A Market Analysis of the Bitcoin Economy - Finance 2.0 Market Analysis of the Bitcoin Economy Paolo...

28

A Market Analysis of the Bitcoin Economy Paolo Tasca Deutsche Bundesbank, 1 ECUREX Research Zurich :: Finance 2.0 | CRYPTO 2015 September 23, 2015 1 The statements reflect the personal views of the speaker and do not necessarily coincide with the position of the Deutsche Bundesbank. Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 1 / 28

Transcript of A Market Analysis of the Bitcoin Economy - Finance 2.0 Market Analysis of the Bitcoin Economy Paolo...

A Market Analysis of the Bitcoin Economy

Paolo Tasca

Deutsche Bundesbank,1 ECUREX Research

Zurich :: Finance 2.0 | CRYPTO 2015

September 23, 2015

1The statements reflect the personal views of the speaker and do not necessarilycoincide with the position of the Deutsche Bundesbank.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 1 / 28

1 Bitcoin as Payment Network

2 Bitcoin as Currency

3 Groups of Interest. Investors

4 Distribution of Income and Wealth

5 Take-home Message

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 2 / 28

https://ecurex.com/2015report

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 3 / 28

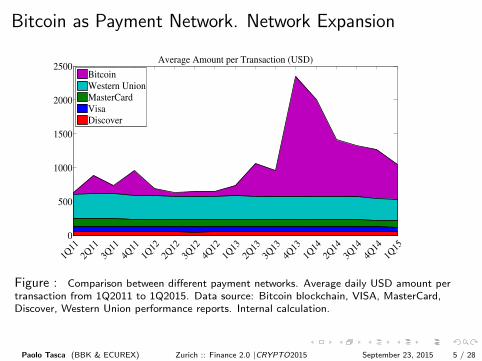

Bitcoin as Payment Network. Network Expansion

The average amount transferred per Bitcoin transaction is larger thanin any other major payment network.

During the period 2011–2015, the average amount (in USD equivalent) pertransaction constantly increased, and remained larger than in the majorpayment networks such as Visa, Mastercard, Discover, or Western Union.

The Bitcoin network is mostly used to remit money from user to user.2

2Studies show that the amount migrants send per transaction typically rangesbetween USD 100 and USD 1,000 for international remittances (e.g., Sander C., 2003);Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 4 / 28

Bitcoin as Payment Network. Network Expansion

0

500

1000

1500

2000

2500

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

Average Amount per Transaction (USD)

Bitcoin

Western Union

MasterCard

Visa

Discover

Figure : Comparison between different payment networks. Average daily USD amount pertransaction from 1Q2011 to 1Q2015. Data source: Bitcoin blockchain, VISA, MasterCard,Discover, Western Union performance reports. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 5 / 28

Bitcoin as Currency. Network Expansion

The relative capitalisation of Bitcoin with regard to other digitalcurrencies is receding in favour of Ripples.

Until mid-2014, Bitcoin dominated the digital currency market bycovering up to 95% of its total volume.

Since the 2nd part of 2014, the Bitcoin dominant position has beeneroded by Ripple, which now covers about 10% of the total marketcapitalisation.

Even though Bitcoin remains dominant on the digital currencymarket, the relative currency strength of Bitcoin has decreased – onaverage –, compared to that of the other (almost) existing 500 digitalcurrencies.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 6 / 28

Bitcoin as Currency. Network Expansion

01/11 07/11 01/12 07/12 01/13 07/13 01/14 07/14 01/15 07/15

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Relative Market Cap

% Dogecoin

% Dash

% Litecoin

% Ripple

% Bitcoin

Figure : Relative market capitalisation of Bitcoin, Ripple, Litecoin, Dash, Dogecoin. Datasource : Coinmarketcap. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 7 / 28

Bitcoin as Currency. Currency Competition

01/14 04/14 07/14 10/14 01/15 04/15 07/150

50

100

150

200

250

300

350

400Relative Currency Strength

BTCX

LTCX

XRPX

Figure : Comparison between relative index strengths. Ba= 100 on 01.01.2014 (BTCX, LTCX,XRPX). Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 8 / 28

Bitcoin as Currency. Currency CompetitionBTCX: rel. strength of BTC wrt LTC and XRP, weighted by: (1) their respective rel.market cap. expressed in USD; (2) the inverse of the BTC exchange rate volatility.

LTCX: rel. strength of LTC wrt both BTC and XRP, weighted by: (1) their respective rel.market cap. expressed in USD; (2) the inverse of the LTC exchange rate volatility.

XRP: rel. strength of XRP wrt both BTC and LTC, weighted by: (1) their respective rel.market cap. expressed in USD; (2) the inverse of the XRP exchange rate volatility.

Currency competition expressed in currency strength indices

BTCX := ∆BTC × Exp

{Log

[BTC/LTC

σ (BTC/LTC)

](WBTC ) + Log

[BTC/XRP

σ (BTC/XRP)

](1−WBTC )

}LTCX := ∆LTC × Exp

{Log

[LTC/BTC

σ (LTC/BTC)

](WLTC ) + Log

[LTC/XRP

σ (LTC/XRP)

](1−WLTC )

}XRPX := ∆XRP × Exp

{Log

[XRP/BTC

σ (XRP/BTC)

](WXRP) + Log

[XRP/LTC

σ (XRP/LTC)

](1−WXRP)

}where:

WBTC =

(ωLTC

ωLTC + ωXRP

);WLTC =

(ωBTC

ωBTC + ωXRP

);WXRP =

(ωBTC

ωBTC + ωLTC

);

∆BTC , ∆LTC and ∆XRP are normalisation factors;

ωBTC , ωLTC , ωXRP : market capitalisation of BTC, LTC and XRP expressed in USD.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 9 / 28

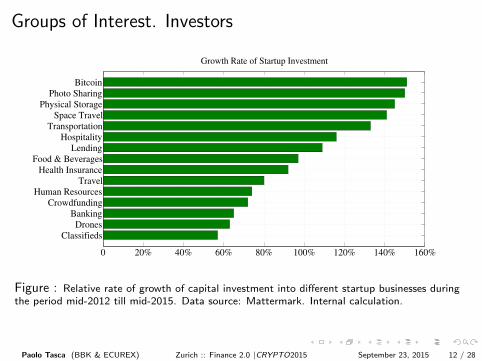

Groups of Interest. Investors

Bitcoin startups raised almost USD 1 billion in three years with anannual investment growth rate of about 150%

Capital investments in Bitcoin-related startups is a recent trend thatstarted in 1Q 2012.

Since 1Q 2012, the Bitcoin industry represents the fastest growingsector for capital investment.

Within the Bitcoin sector, the Mining and Payment & Remittanceindustries drove the funding race.

21 Inc alone covered over half of the capital raised by the Miningindustry and Coinbase one third of the capital raised by the wholePayment & Remittance industry.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 10 / 28

Groups of Interest. Investors

0 1% 2% 3% 4% 5% 6% 7%

Classifieds

Drones

Banking

Crowdfunding

Human Resources

Travel

Health Insurance

Food & Beverages

Lending

Hospitality

Transportation

Space Travel

Physical Storage

Photo Sharing

Bitcoin

Relative Share of Dollars Raised

Figure : Relative Capital investment into different startup businesses during the periodmid-2012 till mid-2015. Data source: Mattermark. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 11 / 28

Groups of Interest. Investors

0 20% 40% 60% 80% 100% 120% 140% 160%

Classifieds

Drones

Banking

Crowdfunding

Human Resources

Travel

Health Insurance

Food & Beverages

Lending

Hospitality

Transportation

Space Travel

Physical Storage

Photo Sharing

Bitcoin

Growth Rate of Startup Investment

Figure : Relative rate of growth of capital investment into different startup businesses duringthe period mid-2012 till mid-2015. Data source: Mattermark. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 12 / 28

Groups of Interest. Investors

Capital Market Payment and Financial Blockchain Mining MiscellaneousRemittance Services Application Industry

Exchange Payment Accounting Smart Contracts Mining Solutions Bitcoin FaucetDerivatives Remittance Security Blockchain API Mining Pool TippingCommodity Wallet ATM MessagingInstitutional Trading Market andCrowdfunding and Data AnalysisCrypto Equity

Table : Classification of business categories in the Bitcoin industry.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 13 / 28

Groups of Interest. Investors

0

5

10

15

20

25

30

35

2012

Q1

2012

Q2

2012

Q3

2013

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

Number of Deals

Payment & Remittances

Mining Industry

Capital Market

Blockchain Application

Financial Service

Miscellaneous

0

50

100

150

200

250

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

(mil

lio

n U

SD

)

Quarterly Funding Amount for Bitcoin Startups

Payment & Remittances

Mining Industry

Capital Market

Blockchain Application

Financial Service

Miscellaneous

Figure : Left: Quarterly number of deals for startups in different Bitcoin industries. Right:Quarterly funding amount for startups in different Bitcoin industries. Data source: Bitangel,Cbinsight, Coinfilter, Coindesk, Crunchbase. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 14 / 28

Groups of Interest. Investors

0

20

40

60

80

<0.1

mill

ion

0.1−

0.5

mill

ion

0.5−

1 m

illio

n

1−10

mill

ion

>10 m

illio

n

Number of Deals in Each Funding Scale (2012−2015)

Num

ber

of

Deals

Miscellaneous

Blockchain Application

Mining Industry

Financial Service

Capital Market

Payment & Remittances

Figure : Number of deals in each funding scale (Q1/2012 to Q1/2015). Deals in each fundingscale are further divided into business categories. Data source: Bitangel, Cbinsight, Coinfilter,Coindesk, Crunchbase. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 15 / 28

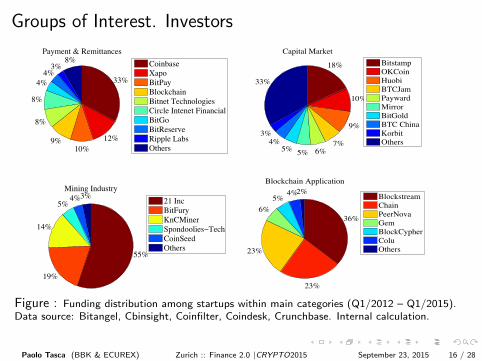

Groups of Interest. Investors

8%3%

4%4%

8%

8%

9%10%

12%

33%

Payment & Remittances

CoinbaseXapoBitPayBlockchainBitnet TechnologiesCircle Intenet FinancialBitGoBitReserveRipple LabsOthers

33%

3%4%

5% 5% 6%7%

9%

10%

18%

Capital Market

BitstampOKCoinHuobiBTCJamPaywardMirrorBitGoldBTC ChinaKorbitOthers

3%4%5%

14%

19%

55%

Mining Industry

21 IncBitFuryKnCMinerSpondoolies−TechCoinSeedOthers

2%4%5%

6%

23%

23%

36%

Blockchain Application

BlockstreamChainPeerNovaGemBlockCypherColuOthers

8%3%

4%4%

8%

8%

9%10%

12%

33%

Payment & Remittances

CoinbaseXapoBitPayBlockchainBitnet TechnologiesCircle Intenet FinancialBitGoBitReserveRipple LabsOthers

33%

3%4%

5% 5% 6%7%

9%

10%

18%

Capital Market

BitstampOKCoinHuobiBTCJamPaywardMirrorBitGoldBTC ChinaKorbitOthers

3%4%5%

14%

19%

55%

Mining Industry

21 IncBitFuryKnCMinerSpondoolies−TechCoinSeedOthers

2%4%5%

6%

23%

23%

36%

Blockchain Application

BlockstreamChainPeerNovaGemBlockCypherColuOthers

Figure : Funding distribution among startups within main categories (Q1/2012 – Q1/2015).Data source: Bitangel, Cbinsight, Coinfilter, Coindesk, Crunchbase. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 16 / 28

Distribution of Income and Wealth.

The wealth distribution in the Bitcoin ecosystem is highlyunequal,and this inequality is growing.

The inequality of the distribution of Bitcoins amongst addresses,summarised by the Gini coefficient grew from 0.09 in 2010 to 0.99in 2015.

During the period 20092015, the top 100 richest addresses kept aconstant relative wealth, totalling about 20% of the total value ofthe Bitcoin economy.

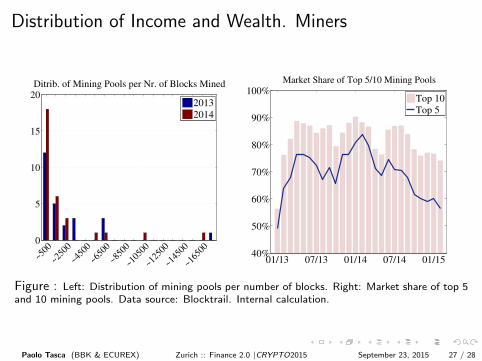

The Bitcoin mining market is under control by 5 to 7 major miningpools.

During the period 2013-2015, the cumulative market share of thelargest 10 pools relative to the total market hovered in the 70% –80% range.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 17 / 28

Distribution of Income and Wealth. Users

! !

Figure : Lorenz Curve and Gini Coefficient for the Bitcoin Economy. Percentile of addressessorted by wealth wrt to the percentile of the wealth own.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 18 / 28

Distribution of Income and Wealth. Users

! !

Figure : Lorenz Curve and Gini Coefficient for the Bitcoin Economy. Percentile of addressessorted by wealth wrt to the percentile of the wealth own.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 19 / 28

Distribution of Income and Wealth. Users

! !

Figure : Lorenz Curve and Gini Coefficient for the Bitcoin Economy. Percentile of addressessorted by wealth wrt to the percentile of the wealth own.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 20 / 28

Distribution of Income and Wealth. Users

The Gini coefficient (G) is an inequality index of income or wealth.3

G can be calculated from unordered size data as half of the Relative MeanDifference (RMD), which is the average absolute difference between everypossible pair of values, divided by the mean size µ,

G =RMD

2with : RMD =

MD

µ,MD =

1

n2

n∑i=1

n∑j=1

|xi − xj |

G=0: every person receives the same income;

G=1: theoretical value for n→∞ where a single person receives100% of the total income and the remaining people receive none

xi : income or wealth of person i .

n: population size.

3Gini C., Variabilita’ e mutabilita’, 1912, reprinted in Memorie di metodologica statistica(Ed. Pizetti E, Salvemini, T). Rome: Libreria Eredi Virgilio Veschi 1955.Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 21 / 28

Distribution of Income and Wealth. UsersThe Lorenz curve can be represented by a function L(F ) where:

F is the cumulative portion of the population represented by thehorizontal axis;

L is the cumulative portion of the total wealth or income representedby the vertical axis.

For a discrete probability function f (y), let yi , i = 1, .., n, be the pointswith non-zero probabilities indexed in increasing order (yi < yi+1). TheLorenz curve is the continuous piecewise linear function connecting thepoints (Fi , Li ), i = 0, ..., n, where F0 = 0, L0 = 0, and for i = 1, ..., n:

Fi =i∑

j=1

f (yj)

Li =SiSn

with Si =i∑

j=1

f (yj)yj

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 22 / 28

Distribution of Income and Wealth. Users

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

01.09 04.10 12.10 10.11 09.12 08.13 05.14 03.15

Percent of Bitcoins Owned by Richest Addresses

Top 500Top 100

1 2 3 4 5 10 50 100 1500

50

100

150

200

250

300

Magnitude (thousand Bitcoin)

Fre

quency

Wealth Distribution of Top 500 Richest Addresses

2010

2011

2012

2013

2014

Figure : Left: Relative wealth of the top 100 and 500 richest Bitcoin addresses. Right: Wealthdistribution among the top 500 richest Bitcoin addresses (with x-axis log-transformed). Datasource: Bitcoin blockchain. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 23 / 28

Distribution of Income and Wealth. Users

100BTC 1000BTC 10000BTC 100000BTC

101

102

103

104

105

Fre

quen

cy

Income Distribution for All Clusters (bin size: 100BTC)

Power Law Function:

y = (2.0133e+05) * x−1.2038

MSE: 1794790.7437

R2: 0.89329

Figure : Income distribution for all clusters. Data source: Bitcoin Core parsed from the 3rd ofJanuary 2009 until the 8th of May 2015. Total nr. addresses: 75,191,953. Total nr. clusters(contains at least addresses): 30,708,660 (9,847,999 ≥ 2 nodes) and 4,810,342 with non-zerobalance. Total TXs between clusters: 88,950,021. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 24 / 28

Distribution of Income and Wealth. MinersGhash.IO hashing power was close to “51% attack” for several times.

01/13 05/13 09/13 12/13 04/14 08/14 12/14

20%

40%

60%

80%

100%Distribution of Transaction Fee in Each Diffeculty Level

Unknown

Others

BTCChina Pool

P2Pool.org

DeepBit

Ozcoin

CloudHashing

KNCMiner

Bitfury

AntPool

EclipseMC

ASICMiner

BitMinter

50BTC

Slush

Eligius

DiscusFish / F2Pool

BTC Guild

GHash.IO

Figure : Top 17 mining pools (out of 40) per relative amount of fees earned. In each difficultylevel, transaction fees collected by each mining pool are summed up and compared to the totalfees earned and collected by the market. Period: From January 2013 to February 2015. Datasource: Blocktrail. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 25 / 28

Distribution of Income and Wealth. Miners

01/13 05/13 09/13 12/13 04/14 08/14 12/140

500

1000

1500

20002

01

6 B

lock

s in

Each

Dif

ficu

lty

Lev

el

Mining Market Share among Countries (by number of blocks)

Unknown

USA

Global

Europe

China

Figure : Top mining activity per country. Mining pools are classified per country of operation.Many mining pools operate in different countries (e.g, BTC Guild and BitMinter run theirmining operation in both USA and Europe), so they are classified as “Global”. Period: fromJanuary 2013 to February 2015. Data source: Blocktrail, Bitcoin Wiki (comparison of miningpools). Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 26 / 28

Distribution of Income and Wealth. Miners

0

5

10

15

20

~500

~4500

~6500

~8500

~1050

0

~1250

0

~1450

0

~1650

0

Ditrib. of Mining Pools per Nr. of Blocks Mined

~2500

2013

2014

01/13 07/13 01/14 07/14 01/1540%

50%

60%

70%

80%

90%

100%Market Share of Top 5/10 Mining Pools

Top 10

Top 5

Figure : Left: Distribution of mining pools per number of blocks. Right: Market share of top 5and 10 mining pools. Data source: Blocktrail. Internal calculation.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 27 / 28

Take-Home Message

1 The average amount transferred per Bitcoin transaction is larger than in any other majorpayment network.

2 The relative capitalisation of Bitcoin with regard to other digital currencies is receding infavour of Ripple’s.

3 China is the largest country in the world per: (1) number of active Bitcoin clients; (2)mining capacity; (3) volume of Bitcoins exchanged via electronic trading platforms.

4 Bitcoin startups raised almost USD 1 billion in three years with an annual investmentgrowth rate of about 150%.

5 In Jan. 2015 the Bitcoin volume exchanged on electronic trading platforms reached 50%of the total number of Bitcoins ever mined at that time.

6 During the year 2014, the transaction costs in digital currencies dropped significantly.

7 The year 2014 saw fewer incidences and less arbitrage opportunities than the previousyears. In effect, the digital currency market is becoming more efficient.

8 The wealth distribution in the Bitcoin ecosystem is highly unequal, and this inequality isgrowing.

9 The Mining industry is consolidating as an oligopoly.

Paolo Tasca (BBK & ECUREX) Zurich :: Finance 2.0 |CRYPTO2015 September 23, 2015 28 / 28

![CryptoNote v 2.0 from3.5%creditcardfeestoessentially0 ... › whitepaper_annotated.pdf · CryptoNote v 2.0 Nicolas van Saberhagen October 17, 2013 1 Introduction \Bitcoin" [1] has](https://static.fdocuments.in/doc/165x107/5f1ef555ba0d79177447d92e/cryptonote-v-20-from35creditcardfeestoessentially0-a-whitepaperannotatedpdf.jpg)