A mergermArket report on globAl m&A Activity Monthly M&A ...

37

MONTHLY M&A INSIDER A MERGERMARKET REPORT ON GLOBAL M&A ACTIVITY NOVEMBER 2011

Transcript of A mergermArket report on globAl m&A Activity Monthly M&A ...

Monthly M&A InsIderA mergermArket report on globAl m&A Activity

november 2011

Monthly M&A InsIdermergermarket

GlobAl overvIew 01

AmericAs: lAtin AmericA 06

north AmericA 11

AsiA-pAcific 16

europe 21

middle eAst & AfricA 27

About MerrIll corporAtIon 32

80 strandlondon, Wc2r 0rlunited kingdom

t: +44 (0)20 7059 6100f: +44 (0)20 7059 [email protected]

11 West 19th street 2nd fl.new york, ny 10011usA

t: +1 212 686-5606f: +1 212 [email protected]

suite 2401-3grand millennium plaza181 Queen’s road, centralhong kong

t: +852 2158 9700f: +852 2158 [email protected]

www.mergermarket.comPart of the mergermarket group

CONTENTS

Monthly M&A Insider

globAl overvieW

01

The bar has been raised for M&A rationale in Britain after G4S was forced to retreat from a US$8.2bn bid for ISS due to disapproval from investors. What was momentarily a welcome sign of optimism for Europe now serves as a bitter lesson concerning market sentiment. In defence of G4S, gauging the opinions of institutional investors poses dealmakers with a double edged challenge: shareholders are unwilling to be made privy to inside information because this would cause them to have to relinquish their trading privileges under the law, and in times of uncertainty their demand for flexibility goes up.

Another major deal to grind to a halt was the US$7.1bn sale of BP’s majority stake in Argentine oil giant Pan American Energy to Bridas, which is jointly owned by Chinese CNOOC and the Bulgheroni family in Argentina. This deal, which failed to gain regulatory approval in China and Argentina, serves as an unfortunate blight on what was otherwise a knockout month for the Energy, Mining & Utilities sectors, which posted a record US$63bn announced deals, constituting 40% of the global total. If successful, the US$38bn tie-up between Kinder Morgan and El Paso will create America’s largest energy infrastructure owner, and the need to pay down El Paso’s bulging debt by selling off its upstream arm adds another transaction to the pipeline. The US$4.5bn purchase of Brigham by Statoil, and the US$2.8bn acquisition of Daylight Energy demonstrate continued foreign interest in

US and Canadian oil and gas assets. The Brigham deal gives Norwegian Statoil access to US shale reserves, an answer to diminishing margins on its European assets. Sinopec’s investment in Daylight Energy is a good example of continued expansion by Chinese oil firms overseas: the three largest Chinese producers have spent more than US$14bn on acquisitions this year.

Positive news also came from the TMT space where four large-cap deals were announced in October with a combined value of US$10.4bn. EMI, the indebted music group repossessed by Citigroup from Guy Hands’ Terra Firma earlier this year now looks like it could fetch a total of up to US$3.9bn. The tussle to gain control of EMI’s music recording division could have a transformational effect on the balance of power in the music industry. Meanwhile, Sony’s US$1.5bn acquisition of the half of Sony Ericsson that it does not already own is the latest outbound Japanese deal. Under the terms of agreement Sony will gain access to patents crucial for the development of their Smartphone business.

It is a small consolation for the overall gloomy outlook that depressed European stock markets have weakened prey for private equity buyers. With some analysts suggesting valuations are as much as 30% below what they ought to be, the last quarter of 2011 could be a period when some brave investors build the foundations for profits in the medium term.

GlOBAl OvErvIEW

head of research: Elias latsis

editor: Felicity James

For advertising opportunities contact:

erik wickman

tel: + (1) 212 6863329 [email protected]

Global overview: robert Imonikhe

latin America: Jennifer ruiz and Urna Chakraborty

north America: Jason Cozza

Asia-pacific: rus Beasley

europe: Samuel Tedjasukmana and Damien Julliard

Middle east & Africa: Yannis Papacostas and Marie-laure Keyrouz

GlobAl overvIew

THIS HAS BEEN A DISAPPOINTING MONTH FOr DEAl MAKErS; THE US$134.4BN WOrTH OF ANNOUNCED DEAlS IS MOrE THAN A qUArTEr lESS THAN IN OCTOBEr OF lAST YEAr AND JUST 7% HIGHEr THAN FOr THE SAME PErIOD IN 2009. IT SEEMS THAT vOlATIlE MArKETS AND THE ECONOMIC MESS IN THE EUrOzONE HAvE TAKEN THEIr TOll ON M&A AMBITIONS. TO MAKE MATTErS WOrSE, A NUMBEr OF HIGH PrOFIlE DEAlS HAvE COllAPSED WHICH IS lIKElY TO DAMAGE CONFIDENCE GOING FOrWArD. lAST YEAr, THE NUMBEr OF DEAlS rOSE BY MOrE THAN A FIFTH BETWEEN OCTOBEr AND DECEMBEr, BUT WITH CrEDIT MArKETS rEElING AND A DrOP-OFF IN BUSINESS CONFIDENCE, FEW ExPECT TO SEE A rEPEAT OF THIS TrEND IN THE MONTHS TO COME.

Monthly M&A Insider 02

globAl overvieW

TrEND GrAPHS

GlobAl M&A quArterly trend

0

200

400

600

800

1,000

1,200

1,400

Q411*

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Valu

e (U

S$bn

)

Total value Mid-market value

Num

ber of deals

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Total volume Mid-market volume

0

50

100

150

200

250

300

350

400

Q411*

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

100

200

300

400

500

600

700

800

900

GlobAl M&A AnnuAl trend GlobAl M&A AnnuAl prIvAte equIty trend

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

YTD 2011*201020092008200720062005

Valu

e (U

S$bn

)

Total value Mid-market value

Num

ber of deals

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Total volume Mid-market volume

0

100

200

300

400

500

600

700

800

900

YTD 2011*201020092008200720062005

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

500

1,000

1,500

2,000

2,500

3,000

3,500

GlobAl M&A quArterly prIvAte equIty trend

Monthly M&A Insider 03

globAl overvieW

TrEND GrAPHS

GlobAl M&A sector breAkdown ytd 2011

GlobAl GeoGrAphIc breAkdown ytd 2011

vAlUE

vAlUE

vOlUME

vOlUME

24.8% 4.1%

0.2%

2.2%3.5%2.0%

0.3%

9.2%

1.2%

12.4%

16.8%

15.2%

8.0%

Industrials & Chemicals

TMT

Consumer

Business Services

Energy, Mining & Utilities

Financial Services

Pharma, Medical & Biotech

Construction

Leisure

Transportation

Real Estate

Agriculture

Defence

1.6% 5.3%

44.4%

31.7%

17.0% Asia-Pacific

Europe

North America

Middle East & Africa

Latin America

3.0%3.5%

1.1%1.5%

9.2%

8.7%

0.3%

12.7%13.3%

15.0%

20.0%3.5%

3.5%

Industrials & Chemicals

TMT

Consumer

Business Services

Energy, Mining & Utilities

Financial Services

Pharma, Medical & Biotech

Construction

Leisure

Transportation

Real Estate

Agriculture

Defence

4.8%2.4%

32.2%

41.3%

19.3% Asia-Pacific

Europe

North America

Middle East & Africa

Latin America

Monthly M&A Insider 04

globAl overvieW

TrEND GrAPHS

GlobAl M&A deAl sIze breAkdown

vAlUE vOlUME

0

10

20

30

40

50

60

70

80

90

100

YTD 2011*201020092008200720062005

38.8%

15.5%

22.1%

8.5%

15.1%

42.3%

16.8%

20.8%

7.5%

12.6%

39.8%

16.9%

22.1%

7.9%

12.5%

42.0%

15.3%

19.3%

8.9%

14.5%

40.6%

16.5%

20.5%

7.9%

14.5%

27.2%

21.0%

27.8%

9.3%

14.7%

34.4%

18.2%

24.9%

9.5%

13.1%

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

Per

cent

age

80

82

84

86

88

90

92

94

96

98

100

YTD 2011*201020092008200720062005

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

1.0%

4.5%

4.7%

89.2%

1.2%

5.0%

4.7%

88.3%

0.7%

1.3%

5.5%

5.1%

87.4%

0.6%

0.9%

3.9%

4.6%

90.1%

0.5%

1.0%

3.8%

3.9%

90.9%

89.1%

4.5%

4.8%

1.2%

0.4%

1.1%

5.0%

5.1%

88.2%

0.7% 0.6%

Per

cent

age

0.7%

You can be ready for due diligence in a matter of hours with Merrill DataSite. In today’s dynamic market,

you need to be poised and ready to take advantage of fast-moving opportunities. That’s why so many dealmakers

rely on Merrill DataSite to give them an edge. We make it easy to transform a paper data room of thousands – or

millions – of pages into a secure, virtual data room that is accessible around the clock to prospective buyers via

the Internet worldwide.

Best of all, you don’t have to be an expert to get started. Merrill DataSite’s expert project managers are available

24-7 to help you. We’ve helped clients launch thousands of projects for deals

of all sizes – valuable experience that we’ll put to work for you.

At Merrill DataSite, we believe in sharing ideas and best practices that assist

companies in expanding and capturing new opportunities. To download our

FREE industry survey reports please visit the Merrill DataSite Knowledge

Center at www.datasite.com.

datasite.com

M E R R I L L D A T A S I T E

We thought of that.

“We have one week to make

40,000 pagesof informationavailable for due diligence.Where do we start?”

LATIN AM

ERICA

LATIN AMERICAA MERgERMARkET M&A REpoRT oN

Monthly M&A Insider 06

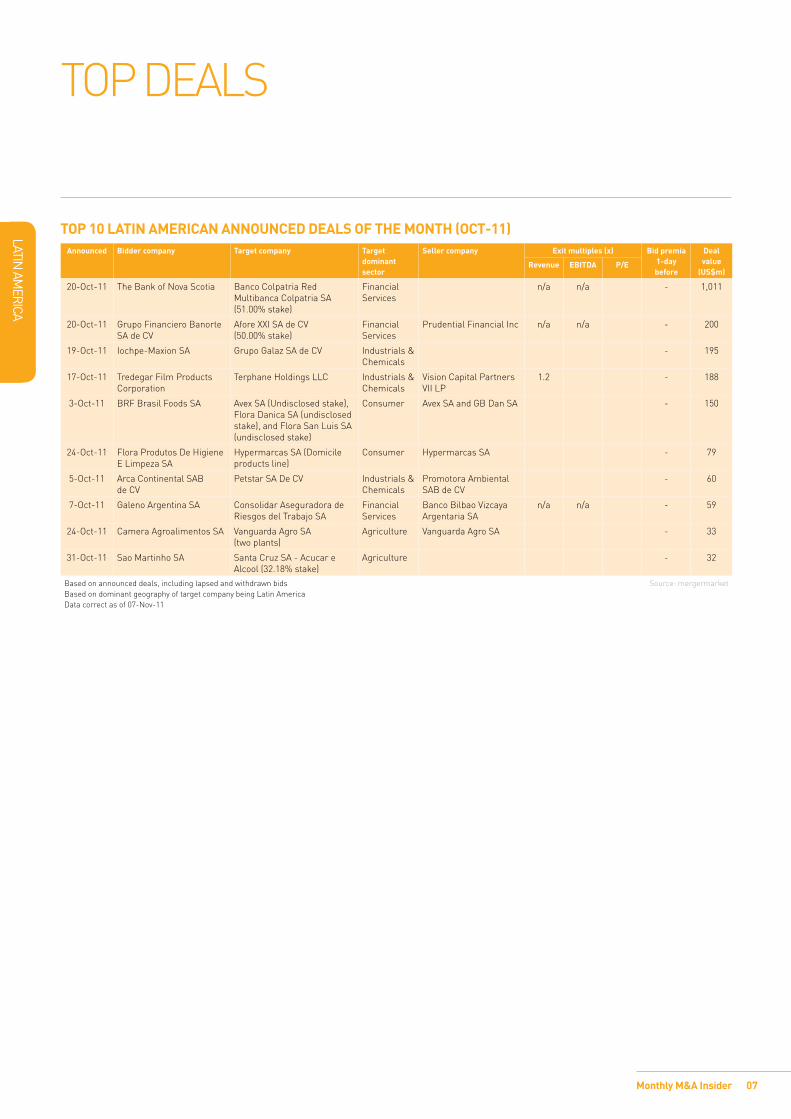

The Telecommunications sector has led in terms of value with US$26.1bn worth of deals in 2011YTD, tallying 11 deals in october. The sector comprises 26.8% of Latin American M&A by value and 2.4% by volume but is surprisingly absent from october’s list of top deals.

This month’s top deal, Bank of Nova Scotia’s US$1bn acquisition of a majority stake in Colombia-based Banco Colpatria Red Multibanca Colpatria SA expands the Canada-based banks presence in South America. In the year to date, Brazil and Chile are the two leading countries by value with US$67.4bn or 69.1% of total market share and US$ 7.9bn or 8.1% respectively.

Deal value down, deal count up

overall, M&A in october this year decreased in value by 81.6% compared to M&A performance last year (US$11.4bn in 2010). Deal volume also decreased by 20.6% from last year (34 deals in 2010). This has led to lower year-to-date aggregate value in 2011 (US$97.6bn), a decrease of 26% from last year’s US$132bn.

Exit deal made top 5 YTD in Latin AmericaDespite less private equity activity in october, the month saw a successful exit for Vision Capital. Having made its investment one year earlier, the firm sold Brazil-based Terphane Holdings, a manufacturer and supplier of polyester films to Tredegar, the US-based company that produces and supplies aperture and elastic materials, for a consideration of US$188m. This transaction is the fourth largest exit in Latin America in 2011 so far. The largest exit of the year remains Intercontinental Exchange’s acquisition of Cetip for US$512m.

LATIN AMERICAN M&A IN oCToBER of 2011 SAw Low VoLUME AND Low VALUE wITH 27 DEALS CoLLECTIVELY VALUED AT oNLY US$2.1BN. So fAR THIS YEAR, THE CoNSUMER SECToR HAS DoMINATED IN TERMS of VoLUME wITH 86 DEALS, TRAILED CLoSELY BY INDUSTRIALS & CHEMICALS wHERE 81 DEALS wERE RECoRDED, THREE of wHICH wERE A pART of oCToBER’S Top DEALS.

07

LATIN AM

ERICA

Monthly M&A Insider

Top 10 LATIN AMERICAN ANNouNCED DEALs of ThE MoNTh (oCT-11)Announced Bidder company Target company Target

dominant sector

seller company Exit multiples (x) Bid premia1-day before

Deal value

(us$m)Revenue EBITDA p/E

20-oct-11 The Bank of Nova Scotia Banco Colpatria Red Multibanca Colpatria SA (51.00% stake)

financial Services

n/a n/a - 1,011

20-oct-11 grupo financiero Banorte SA de CV

Afore XXI SA de CV (50.00% stake)

financial Services

prudential financial Inc n/a n/a - 200

19-oct-11 Iochpe-Maxion SA grupo galaz SA de CV Industrials & Chemicals

- 195

17-oct-11 Tredegar film products Corporation

Terphane Holdings LLC Industrials & Chemicals

Vision Capital partners VII Lp

1.2 - 188

3-oct-11 BRf Brasil foods SA Avex SA (Undisclosed stake), flora Danica SA (undisclosed stake), and flora San Luis SA (undisclosed stake)

Consumer Avex SA and gB Dan SA - 150

24-oct-11 flora produtos De Higiene E Limpeza SA

Hypermarcas SA (Domicile products line)

Consumer Hypermarcas SA - 79

5-oct-11 Arca Continental SAB de CV

petstar SA De CV Industrials & Chemicals

promotora Ambiental SAB de CV

- 60

7-oct-11 galeno Argentina SA Consolidar Aseguradora de Riesgos del Trabajo SA

financial Services

Banco Bilbao Vizcaya Argentaria SA

n/a n/a - 59

24-oct-11 Camera Agroalimentos SA Vanguarda Agro SA (two plants)

Agriculture Vanguarda Agro SA - 33

31-oct-11 Sao Martinho SA Santa Cruz SA - Acucar e Alcool (32.18% stake)

Agriculture - 32

Based on announced deals, including lapsed and withdrawn bids Based on dominant geography of target company being Latin AmericaData correct as of 07-Nov-11

Source: mergermarket

Top DEALS

LATIN AM

ERICA

Monthly M&A Insider

TREND gRApHS

LATIN AMERICAN M&A quARTERLY TREND

0

10

20

30

40

50

60

70

Q411*

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Total value Mid-market value

Num

ber of dealsValu

e (U

S$bn

)

0

20

40

60

80

100

120

140

160

180

Total volume Mid-market volume

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Q411*

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Valu

e (U

S$m

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

2

4

6

8

10

12

14

16

18

LATIN AMERICAN M&A ANNuAL TREND LATIN AMERICAN M&A ANNuAL pRIvATE EquITY TREND

0

20

40

60

80

100

120

140

160

180

YTD 2011*201020092008200720062005

Total value Mid-market value

Num

ber of dealsValu

e (U

S$bn

)

0

100

200

300

400

500

600

Total volume Mid-market volume

0

1000

2000

3000

4000

5000

6000

7000

8000

YTD 2011*201020092008200720062005

Valu

e (U

S$m

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

5

10

15

20

25

30

35

40

45

50

LATIN AMERICAN M&A quARTERLY pRIvATE EquITY TREND

08

LATIN AM

ERICA

Monthly M&A Insider

TREND gRApHS

LATIN AMERICAN M&A gEogRAphIC BREAkDowN YTD 2011

VALUE VoLUME

69.1%

8.1%

5.8%0.1%

0.2%0.2%

0.5%0.02%

0.2%

2.4% 1.5% 4.6%

7.2% Brazil

Chile

Colombia

Dominican Republic

Ecuador

El Salvador

Guatemala

Honduras

Mexico

Panama

Peru

Uruguay

Argentina

0.9%

0.6%

8.4%

7.4%

0.4%

0.6%0.4%

0.2%

1.1%

0.4% 9.7%0.2%

53.9%

6.3%

0.6%

8.7%

Brazil

Chile

Colombia

Costa Rica

Dominican Republic

Ecuador

El Salvador

Guatemala

Honduras

Mexico

Panama

Peru

Uruguay

Venezuela

Argentina

Bolivia

LATIN AMERICAN M&A sECToR BREAkDowN YTD 2011

VALUE VoLUME

26.8%

13.5%

23.3%

0.04%

0.1%

0.2%

3.5%1.4% 11.0%

0.7%

11.0%

0.4%

0.6%

2.0%

5.6%

Consumer

Industrials & Chemicals

Energy, Mining & Utilities

Business Services

Financial Services

Pharma, Medical & Biotech

Agriculture

Technology

Transportation

Construction

Telecommunicatons

Media

Leisure

Real Estate

Defence

18.6%

17.5%5.6%

5.0%

3.9%

3.9%

3.0%

1.9%

2.2%2.4%

1.9% 0.6%

8.2%

13.8%11.4%

Consumer

Industrials & Chemicals

Energy, Mining & Utilities

Business Services

Financial Services

Pharma, Medical & Biotech

Agriculture

Technology

Transportation

Construction

Telecommunicatons

Media

Leisure

Real Estate

Defence

09

10

LATIN AM

ERICA

Monthly M&A Insider

LATIN AMERICAN M&A DEAL sIzE BREAkDowN

VALUE VoLUME

0

10

20

30

40

50

60

70

80

90

100

YTD 2011*201020092008200720062005

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

17.6%

7.1%

26.9%

21.0%

27.3%

46.9%

8.3%

21.8%

10.3%

12.7%

16.2%

10.8%

31.4%

16.2%

25.4%

30.5%

20.3%

24.5%

10.0%

14.7%

9.2%

29.3%

36.7%

10.1%

14.8%9.5%

6.9%

24.9%

19.2%

39.5%

26.6%

16.8%

31.2%

11.5%

13.9%

Per

cent

age

20

30

40

50

60

70

80

90

100

201020092008200720062005

0.3%

4.4%

7.1%

87.8%

1.0%

5.4%

7.4%

85.1%

0.2%

5.3%

6.4%

87.4%

0.6%

4.7%

5.3%

88.2%

0.3%

6.9%

5.4%

85.6%82.2%

6.3%

8.2%

1.2%0.3% 1.0% 0.7% 1.2% 1.8% 2.0%

6.9%

6.5%

84.9%

0.6%

Per

cent

age

1.1%

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

YTD 2011*

TREND gRApHS

NORTH

AMERICA

A mergermArket m&A report on

11Monthly M&A Insider

nortH AmerICA

EnErgy dEAls doMInAtE nortH AMErICAn top dEAls for tHE MontH of oCtobEr

For tHe montH oF oCtober, tHe ConsolIdAted energy, mInIng & UtIlItIes seCtor domInAted tHe top deAls In nortH AmerICA. AnnoUnCed on 16 oCtober, kInder morgAn’s bId For el pAso CorporAtIon HAd A totAl deAl vAlUe oF Us$37bn - tHe lArgest deAl In tHe seCtor tHIs yeAr And tHe seCond lArgest overAll In nortH AmerICA And globAlly. tHe trAnsACtIon Is expeCted to reCeIve An extended revIew by tHe FederAl trAde CommIssIon. FtC ConCerns CoUld be resolved tHroUgH dIsposAl oF CertAIn Assets, sAy soUrCes FAmIlIAr wItH tHe trAnsACtIon.

statoil’s acquisition of brigham exploration was the second largest deal of the month with a total deal value of Us$4.5bn, followed by Cigna’s acquisition of Healthspring for Us$3.7bn in the pharma, medical & Utilities sector.

overall M&A transaction values for 2011 indicate economic health may be improvingoverall m&A activity by aggregate deal value has already surpassed overall year-end deal value from last year. In 2010, aggregate deal value reached Us$797.9bn with 4,069 announced deals. 2011 has surpassed this value with an aggregate 3,094 deals worth Us$823.4bn – representing a 3% increase by deal value.

similarly, private equity buyouts are almost ahead of 2010, which saw 748 deals valued at Us$105bn. In the year to date, 2011 has seen 550 buyout transactions worth Us$103.9bn.

ytd north America sector breakdown In the year to date in 2011, energy, mining & Utilities are dominating the deal value sector breakdown with 31% of the market. Industrial & Chemicals represented the second largest sector with 15% of the market share, followed by pharma, medical & biotech with 13% of the market.

by volume, Industrials & Chemicals is the most active sector, representing 17% of north America deals. tmt came next with 15%, followed by business services and pharma, medical & biotech representing 13% and 12%, respectively.

12

NORTH

AMERICA

Monthly M&A Insider

top deAls & expeCted deAls

top 10 nortH AMErICAn AnnounCEd dEAls of tHE MontH (oCt-11) Announced bidder company target company target dominant

sectorseller company Exit multiples (x) bid premia

1-day before

deal value(us$m)revenue EbItdA p/E

16-oct-11 kinder morgan Inc el paso Corporation energy, mining & Utilities

8.1 11.4 25.2 32.3% 37,439

17-oct-11 statoil AsA brigham exploration Company

energy, mining & Utilities

26.7 72.7 96.1 20.2% 4,520

24-oct-11 Cigna Corporation Healthspring Inc pharma, medical & biotech

1.2 10.5 16.2 37.0% 3,734

03-oct-11 Carlyle group and Hellman & Friedman llC

pharmaceutical product development Inc

pharma, medical & biotech

2.3 13.6 31.1 29.6% 3,416

10-oct-11 superior energy services Inc Complete production services Inc

energy, mining & Utilities

2.0 8.3 30.6 62.3% 3,101

17-oct-11 Amerigas partners lp titan energy partners lp and Heritage operating lp

energy, mining & Utilities

energy transfer partners lp

- 2,871

10-oct-11 China petroleum & Chemical Corporation

daylight energy ltd energy, mining & Utilities

5.1 8.1 41.9 121.6% 2,760

11-oct-11 Ares management llC and Canada pension plan Investment board

99 Cents only stores Consumer 1.1 10.6 21.0 7.4% 1,531

19-oct-11 permira genesys telecommunications laboratories Inc

technology Alcatel-lucent 3.0 - 1,500

12-oct-11 pratt & whitney International Aero engines Ag (undisclosed stake)

Industrials & Chemicals

rolls-royce plc - 1,500

based on announced deals, including lapsed and withdrawn bids based on dominant geography of target company being north America (Us + Canada) data correct as of 07-nov-11

source: mergermarket

13

NORTH

AMERICA

Monthly M&A Insider

situation target company sector potential bidder company

financial advisor to bidder (b); target (t); seller (s)

seller company

Market cap/ est.

value (us$m)

Comments

expected deal Interdigital telecommunications google Inc; Apple Inc; Intel Corporation; ericsson Ab; research in motion limited; microsoft Corporation; sony Corporation

barclays (t), evercore partners (t)

2,362 Interdigital Inc, the listed Us based company engaged in the design and development of digital wireless technology solutions, announced on 19-Jul-2011 that its board of directors has initiated a process to explore and evaluate potential strategic alternatives for the company, including a possible sale. Interested parties are said to have included google, Apple, Intel, ericsson, research in motion, microsoft, and sony.

expected deal Jakks pacific Inc Consumer oaktree Capital rothschild (t) 492 on 13-sep-2011, Jakks pacific Inc, the listed Us-based manufacturer of toy products, received a public unsolicited offer from oaktree Capital to buy the target at Us$20 per share. the bidder already owns a 4.99% stake in Jakks. this offer was unanimously rejected by the target's board of directors on 05-oct-2011

expected deal semgroup Corporation

energy, mining & Utilities

plains All American pipeline

1,190 on 24-oct-2011, plains All American pipeline, l.p. made an offer of Us$24 per share for semgroup Corporation, the listed Us based provider of transportation and storage services to the oil and gas sector. plains stated that the offer represented a 16% premium over semgroup's 10-day average closing price through 05-oct-2011. nonetheless, semgroup has rejected the offer as being too low and claimed that the offer actually represented a mere 2% premium over the previous trading day's close.

expected deal AmAg pharmaceuticals Inc

pharma, medical & biotech

msmb Capital mA 286 on 03-Aug-2011, AmAg pharmaceuticals, the listed Us based biopharmaceutical company, received an unsolicited proposal from msmb Capital management to acquire the company at Us$18 per share in cash. AmAg board of directors has unanimously opposed the proposal and urged stockholders to take no action on the offer. one of the reasons why the board of directors might not support the acquisition is that msmb is proposing to remove six of the seven current members of AmAg's board and to replace them with its own nominees.

expected deals based on confirmed announcements by companies involved

pIpElInE of nortH AMErICAn ExpECtEd dEAls

top deAls & expeCted deAls

14

NORTH

AMERICA

Monthly M&A Insider

trend grApHs

nortH AMErICAn M&A quArtErly trEnd

0

100

200

300

400

500

600

Q411*

Q3 11

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Valu

e (U

S$bn

)

Total value Mid-market value

Num

ber of deals

0

200

400

600

800

1,000

1,200

1,400

1,600

Total volume Mid-market volume

0

50

100

150

200

250

Q411*

Q 11

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

50

100

150

200

250

300

350

nortH AMErICAn M&A AnnuAl trEnd nortH AMErICAn M&A AnnuAl prIvAtE EquIty trEnd

0

200

400

600

800

1,000

1,200

1,400

1,600

YTD 2011*201020092008200720062005

Total value Mid-market value

Num

ber of dealsValu

e (U

S$bn

)

0

1,000

2,000

3,000

4,000

5,000

6,000

Total volume Mid-market volume

0

50

100

150

200

250

300

350

400

450

500

YTD 2011*201020092008200720062005

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

200

400

600

800

1,000

1,200

nortH AMErICAn M&A quArtErly prIvAtE EquIty trEnd

15

NORTH

AMERICA

Monthly M&A Insider

trend grApHs

nortH AMErICAn M&A sECtor brEAkdown ytd 2011

vAlUe volUme

16.0%

1.0%

2.0%

9.0%3.0%

30.0%

5.0%

13.0%

9.0%

7.0%1.0%4.0%

0.4% 0.1%

Industrials & Chemicals

Technology

Business Services

Pharma, Medical & Biotech

Financial Services

Energy, Mining & Utilities

Consumer

Media

Leisure

Construction

Transportation

Telecommunications

Real Estate

Defence

Agriculture

17.0%

15.0%

13.0%

2.0%2.0%

12.0%

10.0%

3.0%3.0%

9.0%

10.0%

0.1%

1.0%0.4%0.5%

Industrials & Chemicals

Technology

Business Services

Pharma, Medical & Biotech

Financial Services

Energy, Mining & Utilities

Consumer

Media

Leisure

Construction

Transportation

Telecommunications

Real Estate

Defence

Agriculture

nortH AMErICAn M&A dEAl sIzE brEAkdown

vAlUe volUme

0

10

20

30

40

50

60

70

80

90

100

YTD 2011*201020092008200720062005

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

46.5%

15.8%

18.1%

7.0%

12.6%

52.1%

14.9%

17.1%

6.3%

9.6%

42.9%

19.0%

21.8%

6.6%

9.6%

49.3%

13.8%

17.5%

7.2%

12.2%

58.8%

13.3%

13.2%

5.4%

9.2% 12.5%

9.6%

27.8%

18.0%

32.1%

44.0%

20.0%

18.2%

8.0%

9.8%

Per

cent

age

75

80

85

90

95

100

YTD 2011*201020092008200720062005

0.9%1.3%

4.5%

4.8%

88.5%

1.1%

1.5%

5.4%

5.3%

86.8%

1.1%

1.8%

6.3%

5.3%

85.6%

0.9%

3.7%

4.1%

90.6%

1.0%

3.5%

3.8%

91.0%

87.4%

5.2%

5.7%

1.1%0.9%

1.6%

5.3%

5.9%

86.3%

0.7% 0.7% 0.6%

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

Per

cent

age

ASIA-PAcIfIc

A mergermArket m&A report on

Monthly M&A Insider 16

ASIA-pAcIfIc

No rest for the Leisure sector many of october’s top deals were domestic, but there were some significant cross-border transactions as well. the two largest deals of the month by value both involved Japanese companies in the Leisure sector. the first saw Heiwa, the Japan-listed casino gaming device manufacturer, purchase pgm Holdings, the Japan-listed golf club operator for US$2.2bn. According to Heiwa, the deal is an effort to transform the company into a full-scale leisure business. In the second, Bain capital, the US-based private equity firm acquired Skylard, the Japan-based restaurant chain operator, from nomura principal finance and npf-Harmony for a total consideration of US$1.7bn. Largely attributable to these two deals, the Leisure sector represented over one third of Asia-pacific deal value, making it the hottest in the region for the month of october.

A solid month in North AsiaIn terms of geography, north Asian countries including china, Japan and South korea showed the strongest m&A activity in the region during october. Japan saw the greatest transaction value over the month, with the bulk largely attributable to the aforementioned Heiwa and Bain acquisitions. But china hosted the largest number of deals, with 19 transactions worth US$1.9bn taking place over the month. most often, bidders for chinese assets targeted energy, consumer, construction and Industrials & chemicals sectors. close behind china in terms of volume was South korea, which saw 18 deals worth US$1.2bn. In a noteworthy transaction worth US$378m, Interpark, a South korea-based online retailer, agreed to acquire imarketkorea, a South korea-based provider of strategic, outsourcing and consulting procurement services. the deal is expected to close in December 2011.

Asian bidders set to do some buying globallygoing forward, Asian bidders could ramp up outbound deal making as opportunities arise in the struggling global economy. for example, korea national oil (knoc), which has invested approximately US$10bn acquiring overseas energy assets since 2009, is eyeing oil assets in kazakhstan in efforts to produce 300,000 barrels a day next year from its oil fields throughout the world. furthermore in the retail sector, Japanese clothing company, fast retailing, could buy a rival its size or bigger in the US or europe. reports indicate the company believes the strength of the Yen and anemic stock markets make it a good time to buy. In the private equity space, proprietary mergermarket intelligence indicates that a Hong kong-based commodities trader and investment firm, is seeking to raise US$100m for a new private equity fund that will invest in junior explorers in Africa, focused on all types of metal and mineral resources. As Asia-pacific rises in relative strength, bidders from the region will continue to take advantage of m&A opportunities abroad.

WHILe tHe ASIA-pAcIfIc regIon WItneSSeD A fLUrrY of LArger DeALS In Q3 2011, Q4 BegAn WItH A SLoW StArt. octoBer DeAL fLoW cAme Up SHort of SeptemBer ActIvItY, WItneSSIng JUSt 100 DeALS vALUeD At A totAL of US$11.4Bn, A 69% DecLIne In vALUe AnD A 29% DecLIne In voLUme, AmIDSt contInUeD gLoBAL mArket tUrBULence. HoWever, gLoBAL mArket concernS ASIDe, ASIA-pAcIfIc DID See Some IntereStIng ActIvItY tHroUgHoUt octoBer.

17Monthly M&A Insider

ASIA-PAcIfIc

top DeALS

Top 10 AsIA-pAcIfIc ANNouNced deALs of The MoNTh (ocT-11)Announced Bidder company Target company Target dominant

sectorseller company exit multiples (x) Bid premia

1-day beforedeal value

(us$m)Revenue eBITdA p/e

26-oct-11 Heiwa corporation pgm Holdings k k Leisure 2.1 15.0 4.0 28.6% 2,190

21-oct-11 Bain capital LLc Skylark co Ltd (77.76% stake) Leisure nomura principal finance co Ltd; and npf Harmony

0.5 - 1,677

11-oct-11 eurasian natural resources corporation plc

Shubarkol komir JSc (75.00% stake)

energy, mining & Utilities

eurasian Industrial company JSc

10.0 - 650

17-oct-11 Super retail group Limited

rebel Sport Limited consumer Archer capital pty Limited

1.0 7.9 - 631

5-oct-11 Aeon co Ltd marunaka co Ltd (94.96% stake)

consumer nakayama family 0.2 1324.1 - 474

24-oct-11 Jizhong energy group co Ltd

north china pharmaceutical company Limited (25.39% stake)

pharma, medical & Biotech

1.6 21.5 71.1 - 468

31-oct-11 Interpark corporation imarketkorea co Ltd (48.7% stake)

Business Services

Samsung group 0.5 20.6 24.1 24.7% 378

14-oct-11 Wuhan Linuo Solar energy group co Ltd

Xiamen Hongfa electroacoustic co Ltd (75.01% stake)

Industrials & chemicals

Jiangxi electronics group; Lianfa group; and Xiamen Hongfa electroacoustic co Ltd (management and employees)

1.3 12.6 - 359

17-oct-11 H'ng Bok San; H'ng chun Hsiang; and H'ng Hsieh Ling (senior management of Leader Universal Holdings Berhad)

Leader Universal Holdings Berhad (85.59% stake)

energy, mining & Utilities

0.5 11.9 9.4 31.2% 355

28-oct-11 Undisclosed bidder evans Shoal gas field (40.00% stake)

energy, mining & Utilities

Santos Ltd - 350

Based on announced deals, including lapsed and withdrawn bids Based on dominant geography of target company being Asia-pacific Data correct as of 07-nov-11

Source: mergermarket

18

ASIA-PAcIfIc

Monthly M&A Insider

trenD grApHS

AsIA-pAcIfIc M&A quARTeRLy TReNd

0

20

40

60

80

100

120

140

160

180

Q411*

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Valu

e (U

S$bn

)

Total value Mid-market value

Num

ber of deals

0

100

200

300

400

500

600

700

800

900

Total volume Mid-market volume

0

5

10

15

20

25

Q4 11*

Q3 11

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q 06

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

10

20

30

40

50

60

70

80

90

100

AsIA-pAcIfIc M&A ANNuAL TReNd AsIA pAcIfIc M&A ANNuAL pRIvATe equITy TReNd

0

50

100

150

200

250

300

350

400

450

500

YTD 2011*201020092008200720062005

Total value Mid-market value

Num

ber of dealsValu

e (U

S$bn

)

0

500

1,000

1,500

2,000

2,500

3,000

Total volume Mid-market volume

0

10

20

30

40

50

60

70

YTD 2011*201020092008200720062005

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

50

100

150

200

250

300

350

AsIA-pAcIfIc M&A quARTeRLy pRIvATe equITy TReNd

19

ASIA-PAcIfIc

Monthly M&A Insider

trenD grApHS

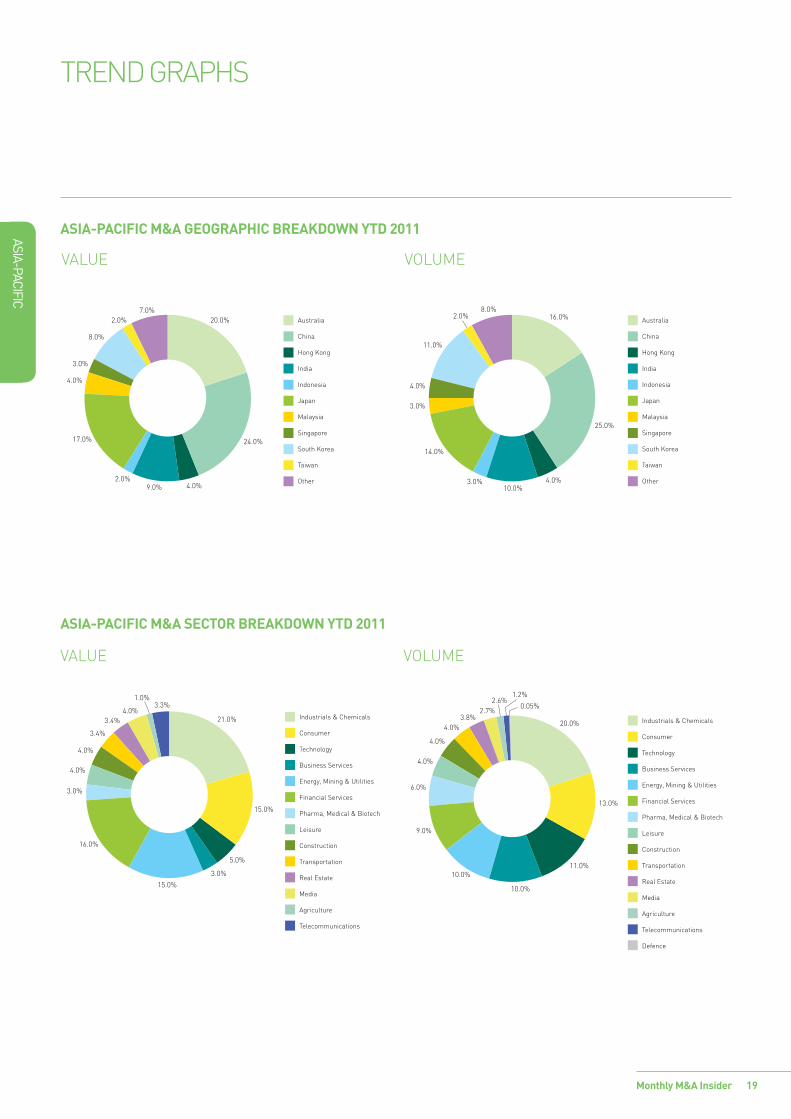

AsIA-pAcIfIc M&A GeoGRAphIc BReAKdoWN yTd 2011

vALUe voLUme

Australia

China

Hong Kong

India

Indonesia

Japan

Malaysia

Singapore

South Korea

Taiwan

Other

20.0%

4.0%2.0%

9.0%

3.0%

17.0%

4.0%

8.0%

2.0%7.0%

24.0%

Australia

China

Hong Kong

India

Indonesia

Japan

Malaysia

Singapore

South Korea

Taiwan

Other

16.0%

4.0%3.0%10.0%

4.0%

14.0%

3.0%

11.0%

2.0%8.0%

25.0%

AsIA-pAcIfIc M&A secToR BReAKdoWN yTd 2011

vALUe voLUme

21.0%

15.0%

3.0%

5.0%

15.0%

16.0%

3.0%

4.0%

3.4%

3.4%

4.0%

1.0%3.3%

4.0%

Industrials & Chemicals

Consumer

Technology

Business Services

Energy, Mining & Utilities

Financial Services

Pharma, Medical & Biotech

Leisure

Construction

Transportation

Real Estate

Media

Agriculture

Telecommunications

20.0%

13.0%

11.0%

10.0%

10.0%

4.0%

4.0%

6.0%

9.0%

4.0%3.8%

2.7%0.05%

1.2%2.6%

Industrials & Chemicals

Consumer

Technology

Business Services

Energy, Mining & Utilities

Financial Services

Pharma, Medical & Biotech

Leisure

Construction

Transportation

Real Estate

Media

Agriculture

Telecommunications

Defence

20

ASIA-PAcIfIc

Monthly M&A Insider

AsIA-pAcIfIc M&A deAL sIze BReAKdoWN

vALUe voLUme

0

10

20

30

40

50

60

70

80

90

100

YTD 2011*201020092008200720062005

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

23.0%

18.8%

28.6%

9.3%

20.3%

19.0%

22.7%

26.9%

11.0%

20.4%

15.6%

17.1%

30.4%

12.6%

24.4%

29.6%

15.8%

22.13%

12.0%

20.4%

19.9%

17.0%

30.5%

11.1%

21.5% 20.9%

10.4%

27.6%

29.4%

11.6%

21.3%

13.9%

31.8%

12.5%

20.4%

Per

cent

age

75

80

85

90

95

100

YTD 2011*201020092008200720062005

1.0%

5.1%

4.5%

89.0%

1.2%

4.8%

4.9%

88.8%

0.9%

5.1%

5.4%

88.3%

0.9%

4.5%

5.8%

88.4%

1.0%

5.5%

5.3%

87.9% 88.4%

5.0%

4.7%

1.7% 0.8%

5.4%

5.9%

87.5%

0.3% 0.3% 0.2%0.4% 0.4%0.4% 0.4%

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

Per

cent

age

trenD grApHS

21Monthly M&A Insider

europe

A mergermArket m&A report on

eUrope

Looking more closely at europe, there has been a constant decline in the total value of deals announced on a monthly basis. Since the peak of €59.7bn reached in April, the value continued to slide, with october closing at €27.6bn, the second lowest month of the year behind January (€21.3bn). the biggest one month drop was in June, when european m&A recorded €42.1bn worth of deals, a 25.5% drop from the €57.9bn seen in may.

Conventional wisdom states that deals are scarce during the summer months due to holidays, which is very much reflected in this year’s stats. However, a linear monthly decline since April to September, and october’s confirmation that the decline did not stop at the end of summer, tells us an altogether different story. Is the recovery in european m&A deal making we saw in 2010 losing steam, and now on potentially prolonged bearish territory? As argued in the last edition of this report, 2010 was the year for companies looking for cut-price deals in europe whilst boosted by cash hoarded during the crisis years of 2008 and 2009. that cash seemed to begin to run out by 2011. the record in october, the first month of Q4 2011, again confirmed that.

With an average of 10.6% monthly decline in value since may, assuming the downward trend continues in the two remaining months, european m&A will record €470bn worth of deals in 2011, down 7% from 2010.

Zimbabwean diamonds versus Anglo-American/De Beersthe US, eU and African countries lifted the ban on Zimbabwean diamond exports in early november, after having imposed it in 2009. the decision will significantly boost the global diamond supply because, as suggested by the Financial times, Zimbabwe may hold about a quarter of the world’s current diamond reserves. this poses a threat to De Beers, which currently controls 35% of the diamond market according to the same source, after its cartel virtually monopolised the diamond market over the last century.

Almost immediately, Anglo-American announced the US$5.1bn acquisition of a 40% stake in De Beers held by the oppenheimer family. the acquisition increases Anglo-American’s holding in the diamond company to 85%, effectively consolidating it. It sends a strong message to De Beers’ strongest competitor Alrosa, as well as to competitors, such as rio tinto and petra Diamonds, that Anglo-American means business in the diamond sector. It is ready to beef up De Beers to challenge the ever-increasing competition, especially now that Zimbabwe’s huge diamond reserve is up for grabs. Bids for marange resources and mbada, both diamond producers in Zimbabwe, are therefore expected in the coming weeks and months, especially from De Beers’ big competitors. Anglo-American may also be in a position to buy as well.

EuropEAn M&A on coursE to closE 2011 lowEr thAn 2010

AS oF 31 oCtoBer 2011, eUrope SAW A totAL oF €423.4Bn WortH oF m&A DeALS AnnoUnCeD In 2011, ABoUt €80.7Bn SHort oF tHe €504.1Bn reCorDeD At tHe enD oF 2010. WItH An AverAge oF €42.3Bn WortH oF DeALS AnnoUnCeD per montH In eUrope tHIS yeAr, It DoeS not Seem too UnreALIStIC to At LeASt reACH tHe 2010 FIgUre, AS tHe yeAr StILL HAS tWo montHS to go.

22

europe

Monthly M&A Insider

top DeALS & expeCteD DeALS

top 10 EuropEAn AnnouncED DEAls of thE Month (oct-11) Announced Bidder company target company target dominant

sectorseller company Exit multiples (x) Bid premia

1-day before

Deal value(€m)revenue EBItDA p/E

17-oct-11 g4S plc ISS A/S Industrials & Chemicals

eQt partners AB; andgS Capital partners

0.6 9.0 5,927

10-oct-11 government of Belgium

Dexia Banque Belgique S.A. Financial Services

Dexia SA 5.9 4,000

31-oct-11 China Investment Corporation

gDF Suez exploration & production (30.00% stake)

energy, mining & Utilities

3.5 5.5 2,300

10-oct-11 Banco popular espanol S.A.

Banco pastor S.A. Financial Services

1.1 30.6% 1,349

27-oct-11 Sony Corporation Sony ericsson mobile Communications management Ltd (50.00% stake)

technology ericsson AB 0.3 23.2 1,050

12-oct-11 marubeni Corporation; and teekay Lng partners Lp.

A.p. moeller – maersk (8 Lng carriers)

transportation A.p. moller – maersk A/S 1,048

10-oct-11 precision Capital kBL european private Bankers S.A.

Financial Services

kBC groep nv 14.8 1,000

14-oct-11 Unilever plc oJSC Concern kalina Consumer 2.1 12.9 23.8 57.8% 604

31-oct-11 China Investment Corporation

gDF Suez SA (train 1 of the Atlantic Lng liquefaction plant located in trinidad and tobago) (10.00% stake)

energy, mining & Utilities

gDF Suez SA 600

27-oct-11 Lansforsakringar AB Lansforsakringar Fondliv Financial Services

Lansforsakringar Liv Forsakrings AB

587

Based on announced deals, including lapsed and withdrawn bids Based on dominant geography of target company being europe Data correct as of 07-nov-11

Source: mergermarket

23

europe

Monthly M&A Insider

pIpElInE of EuropEAn ExpEctED DEAlssituation target company sector potential bidder

companyfinancial adviser to bidder (B); target (t); seller (s)

seller company Market cap/est.

value (€m)

comments

rumoured takeover

telecom Italia SpA telecommunications vivendi SA 16,200 vivendi [vIv Fr], the listed French media and telecom group, today denied any interest in listed Italian group telecom Italia (tI).

expected deal

orange Switzerland telecommunications Doughty Hanson; providence; eQt; goldman Sachs; and Apax

1,650 Second round bids for France telecom-owned orange Switzerland are due on 12 December, two sources close to the situation said.

potential takeover target

Detskiy mir Consumer AFk Sistema; Sberbank

478 Detskiy mir, a private, russian retailer of children's goods, is interested in approaches from strategic investors, chief financial officer katerina Laryushkina told this news service at the Adam Smith CFo Summit in moscow

potential takeover target

magellan SA pharma, medical & Biotech

enterprise Investors 55 magellan, the listed polish medical sector financing provider, is holding off a decision on a possible management buyout (mBo) and on its planned entry into the Hungarian market, Chief executive officer krzysztof kawalec said

potential takeover target

Ad2one technology France telecom; BSkyB group plc

46 Ad2one, a Uk-based digital sales agency, will look to hire an advisor in Q1 2012 with a view to selling, grant Alloway, joint managing Director said

note: expected deals based on confirmed announcements by companies involved Source: mergermarket

top DeALS & expeCteD DeALS

europe

Monthly M&A Insider 24

trenD grApHS

EuropEAn M&A quArtErly trEnD

0

100

200

300

400

500

Q4 11*

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q 09

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Valu

e (€

bn)

Total value Mid-market value

Num

ber of deals

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Total volume Mid-market volume

0

10

20

30

40

50

60

70

80

90

100

110

120

Q411*

Q3 11

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Buyout value Exit value Buyout volume Exit volume

Valu

e (€

bn)

Num

ber of deals

0

50

100

150

200

250

300

350

400

450

EuropEAn M&A AnnuAl trEnD EuropEAn M&A AnnuAl prIvAtE EquIty trEnD

0

200

400

600

800

1,000

1,200

YTD 2011*201020092008200720062005

Total value Mid-market value

Num

ber of deals

Valu

e (€

bn)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Total volume Mid-market volume

0

50

100

150

200

250

300

YTD 2011*201020092008200720062005

Valu

e (€

bn)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

200

400

600

800

1,000

1,200

1,400

1,600

EuropEAn M&A quArtErly prIvAtE EquIty trEnD

europe

Monthly M&A Insider 25

trenD grApHS

EuropEAn M&A GEoGrAphIc BrEAkDown ytD 2011

vALUe voLUme

UK

CEE

Iberia

France

Nordic

Germany

Benelux

Italy

Others

8.0%

5.3%

8.1%

17.6%

15.0%

10.8%

13.2%

11.5%10.5%

11.9%

9.2%

9.1%

5.7%20.0%

11.8%

12.7%

6.2%

13.4%

UK

CEE

Iberia

France

Nordic

Germany

Benelux

Italy

Others

EuropEAn M&A sEctor BrEAkDown ytD 2011

vALUe voLUme

5.7%

18.0%

10.2%

0.2%

16.1%

1.3%

9.1%

1.6%2.0% 2.4%

2.2%

3.4%

22.2%

5.5%

Industrials & Chemicals

Consumer

Business Services

Technology

Energy, Mining & Utilities

Financial Services

Pharma, Medical & Biotech

Construction

Leisure

Media

Transportation

Real Estate

Telecommunications

Agriculture

Defence

0.1% 1.3%

22.1%

1.0%

4.1%

1.3%

4.1%

6.0%

3.7%3.6%

0.2%

15.6%

14.0%7.9%

7.5%

7.5%

Industrials & Chemicals

Consumer

Business Services

Technology

Energy, Mining & Utilities

Financial Services

Pharma, Medical & Biotech

Construction

Leisure

Media

Transportation

Real Estate

Telecommunications

Agriculture

Defence

europe

Monthly M&A Insider 26

trenD grApHS

EuropEAn M&A DEAl sIZE BrEAkDown

vALUe voLUme

0

10

20

30

40

50

60

70

80

90

100

YTD 2011*201020092008200720062005

<€250m or undisclosed value

€251m-€500m

€501m-€2,000m

€2,001m-€5,000m

>€5,001m

15.1%

23.9%

10.1%

17.9%

33.0%

17.7%

23.2%

8.4%

15.7%

35.1%

16.4%

22.4%

8.3%

13.7%

39.2%

14.5%

19.9%

8.8%

16.6%

40.3%

20.3%

23.7%

9.0%

20.3% 17.1%

9.2%

29.8%

20.4%

26.7% 23.5%21.2%

22.0%

29.7%

10.3%

16.8%

Per

cent

age

88

90

92

94

96

98

100

YTD 2011*201020092008200720062005

3.3%

0.7%

3.9%

91.6%

3.8%

0.9%

3.5%

91.4%

4.0%

0.9%

3.9%

90.8%

2.7%

0.6%

3.2%

93.1%

2.0%

0.6%

2.2%

95.0%

93.1%

2.8%

3.3%

0.7% 0.7%

3.4%

3.0%

92.6%

0.5% 0.5% 0.3%0.4% 0.4% 0.2% 0.2%

<€250m or undisclosed value

€251m-€500m

€501m-€2,000m

€2,001m-€5,000m

>€5,001m

Per

cent

age

27

Mid

dle east &

africa

A mergermArket m&A report on

Monthly M&A Insider

Slow Month for MIddle eASt And AfrIcA

the totAl Amount of deAls in the middle eAst And AfricA region Amounted to us$950m for the month of october, representing A 71% decreAse in vAlue compAred to the month of september (us$3.3bn) And A 77% decreAse compAred to the sAme period lAst yeAr. this shows thAt the politicAl uncertAinty in the region hAs An importAnt impAct on m&A Activity And remAins A big chAllenge to growth.

the middle eAst & AfricA

energy, mining & utilities has been the dominant sector by far for ytd 2011, with 33.5% of the total m&A activity in value, accounting for us$10.4bn. this is mainly due to the large deals that occurred in this sector, including the acquisition of south Africa based multi-commodity mining company metorex ltd by Jinchuan group international resources co. ltd for us$1.4bn and tronix inc’s us$1.3bn purchase of namakwa. industrials & chemicals came in second position with a total of us$6.3bn worth of deals and 20.6% of the total deal value, when in 2010 the sector had only 4.8% of the total m&A activity in value.

with some countries in the region still suffering from political unrest, south Africa was the most popular target for investments in october, with six deals valued at a total of us$367m, representing 39% of total m&A value for the month. the prescient holdings tender offer by ptb group topped the m&A deals in the me&A region for the month of october.

Political uncertainty hampers negotiations october has been marked by the cancellations of several acquisitions announced earlier this year. saudi food processing company, the savola group, has decided to drop its plans to acquire Al-hokair’s stake in Al-Aziza panda united company, a deal valued at us$80m, citing that the two companies failed to reach an agreement within the timeframe. national metal manufacturing and casting company (maadaniyah), the saudi steel wire manufacturer, has also decided to stop negotiations to acquire gulf twisted steel co. and its sister company techno ceram middle east. the deal was valued at around sAr255.56m (us$68.1m). it seems that companies find it more and more difficult to reach a friendly agreement in a hectic political situation. however, despite the difficult environment, some investors are trying to look beyond the current uncertainty and focus on looking for untapped opportunities.

28

Mid

dle east &

africa

Monthly M&A Insider

top deAls

toP 10 MIddle eAStern & AfrIcAn Announced deAlS of the Month (oct-11) Announced Bidder company target company target dominated

sectorSeller company exit multiples (x) Bid premia

1-day before

deal value(uS$m)revenue eBItdA P/e

03-oct-11 pbt group prescient holdings financial services 201

20-oct-11 france telecom sA congo-china telecom sArl

tmt Zte corporation; and government of democratic republic of congo

196

03-oct-11 hikma pharmaceuticals plc

promopharm sA pharma, medical & biotech

3.5 11.9 57.4% 158

03-oct-11 shanduka group pty ltd western platinum ltd. (50.00% stake)

energy, mining & utilities

lonmin plc 139

18-oct-11 savola foods limited el-maleka food industries (78.00% stake); and Al-farasha (78.00% stake)

consumer 95

20-oct-11 Qafila for trade and distribution

b-tech for trading and distribution (90.77% stake)

consumer 0.3 16.2 25.1 2.5% 35

20-oct-11 fipar holding Jibal safilait sA (37.00% stake)

consumer 1.1 25

04-oct-11 heritage energy international, limited

sahara oil services holding limited (51.00% stake)

energy, mining & utilities

20

31-oct-11 magic software enterprises ltd

bluephoenix solutions ltd (Appbuilder business)

tmt bluephoenix solutions ltd.

17

06-oct-11 psagot ofek investment house ltd

davidoff pension management (50.00% stake)

financial services davidoff group n/a n/a 13

based on announced deals, including lapsed and withdrawn bids based on dominant geography of target being middle east or Africa data correct as of 07-nov-11

source: mergermarket

29

Mid

dle east &

africa

Monthly M&A Insider

trend grAphs

MIddle eAStern & AfrIcAn M&A quArterly trend

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Q411*

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q05

Q205

Q105

Valu

e (U

S$m

)

Total value Mid-market value

Num

ber of deals

0

20

40

60

80

100

120

140

160

Total volume Mid-market volume

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Q411*

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Q405

Q305

Q205

Q105

Buyout value Exit value Buyout volume Exit volume

Num

ber of dealsValu

e (U

S$m

)

0

5

10

15

20

25

MIddle eAStern & AfrIcAn M&A AnnuAl trend

MIddle eAStern & AfrIcAn M&A AnnuAl PrIvAte equIty trend

0

10

20

30

40

50

60

70

80

90

100

YTD 2011*201020092008200720062005

Total value Mid-market value

Valu

e (U

S$bn

)

Num

ber of deals

0

50

100

150

200

250

300

350

400

450

500

Total volume Mid-market volume

0

2

4

6

8

10

12

14

YTD 2011*201020092008200720062005

Buyout value Exit value Buyout volume Exit volume

Valu

e (U

S$bn

)

0

10

20

30

40

50

60

70

Num

ber of deals

MIddle eAStern & AfrIcAn M&A quArterly PrIvAte equIty trend

30

Mid

dle east &

africa

Monthly M&A Insider

41.7%4.8%

4.7%

2.6%

20.0%

7.2%

3.0%

2.2%

1.9%

2.2%2.6%

2.4%

South Africa

Israel

United Arab Emirates

Saudi Arabia

Egypt

Nigeria

Morocco

Kuwait

Ghana

Tunisia

Sudan

Zimbabwe

trend grAphs

MIddle eAStern & AfrIcAn M&A GeoGrAPhIc BreAKdown ytd 2011

MIddle eAStern & AfrIcAn M&A Sector BreAKdown ytd 2011

vAlue

vAlue

volume

volume

12.6%

0.2%0.3%

20.6%

13.5%

6.8%

5.1%

2.3%

0.6%

0.4%

4.2%

33.5%

Industrials & Chemicals

Consumer

Energy, Mining & Utilites

TMT

Financial Services

Business Services

Pharma, Medical & Biotech

Transportation

Construction

Real Estate

Leisure

Defence

2.1%

1.7%1.2%

2.5%

2.5%

2.9%

1.7%1.7%

1.7%

33.2%

6.2%

23.7%

5.8%

3.3%

South Africa

Israel

United Arab Emirates

Saudi Arabia

Egypt

Nigeria

Morocco

Kenya

Kuwait

Ghana

Jordan

Qatar

Namibia

Mozambique

2.8%2.8%

2.3% 0.9%0.5%

3.7%

13.8%

16.6%

18.0%

7.4%

8.3%

10.6%

12.4%

Industrials & Chemicals

Consumer

Energy, Mining & Utilites

TMT

Financial Services

Business Services

Pharma, Medical & Biotech

Transportation

Construction

Real Estate

Leisure

Defence

Agriculture

values <1% have not been shown values <1% have not been shown

31

Mid

dle east &

africa

Monthly M&A Insider

trend grAphs

MIddle eAStern & AfrIcAn M&A deAl SIZe BreAKdown

vAlue volume

0

10

20

30

40

50

60

70

80

90

100

YTD 2011*201020092008200720062005

12.1%

21.5%

54.8%

12.5%

12.8%

65.9%

13.3%

11.3%

67.2%

17.5%

19.0%

47.7%

19.2%

13.2%

53.2%

66.9%

11.6%

11.0%

11.6%

14.3%

10.3% 7.8% 7.3%14.1% 12.9% 9.3%

8.2%

13.0%

52.9%

1.3% 1.0% 0.9% 1.7% 1.6% 1.1%

<US$14.9m or undisclosed value

US$15m-US$100m

US$101m-US$250m

US$251m-US$500m

>US$501m

Per

cent

age

0

10

20

30

40

50

60

70

80

90

100

YTD 2011*201020092008200720062005

34.8%

10.7%

8.6%

5.6%

34.0%

14.2%

6.2%

9.2%

32.6%

15.4%

5.7%

7.2%

36.8%

11.2%

5.7%3.8%

32.2%

13.2%

4.1%3.4% 5.8%

5.1%

33.3%

11.2%10.4%

5.8%

40.3%36.4% 39.1% 42.5%

47.1% 44.6%48.5%

27.8%

7.5%

<US$14.9m or undisclosed value

US$15m-US$100m

US$101m-US$250m

US$251m-US$500m

>US$501m

Per

cent

age

Monthly M&A Insider 32

aBO

Ut M

err

ill cOr

POr

atiON

About merrill corporAtion

Merrill transaction and compliance Services through a broad range of tools and services, merrill corporation streamlines document composition, filing, printing, distribution and electronic access to the transaction and regulatory compliance activities of its clients engaged in securities offerings, reorganisations, mergers and acquisitions, sec and other regulatory filings. As a registered, third-party service provider offering public companies expert edgArization and Xbrl filing services, merrill professionals can compose, edit, electronically file, manage and distribute data in printed or electronic format.

Merrill legal Solutions provide both on-demand and on-site litigation support, information management and electronic and print document management services for law firms, corporate legal departments and professional services firms.

examples of our expertise include the creation of searchable litigation document repositories, management of electronic data discovery and the delivery of real-time court reporting and deposition videography services.

Merrill’s Marketing and communication Solutions supply brand identity management, customer communication and packaged direct marketing programs for sales professionals in industries such as real estate, mutual funds and insurance. examples of our services include customisable corporate identity materials, direct-mail marketing pieces and promotional programs supported by web-based technologies.

Merrill’s translations Services provide a range of translation options to help clients achieve the most efficient and cost effective approach to their translation projects. merrill brink offers extensive legal translation services for international litigation, intellectual property, patents, contractual matters, antitrust matters, mergers and acquisitions, arbitration and more.

www.datasite.com

About Merrill dataSite®

revolutionising the due diligence process

merrill datasite is designed for rapid deployment and can be up and running within two hours of a client’s need. our team can scan, upload and organise thousands of pages of content from any source in 24 hours or less. every aspect of the process, from document scanning to vdr hosting and project management is delivered by merrill’s multilingual team, available around the clock worldwide.

with merrill datasite, all documents are captured and indexed to an online database and because all rights are designated by the client, security and control are guaranteed. each user’s ability to view, print or access source documents is set up by the client administrator and can be changed at any time. merrill datasite provides useful tools, including full search, viewer audit capability, Q&A, bulk uploads and detailed user activity tracking that help clients maintain tighter control and have greater insight into reviewer behaviour.

Merrill dataSite® enhances transaction success

merrill datasite is the industry’s acknowledged leader. more than 61,000 different private and public companies across the globe have leveraged merrill datasite to increase the value of the following types of transactions:

• mergers, acquisitions and divestitures

• private placement transactions

• leveraged buyout transactions

• bankruptcy and reorganisation transactions

• financial restructuring transactions

• initial public offerings and dual-track processes

• Asset purchases and liquidations

• post-merger integration

founded in 1968 And heAdQuArtered in st. pAul, minnesotA, merrill corporAtion is A leAding provider of outsourced solutions for compleX business communicAtion And informAtion mAnAgement. merrill’s services include document And dAtA mAnAgement, litigAtion support, lAnguAge trAnslAtion services, fulfillment, imAging And printing. merrill serves the corporAte, legAl, finAnciAl services, insurAnce And reAl estAte mArkets. with more thAn 5,000 people in over 40 domestic And 22 internAtionAl locAtions, merrill empowers the communicAtions of the world’s leAding orgAnisAtions.

33Monthly M&A Insider

About merrill dAtAsite

Merrill dataSite – built with the client in mindmerrill datasite was created to meet its clients’ needs and built to their specifications. since 2002 we have consistently leveraged the experiences of our clients to add leading-edge functionality to the available toolset. merrill datasite allows its users and administrators to:

examine documents immediately. patented technology ensures you never have to wait for a document to be downloaded. because the data resides on merrill’s servers, you can simultaneously view an unlimited number of documents in multiple windows without having to close out or save to your “temp” file. when faced with hundreds of documents to review, this feature saves significant time and expense.

designate user permissions. team administrators can control which users will be able to view, print or download specific documents, folders or projects – simply and quickly.

Search every word in every document. with large document collections, sophisticated search features are key to finding critical information and accelerating the due diligence process. merrill datasite performs optical character recognition (ocr) on each and every letter in each and every document. our search capabilities allow users to search tens – if not hundreds – of thousands of pages to find what’s relevant to them. merrill datasite’s search capabilities ensure nothing is missed in any of the posted documents - regardless of where they may be organised within the index (e.g. find every instance of “contract” and “termination” within 5 words of each other, etc.). search results are returned much faster and are unlimited in terms of document results and hits within a document.

using wildcard, fuzzy, proximity, boosting, boolean and grouping modifiers, you can search and find exact matches and near-matches, including misspelled words. potential buyers will enjoy increased confidence knowing they’ve received and seen all materials and documents that are relevant to their decision-making.

Protect confidential information. ”view-only” documents are never downloaded. merrill datasite, not the computer’s browser, controls thecaching process providing unmatched security levels. unlike other vdrproviders, images are never viewable on the pc’s cache after the conclusion of a session.

track all activity accurately. Auditing and reporting tools provide a verifiable account of each individual’s time spent viewing both documents and specific pages – information that adds negotiating leverage.

need to work remotely?no problem. whether you’re working in beijing or new york, you can view your documents online without having to navigate through internal firewalls and email restrictions that often exist for outside company connections and which delay the due diligence process.

Security is our highest prioritymerrill has been a trusted provider of secure information to the financial and legal industries for more than 40 years. our employees execute letters of confidentiality and we are audited annually (internal and third-party) to make certain our it infrastructure and processes remain sound.

merrill datasite was the first virtual data room to receive the iso 27001 certification for its comprehensive information security management system (isms).

the iso 27001 standard, developed by the international organisation for standards to establish international requirements for information security and certification of isms, is designed to ensure effective protection of information assets in foreign markets, as well as across national and regional boundaries.

the best tool in the industrymerrill datasite technology allows for the fastest conversion of soft and hard copy documents to the electronic viewing platform. As a result, designated administrators are able to review documents the moment they are available.

through secure, simultaneous access, full text search capabilities and robust reporting tools, both archival and transactional due diligence processes are streamlined. As a result, merrill datasite gives you more insight and control, and dramatically reduces transaction time and costs.

As a leading provider of vdr solutions worldwide, merrill datasite has empowered nearly two million unique visitors to perform electronic due diligence on thousands of transactions totalling trillions of dollars in asset value.

now SMArter, fASter, eASIer!

PleASe vISIt our weBSIte: www.dAtASIte.coM

aBO

Ut M

err

ill datasite

ABOUT MERRILL CORPORATION

EXECUTIVE MANAGEMENT

Ed Bifulk

President Tel: +1 212 229 6563

Paul Hartzell Senior Vice President

Tel: +1 212 367 5950

EXECUTIVE SALES

Chris Beckmann

Regional Director, Europe Tel: +49 69 25617 110

Alex Gross

Regional Director, Europe Tel: +49 69 7593 7148

Michael Hinchliffe

Regional Director, Europe Tel: +44 20 7422 6100

Jonathan Hughes

Account Manager, Northern Europe Tel: +44 20 7422 6100

Shashank Jain

Representative, United Arab Emirates Tel: +52 55 9171 2237

Alvaro Ortega

Regional Director, Europe Tel: +44 20 7422 6100

Merlin J. Piscitelli

Regional Director, Europe Tel: +44 20 7422 6100

Jérôme Pottier

Regional Director, France Tel: +33 (0) 1 40 06 13 12

Colin Schopbach

Regional Director, Europe Tel: +44 20 7422 6100

Anna Scott

Regional Director, Europe Tel: +44 20 7422 6100

Hakema El-Hadad

Regional Director, Northern Africa Tel: +33 (0) 1 40 06 13 10

Mark Finnie

Regional Director, Hong Kong

Tel: +852 2536 2534

Ari Lee

Regional Director, Asia-Pacific Tel: +852 9855 3758

Vincent Lork

Regional Director, South Asia Tel: +65 6248 4602

Chris Robilliard

Regional Director, Australia & New Zealand

Tel: +612 8667 3064

Manuel Bentosinos

Regional Director, Mexico Tel: +52 55 9171 2237

Ana Paula Macêd Távora de Castro

Regional Director, South America Tel: +55 11 9908 0858

Felipe Cunha

Regional Director, Brazil Tel: +55 11 3568 2429

Carlos Nogueira

Diretor Regional, Brazil Tel: +55 11 3895 8572

Will Brown

Regional Director, Canada Tel: +1 514 877 5177

Hank Gregory

SVP, Western Canada & US Tel: + 604 603 4360

Ryan MacMillan

Regional Director, Canada Tel: +1 416 214 2448

Michael Kennedy

Regional Director, Boston Tel: +1 207 829 4369

Ross Whittaker

Regional Director, New England Tel: +1 617 535 1516

Forrest R. Doane

Regional Director, New York Tel: +1 917 934 7341

Adam Kuritzky

Regional Director, New York Tel: +1 917 934 7340

Shelle Martin

Regional Director, New York Tel: +1 212 229 6613

John McElrone

Regional Director, New York Tel: +1 212 229 6656

Matthew Mezzancello

Regional Director, New York Tel: +1 917 934 7346

Steve Piccone

Vice President, New York Tel: +1 212 229 6883

William Polese

Regional Director, New York Tel: +1 212 229 6612

Paul Kleinkauf

Regional Director, Southeast Tel: +1 404 602 3251

Scott Haugen

Regional Director, Minnesota Tel: +1 651 632 4375

Anthony Crosby

Regional Director, Chicago Tel: +1 312 674 6511

Mark Plaehn

Regional Director, Chicago Tel: +1 312 674 6527

Brian Gilbreath

Regional Director, Omaha Tel: +1 404 934 8085

Nicholas Renter

Regional Director, Dallas Tel: +1 214 754 2100

Andrew Buonincontro

Regional Director, Palo Alto Tel: +1 650 493 1400

Erik Sandie

Regional Director, Palo Alto Tel: +1 650 493 1400

Dan Phelan

Regional Director, Los Angeles Tel: +1 213 253 2139

Jay Loyola

Regional Director, Irvine Tel: +1 949 622 0663

Hans Schumann Regional Director, San Diego Tel: +1 760 635 0830

David Yeary

VP, DataSite Life Sciences Tel: +1 415 307 4414

James Snaza

Director, Life Sciences Tel: +1 651 632 4585

AB

OU

T M

ER

RIL

L C

OR

PO

RA

TIO

N

34Monthly M&A Insider

www.mergermarket.comremark, part of the mergermarket group

80 StrandLondon, WC2R 0RLUnited Kingdom

t: +44 (0)20 7059 6100f: +44 (0)20 7059 [email protected]

11 West 19th Street, 2nd fl.New York, NY 10011USA

t: +1 212 686-5606f: +1 212 [email protected]

Suite 2401-3Grand Millennium Plaza181 Queen’s Road, CentralHong Kong

t: +852 2158 9700f: +852 2158 [email protected]

disclaimer