A guide to Halifax structured...

22

A guide to Halifax structured products Halifax Share Dealing Limited Please note, this guide is for further reading and does not act as a replacement for any point of sale product specific literature, nor is it a legal document required to be read prior to trading Halifax structured products. The guide is aimed at clients wishing to gain more detailed understanding of the ‘under the bonnet’ mechanics of structured products. This document contains some indicative price scenarios which reflect market conditions at the time of writing. These indicative price scenarios do not represent an investment offer. SHARE DEALING

Transcript of A guide to Halifax structured...

A guide to Halifax structured productsHalifax Share Dealing Limited

Please note, this guide is for further reading and does not act as a replacement for any point of sale product specific literature, nor is it a legal document required to be read prior to trading Halifax structured products.

The guide is aimed at clients wishing to gain more detailed understanding of the ‘under the bonnet’ mechanics of structured products.

This document contains some indicative price scenarios which reflect market conditions at the time of writing. These indicative price scenarios do not represent an investment offer.

SHARE DEALING

29837AP_HXGSPWEB_0612_A4.indd 1 27/06/2012 11:09

Call 08457 22 55 252

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

Contents See page

Background 2

1 WhatisaHalifaxstructuredproduct? 3

a)Returnofcapitalatmaturity 3

b)Term 3

c)Underlyingexposure 3

d)Pre-defined(formula-based)solutions 4

2 HowareHalifaxstructuredproductsconstructed? 5

a)Hardbarrierstructuredproducts 5

b)Softbarrierstructuredproducts 9

3 RisksofinvestinginHalifaxstructuredproducts 11

a)OptionBarrierrisk 11

b)Counterpartyrisk 14

c)Earlywithdrawalriskduringtheterm 15

4 TaxationofHalifaxstructuredproducts 16

5 ReasonstoconsiderHalifaxstructuredproducts 17

6 Frequentlyaskedquestions 18

Glossary 20

Capitalisedtermsusedinthisdocumenthavethemeaningasdefinedintheglossaryonpage19.

BackgroundTheuseofstructuredproductsintheUKhasevolvedoverthepasttwodecadestobecomeathrivingindustryover£50bninsize.

Thechallengingeconomicandmarketconditionsoflowinterestratesandvolatileequitymarketsobservedsince2008hasseeninvestorsseekalternativesolutionstotraditionalcollectiveinvestmentfundsasameansofgeneratingpossibleattractivereturns.

Source:StructuredRetailProducts.com2012

29837AP_HXGSPWEB_0612_A4.indd 2 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing3

1. What is a Halifax Structured Product?Thetermstructuredproductisthenamegiventoaninvestmentthatprovidesareturnthatispre-determinedwithreferencetotheperformanceofoneormoreunderlyingasset(s).

Pre-determined return for Given investment circumstances

Structuredproductsareavailablenowinavarietyofproductwrapperssuchasstructureddeposits,structuredfundsandsecurities(whichincludeNotes,SpecialPurposeVehicles(SPVs),certificatesandwarrants).

AHalifaxstructuredproductisastructuredNote.ThisisatypeofsecurityissuedbyLloydsTSBBankplc(asCounterparty)anddistributedbyHalifax.

Halifaxstructuredproductsoffersolutionsthatemphasiseriskcontrolastheyallowinvestorstomanageriskandreturnexpectations.Structuredproductscanthereforebecustomisedtomeetthediverseneedsofinvestorsinarangeofmarketconditions.

Thekeyvariablesinvolvedintheirconstructionare:

a) Return of capital at maturityOneofthemaindifferentiatorsbetweenstructuredproductsandotherinvestmentsisthatmanystructuredproductscanbebuilttoensureinvestorsinitialcapitalisreturnedinfullatmaturity,whichmeansaninvestorcanshareinthegrowthofspecificmarketsatalevelofriskthatsuitsthem.ThereturnofcapitalatmaturitymaybeofferedbyusingaHardBarrierwhereapre-definedamountofinvestors’capitalwillbereturned(e.g.90%or100%ofinitialcapitalisreturnedatmaturity)oraSoftBarrierwhereatriggerlevelissetattheoutsetwhichplacesfullcapitalatriskonlyifthebarrierisbreached.Seesection3a‘Option Barrier Risk’forfurtherinformation.

WhenyouinvestintoaHalifaxstructuredproduct,LloydsTSBBankplc,initsroleactingasCounterparty,placespartofyourinvestmentintoaZeroCouponBondwhichaimstopaybackafixedamountinordertoreturncapitalatthematuritydate.ItisthereforeimportantthatthefinancialstrengthoftheCounterpartyisexaminedpriortopurchasingthestructuredproduct.Seesection3b‘Counterparty risk’forfurtherinformation.

b) TermMostproductshaveafixedTerm,soinvestorsknowwhentheirinvestmentwillmature(typically3-6years).HalifaxstructuredproductsaredesignedforinvestorswhocanleavetheirinitialcapitalinvestedforthefullTerm.Ifaninvestorsellstheirstructuredproductpriortomaturitytheamountthattheygetbackmaybesignificantlylessthantheiroriginalinvestment.Seesection3c‘Early withdrawal risk during the term’forfurtherinformation.

c) Underlying exposureEachnewHalifaxstructuredproductthatislaunchedwillclearlydescribetheunderlyingasset(s)itoffersexposureto.Structuredproductscanbeusedtoaccesstheperformance,viatheuseofDerivatives,ofawiderangeofassetclasses(the‘Underlying’),includingglobalequityindices(e.g.theFTSE100orS&P500),commoditypricesorindices,currencies,andtheperformanceofindividualequities.

Thefrequencyofmovement,eitherupordown,oftheseassetclassesisknownasVolatility.HigherVolatilitywouldsuggestgreatermovementintermsofthepricevariabilityoftheassetand,therefore,greaterrelativerisk.LowerVolatilitywouldsuggestlessmovementintermsofthepricevariabilityoftheassetand,therefore,lowerrelativerisk.WhenconstructingastructuredproductthereisalinkbetweenVolatilityandthecostofgainingexposuretoagivenassetclass,thehighertheVolatilitythemoreexpensivetherighttobuy.Thisrighttobuyisknownasa‘CallOption’(arighttosellisa‘PutOption’).

29837AP_HXGSPWEB_0612_A4.indd 3 27/06/2012 11:09

Call 08457 22 55 254

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

TheimpactofCallOptionsbeingmoreexpensiveisthatlessexposuretothatgivenassetclasscanbeachievedandthereforethepossiblereturnsofthestructuredproductarelower.

d) Pre-defined (formula-based) solutionsStructuredproductsmaybeusedforinvestorsseekingeitherincomeorgrowthwhichisbasedonapre-definedformula.Thismeansinvestorshaveaclearlydefinedreturnprofile.Unlikesomeotherinvestmentssuchasactivelymanagedfunds,structuredproductsprovideaclearviewofhowtheproductshouldperformoverarangeofperformancesoftheUnderlying.Forexample,a5yearstructuredproductwhichofferstoreturn100%ofinvestors’capitalatmaturitywillofferasetParticipationintheFTSE100Index,typicallyreflectedasafixedpercentage.Caps(maximumreturns)aresometimesintroducedtoincreaseParticipationlevels.

29837AP_HXGSPWEB_0612_A4.indd 4 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing5

2. How are Halifax StructuredProducts Constructed?Halifaxstructuredproductsarelaunchedregularly.Theconstructionofeachproductwillvaryfromlaunchtolaunch.However,generallywereturntothekeyvariableslistedinsection1asthebuildingblocksforeachstructure.

BelowweexplorethemechanicsinvolvedinconstructingaHardBarrierstructuredproductandastructuredproductwithaSoftBarrier.

a) Hard Barrier structured productsHardBarrierstructuredproductsofferthereturnofcapitalatmaturityregardlessofhowtheUnderlyinghasperformed.Thebarrierislikelytobeexpressedasafixedpercentageofinitialcapitale.g.80%,90%or100%.

Example 1: 100% return of capital at maturity.Let’sstartbybuildingasimple5yearstructuredproductofferingexposuretotheFTSE100Indexwhichalsooffers100%returnofcapitalatmaturity.Weassumeatinceptionthatwehave100%tospendonbuildingthestructure(‘totalamounttoinvest’).

Return of capital at maturity + Term: Firstly,asweareoffering100%returnofcapitalatmaturityweneedtocalculatehowmuchitcoststoensurethataninvestor’sinitialcapitalisreturnedinfullonthematuritydate.TheproductTermisakeyinfluenceonthiscostasthisimpactsonhowmuchweneedtosetasidenowinordertomeetthisfuturerepayment.

ThecostofdoingsoisessentiallyapresentvaluecalculationwherebyweestablishhowmuchitwillcostustodaytopurchaseaZeroCouponBondwhichwillmeetthefutureobligationofreturninganinvestors’capitalinfullatmaturity.So,thismeansattimesoflowinterestrates,thegreatertheamountrequiredtobeallocatedtotheZeroCouponBond.ItisalsotruethattheshortertheTermthehighertheamountthatneedstobeallocatedtotheZeroCouponBondelementofthestructure.Basedoncurrentlowinterestrates,wewillassumeforthisexamplethatitwouldcostus80%ofour‘totalamounttoinvest’.

Underlying + Pre-defined (formula-based solutionsWiththeremainingamountavailable,20%ofthe‘totalamounttoinvest’,CallOptionsonthechosenUnderlyingwillbepurchased.So,inourexample,wewillbuyCallOptionsontheFTSE100IndextogainexposuretothegrowthintheIndex.ThenumberofCallOptionsthatwepurchaseisdeterminedbyhowmuch‘totalamounttoinvest’wehavelefthavingaccountedfortheaforementionedcostsoftheZeroCouponBondaswellasthecostsinvolvedinmanufacturingandadministeringtheproductover5years.ThespecificcostsmayvaryfromlaunchtolaunchoneachHalifaxstructuredproductandwillbedetailedintheindividualproductbrochure.

Byassumingtotalfeesandexpensesof3%wehave17%remainingforpurchasingCallOptions.Thiscouldenableustoofferaproductwithfeaturessuchas:

2 times the growth in the Index subject to a cap of 40% growth (i.e. to put this another way, 200% participation in the first 20% growth of the Index).ThenumberofCallOptionsthatcanbeboughtwiththe17%‘totalamounttoinvest’willdependontheVolatilityoftheUnderlying.ThemorevolatiletheUnderlyingthemoreexpensivetheCallOptionsthereforethefewerthatcanbepurchased.

29837AP_HXGSPWEB_0612_A4.indd 5 27/06/2012 11:09

Call 08457 22 55 256

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

R e t u r n %

I n d e x %

+

+-

-

100% capitalreturn atmaturity

Cap

40

20

Product return profile Building Block Term (yrs)

Cost Details

ZeroCouponBond 5 80% Presentvaluecalculationtosecurereturnof|100%ofinitialcapitalatmaturity

Totalfees&expenses – 3% Accountsformanufacturingandadministrationcostsandfees

CallOptions 5 17% Provides200%participationinthefirst20%growthoftheIndex

‘Total amount to invest’ 100%

Allocation of ‘total amount to invest’

Investor’s capital Initial allocationinside structured

product

Final valuationinside structured

product

Repayment to investor at maturity

Fees

100% of capital invested

100 105

Possible Return

X%

100

Return of capitalat maturity

Call Options

80

17

3

100+ X%

100% of capitalplus X% return

from Call Options

5 year zero coupon bond grows to 100%

at maturity

Example 1: 100% return of capital at maturity (continued).

29837AP_HXGSPWEB_0612_A4.indd 6 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing7

Example 2: 90% return of capital at maturity.Inthisexamplewearenotlookingtogivecertaintythatallaninvestors’capitalisreturnedatmaturity.InsteadofourHardBarrierlevelbeingsetat100%ofinitialcapitalbeingreturnedatmaturity,wewillintroduceapotentialmaximumlossof10%.Thismeansinvestorshavethepotentialtoloseupto10%ofinitialcapitalatmaturityastheyhaveexposuretothefirst10%fallintheUnderlyingbutnomore.

Toconstructthisproduct,forsimplicity,let’skeeptheothervariablesconsistentwithexample1onpreviouspage.TheproductwillhaveaTermof5years,willofferexposuretotheFTSE100Indexandwillembed3%tocoveradministrationcostsandfees.

Return of capital at maturity + Term: Westillneedtocalculatehowmuchitcoststoensurethat100%ofaninvestor’sinitialcapitalisreturnedatmaturity(in5yearstime).Basedoncurrentlowinterestrateswecanassumethiswouldcostus80%ofour‘totalamounttoinvest’.However,secondly,asexposuretothefirst10%fallintheUnderlyingisbeingtaken,wewill

receivesomeofour‘totalamounttoinvest’backfortakingonthiselementofrisk.Bysellingwhatisknownasa‘spread’PutOptionwewillreceive,say,5%whichwecanaddontoour‘totalspend’.Thismeanswenowhave25%availabletoinvestinCallOptions(100%-80%+5%=25%).

Underlying + Pre-defined (formula-based) solutionsSowenowhave25%ofour‘totalamounttoinvest’availabletopurchaseCallOptionsontheFTSE100IndextogainexposuretothegrowthintheIndex.Aspreviouslymentionedadministrationcostsandfeestotal3%,meaningwenowhave22%remainingforpurchasingCallOptions.Thiscouldenableustoofferaproductwithfeaturessuchas:

2 times the growth in the Index subject to a cap of 60% growth (i.e. to put another way, 200% participation in the first 30% growth).Thisexamplehighlightshowintroducinganelementofrisktocapitalwillincreasethepotentialreturn.

29837AP_HXGSPWEB_0612_A4.indd 7 27/06/2012 11:09

Call 08457 22 55 258

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

Building Block Term (yrs)

Cost Details

ZeroCouponBond 5 80% Presentvaluecalculationtosecurereturnof100%ofinitialcapitalatmaturity

Putoption(selling) 5 (5%) BysellingaPutOptionweareexposedtolossestothefirst10%fallintheUnderlyingatmaturity,butnomore.Fortakingonthisriskwereceive5%toaddtoour‘totalamounttoinvest’

Totalfees&expenses

– 3% Accountsformanufacturingandadministrationcostsandfees

CallOptions 5 22% Provides200%participationinthefirst30%growthoftheindex

‘Total amount to invest’

100%

Allocation of ‘total amount to invest’

Investor’s capital Risk premium added

Initial allocationinside structured

product

Final valuationinside structured

product

Repayment to investor at maturity

100% of capital invested

100

100+ X%- Y%

100% of capitalplus X% return

from Call Options...

...MINUS Y%return from Put Options

Call Options

Fees

Proceeds of sellingPut Options added

to capital

105

Possible Return

X%

-Y%

100

Return of capitalat maturity

80

22

5

3

Example 2: 90% return of capital at maturity (continued).

R e t u r n %

I n d e x %

+

+-

-

90% capitalreturn atmaturity

Cap

60

30

Product return profile

29837AP_HXGSPWEB_0612_A4.indd 8 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing9

b) Soft Barrier structured productsThebuildingblocksofSoftBarrierstructuredproductsremainsthesameasthoseforHardBarrierstructuredproductsbutthecostofeachbuildingblockvaries.Let’suseanexampleofaproductwiththeFTSE100IndexagainrepresentingourUnderlying,a4yearTermandaEuropeanOptionBarrier.AEuropeanOptionBarrieroffersfullreturnofcapitalatmaturitysolongastheUnderlyingisatoraboveaspecifiedlevelonthematuritydate(seesection3a‘Option Barrier Risk’forfurtherinformation).

Return of capital at maturity + Term: Whencalculatinghowmuchitcoststoensurethereturnofcapitalatmaturitytherearetwodifferencesfromourpreviousexample.Firstly,theTermisshorter(4yearsnot5years)which,ifeverythingwasequalwouldmeanthatmoreofour‘totalamounttoinvest’wouldberequiredtoaffordtheZeroCouponBondelementofthestructure(whichisrequiredtoreturnaninvestor’scapitalin4yearstime).Let’ssaythisequatestoapproximately85%ofthe‘totalamounttoinvest’(asopposedto80%forthe5yearTerm).However,secondly,aswearelookingataSoftBarrierinsteadofHardBarrierwewillreceivesomeofour‘totalamounttoinvest’backfortakingontheelementofriskembeddedintheEuropeanOptionBarrier.ThisbarriermeansthatiftheIndexfallsbelowapre-definedlevel,say50%ofitsinitiallevelatmaturityinvestors’capitalwillbeexposedtolosses.

Bysellingwhatisknownasa‘knock-in’PutOptionwewillreceive,say,15%whichwecanaddontoour‘totalamounttoinvest’.Thismeanswehave30%left(100%-85%+15%=30%).

Underlying + Pre-defined (formula-based) solutionsWiththeremainingamountavailable(30%),againwebuyCallOptionsontheFTSE100IndextogainexposuretothegrowthintheIndex.Becausewehaveincorporatedgreaterriskintothisstructurewehavemoretospend(30%asopposedto20%inthepreviousexample).BeforepurchasingCallOptionswefactorinthecostsofmanufacturingandadministeringwhichwillbemarginallylowerfora4yearproductratherthana5yearproduct.

Byassumingtotalfeesandexpensesof2%,wehave28%remainingforpurchasingCallOptions.Thiscouldenableustoofferaproductwithfeaturessuchas:

5 times the growth in the Index subject to a cap of 60% growth (i.e. to put another way, 500% participation in the first 12% growth).Again,thenumberofCallOptionsthatcanbeboughtwith28%‘totalamounttoinvest’willdependontheVolatilityoftheUnderlying.ThemorevolatiletheUnderlyingthemoreexpensivetheCallOptionsthereforethefewercanbepurchased.

29837AP_HXGSPWEB_0612_A4.indd 9 27/06/2012 11:09

Call 08457 22 55 2510

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

Building Block

Term (yrs)

Cost Details

ZeroCouponBond

4 85% Presentvaluecalculationtosecurereturnofcapitalatmaturityof100%.Asnow4yearterminsteadof5yearsthiscostsagreateramount

PutOption(selling)

4 (15%) Bysellinga‘knock-in’PutOptionweareexposedtolossesiftheindexfallsbelow50%ofitsinitiallevel.Fortakingonthisriskwereceive15%tospend

Totalfees&expenses

– 2% Accountsformanufacturingandadministrationcostsandfees(slightlylowerthanthepreviousexampleas4yearratherthan5year)

CallOption(buying)

4 28% Provides500%participationinthefirst12%growthoftheIndex

‘Total amount to invest’

100%

Allocation of ‘total amount to invest’

Investor’s capital Risk premium added

Initial allocationinside structured

product

Final valuationinside structured

product

Repayment to investor at maturity

Return of capitalat maturity

Call Options

Fees

100% of capital invested

100

Proceeds of sellingPut Options added

to capital

11585

28

15

2 Possible Return

X%

-Y%

100

100% of capitalplus X% return

from Call Options...

...MINUS Y%return from Put Options

100+ X%- Y%

Soft Barrier structured products (continued).

R e t u r n %

I n d e x %

+

+-

-

50% soft barrier

60

12

Cap

Product return profile

29837AP_HXGSPWEB_0612_A4.indd 10 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing11

3. Risks of investing in Halifaxstructured productsHalifaxstructuredproductsallowinvestorstomanageriskwithintheirportfoliobyprovidingpre-definedrulesonhowaninvestor’scapitalwillbereturnedatmaturity.TheprevailingclimateofheightenedVolatilityobservedinequitymarketsoverrecentyearshasraisedawarenessofthepotentialvalueofensuringthefullorpartialreturnofinitialcapitalatmaturity.

Therearethreemainriskstobeawareofwheninvestinginstructuredproducts:

a) Option Barrier risk (dependent upon the Option Barrier used)

b) Counterparty risk (the ability of the issuer to meet its obligations to repay initial capital at maturity and any income during the Term)

c) Early withdrawal risk during the term

a) Option Barrier riskClearly,includingfullreturnofcapitalatmaturitywithinaproducthasacostassociatedwithit(ashighlightedinsection2‘How are structured products constructed?’).Thehigherthelevelofinitialcapitalthatisensuredtobereturnedatmaturitythelowerthepercentageof‘totalamounttoinvest’allocatedtopurchasingCallOptions.ThisresultsinalowerpotentialexposuretotheUnderlying.Sotheopportunitycostofensuringfullreturnofcapitalatmaturityintoastructuredproductmaywellresultinalimitationonthegrowthpotential…thefullreturnofcapitalatmaturityisnotprovidedforfree!

Aspreviouslydiscussedinsection2werefertoourstructuredproductsaseitherincorporatingaHardBarrierorSoftBarrier.OptionBarriersareaspecifiedleveloftheUnderlyingthatifbreachedwilltriggerachangeinthepotentialproductreturn.

Hard Barriers in greater detail.AsdescribedinExample1and2ofsection2athisdefinesthemaximumloss(ifany)thatcanbeincurredwhenpurchasingtheproduct.AHardBarrierdescribesthemaximumlosspossible,irrespectiveofhowtheUnderlying(e.g.FTSE100Index)performs.

ThedegreeofinitialcapitalreturnedatmaturityisexpressedasapercentageoftheInitialLeveloftheUnderlying(the‘OptionBarrier’).MostcommonlyweseeHardBarriersbeingofferedat100%(i.e.fullreturnofcapitalisaffordedatmaturity).Incasesthatdon’tofferfullreturnofcapitalatmaturitylossescanbeincurredforanynegativemovementintheUnderlyinguptothelevelsetbytheOptionBarrier.So,a90%HardBarrierreflectsthefactthat90%oftheinitialcapitalwillbereturnedatmaturitysoaninvestorisexposedtothefirst10%fallintheUnderlying.

R e t u r n %

I n d e x %

+

+-

-

90% capitalreturn atmaturity

Product return profile

The Hard Barrier pre-defines the maximum loss that can be incurred by the investor at maturity. A 90% Hard Barrier means that investors can lose up to 10% of their initial capital at maturity, but no more.

29837AP_HXGSPWEB_0612_A4.indd 11 27/06/2012 11:09

Call 08457 22 55 2512

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

Soft Barriers in greater detail.ThedegreeofcapitalreturnedatmaturityisexpressedasapercentageoftheInitialLeveloftheUnderlying(e.g.50%,60%,70%).ThispercentagedefinesthechangeinvalueoftheUnderlyingbeforeinitialcapitalisplacedatrisk(the‘OptionBarrier’).Oncethebarrierisbreached,theamountofinitialcapitalatriskisdeterminedbytheleveloftheUnderlyingontheFinalReferenceDate.

So,a60%SoftBarrier,forexample,meansthattheUnderlyinghastofallbymorethan40%fromitsInitialLevel(i.e.tobelow60%ofitsInitialLevel)beforecapitalisplacedatrisk.OptionBarriersuseeitherEuropeanorAmericanoptions.Thetypeofoptionuseddictatesthefrequencythatthebarrierisobserved.

European Option Barrier: OffersfullreturnofcapitalatmaturityiftheUnderlyingisatorabovethebarrierontheFinalReferenceDate.IftheUnderlyingisbelowthebarrier,AT MATURITY ONLY,theamountofinitialcapitalatriskdirectlyreflectsthe

percentageamountbywhichtheFinalLeveloftheUnderlyingisbelowtheInitialLeveloftheUnderlying.ThemovementintheUnderlyingduringtheTermhasnoimpact.

American Option Barrier: OffersfullreturnofinitialcapitalatmaturityunlesstheUnderlyingfallsbelowthebarrierAT ANY POINT DURING THE TERM(typicallyobservedatdailycloseasopposedtointraday).

IftheAmericanOptionBarrierisbreachedatcloseofbusinessonanydayduringtheTerm,theninitialcapitalisatrisk.TheamountofcapitalreturnedisdeterminedbytheleveloftheUnderlying.IftheUnderlyingisatoraboveitsInitialLevelontheFinalReferenceDateinvestors’initialcapitalisreturnedinfull.IftheUnderlyingisbelowitsInitialLevelontheFinalReferenceDatetheamountofinitialcapitalreturnedisdeterminedbythepercentageamountbywhichtheFinalLeveloftheUnderlyingisbelowtheInitialLeveloftheUnderlying.

The graph and explanation below illustrates a number of performance outcomes for the Underlying (the FTSE 100 Index). These scenarios assume an Initial Level of the Index (the ‘Initial Index Level’) is 5,500 and the Soft Barrier is set at 50% of the Initial Index Level.

0

1000

2000

3000

4000

5000

6000

7000

Scenario 1

Scenario 2

Scenario 3

Scenario 4 Initial Index Level

50% of Initial Index LevelScenario 5

29837AP_HXGSPWEB_0612_A4.indd 12 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing13

Scenario 1:TheIndexremainsaboveboththe50%OptionBarrierandtheInitialIndexLevelduringtheTerm.

– ForbothEuropeanandAmerican Option BarriersinitialcapitalisthereforereturnedinFULLatmaturity.

Scenario 2:TheIndexbreachesthe50%OptionBarrierduringtheTermANDdoesnotrecoverbacktobeingatorabovetheInitialIndexLevelatmaturity.

– IfitisaEuropean Option Barrier,capitalisreturnedinFULLatmaturityastheleveloftheIndexatmaturityisabovethe50%OptionBarrier.

– IfitisanAmerican Option Barrier,capitalisLOSTatmaturityonaoneforonebasis(inthisinstancetheIndexclosesat60%oftheInitialIndexLeveltherefore40%ofcapitalisLOST).

Scenario 3:TheIndexbreachesthe50%OptionBarrierduringtheTermbutrecoversabovetotheInitialIndexLevelatmaturity.

– ForanAmerican Option BarrierinitialcapitalwasatriskBUTtheIndexdoesrecovertobeingatorabovetheInitialIndexLevelatmaturityandsocapitalisreturnedinFULLatmaturity.

– InitialcapitalisalsoreturnedinFULLatmaturityforaproductwithaEuropean Option BarrierbecausetheIndexisat(orabove)theInitialIndexLevelatmaturity.

Scenario 4:TheIndexfallsbelowtheInitialIndexLevelbutremainsabovethe50%OptionBarrierthroughouttheTermandatmaturity.

– ForbothEuropean and American Option BarriersinitialcapitalisreturnedinFULLatmaturity.

Scenario 5:TheIndexbreachesthe50%OptionBarrierduringtheTermANDisbelowthe50%OptionBarrieratmaturity.

– ForbothEuropean and American Option BarriersinitialcapitalisLOSTatmaturityonaoneforonebasis(inthisinstancetheIndexclosesat40%oftheInitialIndexLeveltherefore60%ofcapitalisLOST).

29837AP_HXGSPWEB_0612_A4.indd 13 27/06/2012 11:09

Call 08457 22 55 2514

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

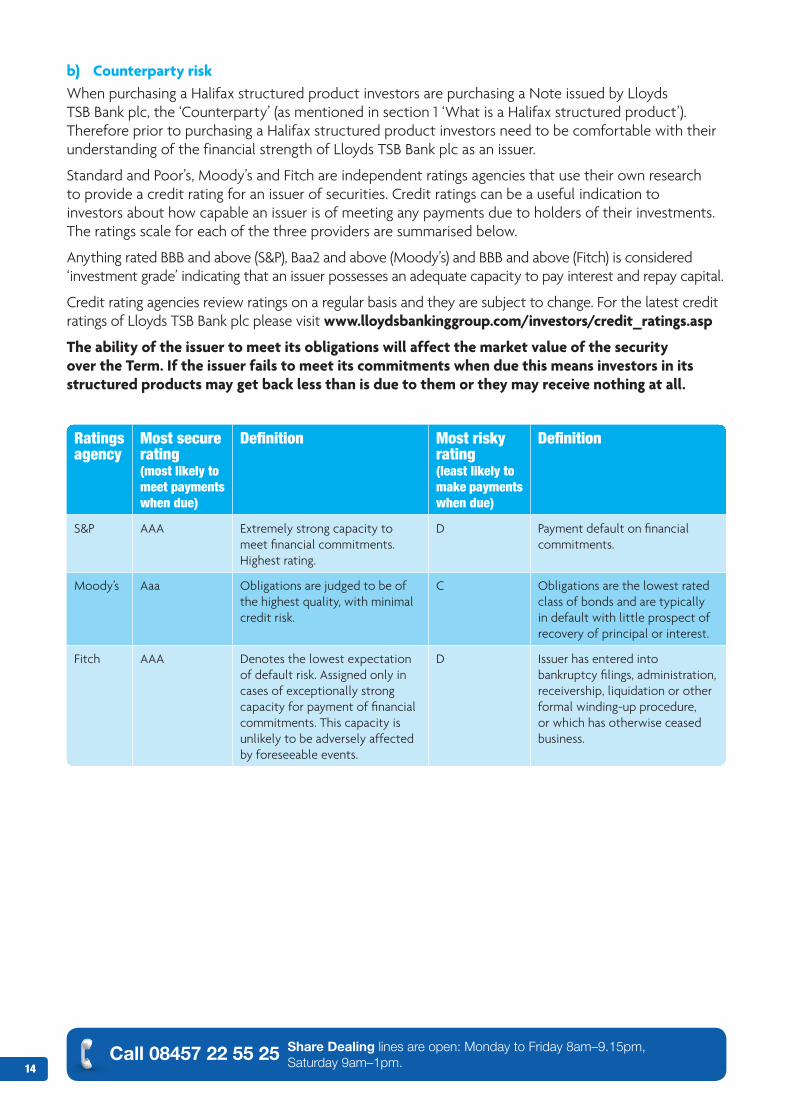

b) Counterparty riskWhenpurchasingaHalifaxstructuredproductinvestorsarepurchasingaNoteissuedbyLloydsTSBBankplc,the‘Counterparty’(asmentionedinsection1‘WhatisaHalifaxstructuredproduct’).ThereforepriortopurchasingaHalifaxstructuredproductinvestorsneedtobecomfortablewiththeirunderstandingofthefinancialstrengthofLloydsTSBBankplcasanissuer.

StandardandPoor’s,Moody’sandFitchareindependentratingsagenciesthatusetheirownresearchtoprovideacreditratingforanissuerofsecurities.Creditratingscanbeausefulindicationtoinvestorsabouthowcapableanissuerisofmeetinganypaymentsduetoholdersoftheirinvestments.Theratingsscaleforeachofthethreeprovidersaresummarisedbelow.

AnythingratedBBBandabove(S&P),Baa2andabove(Moody’s)andBBBandabove(Fitch)isconsidered‘investmentgrade’indicatingthatanissuerpossessesanadequatecapacitytopayinterestandrepaycapital.

Creditratingagenciesreviewratingsonaregularbasisandtheyaresubjecttochange.ForthelatestcreditratingsofLloydsTSBBankplcpleasevisitwww.lloydsbankinggroup.com/investors/credit_ratings.asp

The ability of the issuer to meet its obligations will affect the market value of the security over the Term. If the issuer fails to meet its commitments when due this means investors in its structured products may get back less than is due to them or they may receive nothing at all.

Ratings agency

Most secure rating (most likely to meet payments when due)

Definition Most risky rating (least likely to make payments when due)

Definition

S&P AAA Extremelystrongcapacitytomeetfinancialcommitments.Highestrating.

D Paymentdefaultonfinancialcommitments.

Moody’s Aaa Obligationsarejudgedtobeofthehighestquality,withminimalcreditrisk.

C Obligationsarethelowestratedclassofbondsandaretypicallyindefaultwithlittleprospectofrecoveryofprincipalorinterest.

Fitch AAA Denotesthelowestexpectationofdefaultrisk.Assignedonlyincasesofexceptionallystrongcapacityforpaymentoffinancialcommitments.Thiscapacityisunlikelytobeadverselyaffectedbyforeseeableevents.

D Issuerhasenteredintobankruptcyfilings,administration,receivership,liquidationorotherformalwinding-upprocedure,orwhichhasotherwiseceasedbusiness.

29837AP_HXGSPWEB_0612_A4.indd 14 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing15

S&P RatingMost risky rating Most secure rating

Moody’s RatingMost risky rating Most secure rating

Fitch RatingMost risky rating Most secure rating

c) Early withdrawal risk during the termAspreviouslymentionedtheHalifaxstructuredproductisastructuredNote.InvestorsareabletoselltheNoteinfullpriortomaturity.

ShouldinvestorschoosetoselltheirNotepriortotheMaturityDate,theywillreceivethemarketvalueoftheNoteissuedbyLloydsTSBBankplcontheweeklysell-backdate.ThemarketvalueoftheNotewillbeinfluencedbythefollowingfactors:

i) WhetheritisanincreasingordecreasinginterestrateenvironmentandthemovementofinterestratessincetheInitialReferenceDate

ii) Themovementintheleveloftheindexiii) Theperiodleftuntilthematuritydateiv) Thelevelsatwhichtheissuerlendsandborrowsfromotherbanksandfinancialinstitutionsv) Marketperceptionoftheissuer’sabilitytopayitscommitmentsasandwhentheyfalldue

The impact of these factors may mean that if the investor sells the Note before the maturity date the amount that you receive may be less than the amount you originally invested.

D CC -CCC+ -B+ -BB+ -BBB+ -A+ -AA+ AAA

DRD C CC CCC -B+ -BB+ -BBB+ -A+ -AA+ AAA

C CaCaa321

B321

Ba321

Baa321

A321

Aa321

Aaa

29837AP_HXGSPWEB_0612_A4.indd 15 27/06/2012 11:09

Call 08457 22 55 2516

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

4. Taxation of Halifax structured products

It is important to note that levels and bases of taxation, and relief from taxation, are subject to Government legislation and may change during the Term of the Note and the amount of tax you pay will depend on your individual circumstances. All references to taxation are to UK taxation and are based on our current understanding of UK laws and HM Revenue & Customs published practice. No tax advice is given in this document and the following information is of a general nature only. If you have any doubts or concerns regarding the tax treatment of an investment in the Note, you should seek independent advice.

Direct investmentIncomefromtheNotewillbepaidgrossoftax;wewillnotdeductanytaxes.Youwillthereforebeliabletoincometaxontheincomepaid.For2012/13thetaxrateis20%forabasicratetaxpayer,40%forahigherratetaxpayerand50%foranadditionalratetaxpayer.TheincomepaidwillneedtobedeclaredtoHMRCandanytaxliabilityarisingwillneedtobedealtwithbyyouoryourtaxadvisor.

Ifyouareanon-taxpayerthereshouldbenotaxliabilitysubjecttoyouremainingwithinyourpersonalallowancelimitswhenaddingtheincomereceivedtoyourotherincome.

SIPPIfyouinvestviaaSIPPtherewillbenofurtherobligationonyoutopaytaxasinvestmentreturnsonallSIPPinvestmentsaretaxfreefortheinvestor.

ISAAnIndividualSavingsAccount(ISA)isasavingsvehiclesetupbytheGovernment.TherearetwotypesofISA:aCashISAandaStocksandSharesISA.UnderISARegulationsalleligibleinvestors*canonlyopenoneStocksandSharesISAandoneCashISAinataxyear.

TheannualISAallowanceforthe2012/2013taxyearis£11,280ofwhichamaximumof£5,640canbeinvestedintoacashISAwiththebalancebeingavailableforinvestmentinastocksandsharesISA.

ThisNoteiseligibletobeheldinaStocksandSharesISA.IfyouinvestviaaStocksandSharesISAtherewillbenopersonaltaxliabilityinrespectofanyincomeorgrowtharisingontheNote.Onceyouhaveusedyourfullallowanceinataxyear,youcannotmakeanyfurtherinvestmentsevenifyouwithdrawsome,orall,oftheamountinvested.ThereforeifyoudecidetocloseyourISAinthesametaxyearthatyouinvested,youwillnotbeabletore-investtheproceedsintoanotherISAinthesametaxyear.

The tax position described above and the favourable tax treatment of ISAs and SIPPs might not continue in future. The value of any tax relief will depend on your individual circumstances.

*YoumustberesidentandordinarilyresidentintheUKfortaxpurposes,orperformdutiesasacrownemployeeservingoverseas,orbemarriedorinacivilpartnershipwithsuchaperson.Ifyouareunsureaboutyourstatuspleaseseekindependentfinancialadvice.Youmustbe18orovertoholdaStocksandSharesISA.

29837AP_HXGSPWEB_0612_A4.indd 16 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing17

5. Reasons to consider Halifax structured productsProvides exposure to a broad range of assets StructuredproductsallowinvestorstogainexposuretovariousmarketsandUnderlyingsfromallovertheworldwhichmayotherwisebedifficulttoaccess.

Risk controlStructuredproductsoffersolutionswithanemphasisonriskcontrolastheyallowinvestorstomanagetheirriskandreturnexpectations,thereforemeetingtheneedsofmanydifferenttypesofinvestorsinavarietyofmarketconditions.

Potential tax efficiencyStructuredproductsallowindividualstobenefitfromlowertaxcostsbyprovidinginvestorswiththeopportunitytoinvesttheNotewithinvarioustaxwrappers.TheseincludethepossibilityofinvestingusinganISAand/orSIPPaccountandbenefitfromthetaxefficientenvironment(aslongastheTermofthestructuredproductis5yearsorgreatertoensureISAeligibility).

Lower costsTherearegenerallylowercostsinvolvedinstructuredproductsincomparisonwithotherinvestmentproductssuchasactivelymanagedunittrustsandhedgefunds.Halifaxstructuredproductstypicallyhaveatotalembeddedfeestructureoflessthan3%andthesefeesarenormallyalreadyincorporatedasapercentageoftheinitialcapitalinvested.

Speed to marketFlexibilitytolaunchthematicstructuredproductswithinashorttimescalethusenablinginvestorstotakeadvantageofchangingmarketconditions.

29837AP_HXGSPWEB_0612_A4.indd 17 27/06/2012 11:09

Call 08457 22 55 2518

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

6. Frequently asked questionsAre structured products right for me?Halifaxstructuredproductsareavailabletoselfdirectedretailinvestorsonanexecutiononlybasis–noadviceisprovided.Itisthereforeimportantthatifyouareunsurewhetherinvestinginastructuredproductisrightforyou,youshouldseekindependentfinancialandtaxadvice.

What is the most I could possibly lose?Thiswillbedetailedintheproductinformationandislikelytochangewitheachnewproductlaunch.However,therearesomeriskswhichwillbecommontoallproductsandwithwhichyoushouldfamiliariseyourself.(PleaseseeSection3‘Risks of investing in Halifax structured products’forfurtherdetails).

WheninvestingintoHalifaxstructuredproductsitispossibletoloseallyourinitialcapitalevenifyouholdtheproductuntilmaturity.Thethreemainrisks(asexplainedinsection3)are:

Counterparty risk:whichwillexistoneveryHalifaxstructuredproductandconsistsoftheabilityoftheissuer,LloydsTSBBankplc,tomeetitsobligationstorepayyourinitialcapitalatmaturityandanyincome/returnduringtheTerm.

Option Barrier risk:basedonacombinationofthepre-definedformulaandOptionBarrierlevelused.Forexample,ifyouinvestintoan‘acceleratedreturn’productandatmaturitytheUnderlyinghasnotrisenthennoreturnwillbegenerated.If,theOptionBarrierusedinconstructingtheproductisbreachedthencapitalmayalsobelostatmaturity.

Early withdrawal risk during the Term:shouldyoudecidetosellyourNoteearly,beforematurity,youwillreceivethemarketvalueoftheNoteonthesell-backdate.Theamountthatyoureceivemaybelessthanormorethantheamountyouoriginallyinvested.

How different is a Halifax structured product to a deposit account?AHalifaxstructuredproductisnotadepositaccount.Unlikeadepositaccount,itisnotcoveredbytheFinancialServicesCompensationScheme.IfLloydsTSBBankplcwereunabletopaythebenefitsdueorrepaycapitalduetoyou,youwouldnothaveaclaimunderthescheme.

TheperformanceofthestructuredproductisreliantontheperformanceoftheUnderlying.Adepositaccountwillinsteadpayarateofinterest.

HalifaxstructuredproductsaredesignedforinvestorswhocanleavetheirinitialcapitalinvestedforthefullTerm.Youcansellyourstructuredproductpriortomaturitybutyoumustsellyourentireholdingandtheamountthatyougetbackmaybesignificantlylessthanyouroriginalinvestment.

How different is a structured product to a direct equity investment?Investinginastructuredproductisnotthesameasinvestinginshareslistedonanexchange.Youmightearnmoreorlessthanifyouwereinvesteddirectlyintheshares.

Furthermore,ifyourstructuredproductislinkedtoanindexthenthatindexwillmeasurethecapitalvalueofthesharesintheindexandnoallowanceismadefordividendsorotherdirectpaymentsmadebythecompanieswhosesharescompriseeachindex.

What charges are applied when I purchase a structured product?Therearenoinitialchargesorongoingfeesrelatedtotheproduct.Allmanufacturingandadministrationcostspayablearebuiltintotheinitialproductandarereflectedinthetermsofthestructuredproduct.Thesechargeswillnotnormallyexceed3%ofyouroriginalinvestment.ThespecificchargesoneachHalifaxstructuredproductwillbedetailedintheindividualproductbrochure.

29837AP_HXGSPWEB_0612_A4.indd 18 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing19

What is the offer period and the Initial Reference Date?Theofferperiodistheperiodwhentheoffertoinvestisavailable.Oncetheofferperiodcloseswewillnotbeabletoacceptanyfurtherorders.WewillrecordthestartingleveloftheUnderlyingontheInitialReferenceDate.

Can I change my mind once I’ve made an investmentYoucanchangeyourmindbetweenplacingtheorderandthelastdayoftheofferperiod.Afterthisdaythereisnocancellationprocess.However,youmaysellyourNote,althoughbydoingsoyoumaygetbacklessthanyouinitiallyinvested.

What is a product brochure?Aproductbrochureisthedocumentthatidentifiesthekeyinformationregardingastructuredproduct.Itincludesareassuchastheproductreturn,OptionBarrier,totalfeesandInitialandFinalReferenceDates.

What will I receive when I invest?Oncetheproductislaunched,wewillsendyouanallocationconfirmationcontainingthedetailsofyourinvestmentwhichwillbepostedtothe‘ImportantNotifications’sectionofyouraccount.Youshouldkeepyourconfirmationforfuturereference.

Inaddition,youwillbeabletoviewyourportfoliovaluationshowinguptodatedetailsofyouraccount,includinganystructuredproductsyouhold,withinthesecureareaofourwebsite.

What happens at the end of the Term?ThestructuredproductwillautomaticallymatureattheendoftheTerm.Thestructuredproductwillbesoldandthepayout(return/incomeandcapitalrepayment,ifany)creditedtoyourHalifaxShareDealingAccount.Towithdrawthecashfromyoursharedealingaccount,simplyringourcallcentreoruseouronlineservice.

Can I invest if I don’t have a Halifax Share Dealing Account?Youmusthaveanactivesharedealingaccountwithustoinvestinastructuredproduct.Ifyouapplyonlinenow,youraccountcouldbeactiveimmediately.Pleasenotefurtherdocumentationmayberequiredtocompleteyourapplication.

How do I check how much my investment is worth?Ifyousign-intoyoursharedealingaccountonline,you’llbeabletoseeanup-to-datevaluationofyourstructuredproduct.We’llalsosendyouastatementeverysixmonths.

29837AP_HXGSPWEB_0612_A4.indd 19 27/06/2012 11:09

Call 08457 22 55 2520

Share Dealing lines are open: Monday to Friday 8am–9.15pm, Saturday 9am–1pm.

GlossaryAmerican Option Barrier: OffersreturnofinitialcapitalatmaturityunlesstheUnderlyingfallsbelowtheOptionBarrieratanypointduringtheTerm(typicallyobservedatthedailycloseasopposedtointraday).IftheUnderlyinghasadailyclosevaluebelowthebarrierduringtheTermtheamountofinitialcapitalatriskdirectlyreflectsthepercentageamountbywhichtheFinalLeveloftheUnderlyingisbelowtheInitialLeveloftheUnderlying.

Call OptionAtypeofDerivativethatgivesthepurchasertheright,butnotobligation,topurchaseasetquantityoftheUnderlyingatagivenpriceonorbeforeaspecifieddate.CallOptionsthereforebenefitthepurchaserifthepriceoftheUnderlyingrises.

CapAmaximumreturnthancanbepaidonaproduct.

CounterpartyTheinstitutionthatissuesfinancialinstrumentswhichdelivertheinvestmentreturnslinkedtoastructuredproductaswellaspermitcapitaltobereturnedatmaturity.

Counterparty RiskTheriskofacounterparty(theissuerofastructuredproduct)defaultingonatransactionalobligationresultinginconsequentiallosstotheinvestorinthatstructuredproduct.

DerivativesDerivativesarefinancialproductsthatderivetheirvaluefromthepriceofsomeotherUnderlying.AtypicalderivativeproductiseitheraCallOptionorPutOption.

European Option BarrierOffersfullreturnofcapitaliftheUnderlyingisatorabovethebarrierontheFinalReferenceDate.IftheUnderlyingisbelowthebarrier,atmaturityonly,theamountofinitialcapitalatriskdirectlyreflectsthepercentageamountbywhichtheFinalLeveloftheUnderlyingisbelowtheInitialLeveloftheUnderlying.ThemovementintheUnderlyingduringtheTermhasnoimpact.

Final LevelThisisthefinalleveloftheUnderlyingusedwhencalculatingthereturnfromastructuredproduct.TheFinalLevelisusuallycalculatedatcloseofbusinessontheFinalReferenceDate.

Final Reference DateThisisthedayonwhichtheFinalLeveloftheUnderlyingisobserved.

Hard BarrierProvidesaspecifiedminimumlevelofcapitaltobereturnedatmaturity,regardlessoftheperformanceoftheUnderlying.HardBarrierstructuredproductscanofferfullreturnofcapitalatmaturityoronlyafixedpercentageofcapitalcanbereturnedatmaturity(e.g.80%or90%).

Initial Level TheleveloftheUnderlyingisrecordedatthestartoftheTermwhichisusedtocalculatethestructuredproductreturn.TheInitialLevelisusuallycalculatedatcloseofbusinessontheInitialReferenceDate.

Initial Reference DateThisisthedayonwhichtheInitialLeveloftheUnderlyingisobserved.

NoteANoteisatypeofcorporatebond;effectivelyaloanmadebytheinvestortoLloydsTSBBankplcasissueroftheNote.However,unlikeatypicalloan,theprincipalamountoftheNoteisnotnecessarilyrepaidinfullonmaturity.

Option AnoptionisaformofDerivativecontract.TheownerofanOptionhastheright,butnottheobligation,tobuyorsellafixedquantityofsomeUnderlying,atafixedprice,onorbeforeagivenfuturedate(seeCallOptionandPutOption).

Option BarrierAspecifiedleveloftheUnderlyingthatifbreachedtriggersachangeinthepotentialproductreturnatmaturity.

29837AP_HXGSPWEB_0612_A4.indd 20 27/06/2012 11:09

Visit us online halifax.co.uk/sharedealing21

ParticipationThereturncalculatedbymultiplyinganyriseintheUnderlyingbyafixedpercentage.Forexample,90%participationratemeansthatforeachonepercentagepointincreaseintheUnderlyingthereturntracksat0.9%.Aparticipationrateof200%forexamplemeansthatforeachonepercentagepointriseistrackedby2%(orinotherwordstwotimesthegrowthintheUnderlying).

Put OptionAtypeofDerivativethatgivesthepurchasertheright,butnotobligation,tosellasetquantityoftheUnderlyingatagivenpriceonorbeforeaspecifieddate.PutOptionsthereforebenefitthepurchaserifthepriceoftheUnderlyingfalls.

Soft BarrierFullreturnofcapitalatmaturityissubjecttotheUnderlyingnotfallingbelowtheOptionBarrierpriortomaturity.TheOptionBarriermeansthateveniftheUnderlyingfallsduringtheTerm,butdoesnotbreachtheleveloftheOptionBarrierthencapitalisreturnedinfullatmaturity.SoftBarriersconsistofeitherEuropeanOptionBarriersorAmericanOptionBarriers.Thetypeofoptionuseddictatesthefrequencythatthebarrierisobserved.

Term Thedurationoftheinvestment.StructuredproductstypicallyhavefixedTermsbetweenthreeandsixyearsbutcanbebothshorterandlonger.

UnderlyingThereturnofastructuredproductislinkedtotheperformanceofanUnderlyinge.g.globalindex,commoditypriceorindex,currencyortheperformanceofindividualequities.

VolatilityThefrequencyofmovement,eitherupordown,oftheUnderlying.HigherVolatilitywouldsuggestgreatermovementintermsofthepricevariabilityandgreaterrelativerisk.LowerVolatilitywouldsuggestlessmovementintermsofpricevariabilityoftheUnderlyingandthereforelowerrelativerisk.

Zero Coupon BondAZeroCouponBondisabondthatpaysnocouponsorperiodicinterestpayments.Thepriceofsuchabondthereforerepresentsadiscounttoitsmaturityvalue.

29837AP_HXGSPWEB_0612_A4.indd 21 27/06/2012 11:09

HalifaxShareDealingLimited.RegisteredinEnglandNo.3195646.

RegisteredOffice:TrinityRoad,Halifax,WestYorkshire,HX12RG.

AuthorisedandregulatedbytheFinancialServicesAuthority,

25TheNorthColonnade,CanaryWharf,London,E145HS.

AMemberoftheLondonStockExchangeandanHMRevenue&CustomsApprovedISAManager.

HXGSPWEB(06/12)

It’s easy to get in touch

Share dealing 08457 22 55 25

Current accounts 08457 20 30 40

Savings 08457 26 36 46

Credit cards 08457 28 38 48

Personal loans 08457 24 34 44

Mortgages 08457 27 37 47

Secured lending 08457 27 37 47

Insurance 08457 23 33 43

Investments 08456 01 77 05

Lost and stolen cards 08457 20 30 99

Speak to a colleague in branch today

Phone your local branch direct. You can find the number online at www.halifax.co.uk/branchfinder

29837AP_HXGSPWEB_0612_A4.indd 22 27/06/2012 11:09

![[BNP Paribas] Guide to Structured Products](https://static.fdocuments.in/doc/165x107/5868b6301a28abf23f8be7bf/bnp-paribas-guide-to-structured-products.jpg)