A FINANIAL NEWSLETTER July issue(1).pdf · FDI in collaborations and joint ventures in other areas...

20

Nishka Nishka Nishka A FINANCIAL NEWSLETTER Infrastructure financing July 2014, Volume V, Issue 48 Christ University Institute of Management, Kengeri

Transcript of A FINANIAL NEWSLETTER July issue(1).pdf · FDI in collaborations and joint ventures in other areas...

NishkaNishkaNishka A FINANCIAL NEWSLETTER

Infrastructure

financing

July 2014, Volume V, Issue 48

Christ University Institute of Management, Kengeri

Cementing the Future

Upasana Gurung, F1 & George P. Job, F2

Infrastructure financing, though unglamorous, is very crucial for the development and growth of a

nation. Infrastructure funding could include funding projects of generation/transmission of power, develop-

ing roadways, seaports and airports, laying/maintaining pipelines for gas, setting up industrial parks, tele-

communication services, irrigation projects, etc.

These infrastructure projects are the backbone of any economy, and a growing economy needs to

supply the ever growing need for infrastructure, and therefore the need for funding infrastructure creation.

India, being a developing nation, has a huge need for infrastructure financing. According to the esti-

mates made by the planning commission in March 2010, and after taking into account the recent trends in

different sources of infrastructure financing, the funding gap in the infrastructure sector during the last two

years of the Eleventh Five year plan is likely to be Rs 1, 27,570 Crores, which is around 18 percent of the

total estimated requirement.

In a visibly weak macroeconomic setting, a well planned economic revival policy focused on infra-

structure development is expected to guide the economy back to a robust growth path.

Usually, funds for infrastructure projects are financed by the government through cash/ guarantees.

But this support is no longer sustainable due to the significant deficiency of funds and high sovereign debt

levels in developed countries. Furthermore, infrastructure stimulus packages will likely reverse as govern-

ments look to bring their finances under control.

The maximum tenor for infrastructure funding is 20 years. Funds for the project can be availed in

domestic as well as in foreign currency. The World Bank, export credit agencies and other multilateral

agencies, along with state-owned infrastructure banks, play an important role in financing infrastructure

projects. Private investment will also need to grow, which could prove to be really important.

In India, private participation in the process of infrastructure development has received a lackluster

response. The PPP (Public-Private Partnership) constitutes only a miniscule share in overall infrastructure

building despite initiation of various policy adjustments and sector-specific reform programs. The key to

successfully raising enough investment for the much needed tomorrow’s essential infrastructure will rest in

finding the optimum balance between public and private money.

Given that infrastructure financing is falling out of favor with banks, the question is, if other inves-

tors can fill the gap. If yes, who and in what form?

http://www.economist.com/news/finance-and-economics/21599394-world-needs-more-infrastructure-how-will-it-pay-it-long-and-winding

http://www.assocham.org/events/recent/event_835/Arun-Jain-overseas-listing.pdf

http://www.deloitte.com/assets/Dcom-India/Local%20Assets/Documents/Thoughtware/Funding_the_InfrastructureInvestment_Gap.pdf

http://www.rbi.org.in/scripts/BS_VIEWContent.aspx?ID=1912

Financing of Infrastructure Projects

Niharika Shadra, F1 & Purnima Singh, F2

Infrastructure financing has been a pivotal issue in a developing economy like India. The need has

been more pronounced by the fact that Banks have to implement Basel III norms, which would steer banks

away from long-term loans of 20 years, as it is normal for infrastructure projects to have long gestation pe-

riods which may result into NPAs if in the long run, the situations may change. Government is also tight

stringed with huge inflation bills and is therefore not in the position to take on very large infrastructure

funding commitments. This is creating a need, and opportunity, for new entrants. Long-term investors such

as Insurance companies and Pension Funds are eager to put money into infrastructure, as are endowments

and sovereign-wealth funds. This would ease the pressure on the traditional commercial banks as these

players have a huge funding base to commit to infrastructure commitments for longer gestation periods. As

equity markets are not favorably inclined towards financing projects because of uncertainties in the global

economy, and due to present regulatory requirements limiting exit options, which hinder possibilities of

equity infusion. Other measures that could be taken are the development of a vibrant debt market. Insur-

ance and pension fund companies are using the instrument of Infrastructure Debt Funds, which essentially

act as vehicles for refinancing existing debt of infrastructure companies, thereby creating fresh headroom

for banks to lend to fresh infrastructure projects, a part of which again qualify for refinancing. IDF-NBFCs

would take over loans extended to infrastructure projects that are created through the Public Private Part-

nership (PPP) route.

The government in its latest move has also allowed the infrastructure finance companies to issue

secured debentures with tenure of up to 30 years. This move is expected to help raise long term funds for

this sector. IDF-NBFC’s have also been allowed to issue similar instruments. The infrastructure investment

that is currently required by our reeling economy during the current Five year Plan (2012-17) is about US $

1 trillion. The way of raising this amount is either through PPP or directly through the private sector route.

The first of the two options seem more viable. Though the government spending in this sector is at the top

of the agenda, the need for the private sector to step in is still high. The role of IDF’s is therefore becom-

ing increasingly important. India Infra-debt is India’s first infrastructure debt fund under

the NBFC structure. It is a strategic alliance between ICICI Bank, Bank of Baroda, Citicorp Finance and

Life Insurance Corporation of India. It has successfully raised Rs 300 Crores and plans to raise another Rs

3,000 Crores in the next two years. A key point here is that income from IDF-NBFC’s is exempt from tax.

Tax levied on interest income of IDF-NBFC’s of foreign investors stand significantly lower at 5% com-

pared to a 20% rate for other debt funds. IDF can surely provide the much needed relief to this sector as

they meet two of the most basic requirements of this sector- low cost of funds & long term sourcing. But

we need to see how the sluggish Indian economy taps this source in the future.

http://www.rbi.org.in/SCRIPTs/FAQView.aspx?Id=90

FDI and PPP: Welcoming steps for Indian Railways

Challapalli Kalyana Karthik and Pawanpreet Kaur, F2

FDI:

In January 2014, the Ministry of Home Affairs gave in-principle approval for Foreign Direct Invest-

ment (FDI) in Railway infrastructure. The Cabinet Committee on Economic Affairs (CCEA), however, is

yet to consider the proposal. According to Department of Industrial Policy and Promotion (DIPP), 100%

FDI could be allowed in dedicated freight corridors and high speed railway networks while allowing a 74%

FDI in collaborations and joint ventures in other areas which can help Indian Railways perform better.

PPP:

Several policies have also been announced in the past to attract private investment but most of them

have fallen flat. The main reason for the failure is that these policies did not convert to time-bound projects

and Railway Ministry wants operation, con-

trol and management in their hands which is

unacceptable to the private investors.

Railway ministry managed to attract a

lot of private players for rail port connectivity

projects after incorporation in participative

policies for an amount of about Rs. 38 billion.

The automobile freight train operator scheme

showed some success in the past year with

railway wagons of higher capacity being manufactured for transporting vehicles of Maruti Suzuki. About

18 logistics companies including Concor, Pristine logistics came up with proposals for freight terminals and

about 23 firms including Lloyd Steel and Tata Steel did show interest in developing brown field freight ter-

minals.

PPP model has been successful in Rail Port connectivity projects. Till date, four projects have been

completed through PPP model with a total investment of Rs 16.11 billion, of which, the private sector con-

tribution was around 24%.

At present three PPP rail port connectivity projects are under construction which involves a total

investment of Rs. 34.29 billion, of which, private investment is Rs. 5.62 billion. These projects are ex-

pected to be completed in the next five to six years. Several railway projects worth over Rs. 1,000 billion

are in the pipeline which are planned to be undertaken on PPP basis.

Over the last decade, the private investment in this sector has witnessed growth of less than 1% in

tenth five year plan (2002-2007) to 4% in eleventh five year plan (2007-2012). Clearly, PPPs have proceed-

ed very slowly but during the 12th plan, investment of about Rs. 8.69 billion has been mobilized through

extra budgetary resources including PPPs until December 2013 against the five year plan target of Rs.

2,200 billion.

The government should liberalize policies to encourage more private investment in the Indian Rail-

ways.

Source: Indian Infrastructure Volume 16.

It is commonly believed

that the economy of India is on the

threshold of achieving significant

growth in the coming years. The

availability of adequate infrastruc-

ture facility will play a key role in

realizing this growth potential. To

accelerate the process of creating

infrastructure capacity, the Gov-

ernment of India has opened up

many infrastructure projects to the

private sector. Making available

international airport facilities is an

important component of the new

infrastructure development policy.

This case study presents the initial

development and financing of the

Kempegowda International Air-

port Limited (KIAL), a major pri-

vate sector airport in India. In ret-

rospect, it is generally felt that

KIAL is an important milestone in

the privatization of airports in In-

dia. The blueprint for the Green-

field PPP (Public-Private Partner-

ship) airport in Hyderabad was

closely modeled on the KIAL pro-

ject. The experience gained in the

development of KIAL also played

a major role in subsequent Brown-

field PPP airport expansion pro-

jects in Mumbai and Delhi.

Structuring:

Though the concessionaire

for the Bangalore airport is a pri-

vate limited company, the Govern-

ment through its agencies and in-

termediaries, holds 26% share-

holding (13% held by the AAI and

the remaining 13% by the State

Government). This 26% share-

holding ensures that the Govern-

ment is able to veto certain funda-

mental resolutions which as per

the Indian Companies Act, require

a minimum of 75% shareholders

vote like issuance of new shares;

change of directors; change of au-

ditors etc., Hence, the Government

does not give away complete con-

trol to the private entity. Amongst

the private players in the Banga-

lore airport project, Siemens of

Germany has the majority 40%

with Zurich airport holding 17%.

Description of the project:

The site is situated about

29 km from Bangalore and covers

about 4,300 acres. The airport de-

sign allows a second runway to

come up in the near future with a

separation distance of about 2 km

between the two run ways. The

run way would be approximately

4,000 meters in length with a

width of 60 meters. The airport

would be on par with any world

class international airport.

A significant part of the

project is permissible for "Non-

Airport" activities. The conces-

sionaire can develop up to 300

acres of land commercially for any

activity not connected with the

airport. In these 300 acres, the

concessionaire is free to set up not

only hotels or malls, it can even go

for Special Economic Zones, man-

ufacturing factories, country clubs,

golf courses, power plant etc. Con-

sidering that this huge chunk of

prime land comes to the conces-

sionaire on a long term lease, vir-

tually free of cost, it is easy to im-

agine that this would be the com-

mercial backbone of the project.

Nature of the concession:

Basically the concession is

for development, construction, op-

eration & maintenance of the air-

port. The agreement allows the

concessionaire to develop, con-

struct, operate and maintain the

Bangalore International Airport

for a period of 30 years, extenda-

ble at its sole option for another 30

years (i.e. total 60 years). The land

for the same is leased by the State

Government. The concessionaire

has the burden to independently

evaluate the scope of the project

and be responsible for all risks

which may exist in relation there-

to. It is obliged to follow good in-

dustry practices and all applicable

laws. The Government on the oth-

er hand, undertakes to support the

project.

To conclude, India is firm-

ly on the path of privatization in

the aviation sector. However, the

Concession Agreements do need a

further in-depth look. Hopefully,

there would be a Model Conces-

sion agreement in the near future

which would bring uniformity and

address some of the issues which

need a second look.

Greenfield Airports In India – An Infrastructural financing Case Study of the Kempe-

gowda (Bengaluru) International Airport

Sudeshna Bhattacharya, F1 & Srijita Mukherjee, F2

Project cost:

The KIAL airport was ini-

tially planned for a passenger ca-

pacity of 8 to 10 million per year.

The capacity of the airport was

increased, by Airport Authority of

India (AAI) to 12 million in antic-

ipation of enhanced future air

traffic. This has resulted in in-

crease of the project cost from US

$389 million to US $495.6 mil-

lion. The cost over-run was due to

scope change introduced by pub-

lic agency AAI. The user tariffs

are to be fixed based on the final

audited report on project cost on

completion. Since project cost

was not frozen initially, it is diffi-

cult to explicitly say anything

about the cost efficiency achieved

in the project.

Challenges for Infrastruc-

ture Financing

Aswathy Edison, F1

Infrastructure is the basic

need of all countries. Infrastruc-

ture provides the path for devel-

opment of a country. In India,

lack of quality infrastructure is a

major issue which retards the de-

velopment of the country. The

major requirement for an infra-

structure project is adequate sus-

tainable funding. In India, the in-

frastructure projects are either

publicly funded or in the form of

Public Private Partnerships. A

major drawback in India is the

delay in the completion of infra-

structure projects. The initial ap-

proval process and notably land

acquisition and resettlement is-

sues gets embroiled in protracted

litigations leading to delays in the

development of the projects. A

country needs adequate infra-

structure to support the business,

citizens and the country itself.

What are the challenges

for Infrastructure Financing in

India?

Funding Gap: Funding Gap

is a major challenge facing

the sector. The inability to

access reasonably priced

funds is an issue that needs

attention. Commercial Banks

hesitate in lending to infra-

structure projects because the

funds get locked up for a

longer period. They also fear

widening of an already ad-

verse Asset Liability Mis-

match. The other avenues of

funding are Equity, FDI, and

ECB etc.

Fiscal Deficit: Besides the

private players, the onus is on

Government to finance the

infrastructure projects in In-

dia. The fund available to the

Government needs to be even-

ly distributed for investing in

other areas such as Education,

Health, and others. This re-

stricts the availability of funds

for infrastructure financing.

Insurance and Pension

Funds: From the point of

view of asset-liability mis-

matches, insurance and pen-

sion funds are one of the best

suited institutions to invest in

the infrastructure sector. In

contrast to the commercial

banks, these institutions lever-

age on long-term liabilities.

They face a major constraint

in the form of mandatory in-

vestment in Government se-

curities. This facilitates the

financing of gross fiscal defi-

cit of the Central Government

and hence enables the Central

Government to make more

investments in multiple com-

peting sectors including the

infrastructure sector. Howev-

er, this limits the direct in-

vestment of these institutions

in the infrastructure sector.

Insufficient User Charges:

The user charges/toll fees lev-

ied on availing the services

are not sufficient for infra-

structure companies to service

their debt obligations. These

user charges are essential for

generating operating cash

flows. These projects are

heavily dependent on such

cash flows to pay off their

debts.

Need for a dynamic bond market: As

expressed by Shri Harun R Khan, Depu-

ty Governor of RBI, there is a need for

development of a vibrant and robust

bond market in India to fund infrastruc-

ture projects. In his opinion, the bond

market could be a major avenue for

funding but the bond market in India is

in its nascent stages and needs to grow

further.

Political Issues: In a country like India, getting infrastructure projects started is an overwhelming task.

The major reason is the rift between the political parties. When one party decides to float a proposal,

the opposition blocks the idea and declares it as a bane for the country. After prolonged slugfest, the

proposal gets approved only to see more delay through ill planned implementation. A project expected

to be completed within 3 years eventually is completed in 10 years or more.

Conclusion

Shri Narendra Modi said ―Economy is bleak without Infrastructure. Hence, the prime focus of my

government should be infrastructure‖. As promised by his government, there has been a series of infra-

structure projects lined up such as Diamond Quadrilateral high speed trains, freight corridors, 100 smart

cities etc. These projects need the adequate financing and implementation within the proposed time. Let us

hope to see India setting up adequate world class infrastructure that it requires, in the near future.

Sources:

Rbi.org.in

The Hindu

Corporate Column

Sai Nanthini. R.K, F2

To gain insights on Infrastructure Financing, we interviewed Mr Murali, Finance Head, L&T Ge-

ostructure LLP based out of Chennai.

1. Your view on Infrastructure financing in India.

A: There is always a connection between Infrastructure and economic development. While infrastructure

facilitates economic growth; economic growth increases the demand for infrastructure. Therefore devel-

opment of adequate and quality infrastructure is a necessity. Hence the success of it will depend on effi-

cient financing model. As we all know, building infrastructure is a capital intensive process with large

initial costs and low operating costs. It requires long term finance involving long gestation periods. As

the infra projects are mostly done on SPV basis, this makes the financing of these projects more complex.

In India, we also need a setup which regulates financing for infra projects.

2. What makes this infrastructure sector distinct and separate from other projects?

A: It is worthwhile to know what makes it distinct from other projects. The construction period and initial

start-up period for any project would run into years, as they are generally huge, involving the coordina-

tion of a variety of agencies. Hence these projects tend to have large capital costs and long gestation peri-

ods. This is one of the reasons why banks are reluctant to finance this sector.

3. What are the issues faced in Infrastructure Financing?

A: Funding Gap is the most important issue that we face on this front. According to the estimates made

by the Planning Commission, after taking into account the recent trends in different sources of infrastruc-

ture financing, the funding gap in the infrastructure sector during the last two years was around 18 per

cent of the total estimated requirement. Demand continues to outpace supply in all sectors of infrastruc-

ture in India. Also factors like fiscal burden, asset liability mismatch of commercial banks are hurting

lending to the infrastructure sector. We also have a great need for an efficient and vibrant corporate bond

market and PPP projects in infra sector. Huge sunk costs and longer gestation period are the reasons why

banks have been shying away from financing the infrastructure projects.

4. What more needs to be done to encourage more infrastructure financing?

Making the infrastructure projects commercially viable.

Encouraging participation in Private Public Partnership market.

Credit enhancement.

Simplification of procedures - enabling single window clearance.

These are the things which they must concentrate more to encourage infra financing.

Two important steps are required for Indian Infrastructure sector. First, we need to setup an independ-

ent regulatory body like SEBI for infrastructure. The primary role of this body would be to attract private

investments and protect the investor for various risks. Second, we need to have an authority which should

take care of sovereign obstacles. The basic role of this body will be to remove the obstacles for public

projects and monitor the development of the project.

The new PPP (Public Private Partnership) model has a lot of potential to carry out various infrastruc-

ture projects and provide a better infrastructure for each sector. Success stories of Gujarat Solar innova-

tive project, Delhi Metro Rail Project showcase the power of PPP.

5. Can you give some insights on PPP projects?

A: Public Private Partnership projects have to be encouraged by government importantly. PPP Projects

take more time, more effort, and are also – prima-facie – costlier but it has some positive points like:

Improvement in levels of service to users.

Innovation in designs, project management and implementation of projects.

Long-term operations and maintenance of assets.

Focus on service to users – not just asset creation. This mechanism actually provides built in credit en-

hancement by improving project viability by way of payback guarantee, substitution rights for lenders

etc.

Stock Market Analysis

Anwesh Jain & Sooraj Kumar C, F1

The Indian Stock market’s benchmark index Sensex increased to 25099.92 points in June from

24217.34 points in May, 2014. The Sensex aver-

aged 6219.74 points since its inception in 1979,

reaching an all-time high of 25583.69 points in

June 2014.

The key BSE and Nifty indices are ex-

pected to gain further this week adding to the

gains made last week. Expectations from the Un-

ion budget, which would be presented by Finance

Minister Arun Jaitley on July 10th, are increasing

the chances of a pre-budget rally, but analysis of

prior budgets going back to the early 1990’s

shows higher instances of a pre-budget pullback

and even higher counts of post- budget weakness.

The top gainers in S&P BSE Sensex were

GAIL (20.92%), Bajaj Auto Ltd. (18.20%), Cipla

(13.84%), Hero Motocorp (11.93%), TCS (11.86%) followed by HDFC, Infosys and Tata steel.

The top Losers for the month were ITC with a 6.34 % reduction from its previous month close,

Mahindra & Mahindra dipped by 6.23 %, Reliance Industries 4.89%, NTPC 4.54%, Bharti Airtel 3.60%

followed by ICICI 2.37% and Tata Power 0.05%.

Market volatility will be higher as the nation is moving closer to the budget day. Investors might

reallocate portfolios ahead of the budget and fresh buying could emerge in infrastructure, power and capital

goods stocks keeping in mind the added attention given to the Infra sector by the Narendra Modi led NDA

government.

Stock of the Month- GAIL

Face value: 10

Traded Volume: 18, 92,941

Market cap (Rs. Crores): 21, 239, 23

Recent News:

Jan 29, 2014: GAIL to import 32-33 LNG cargoes in 2014-15- Chairman. (Closing Price: 346.30)

May 26, 2014: GAIL plans more LNG deals with U.S. (Closing Price: 410.05)

May 27, 2014: India’s GAIL shares fall after earnings miss estimates. (Closing Price: 379.05)

June 20, 2014: Investors switching to Cairn India from GAIL. (Closing Price: 439.40)

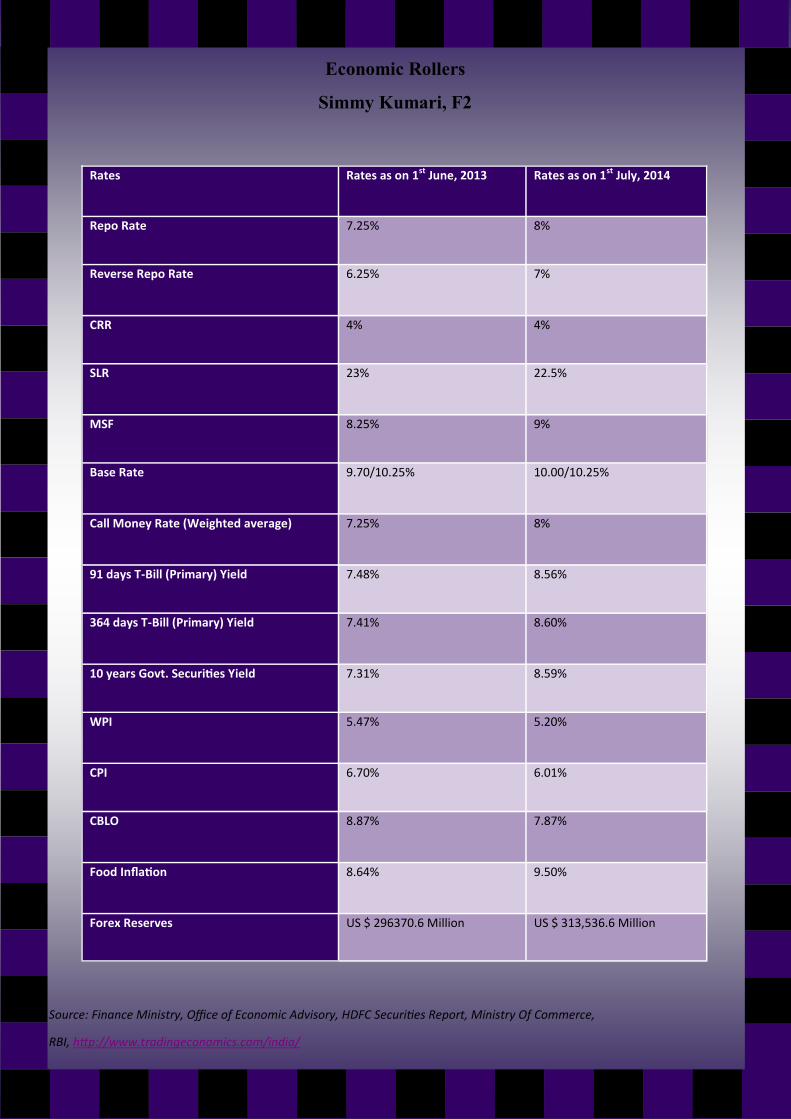

Economic Rollers

Simmy Kumari, F2

Source: Finance Ministry, Office of Economic Advisory, HDFC Securities Report, Ministry Of Commerce,

RBI, http://www.tradingeconomics.com/india/

Rates Rates as on 1st June, 2013 Rates as on 1st July, 2014

Repo Rate 7.25% 8%

Reverse Repo Rate 6.25% 7%

CRR 4% 4%

SLR 23% 22.5%

MSF 8.25% 9%

Base Rate 9.70/10.25% 10.00/10.25%

Call Money Rate (Weighted average) 7.25% 8%

91 days T-Bill (Primary) Yield 7.48% 8.56%

364 days T-Bill (Primary) Yield 7.41% 8.60%

10 years Govt. Securities Yield 7.31% 8.59%

WPI 5.47% 5.20%

CPI 6.70% 6.01%

CBLO 8.87% 7.87%

Food Inflation 8.64% 9.50%

Forex Reserves US $ 296370.6 Million US $ 313,536.6 Million

Finance Buzz

Vyom Goel, F2

Infrastructure Trust: A type of income trust that exists to finance, construct, own, operate and maintain

different infrastructure projects in a given region or operating area. The infrastructure trust will also

provide distribution payments to unit holders on a periodic basis.

Private Finance Initiative – PFI: A method of providing funds for major capital investments where pri-

vate firms are contracted to complete and manage public projects. Under a private finance initiative, the

private company, instead of the government, handles the up-front costs. The project is then leased to the

public, and the government authority makes annual payments to the private company.

"A" Round Financing: The first major round of business financing by private equity investors or venture

capitalists. An "A" round by external investors generally takes place after the founders have used their

seed money to provide a "proof of concept" demonstrating that their business concept is a viable - and

eventually profitable - one.

Super Sinker: Bond with long-term coupons but short maturity, usually a home financing bond. Super

sinker bonds are sometimes used when some of the mortgages backing the bond get prepaid, and so the

bond is likely to be paid off quite soon. The bond holder is uncertain as to when exactly the pay-

off may occur, but the annual return on these bonds works out quite high over the short-to-medium-

term holding period.

Housing Bonds: Debt securities issued by state or local governments to raise money for affordable housing

development. Housing bonds sometimes require voter approval and are repaid out of the government's

general tax fund or from an increase in the sales tax rate, income tax rate or property tax rate.

Direct Bidder: An entity that purchases Treasury securities at auction for a house account rather than on

behalf of another party. Direct bidders include primary dealers, non-primary dealers, hedge funds, pen-

sion funds, mutual funds, insurers, banks, governments and individuals.

RBI Column

Pawanpreet Kaur, F2 RBI issues additional guidelines for banks giving GMLs (Gold Metal Loans):

The central bank has asked the lenders to check the track record and credit worthiness of borrow-

ers, collateral securities against the loan as well as the trade cycle of the manufacturing activity before

sanctioning GMLs. The central bank has clarified that such loans can be availed only by those who

manufacture gold jewelry themselves. Other

steps being taken are as follows:

Carrying out proper quality check of

the gold stock and verifying the in-

surance cover.

Detailed credit appraisal to mitigate

the risk of misuse. A Stand-by Letter

of Credit or a Bank Guarantee by the

issuing bank will serve as proof.

Inspection of stocks, quality check of

the gold stock, verification of insur-

ance cover, etc may be undertaken

jointly or on rotation basis by the

GML providing bank and the bank

issuing the Stand-by LC/BG.

These activities will bring more transpar-

ency; RBI can also monitor the final use of

gold and enforce its maxim on 20% export of finished goods.

RBI to tweak bonds linked to inflation:

The RBI will modify its retail bonds linked to consumer prices as its first attempt to insulate inves-

tors from price rises. This measure was taken after Central Bank adopted Consumer Price Index as the

key measure of inflation instead of the Wholesale Price Index, to which more weightage was given.

This instrument is being used to bring savings back into financial instruments rather than investing in

gold, real estate or any other physical asset. Advantages investors will get on investment in financial

instruments are:

Tax benefits

RBI monetary policy review: Key Takeaways

RBI leaves repo rate unchanged at 8.00 per cent.

RBI cuts banks' SLR requirement by 50 bps to 22.5 % of deposits w.e.f June 14th.

RBI reiterates CPI inflation target of 8 % by January 2015 and 6 % by 2016.

RBI sees marginal improvement in economic growth to 5-6% in FY15.

Cash reserve ratio was kept unchanged at 4 per cent.

The decrease in SLR is expected to result in additional cash of Rs. 40,000 Crores with banks. RBI

is providing more liquidity to banks with an intention to encourage banks to lend more, but banks are un-

der no obligation to lend it to customers or corporate. They can invest the surplus, say in mutual funds.

Market Round Up

K. Alekhya, F2 & B. Suma Sravya, F1

Foreign investors can now hedge currency risk: To enhance the depth of the foreign exchange market,

the Reserve Bank on (20/06/2014) allowed foreign portfolio investors to participate in the domestic ex-

change-traded currency derivatives. It is also expected to reduce volumes in the NFD markets. –

21/06/2014 (ET).

Rupee falls to 7-week low as oil prices rise on Iraq unrest: The rupee fell 36 paisa to end at an over sev-

en-week low of 60.39 against the US dollar as growing unrest in Iraq pushed up crude and caution pre-

vailed in the currency markets ahead of the outcome of US Fed meeting – 21/06/2014 (Times of India).

First bitter pill by Modi Government: Rail passenger fare raised by 14.2%, freight charge by 6.5%

ahead of Budget – 20/06/2014 (BS).

SEBI proposal on PSU Stake cut to spur $10 billion in share sales: The government should dilute its

stake in listed public-sector companies over the next three years and cap it at 75 per cent; a recommen-

dation, if taken forward would lead to at least $10 billion worth of PSU share sales – 19/06/2014(ET).

Foreign investors pour Rs 26,000-crore in Indian market in June primarily on account of oriented deci-

sions taken by the new government. Net investment into equity markets stood at Rs 10,359 Crores,

while in debt market it was Rs 15,806 Crores – 15/06/2014(ET).

Government imposes $300/tonne minimum export price on onion exports to curb exports as retail pric-

es had shot up to as high as Rs 100 per kg in major parts of the country. Rising prices of essential food

items like vegetables, fruits and cereals, pushed up wholesale price index based inflation to five-month

high of 6.01 per cent in May – 17/06/2014(ET).

Factory output rises 3.4% in April: Raising hopes of recovery, industrial production grew at 3.4 per cent

in April after contracting for two months in a row, mainly due to improved performance of manufactur-

ing, mining and power sectors and higher output of capital goods – 12/06/2014 (The Hindu).

Siemens AG is in talks with Mitsubishi Heavy Industries Ltd about a joint bid to acquire Alstom SA’s

energy business and counter a $17 billion offer by General Electric Co -11/06/ 2014 (GE)( Live mint).

The World Bank lowered India’s gross domestic product (GDP) growth forecast for 2014 to 5.5% from

6.2% estimated in January – 11/06/2014 (Live mint)

France has proposed to give India a 1 billion euro ($1.4 billion) credit line to fund sustainable in-

frastructure and urban development projects, Foreign Minister Laurent Fabius said on Tuesday.

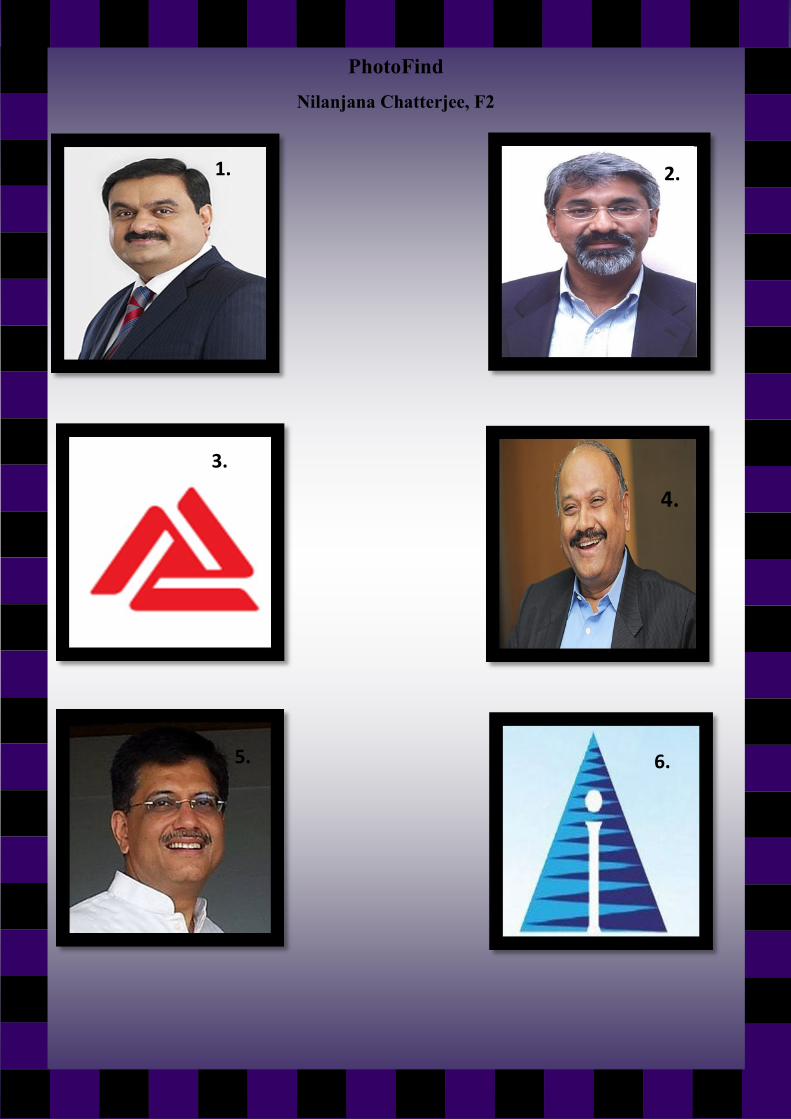

PhotoFind

Nilanjana Chatterjee, F2

1. 2.

3.

4.

5. 6.

Finance Quiz

Samyuktha Reddy, F2

1. For how many years has the government allowed infrastructure companies to issue secured debenture

bonds?

2. India’s second largest software exporter Infosys Ltd has named former SAP AG global product

head ___________ as its first non-founder chief executive.

3. _____________ has named Kaustubh Kulkarni as its head of India investment banking to replace Rohit

Chatterji, who will become head of the bank's emerging Asia mergers and acquisitions business.

4. ________India’s third largest wireless service operator will issue 51 million equity shares, aggregating

to approximately Rs.750 Crores on a preferential basis to Axiata Investments.

5. Which Bank had raised Rs 4,000 Crores from QIP/FPO in June?

6. Which company has roped the former Mphasis Vice President Ganesh Murthy as CFO?

7. ______________ was unanimously elected as the speaker of the 16th Lok Sabha, becoming the second

woman presiding officer of the lower House after her predecessor Meira Kumar.

8. Which is the world’s first Central Bank to use negative rate on deposits i.e. reduced the deposit rate

from 0% to -0.10%?

9. Which e-commerce website hired ex-IBM executive Craig Hayman to head Enterprise division?

10. Which company in Iraq has shut down its oil refinery operations recently?

An

swers:

1.

30 y

ears

2.

Vish

al Sik

ka

3.

JP M

org

an C

hase an

d C

o

4.

Idea C

ellular

5.

IDB

I ban

k

6.

Dell S

ervices

7.

Sum

itra Mah

ajan

8.

EC

B(E

uro

pean

Cen

tral Ban

k)

9.

e-Bay

10. B

aiji

Crossword

Srinivas Rahul Chaganti, F2

1.

1.

4.

5. 2.

7.

3.

6.

8. 10.

9.

Horizontal:

1. -------------- the country's first infrastructure debt fund ( IDF) under the NB structure, is a joint ven-

ture among ICICI Bank, Bank of Baroda, Citicorp Finance and Life Insurance Corporation of India

2. These investments are into new projects that have yet to be constructed that will not generate cash

flow until completed. Often these investments include design and build risk, as well as operating

risk.

3. Which states, Finance Minister, O Pannerselvam has recently mooted to the Centre such a line

of credit to States to provide ―long-term finance‖ for 12 years and more to help execute mega

infrastructure projects in the public-private partnership (PPP) mode

4. ----------- which country's unemployment insurance fund FGTS reassigned US$4.45bn in debt from

federal savings bank Caixa Economica Federal to finance waterworks, housing and urban mobility

projects throughout the country.

5. The Narendra Modi government has cleared ---- how many big-ticket investment projects worth

Rs 21,000 Crores, some of whom have been held up for decades, because of hurdles ranging from envi-

ronmental issues to financing problems.

Vertical:

6. ------- Pvt. Ltd on Thursday launched the S&P BSE India Infrastructure Index that comprises the top

30 companies based on market capitalization from five sectors—energy, transportation, non-banking

financial institutions, telecommunications and utilities.

7. Which book written by RAHUL SARAOGI The apathy of the previous government that ruled India for

almost a decade and the myriad corruption scandals that have plagued the country resulted in a state of

policy paralysis that scuttled almost all large infrastructure projects in India.

8. This international institution on Thursday said that projects worth Rs US$ 500 million are in pipeline in

Northeast India. These projects encompass different sectors including healthcare, e-governance, infra-

structure, water management and inland waterways

9. ---- an SPV, was incorporated in Jan, 2006,by the Central Government for providing long term loans

for financing infrastructure projects providing financial assistance up to 20%of the project costs, both

through direct lending to project companies and by refinancing banks and financial institutions.

10. World Bank Country Director ------ suggested short and medium-term priorities that could help India

return to growth and further reduce poverty. The report says growth in India is projected to rise to

5.5% in FY 2014-15, accelerating to 6.3% in 2015-16 and 6.6% in 2016-17.

An

swe

rs fir C

rossw

ord

:

1.

Ind

ia Infrad

ebt

2.

Gre

enfi

eld

3.

Tamil n

adu

4.

Brazil's

5.

Seven

6.

Asia In

dex

7.

Investi

ng in

Ind

ia

8.

Wo

rld B

ank

9.

IIFCL

10

. O

nn

o R

uh

l

PhotoFind Answers:

1. Gautam Adani, the first generation Indian entrepreneur who is the Chairman and founder of Adani

Group. He founded The Adani Group in 1988 and today it is a globally integrated infrastructure player

with businesses spanning coal trading, coal mining, oil & gas exploration, ports, multi-modal logistics,

power generation,etc.

2. Dr. Rajiv B. Lall is the Managing Director and Vice Chairman of Infrastructure Development Fi-

nance Company (IDFC), India's leading integrated infrastructure finance player providing end to end

infrastructure financing and project implementation services.

3. Logo of Infrastructure Leasing & Financial Services Limited (IL&FS), an Indian infrastructure de-

velopment and finance company.

4. Grandhi Mallikarjuna Rao, a mechanical engineer and the founder chairman of GMR Group, a

global infrastructure developer and operator based in India. Started in 1978, GMR Group is now pre-

sent in 7 countries, active in Energy, Highways, Large Urban Development and Airports sectors,

known for building and operating world class national assets.

5. Piyush Goyal, the Hon’ble Minister of State with Independent Charge for Power, Coal and New &

Renewable Energy in the Government of India. He is currently a Member of Parliament (Rajya Sabha)

and was earlier the National Treasurer of the Bharatiya Janata Party (BJP).

6. Logo of IIFCL (India Infrastructure Finance Company Ltd.), a wholly-owned Government of In-

dia company aimed to provide long term finance to viable infrastructure projects through the Scheme

for Financing Viable Infrastructure Projects.

NISHKA TEAMNISHKA TEAMNISHKA TEAM

Nishka is a monthly finance magazine brought by the students of the finance club of

Christ University Institute of Management, Kengeri Campus. The idea behind coining this

issue of the magazine is to establish a learning among the students, which helps them to

gain an insight about the world of finance.

Faculty Coordinator

Prof. Shrikant Rao

Coordinators

Niharika Shadra, F1

Niken Jain, F2

Editor

George P Job, F2

Neha Mishra , F2

Introduction

Upasana Gurung, F1

Article coordinators

Ashwathy Edison, F1

Sudeshna Bhattacharya,

F1

Article writing

Kalyana KarthiK, F2

Purnima Singh, F2

Srijita Mukherjee, F2

RBI Column

Pawanpreet Kaur, F2

Finance Buzz

Vyom Goel, F2

Market Round-Up

B.S Sravya, F1

Katepalli Alekhya, F2

Economic Rollers

Simmy Kumari, F2

Stock Analysis

Sooraj Kumar, F1

Anwesh Jain, F1

Crossword

Samyuktha Reddy, F2

Quiz

Rahul Srinivas, F2

Photofind

Nilanjana Chatterjee, F2

Corporate interview

Sai Nanthini, F2

Designing

Krishnendu Kundu, F2

Niken Jain, F2

CHRIST UNIVERSITY INSTITTUTE OF MANAGEMENT, KENGERI CAMPUS

Please mail your valuable feedback/reviews to [email protected]

(For private circulation only)