A IAUDIT OFFICE - World Bank

14

$ 1MONGOLIAN NATIONAL A I IAUDIT OFFICE 4DcW01 Il FINANCIAL AUDITING REPORT The Financial and Auditing Statement for December 31, 2014 of "Institutional strengthening for Donor Assistance Management" Project Code of auditing: YAF-CAr/2015/07/CTA-TX I June 2015 Ulaanbaatar city Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of A IAUDIT OFFICE - World Bank

$ 1MONGOLIAN NATIONALA

I IAUDIT OFFICE4DcW01 Il

FINANCIAL AUDITING REPORT

The Financial and Auditing Statement for December 31, 2014 of"Institutional strengthening for Donor Assistance Management" Project

Code of auditing: YAF-CAr/2015/07/CTA-TX

I

June 2015

Ulaanbaatar city

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

AV M .G ,

a4jj o NATIONAL.

AUDIT OFFICE

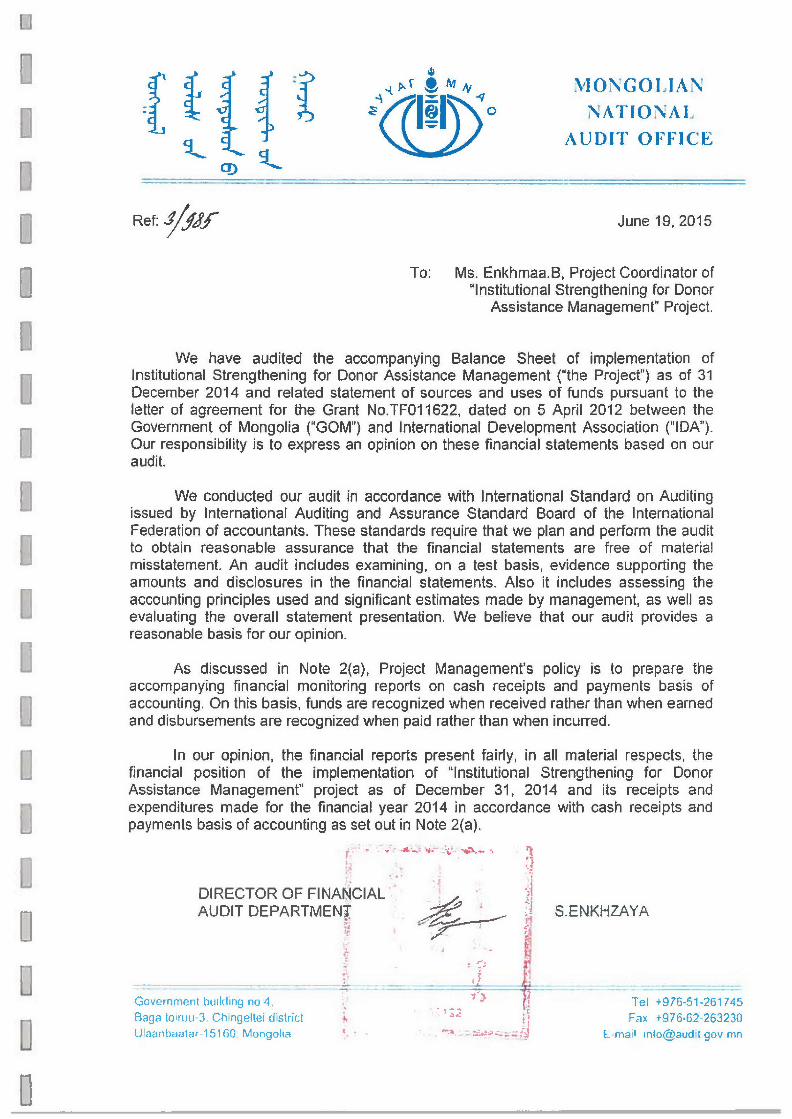

RefJfff June 19, 2015

To: Ms. Enkhmaa.B, Project Coordinator of"Institutional Strengthening for Donor

Assistance Management" Project.

We have audited the accompanying Balance Sheet of implementation ofInstitutional Strengthening for Donor Assistance Management ("the Project") as of 31December 2014 and related statement of sources and uses of funds pursuant to theletter of agreement for the Grant No.TF01 1622, dated on 5 April 2012 between theGovernment of Mongolia ("GOM") and International Development Association ("IDA").Our responsibility is to express an opinion on these financial statements based on ouraudit.

We conducted our audit in accordance with international Standard on Auditingissued by International Auditing and Assurance Standard Board of the InternationalFederation of accountants. These standards require that we plan and perform the auditto obtain reasonable assurance that the financial statements are free of materialmisstatement. An audit includes examining, on a test basis, evidence supporting theamounts and disclosures in the financial statements. Also it includes assessing theaccounting principles used and significant estimates made by management, as well asevaluating the overall statement presentation. We believe that our audit provides areasonable basis for our opinion.

As discussed in Note 2(a), Project Management's policy is to prepare theaccompanying financial monitoring reports on cash receipts and payments basis ofaccounting. On this basis, funds are recognized when received rather than when earnedand disbursements are recognized when paid rather than when incurred.

In our opinion, the financial reports present fairly, in all material respects, thefinancial position of the implementation of "Institutional Strengthening for DonorAssistance Management" project as of December 31, 2014 and its receipts andexpenditures made for the financial year 2014 in accordance with cash receipts andpayments basis of accounting as set out in Note 2(a).

DIRECTOR OF FINANCIALAUDIT DEPARTMENT SENKHZAYA

Gn gTel +976-51-261745Fax +976-62 263230

Ubr6 nE ma! inlo@aud t gov mn

-L SM 4'MONGOLIAN

ic 0 NATIONALa AUDIT OFFICE

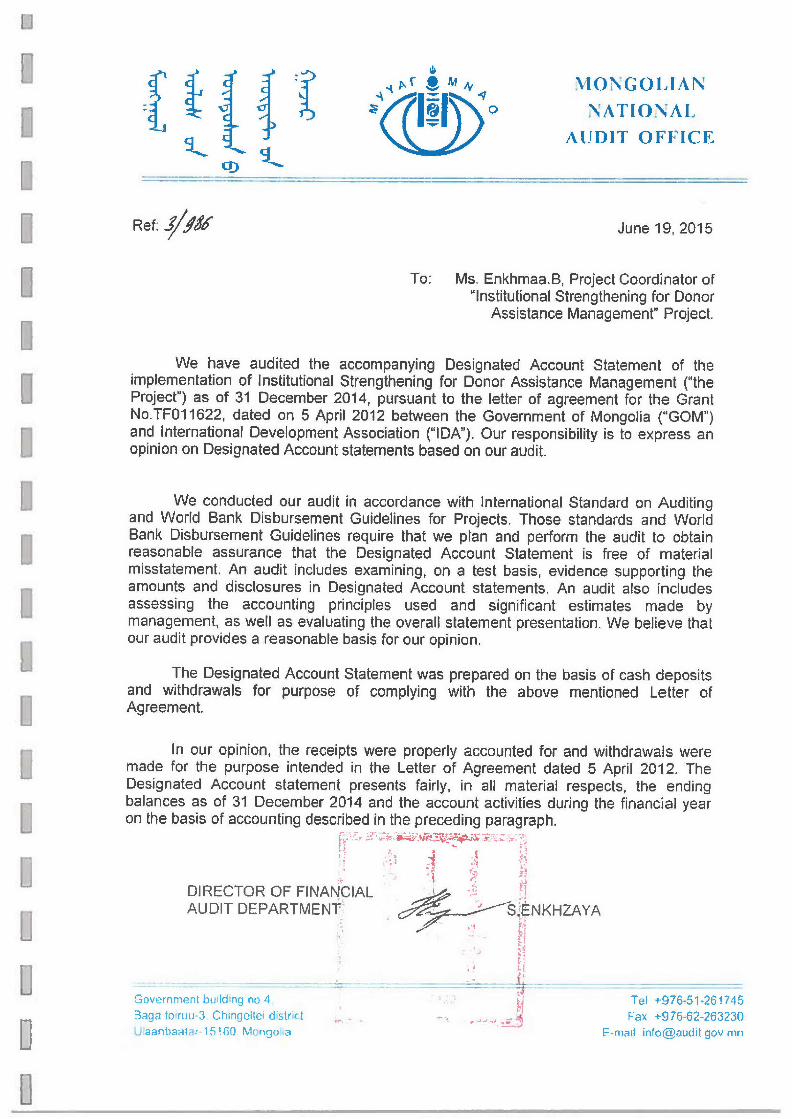

F Ref:.- f June 19, 2015

To: Ms. Enkhmaa.B, Project Coordinator of"Institutional Strengthening for Donor

Assistance Management" Project.

We have audited the accompanying Designated Account Statement of theimplementation of Institutional Strengthening for Donor Assistance Management ("theProject") as of 31 December 2014, pursuant to the letter of agreement for the GrantNo.TF01 1622, dated on 5 April 2012 between the Government of Mongolia ("GOM")and International Development Association ("IDA"). Our responsibility is to express anopinion on Designated Account statements based on our audit.

We conducted our audit in accordance with International Standard on Auditingand World Bank Disbursement Guidelines for Projects. Those standards and WorldBank Disbursement Guidelines require that we plan and perform the audit to obtainreasonable assurance that the Designated Account Statement is free of materialmisstatement. An audit includes examining, on a test basis, evidence supporting theamounts and disclosures in Designated Account statements. An audit also includesassessing the accounting principles used and significant estimates made bymanagement, as well as evaluating the overall statement presentation. We believe thatour audit provides a reasonable basis for our opinion.

The Designated Account Statement was prepared on the basis of cash depositsand withdrawals for purpose of complying with the above mentioned Letter ofAgreement.

In our opinion, the receipts were properly accounted for and withdrawals weremade for the purpose intended in the Letter of Agreement dated 5 April 2012. TheDesignated Account statement presents fairly, in all material respects, the endingbalances as of 31 December 2014 and the account activities during the financial yearon the basis of accounting described in the preceding paragraph.

DIRECTOR OF FINANCIALAUDIT DEPARTMENT ,SNKHZAYA

Un gTel +976-51-261745

Fax +976-62-263230E-mail info@audit gov mn

/V MONGOLIAN

SO NATIONALAUDIT OFFICE

Ref- S fA June 19, 2015

To: Ms. Enkhmaa.B, Project Coordinator of"Institutional Strengthening for Donor

Assistance Management" Project.

In addition to our audit of the project financial reports, we have audited thestatements of expenditures submitted to the IDA during the financial year 2014 insupport of applications for replenishment and direct payments under the letter ofAgreement for Institutional Strengthening for Donor Assistance Management GrantNo.TF011622 dated 5 April 2012.

The management of the project is responsible for the preparation of thestatements of expenditures. Our responsibility is to express an opinion on thestatements of expenditures, on the basis of our audit.

We conducted our audit in accordance with generally accepted auditing standardthat accordingly included examination, on a test basis, evidence supporting the amountsand disclosures in the statements of expenditures. An audit also includes assessment ofthe accounting principles used and significant estimates made by management, as wellas evaluating the overall statement presentation. We believe that our audit provides areasonable basis for our opinion.

In our opinion, the statements of expenditures submitted together with theinternal controls and procedures involved in their preparation can be relied upon tosupport the application for grant disbursements for the financial year 2014.

DIRECTOR OF FINANCIALAUDIT DEPARTMENT S.ENKHZAYA

Li

G r n udn no4 Tel +976-51-261745a u - hn Fax +976-62-263230

U ar 156 o F-mail mfo@audit gov mn

I

U

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

o ANNUAL FINANCIAL REPORT

Institutional Strengthening for Donor Assistance ManagementGrant No.TF01 1622

AUDITOR'S REPORT

If you need more information, pleaseContact us with the following address: CONTENT PAGES

Director of Department: Enkhzaya.S Foreword 2

Phone: 263533 Financial International Control 2

Audit-manager: Ts.Oidov Auditing opinion 2

Phone: 260512 Financial Reports

Analyst: N.Nyamdavaa Project Balance sheet 6

Phone: 261885 Statement of Sources and Uses of funds 7

Summary of Withdrawal Applications 7

Designated Account Statement 8

Notes to the Financial Monitoring Reports 9

IMongolian National Audit Office

Address: Government Building IV,

BagalToiruu-3

Chingeltei district, 15160

Ulaanbaatar, Mongolia

Web-site: www.audit.mn

May-2015

1

Il

LI

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

FOREWORD

We introduce to the World Bank and the Project Management the Auditor's Report on financialstatements of "Institutional Strengthening for Donor Assistance Management" as of DecemberB 31, 2014 accordance with the agreement of the GRANT NUMBER TF01 1622, which was signedbetween Mongolian Government and International Development Association on April 5th, 2012.

FINANCIAL INTERNAL CONTROL

We have audited the Financial Report to obtain reasonable assurance, free from materialmisstatements.During the course of audit, we assessed the financial risks by considering the ProjectManagement Internal Control System and implemented by comparing to our information oncontrol.

I THE MAIN FINDINGS AND SOLUTIONS

An audit involved the performing procedures to obtain evidence about disclosures in the financialstatements and financial instruments. We are confident with auditing conducted by us willprovide sufficient information and reliable justification for opinion and conclusion to financialstatements due to the inspection of the project as of December 31, 2014, annual year's FinancialTransaction Records, designated account expenditures which are spent compliance by theagreement of the grant and whether the expenditure per Project Activity is under the qualifiedInternal Control.

Thus, the following are the designated account.

1. The funds were used to the Project Activities according to the purpose.

2. In order to fund the all costs under the Grant, Transactions were transferred from theDesignated Account.

3. All those Designated Account Receipts are shown the Implementation of the Projectcorrectly and fairly.

4. Ten (10%) percent of personal income tax of 2.2 thousand US dollars were subtractedfrom international consultant remuneration in fiscal year 2014. But these amount of taxhave not been paid yet.

An Audit involved the designated account, relevant documents, procedures to prepare the reportand Internal control system; the relevant disbursements of the Grants are included in thesestatements according to the Agreement.

We confirm that the designated account is shown the annual year's Implementation of theProject correctly and fairly based on the explanatory notes involved in the audit and theprocedures of the Audit.

AUDITOR'S OPINION

In our opinion, the Financial Statements of the "Institutional Strengthening for Donor AssistanceManagement" which is funded by the World Bank and comprised balance Sheet, summary ofsources and uses of funds, designed account statement of December 31, 2014, was representedfairly and prepared in accordance with International Financial Reporting Standards.

2

U

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

BALANCE SHEETAS AT DECEMBER 31, 2014

1213112013 12131/2014Notes (USD) (USDI

ASSETS

Cash and cash equivalents 5 53,924.27 59,813,26U Cumulative project expenditures 6 91,680.76 163h678.66

I TOTAL ASSETS 145,605.03 223,491.92

FUNDS

IDA Funds 7 145,239.67 222,828.90Net Interests Earned 8 367.29 664.95Foreign Exchange Difference (1,93) (1,93)

TOTAL FUNDS 145,605.03 223,491.92

I

I

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

SUMMARY OF SOURCES AND USES OF FUNDSAs of December 31, 2014

Cumulative Cumulative

Note as at as at31.12.2013 31.12.2014

IUSD) (USD)Sources of Funds

IDA Funds 7 145,239.67 222,828.90

Interest Earnings 8 408.90 714.75Other revenue 29.19

Total sources of Funds 146,648.57 223,572.84

Goods 6,309.65

Consultants' Services 6a 43,164.46 107,452.60Training and Workshops 48,516.30 48,51630

Bank Service Charge 8 41.61 78.99

Foreign exchange rate difference 1.93 1.93Financial audit fee 1400.11

Total uses of Funds 91,724.30 163,759.58

Excess of sources over uses offunds 53,924.27 59,813.26

Cash balances at 31 Dec 2014 53,924.27 59,813.26

Designated Account 5 53,924.27 59,813.26

SUMMARY OF WITHDRAWAL APPLICATIONSAs December 31, 2014

'USDClaimed Credited Credited

WA No. date date amount

WA 3 Replenishment 30.04.2014 16.05.2014 47,920.13

WA 4 Replenishment 14.10.2014 30.10.2014 29,669.10

77,589.23

4

U

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

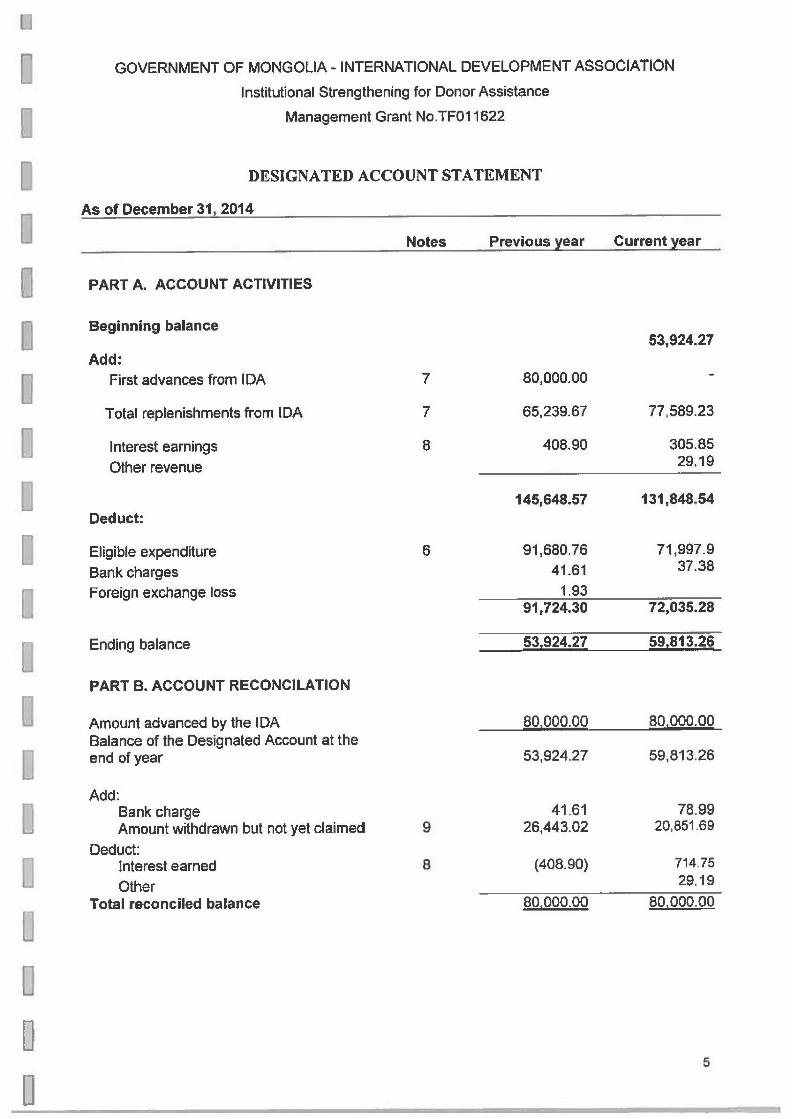

DESIGNATED ACCOUNT STATEMENTn As of December 31~ 2014

Notes Previous year Current year

PART A. ACCOUNT ACTIVITIES

Beginning balanceAdd: 53,924.27

Add:First advances from IDA 7 80,000.00 -

Total replenishments from IDA 7 65,239.67 77,589.23

Interest earnings 8 408.90 305.85Other revenue 29.19

145,648.57 131,848.54Deduct:

Eligible expenditure 6 91,680.76 71,997.9Bank charges 41.61 37.38

Foreign exchange loss 1.9391,724.30 72,035.28

Ending balance 53,924.27 59,813.26

PART B. ACCOUNT RECONCILATION

Amount advanced by the IDA 80Q0000 00.00Balance of the Designated Account at theend of year 53,924.27 59,813.26

Add:Bank charge 41.61 78.99Amount withdrawn but not yet claimed 9 26,443.02 20,851.69

Deduct:Interest earned 8 (408.90) 714.75

Other 29.19Total reconciled balance 80,000.00 80.00

U

I

Li

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

Notes to the financial monitoring reports for the financial year 2014

1. Introduction

I Financing Agreement of the Project Grant No TF011622 was signed between the InternationalDevelopment Association ("World Bank") and Government of Mongolia on April 5, 2012. Theproject implementation has started on February 1, 2013.

The objective of the grant is to strengthen the government's ability to manage developmentprojects funded by the Official Donor Assistance (ODA) in Mongolia, through

a) Establishing result-oriented Monitoring and Evaluation (M&E) systems with a focus on

effective and efficient delivery of intended results of development projects,

b) Strengthening M&E network and capacity, and

c) Enhancing the quality and accessibility of information for decision makers and stakeholders.

The project consists of the following parts:

Part 1. Develop result-oriented M&E system for ODA-funded projects.

1.1 Carrying out of a diagnostic study of existing M&E practice for the development projects:

1.2 Developments of result-oriented M&E framework, based on the results of the diagnostic

study, including consultative and brainstorming workshops and seminars among key

stakeholders, and formulation, piloting and implementation of relevant M&E regulations

and guidelines:

1.3 Development of a result-oriented M&E Management Information System (MIS) for relevant

M&E department of selected ministries, including the carrying out of a needs assessment,

training of M&E staff of the national network, procurement, installment, piloting and

implementation of computerized M&E MIS, and development and implementation of a

Financial Management Information System for ODA- funded project; and

1.4 Project management.

Part 2. Strengthening of M&E capacity at National and local levels.

2.1 Training of key staff of the M&E network at the national level on M&E strategy, principles

and practices, including south-south learning activities for key stakeholders from the

Ministry of Finance, Cabinet Secretariat, selected line ministries and the provincial M&E

networks;

2.2 Training of staff of project management units and local M&E staff on M&E guidelines,

Procedures and good practices; and

2.3 Design and implementation of a knowledge sharing and public awareness program for

various stakeholders, covering, inter alia, M&E principles, quality and transparency of

information, communications strategy, usage of information for decision-making, third party

monitoring and community participation

6

U

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

Part 3: Support utilization of M&E results to inform strategic and operational decisionmaking.

Carrying out of workshops to disseminate findings and recommendations for M&E activities inkey sectors and to summarize and share lessons and experience from the Projectimplementation.

In accordance with the letter of Agreement signed on 5 April 2012 for Official Donor AssistanceProject Grant No.TF01 1622, the project is funded by a grant in the amount of USD 350,000provided by Institutional Development Fund through IDAANorld Bank.

The eligible expenditures that may be financed out of the proceeds Grant and allocations of theamounts of the Grant to categories of expenditures are as follows:

Amount of the Grant Percentage ofCategory allocated expenditures to

be financedConsultants' services, Goods and non-consultingservices, Audit, Training and Workshops, 350,000 100%

THE PROJECT IMPLEMENTATION

Part 1:

j In order to develop a result-oriented M&E Management Information System (MIS), the Ministry ofFinance hired the IT expert, and made contract with him on June 13, 2014 under the project.IT expert has been drafted system design together with Project coordinator (National consultant)and finalized it based on the comments provided by the Financial Policy and Debt ManagementDepartment, Monitoring, Evaluation and Internal Auditing Department, IT Department of MOF,Ministry of Economic Development, Head of the Monitoring, Evaluation and Internal AuditingDepartment of the Cabinet Secretariat.

Based on the World Bank's no objection on the TOR for consultancy service for developing theM&E Management Information System, dated September 10, 2014, a vacancy announcement forthe IT firm. The selection of the Consultant has been conducted in accordance with theConsultants' Qualifications (CQS) method set out in the Consultant Guidelines of the Worldbankand the evaluation was carried out based on the qualification criteria, stated in the REOI and theTOR for the National Consultant firm. The best qualified firm (ITZone LLC) from the fourconsultant firms who have submitted proposals has been invited to submit the technical andfinancial proposals in October 30, 2014 and awarded a contract on November 21, 2014

The ITZone LLC submitted system development plan on December 1, 2014 and finalized thedesign report of the system on December 12, 2014.

U

7

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF011622

2. Summary of Significant accounting policies

(a) Accounting basis

The financial statements, expressed in United States Dollars ("USD"), have been prepared on acash receipts and payments basis of accounting. On this basis, receipts are recognised whenreceived or direct payment to creditors are made rather than when earned and disbursementsare recognised when paid rather than when incurred.

(b) Foreign currency translation

The project financial statements are stated in USD. Transactions in currencies other than USDduring the year have been translated into USD at FIFO rates ruling at the transaction dates.Exchange differences arising therefrom are taken up in the Statement of Sources and Uses ofFunds.

The statement of designated account is presented in USD. The amounts in USD are the actualamounts debited or credited to the Designated Account.

The summery of statements of expenditure is also presented in USD. The amounts in USD arethe actual amounts applied for replenishment from the IDA.

(c) Sources of funds

The funds received are recognized as source of funds when received at the Designated Accountplus the inter-bank charges deducted from the remittance.

Based on reconciliation of Designated Account and actual expenditures, the withdrawalApplication are prepared and submitted to the IDA for reimbursement of eligible expenditures.

I(d) Uses of funds

The expenditure eligible for the Project is recognized as use of funds when actual disbursementsare made for project activities.

3. Designated Account

In accordance with Standard Condition for Grant made by the World Bank and under theprovision of Grant Agreement, the Project should open and maintain a United States DollarDesignated Account. This account is used for eligible expenditures in accordance with the GrantAgreement and is replenished from time to time from the grant account.

4. Procurement

The goods and consultants' services required for the project and to be financed out of theproceeds of the Grant are procured in accordance with Section I of the "Guidelines: Procurementof Goods, Works and consulting Services under IBRD Loans and IDA Credits and Grants byWorld Bank Borrowers" dated January 2011 and Section I and IV of the "Guidelines: Selectionand Employment of Consultants under IBRD Loans and IDA Credits and Grants by World BankBorrowers" dated January 2011.

8

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

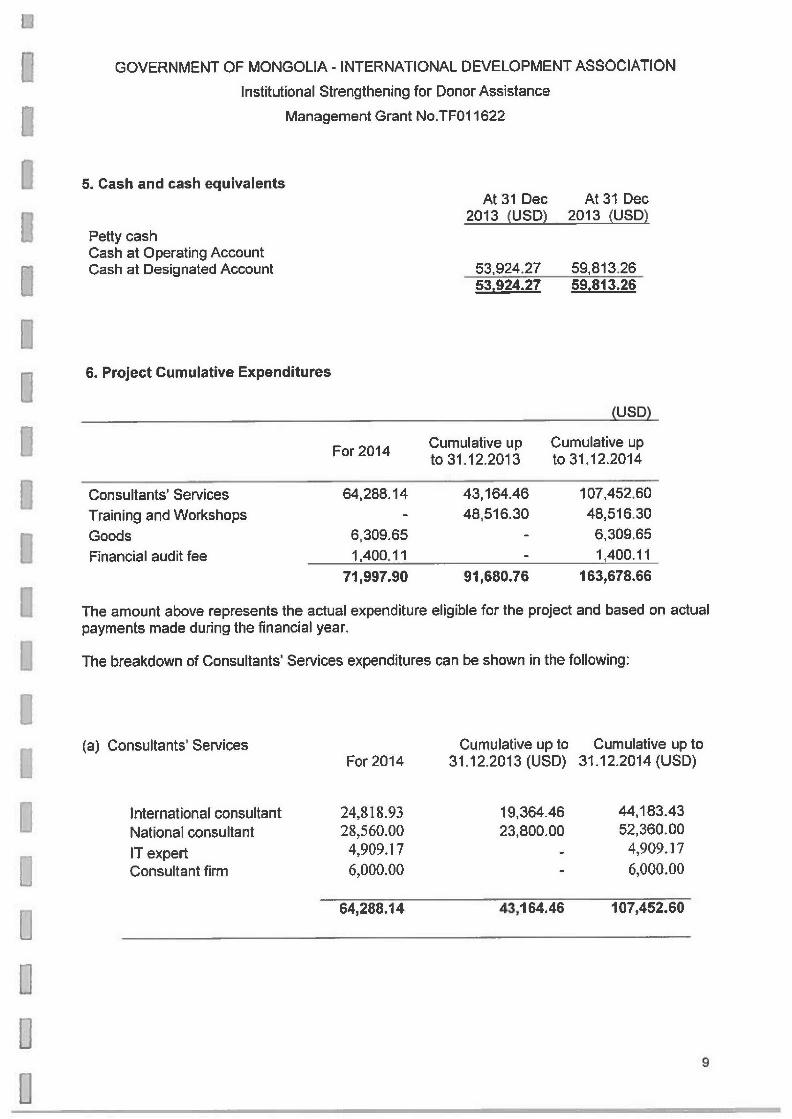

5. Cash and cash equivalentsAt 31 Dec At 31 Dec

2013 (USD) 2013 (USD)I Petty cash

Cash at Operating AccountCash at Designated Account 53,924.27 59,813.26

53,924.27 59,813.26

o 6. Project Cumulative Expenditures

(USD)Cumulative up Cumulative up

to 31.12.2013 to 31.12.2014

Consultants' Services 64,288.14 43,164.46 107,452.60Training and Workshops - 48.516.30 48,516.30Goods 6,309.65 - 6,309.65Financial audit fee 1,400.11 - 1,400.11

71,997.90 91,680.76 163,678.66

The amount above represents the actual expenditure eligible for the project and based on actualpayments made during the financial year.

The breakdown of Consultants' Services expenditures can be shown in the following:

(a) Consultants' Services Cumulative up to Cumulative up toFor 2014 31.12.2013 (USD) 31.12.2014 (USD)

International consultant 24,818.93 19,364.46 44,183.43National consultant 28,560.00 23,800.00 52,360.00IT expert 4,909.17 - 4,909.17Consultant firm 6,000.00 - 6,000.00

I 64,288.14 43,164.46 107,452.60

1

LJ

GOVERNMENT OF MONGOLIA - INTERNATIONAL DEVELOPMENT ASSOCIATION

Institutional Strengthening for Donor Assistance

Management Grant No.TF01 1622

fl 7. IDA Funds

Cumulative up to Cumulative up toFor 2014 31.12.2013 (USD) 31.12.2014 (USD)

Advance to designated account - 80,000 80,000

Replenishment to designated account 77,589.23 65,239.67 142,828.90

77,589.23 145,239.67 222,828.90

8. Interest earned

The amount represents the interest earned on the balances of designated account.

Cumulative up to Cumulative up toFor 2014 31.12.2013 (USD) 31.12.2014 (USD)

Interest earned 305.85 408.90 714.75LI Bank charges (37.38) (41.61) (78.99)

Other income* 29.19 29.19Net interest earned 297.66 367.29 664.95

Note:* Bank charges have been credited back into the designated account from previous year.

9. Amount withdrawn but not yet claimed

The amount represents the disbursements were made from the account up to 31 December2013 but have not been claimed from IDA as of 31 December 2013.

Cumulative up to Cumulative up to

L 31.12.2013 (USD) 31.12.2014 (USD)

International Consultant service 19.301.09National Consultant service 7,140 13,140.00Goods 6,309,65Financial audit service 1,400.11Foreign exchange difference 1.93

26,443.02 20,851.69

[I10