A Morning with an Irreplacable Element: CHROME Morning with an Irreplacable Element: CHROME . ......

108

A Morning with an Irreplacable Element: CHROME Johannesburg & Cape Town, November 2010

Transcript of A Morning with an Irreplacable Element: CHROME Morning with an Irreplacable Element: CHROME . ......

A Morning with an Irreplacable Element: CHROME

Johannesburg & Cape Town, November 2010

Presenter

Presentation Notes

United States of America? Rather USA – New York and Boston

2

F. P. Bath, 1968

Source: Bath, F.P.: “Chromium in South Africa”, Journal of the SAIMM, March 1968

South Africa – Sales Values

3

5,782

0

2,000

4,000

6,000

8,000

10,000

12,000

14,00019

80

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

in M

ill US

$

Cr Ore & FeCr SalesG.R.: 7.8%

GoldG.R.: -2.9%

2,84290 %

Source: DMR, Heinz H. Pariser

Agenda

4

1. The Effect of Chrome

2. South Africa – A Sleeping Cr Giant

3. Support for the Global Stainless Steel Industry

4. Nickel – the „Be-devilled“ Metal

5. Stainless Scrap – the Strongest Competitor

6. The Way Forward – Opportunities and Obstacles

7. Conclusions

5

The Effect of Chrome

Chromite – a Selective Historic Review

6

1797: Vauqeulin discovers a new element in „red lead“ – the mineral crocoite – and names it „chrôme“ 1821: First „Ferro Chrome“ obtained by direct reduction 1890: Research on „Chrome Steels“ starts 1909-15: Discovery of „Stainless Steel“ through the work of Haynes (USA – 1911), Brearley (UK - 1913), Maurer & Straus (Germany – 1914) 1920s: Various Cr-Alloy Steels and Stainless Steel in existence 1930s: NiCrFe „Super Alloys“ and NiCr / AlCr Electrical Resistance

1797 1821 1890 >1909 >1920

>1930

7

Value Added Structure of Chromium Alloys

Charge3.93

HC4.18

MC0.18

LC0.36

ULC0.05

4.0 – 7.5

7.5 – 8.5

0.5 – 4.0

0.05 – 0.5

< 0.05

< 0.02

0.03

1.01 – 1.36

0.65 – 1.16

0.85 – 1.40

2.00 – 2.17

2.33 – 2.50

3.78 – 5.13

Basis 2010 – Volumes in Mill. t Material Weight – Price Ranges 1st HY 2010

Cr Metal

Overview First Use for Chromite

8

Global Cr Ore & Concentrate Use 2009, in %

9

Metallurgical; 94.5

Foundry Sands; 2.5

Chemical; 2.0 Refractory; 1.0

Source: Heinz H. Pariser

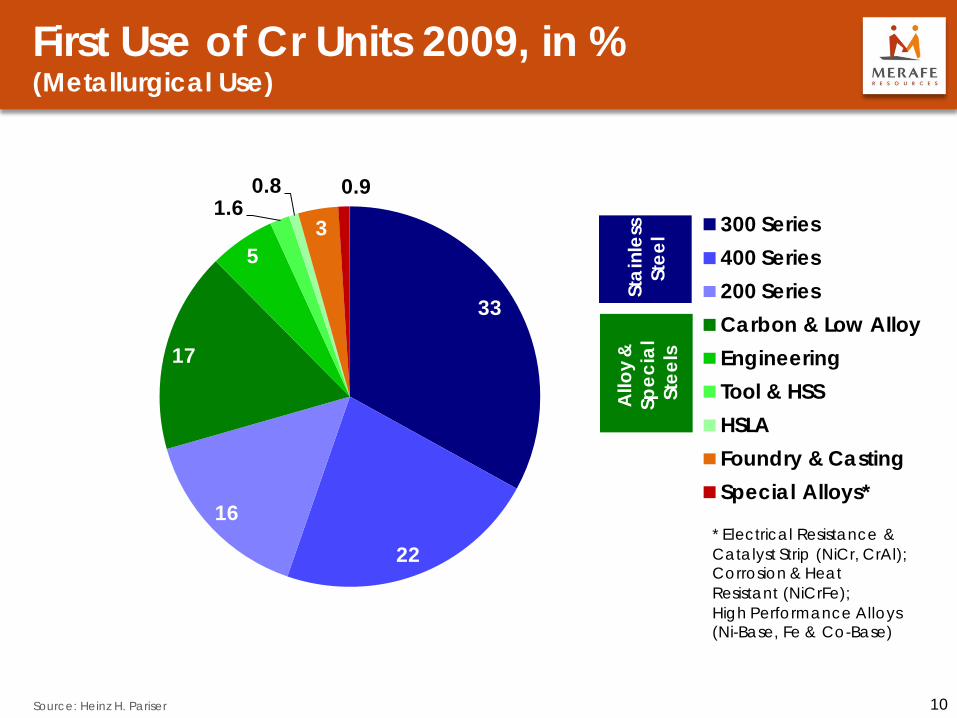

First Use of Cr Units 2009, in % (Metallurgical Use)

10 Source: Heinz H. Pariser

33

22

16

17

5

1.60.8

3

0.9

300 Series400 Series200 SeriesCarbon & Low AlloyEngineeringTool & HSSHSLAFoundry & CastingSpecial Alloys*

Stai

nles

sSt

eel

Allo

y &

Spec

ial

Stee

ls

* Electrical Resistance & Catalyst Strip (NiCr, CrAl); Corrosion & Heat Resistant (NiCrFe); High Performance Alloys (Ni-Base, Fe & Co-Base)

Cr End Use Markets 2009, in % (Metallurgical Use)

11 Source: Heinz H. Pariser

24

21

18

16

11

54

Engineering (Petro-chemical, Food Processing, etc.)Metal Goods (Cutlery, Tableware, etc.)

Building & Construction(Panels, Sinks, etc.)

Transport(Automotive, Aerospace, etc.)

Tubular Products

Electromechanical & Electronic Products(White goods,brown goods, etc.)Others

Overview First Use for Chromite

12 Source: Heinz H. Pariser

Sodiumdichromate Refractory Bricks & Mortars Molds for Casting

Metallurgical Chromite

(Lump, Chips, Fines & Concentrates) 20.0 Mill t

Chemical Chromite ( Concentrates)

0.3 Mill t

Refractory Chromite (Lump, Fines & Concentrates)

0.2 Mill t

Foundry Sand Chromite

( Concentrates)0.5 Mill t

Smelting Roasting Upgrade / Blend / Fire Upgrade

Ferro ChromeCharge/HC/MC/LC

8.3 Mill t / 4.3 Mill t Cr-units

Internal & External Stainless Scrap

10.2 Mill t,1.8 Mill t Cr-units

Stainless Steel (Cr input)Cr-units 2.9 Mill t Alloy Steel

Aust.Cr-units1.4 Mill t

Ferr.Cr-units0.9 Mill t

CrMnCr-units0.6 Mill t

Tool & High Speed Steel

Low Alloy Steel

Others

Nickel Alloys Foundries Welding Elec.

67.4% 5.5%27.1%

10

12

14

16

18

20

22

24

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in M

ill t

Growth Rate6.9%

Chrome Ore Production - Metallurgical Grade -

Metallurgical Chromite Production & Applications

13 Source: Heinz H. Pariser

Stainless Steel

Automotive exhaust system

„General Purpose“ Architecture,

food processing, deep drawing

Process industry, Desalination plants, Flue-gas Cleaning

Shafts, parts requiring high toughness

mandrel rods, forging and

pressing dies, pressure casting

plastic molds & forms

Alloy Steel

200

300

400

500

600

700

800

900

1,000

1,100

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in 0

00 t

Growth Rate-9.9%

Chemical Grade Production & Applications

14 Source: Heinz H. Pariser Source: Wikipedia

Chrome Ore Production - Chemical Grade -

Crocoite from Tasmania

Potassium Chromate

Potassium Dichromate

Tannery

Chrome Wheels

80

100

120

140

160

180

200

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in 0

00 t

Growth Rate2.0%

Refractory Chromite Production & Applications

15 Source: Heinz H. Pariser

Chrome Ore Production - Refractory Grade -

Source: Nelion Exports Source: Sterling Coomodities Ltd.

Refractory Bricks

Source: www.asia.ru

Foundry Grade Production & Applications

16 Source: Heinz H. Pariser

Source: www.metrom.com

Chrome Ore

Custom Mold Made of Foundry Sand

300

350

400

450

500

550

600

650

700

750

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in 0

00 t

Growth Rate7.3%

Chrome Ore Production - Foundry Grade -

17 Source: Heinz H. Pariser

Any Questions?

18

South Africa – A Sleeping Cr Giant

Chrome Ore Reserves & Resources 2009

19

Rankin Mill t in % in Mill t in %

South Africa 5,500 72 1 11.4 *) 50.0Zimbabwe 930 12 2 0.3 1.2

Kazakhstan 387 5 3 3.6 15.9

Finland 120 1.6 4 0.2 1.1

Turkey 70 0.9 5 1.6 7.3

India 67 0.9 6 2.4 10.6

Brazil 17 0.2 7 0.4 2.0

Others 576 7.5 8 2.7 12.0

Total 7,667 100.0 22.7 100.0*) incl. UG2 & Independent Mines

Source: Departm ent of Mineral Resources, South Africa, Heinz H. Pariser

Chromite Ore Reserves Chromite Ore Output

South Africa's Chrome Ore Market 2009

20 Source: Heinz H. Pariser

FeCr - Domestic & Export Sales

Revenues: 2,455 Mill $

Output 11.4 Mill tRevenues: 1,071 Mill $

ExportRevenues: 704 Mill $

MetallurgicalRevenues: 239 Mill $

internal sales

Chemical & FoundryRevenues: 128 Mill $

Chrome Ore Demand Structure 2009

21 Source: Heinz H. Pariser

China

Australia

Other Europe

AfricaAmerica

EU

Japan

Other Asia

-20

-15

-10

-5

0

5

10

15

20

25

30

0 20 40 60 80

Gro

wth

Rat

e 20

00 -

2009

in %

p.a

.

Share of Cr Ore Demand in %

Average Growth Rate: 6.8%

10

15

20

25

30

35

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in M

ill t

South African Platinum Industry – Mine Production

22 Source: Heinz H. Pariser

588_

2000 2007 2008 2009 G.R.in %

Merensky 25.1 36.7 36.7 35.0 4.5

UG 2 28.3 47.8 49.7 54.9 7.3

Total 53.3 84.5 86.4 90.0 6.1

UG 2 Ratio in % 53.0 56.6 57.5 61.1 1.1

in Mill t

Anglo American Platinum

47%

Impala Platinum

15%

Aquarius Platinum

23%

Lonmin Platinum

15%

2009

20

30

40

50

60

70

80

90

100

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in M

ill t

UG 2G.R.: 7.3%

Total Mine ProductionG.R.: 6.1%

Mine Production & Supply

23 Source: Heinz H. Pariser

2007 2008 2009

Mine ProductionDMR 9.6 9.6 6.6ICDA 8.7 9.3 6.2

HHP Supply 13.3 14.1 11.4Independent Mines & UG2 5.0 6.5 5.5

in Mill t

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in M

ill t

HHP SupplyG.R.: 5.8%

Mine Production DMRG.R.: 3.6%

Mine Production ICDAG.R.: 2.3%

Export Sales

24 Source: Heinz H. Pariser

2007 2008 2009

Official Exports 3,397 4,938 4,986

Exports Independent Mines 1,002 1,266 1,197

Exports of UG2 1,503 2,953 2,794

Export Sales Integrated Mines 893 720 995

in ´000 t

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in M

ill t

Export SalesIntegrated Mines

G.R.: 0.2%

ExportsIndependent Mines

G.R.: 24.0

Official ExportsG.R.: 19.2%

Exports of UG 2G.R.: 67.2

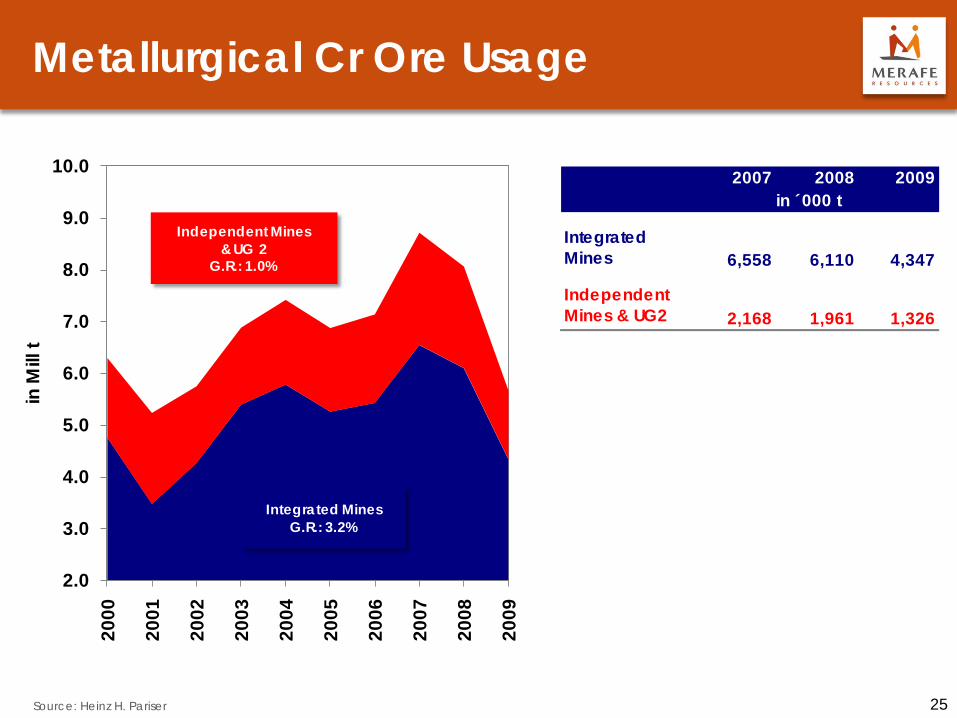

Metallurgical Cr Ore Usage

25 Source: Heinz H. Pariser

2007 2008 2009

Integrated Mines 6,558 6,110 4,347

Independent Mines & UG2 2,168 1,961 1,326

in ´000 t

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in M

ill t

Integrated MinesG.R.: 3.2%

Independent Mines& UG 2

G.R.: 1.0%

Chemical & Foundry Usage

26 Source: Heinz H. Pariser

2007 2008 2009

Integrated Mines 831 797 496

Independent Mines & UG2 327 317 213

in ´000 t

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in M

ill t

Integrated MinesG.R.: -5.4%

Independent Mines & UG 2G.R.: 7.2%

The Potential of UG2

27 Source: Heinz H. Pariser

-100

-80

-60

-40

-20

0

20

40

60

0.0 20.0 40.0 60.0 80.0 100.0

Rela

tive

Cha

nge

in O

re In

put C

ost,

in %

UG2 Transfer Price, in US$ per t

0% 10% 30%50% 70%

UG2 Share in Ore Mix

UG2 Transfer Price Range

UG2 in SAF Technology:

• Reduction of ore input costs

UG2 in DC Technology:

• Direct use, • Increased reduction of ore input cost • Lower reductant cost

Calculation based on: SAF Technology , 70% Pellets, 30% Lumpy, ZAR/US$ = 8.4

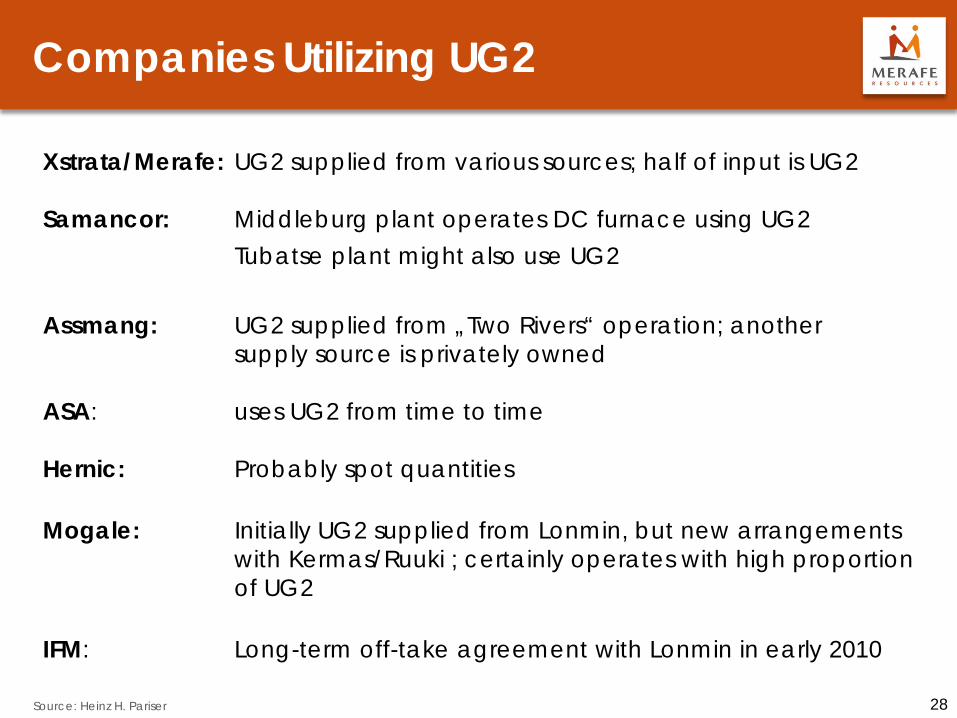

Companies Utilizing UG2

28 Source: Heinz H. Pariser

Xstrata/Merafe: UG2 supplied from various sources; half of input is UG2 Samancor: Middleburg plant operates DC furnace using UG2 Tubatse plant might also use UG2 Assmang: UG2 supplied from „Two Rivers“ operation; another supply source is privately owned ASA: uses UG2 from time to time Hernic: Probably spot quantities Mogale: Initially UG2 supplied from Lonmin, but new arrangements with Kermas/Ruuki ; certainly operates with high proportion of UG2 IFM: Long-term off-take agreement with Lonmin in early 2010

Metallurgical Chrome Ore & Concentrate

29 Source: Heinz H. Pariser

KazakhstanSudan

MadagascarTurkey

ZimbabweSouth Africa

IndiaIndonesia

OmanBrazilUG2

AlbaniaFinland

IranRussia

20 30 40 50 60 70

Cr2O3 Content in wt.-%

Cr2O3 Content

SudanKazakhstanZimbabwe

IndiaRussiaTurkey

AlbaniaIran

OmanBrazil

MadagascarFinland

South AfricaIndonesia

UG2

1.00 2.00 3.00 4.00 5.00Cr : Fe Ratio in wt.-%

Cr : Fe Ratio

Ferrochrome Production Technologies (I)

30

Pre-heating

Source: IFML Company Information

Beneficiation

SAF

FeCr Ingots

Fines

SAF (Outokumpu & Conventional Process)

Lumpy Ore

Pelletising

Sintering

Offgas

Offgas

Reductants Fluxes

Power

Slag

Fines

Beneficiation

DC Furnace Offgas Power

FeCr Ingots

Slag

Reductants Fluxes

DC Furnace

Ferrochrome Production Technologies (II)

31 Source: Heinz H. Pariser

Milling

Drying

Raw Materials: Cr2O3, Reductants, Binder Clay

Rotary Kiln (Pre-Reduction)

Electric Furnace

Reductants, Fluxes

Slag

FeCr Ingots

Power

Pelletizing

H2O

Roasting

Hot sintered pellets

Hot sintered pellets

Coal, Off Gas

FeCr Granules

Xstrata / Merafe – Premus Process

Generic*) Charge / HC FeCr – Capacity Changes

32 Source: Heinz H. Pariser

2007 2008 2009 2010 e 2011 f 2012 f 2013 f

Europe 1,021 1,068 1,071 1,122 1,197 1,287 1,502

South Africa 4,354 3,740 3,890 4,095 4,195 4,275 4,734Zimbabwe 250 250 250 250 250 250 250

Brazil 190 200 200 200 200 200 200

China 1,300 1,500 1,500 1,520 1,620 1,720 1,820

India 1,040 1,066 1,041 1,156 1,406 1,476 1,576I ran 20 50 50 50 50 50 50

Kazakhstan 1,150 1,150 1,170 1,170 1,300 1,500 1,600

Total Capacity 9,325 9,024 9,172 9,563 10,218 10,758 11,732

Demand 7,591 6,639 7,117 8,210 8,835 9,360 10,012Utilisation (%) 82.9 82.7 67.2 85.4 82.9 82.1 79.9*) incl. Feed Material for LC & MC FeCr

*) incl. Saleble & internal Feed

in ´000 t

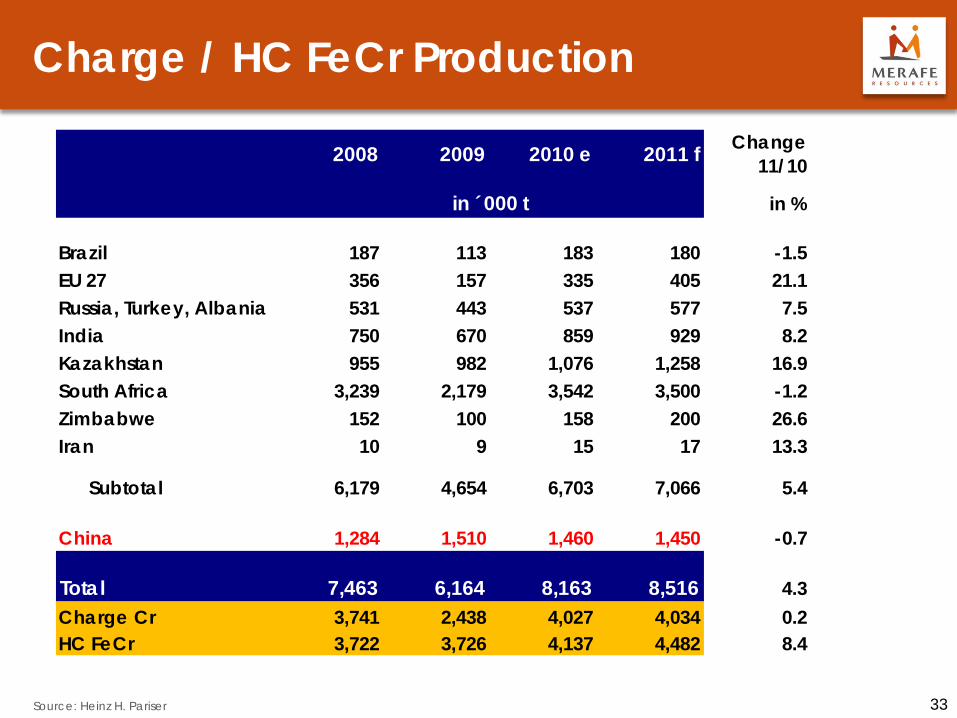

Charge / HC FeCr Production

33 Source: Heinz H. Pariser

2008 2009 2010 e 2011 f Change11/10

in %

Brazil 187 113 183 180 -1.5EU 27 356 157 335 405 21.1Russia, Turkey, Albania 531 443 537 577 7.5India 750 670 859 929 8.2Kazakhstan 955 982 1,076 1,258 16.9South Africa 3,239 2,179 3,542 3,500 -1.2Zimbabwe 152 100 158 200 26.6Iran 10 9 15 17 13.3

Subtotal 6,179 4,654 6,703 7,066 5.4

China 1,284 1,510 1,460 1,450 -0.7

Total 7,463 6,164 8,163 8,516 4.3Charge Cr 3,741 2,438 4,027 4,034 0.2HC FeCr 3,722 3,726 4,137 4,482 8.4

in ´000 t

Producers of Charge / HC FeCr

34 Source: Heinz H. Pariser

5141

2528

24 31

2008 2009

Production Breakdown Type

Charge Cr

Low Grade HC FeCr

High Grade HC FeCr

Total Output(Cr Units)4,237 kt

Total Output(Cr Units)3,406 kt

2008 2009

ENRC 696 740Chelyabinsk 85 64Mechel 45 57Eti Krom 44 24Vargön 13 5India 466 417China 305 334Zimbabwe 98 65Albania 18 4Iran 11 6Xstrata / Merafe 665 488Samancor 416 312Hernic 168 109Outokumpu 124 65IFML 109 61Assmang 103 50Ferbasa 101 59ASA Metals 61 25Tata & Others 66 45Vargön 54 17

High

Gra

deLo

w G

rade

Cha

rge

Cr

in ´000 t Cr Units

High Carbon overtaking Charge Chrome (Production)

35 Source: Heinz H. Pariser

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 e 2011 f

in ´0

00 t

Mat

eria

l Wei

ght Charge Cr

G.R.: 2.7%

HC FeCrG.R.: 10.3%

Regional Production Breakdown 2009

36 Source: Heinz H. Pariser

-40

-30

-20

-10

0

10

20

30

40

0 10 20 30 40 50 60 70 80 90

Gro

wth

Rat

e 20

00 -

2009

, in

%

Share of Production, in %

Brazil

Others

China

India

Russia

Finland

South Africa

Average Growth Rate: 5.9% p.a.Kazakhstan

Zimbabwe

Turkey

Sweden

Others incl. Slovakia, Albania & Iran

Charge Cr

HC FeCr

Charge / HC FeCr Production – Integrated vs. Converters

37 Source: Heinz H. Pariser

0.0

5.0

10.0

15.0

20.0

25.0

30.0

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

% share of C

hinese Converters

in ´0

00 t

587_063_D3

Integrated ProducersG.R.: 3.7%

ChinaG.R.: 24.2%

Other ConvertersG.R.: -5.0%

Converters with own Cr Ore BaseG.R.: 11.2%

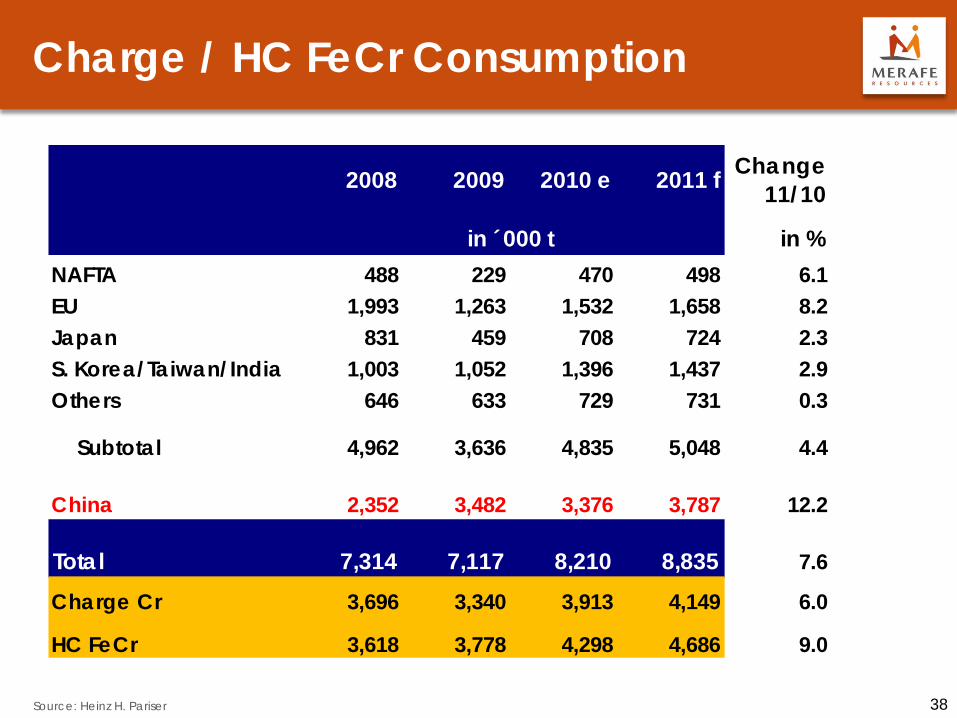

Charge / HC FeCr Consumption

38 Source: Heinz H. Pariser

2008 2009 2010 e 2011 f Change11/10

in %NAFTA 488 229 470 498 6.1EU 1,993 1,263 1,532 1,658 8.2Japan 831 459 708 724 2.3S. Korea/Taiwan/India 1,003 1,052 1,396 1,437 2.9Others 646 633 729 731 0.3

Subtotal 4,962 3,636 4,835 5,048 4.4

China 2,352 3,482 3,376 3,787 12.2

Total 7,314 7,117 8,210 8,835 7.6

Charge Cr 3,696 3,340 3,913 4,149 6.0

HC FeCr 3,618 3,778 4,298 4,686 9.0

in ´000 t

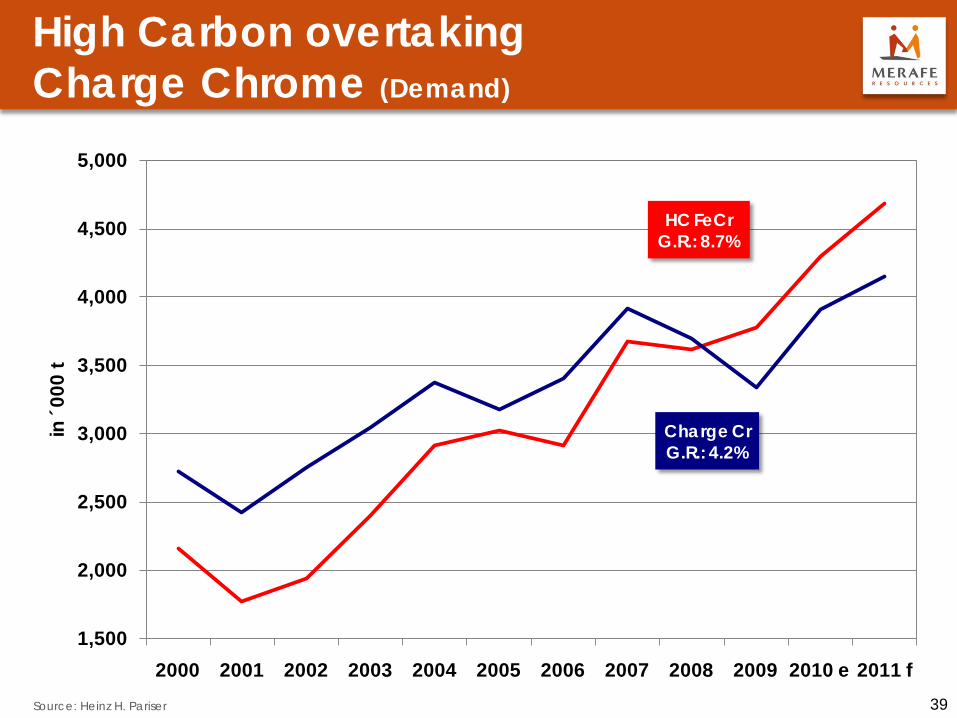

High Carbon overtaking Charge Chrome (Demand)

39 Source: Heinz H. Pariser

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 e 2011 f

in ´0

00 t

HC FeCrG.R.: 8.7%

Charge CrG.R.: 4.2%

Regional Demand Breakdown

40 Source: Heinz H. Pariser

China

South Africa Other

America

NAFTA EU

Taiwan

Japan

South Korea

-10

-5

0

5

10

15

20

25

30

35

40

45

0 20 40 60 80

Gro

wth

Rat

e 20

00 -

2009

in %

p.a

.

Share of FeCr Demand in %

Charge Cr Demand Structure2009

Av. Growth Rate: 4.2%

China

Others

South Korea

NAFTA

Japan

EUIndia

-10

0

10

20

30

40

50

60

0 20 40 60 80

Gro

wth

Rat

e 20

00 -

2009

in %

p.a

.

Share of FeCr Demand in %

HC FeCr Demand Structure 2009

Average Growth Rate: 8.9%

Characteristics of Charge / HC FeCr

41 Source: Heinz H. Pariser

High Carbon FeCr Charge Cr Wide range of usage in alloy steels, the foundry industry as well as for other materials – but also in stainless steel

Almost exclusively for stainless steel melting Application

Benefits

High Cr Content (typically 58%-70%); advantages when limited Cr input is required, where specific constraints exist for certain special steels – in particular with regards to trace elements such as Ti, V, P, Si, etc.

Low Cr Content (48%-58%), high (free) iron content, typically high Si content (2%-6%); competitive bulk product for mass production

Marketing Mainly direct sales to main stainless producers

Often sold indirectly via traders / distributors to numerous users

Logistics Large monthly shipments to end user warehouses

Supplies from local mostly in truck loads; consignment stocks

Contracts Annual contracts Annual contracts and spot sales

Price Leadership

South Africa Global Market

South Africa and Kazakhstan; often isolated local markets

Cr:C ratio 6.5:1

Cr:Si ratio 12:1

Cr:C ratio 9:1

Cr:Si ratio >100:1

Charge / HC FeCr Supply & Demand Balance

42 Source: Heinz H. Pariser

2006 2007 2008 2009 2010 2011

´000 t

Demand* 6,316 7,591 6,639 7,117 8,210 8,835

Supply - Cr Production 6,555 7,727 7,463 6,164 8,163 8,516 - Capacity 7,807 9,325 9,024 9,172 9,563 10,278 - Ut ilisat ion (in %) 84.0 82.9 82.7 67.2 85.4 82.9

Supply & Demand Balance 238 136 824 -954 -47 -319

Charge Cr Prices in $ / lb 0.70 0.91 1.76 0.85 1.24 1.76

*) excl. Consum er stocking 675 kt in 2008

Charge / HC FeCr Supply & Demand

43 Source: Heinz H. Pariser

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

in ´0

00 t

2007 2008 2009 2010 e

Demand

Actual Forecast

Supply

2006 2011 f

Power Supply

44 Source: Heinz H. Pariser

1. According to Escom, sufficient electricity will be available from 2013 onwards.

2. Industry sources believe that electricity demand will shortly thereafter exceed capacity again

3. Other power stations in Botswana are providing additional electricity.

With exception of the recently announced LION II expansion, no other FeCr capacity expansions in South Africa will take place in large scale within the next 3 years. The LION II expansion as well as lifted capacity restrictions after 2013 are expected to add 360 ktpy new and some 600 ktpy idled FeCr capacity.

Charge Cr Long-term Price Development

45 Source: Heinz H. Pariser

0.00

0.50

1.00

1.50

2.00

2.50

3.00

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

in U

S$ /

lb

Deflated Prices 2009 US$

Nominal Prices

Realistic Price Forecast

(in 2009 US$)

Phase : IG.R. : -3.8%

II-1.4%

III-1.0%

IV+8.0%

V-3.2%

FeCr Production Cost

46 Source: Heinz H. Pariser

Any Questions?

47

Support for the Global Stainless Steel Industry

Chrome makes Stainless Stainless

48 Source: Steel Manual / Heinz H. Pariser

Stainless Steels

are alloyed steel grades with a carbon mass fraction of 1.2% or less, and 10.5% Cr or more, with or without other elements.

Environment

Stainless Steel

O O

O

O OO O

OO

O

Cr

Cr CrCr

Cr

Cr

Stainless Steels – More than 200 Different Grades (but all with Cr)

49 Source: Heinz H. Pariser

Ferritic X 5 CrTi 12 4 („409“- 12% Cr)

% Cr

10.5%-

30.0%

Ø Cr: 17.0%

Typical Grades Applications

Automotive exhaust system

MartensiticX 20 Cr 13 („420“- 13% Cr)

Cutlery, needlevalves, nozzles

Austenitic / CrMnX 5 CrNi 18 9 („304“- 18% Cr) „General Purpose“

Architecture, food processing, deep drawing

X 12 CrMnNiN 18 9 5 („202“- 18% Cr)

DuplexX 2 CrNiMoN 22 5 3 („2205“- 22% Cr) Process industry,

Desalination plants,Flue-gas Cleaning

Typical Stainless Grades

50 Source: Heinz H. Pariser

Austenitic CrMn Ferritic Duplex

"Superaustenitics" "Superferritics" "Superduplex"

Chemical Composition

301 17Cr; 7Ni

304 18.5Cr; 8Ni

31618Cr; 11Ni;

2Mo

904 L23Cr; 25Ni;

4.3Mo

201 17Cr; 3.5Ni;

6Mn

20218Cr; 4Ni;

8Mn

India/China200 series

~16Cr; 9Mn;<2Ni

43017Cr

40911.5Cr; 0.25Ti

44418.5Cr; 1.5Mo

0.45Ti

"LDX 2101"21.5Cr; 1.5Ni;5Mn; 0.3Mo

220522Cr; 5.7Ni;

3.1Mo

250725Cr; 7Ni

4Mo

Stainless Steel in the Global Steel Environment

51 Source: Heinz H. Pariser

Stainless Steel Production

2.4%

Crude Steel Production

97.6%

Steel Production 2009

1,925 1,618 2,333 2,382

7,8285,974

7,411 7,663

7,344 9,751

11,258 12,010

3,564 2,607

3,3403,3504,458 4,811

5,6165,897

1,298 1,210

1,2621,349

Stainless Steel Production

OthersAsiaJapanChinaEU 27USA

26,418 25,971

31,220

2008 2010e2009 2011f

32,652

Global Stainless Steel End Use - 2009

52 Source: Heinz H. Pariser

5.8%

6.8%

11.6%

12.9%

17.2%

22.1%

23.6%

Non-Allocated

Electromechanical & Electronic Products

Transport(incl. Automotive)

Tubular Products

Building & Construction

Metal Goods

Engineering

Stainless Steel Melting

53 Source: Heinz H. Pariser

2008 2009 2010 e 2011 f Change 11/10

in %

USA 1,925 1,618 2,333 2,382 2.1Brazil 557 482 507 528 4.2European Union 7,828 5,974 7,411 7,663 3.4Other Europe 213 140 197 210 6.5Japan 3,564 2,607 3,340 3,350 0.3S. Korea/Taiwan 2,914 3,121 3,605 3,717 3.1S. Africa 529 588 558 611 9.5

Subtotal 17,530 14,530 17,951 18,462 2.8

China 7,344 9,751 11,258 12,010 6.7India 1,544 1,690 2,011 2,180 8.4

Subtotal 8,888 11,441 13,269 14,190 6.9

Total 26,418 25,971 31,220 32,652 4.6

in ´000 t

Global Stainless Melting – Since 1950

54 Source: Heinz H. Pariser

0.0

10.0

20.0

30.0

40.0

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

in M

ill t

Post-War Reconstruction Crisis Years StSt Boom I:Japan, Taiwan,S. Korea

East

ern

Euro

pe

Tran

sitio

n StSt Boom II:Europe, USA

ChinaMarketEntrance

AOD / VODRefining

ContinuosCasting

Phase : IG.R. : +8.1%

II+2.9%

III+7.8%

IV-0.7%

V+7.0%

VI+0.9%

VII+5.3%

Stainless Steel Melting ProductionG.R. 50 - 10: 5.7%

Charge / HC FeCr Consumption

G.R. 70 - 10: 4.0%

Typical Material Charge for 304 Stainless

55 Source: Heinz H. Pariser

Stainless scrap

Carbon steel scrap

(C-scrap) Nickel Other alloys

Ferrochrome Charge Cr HC FeCr LC FeCr

Electric arc furnace melting 165kg

Trimming & refining AOD / VOD(1)

180kg

80kg

4kg

70kg 15kg 10kg

1kg

Continuous casting 180kg

Slabs / billets 180kg

Cr input in kg Cr units

(yield losses ignored)

53% Primary Cr Units 47% Stainless Scrap

Stainless Steel – Made of Scrap?

56 Source: Outokumpu Oy Annual report, Heinz H. Pariser

Stainless Melting

Outokumpu´s

Raw Material Mix between 2005 - 2009

Primary Metals 22.8 - 31.5%

Internal Scrap 20.1 – 20.6%

External Scrap 47.9 – 57.1%

Total Scrap Input 68.0 – 77.7%

Primary Metals

External Scrap

Internal Scrap

South Africa‘s FeCr Position in Main Stainless Countries

57 Source: Heinz H. Pariser

0

22

33

41

69

0

43

60

55

139

China

USA

Japan

Asia

EU27

50.3%

49.4%

56.1%

74.3%

2000 2010

Total

South Africa

FeCr Imports in ´000 t per Month

South Africa Average 55.5% South Africa Average 56.9%

25

30

61

74

96

44

61

81

148

172

48.8%

56.0%

75.6%

49.9%

57.1%

Charge / HC FeCr Imports

58 Source: Heinz H. Pariser

0

10

20

30

40

50

60

70

80

90

100

0

100

200

300

400

500

600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Share in %in

´000

t pe

r Mon

th

Total Charge / HC FeCr Importsby Stainless Producing Countries

G.R.: 5.3%

Supplies from South AfricaG.R.: 4.6%

Stainless Steel Substitution Process – Substitution Trigger

59 Source: Heinz H. Pariser

50.0

55.0

60.0

65.0

70.0

75.0

80.0

5

10

15

20

25

30

35

40

45

50

Austenitic Ratio in %

LME

Ni P

rice

in ´0

00 U

S$/t

Ni Price

SS Austenitic Ratio

2000 2001 2002 2003 2004 2005 2006 2007

23.7Ferritics

CrMn

22.7 22.0 22.9 23.0 24.6 23.5 25.6

3.8 5.3 5.3 6.9 10.2 11.5 11.1 14.3

Ratios of:

2008

24.8

14.7

2009

15.9

26.4

15.8

28.0

2010 2011

28.2

16.0

Substitution Potential: Chrome vs. Nickel

60 Source: Heinz H. Pariser

End Use of Chrome Units

Substitution Potential End Use of Nickel Units

Substitution Potential

in % in %

Stainless Steel 65 59300 29 Not Replaceable 56 Yes, Int ernal Subst it ut ion400 24 0 bet ween St ainless Grades200 12 3

Alloy Steels 30 Limit ed Subst it ut ion 7 Limit ed Subst it ut ion

Ni-Base Alloys 1 Not Replaceable 12 Wide Range of Subst it ut es incl. Cu-Alloys,Ceramics, High Grade St ainless St eel

Cu-Base Alloys 0 1 Not Relevant

Plating 0 11 High Subst it ut ion Risk! Decorat ive Usage

Foundry 3 Limit ed Subst it ut ion 3 St ainless Scrap

Others 1 6

Total 100 100

Summary Substitution in Stainless

61 Source: Heinz H. Pariser

• Chrome is irreplacable: No Chrome – No Stainless!

• High nickel prices trigger substitution,

• But with China‘s growing stainless market – the global product mix has changed as well!

• Growing expansion of either ferritics or duplex will push ferrochrome demand, aided by low scrap input.

• E.g.: a 10% increase in ferritics (from 28% to 31% production share) would result in a 75 kt FeCr demand increase

Stainless Price Competitiveness

62

0

50

100

150

200

250

1967 1972 1977 1982 1987 1992 1997 2002 2007

in In

dex

Poin

ts

304 (18% Cr, 8% Ni)

430 (18% Cr)

*) Base Germany

Index 1967 =100 Source: Heinz H. Pariser200991.6

173.4161.9184.6233.0

430 SS CRNon FerrousPlasticAluminiumIron & Steel

2008137.7 197.5178.9200.3313.5

2010 (1-8) 118.6214.7166.8191.0251.6

Intrinsic Element Value in Stainless Prices

63 Source: Heinz H. Pariser

22.6

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Intri

nsic

Val

ue, i

n %

Grade 430 (18% Cr)

Chrome

Basis: Effective German Trader PriceCold Rolled Sheet, 2mm

DB/StSt Prices 304_316

75.9

19.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Intri

nsic

Val

ue, i

n %

Grade 304 (18% Cr, 8% Ni)

Nickel

Chrome

Basis: Effective German Trader Price Cold Rolled Sheet, 2mm

DB/StSt Prices 304_316

64 Source: Heinz H. Pariser

Any Questions?

65

Nickel – the “Be-devilled” Metal

Long-Term Historic Nickel Price Development

66 Source: Heinz H. Pariser

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

1950 1960 1970 1980 1990 2000 2010 2020

in U

S$ /

t

Nickel Price Crises I

LME NickelContract

Nickel Price Crises III

Nic

kel P

rice

Cris

es II

Nickel PriceNominal

Nickel PriceDeflated

23,200 US$/t

15,500 US$/t

19,400 US$/t

Chrome vs Nickel – A First Use Comparison (Basis: 2009 First Use Data)

67 Source: Heinz H. Pariser

4.5% p.a.

-0.6 % p.a.

4.0% p.a.

4.2% p.a.

1.7% p.a.

2.7% p.a.

Chr

ome

Nic

kel

in Stainless Steel in Other Applications in Alloy Steel

033.7 70.5 4.4 60.1 25.1

6.2

Stainless Driving Nickel Demand

68 Source: Heinz H. Pariser

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

in 0

00 t

First Use of Nickel

Stainless SteelG.R.: 4.9 %

Non-Stainless ApplicationG.R.: 2.2 %

Stainless Steel59%

Alloy Steel8%

Ni Base10%

Cu Base1%

Plating11%

Foundry4%

Batteries & Others

7%

2009 p

Primary Nickel Consumption – 2006 to 2011

69 Source: Heinz H. Pariser

847 755 722 651 746 744

3748 43

4860 62

517520 521 543

622 718

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2006 2007 2008 2009 2010 2011

in ´0

00 t

All Other Applications

CrNi SS(8.5%)

Low Ni CrMn(1.5%)

1,4011,323 1,287

1,242

1,428

Actual Forecast

+6.8

%

+ 15

.0%

1,525

Regional Nickel Consumption Breakdown 2009

70 Source: Heinz H. Pariser

China / Hong Kong

Australasia

Other Euorpe AfricaAmerica EU 27 JapanAsia

-5

0

5

10

15

20

25

30

0 20 40 60 80

Gro

wth

Rat

e 20

00 -

2009

in %

p.a

.

Share of Ni Consumption in %

Average Growth Rate: 1.8%

1,000

1,100

1,200

1,300

1,400

1,500

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

in ´0

00 t

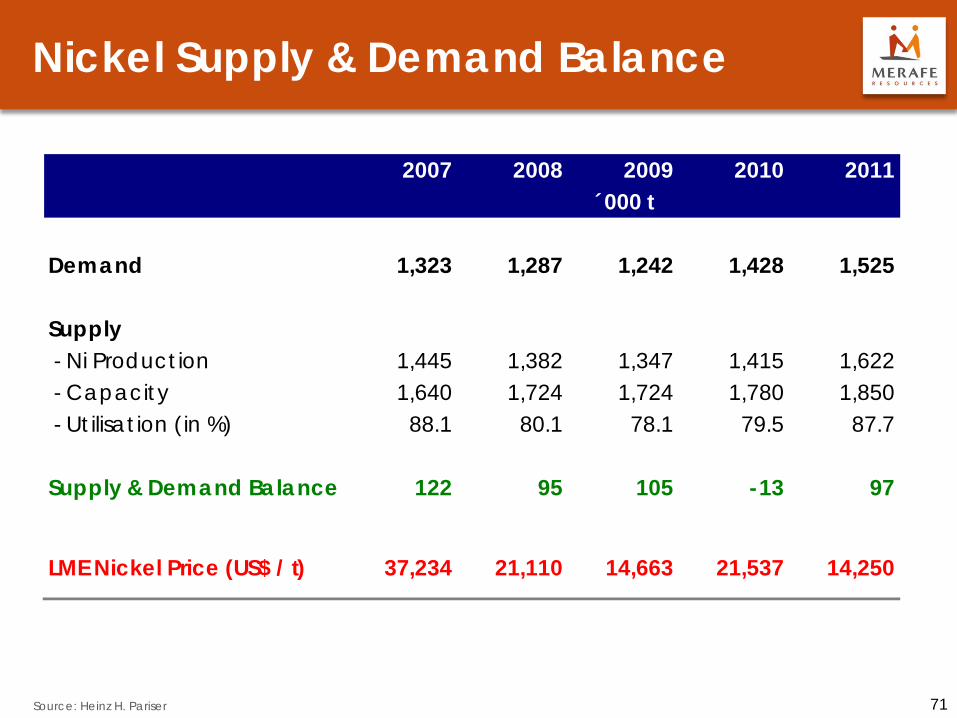

Nickel Supply & Demand Balance

71 Source: Heinz H. Pariser

2007 2008 2009 2010 2011

Demand 1,323 1,287 1,242 1,428 1,525

Supply - Ni Production 1,445 1,382 1,347 1,415 1,622 - Capacity 1,640 1,724 1,724 1,780 1,850 - Ut ilisat ion (in %) 88.1 80.1 78.1 79.5 87.7

Supply & Demand Balance 122 95 105 -13 97

LME Nickel Price (US$ / t) 37,234 21,110 14,663 21,537

´000 t

14,250

72 Source: Heinz H. Pariser

Any Questions?

73

Stainless Scrap – The Strongest Competitor

Stainless Scrap Cycles

74 Source: Heinz H. Pariser

T I M E

Internal Scrap External ScrapBlend

Material

Influencing Factors

Recycling Time

Recycling Ratio

Stainless Production Stainless Consumption Historical Stainless and AlloyConsumption, Nickel Price

3 days – 3 months Approx. 6 months 15 – 20 years

Approx .100 % Approx. 100% 60 – 80%

Stainless Scrap Availability

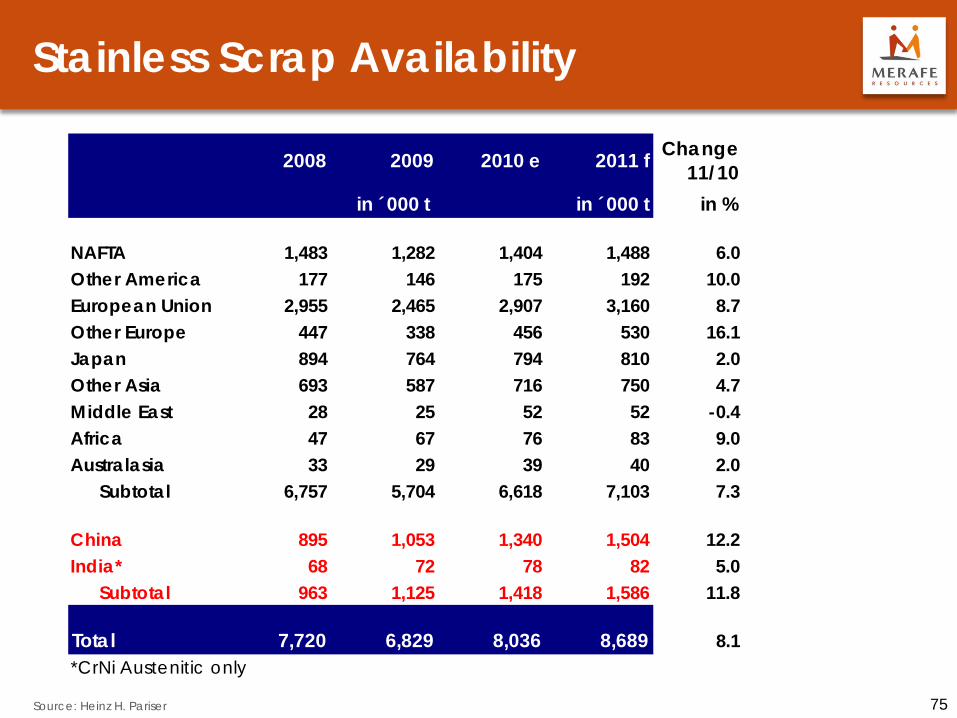

75 Source: Heinz H. Pariser

2008 2009 2010 e 2011 f Change11/10

in ´000 t in %

NAFTA 1,483 1,282 1,404 1,488 6.0Other America 177 146 175 192 10.0European Union 2,955 2,465 2,907 3,160 8.7Other Europe 447 338 456 530 16.1Japan 894 764 794 810 2.0Other Asia 693 587 716 750 4.7Middle East 28 25 52 52 -0.4Africa 47 67 76 83 9.0Australasia 33 29 39 40 2.0

Subtotal 6,757 5,704 6,618 7,103 7.3

China 895 1,053 1,340 1,504 12.2India* 68 72 78 82 5.0

Subtotal 963 1,125 1,418 1,586 11.8

Total 7,720 6,829 8,036 8,689 8.1*CrNi Austenitic only

in ´000 t

Scrap Availability – Dependency on Nickel

76 Source: Heinz H. Pariser

0.00

5.00

10.00

15.00

20.00

25.00

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2006 2007 2008 2009 2010e 2011f

LME C

ash Nickel Price, US$/lb

Scra

p A

vaila

bilit

y, '0

00 t

Scrap AvailabilitySource: Heinz H. Pariser

LME Cash Nickel Price

Long-term Global Scrap Reserve

77 Source: Heinz H. Pariser

0.0

100.0

200.0

300.0

400.0

500.0

600.0

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

in M

ill t

1980 2000 2009 2010 2020in Mill t

Cum. Aust. Consumption 66.1 208.1 322.2 338.2 560.4Cum. Scrap Consumption 20.2 92.0 159.1 169.1 303.3Scrap Reserve 45.9 116.1 163.1 169.1 257.2

Cum. Scrap Consumption

Cum. Aust. Consumption

Scrap Reserve

Product Mix Defining Scrap Input

78 Source: Heinz H. Pariser

External Stainless Scrap Consumption(Ratio in %)

MIN MAXGlobal Average

42.2300 Series China27.6

USA74.4

10.1200 SeriesChina

8.5USA, EU, Japan25.0

4.5400 SeriesChina

5.0India10.0

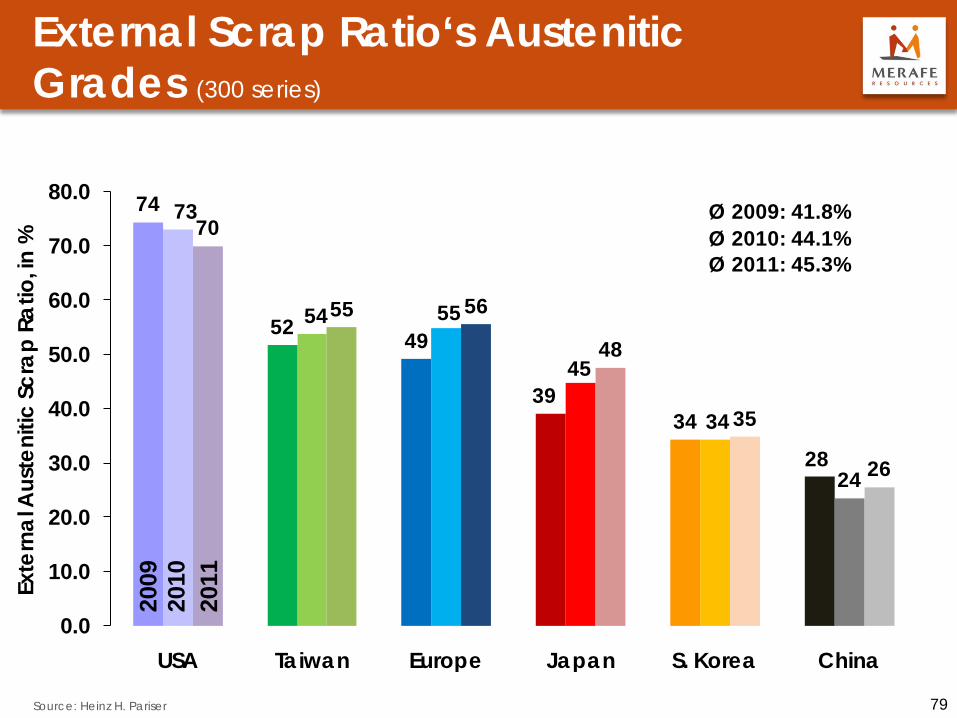

External Scrap Ratio‘s Austenitic Grades (300 series)

79 Source: Heinz H. Pariser

74

52 49

3934

28

73

54 55

45

34

24

70

55 56

48

35

26

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

USA Taiwan Europe Japan S. Korea China

Exte

rnal

Aus

teni

tic S

crap

Rat

io, in

%

2009

2010

Ø 2009: 41.8%Ø 2010: 44.1%Ø 2011: 45.3%

2011

Contribution to Primary Raw Materials

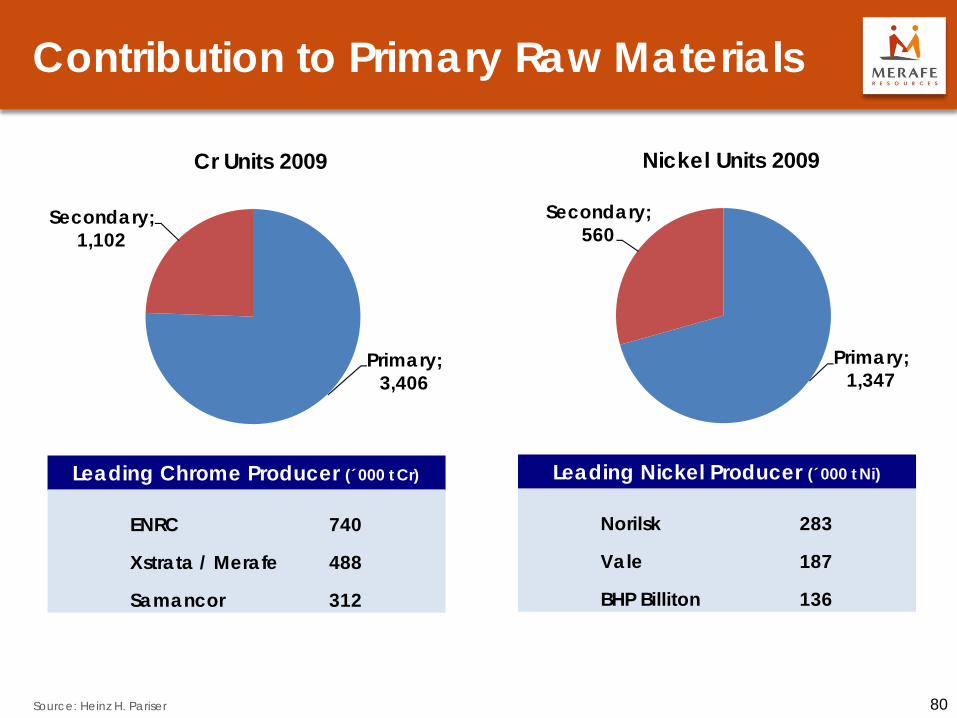

80 Source: Heinz H. Pariser

ENRC 740

Xstrata / Merafe 488

Samancor 312

Leading Chrome Producer (´000 t Cr)

Primary; 3,406

Secondary; 1,102

Cr Units 2009

Norilsk 283

Vale 187

BHP Billiton 136

Leading Nickel Producer (´000 t Ni)

Primary; 1,347

Secondary; 560

Nickel Units 2009

Ni Units in External Stainless Scrap

81 Source: Heinz H. Pariser

2006 2007 2008 2009 2010e 2011fNi Units in ´000 t 707 652 633 560 659 712

350

400

450

500

550

600

650

700

750in

000

t N

i Con

tent

+ 14.5%

- 7.9%- 2.9%

- 11.5%

+ 17.7%

+ 8.1%

Cr Units in External Stainless Scrap

82 Source: Heinz H. Pariser

2006 2007 2008 2009 2010e 2011fCr Units in ´000 t 1,368 1,321 1,234 1,102 1,339 1,457

800

900

1,000

1,100

1,200

1,300

1,400

1,500in

000

t C

r Con

tent

+ 13.9%- 3.5%

- 6.6%

- 10.6%

+ 21.4%

+ 8.9%

Cr Units in External Stainless Scrap

83 Source: Heinz H. Pariser

0

1,000

2,000

3,000

4,000

5,000

6,000

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

e

in 0

00 t

Cr C

onte

nt

Cr Requirement inStainless Steel - Total

Cr Requirements inStainless Steel

Cr Units from Cr in Scrap

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

e

in 0

00 t

Cr C

onte

nt

Cr Requirement inStainless Steel - China

Cr Requirements inStainless Steel

Cr Units from Cr in Scrap

Element Valuation in Stainless Scrap

84 Source: Heinz H. Pariser

40

50

60

70

80

90

100

110

2006 2007 2008 2009 2010

Valu

atio

n re

lativ

e to

Ref

eren

cepr

ice,

in % Referenceprice

Nickel

ChromeMolybdenum

Scrap offers discounts… … but Ni is the main

determinant (e.g. grade 304 type scrap)

74.0%

9.0%

18.0%

19.4%

8.0%

71.7%

quantity in kg

valuein US$

NiCrFe

Staus: September 2010

Chrome Valuation in Scrap vs. SA Producer Price

85 Source: Heinz H. Pariser

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

0.00

0.50

1.00

1.50

2.00

2.50

Cr in Scrap Discount, in %

Pric

es in

US$

/ lb

Charge Chrome South African

Producer PriceChromein Scrap

2000 2010200920082007200620052004200320022001

86 Source: Heinz H. Pariser

Any Questions?

87

The Way Forward – Opportunities & Obstacles

China‘s Position in Stainless & Related Raw Materials 2000 vs 2009

88 Source: Heinz H. Pariser

2.9 4.71.3

6.0 5.17.6 5.5

8.03.7 2.2

37.5

20.0

1.2

24.5

15.4

42.437.9

33.5

48.9

22.3

Stainless Steel

Nickel Chrome Ore

Chrome Stainless Scrap

Stainless Steel

Nickel Chrome Ore

Chrome Stainless Scrap

Share in %

2000 2009

Production Consumption

DB

Stainless Steel Intensity in the Year 2000 Cold Rolled Flat Products

89 Source: Heinz H. Pariser

NAFTA

EU 27

Turkey

Other Europe

Japan

China

Taiwan

India

South Korea

Other Asia Middle East

Africa Australasia

South America

-5

0

5

10

15

20

25

0 1 10 100 1,000

Con

sum

ptio

n pe

r Cap

ita in

kg

PPP per Capita in 000 US$ (Logarithmic Scale)

Newly IndustrializedAsian Economies

Advanced Economies

Emerging Markets

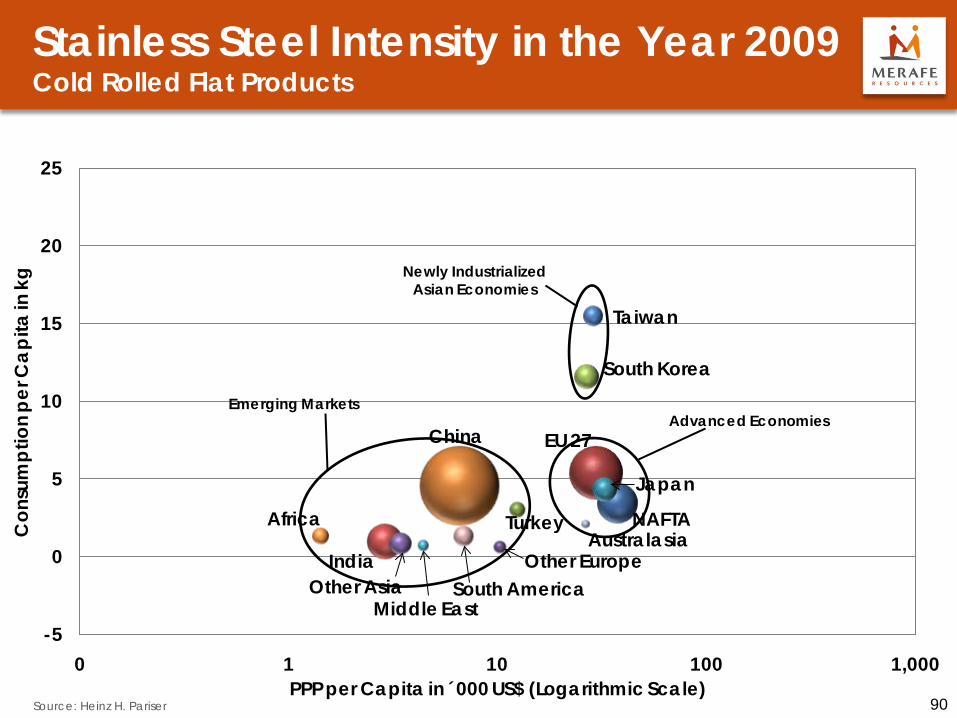

Stainless Steel Intensity in the Year 2009 Cold Rolled Flat Products

90 Source: Heinz H. Pariser

NAFTA

EU 27

Turkey

Other Europe

Japan

China

Taiwan

India

South Korea

Other AsiaMiddle East

AfricaAustralasia

South America

-5

0

5

10

15

20

25

0 1 10 100 1,000

Con

sum

ptio

n pe

r Cap

ita in

kg

PPP per Capita in 000 US$ (Logarithmic Scale)

Newly IndustrializedAsian Economies

Advanced EconomiesEmerging Markets

Stainless Steel Intensity in the Year 2020 Cold Rolled Flat Products

91 Source: Heinz H. Pariser

NAFTA

EU 27

Turkey

Other Europe

JapanChina

Taiwan

India

South Korea

Other AsiaMiddle East

Africa Australasia

South America

-5

0

5

10

15

20

25

0 1 10 100 1,000

Con

sum

ptio

n pe

r Cap

ita in

kg

PPP per Capita in 000 US$ (Logarithmic Scale)

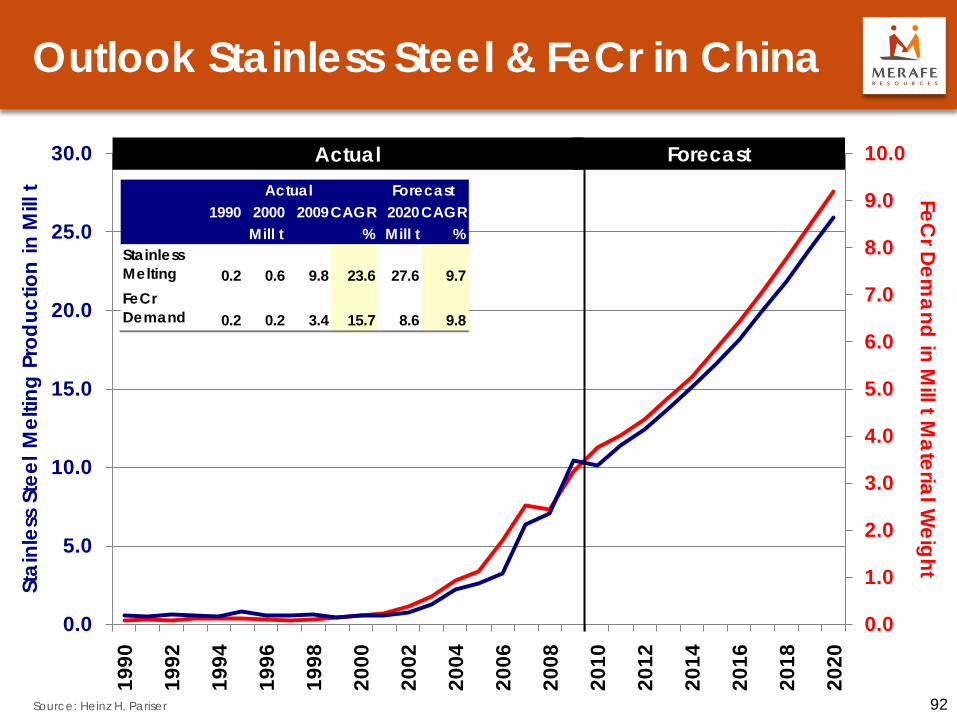

Outlook Stainless Steel & FeCr in China

92 Source: Heinz H. Pariser

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

0.0

5.0

10.0

15.0

20.0

25.0

30.019

90

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

FeCr Dem

and in Mill t M

aterial Weight

Stai

nles

s St

eel M

eltin

g Pr

oduc

tion

in M

ill t

Actual Forecast

1990 2000 2009CAGR 2020CAGR% Mill t %

StainlessMelting 0.2 0.6 9.8 23.6 27.6 9.7FeCrDemand 0.2 0.2 3.4 15.7 8.6 9.8

Actual Forecast

Mill t

China‘s Challenges (1)

93 Source: Heinz H. Pariser

1. It appears that China’s Stainless Steel Market might not reach saturation before 2025.

2. Stainless Steel Demand is expected to increase from presently 7.1 kg /capita to almost 20 kg / capita by 2020 as rural areas are further developed.

3. Crude Stainless Output might subsequently increase by 20 Mill t from presently 9.7 Mill t to 27 Mill t.

4. As China has no intention to intensify (stainless) scrap recycling, ferrochrome requirement might expand parallel to stainless melting, which means FeCr demand will increase from 3.5 Mill t material weight to 8.7 Mill t.

China‘s Challenges (2)

94 Source: Heinz H. Pariser

During the past decade China has rapidly expanded FeCr production on the basis of imported Cr ore. It is questionable whether this can be maintained in future if the following aspects are considered.

1. China’s National Development & Reform Commission (NDRC) is already controlling energy usage, keeping the official reduction of carbon dioxide emission by 40-45% below the 2005 values in mind.

2. During Q3 2010 NDRC has already taken action against 13 of the 31 provinces which had over proportionally energy usage and numerous plants of the iron & steel industry, the ferroalloy industry and the cement industry have been cut off from electricity supply.

3. Pollution is becoming a major concern in China as well and it is the declared policy to reduce emissions. China’s numerous small and often outdated FeCr smelters account for approx. 80% of the country’s ferroalloy output. There is no doubt that also FeCr production in the country is under threat and probably not sustainable.

China‘s Challenges (3)

95 Source: Heinz H. Pariser

4. On the other hand, countries providing Cr ore to China’s FeCr converters are taking a more and more critical stand vs. exports of unprocessed vital raw materials such as Nickel and Chrome

5. South Africa might well benefit from this development provided electricity

availability would be rapidly expanded and triggering expansions of FeCr production facilities.

6. If in the 2009 depression year South Africa had provided China with the same volume of Cr units (1,350 kt) in form of FeCr rather than Cr ore, additional export revenues of more than US$ 2.1 Bill would have been generated. In addition the impact on employment would have resulted in an increase of 77 % or at least 9,500 employees.

96

India – Opportunity or Threat?

India – Stainless Steel & FeCr Demand

97 Source: Heinz H. Pariser

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.519

90

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

FeCr Dem

and in Mill t M

aterial Weight

Stai

nles

s St

eel M

eltin

g Pr

oduc

tion

in M

ill t

Actual Forecast

CAGR:7.5%

CAGR:7.6%

CAGR:12.2%

CAGR:7.2%

India – FeCr Production & Demand

98 Source: Heinz H. Pariser

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

0.0

0.2

0.4

0.6

0.8

1.0

1.219

90

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

FeCr Dem

and in Mill t M

aterial Weight

FeC

r Pro

duct

ion

in M

ill t M

ater

ial W

eigh

t

Actual Forecast

CAGR:7.5%

CAGR:7.6%

CAGR:7.6%

CAGR:7.2%

India – Opportunity or Threat?

99 Source: Heinz H. Pariser

1. India’s Cr Ore reserves are of high quality – but very limited. Subsequently, the Government wants to protect these and has imposed export restrictions and an export tax.

2. India is the third largest exporter of FeCr after South Africa and Kazakhstan. In 2009, the export ratio of FeCr was as high as 72.6%.

3. At the same time, domestic FeCr requirement will be strongly increasing as major stainless steel expansions are under way.

4. Since 2004, India is a regular importer of Cr ore; import volumes reached in 2008 a record volume of 122 kt, but declined last year to 57 kt. Main supply sources include UAE and Oman; South Africa plays a minor role.

5. With sufficient electricity availability, South Africa might be well positioned to provide India not only with Cr ore but also FeCr.

100

Stainless Steel – Old concepts renewed?

Changing Stainless Market Leadership…

101 Source: Heinz H. Pariser

… Changing (Raw Material) Strategies Region Scrap

AvailabilityScrap Input

RatioScrap Trade Interest in

PrimaryMetals

United States High High Exports Very low

Japan Sufficient Medium Exports Backward integrated

EU High Above average Large Exports Minimal

China Low Low High ImportsContinuing

Investments in Cr & Ni

1950 1960 1970 1980 1990 2000 2010

United States Japan EU China

RoW - Stainless Steel Old Concepts Renewed?

102 Source: Heinz H. Pariser

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0.0

5.0

10.0

15.0

20.0

25.019

90

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

FeCr Dem

and in Mill t M

aterial Weight

Stai

nles

s St

eel M

eltin

g Pr

oduc

tion

in M

ill t

Actual Forecast

CAGR:3.5%

CAGR:3.7%

CAGR:2.6%

CAGR:2.1%

Stainless Steel Old Concepts Renewed?

103 Source: Heinz H. Pariser

1. Underlying desire to further consolidation in Europe (ArcelorMittal; ThyssenKrupp Stainless)

2. Phasing out high of nickel containing stainless grades favors primary chrome requirements for ferritic stainless steels.

3. Subsequently primary Cr units will benefit from the changing product mix

4. Cr requirements outside China and India are expected to expand from 3.3 Mill t last year to 5.5 Mill t by 2020 (CAGR 2.3%)

104

Conclusions

Conclusion

105 Source: Heinz H. Pariser

1. South Africa has the largest Cr reserves and accounts presently for half of the global Cr ore supply. Ore availability is further supported through mining of UG2 platinum containing ores. Due to lack of electricity, this wealth is not fully utilised for a few years now.

2. China has become the World’s largest stainless steel producer for which substantial volumes of Cr are needed. The country is presently meeting some 40% of the requirement through converting imported Cr ore into FeCr while almost 60% are covered through imports of FeCr. As China’s policy aims at reducing energy usage and pollution drastically, South Africa is well positioned to meet the needs as soon as sufficient electricity is available.

Conclusion

106 Source: Heinz H. Pariser

3. India is in a similar situation as stainless demand and production expands rapidly. High grade Cr reserves are limited and India has already undertaken counteractions by imposing export restrictions as well as an export tax and noteworthy volumes of Cr ore are meanwhile imported from Middle East countries. Opportunities exist for South Africa to participate in this market development either through Cr ore or preferably with FeCr supply.

4. Stainless demand and production in all other markets continues growing but at a slower pace than in the past. These markets in America, Europe, Japan and Asia are already well covered by South Africa and it is assumed that the present position will be maintained.

5. In conclusion: South Africa enjoys excellent opportunities for its Cr industry, but substantial investments in electricity supply are needed to harvest the country’s wealth and recover its dominant market position.

107 Source: Heinz H. Pariser

Any Questions?

108 Source: Heinz H. Pariser

Contact Details

Heinz H. Pariser Heinz H. Pariser Alloy Metals & Steel Market Research Scharnstr. 51 46509 Xanten Germany Tel.: +49 2801 77 11 0 Email: [email protected] You are always welcome to contact us.