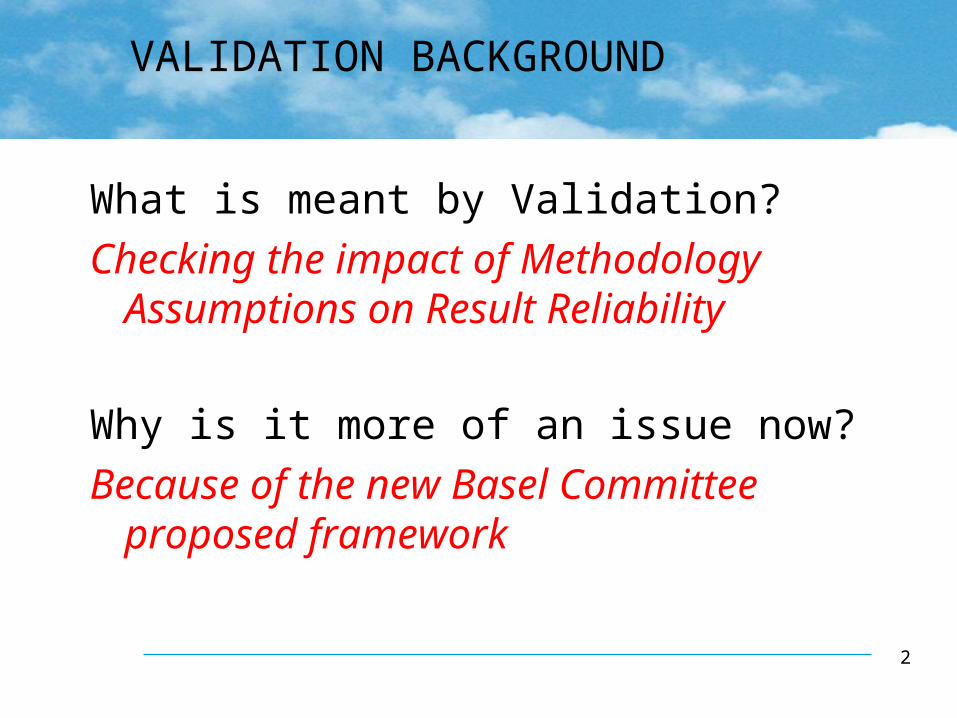

VALIDATION BACKGROUND

What is meant by Validation?Checking the impact of Methodology

Assumptions on Result Reliability

Why is it more of an issue now?Because of the new Basel Committee

proposed framework

3

VALIDATING METHODOLOGIES

Common computations call on:

Market Price assumptions Rating Judgment assumptions Historical Reference assumptions Economic Environment assumptions

What are their limitations?

4

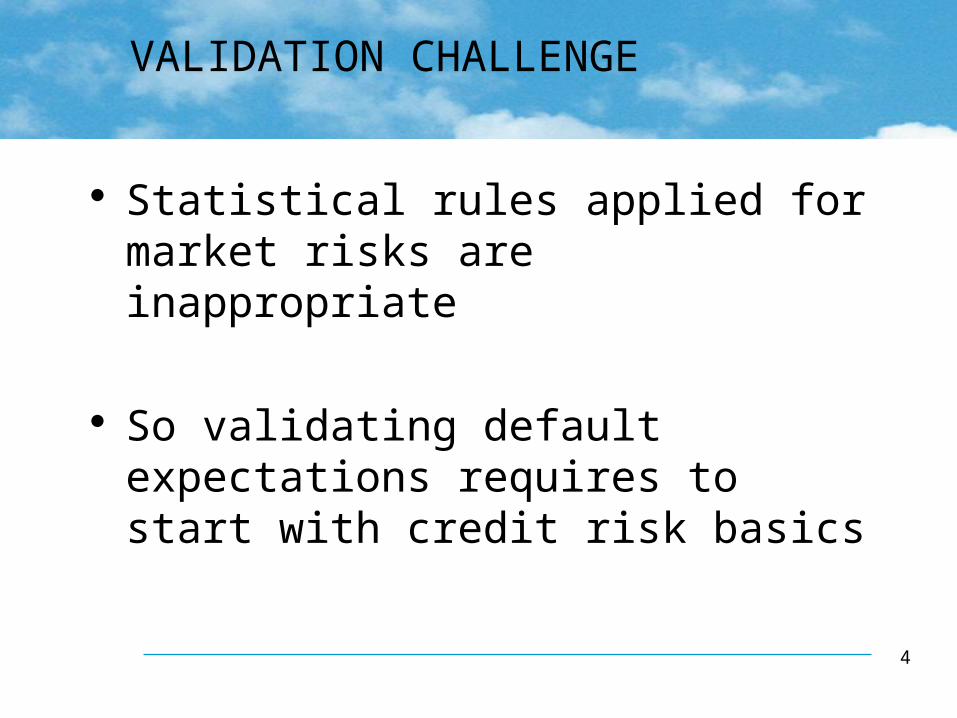

VALIDATION CHALLENGE

Statistical rules applied for market risks are inappropriate

So validating default expectations requires to start with credit risk basics

5

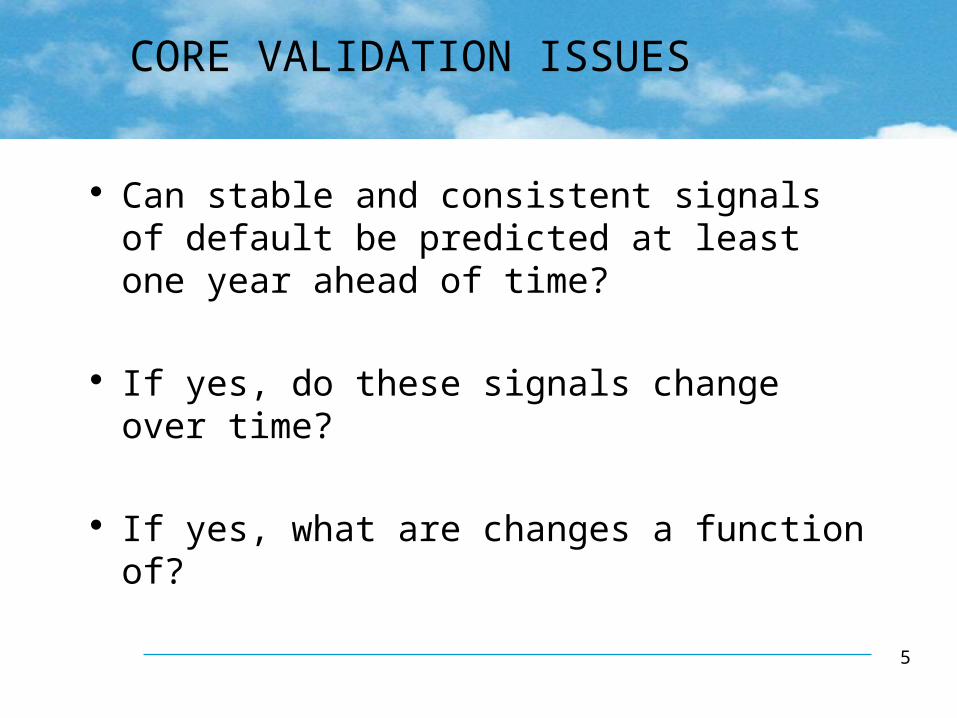

CORE VALIDATION ISSUES

Can stable and consistent signals of default be predicted at least one year ahead of time?

If yes, do these signals change over time?

If yes, what are changes a function of?

6

ADDRESSING VALIDATION ISSUES

With the Default Filter(TM) Probability of Default computation methodology

Methodology: “Model assisted numerical analysis” allowing macro-economic and specific company simulations

Default: Missing committed payment after 3 months grace period

7

VALIDATION DATA

The issue with historical data:

Choice of a good reference base Choice of time period Addressing missing data Addressing data reliability

8

VALIDATION DATABASES

.

DATABASETOTAL NUMBER

OFBORROWERS

INDUSTRIESREPRESENTED

MONTH-TO-DATECOMPLETION

UPDATE

PLANNEDCOMPLETION

DATE

Asia( Excluding Japan)

11,000 ManufacturingConstructionFinanceServicesOthers

455616905533332428

Maintain

Japan 20,000 ManufacturingConstructionFinanceServices

1078173160478

Expand

Western Europe 20,000 ManufacturingConstructionFinanceServices

15344025251900

Expand

9

BUILDING REFERENCE DATABASES

Driven by Distance and Homogeneity measures

0

CR

TD/TNW

GPM

Complemented Ranked Datapoints vs Current Ratio (-) values.

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Cu

rre

nt

Ra

tio

(-) Nondefaults

Defaults

Added Nondefaults

Added Defaults

10

HOMOGENEITY OF COMPLEMENTARY DATA

ILLUSTRATION OF DISTRIBUTION OF GREATER CHINA COMPANIES CREDIT FACTOR VALUES AGAINST OTHER ASIAN

CREDIT FACTOR VALUES

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

Dis

tan

ce f

rom

no

n d

efau

lt o

rig

in

Other_Asian_Portfolio

Greater ChinaCompanies_Portfolio

11

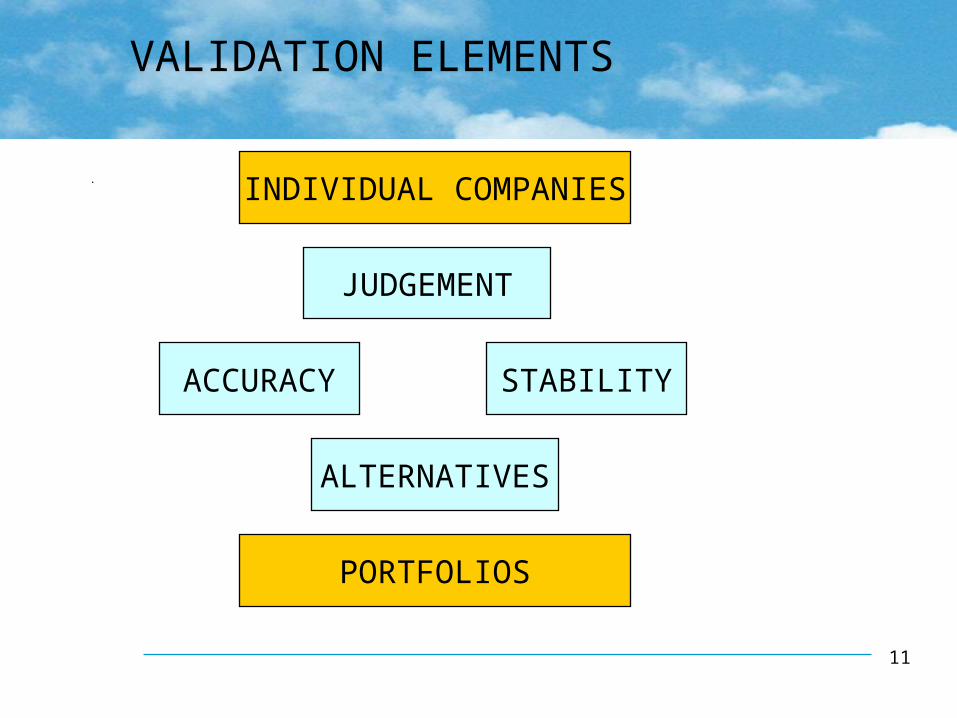

VALIDATION ELEMENTS

.

ACCURACY STABILITY

INDIVIDUAL COMPANIES

PORTFOLIOS

ALTERNATIVES

JUDGEMENT

12

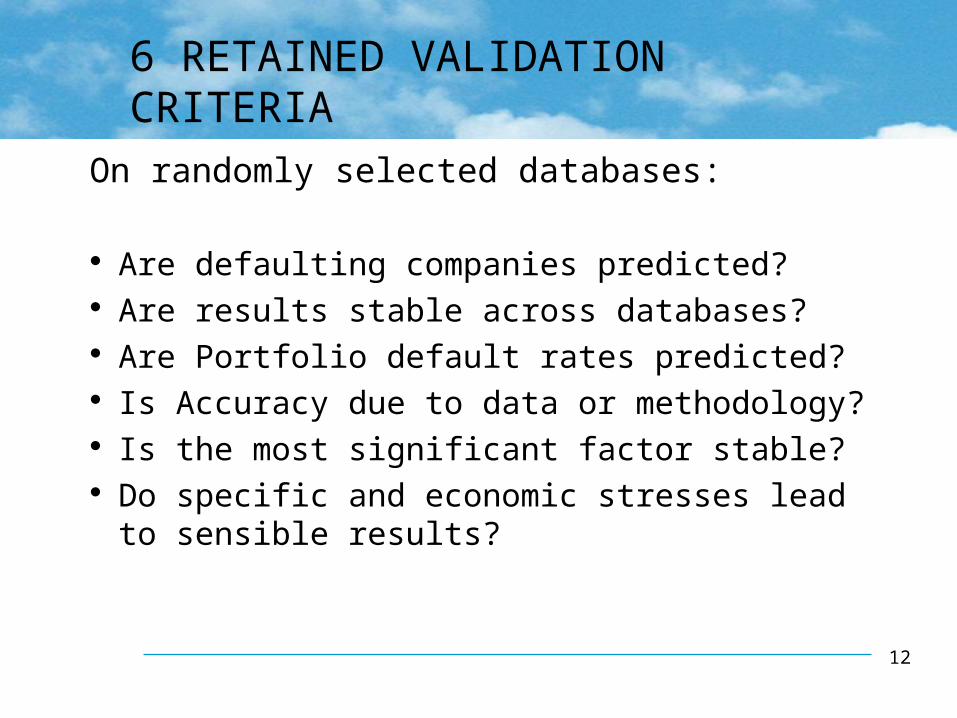

6 RETAINED VALIDATION CRITERIA

On randomly selected databases:

Are defaulting companies predicted? Are results stable across databases? Are Portfolio default rates predicted? Is Accuracy due to data or methodology? Is the most significant factor stable? Do specific and economic stresses lead

to sensible results?

13

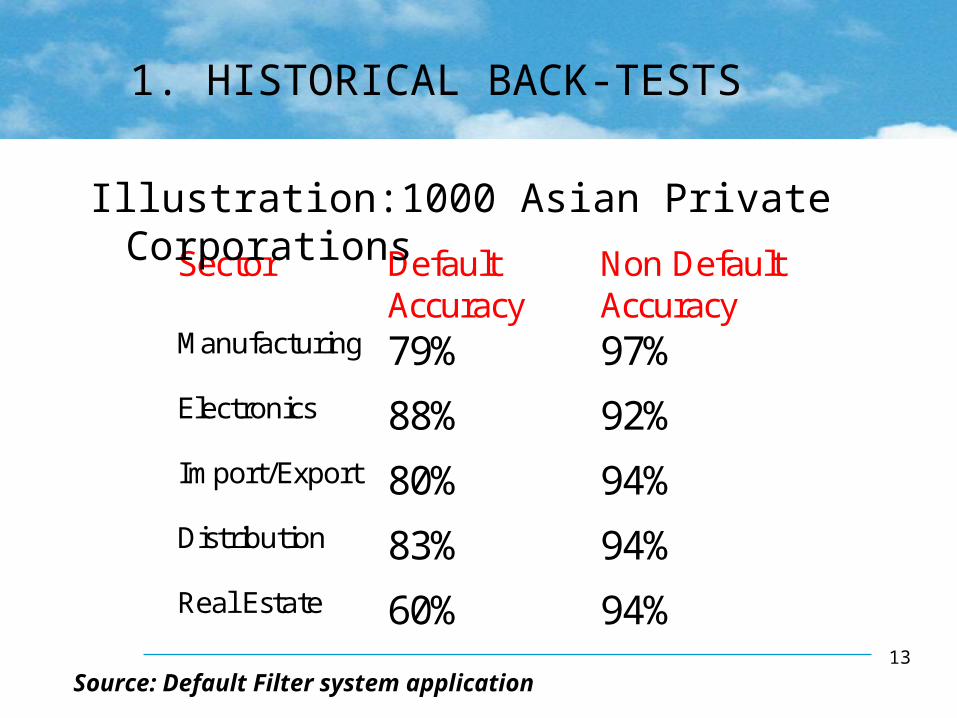

1. HISTORICAL BACK-TESTS

Source: Default Filter system application

Sector DefaultAccuracy

Non DefaultAccuracy

Manufacturing 79% 97%Electronics 88% 92%Import/Export 80% 94%Distribution 83% 94%Real Estate 60% 94%

Illustration:1000 Asian Private Corporations

14

2. COMPARATIVE BACK-TESTS

Source: Default Filter system application

Comparative Back-Testing AccuracyASIAN CONSTRUCTION INDUSTRY

0%

20%

40%

60%

80%

100%

120%

1 17

33

49

65

81

97

113

129

145

161

177

193

209

225

241

257

273

289

305

321

337

353

369

385

401

417

433

449

465

481

497

Sample Number

Accu

racy L

evel

Illustration: Same data but alternative methodologies

Default FilterNo Default Portfolio Default

15

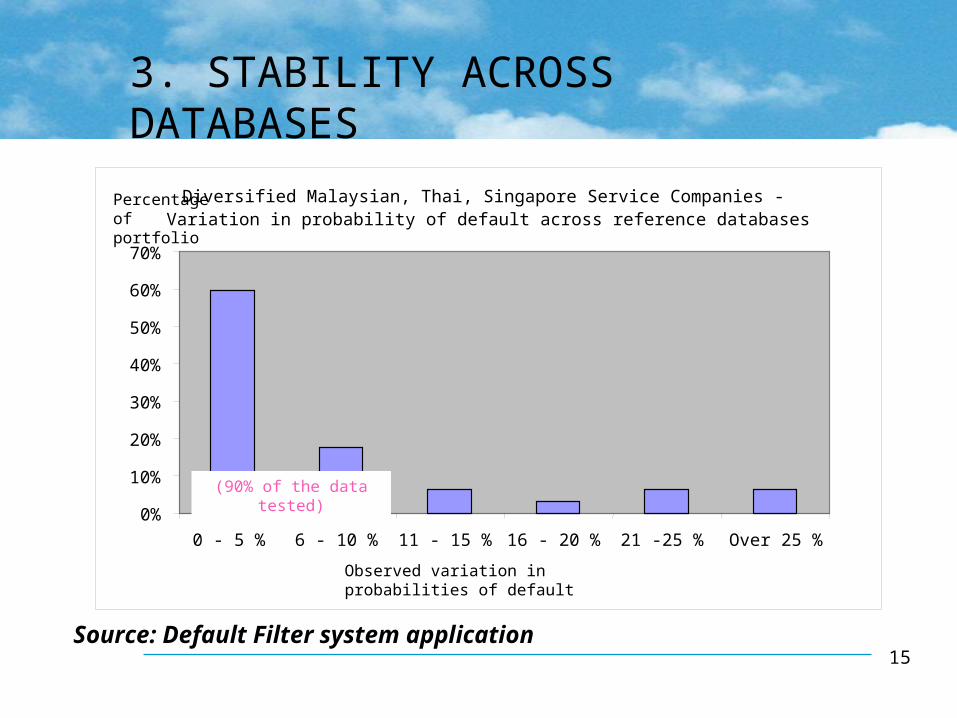

3. STABILITY ACROSS DATABASES

0%

10%

20%

30%

40%

50%

60%

70%

0 - 5 % 6 - 10 % 11 - 15 % 16 - 20 % 21 -25 % Over 25 %

Diversified Malaysian, Thai, Singapore Service Companies - Variation in probability of default across reference databases

Percentage of portfolio

Observed variation in probabilities of default

(90% of the data tested)

Source: Default Filter system application

16

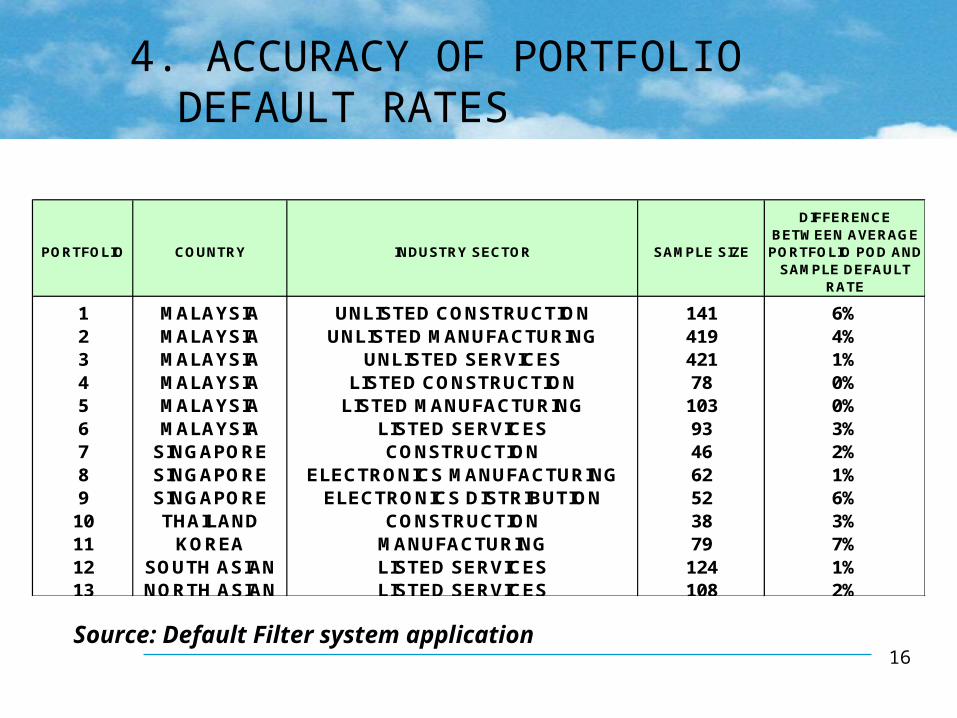

4. ACCURACY OF PORTFOLIO DEFAULT RATES

PORTFOLIO COUNTRY INDUSTRY SECTOR SAMPLE SIZE

DIFFERENCE BETWEEN AVERAGE PORTFOLIO POD AND

SAMPLE DEFAULT RATE

1 MALAYSIA UNLISTED CONSTRUCTION 141 6%2 MALAYSIA UNLISTED MANUFACTURING 419 4%3 MALAYSIA UNLISTED SERVICES 421 1%4 MALAYSIA LISTED CONSTRUCTION 78 0%5 MALAYSIA LISTED MANUFACTURING 103 0%6 MALAYSIA LISTED SERVICES 93 3%7 SINGAPORE CONSTRUCTION 46 2%8 SINGAPORE ELECTRONICS MANUFACTURING 62 1%9 SINGAPORE ELECTRONICS DISTRIBUTION 52 6%

10 THAILAND CONSTRUCTION 38 3%11 KOREA MANUFACTURING 79 7%12 SOUTH ASIAN LISTED SERVICES 124 1%13 NORTH ASIAN LISTED SERVICES 108 2%

Source: Default Filter system application

17

5. STABILITY OF MOST SIGNIFICANT FACTOR

Source: Default Filter system application

QUICK RATIO FOR A PORTFOLIO OF NON-DEFAULTING UNLISTED MALAYSIANCONSTRUCTION COMPANIES PLOTTED AGAINST RISK GRADUATION

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

GRADE 5 POD 21 - 25 %

GRADE 4 POD16 - 20 %

GRADE 3 POD11-15 %

GRADE 2 POD6 -10 %

GRADE 1 POD0-5 %

18

6. SENSITIVITY TO CHANGES

Scenario Scenario User defined scenario1 1 2 1

Probability of Default 0.15 0.25 0.24 0.05Credit Margin 3.00% 5.00% 4.80% 1.00%FACTORSTurnover 984,750 Gross Profit 427,822 Net Profit Before Tax 43,492 Net Cashflow from Operations 20,000

Current Ratio 0.80 0.64 0.40 1.34Quick Ratio 0.78 0.62 0.39 1.07

Average Collection Period (Days) 90.00 117.00 90.00 102.87Average Payment Period (Days) 30.00 39.00 30.00 17.77Total Liabilities/NTW 0.93 0.93 0.93 0.49Total Interest Bearing Debt/NTW 0.51 0.51 0.51 1.43

Times Interest Earned 1.00 0.60 1.00 2.11

NPBT over Turnover 0.04 0.03 0.04 0.24

Construction Weakening Economy Liquidity Squeeze Correlated

Source: Default Filter system application

19

SUMMARISED VALIDATION BOARD

Illustration for the Asian Electronic Manufacturing Industry

Accuracy

TotalDefault

WeightsSign

s

94%82%

6

Stability

Portfolio

Predicted

Observed

13%

12%

Significance

0%

20%

40%

60%

80%

100%

120%

1 4 7 10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

55

58

61

64

67

70

73

76

79

82

85

88

Samples

Pred

icti

ve A

ccu

racy

Default Filter Default rate

No Default

Comparison

63% < 5%

72% < 10%

76% < 20%

deviations

deviations

deviations

[0.004,6.23] ok

FactorsQuick Ratio

0.00

0.50

1.00

1.50

2.00

2.50

Soundness

20

SUMMARISED VALIDATION BOARD

Illustration for the Asian Oil and Gas Industry

Accuracy

TotalDefault

Factors

WeightsSigns

95%60%

8

[-3.38,0.02] ok

Stability

77% < 5%

Portfolio

Predicted

Observed

7%

9%

Significance

0

0.5

1

1.5

[30,100] [10,30[ [5,10[ [1,5[ [0,1[

Probability of Default

Cu

rren

t A

sset

s/S

ales

Soundness

84% < 10%

91% < 20%

Comparison

deviations

deviations

deviations0%

20%

40%

60%

80%

100%

120%

1 4 7 10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

55

58

61

64

67

70

73

76

79

82

85

88

91

94

97

100

Samples

Pred

ictiv

e A

ccu

racy

Default Filter

No Default

Default rate

21

OPPORTUNITIES FOR RISK MANAGEMENT

Compare Risk Signals between Homogeneous Groups

Developed Markets Electronics

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0 50 100 150

Po

D

Non Japan Asia Electronics

0.00

0.20

0.40

0.60

0.80

1.00

1.20

0 50 100 150 200

Po

D

•Current Profile•For 10% decrease in Sales

Legend:

22

1997 Probability of default of banks in Asia Under Normal Conditions

Philip

pin

es

Hong

Kong

Assess sensitivity to Macro-economic Changes

Pro

bab

ility o

f D

efa

ult

Taiw

an

Mala

ys

ia Sin

gapo

re Kore

a

Thaila

nd In

donesi

a0.0

0.2

0.4

0.6

0.8

1.0

1.2

Probability of bank default

OPPORTUNITIES FOR RISK MANAGEMENT

23

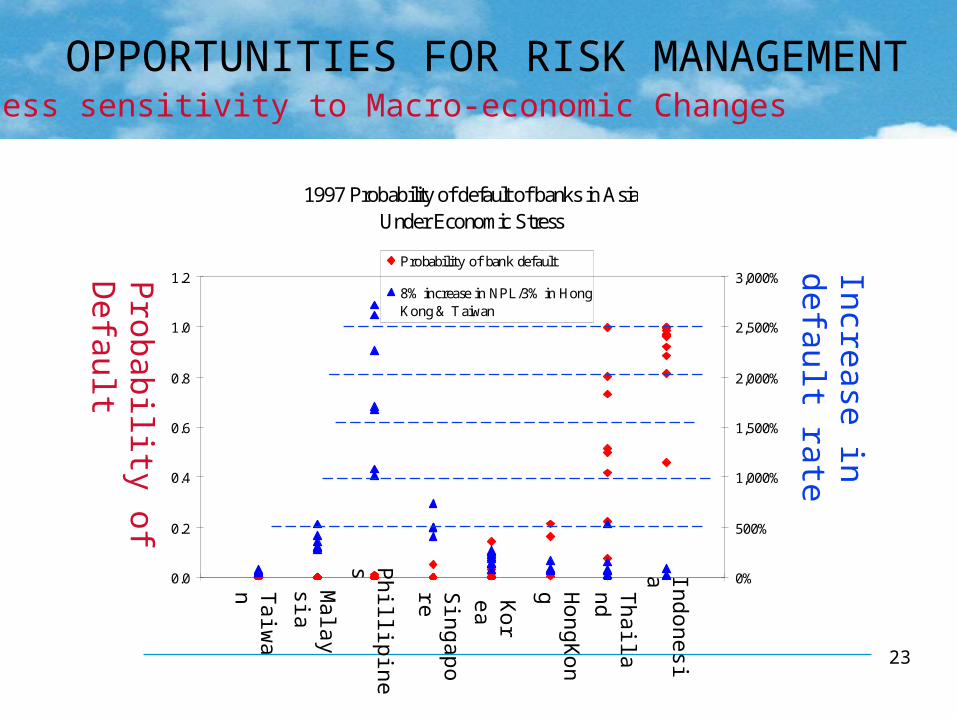

1997 Probability of default of banks in Asia Under Economic Stress

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0%

500%

1,000%

1,500%

2,000%

2,500%

3,000%Probability of bank default

8% increase in NPL/3% in HongKong & Taiwan

Taiw

an

Malaysi

a Phillipin

es Singapore

Kore

a HongK

ong

Thailand

Indonesia

Assess sensitivity to Macro-economic Changes

Probability of D

efault

Increase in default rate

OPPORTUNITIES FOR RISK MANAGEMENT

24

BUSINESS OPPORTUNITIES

1. Risk Communication tool to trade assets

2. Default Indices and sensitivity to economy

3. Contingent Pricing for Portfolios

4. Portfolio Insurance

25

INDUSTRY INITIATIVE FOR BENCHMARKING DEFAULT RISK

Internet Interface iqfinancial.comSector

Credit Factor InputFactor 1

Factor 2

Factor 3

Factor 4

Factor 5

Save Input?Open Input?

Yes/No

Yes/No

Future Environmentin country GDPin sector growthin FX rate

in interest rateScenario

NameSave Scenario?Open Scenario?Open Simulation?

Yes/No

Yes/No

Yes/No

Probability of Default

Rating Equivalent

Validation Results?Save Probability?

Yes/No

Yes/No

Validation Definition

Sector Definition

Factor Definition

Rating Equivalent Definition

Instructions Sector’s Default Profile